Embed Size (px)

Citation preview

The Mosaic Company February 2014

Click to edit Master title style

2

This presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements include, but are not limited to, statements about the proposed acquisition and assumption of certain related liabilities of the Florida phosphate assets of CF Industries, Inc. (“CF”) and the ammonia supply agreements with CF; the benefits of the transactions with CF; future strategic plans and certain related liabilities and other statements about future financial and operating results. Such statements are based upon the current beliefs and expectations of The Mosaic Company's management and are subject to significant risks and uncertainties. These risks and uncertainties include but are not limited to risks and uncertainties arising from the possibility that the closing of the proposed phosphate assets acquisition may be delayed or may not occur, including delays arising from any inability to obtain governmental approvals of the transaction on the proposed terms and schedule and the ability to satisfy other closing conditions; difficulties with realization of the benefits of the transactions with CF, including the risks that the acquired assets may not be integrated successfully or that the cost or capital savings from the transactions may not be fully realized or may take longer to realize than expected, regulatory agencies might not take, or might delay, actions with respect to permitting or regulatory enforcement matters that are necessary for Mosaic to fully realize the benefits of the transactions including replacement of CF’s escrowed financial assurance funds, or the price of natural gas or ammonia changes to a level at which the natural gas based pricing under one of the long term ammonia supply agreements with CF becomes disadvantageous to Mosaic; customer defaults; the effects of our decisions to exit business operations or locations; the predictability and volatility of, and customer expectations about, agriculture, fertilizer, raw material, energy and transportation markets that are subject to competitive and other pressures and economic and credit market conditions; the level of inventories in the distribution channels for crop nutrients; changes in foreign currency and exchange rates; international trade risks; changes in government policy; changes in environmental and other governmental regulation, including greenhouse gas regulation, implementation of numeric water quality standards for the discharge of nutrients into Florida waterways or possible efforts to reduce the flow of excess nutrients into the Mississippi River basin or the Gulf of Mexico; further developments in judicial or administrative proceedings, or complaints that Mosaic's operations are adversely impacting nearby farms, business operations or properties; difficulties or delays in receiving, increased costs of or challenges to necessary governmental permits or approvals or increased financial assurance requirements; resolution of global tax audit activity; the effectiveness of the Company's processes for managing its strategic priorities; the ability of the Northern Promise joint venture among Mosaic, Ma'aden and SABIC to obtain project financing in acceptable amounts and upon acceptable terms, the future success of current plans for the joint venture and any future changes in those plans; adverse weather conditions affecting operations in Central Florida or the Mississippi River basin or the Gulf Coast of the United States, and including potential hurricanes, excess rainfall or drought; actual costs of various items differing from management's current estimates, including, among others, asset retirement, environmental remediation, reclamation or other environmental regulation, Canadian resources taxes and royalties, or the liabilities Mosaic is assuming in the proposed phosphate assets acquisition; brine inflows at Mosaic's Esterhazy, Saskatchewan, potash mine or other potash shaft mines; other accidents and disruptions involving Mosaic's operations, including potential mine fires, floods, explosions, seismic events or releases of hazardous or volatile chemicals, as well as other risks and uncertainties reported from time to time in The Mosaic Company's reports filed with the Securities and Exchange Commission. Actual results may differ from those set forth in the forward-looking statements.

Safe Harbor

Near-term Potash Market Outlook

54

30

35

40

45

50

55

60

Global MOP Shipments

2013 Incremental 2014F

+(3-5)

India:

2013 2014F

3.2 4.0 - 4.5

China: 11.0 11.6 - 12.0

Brazil: 8.2 8.5 - 8.8

Total: 54 57 - 59

…..

In m

illion

s to

nnes

Expecting record global potash shipments in 2014.

Expect price improvement in H2 2014 Source: Mosaic

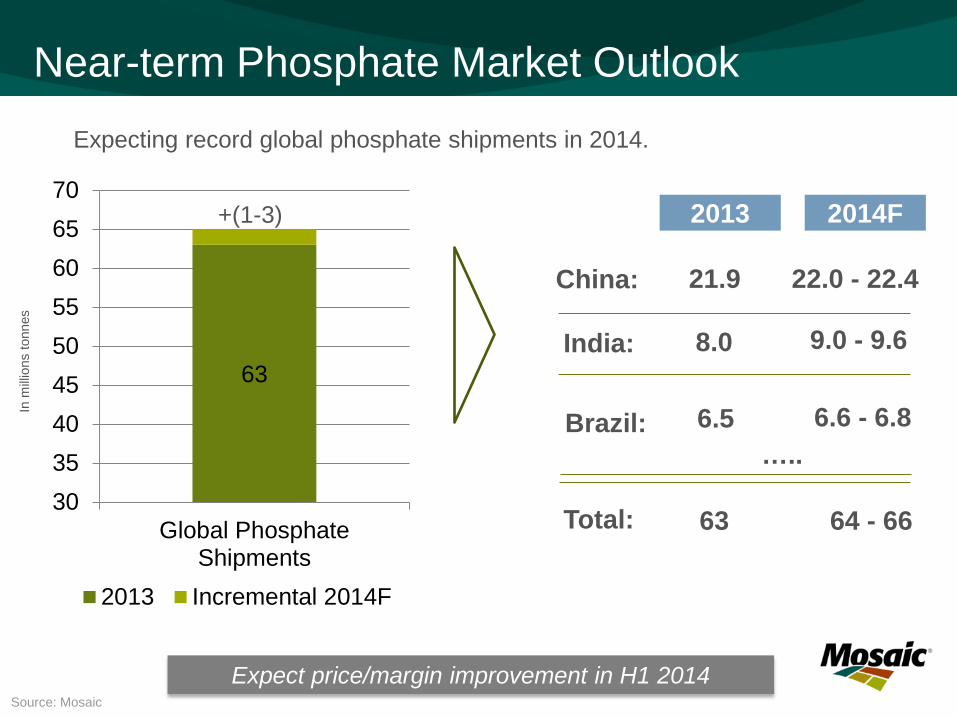

Near-term Phosphate Market Outlook

63

303540455055606570

Global PhosphateShipments

2013 Incremental 2014F

+(1-3)

In m

illion

s to

nnes

Expecting record global phosphate shipments in 2014.

Expect price/margin improvement in H1 2014

India:

2013 2014F

8.0 9.0 - 9.6

Brazil: 6.5 6.6 - 6.8

Total: 63 64 - 66

…..

China: 21.9 22.0 - 22.4

Source: Mosaic

Click to edit Master title style

5

Key Environmental Factors

Agricultural commodity pricing:

South American crop progress

Energy, bio-fuels and livestock prices

U.S. Prospective Plantings Report – 3/31/14

India P&K subsidy for 2014/15

Producer and channel inventories

Macro economic developments

5

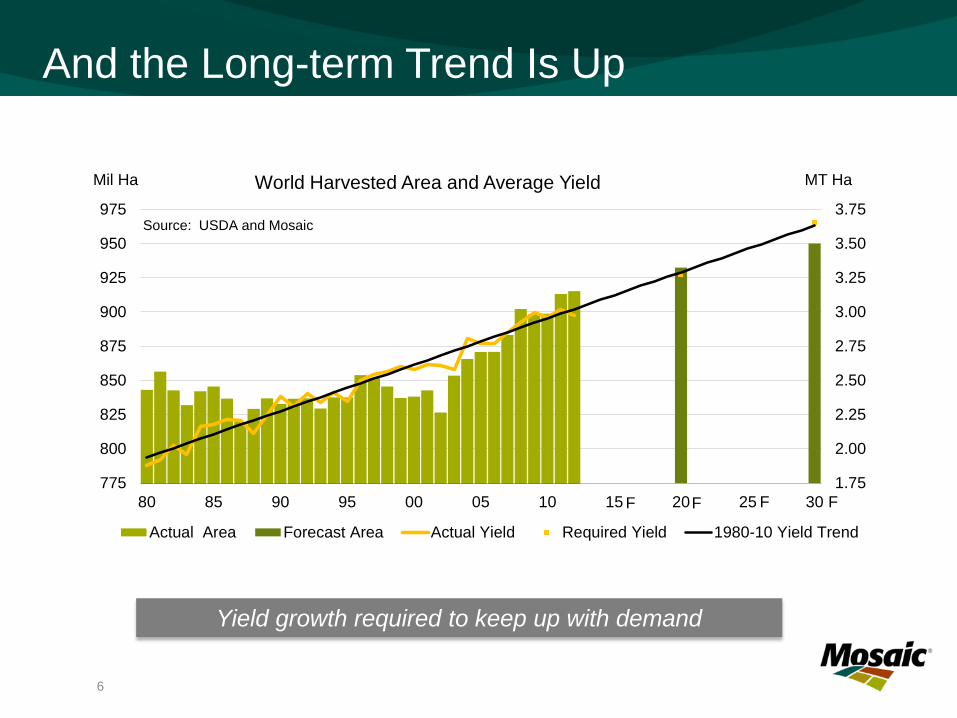

And the Long-term Trend Is Up

Yield growth required to keep up with demand

1.75

2.00

2.25

2.50

2.75

3.00

3.25

3.50

3.75

775

800

825

850

875

900

925

950

975

80 85 90 95 00 05 10 15 20 25 30

MT Ha Mil Ha

Source: USDA and Mosaic

World Harvested Area and Average Yield

Actual Area Forecast Area Actual Yield Required Yield 1980-10 Yield Trend

6

F F F F

What Differentiates Mosaic?

The Largest Potash and Phosphates Company

0.0 1.0 2.0 3.0 4.0 5.0 6.0 7.0 8.0

Mosaic

PotashCorp

Uralkali

Belaruskali

OCP

Israel Chemical

K+S

Yuntianhua

PhosAgro

Agrium

Mosaic's K2O production excludes Esterhazy tolling production Source: Mosaic, Fertecon

World's Largest P + K Companies

K2O P2O5

We help the world grow the food it needs.

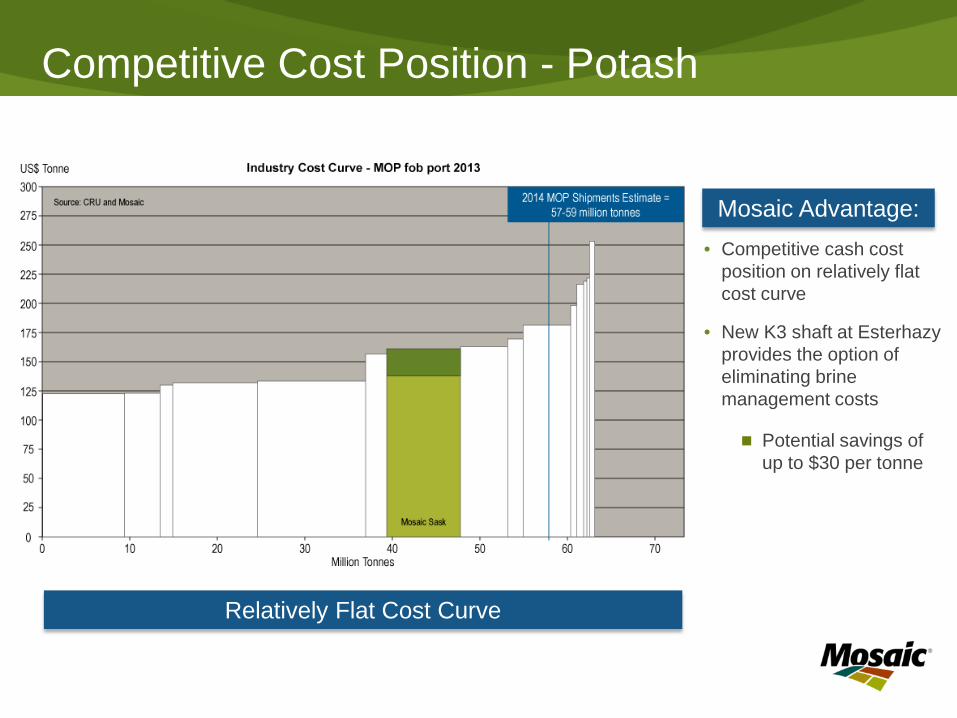

Competitive Cost Position - Potash

• Competitive cash cost position on relatively flat cost curve

• New K3 shaft at Esterhazy provides the option of eliminating brine management costs

Mosaic Advantage:

Relatively Flat Cost Curve

Potential savings of up to $30 per tonne

Strong Cost Position - Phosphates

• Vertically integrated with phosphate rock sources from Florida and Miski Mayo JV.

• Saudi Arabian JV is expected to be low cost with advantaged access to India

• CF phosphates business acquisition provides access to more phosphate rock and ability to realize significant synergies

• Long term ammonia supply agreement based on U.S. natural gas prices

Best Quartile Producer

Mosaic Advantage:

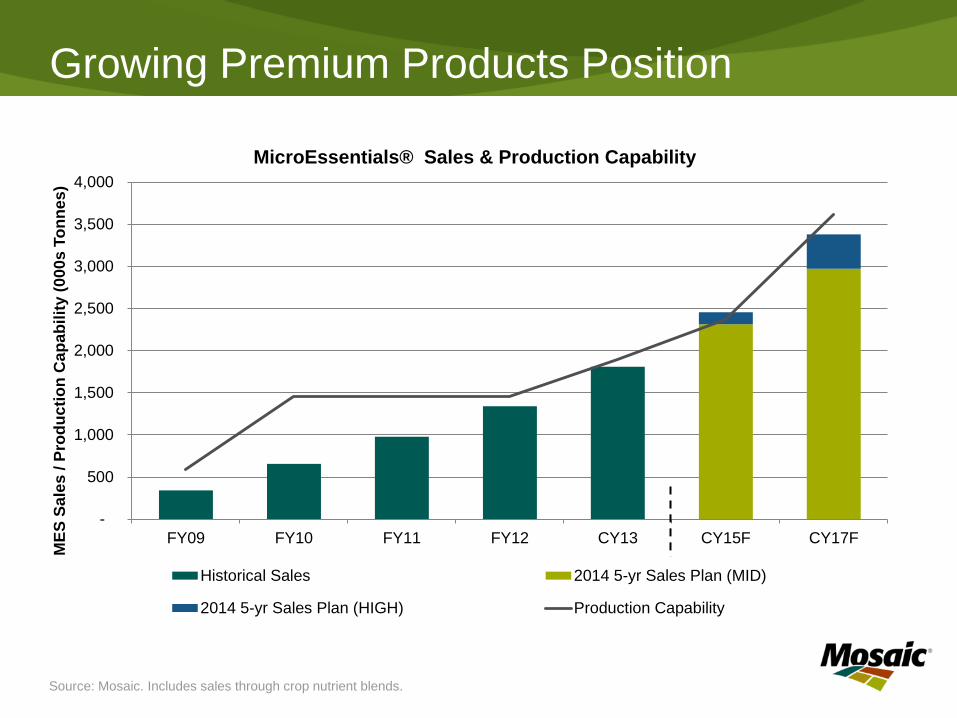

Growing Premium Products Position

Source: Mosaic. Includes sales through crop nutrient blends.

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

FY09 FY10 FY11 FY12 CY13 CY15F CY17F

MES

Sal

es /

Prod

uctio

n C

apab

ility

(000

s To

nnes

)

MicroEssentials® Sales & Production Capability

Historical Sales 2014 5-yr Sales Plan (MID)

2014 5-yr Sales Plan (HIGH) Production Capability

Diversified Customer Base

We ship product to approximately 40 countries with balanced exposure to North America and International

63%

37% 44%

56%

Calendar 2013

Sales by Product and Geography

Phosphates Potash

North America

International

Calendar 2013

Mosaic Product Shipments by Destination

Source: Fertecon & Mosaic

North America 51%

Latin America 15%

Asia 31%

Others 3%

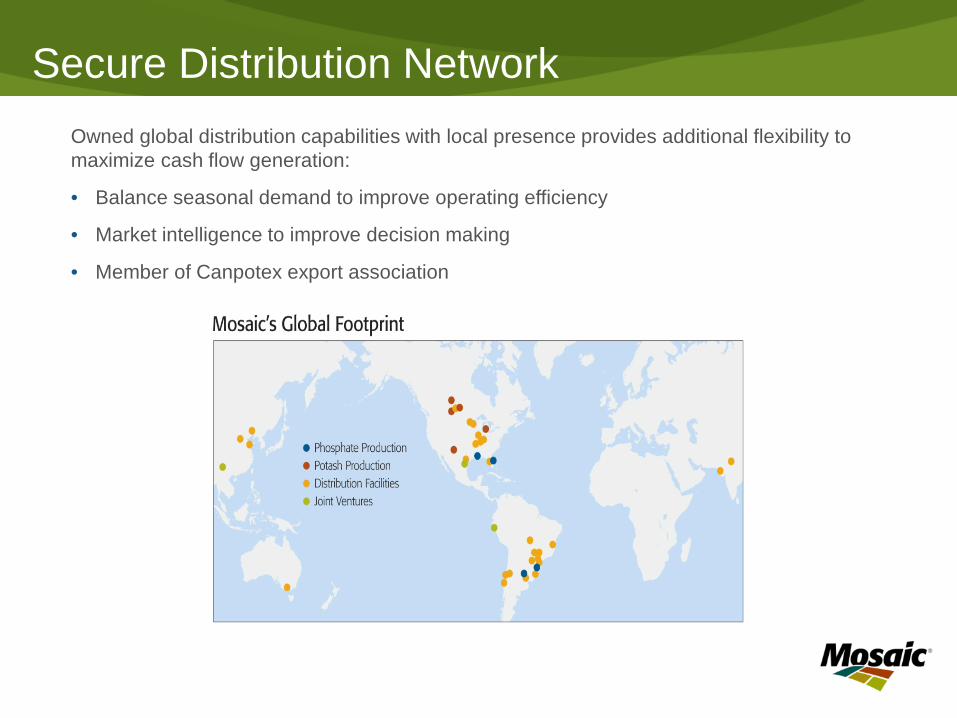

Secure Distribution Network Owned global distribution capabilities with local presence provides additional flexibility to maximize cash flow generation:

• Balance seasonal demand to improve operating efficiency

• Market intelligence to improve decision making

• Member of Canpotex export association

Mosaic’s Strategic and Cash Use Priorities

Our Strategic Priorities

+ =

Unchanged Cash Use Priorities

Maintain ratings & financial strength

Sustain assets & recurring dividend

Investments to drive organic growth

Opportunistic strategic investments

Return excess to shareholders

Cyclical Nature Provides Excellent Opportunities…

Buy CF Industries Phosphates

Business 300

400

500

600

700

11 12 13 14

$ MT Weekly DAP Prices

fob Tampa

Source: Fertecon

…Including Returning Capital to Shareholders

*Average repurchased to-date.; actual repurchase costs varies with market prices. Actual 2014 dividend payout may vary with outstanding share count.

$0

$500

$1,000

$1,500

$2,000

$2,500

2012 2013 2014F*Class A Share Repurchases Dividends

+ $1B Open Market

Authorization

$55 / Share

$46 / Share

Click to edit Master title style

19

Largest combined phosphate and potash producer in the world High quality assets in stable geographies

Geographically diversified – customers in approximately 40 countries

Strong balance sheet leaves us well positioned to capitalize on cyclical opportunities and strong secular trends

Optimizing asset portfolio for long-term value creation

Target optimal balance sheet by mid-2014 $1 billion share repurchase authorization

Experienced management team focused on execution and operational excellence

Investment Highlights

Market Outlook

The Food Story Is Unfolding

21

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

0

20

40

60

80

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

Percent Million Tonnes U.S. Corn Exports

Total US Exports % of Total to China

Source: USDA Calendar Year Basis

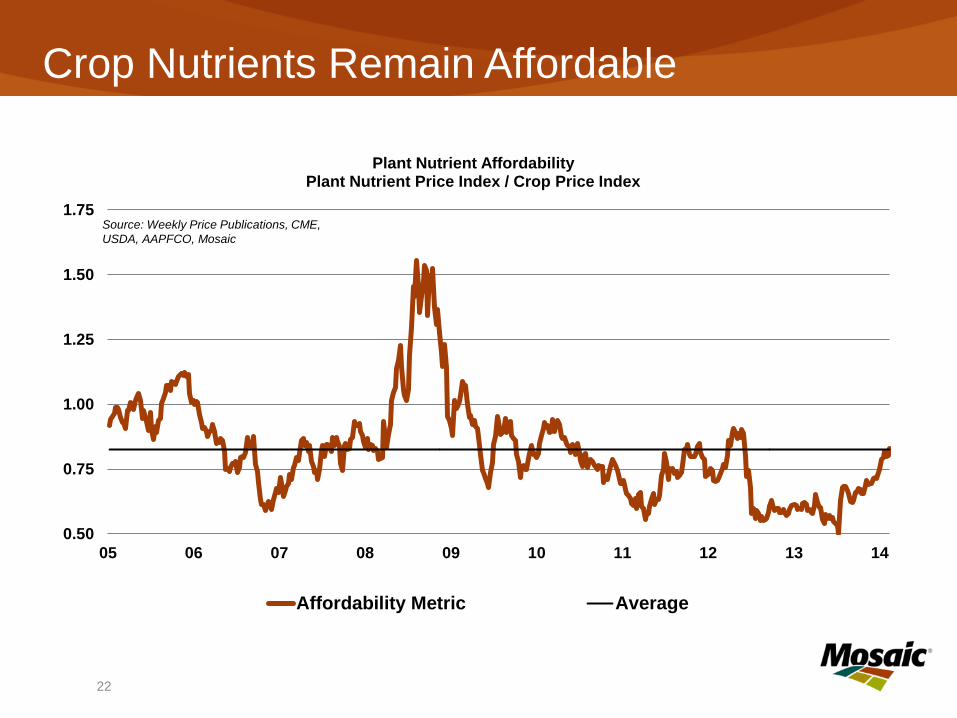

Crop Nutrients Remain Affordable

22

0.50

0.75

1.00

1.25

1.50

1.75

05 06 07 08 09 10 11 12 13 14

Plant Nutrient Affordability Plant Nutrient Price Index / Crop Price Index

Affordability Metric Average

Source: Weekly Price Publications, CME, USDA, AAPFCO, Mosaic

23

Global Phosphate Shipments by Region Million Tonnes DAP/MAP/TSP 2012 2013E

2014F Low*

2014F High* Commentary

China 21.2 21.9 22.0 22.4 Moderate growth - high analysis products capture phosphate growth and displace low analysis products.

India 10.0 8.0 9.0 9.6 Strong rebound expected due to an increase in farm use and a smaller drawdown of channel inventories this year.

Other Asia/Oceania 6.7 6.6 6.6 6.8 Demand is expected to hold steady or increase modestly in most countries.

Europe and FSU 4.4 4.4 4.4 4.6 Demand is expected to hold steady or increase modestly in most countries.

Brazil 5.7 6.5 6.6 6.8 Further moderate increase is forecasts following a step-up in shipments in 2013. Assumes no collapse of crop prices.

Other Latin America 2.8 2.9 2.9 3.0 Demand is expected to hold steady or increase modestly in most countries.

North America 8.8 9.1 8.7 8.9 Assumes U.S. corn acreage of 90-92 million in 2014 and steady application rates.

Other 3.6 3.8 3.9 4.1 Demand is expected to hold steady or increase modestly in most countries.

Total 63.2 63.1 64.1 66.1 Point estimate is in the top half of the range.

Source: Fertecon and Mosaic * Figures may not sum to total due to rounding

24

Global Potash Shipments by Region

Million Tonnes Muriate of Potash (KCl)

CY 2012

CY 2013E

2014F Low*

2014F High* Commentary

China 10.3 11.0 11.6 12.0 Net imports projected to increase from 5.9 million tonnes in 2013 to 6.4 million in 2014. Domestic production also expected to increase another 300,000 tonnes this year.

India 3.2 3.2 4.0 4.5 Significant rebound due to lower prices, decent on farm demand and leaner channel inventories. Import economics work even with a modest subsidy cut.

Indonesia/Malaysia 4.2 4.3 4.5 4.6 Moderate growth underpinned by decent, if not spectacular, palm oil prices and production economics.

Other Asia/Oceania 4.1 4.3 4.5 4.7 Incremental growth with downside risk in countries such as Thailand due to political/economic uncertainty.

Europe and FSU 10.3 10.5 11.3 11.7 Robust growth due to increases in NPK production for both export and domestic markets as well as improved on-farm direct application use especially in the FSU and Eastern Europe.

Brazil 7.9 8.2 8.5 8.8 Shipments remain strong, though weather concerns and deteriorating crop production economics pose risks to the forecast.

Other Latin America 1.6 1.8 1.9 1.9 Moderate incremental growth expected.

North America 8.1 9.0 8.9 9.2 Assumes U.S. corn acreage of 90-92 million in 2014 and steady to slightly higher application rates. Expecting strong spring sales.

Other 1.3 1.5 1.7 1.8 Moderate incremental growth expected.

Total 51.0 53.9 56.8 59.1 Our point estimate is in the lower half of the range.

Source: Fertecon and Mosaic * Figures may not sum to total due to rounding

Stable Long-term Supply and Demand Outlook

40%

50%

60%

70%

80%

90%

100%

0

10

20

30

40

50

60

70

80

90

2000 2004 2008 2012 2016 2020

Op RateMMT KClGlobal Potash Capacity, Production and Operating Rate

Most Likely Scenario

Capacity Production Op Rate

Potash Production, Capacity and Operating Rate Forecast

Operating rate

Mill

ion

tonn

es p

rodu

ct K

Cl

Capacity Production Operating Rate

Source: Mosaic

25

Positive Long-term Supply and Demand Outlook

65%

70%

75%

80%

85%

90%

95%

0

20

40

60

80

100

120

2000 2004 2008 2012 2016 2020

Op RateMMT Global Phosphate Capacity, Production and Opr RateMost Likely Scenario

Capacity Production Op Rate

P2O

5 operating rate Phosphate Production,

Capacity and Operating Rate Forecast

Mill

ion

tonn

es

Source: Mosaic

26

Recent Financial Results

0%

5%

10%

15%

20%

25%

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Sales Volumes GM Rate

Volume First, Then Price and Margin

Expect price/margin improvement in H1 2014

Phosphates • In December

prices moved up

• Expect 2014 shipments to be 64-66 million tonnes

Source: Mosaic 28

0%

10%

20%

30%

40%

50%

60%

-

500

1,000

1,500

2,000

2,500

3,000

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Sales Volumes GM Rate

Expect price improvement in H2 2014

Potash

Volume First, Then Price and Margin

• Expect gap to widen in Q1, upward price momentum second half of 2014

• Expect 2014

shipments to be 57-59 million tonnes

Source: Mosaic 29

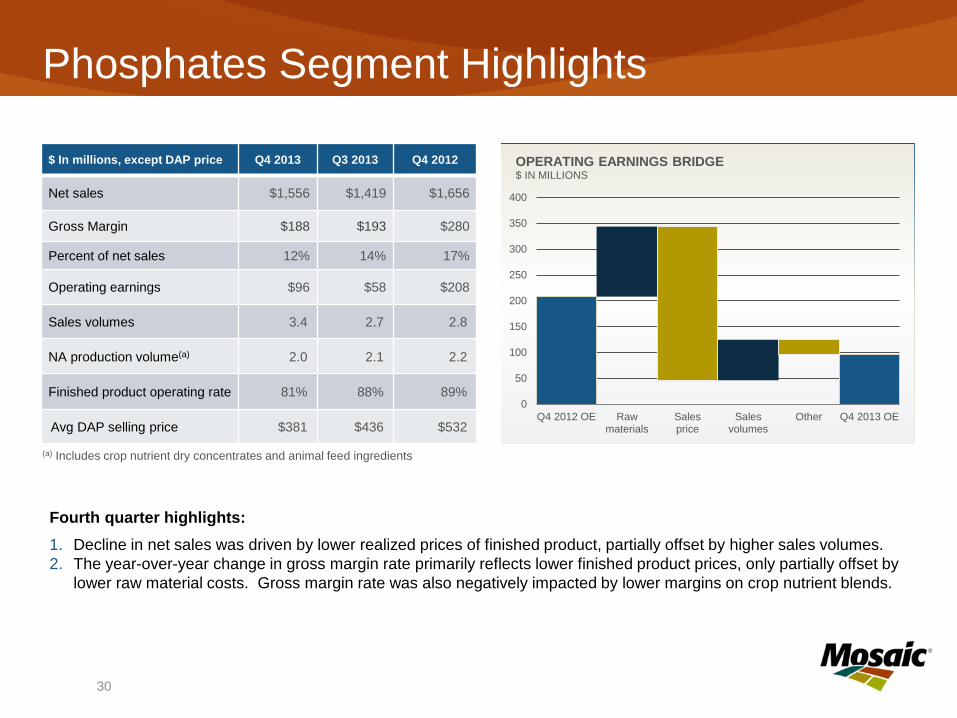

Phosphates Segment Highlights

Fourth quarter highlights: 1. Decline in net sales was driven by lower realized prices of finished product, partially offset by higher sales volumes. 2. The year-over-year change in gross margin rate primarily reflects lower finished product prices, only partially offset by

lower raw material costs. Gross margin rate was also negatively impacted by lower margins on crop nutrient blends.

$ In millions, except DAP price Q4 2013 Q3 2013 Q4 2012

Net sales $1,556 $1,419 $1,656

Gross Margin $188 $193 $280

Percent of net sales 12% 14% 17%

Operating earnings $96 $58 $208

Sales volumes 3.4 2.7 2.8

NA production volume(a) 2.0 2.1 2.2

Finished product operating rate 81% 88% 89%

Avg DAP selling price $381 $436 $532

(a) Includes crop nutrient dry concentrates and animal feed ingredients

0

50

100

150

200

250

300

350

400

Q4 2012 OE Rawmaterials

Salesprice

Salesvolumes

Other Q4 2013 OE

OPERATING EARNINGS BRIDGE $ IN MILLIONS

30

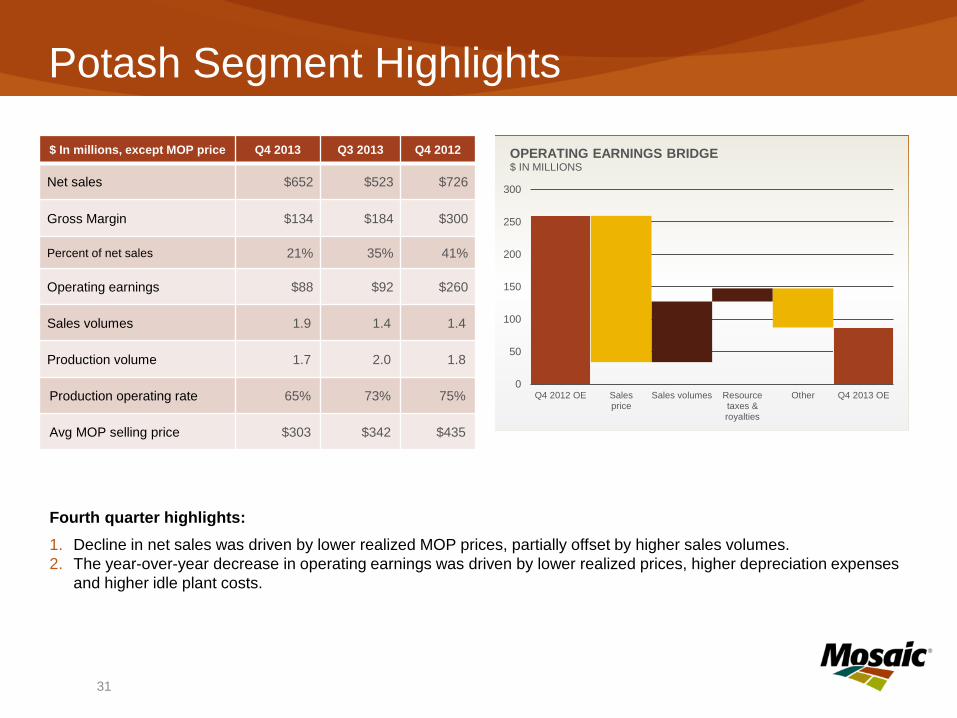

Potash Segment Highlights

Fourth quarter highlights: 1. Decline in net sales was driven by lower realized MOP prices, partially offset by higher sales volumes. 2. The year-over-year decrease in operating earnings was driven by lower realized prices, higher depreciation expenses

and higher idle plant costs.

$ In millions, except MOP price Q4 2013 Q3 2013 Q4 2012

Net sales $652 $523 $726

Gross Margin $134 $184 $300

Percent of net sales 21% 35% 41%

Operating earnings $88 $92 $260

Sales volumes 1.9 1.4 1.4

Production volume 1.7 2.0 1.8

Production operating rate 65% 73% 75%

Avg MOP selling price $303 $342 $435

0

50

100

150

200

250

300

Q4 2012 OE Salesprice

Sales volumes Resourcetaxes &royalties

Other Q4 2013 OE

OPERATING EARNINGS BRIDGE $ IN MILLIONS

31

Phosphate Raw Material Trends

32

$-

$50

$100

$150

$200

$250

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Q12014F

Realized in Cost of Goods Sold Market Prices

$-

$100

$200

$300

$400

$500

$600

$700

$800

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Q12014F

Realized Costs Market Prices

Ammonia Sulfur ($/tonne) ($/tonne)

1) Market ammonia prices are average prices based upon Tampa C&F as reported by Fertecon 2) Market sulfur prices are average prices based upon Tampa C&F as reported by Green Markets

2

2 1

Click to edit Master title style

33 33

Financial Guidance Summary

Phosphates Guidance – 2014 Q1 Sales volume 2.3 – 2.6 million tonnes Q1 DAP selling price $390 - $420 per tonne Q1 Gross margin rate in the upper teens Q1 Operating rate in the low 80 percent range

Potash Guidance – 2014 Q1 Sales volume 2.3 – 2.7 million tonnes Q1 MOP selling price $245-$275 per tonne Q1 Gross margin rate around the 30 percent range Q1 Operating rate mid 80 percent range

Canadian Resource Taxes and Royalties - 2014 $120 -$180 million

Brine Management – 2014 Approximately $200 million

Click to edit Master title style

34 34

Financial Guidance Summary

Corporate Guidance – 2014

Total SG&A - 2014 $350 - $400 million

Capital Expenditures - 2014 $1.0 billion to $1.3 billion

Effective Tax Rate - 2014 Mid to high 20 percent range