Embed Size (px)

Citation preview

1Confidential

THE NEW PAYMENTSECOSYSTEM: FAST, OPEN, SECURE ANDDISRUPTIVE

OPEN! Open Payments and theirImpact on Banks.

2Confidential

FOREWORD BY DAREN WEDGE AND JOEL VAN ARSDALEDigital payments, open APIs and real-time account to account transactions are driving change across the payments landscape. As a result, consumers, businesses, merchants, and financial institutions present a growing list of fast-changing demands.

By aligning business models with today’s evolving payment trends, banks have the opportunity to securely grow their offerings and boost top-line revenue.

ACI partners with all types of payment service providers from around the globe to help them adapt to the new payments ecosystem, improve efficiencies, create new revenue opportunities and shield against increasing fraud risk.

OPEN payments represent one of the four pillars of the new payment ecosystem bringing new opportunities for growth for banks and FinTechs alike.

Daren Wedge, SVP Sales, ACI Worldwide

Payments are becoming more OPEN - offering greater accessibility, flexibility, and transparency. Market forces including globalization and the impact of mobile technologies are forcing providers of payment services to embrace open technologies and open business models. This shift is positive for users and providers of payment services who are well positioned to leverage innovation to achieve exceptional growth. In Europe, the legislature and regulators continue to push for greater openness in the form of open banking. PSD2 is a significant agenda for change and ultimately all providers of payment services must strive to become more open in order to avoid disruption.

Joel Van Arsdale, Partner, First Annapolis Consulting

3Confidential

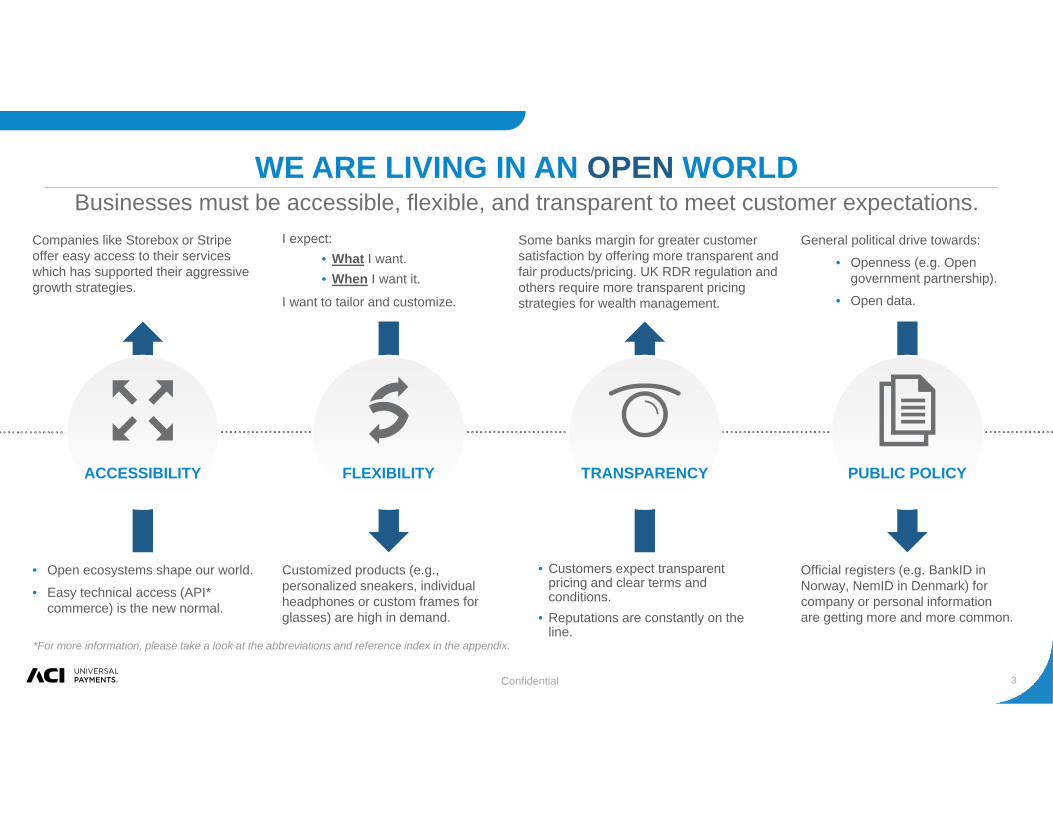

WE ARE LIVING IN AN OPEN WORLDBusinesses must be accessible, flexible, and transparent to meet customer expectations.

• Open ecosystems shape our world.

• Easy technical access (API* commerce) is the new normal.

ACCESSIBILITY FLEXIBILITY TRANSPARENCY PUBLIC POLICY

Customized products (e.g., personalized sneakers, individual headphones or custom frames for glasses) are high in demand.

• Customers expect transparent pricing and clear terms and conditions.

• Reputations are constantly on the line.

Official registers (e.g. BankID in Norway, NemID in Denmark) for company or personal information are getting more and more common.

Companies like Storebox or Stripe offer easy access to their services which has supported their aggressive growth strategies.

I expect:• What I want.• When I want it.

I want to tailor and customize.

Some banks margin for greater customer satisfaction by offering more transparent and fair products/pricing. UK RDR regulation and others require more transparent pricing strategies for wealth management.

General political drive towards:

• Openness (e.g. Open government partnership).

• Open data.

*For more information, please take a look at the abbreviations and reference index in the appendix.

4Confidential

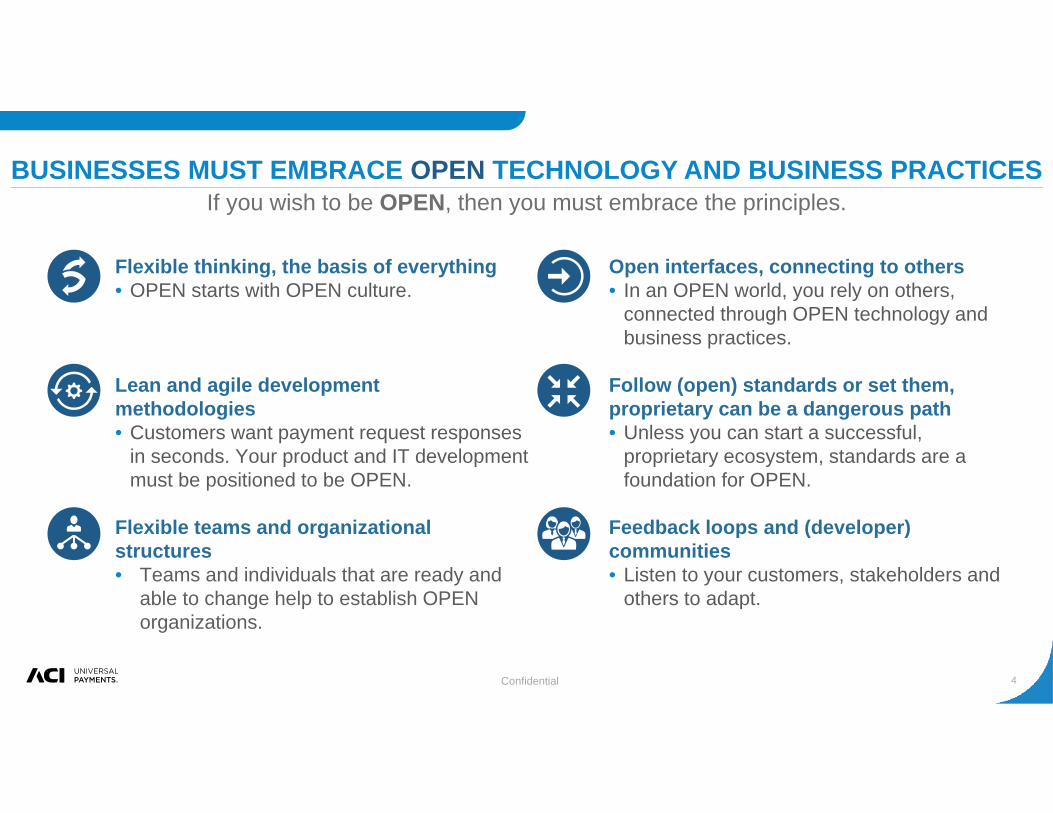

BUSINESSES MUST EMBRACE OPEN TECHNOLOGY AND BUSINESS PRACTICESIf you wish to be OPEN, then you must embrace the principles.

Flexible thinking, the basis of everything• OPEN starts with OPEN culture.

Lean and agile development methodologies• Customers want payment request responses

in seconds. Your product and IT development must be positioned to be OPEN.

Flexible teams and organizational structures• Teams and individuals that are ready and

able to change help to establish OPEN organizations.

Open interfaces, connecting to others• In an OPEN world, you rely on others,

connected through OPEN technology and business practices.

Follow (open) standards or set them, proprietary can be a dangerous path• Unless you can start a successful,

proprietary ecosystem, standards are a foundation for OPEN.

Feedback loops and (developer) communities• Listen to your customers, stakeholders and

others to adapt.

5Confidential

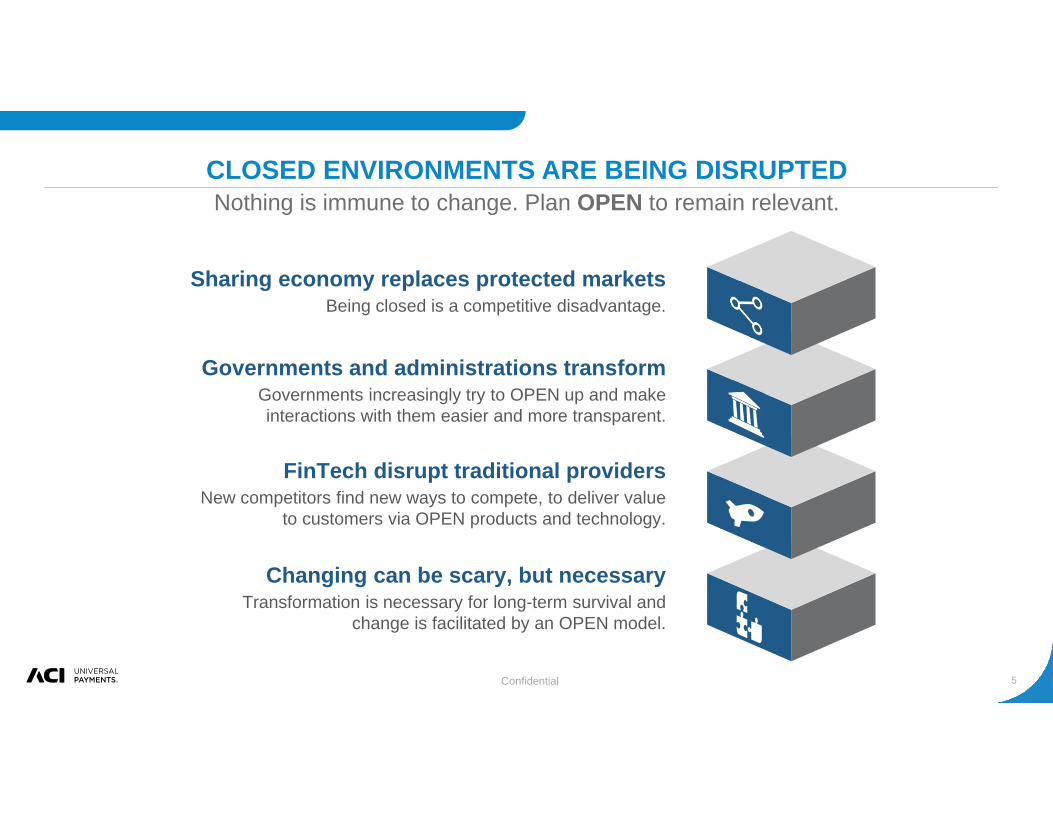

CLOSED ENVIRONMENTS ARE BEING DISRUPTEDNothing is immune to change. Plan OPEN to remain relevant.

Governments and administrations transformGovernments increasingly try to OPEN up and make interactions with them easier and more transparent.

FinTech disrupt traditional providersNew competitors find new ways to compete, to deliver value

to customers via OPEN products and technology.

Changing can be scary, but necessaryTransformation is necessary for long-term survival and

change is facilitated by an OPEN model.

Sharing economy replaces protected marketsBeing closed is a competitive disadvantage.

6Confidential

OPENNESS DRIVES AGILITY, WHICH IS AN INCREASINGLY IMPORTANT FACTOR FOR SUCCESS

OPEN and agile businesses are not hindered by change.

AGILETECHNOLOGY

*For more information, please take a look at the abbreviations and reference index in the appendix.

AGILEORGANIZATION

AGILE BUSINESSPRACTICES

Your tech stack should be adaptableand adjustable with a mindset for continuous improvement. Agile

technology is about having the right systems, people, and processes (you

need all three).

Start with the customer and go from there. Learn to break ambitions

into bite sized pieces. Embrace failure, learn, and adapt. Seek out

others with similar or complementary ambitions.

Think of how to not only develop but also manage agile. Only by combining agile

development and agile management, will you achieve a truly agile organization.This is ultimately needed to thrive in an

OPEN environment.

7Confidential

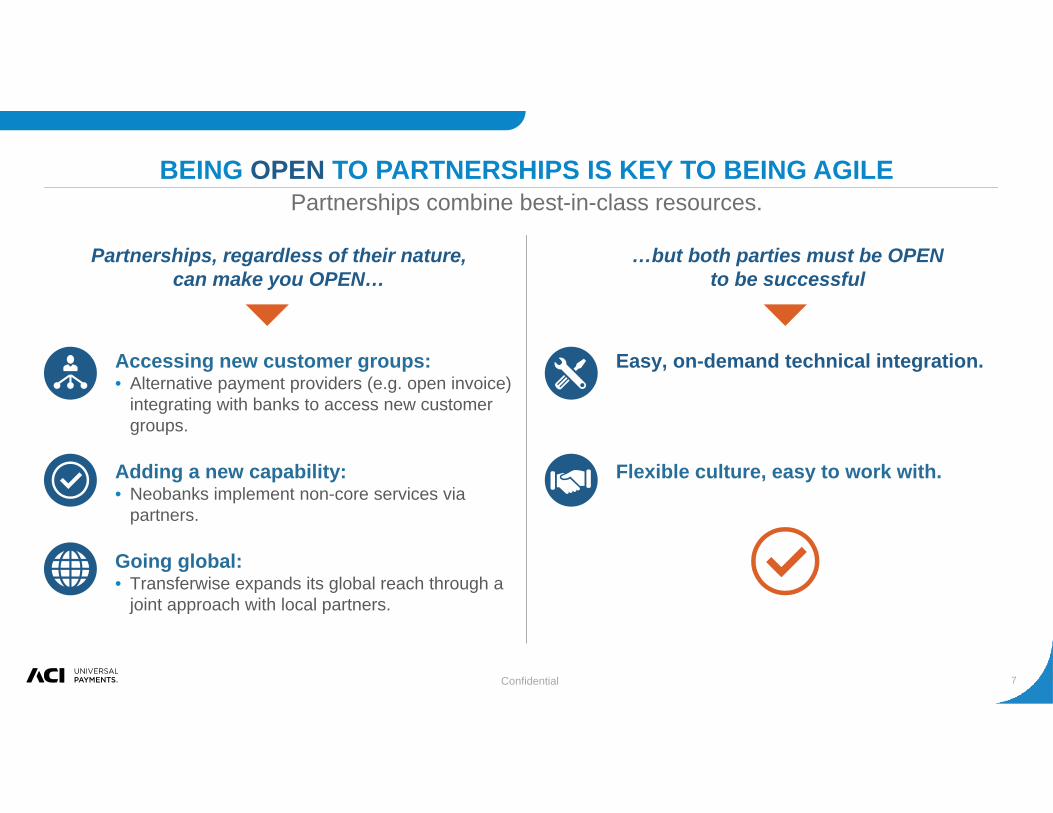

BEING OPEN TO PARTNERSHIPS IS KEY TO BEING AGILEPartnerships combine best-in-class resources.

Partnerships, regardless of their nature, can make you OPEN…

…but both parties must be OPENto be successful

Accessing new customer groups:• Alternative payment providers (e.g. open invoice)

integrating with banks to access new customer groups.

Adding a new capability:• Neobanks implement non-core services via

partners.

Going global:• Transferwise expands its global reach through a

joint approach with local partners.

Easy, on-demand technical integration.

Flexible culture, easy to work with.

8Confidential

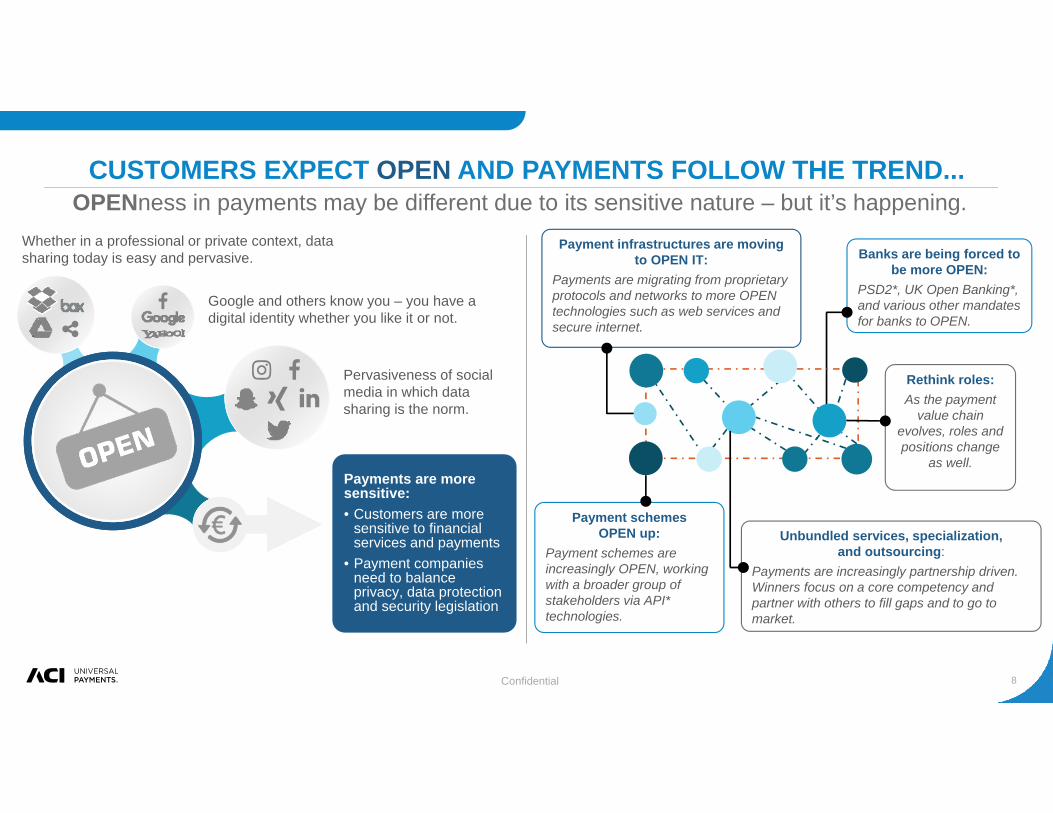

CUSTOMERS EXPECT OPEN AND PAYMENTS FOLLOW THE TREND...OPENness in payments may be different due to its sensitive nature – but it’s happening.

Payments are more sensitive:• Customers are more

sensitive to financial services and payments

• Payment companies need to balance privacy, data protection and security legislation

Pervasiveness of social media in which data sharing is the norm.

Whether in a professional or private context, data sharing today is easy and pervasive.

Google and others know you – you have a digital identity whether you like it or not.

Rethink roles:As the payment

value chain evolves, roles and positions change

as well.

Payment infrastructures are moving to OPEN IT:

Payments are migrating from proprietary protocols and networks to more OPEN technologies such as web services and secure internet.

Banks are being forced to be more OPEN:

PSD2*, UK Open Banking*, and various other mandates for banks to OPEN.

Unbundled services, specialization, and outsourcing:

Payments are increasingly partnership driven. Winners focus on a core competency and partner with others to fill gaps and to go to market.

Payment schemesOPEN up:

Payment schemes are increasingly OPEN, working with a broader group of stakeholders via API* technologies.

9Confidential

Openness and new technologies bring new threats:• Digital identity theft; malware.• Foreign cyber assaults.• Mobile device fraud.• Phones as repositories of ID data.

Former pillars of trust change:• Physical cards.• Physical decoders. • Physical signatures.• Personal interaction.

New threats can be targeted technically or regulatory – but not every idea is a good solution:• Device fingerprinting*.• Machine learning and AI*.• Detection systems.• Biometrics.• Strong authentication*/liability.

OPEN PAYMENTS CAN’T EXIST AT THE COST OF SECURITYPayment systems must be OPEN and SECURE.

Building new trust is possible with data transparency and sharing:• National or bank digital IDs.• Social IDs.• Digital profiles (Google, etc.).• User ratings.• Mobile app transparency (history, locations, etc.).

*For more information, please take a look at the abbreviations and reference index in the appendix.

10Confidential

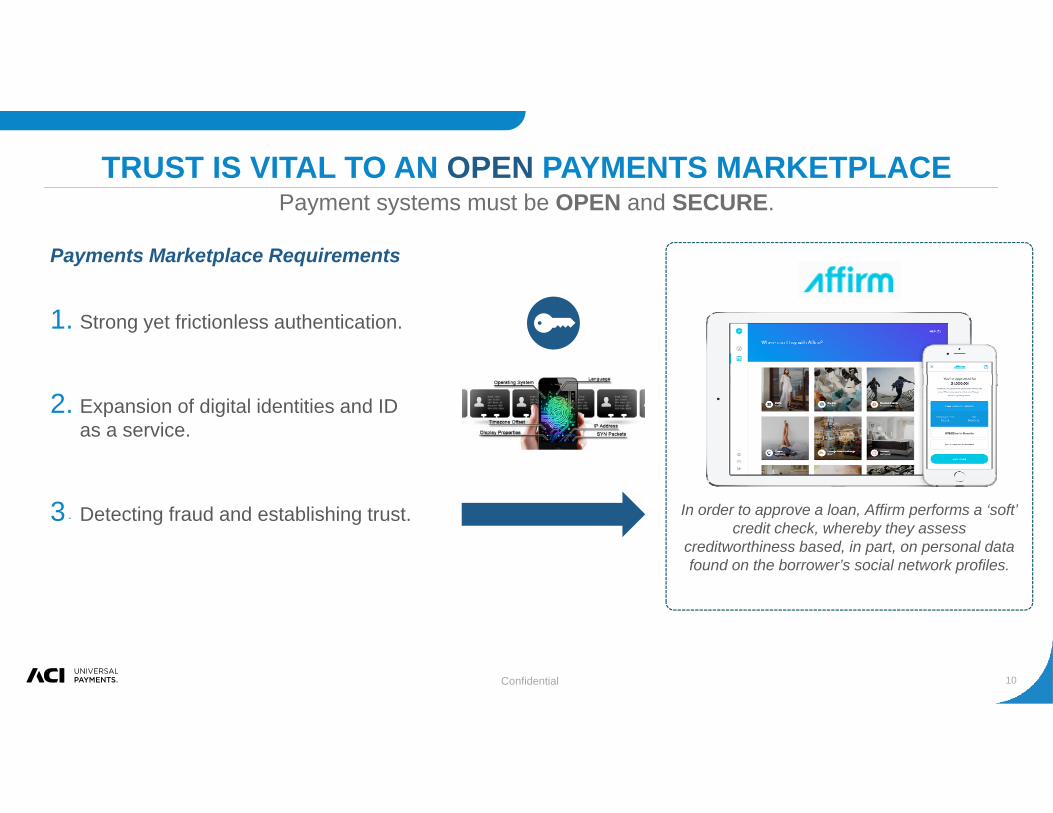

TRUST IS VITAL TO AN OPEN PAYMENTS MARKETPLACEPayment systems must be OPEN and SECURE.

Payments Marketplace Requirements

1. Strong yet frictionless authentication.

2. Expansion of digital identities and IDas a service.

3. Detecting fraud and establishing trust.3 In order to approve a loan, Affirm performs a ‘soft’ credit check, whereby they assess

creditworthiness based, in part, on personal data found on the borrower’s social network profiles.

11Confidential

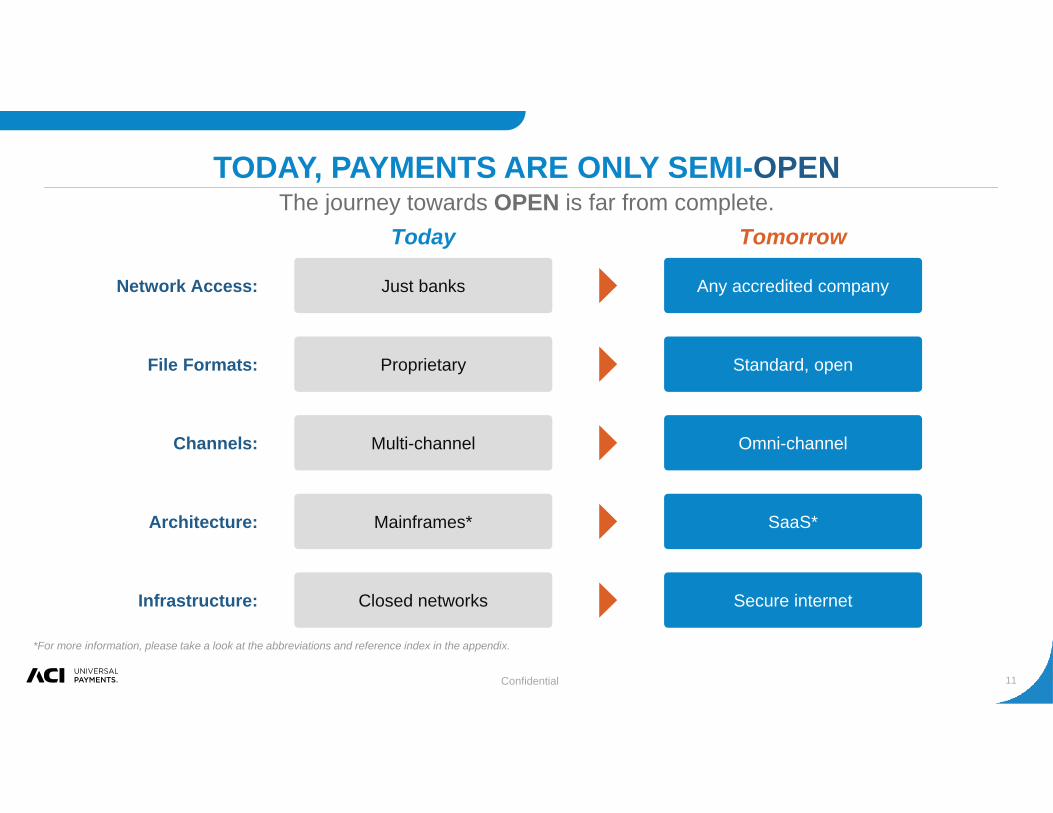

TODAY, PAYMENTS ARE ONLY SEMI-OPENThe journey towards OPEN is far from complete.

Today

Just banks

Tomorrow

Any accredited company

Proprietary Standard, open

Multi-channel Omni-channel

Mainframes* SaaS*

Closed networks Secure internet

Network Access:

File Formats:

Channels:

Architecture:

Infrastructure:

*For more information, please take a look at the abbreviations and reference index in the appendix.

12Confidential

TRUST IS VITAL TO AN OPEN PAYMENTS MARKETPLACEPayment systems must be OPEN and SECURE.

Tomorrow’s Enhancements

1. Enhanced interoperability (payment “apps” leveraging multiple payment networks).

2. Digitization of identities and trust.

3. Invisible payments (touch and go).

4. Data access and transparency.

5. Product and business stacks, built via partnerships, not black boxes.

Mer

chan

t Sta

ck

[Vendor] Payment terminals

all of which is ideally sold in a single, simple, bundled service for small

merchants

[Vendor] Terminal maintenance

ACI Processing software

[Vendor] Data center infrastructure

[Vendor] Comms infrastructure

ACI Gateway services

ACI Fraud management

[Vendor] Call center systems

[Vendor] Web portal development & workflow tools

[Vendor] Loyalty services

[Vendor] Accounting / ERP

[Vendor] CRM

Con

sum

er P

aym

ent S

tack

[Vendor] Card OEM

all of which is ideally sold in a single, simple, bundled service for small

merchants

[Vendor] Key / Encryption services

[Vendor] Tokenization service

[Vendor] Wallet app

ACI Processing software

[Vendor] Data center infrastructure

[Vendor] Comms infrastructure

ACI Authentication services

ACI Fraud management

[Vendor] Call center systems

[Vendor] Web portal development and workflow tools

[Vendor] Loyalty services

[Vendor] Accounting / ERP

[Vendor] CRM

Exa

mpl

es o

f Pro

duct

/ B

usin

ess

Sta

cks

13Confidential

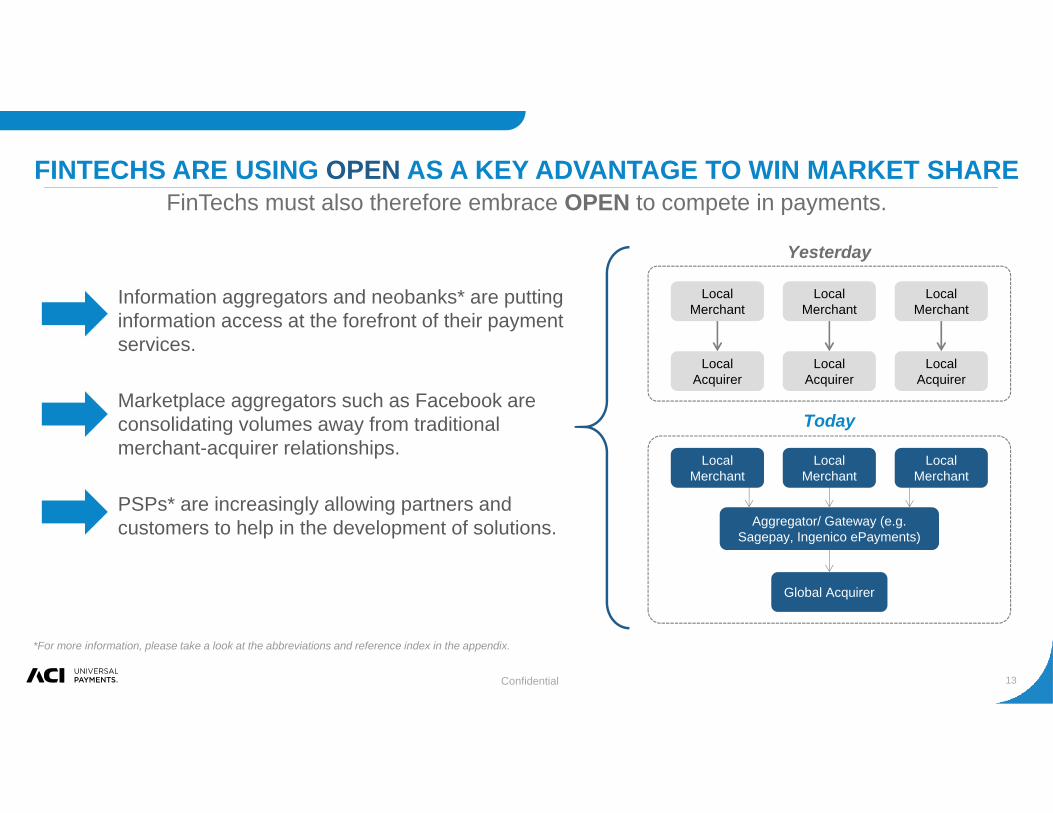

FINTECHS ARE USING OPEN AS A KEY ADVANTAGE TO WIN MARKET SHAREFinTechs must also therefore embrace OPEN to compete in payments.

Information aggregators and neobanks* are putting information access at the forefront of their payment services.

Marketplace aggregators such as Facebook are consolidating volumes away from traditional merchant-acquirer relationships.

PSPs* are increasingly allowing partners and customers to help in the development of solutions.

*For more information, please take a look at the abbreviations and reference index in the appendix.

Yesterday

Today

Local Merchant

Local Acquirer

Local Merchant

Local Acquirer

Local Merchant

Local Acquirer

Aggregator/ Gateway (e.g. Sagepay, Ingenico ePayments)

Global Acquirer

Local Merchant

Local Merchant

Local Merchant

14Confidential

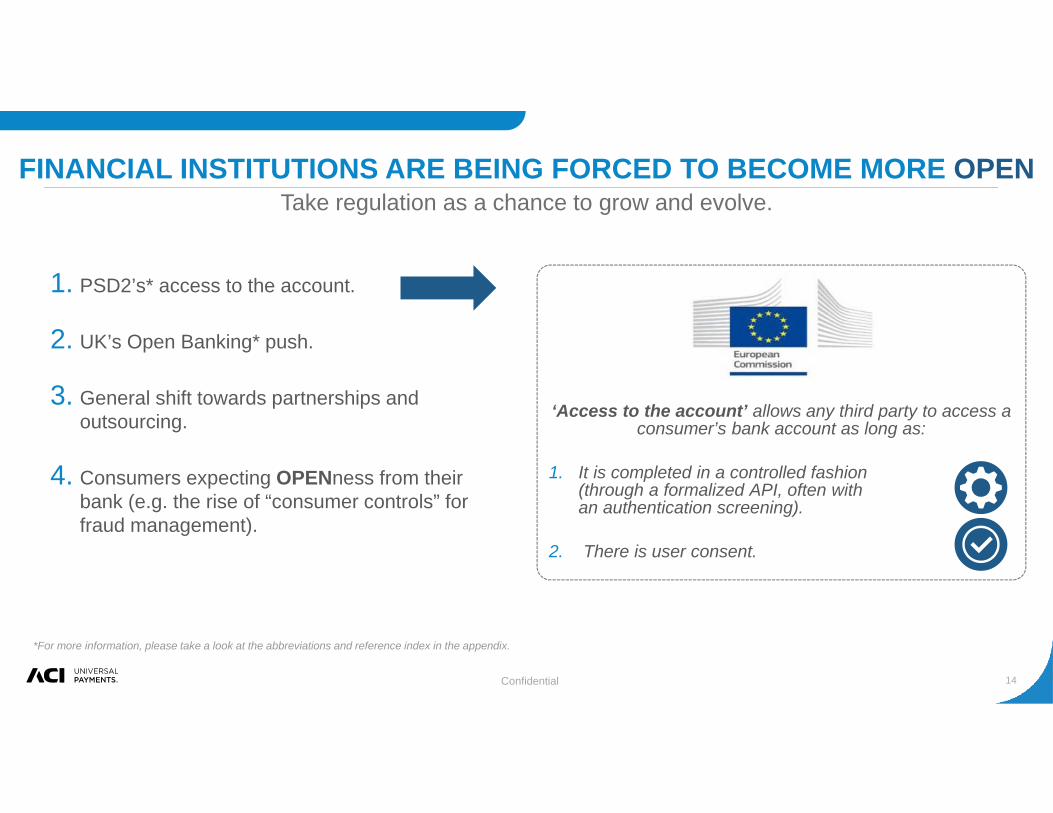

‘Access to the account’ allows any third party to access a consumer’s bank account as long as:

1. It is completed in a controlled fashion (through a formalized API, often with an authentication screening).

2. There is user consent.

FINANCIAL INSTITUTIONS ARE BEING FORCED TO BECOME MORE OPENTake regulation as a chance to grow and evolve.

1. PSD2’s* access to the account.

2. UK’s Open Banking* push.

3. General shift towards partnerships and outsourcing.

4. Consumers expecting OPENness from their bank (e.g. the rise of “consumer controls” for fraud management).

*For more information, please take a look at the abbreviations and reference index in the appendix.

15Confidential

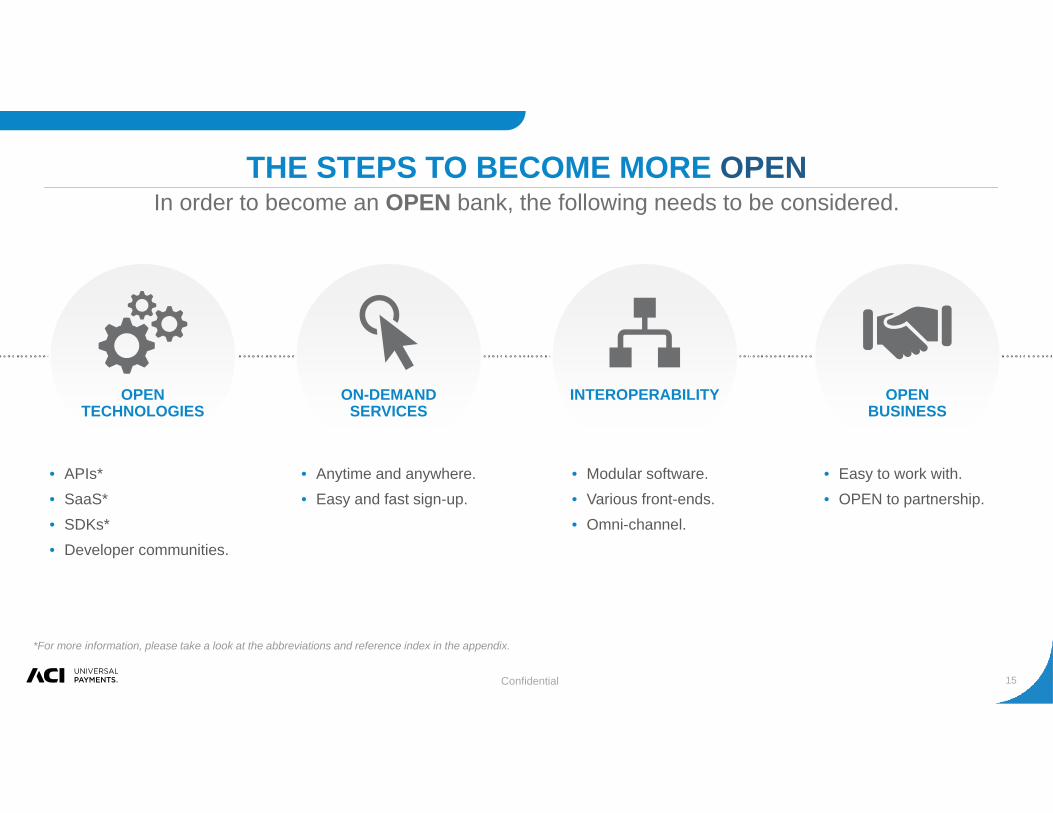

THE STEPS TO BECOME MORE OPEN In order to become an OPEN bank, the following needs to be considered.

• APIs*• SaaS*• SDKs*• Developer communities.

OPEN TECHNOLOGIES

ON-DEMANDSERVICES

INTEROPERABILITY OPENBUSINESS

• Anytime and anywhere.• Easy and fast sign-up.

• Modular software.• Various front-ends.• Omni-channel.

• Easy to work with.• OPEN to partnership.

*For more information, please take a look at the abbreviations and reference index in the appendix.

16Confidential

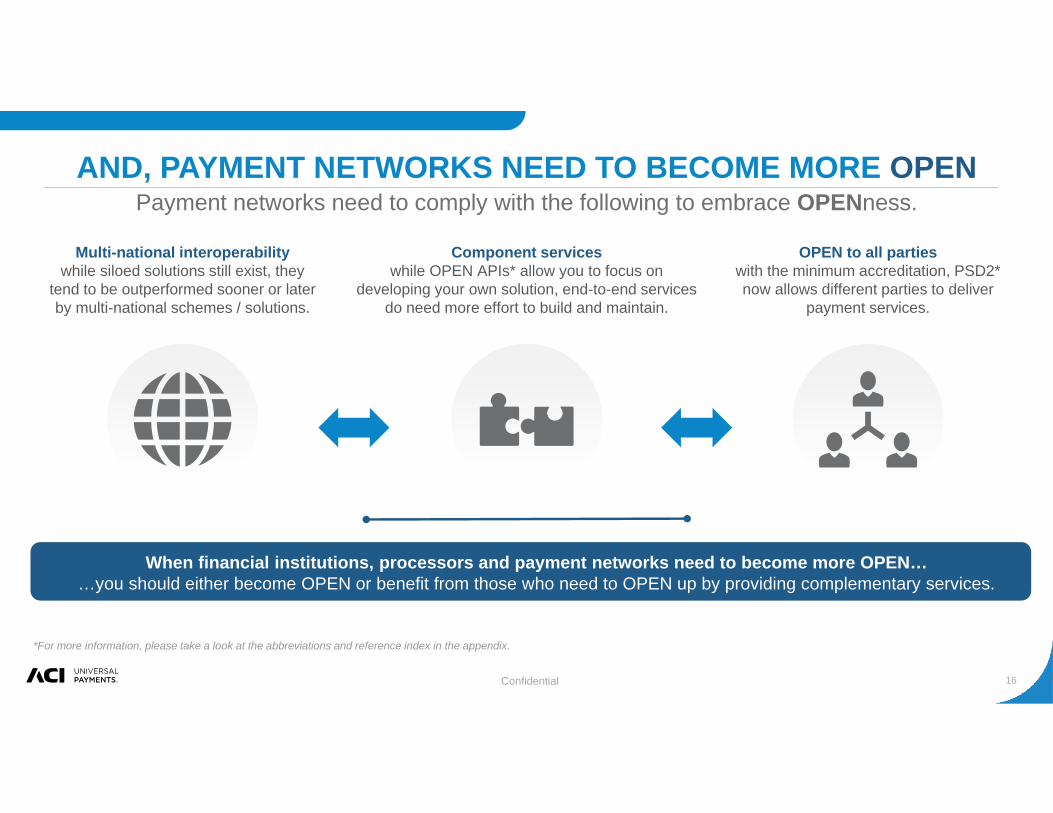

AND, PAYMENT NETWORKS NEED TO BECOME MORE OPENPayment networks need to comply with the following to embrace OPENness.

*For more information, please take a look at the abbreviations and reference index in the appendix.

Multi-national interoperabilitywhile siloed solutions still exist, they

tend to be outperformed sooner or later by multi-national schemes / solutions.

Component services while OPEN APIs* allow you to focus on

developing your own solution, end-to-end services do need more effort to build and maintain.

OPEN to all parties with the minimum accreditation, PSD2* now allows different parties to deliver

payment services.

When financial institutions, processors and payment networks need to become more OPEN……you should either become OPEN or benefit from those who need to OPEN up by providing complementary services.

17Confidential

PSD2 WILL DRIVE A MORE OPEN MARKETPLACEWhich will drive new product development and business models.

*For more information, please take a look at the abbreviations and reference index in the appendix.

Various parties will become TPPs*

With PSD2*, merchants, FinTechs, banks,

processors and others can deliver payment services.

TPPs* will develop new payment services on the back of bank payment infrastructure

As PSD2 allows a broader set of players to serve financial products, banks will be more of

a narrow service provider with OPEN interfaces for other companies.

TPPs* will develop new information services to better

drive digital economyAs TPPs* usually move faster than FIs* and are closer to the market,

they are in a better position to release new products faster.

Aggregators will help to streamline an otherwise complex web of APIs

standards and interfacesTechnical integrators provide

standardized interfaces to easily connect to various different services

with one integration.

The ecosystem will need directories and registers to track trusted parties

and relationshipsAs OPENness can not happen at the

cost of security, a label of trust needs to be established.

$

18Confidential

*For more information, please take a look at the abbreviations and reference index in the appendix.

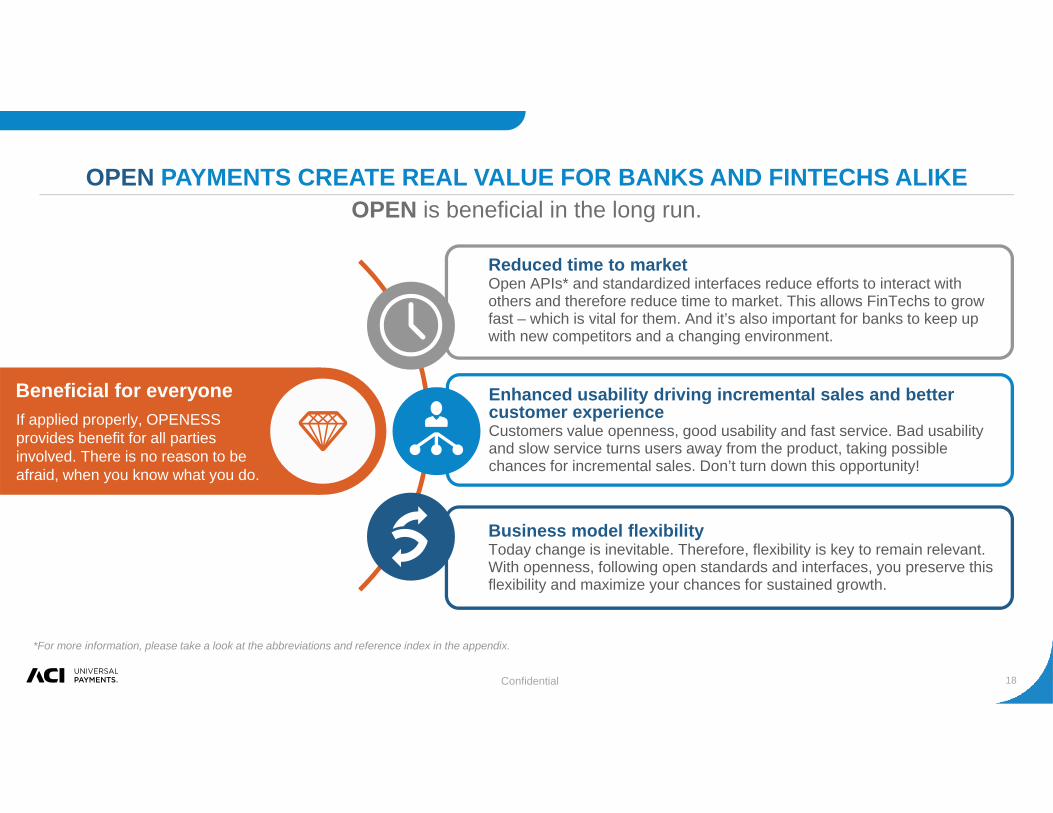

OPEN PAYMENTS CREATE REAL VALUE FOR BANKS AND FINTECHS ALIKEOPEN is beneficial in the long run.

Reduced time to marketOpen APIs* and standardized interfaces reduce efforts to interact with others and therefore reduce time to market. This allows FinTechs to grow fast – which is vital for them. And it’s also important for banks to keep up with new competitors and a changing environment.

Enhanced usability driving incremental sales and better customer experienceCustomers value openness, good usability and fast service. Bad usability and slow service turns users away from the product, taking possible chances for incremental sales. Don’t turn down this opportunity!

Business model flexibilityToday change is inevitable. Therefore, flexibility is key to remain relevant. With openness, following open standards and interfaces, you preserve this flexibility and maximize your chances for sustained growth.

Beneficial for everyoneIf applied properly, OPENESS provides benefit for all parties involved. There is no reason to be afraid, when you know what you do.

19Confidential

APPENDIX

20Confidential

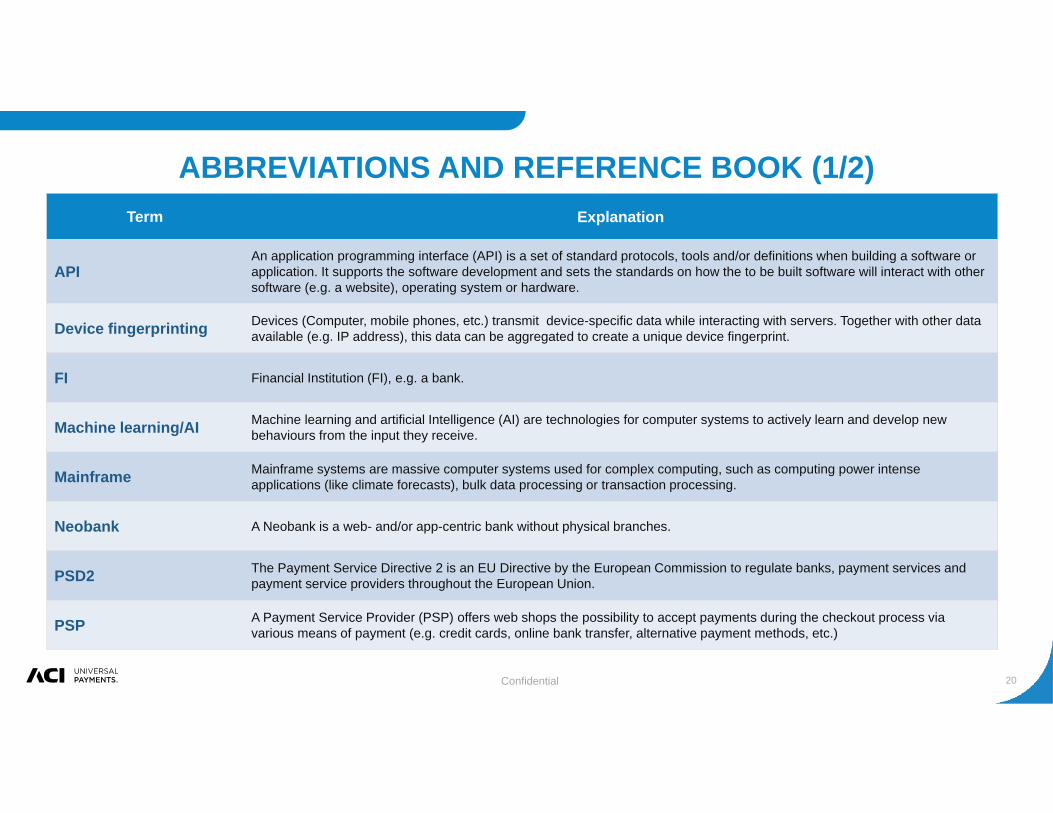

ABBREVIATIONS AND REFERENCE BOOK (1/2)Term Explanation

APIAn application programming interface (API) is a set of standard protocols, tools and/or definitions when building a software or application. It supports the software development and sets the standards on how the to be built software will interact with other software (e.g. a website), operating system or hardware.

Device fingerprinting Devices (Computer, mobile phones, etc.) transmit device-specific data while interacting with servers. Together with other data available (e.g. IP address), this data can be aggregated to create a unique device fingerprint.

FI Financial Institution (FI), e.g. a bank.

Machine learning/AI Machine learning and artificial Intelligence (AI) are technologies for computer systems to actively learn and develop new behaviours from the input they receive.

Mainframe Mainframe systems are massive computer systems used for complex computing, such as computing power intense applications (like climate forecasts), bulk data processing or transaction processing.

Neobank A Neobank is a web- and/or app-centric bank without physical branches.

PSD2 The Payment Service Directive 2 is an EU Directive by the European Commission to regulate banks, payment services and payment service providers throughout the European Union.

PSP A Payment Service Provider (PSP) offers web shops the possibility to accept payments during the checkout process via various means of payment (e.g. credit cards, online bank transfer, alternative payment methods, etc.)

21Confidential

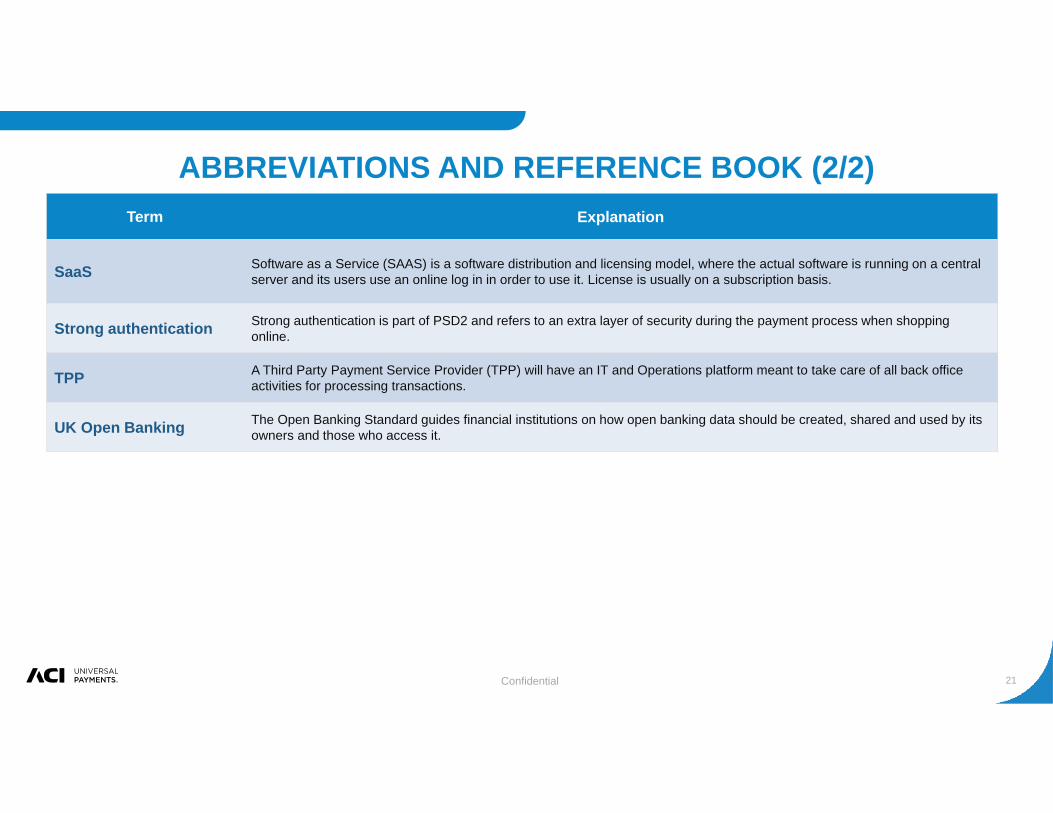

ABBREVIATIONS AND REFERENCE BOOK (2/2)Term Explanation

SaaS Software as a Service (SAAS) is a software distribution and licensing model, where the actual software is running on a central server and its users use an online log in in order to use it. License is usually on a subscription basis.

Strong authentication Strong authentication is part of PSD2 and refers to an extra layer of security during the payment process when shopping online.

TPP A Third Party Payment Service Provider (TPP) will have an IT and Operations platform meant to take care of all back office activities for processing transactions.

UK Open Banking The Open Banking Standard guides financial institutions on how open banking data should be created, shared and used by its owners and those who access it.

22ConfidentialConfidential

The last millennium experienced steady incremental innovation in payments with card the principal disruptive element. Today, regulators and consumers are

demanding FAST, OPEN and SECURE payments causing the pace of innovation to accelerate and payment models to become fragmented.

Welcome to a new era of DISRUPTION in payments!

www.aciworldwide.comAmericas +1 402 390 7600Asia Pacific +65 6334 4843Europe, Middle East, Africa +44 (0) 1923 816393

© Copyright ACI Worldwide, Inc. 2016ACI, ACI Worldwide, ACI Payment Systems, the ACI logo, ACI Universal Payments, UP, the UP logo, ReD and all ACI product names are trademarks or registered trademarks of ACI Worldwide, Inc., or one of its subsidiaries, in the United States, othercountries or both. Other parties’ trademarks referenced are the property of their respective owners.

![2013 Open Payments Cycle Teaching Hospital List [May 2013]](https://img.dokumen.tips/doc/110x75/577cc1761a28aba7119326ba/2013-open-payments-cycle-teaching-hospital-list-may-2013.jpg)