Embed Size (px)

Citation preview

THE NEXT STEP IN SMALL AND MEDIUM ENTERPRISE LENDING

David Alexander Stroud B. Com., University of British Columbia, 1997

A PROJECT SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF

MASTER OF BUSINESS ADMINISTRATION

In the Faculty of

Business Administration EMBA Program

O David Alexander Stroud 2004

SIMON FRASER UNIVERSITY

August 2004

All rights reserved. This work may not be reproduced in whole or in part, by photocopy

or other means, without permission of the author.

ABSTRACT

This project examines the business lending industry in Canada and the strategic

direction of the small and medium enterprise (SME) lending business of the Toronto-

Dominion Bank Financial Group (TDBFG). TDBFG is one of the largest schedule I

banks in Canada, however its market share of the SME lending market is substantially

less than its market share in other business segments.

This paper will assess the current environment in which the Bank operates and

identify key success factors in the SME financing business. It will then present TDBFG's

optimal strategy going forward as well as an alternative strategy. An evaluation of

TDBFG's current internal capabilities will determine whether the Bank is capable of

executing the optimal strategy or should instead undertake alternative strategy.

Presently the SME customer category is served by both the small business banking arm

of the TD Canada Trust and the TD Commerial bank and as a result any recommended

solutions will focus on these two business units.

APPROVAL

Name:

Degree:

Title of Thesis:

Supervisory Committee:

David Stroud

Master of Business Administration

The Next Step in Small and

Medium Enterprise Lending

Dr. Neil Abramson Senior Supervisor Associate Professor Faculty o f ~ i n e s s ~ m i n i s t r a t i o n

Supervisor (1 Associate Professor Faculty of Business Administration

Date Approved: - 0 - b y

Executive MBA Program

Partial Copyright License

I hereby grant to Simon Fraser University the right to lend my thesis, project or extended essay (the title of which is shown below) to users of the Simon Fraser University Library, and to make partial or single copies only for such users or in response to a request from the library of any other university, or other educational institution, on its own behalf or for one of its users. I further agree that permission for multiple copying of this work for scholarly purposes may be granted by me or the Dean of Graduate Studies. It is understood that copying or publication of this work for financial gain shall not be allowed without my written permission.

Title of Thesis/Project/Extended Essay

The Next Step in Small and Medium Enterprise Lending

Author:

ba-

Date

DEDICATION

This paper is dedicated to Isabelle. My work over the past two years pales in

comparison to her love, hard work, dedication and sacrifice throughout my lifetime in her

unrelenting drive to help me realize my potential. My dream is to make her proud.

ACKNOWLEDGEMENTS

Over the past two years many individuals have provided encouragement and

support towards the attainment of my degree and completion of this program. First I

would like to thank my best friend Ed Fidler and brother Chris Stroud for your support,

encouragement and friendly rivalry. I thank John Stroud-Drinkwater for his efforts to

assist me through the last stretch. I thank my two managers throughout the program,

Jim Yee and Ruth Lee for providing support towards my endeavour and acknowledging

my efforts in furthering my education. Finally, I thank my team members, cohorts and

professors through whom I acquired my knowledge and sharpened my critical thinking.

TABLE OF CONTENTS

. . Approval ........................................................................................................................ 11

... Abstract ........................................................................................................................ III Dedication .................................................................................................................... iv

Acknowledgements ....................................................................................................... v

Table of Contents ....................................................................................................... vi ... List of Figures ............................................................................................................ VIII

List of Tables .............................................................................................................. ix

Glossary or List of Abbreviations and Acronyms ....................................................... x

1 Chapter One: Small & Medium Enterprise Lending At The TD Bank Financial Group ................................................................................................... 1

The Toronto Dominion Bank Financial Group ........................................ 1 The Corporate Group ................................................................................... 3 TD Canada Trust ......................................................................................... 4 Business Banking & Insurance .................................................................... 7

.................................................................................... Wholesale Banking 10 Wealth Management .................................................................................. I I

................................................................................. TD Waterhouse USA 12 Focus of this Strategic Analysis ................................................................. 12

Chapter Two: The SME Lending Industry ........................................ 14 Business Lending Defined ......................................................................... 14 Industry Analysis ....................................................................................... 14

............................................................................................. New Entrants 17 Suppliers ................................................................................................... 21

................................................................................... Customers Analysis 23 Substitutes ................................................................................................. 29 Value Chain Analysis ................................................................................. 31 Securities Underwriting .............................................................................. 32 Marketing ................................................................................................... 33 Distribution ................................................................................................ 34 Loan Production & Credit Management ..................................................... 37

..................................................................................................... Service -39 Competitive Analysis ................................................................................. 41 Competitive Concentration is high ............................................................. 44 Increased Competitive Pressure from Mature Market ................................ 44 Commoditization of Banking Products and Services .................................. 44 Technology Enables the Easy Switch ........................................................ 45 High fixed assets costs .............................................................................. 45 Brand Equity Costs and Political Barriers to Exit ........................................ 46 Key Success Factors ................................................................................. 46 Culture ....................................................................................................... 46

................................................................................................... Marketing 47 Sales & Distribution ................................................................................... 48 Systems and Processes ............................................................................ 49 Credit Policy & Risk Management .............................................................. 50

................................................................................. The Current Strategy 50 Core Strategy ............................................................................................ 51 Optimal Rapid Penetration Strategy ........................................................... 52

. ~

Culture ....................................................................................................... 53 ................................................................................................... Marketing 53

Sales & Distribution ................................................................................... 54 Systems and Processes ............................................................................ 56 Credit Policy & Risk Management .............................................................. 60

...................................................... Alternative Rapid Penetration Strategy 61 ......................................................................... Credit Scoring Technology 63

................................................................ Credit Management Technology 63 .................................................... Organization & Compensation Structure 63

................................................................................ Product Development 64

Chapter Three: Internal Analysis of SME Lending at TDBFG ............... 65 ................................................................................................. Resources 65

Culture ....................................................................................................... 65 Marketing ................................................................................................... 66 Sales & Distribution ................................................................................... 66 Systems & Processes ................................................................................ 68 Credit Policy & Risk Management .............................................................. 71 Resource Gap ........................................................................................... 71

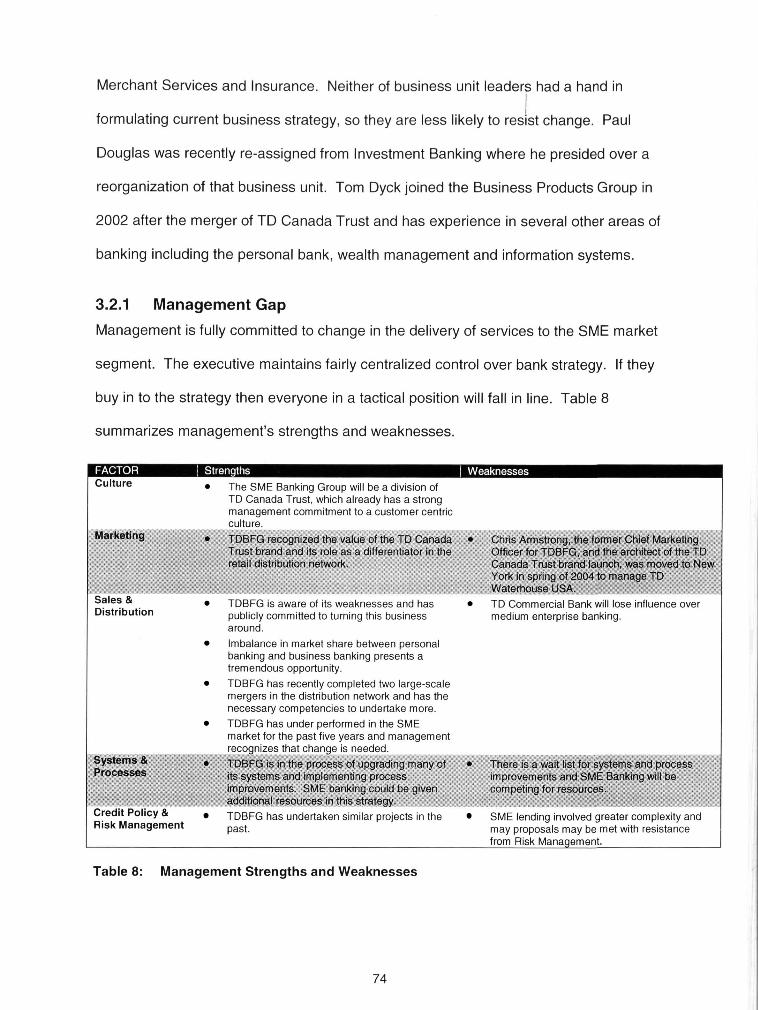

......................................................................... Management Assessment 73 Management Gap ...................................................................................... 74 Organization .............................................................................................. 75 Organizational Capabilities ........................................................................ 75

............................................................................ Organizational Changes 76 ...................................................................................... Organization Gap 78

Chapter Four: Recommendations .......................................................... 80 ................................................................................................... Overview 80

Strategic Recommendation ........................................................................ 80 The Vision ................................................................................................. 80

..................................................................................................... Urgency 81 ............................................................................................. Project Team 81

The Devil in the Details .............................................................................. 83 .................................................................................................... Vigilance 86

............................................................................................... Conclusions 86

.............................................................................................. Appendices 88 Appendix A: Business Loan Product Life Cycle ........................................ 88 Appendix B: SME Banking Reporting Structure ........................................ 89

............................................. Appendix C: Loan Application Process Flow 90 ................................................ Appendix D: Customer Experience Model 91

Bibliography ............................................................................................. 92

LIST OF FIGURES

Figure 1 : TD Bank Financial Group Corporate Structure ................................................ 2 Figure 2: TDBFG Revenue by Business ......................................................................... 3

....................... Figure 3: Personal and Commercial Banking Revenue by Business Unit 4

....................................................................... Figure 4: 9 Regions of Retail Distribution 5 Figure 5: Branch Reporting Structure ............................................................................. 6 Figure 6: Total Credit Authorizations for Firms with Authorizations under $1

million ............................................................................................................ 15 Figure 7: Competitive Analysis Chart of SME Lending in Canada ................................ 16 Figure 8: Authorization Sizes of SMEs Borrowing from Domestic Banks ...................... 24 Figure 9: Breakdown of SME Liabilities by Type. 2000 ................................................. 29 Figure 1O:SME Lending Value Chain ............................................................................ 31 Figure 1 1 :SME lending market share statistics .............................................................. 43

........................................................................... Figure 12: Enterprise Risk Framework 77

viii

LIST OF TABLES

Table 1: Table 2: Table 3: Table 4: Table 5: Table 6: Table 7: Table 8:

Table 9:

Global Bank Rankings by Assets .................................................................. 15 SMEs' Sectors of Operations by Region in 2000 ........................................... 25 Sources of SME Financing ............................................................................ 29 Analysis of small business banking at the 5 largest Canadian banks ............ 42 Business Segmentation under Optimal Strategy ........................................... 54 Business Segmentation under Alternative Strategy ....................................... 63 Resource Strengths and Weaknesses .......................................................... 72 Management Strengths and Weaknesses ..................................................... 74 Organization Strengths and Weaknesses ...................................................... 79

GLOSSARY OR LIST OF ABBREVIATIONS AND ACRONYMS

ACC BMO BNS Cl BC CRM ERP FA FSR GDP GRM HSBC MCC MSBBS RBC ROI SBA SBB SME TDBFG TDCT

Area Credit Centre Bank of Montreal Bank of Nova Scotia I ScotiaBank Canadian Imperial Bank of Commerce Customer Relationship Management Enterprise Resource Planning Financial Advisor Financial Service Representative Gross Domestic Product Group Risk Management Hongkong and Shanghai Banking Corporation Manager Commercial Credit Manager Small Business Banking Sales Royal Bank of Canada Return on Investment Small Business Advisor Small Business Banking Small and Medium Enterprise Toronto-Dominion Bank Financial Group TD Canada Trust

1 CHAPTER ONE: SMALL & MEDIUM ENTERPRISE LENDING AT THE TD BANK FINANCIAL GROUP

Although the TD Bank Financial Group (TDBFG) has a robust 20.05 percent

market share in the Personal Banking arena, its share of small enterprise lending is 10.9

percent and medium enterprise lending is 9.2 percent.' This represents a very large

opportunity to the TDBFG because it implies that many of its personal customers have

business dealings with other Canadian banks and that they can potentially be cross sold

business financing. It also represents lost opportunities in the past, since the Bank has

had a smaller market share in the SME market for some time and its current strategy

has failed to close the gap. The Bank's leadership has recognized the value of this

opportunity and has appointed an Executive Vice President, Bernard Dorval, to preside

over this market segment in addition to the insurance group, as both of these markets

have been identified as high growth opportunities for the Bank.

This paper will examine the competitive environment in the SME lending market

and recommend an optimal and alternative strategy for TDBFG to execute, both of which

could bring a bank success in gaining SME lending market share. Given these

strategies, an audit of TDBFG's internal capabilities will qualify which strategy TDBFG is

capable of executing successfully.

1 .I The Toronto Dominion Bank Financial Group The Toronto Dominion Bank Financial Group was originally founded in 1955 as

the Toronto Bank, which in 1955 amalgamated with the Dominion Bank, which was

chartered in 1869. Since its inception, the Bank has grown through organic growth, as

1 Market share statistics represent a percentage of customers dealing with Canadian chartered banks and deal not include non-bank financing to the SME market.

well as mergers and acquisitions. Most recently the Bank purchased CT Financial

Services Inc., which vaulted the Bank from 5'h largest bank by assit size to 2nd largest,

behind the Royal Bank. Over time, the Bank has also broadened the scope of financial

products offered and as a result has become a group of companies selling financial

services to retail and institutional customers in Canada and abroad.

TDBFG has over 51,000 employees and more than $31 6 billion in assets. As

seen in Figure 1, it is comprised of three key business areas: Personal & Commercial

Banking, Wealth Management and Wholesale Banking.

Personal & Wealth Commercial Banking I Wholesale Banking I Management

Figure 1: TD Bank Financial Group Corporate Structure

TDBFG derives the majority of its revenues from its Personal and Commercial

Business. As seen in Figure 2, this business unit generated 58 percent of revenues in

2003 and it is considered to be TDBFG's core business.

Wealth Management

21 %

Wholesale Banking

21 %

Figure 2: TDBFG Revenue by ~ u s i n e s s ~

TDBFG delivers services to the small and medium enterprise market through the

Personal and Commercial Banking business. SME financing is delivered to the

customer under two brands, TD Canada Trust and TD Commercial Bank. The TD

Canada Trust is a brand that represents TDBFG's retail operations. TD Canada Trust

distributes Personal Banking, Small Business Banking and Wealth Management

products. TD Canada Trust has approximately 10 million personal, small business and

insurance customers. TD Commercial Bank operates parallel to TD Canada Trust and

services medium enterprises, mid-market customers and junior corporate.

As a result of the acquisition of CT Financial Services Inc. in 1999, the retail

banking operations of TD Bank and Canada Trust were merged. Under the brand name

TD Canada Trust, the combined operation is one of Canada's premier retail banking

organizations. Branch conversions to TD Canada Trust branding were successfully

completed in August 2001.

1 .I .I The Corporate Group

The corporate group provides support services, infrastructures and direction in

areas that are common to the three bank businesses. Corporate Group's mandate is to

provide centralized advice and counsel and to design, establish and implement

Source: TD Bank Financial Group Annual Report 2003. Other revenue includes internal commissions on sales of mutual funds and other Wealth Management products, fees for foreign exchange, safety deposit box rentals and other branch services.

processes, systems and technologies to ensure that the Bank's ke. businesses operate r efficiently, effectively and in compliance with all applicable regulations.

1.1.2 TD Canada Trust

TD Canada Trust represents the Personal and Commercial Banking arm of the

TDBFG. It offers banking services to customers in Canada, under the TD Canada Trust

Brand, and in the U.S., under the TD Waterhouse Bank Brand. Financial services are

delivered through a network of branches, the Internet, the telephone, and most recently

through wireless devices such as pagers and cell phones. TD Waterhouse Bank is the

largest electronic bank in the U.S. offering a full suite of personal products and services.

TD Canada Trust represented 82 percent of TDBFG's income on a cash basis in 2003

and as per Figure 3, 21 percent of its revenue is derived specifically from business

banking. This implies that were the Bank to meet its expectations to double its market

share in SME lending, it could increase revenue by up to 20 percent.

insurance Other 4%

Commercial 8% Bank 10%

Personal Small Banking

Business 67% Banking

11%

Figure 3: Personal and Commercial Banking Revenue by Business Unit

1 .I .2.1 Retail Distribution

Retail Distribution is divided into 9 regions in order to manage the banking

network across Canada's large geographic area. The majority of the Bank's branches

are located in Ontario and as a result Ontario has 5 regions. As seen in Figure 4 below:

Ontario

Greater Toronto

Ontario North 81

Figure 4: 9 Regions of Retail Distribution

Retail Distribution is supported by e. Bank, Retail Sales & Service, as well as

Retail Transformation. e.Bank supports TD Canada Trust by completing billions of

transactions annually and selling millions of units of products through call centres,

internet banking and the ABM network. EasyWeb, the Bank's internet banking platform,

has been recognized with several awards recognizing its best-in-class design and

functionality and the Bank is recognized as an industry leader in web banking market

penetration.

Retail Sales & Service is an integrated team dedicated to fulfilling five key

functions: Sales & Service Support, Advice & Channel Support, Retail Real Estate

Management, Branch Optimisation, and Retail Operational Risk. Sales & Service

Support is available through a bank intranet and a call centre to assist employees

throughout the retail network with product knowledge, compliance and systems use.

Advice and Channel Support are a team of specialists within each region who train

employees and regularly visit individual branches in each region to provide coaching.

The other three focuses support the operational functions of the retail network.

1.1.2.2 The Regions

Each region is composed of over one hundred branches a ri d is sub-divided into

districts with up to 20 branches per district. Each region may have its own unique

focuses. For example, Pacific Region has departments in several branches devoted to

Asian banking, which provides banking services in Korean, Japanese, Cantonese,

Mandarin, Punjabi and Hindi. The Prairie Region on the other hand has several

branches with agricultural lending departments.

1.1.2.2.1 The Branches

Each Branch Manager reports to a District Manager, and each branch must focus

on both sales and service. The Manager Customer Service reporting to the Branch

Manager, oversees the frontline Customer Service Representatives (Tellers) and

Greeter (Receptionist) area. The Branch Manager directly oversees the sales staff:

Small Business Advisors, (SBA) Financial Advisors (FA) and Financial Service

Representatives (FSR). In larger branches this supervision is shared between the

Branch Manager and a Manager Financial Services as illustrated in Figure 5. Only

branches with large Small Business loan portfolios will be assigned a Small Business

Advisor.

Branch Manager 7

Figure 5: Branch Reporting Structure

1 .I .3 Business Banking & lnsurance

Business Banking and lnsurance are part of the TD Canada Trust and these two

businesses have been singled out as key opportunities to the Bank. Because of the high

potential of these businesses, the Executive Vice President (EVP) of this group reports

directly to the CEO while still working closely with the President and other EVPs within

TD Canada Trust.

Business and lnsurance Group manages all aspects of the commercial and small

businesses customer experience from product development through to credit

adjudication, product support, and sales distribution. The Bank believes that by aligning

the Commercial Banking, Small Business Banking and Merchant Services teams the

three groups will work together seamlessly to serve business customers and become the

best business bank in North ~ m e r i c a ~ .

The Group also manages TD Canada Trust's insurance products, which include

creditor insurance, international reinsurance, and home & auto insurance.

1.1 .%I Commercial Banking

TD Commercial Banking serves needs of businesses whose borrowing needs

are too complex for the Small Business Banking product suite. Commercial banking

affords more customized financing solutions and involves a greater depth of financial

analysis and due diligence.

TD Commercial Bank offices are primarily found in large urban centres located in

the same building as a TD Canada Trust branch. Customers of TD Commercial Bank

use services provided by the retail bank such as teller services, ATMs and day to day

banking. Commercial banking focuses on providing products and services to Canadian

Merchant Services provides card payment solutions to business customers who need to accept payment using credit cards and debit cards.

large and

investing,

medium sized enterprises. The full suite of products inc!udes lending,

cash management, foreign exchange, trade finance andltreasury products.

Commercial banking is divided into two primary functional areas Credit

Adjudication and Sales. Both functional areas are sub-divided into five regional areas

with a sixth department serving the junior corporate customers who have borrowing

needs in excess of $5 million.

A loan request from a customer new to the Commerial bank would take the

following path. Let us suppose that the customer first met a Manager Business

Development at a Chamber of Commerce function. The Manager of Business

Development would then introduce the customer to a Relationship Manager, who would

then interview the customer and assess her needs. The Relationship Manager would

then structure the deal with the assistance of an Analyst and together they would

escalate the deal to the Manager Commercial Credit (MCC) in their office. The deal is

reviewed by the MCC and she is willing to recommend it, however since it is above her

limit she escalates it to Group Risk Management (GRM) at the regional level. At GRM

two underwriters review the credit and authorize it. If the amount had been much larger,

they would have had to escalate it to Toronto. Six employees have touched the deal

since the first contact with the customer. If GRM had not approved the deal, the

Relationship Manager and Analyst might have restructured it and begun the process

once again.

At the branch level, the Manager Business Development and Relationship

Managers report to a Manager Commercial Sales. The analysts report to the Manager

Commercial Credit. The Manager Commercial Credit reports to Group Risk

Management, whereas the Manager Commercial Sales reports to a District Manager.

The structure is designed to nullify a potential conflict of interest that could occur if the

risk manager were to have sales targets.

1.1.3.2 Small Business Banking and Merchant Services

Small Business Banking delivers products and services that are tailored to meet

the banking needs of small businesses who have relatively simple banking needs that

can be served in a retail branch. A common service used by our small business

customers is Merchant Services. Merchant Services provides card payment solutions to

customers who need to accept payment using credit and debit cards.

1.1 -3.2.1 Small Business Banking Product Group

Small Business Banking Product Group is composed of three functional areas:

Product & Distribution, Agriculture & Franchise Banking, and Small Business Credit.

Product & Distribution is concerned with designing deposit and credit products with

respect to pricing process and promotion. This group develops and executes an annual

marketing plan and must engage multiple distribution channels and business units.

Agriculture and Franchise Banking develops and markets special pricing and

loan guidelines for agricultural businesses and established franchise networks. The

Bank recognizes that these two groups have different risk profiles than the broader

market and therefore require customized solutions. The Product & Distribution unit has

designed a similar pricing and loan package for Professionals, however it is less

formalized than the Agriculture and Franchise packages.

Small Business Credit is composed of two credit adjudication centres. Eastern

Credit Centre is located in Markham, Ontario and Western Credit Centre in Edmonton,

Alberta. Small Business Advisors structure loan submissions and send them to one of

the credit centres to be adjudicated. The centres are organized into teams of up to

seven Underwriters working under one Senior Underwriter. Higher limit deals and deals

i that are declined are all escalated to the Senior Underwriter for a second review.

1.1 A2.2 Small Business Banking Sales

The Manager Small Business Banking Sales (MSBBS) is the individual who

provides sales support to people in the branch network to assist in the sales and

distribution of small business products and services. They provide product and market

information to Small Business Advisors, and they train and coach Financial Advisors and

Financial Service Representatives. The MSBBS reports to a Regional Manager of Small

Business Banking Sales who in turn reports to the Assistant Vice President of Small

Business Banking Sales in Toronto. It is significant to note that SBA's do not report to

any part of the Small Business Banking Sales group.

1 . I .4 Wholesale Ban king

Wholesale Banking, distributed under the TD Securities brand offers a variety of

capital market products and services to corporate, government and institutional

customers in five key finance areas.

Through its Investment Banking division, TD Securities provides services and

advice to clients to assist them in mergers and acquisitions, divestitures, capital

structuring and risk management. lnvestment Banking also provides services in the

placement of common equity, preferred shares, private equity, debt securities, debt

syndications and bridge financing.

TD Securities' Debt Capital Markets division provides its global client base with

origination, trading and sales of money market, investment and non-investment grade

fixed income instruments as well as derivatives.

The Institutional Equities division, under the TD Newcrest brand, provides equity

sales, trading, research, underwriting and distribution in North America.

The Private Equity division, under the TD Capital brand, provides equity and

mezzanine financing to middle-market customers in order to finance management

buyouts, expansion, acquisitions, industry consolidations and recapitalizations.

Finally, the Foreign Exchange division provides foreign exchange spots, forwards

and options.

1 . I .5 Wealth Management

Wealth Management provides a wide array of investment products and services,

the majority of which are provided through three key businesses: TD Mutual Funds, TD

Private Client Group and TD Waterhouse Canada.

1.1.5.1 TD Mutual Funds

TD Mutual Funds offers more than 70 mutual funds and 30 managed portfolios.

These funds are distributed through the retail branch network, TD Waterhouse's

discount and full brokerage as well as in house financial planners. The funds are also

distributed through external brokers and financial planners.

1.1 S.2 TD Private Client Group

TD Private Client Group provides discretionary account management to clients

with large investment portfolios. This group also provides estates and trust services as

well as insurance products for wealth protection. The Private Banking Group is also

division of TD Private Client Group.

1.1.5.3 TD Waterhouse Canada

TD Waterhouse Canada offers brokerage services and no-fee financial planning.

Customers can choose from discount brokerage or full brokerage services. Discount

brokerage provides low cost access to stock market trading for customers who want to

I make their own investment decisions without the benefit of a broker's advice. Trading is

accessible by phone or the Internet and market information is provided via the website

and direct mail. Full brokerage, called TD Waterhouse Investment Advice provides

trading services and advice along with active account management. TD Waterhouse

Financial Planning accounts do not allow trading in stocks, however they do provide no

fee full financial planning and the ability to invest in mutual funds, money market and

fixed income instruments.

1.1.6 TD Waterhouse USA

TD Waterhouse USA provides discount brokerage services to customers in the

United States. TD Waterhouse USA has over 2.1 million customers and over $108

billion in customer assets.

1.2 Focus of this Strategic Analysis TD Canada Trust presently has a three-pronged strategy. The primary initiative

involves preserving and improving on the Bank's core competency in expense

management and efficiency. The second initiative is the Bank's commitment to deliver

superior service and a premium brand based customer experience. This premium brand

will be leveraged to extract lifetime value of the customer by improving customer

retention, customer attraction and cross selling to current customers. The last piece of

the Bank's strategy is to focus on growth of under penetrated businesses that have the

potential for above average growth rates. These "super growth" business units are

commercial banking, small business banking and insurance.

This paper will assess the current environment in which the Bank operates and

identify key success factors in the SME financing business. It will then examine

TDBFG's current internal capabilities, and recommend whether TDBFG should

undertake an optimal strategy or an alternative strategy given its current capabilities.

Presently the SME customer category is served by both the small business banking arm

of the TD Canada Trust and the TD Commercial Bank and as a result any recommended

solutions will focus on these two business units.

i CHAPTER TWO: THE SME LENDING INDUSTRY

Business Lending Defined The small and medium sized enterprises (SME) market segment typically

consists of organizations with fewer than 500 employees, $50 million in revenues and

are owner operated. The Canadian Bankers Association defines small enterprises as

those businesses with authorised borrowing levels under $500,000 and medium

enterprises as those with levels under $1,000,000. SMEs are critical to the Canadian

economy, make up 43 percent of Canada's GDP, and are the primary engine for job

~ rea t ion .~ While SMEs are good for the Canadian economy, they are also a great

opportunity for financial institutions in Canada. In 2001, authorized debt financing to

SMEs reached almost $149 billion of which only 49 percent was supplied by the 14

domestic banks.5 The other 51 percent is supplied from non-bank source^.^

2.2 Industry Analysis Canada is a small player on the world financial stage, which is not surprising

given its relative GDP and population. It represents only 2.4 percent of the world's

equity market capitalization, down from 3.8 percent in 1982 and had only a 2.9 percent

share of global personal financial services and insurance profits in 1998.~ As seen in

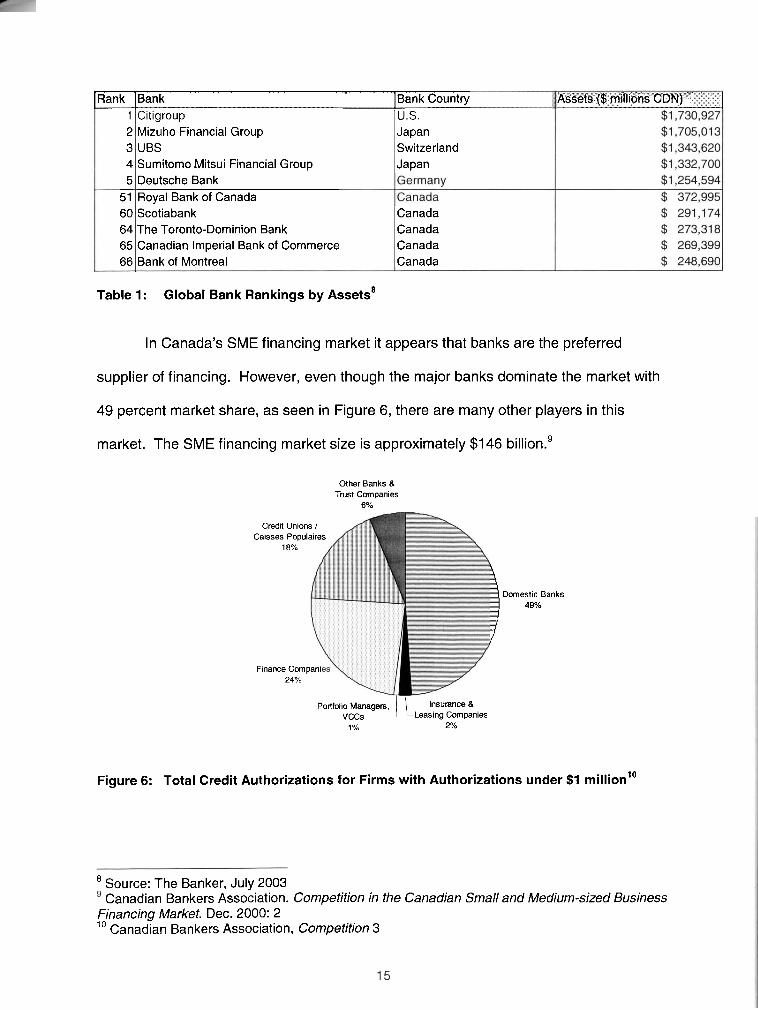

Table 1, ranked by assets, not one of Canada's banks rank in the top 50 globally.

Canada. Industry Canada. Key Small Business Statistics. Ottawa, April 2004: 22 5 Canada. Statistics Canada. Survey of Suppliers of Business Financing 2002 6 See Figure 6 below. 7 McKinsey & Company, The Changing Landscape for Canadian Financial Services: New forces, new competitors, new choices, Ottawa: Department of Finance, September 1998: 1 1

pank [Bank ]Bank Country U.S. Japan Switzerland Japan

1 2 3 4 5

51 60 64 65 66

Canada Canada Canada Canada

Citigroup Mizuho Financial Group UBS Sumitomo Mitsui Financial Group Deutsche Bank Royal Bank of Canada Scotiabank The Toronto-Dominion Bank Canadian Imperial Bank of Commerce Bank of Montreal

A'ssets ($ millions CDN) ' ]

Table 1: Global Bank Rankings by ~ssets '

In Canada's SME financing market it appears that banks are the preferred

supplier of financing. However, even though the major banks dominate the market with

49 percent market share, as seen in Figure 6, there are many other players in this

market. The SME financing market size is approximately $1 46 bi~l ion.~

Other Banks & Tmst Companies

6%

Credit Unions 1 Caisses Populaires

18% 1 Domestic Banks 49%

Finance Compani 24%

Pollfolio Managers, I"surance & v c c s 1 Leasing Companies 1 % 2%

Figure 6: Total Credit Authorizations for Firms with Authorizations under $1 millionlo

8 Source: The Banker, July 2003 Canadian Bankers Association. Competition in the Canadian Small and Medium-sized Business

Financing Market. Dec. 2000: 2 10 Canadian Bankers Association, Competition 3

A five forces analysis of the SME financing market reveals a very competitive

marketplace." As seen in Figure 7, low barriers to entry, high supblier and buyer power,

a high threat of substitutes and high competitive rivalry, characterize the market.

I Level of Significance 1 I Lowest * I Low * * I

Medium

High

Highest *.*+**

Economies of Scale

Lack of Buyer Concentrat_i= ** * * Competitive Concentration * ** * * A lncreasinoht com~lex , * * *

Figure 7: Competitive Analysis Chart of SME Lending in Canada

product offerings' Shifting Industry Growth ** Trends

11 Adapted from Porter, Michael E. Competitive Strategy: Techniques for Analyzing Industries and Competitors. New York: The Free Press, 1 980: 4

2.2.1 New Entrants

2.2.1.1 Legislative Changes are Increasing Ease of Entry

Before 2001, under the Bank Act no shareholder of a large bank could hold more

than 10 ownership. With the changes in brought about in Bill C-8, one

shareholder is now able to own up to 100 percent of a small bank and up to 20 percent

of a medium to large bank. This was expected to encourage the creation of more banks.

Telecommunications companies, grocery retailers, businesses with existing retail

networks or strong online presence that can be used to distribute banking services

would most likely launch these banks. Another legislative change, which increases ease

of entry, is the reduction in capital requirements needed to apply for a bank licence from

$10 million to $5 million. As of year-end 2003 there has not been significant new entry

although there are some interested parties.

Although legislation is facilitating entry, the federal government still retains

control of who can establish a new bank. In order to preserve a safe and stable financial

system, applicants must demonstrate the financial wherewithal, and management ability

to successfully operate a bank in Canada. The federal government must also approve

shareholders wishing to acquire 20 percent of a large bank.

Legislation now allows foreign banks to directly operate in Canada using a

branch network, rather than requiring them to set up a separately capitalized subsidiary.

This increases the capital availability of foreign banks operating in Canada since they

will be able to draw on the capital of the foreign parent company.

Prior to the passage of this legislation only deposit taking institutions could

access the payments system. This meant that other financial institutions could not

access the cheque clearing system, credit card systems or the lnterac network. Under

new law non-deposit taking institutions, such as insurance companies, securities dealers

and mutual fund companies have access to these networks and can offer their I

customers banking services.

2.2.1.2 Technology Reduces Entry Costs

The Internet has had a tremendous impact on banking. Although incumbent

bricks and mortar banks have made unsuccessful attempts at launching online

subsidiaries, ING Group has successfully proven the online banking business model.12

ING Direct was first launched in Canada in 1997 and presently has over 850,000

Canadian clients, and over $12 billion in assets. It has since used this winning business

strategy to enter 6 additional countries in Europe, North America and Australia. It is

possible for ING or another company to enter the SME financing market in the same

fashion.

Wells Fargo, a very successful SME lender from the United States, which

entered the Canadian SME loan market in 1999 using an electronic platform and a direct

mail marketing campaign met with limited success and subsequently exited the market.

The online banking business model reduces capital costs associated with a

physical branch distribution network. This strategy is also easily reproduced however

online banks are limited to providing services that do not require a branch network.

HSBC, entered the market by purchasing the Bank of British Columbia in 1986.

HSBC however entered the market as a full service bank with both personal and

business product lines. HSBC also invested heavily in the business banking division

and presently, among domestic banks, it has a 12.5 percent share of the SME market up

from 3.4 percent in 1999.

12 ING Group, Press Release, Amsterdam, 20 October 1999

18

2.2.1.3 Low Likelihood of Retaliation to Market Entry

Given the close regulatory oversight of the Canadian banking system, it is

unlikely Canadian banks would engage in retaliatory practices in the event of new entry

to the market. in addition, since Canadian banks are perceived to wield excessive clout

domestically, if they were to engage in predatory behaviour, public opinion would quickly

turn against the incumbents and the Canadian government would likely intervene.

2.2.1.4 Economies of Scale

Banking is a low margin business, and as a result there are significant

economies of scale to be gained for small and medium sized banks. Some of these

economies of scale can only be realized through size, however many can be gained

through outsourcing back office and administrative functions. There are few, if any,

economies of scale to large banks becoming even larger. Studies show that size does

not correlate with cost reduction, but that banks find greater efficiencies when faced with

high competition as a result of dereg~lation.'~

Credit Unions, typically smaller players in SME financing have invested

significantly in back office centralization over the past 10 years in order to realize

economies of scale.

2.2.1.5 High Branding 1 Reputation Building Costs

Consumers entrust their savings, personal information, and their consumption

information to financial institutions. As a result, banks invest heavily in promoting an

image of trustworthiness and stability. Banks invest heavily in brand building through

advertising, branch design and community sponsorship.

l 3 Carbo Valverde, S., Humphrey, David B., and Rodriguez Fernandez, F. Bank deregulation is better than mergers. International Financial Markets, Institutions and Money. (2003). Vo1.13: 431

19

2.2.1.6 Mature Market Stifles Entry

The SME financing market is a mature market with an exp (J cted growth rate

between 5 percent and 7 percent.14 Any new entrant would have to gain market share at

the expense of incumbents. The aggressive pricing and advertising necessary to entice

customers to switch erodes margins.

2.2.1.7 Low Barriers to Entry

Although, economies of scale and high reputation building costs present

significant barriers to entry into the Canadian SME financing industry, there are many

foreign banks and large finance companies with the similar products and brand equity

who are not yet operating in the market. Companies such as ING Direct or GMAC could

use the economies of scale afforded by their personal lending businesses and their

recognized brand to enter the market. Witness HSBC's entry into the market in 1986

and its growth to 12 percent market share.

As well, the incumbents in the industry are under heavy government scrutiny, so

their ability to retaliate against a new entrant is very limited. The government is intent on

increasing competition in this industry and is reducing legislative and regulatory barriers

to entry. Finally, technology is allowing banking distribution to take place with lower

overhead costs and without having to employ bricks and mortar distribution, which

increases the potential scale of entry while reducing the capital outlay.

The Canadian SME financing market can expect more attempts to enter the

market. Given the success of HSBC and the lessons learned by Wells Fargo's failed

entry, in the medium term there is a high likelihood of new entrants.

14 Canada. Statistics Canada. Survey.

2.2.2 Suppliers

2.2.2.1 Shortage of employees with experience and training

Training for a new commercial financial analyst can take up to a year. Banks pay

for their employee training courses and on the job training is a significant cost. This

reliance on in house training and the lack of outside accreditations in the business-

lending field has increased the power of trained and experienced employees.

There are frequent instances where employees are poached from one financial

institution to another. This is an attempt to shift the risk of investing in employee training

from the acquiring institution to the one losing the employee; as well it is an attempt to

avoid the cost of training employees. Generally these employees are offered a 10

percent increase in pay to leave their current employer, which leads to an upward trend

in labour costs.

2.2.2.2 Information Technology Providers

Increasingly, banks are relying on third party suppliers for services such as digital

document storage, computer networks, telephone systems, transaction processing,

merchant services, credit scoring and ERP systems. These are fundamental business

functions and as a result the risks of the service providers can potentially impact the risk

to a bank. In most cases, these functions have been outsourced to take advantage of

economies of scale or to large investments in developing business functions, which are

not core competencies. As a result of these needs for economies of scale and the scale

of business transacted with a particular supplier, there are usually very few suppliers in

the market. The scarcity of alternative suppliers as well as the high switching costs for

these services, gives suppliers a degree of power over banks. The largest 5 Canadian

banks have resolved this, in some instance, by securing ownership in many of their

service suppliers, however smaller banks and credit unions have to find other solutions I

to mitigate supplier power.

2.2.2.3 Real Estate Scarcity

Most Canadian banks and credit unions rely on a retail branch distribution

network. Suitable real estate for branches is scarce, as the incumbents have already

established branches in the most suitable locations. As well, since banks require unique

leasehold improvements to accommodate large safes and sophisticated security

systems, landlords have the ability to extract long-term commitments and higher rents.

Finance companies often distribute their loan and lease financing through the

equipment vendors and vehicle dealerships. The finance companies are often affiliated

with the dealers. This reduces the cost of distribution, however since they do not have

direct contact with their customer the risks are greater.

2.2.2.4 High Availability of Capital

Large Canadian banks, insurance companies, and finance companies have high

capital availability both through equity markets, bond issues and securitization of assets

such as their mortgage and consumer credit portfolios. Smaller banks, due to poorer

credit ratings have slightly higher cost of funds. This can have a significant impact on

ROA since banking is a low margin business. Market forces do not set Credit Union cost

of funds. Members own shares of the credit union and receive a dividend at the

discretion of the Board of Directors. Except of Credit Unions, large banks benefit from

lower cost of funds and capital availability.

2.2.2.5 High Supplier Power

Suppliers to the Canadian banking industry, including SME lenders, have high

relative clout. Many have products and skills that are needed in the banking industry but

are transferable to other industries as well. Granted, the incumbents in the SME

financing market have high capital availability. The largest players are major Canadian

banks with billions of dollars in market capitalization and relative ease when raising

capital either in debt or equity markets.

This clout however is tempered by relative real estate scarcity. Banks depend on

branch distribution as their primary method of contact with customers, and the number of

suitable locations is limited. There are very few untapped markets and as a result when

a location does become available the landlords have greater leverage.

As well, once a bank has committed to certain IT and IS providers, the

relationship is necessarily long term. The banks may have clout during the bidding

process, however once a bank is running on a platform and the employees have been

trained to the platform the bank is dependent on that supplier.

Finally, a shortage of accredited, trained and experiences employees constantly

challenges the industry. Banks attempt to reduce turnover by providing high benefits,

profit sharing and stock purchase plans however turnover continues to be a challenge.

2.2.3 Customers Analysis

Relative to their lenders, SME borrowers are very small and diffused. There are

some associations of SMEs, such as the Canadian Chamber of Commerce and the

Retail Merchants Association, which have negotiated group pricing for merchant

services and insurance, however due to the risk characteristics unique to each SME

borrower these Associations have not negotiated group pricing for financing. The only

category that has negotiated group pricing for financing is franchises. Since franchisees

will each have similar risk profiles to one another and the group has a lower risk than

unbranded business, banks have been able to create uniform pricing packages for

franchises.

Traditionally, banks have segmented the SME market base,d on the amount of

authorized credit. Based on this criterion, there are three market segments in the SME

market. There are small enterprises with authorized credit under $500 thousand and

medium sized enterprises with authorized credit under $1 million. Micro businesses are

another segment usually with financing under the $25 to $99 thousand range, however

there is little consensus on the definition of this segment. Micro businesses are also

described as self-employed businesses or home-based businesses. Micro businesses15

comprise 39 percent of SMEs who borrow from domestic banks; Small enterprises16

comprise 52 percent while medium-sized enterprises make up the remaining 9 percent

of the market.

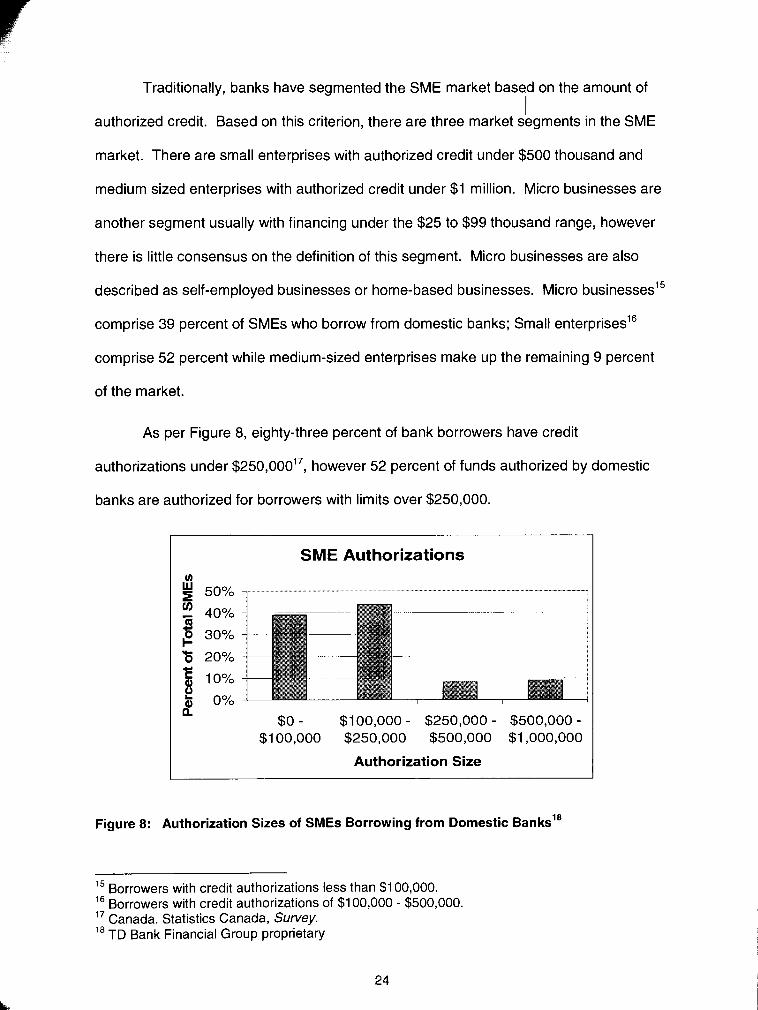

As per Figure 8, eighty-three percent of bank borrowers have credit

authorizations under $250,000~~, however 52 percent of funds authorized by domestic

banks are authorized for borrowers with limits over $250,000.

SME Authorizations

Figure 8: Authorization Sizes of SMEs Borrowing from Domestic ~anks' '

l 5 Borrowers with credit authorizations less than $1 00,000. l6 Borrowers with credit authorizations of $1 00,000 - $500,000. 17 Canada. Statistics Canada, Survey. 18 TD Bank Financial Group proprietary

Different regions of Canada have different industry focuses. As seen in Table 2,

the prairies have a strong agricultural sector. Quebec, Ontario, Alberta and BC all have

significant professional communities. Likewise they have the greatest concentrations of

knowledge-based industries.

Atlantic Provinces 6.6% 9.4% 5.1% 15.0% 7.5% 2.3% 54.2%

Quebec 9.7% 1.7% 7.1% 13.2% 10.8% 4.0% 53.4%

Ontario 8.5% 0.7% 5.6% 10.4% 12.5% 5.6% 56.7%

ManlSasklNunavut 44.8% 1.2% 3.0% 8.2% 4.3% 1.9% 36.7%

Table 2: SMEs' Sectors of Operations by Region in 2000'~

An Angus Reid survey of SMEs in 2000 found four perceived gaps in financing

service^.^' These gaps are size, risk, knowledge, and flexibility. SMEs often feel that

their financing requests are too small to gain the attention of banks and that banks are

more interested in larger volume deals. SMEs also believe that Canadian banks have a

very limited appetite for unsecured lending and are not willing to assume any risk. SMEs

in knowledge based feel that financial institutions do not understand their businesses

and that they are too quick to discount knowledge assets, such as patents, software and

the goodwill associated with an established brand. Finally, SMEs feel frustrated with the

lack of flexibility in what they believe is a "cookie cutter" approach to financing, where

standard ratios and credit scoring methods take precedence over common sense

business decisions. As much as possible, TDBFG's optimal strategy will attempt to

address these financing gaps.

l9 Canada. Industry Canada, Small and Medium-sized Enterprise (SME) Financing in Canada, Ottawa, 2002: 61 20 Angus Reid Group, Financing Services to Canadian Small and Medium Size Enterprises, July 2000: 19

2.2.3.1 Information asymmetry fading

ri Regulators are working in conjunction with institutions to e sure consumers are

adequately informed and protected by establishing disclosure rules and guidelines.*'

Transparency of information is critical given the history of information asymmetry

between consumers and institutions. Although many bank products are very similar,

they are presently presented in a way that makes inter bank comparisons difficult. For

example, a year ago the top five banks described interest rates on unsecured lines of

credit differently. Some tied the variable rate to the Prime rate and others tied it to their

Base rate. The Base rate is proprietary and not set by the market, and although it is

related to the Prime rate, different banks set their own Base rates. As a result of

government intervention, this practice has ended, however there are similar difficulties

when attempting to compare service charges at different institutions. As a result of

government regulated greater disclosure, customers are more informed and

sophisticated.

As demographics change, the average Canadian is becoming older and better

educated. As a result, they are becoming more knowledgeable and sophisticated in

evaluating their financial service providers. They are also becoming more comfortable

with alternatives distribution channels and service providers."

2.2.3.2 Product Homogeneity

Banking products are fairly homogeneous. This limited differentiation allows

customers to more easily compare between providers and reduced differentiation limits

banks' ability to charge higher margins.

2' The Financial Consumer Agency of Canada (FCAC) was founded in 2001 under the Financial Consumer Agency of Canada Act to consolidate and strengthen oversight of consumer protection measures in the federally regulated financial sector, and to expand consumer education. 22 McKinsey & Company, The Changing Landscape 25

26

2.2.3.3 Canadian Consumers Perceive Banks to Provide Little Value ~ d d e d ~ ~

The vast majority of Canadians are satisfied with the service provided by their

banks, however the number of dissatisfied customers is growing. Compared to other

service providers, when consumers were asked if the services provided were very good

or excellent, Canadian banks ranked lower than supermarkets and air travel but higher

than department stores and auto dealerships. If the satisfaction trends continue,

consumers will become increasingly open to alternative banking service providers.

2.2.3.4 Media and Regulators Trumpet Anti-Bank Rhetoric

Canadian media and regulators have increasingly echoed the rhetoric of special

interest consumer groups such as the Democracy Watch, Consumers' Association of

Canada and the People's Network on Banking, Credit and Capital. These groups focus

on the size and power of banks in the Canadian Competitive Analysis Chart of SME

Lending in Canadian economy and push for greater control and regulation of banks.

These groups also advocate nationalizing other industries to protect consumers from

profit seeking corporations. This type of media attention restricts banks to conservative

marketing and sales practices, which in turn reduce differentiation and increase

competition.

2.2.3.5 Increasingly Complex Underwriting Processes

With greater software sophistication and credit scoring systems, customers often

do not understand why they were approved, declined or why they must meet ongoing

financial conditions for leverage and cash flow. An Account Manager at a major

Canadian bank sells from a suite of over 20 debt product products and services in

addition to a multitude of deposit and cash management products. When customers are

presented with a huge product offering with varied bundled and un-bundled pricing

structures, they are more likely to purchase based on the advice of a bank employee,

23 McKinsey & Company, The Changing Landscape 67

27

rather than attempt to learn the product offering well enough to make their own informed

decision. This and the fact that consumers of bank services are not very price sensitive

gives banks some leverage in the producer-consumer relationship.

2.2.3.6 Lack of Buyer Concentration

Except merchant service agreements negotiated by trade associations and group

pricing for franchises, consumers of Canadian financial services do not form buying

groups to negotiate products and pricing with banks. There is a concentrated group of

financial service providers, each negotiating with individual SMEs on a one to one basis.

This again gives banks a distinct advantage in preserving fees and interest rate spreads.

2.2.3.7 Buyer Power is Low

Although public information on SME lending is improving, it is still not high. The SME

lending products are fairly homogeneous, however buyer concentration is very low and

customers are not aware of the high level of homogeneity. Customer price sensitivity is

low and on the whole customer power is low.

Even though buyer power is low, customer retention is still a real issue. Typically it costs

five times more sell to a new customer than cross sell that same product to an existing

customer.24 As a result of this TD Canada Trust has chosen to differentiate itself by

providing the most comfortable banking experience. This does not necessarily

contradict its low cost provider strategy, it is directed more toward the customer

experience and corporate culture. This strategy is similar to those of Walmart and

Westjet, which are both low cost producers but have nurtured customer centric cultures

that result in higher repeat business than their competitors. TD Canada Trust has been

recognized as an industry leader with one of the best managed brands in the financial

24 Deloitte. Global Banking Industry Outlook: 2004 Top Ten Issues.

28

services industry, preserving Canada Trust's reputation for strong customer service.25

Chris Armstrong, Chief Marketing Officer at TDBFG won Marketing's Marketer of the

Year for 2001.

2.2.4 Substitutes

SMEs find financing for their businesses from a variety of sources. Even though,

there are six banks that dominate the business loan market, there are other products to

consider. While Table 3 provides a broad perspective on the types of financing and

shows that individual SMEs source their financing needs from a variety of sources, it

does not provide an accurate picture of their share of SME liabilities.

Financing Instrument Percent of SMEs that use that Instrument Loans from Financial Institutions 49% Su~olier Credit 39% ~ e k o n a l Savings 35% Personal Credit Cards 33% Retained Earnings 31 % Business Credit Cards 26% Leasing 16% Personal Loans 14% Loans from friends and relatives 10% Government lending agencies 7% Angel investment 4%

Table 3: Sources of SME ~ i n a n c i n ~ ~ ~

Figure 9 shows the share of SME financing undertaken by each source.

loans from crown

lease obligations

loans from banks and loans from indiidu credit unions

35%

other liabilities 21 %

Figure 9: Breakdown of SME Liabilities by Type, 2 0 0 0 ~ ~

25 Woolstencroft, Timothy and Hanna, Jeannette. "The Best-managed Brands are about Delivering Customer Esperience" Marketing. 21 June 2004: 33. 26 Canadian Bankers Association, Cornpetion 6

29

2.2.4.1 High Threat from Alternate Distribution Channel

i Canadian Domestic Banks are under increasing pressure f om service providers

using alternative distributions channels. In 2001 ClBC created Amicus a division

responsible for operating non-CIBC branded electronic banking services. In the US,

Amicus offered personal banking in Safeways under the Safeway SELECT brand. In

Canada, Amicus operates President's Choice Financial out of Loblaws and it used to

offer business banking under bizsmart branding in Business Depot stores. There are

challenges related to chequing account and business current account services online

and in November 2002 ClBC began to wind up Safeway SELECT and other US

electronic Banking relationships, as these operations were not meeting financial

expectations. President's Choice Financial was expected to break even in 2003,

however CIBC's reporting for electronic bank operations is now combined with the

branch retail operations and figures for this division are no longer available. ING Direct

and Citizens Bank have both successfully entered the market using electronic

distribution by providing a simple suite of banking services and avoiding highly

transactional, fee based, chequing accounts. Wells Fargo made a failed attempt to enter

the market in 1999. The company has not provided much insight into why it exited the

Canadian market, however its pricing was not lower than the competition.

Mortgage Brokers also compete against traditional branch distribution,

sometimes obtaining greater rate discounts from Canadian Banks than their branch

networks are able to offer. Similar agency issues exist in equipment financing, where

banks have begun to offer car and truck loans though dealerships, in order to compete

against the incumbent finance companies, and these same loans are not offered through

the retail branches.

27 Canadian Bankers Association, Competition 6

30

2.2.4.2 Increased Competition from Monoline Providers

An increasing variety of single product businesses compete against Canadian

retail banks. In credit cards, MBNA, Capitalone, Citibank and American Express are

well established both in Canada and internationally. Other examples of niche players in

credit are, GMAC in car financing and the Business Development Bank, a Crown

Corporation. Factoring companies also fall under this category even though they have

found limited acceptance in the Canadian market.

In 1997 ING Direct began offering non-traditional savings accounts. American

Express followed ING in 1999 offering a similar savings account product with high

interest rates, no fees and no minimum balance requirements.

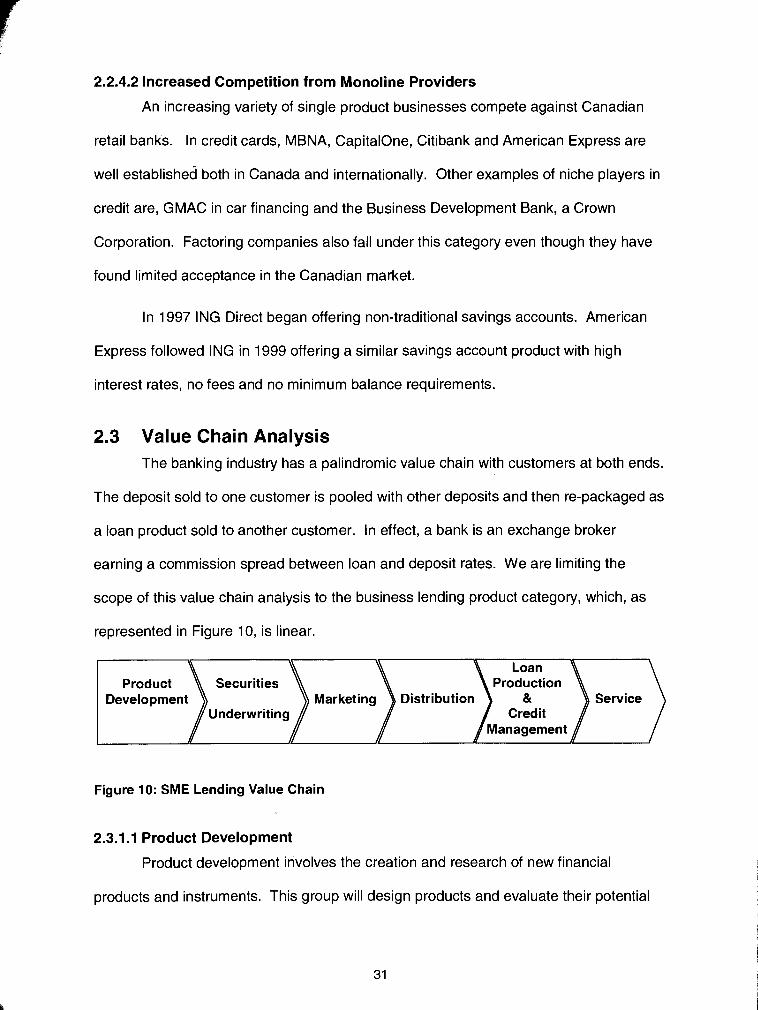

2.3 Value Chain Analysis The banking industry has a palindromic value chain with customers at both ends.

The deposit sold to one customer is pooled with other deposits and then re-packaged as

a loan product sold to another customer. In effect, a bank is an exchange broker

earning a commission spread between loan and deposit rates. We are limiting the

scope of this value chain analysis to the business lending product category, which, as

represented in Figure 10, is linear.

Der7~;;;nt> securities > Marketing > Distribution

Underwriting

Figure 10: SME Lending Value Chain

2.3.1.1 Product Development

Product development involves the creation and research of new financial

products and instruments. This group will design products and evaluate their potential

performance and profitability. This group delineates product definitions, term and

I conditions and evaluates the opportunities for bundling and the appropriate pricing limits.

If Product Development determines that the Bank cannot profitably produce a product

and they determine that the Bank needs to offer the product, they will refer the need to

outsource management. The business product group has made very limited use of

outsourcing.

When designing a product, product group must design with the entire product life

cycle in mind. 28 Using market research, Product Design at TDBFG looks for innovative

ways to redesign traditional banking products to make them more attractive to

customers. An example of this is the "cash back mortgage". A cash back mortgage is

booked at the market rate however the customer receives a percentage of the borrowed

amount as cash back on the mortgage. Another product is the "below prime mortgage"

which offer a rate below prime rate for the first 6 months and then reverts to regular

market rates. In both these instances the benefit to the customer is equivalent to less

than a 0.75 percent discount on the standard mortgage rates. These innovative

products allow the Bank to gain market share without competing on price, effectively

preserving bank margins. They also create a degree of differentiation for what would

otherwise be a commoditized product offering.

2.3.2 Securities Underwriting

Securities and risk management is the process by which bank assets are

classified by risk and matched with a bank liability of corresponding duration. As well,

instead of matching funds from deposits to loans, the Bank may securitize a loan

portfolio and sell it on the secondary market. Securitizing creates a pass through, such

as a mortgage-backed security, by which the pooled assets become standard securities

28 See Appendix A

backed by those assets and is exchanged for cash. The cash in turn increases the

Bank's liquidity and ability to extend more loans.

2.3.2.1 Securitization Design at TDBFG

Securitization is used to preserve the Bank's liquidity. For example, a portfolio of

similar risk mortgages is pooled and sold as an income product with similar

characteristics to a bond. When the instrument is sold, the Bank receives cash in return

for the sale of the assets. The Bank is then able to lend this cash to additional

borrowers. Securitization increases the efficiency of a key component of the multiplier

effect. Loans can be packaged as mortgage backed securities, banker's acceptances

and bonds, issued by the Bank.

2.3.3 Marketing

Marketing is responsible for market research, brand management, advertising,

and sales. Sales may involve sales support for a retail or branch network, or it may

involve direct sales via Internet or direct mail. Marketing will also support product sales

and development for broker and agent channels.

2.3.3.1 Marketing Analytics

The Bank regularly reviews its customer base to look for higher margin

opportunities. Recently marketing analysis has identified commercial and small

business banking, and insurance as high margin growth opportunities for the Bank.

Marketing also researches competing products in North America and around the world to

prepare the Bank for any potential threats.

2.3.3.2 Market Research

The Bank contracts out market research hiring a marketing agency, Harrod &

MirlinIFCB, to conduct surveys and customer focus groups. The Bank also conducts

data mining to support its telemarketing and direct mail efforts.

2.3.3.3 Advertising

The Bank's advertising is split amongst newspaper, radio, A7 agazine, online and

interior transit advertising. Print ads also run in newspapers across the country, including

the Globe and Mail, Toronto Star and National Post, as well as in national consumer and

business magazines. The primary purpose of advertising is to communicate the Bank's

value proposition and positioning as the most comfortable bank to deal with.

2.3.4 Distribution

Distribution represents the contact point with the consumer. In the banking

industry products may be offered through a wide variety of distribution channels.

2.3.4.1 Bank Branch

The majority of Canadian banking services are sold through bank branches.

These are fixed retail locations owned by chartered banks, trust or credit unions. These

retail operations carry a full suite of business lending products.

At TDBFG the retail branch network is considered the most stable source of cash

flow for the Bank. The branch network's primary function is sales of products and

services. The Bank has recently focused the attention of the branch networks on the

higher valued customers. The cost of the branch network is very high, and to the

network to run efficiently employees must add value with the majority of customer

interactions. It is recognized by marketing that 2 percent of customers generate 98

percent of the Banks profits. The Bank is focussing on this highly valued 2 percent of

customers and seeking ways to increase their market penetrations.

The branch is divided into two functions, sales and service. Sales employees

deal in lending and investments whereas service employees deal in day-to-day

transactional banking and sales support. Sales staff is evaluated primarily on sales

revenue generation and service staff is evaluated based on customer service

satisfaction.

Cross Selling Systems

Cross selling systems are considered a key driver to fully leveraging the benefits

of the TD Bank and Canada Trust Merger. Using the following systems, the Bank hopes

to earn greater economies of scope.

Economies of scope occur when the Bank achieves cost savings by increasing

the variety of goods and services that it produces (joint production). Such effects arise

when it is possible to share inputs and to use the same facilities and personnel to

produce several products. For example, the Bank may sell creditor insurance with its

mortgages in its local branches in order to spread the fixed costs (like the office rent)

over a larger number of products.

RadarILeads

Radar Leads is a basic data mining system that cross references customer

demographics with their current product set with the Bank and determines what products

the customer may be interested in buying. The next time the customer visits the branch

to make a transaction, a lead is triggered and the employee is prompted to initiate a

conversation about the target product. This system is designed to increase customer

product penetration, which will in turn lead to greater market share and higher

profitability for each customer relationship.

TD Leads also has the ability to create referrals to other Bank Division with a

consistent referral mechanism for achieving economies of scope. Even though different

business units use different software platforms, the web based referral system is

accessible from every unit in the Bank and allows consistent communication and

tracking of referrals between different business units.

2.3.4.2 Retail Stores

Retail stores such as Staples and Home Depot offer in-ho e credit to business

customers. Staples bizsmart, was a re-branded product line produced by Amicus Bank,

a ClBC subsidiary. ClBC has since discontinued this relationship with Staples.

Apparently the relationship was not profitable.

TDBFG recently disengaged itself from a partnership with Walmart after the US

government declined its request to expand in-store branches into the United States.

2.3.4.3 Brokers & Agents

In the business lending market, brokers and agents primarily offer property

secured business mortgages. Unlike bank branches, brokers will source their products

from a variety of financial institutions and will receive compensation from these

companies based on the volume and pricing negotiated on a product. Brokers can sell

the same products that may be available in branches and are often a source of channel

conflict. Other Agents sell banking products as well. Car dealerships offer loan

financing underwritten by several banks depending on the purchaser's preferences.

TDBFG has several products including mutual funds and mortgages that are sold

through brokers and agents. The Bank has regional marketing support offices that are in

continual contact with brokers and agents supporting them with information and support

for selling the Bank's products. Business loans are not one of the products sold through

the broker agent channel.

2.3.4.4 lnternet & Telephone

The lnternet has allowed Chartered Banks to offer their full product line over the

lnternet and telephone. As well, several credit card companies post links to applications

for their business credit cards online.

TDBFG employs a department called e.Bank whose purpose is to generate sales

through non-branch channels. This includes online adds, telemarketing and direct mail.

This channel competes directly with retail branch network, however the Bank recognized

that competitors market to customers in the same fashion. The Bank feels that

cannibalising customers from the retail channel is better than losing customers to

competitors.

2.3.4.5 Direct Mail

Many monoline finance companies sell products using direct mail. Most often

credit cards are sold in this fashion. Banks often offer businesses term loans via direct

mail offers.

2.3.5 Loan Production & Credit Management

A unique characteristic of production in lending is that the product is customized

and production begins after the first contact with the customer. The customer first

applies for a loan, the Bank produces an offer that the customer in turn accepts or

rejects. At this point, the Bank has already expended resources and time, but has no

guarantee that the customer will purchase the product. If the customer accepts, then the

Bank produces documentation, which the customer signs at the next meeting after which

the loan is funded. The process can be fairly costly.

2.3.5.1 Credit Management

At TDBFG, Credit Management provides effective risk management for the loan

portfolio within quality guidelines while acting as an advisor through ongoing

communication and sharing of information with the distributions network. Credit