Embed Size (px)

Citation preview

ME Printer August - Septem

ber 2014

27

ME

Prin

ter A

ugus

t - S

epte

mbe

r 201

4

26

Smithers Pira ReportPackaging

Rising real incomes, continued urbanisation and a relatively young and growing population

make the Middle East and North Africa a target market for the packaging industry. Smithers Pira has published a major new market study – The Future of Packaging in the Middle East & North Africa to 2019 – to provide an up-to-date view of the current market for anyone involved in or looking to enter

this lucrative market.Smithers Pira is the worldwide authority on packaging, paper and print industry supply chains. Established in 1930, Smithers Pira provides strategic and technical consulting, testing, intelligence and events to help clients gain market insights, identify op-portunities, evaluate product performance and manage com-pliance. Smithers Pira works with packaging suppliers to identify profitable growth opportunities.

The FuTure oF Packag-ing in The Middle easT & norTh aFrica To 2019 rePorTSmithers Pira has published the report ‘The Future of Packaging in the Middle East & North Africa to 2019’. The report is based on an in-depth combination of primary and secondary data. Primary research included structured in-depth telephone and follow-up interviews with leading players in the MENA

value chain, including a select group of end users. Secondary research consisted of multiple sources such as financial reports of publicly held companies participating in the industry, websites of key industry suppli-ers, proceedings of packaging conferences, industry publica-tions, various technology forecasts and global economic projections. In addition, the data and insight in the study includes valuable information gleaned from key industry conventions/exhibits related to MENA’s packaging industry.The report by Smithers Pira examines Middle East and North African (MENA) packaging markets for the period 2009-14 and presents forecasts for the five-year period covering 2014-19. Market value forecasts are presented by packaging prod-uct, end-use sector and twelve national markets. In addition, the report includes an analysis of market drivers and trends, indus-try structure and major market participants.

The broad Mena Pack-aging MarkeTThe MENA packaging market is valued at approximately US$41.1 billion in 2014 and is forecast to grow during the

period 2014-19 at a CAGR of 5.0% to US$52.4 billion (2013 prices). This represents a higher growth rate than the global packaging market, which is forecast to grow at just over 4% during the same period. Packaging demand is being driven by higher economic activity and rising real incomes, urbanisation, a relatively young and growing population and the further development of retail infrastructure in several MENA countries. There are significant differ-ences in these factors across the countries of the Middle

East & North Africa considered in this report. Additionally, po-litical instability in the region will have some affects. Since 2011, the Middle East and North Africa has been the centre of revolutionary pro-democracy movements, starting in Tunisia and Egypt, and spreading across the region. The unrest in the region, together with ad-verse economic conditions in global markets, has negatively affected development of the packaging industry in some countries. However, despite the political instability, the regional economy is expected to grow.

Table 0.2 Middle East & North Africa: packaging market value, 2009, 2013, 2014 and 2019 forecast, (US$ million)

The MENA packaging market is valued at approximately US$41.1 billion in 2014 and is forecast to grow during the period 2014-19

2009 2013 2014 (p) CAGR (%) 2009-14 2019 (f) CAGR (%)

2014-19

MiddlE EAST 22,528.10 29,598.00 30,608.20 6.3 38,459.10 4.7

NoRTh AfRiCA 7,506.50 10,168.00 10,468.30 6.9 13,953.10 5.9

MiddlE EAST & NoRTh AfRiCA 30,034.60 39,766.00 41,076.50 6.5 52,412.20 5.0

Note: totals may not add up due to rounding, p=projected, f=forecast, current prices and exchange rates for the period 2009 to 2013, with constant prices to 2019, using 2013 as the base yearsource: smithers Pira

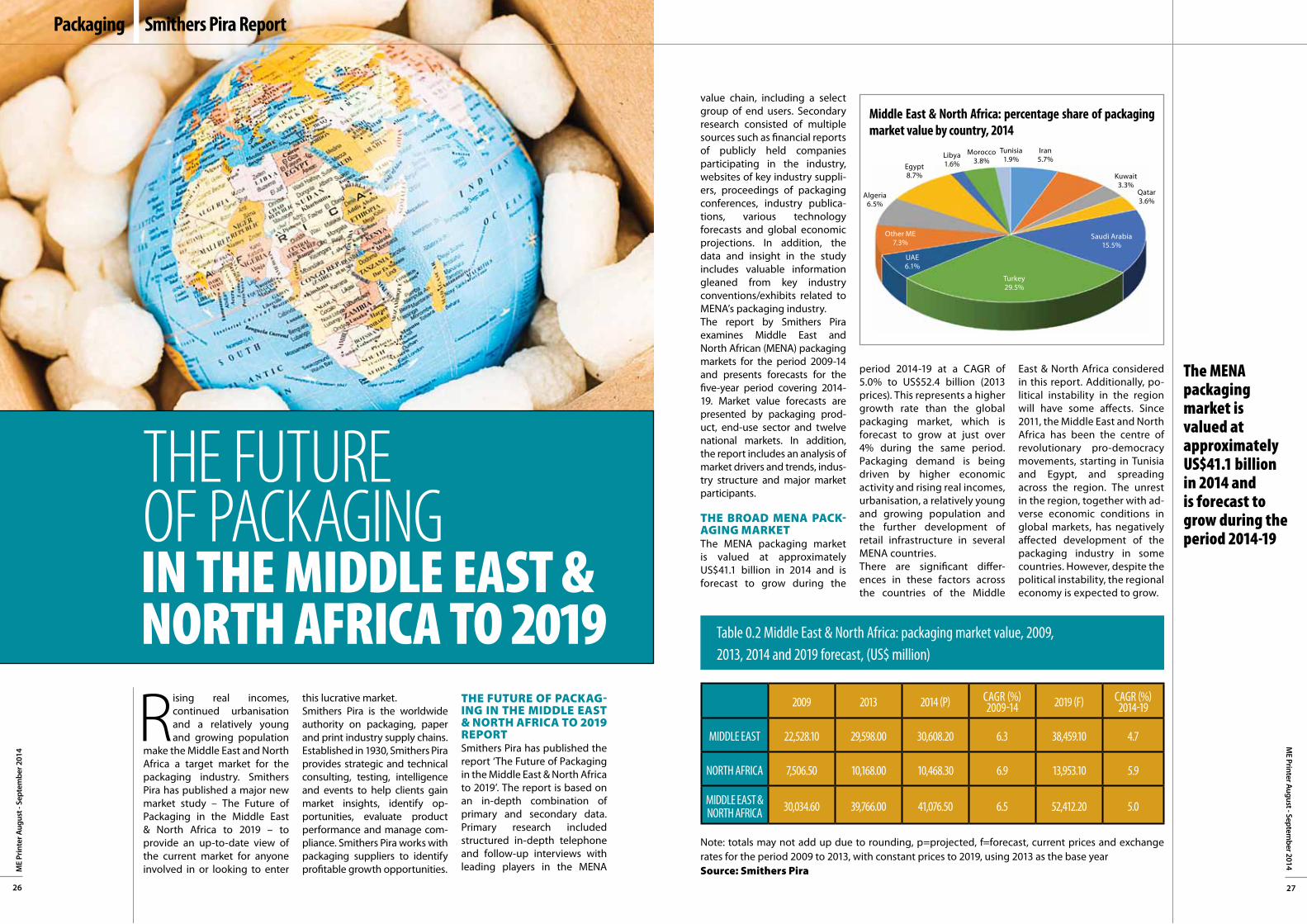

Middle East & North Africa: percentage share of packaging market value by country, 2014

Turkey 29.5%

Iran 5.7%

Tunisia 1.9%

Morocco 3.8%

Libya 1.6%Egypt

8.7%

Algeria 6.5%

Other ME 7.3%

UAE 6.1%

Saudi Arabia 15.5%

Qatar 3.6%

Kuwait 3.3%

iN ThE MiddlE EAST & NorTh AfricA To 2019

The FuTure oF Packaging

ME Printer August - Septem

ber 2014

29

ME

Prin

ter A

ugus

t - S

epte

mbe

r 201

4

28

Middle East & North Africa: packaging consumption by end use sector, percentage share of market value, 2014

key drivers and TrendsThere are various key drivers and trends that are likely to impact the the Middle East & North Africa packaging markets to 2019; these are eco-nomic, demographic, political, packaging and retail. Firstly it is expected that there will be a largely positive impact on packaging demand from rising economic activity and growing incomes per capita, but there are wide variations between countries; in addition, there is a major threat to economic growth from political instabil-ity in the region. In terms of demographics, a high propor-tion of young people and a growing population is a major driver of packaging demand. Politics is expected to likely impact the Middle East & North Africa packaging markets to 2019; struggles for freedom continue across the Middle East and North Africa, but sev-eral countries faced worsening violence as anti-democratic forces asserted themselves. The Middle East and North Africa as a whole have the worst civil lib-erties of any region. Worsening geo-political violence could be major restraint on economic development, and hence packaging demand, during the forecast period. In terms of packaging trends, packag-

ing sales are supported by increased investment in food production and processing, significant investments in new flexible packaging converting capacity and increased avail-ability of locally produced and competitively-priced base sub-strates. Lastly, the retail trend is likely to impact the packaging market in this region to 2019, as packaging demand benefits from the development of a retail infrastructure and grow-ing penetration of pre-packed foods. Hypermarkets/super-markets are gaining market share, though small and local artisan stores still dominate in most MENA countries

a closer look aT The Mena Packaging Mar-keTMiddle Eastern countries ac-count for a projected share of almost three-quarters of total packaging sales in the Middle East & North Africa (MENA) region in 2014. North Africa has however showed a slightly higher growth rate for packag-ing consumption during the 2009-14 review period. Middle Eastern countries grew packag-ing sales during the five-year period to 2014 at a CAGR of 6.3% with North Africa growing at a CAGR of 6.9%. MENA regional packaging market growth was severely restrained during this period by war and civil unrest in several countries including Syria, Iraq, Libya, Tunisia and Egypt.

a closer look aT The Mena Packaging Mar-keT: by counTryTurkey is the largest packaging market in the MENA region ac-counting for a projected 22.1% share of total market value in 2014. Saudi Arabia is second largest packaging market, fol-lowed by Iran and Egypt. Libya is a relatively under-developed packaging market, but is pre-dicted to grow packaging con-sumption at the highest rate, provided that the current civil

unrest in the country does not persist for a prolonged period of time. Qatar, Morocco, Saudi Ara-bia and the UAE are also forecast to grow at a rate faster than the market average. The relatively more developed packaging markets of, Kuwait and Turkey are expected to grow packag-ing sales at rates lower than the regional market average. Iran still faces economic sanctions which are restraining economic growth and packaging market sales. There are however hopes that Western nations will gradu-ally lift some sanctions during 2014 and 2015, which should drive higher packaging sales. ‘Other Middle Eastern’ countries are likely to be restrained by further declines in Iran and Syria packaging consumption as a result of the ongoing civil unrest in these countries.

a closer look aT The Mena Packaging MarkeT: by Packaging ProducTRigid plastics form the largest packaging product group

accounting for a projected market value share of 28.2% for 2014. Board packaging is the second most important category with 25.6% of con-sumption, followed by flexible plastics with a 12.9% share. Rigid plastics and flexible plas-tic packaging have increased their market share during the review period. Rigid plastics and flexible plastics are predicted to grow at the fast-est rates during the forecast period. Plastic packaging is gradually replacing glass bottles, metal cans and paper and board packaging in the MENA and other world region because of its lighter weight, cost saving potential and greater design flexibility.

a closer look aT The Mena Packaging Mar-keT: by end use secTorFood represents the largest end use sector for packaging products accounting for a projected 33.8% market value share in 2014. Industrial/bulk is the second largest sec-

tor with 26.4%, followed by beverage markets with 25.2%. Food and beverage packaging represents a much higher pro-portion of overall packaging demand for the developing countries of the MENA region compared with the world packaging market. Food and beverages in the world pack-aging market account for just over 40.0% of sales, while in MENA region they represent almost 59.0% of packaging sales. Similarly, healthcare packaging sales account for just 2.9% of MENA packaging sales compared with 4.0% for the world packaging market as a whole. The industrial/bulk sector also represents a much lower proportion of MENA packaging sales compared with the world market; 26.4% versus 40.0%. Food and drink packaging sales are predicted to grow their market share fur-ther over the forecast period with industrial/bulk also grow-ing steadily. The healthcare sector is however expected to show the fastest growth.

Overview of key drivers and trends, structure of the market supply chain by region and packaging product.

counTry ProFiles: Iran, Israel, Kuwait, Qatar, Saudi Arabia, Turkey, United Arab Emirates (UAE), Algeria, Egypt, Libya, Morocco, Tunisia

8 end use MarkeTs: Food, Beverages, Healthcare, Medical devices, Prescription and OTC drugs, Cosmetics (incl.

Colourants and shampoos, Perfumes, Deodorants, Soaps, Toothpaste), Other consumer goods (incl. Tobacco, Household, chemicals, soap & detergents, Paper products, Hardware and electrical goods, Glassware and ceramics), Industrial/bulk prod-ucts (incl. Chemicals, oil and oil derivatives, Minerals)

6 Packaging ProducTs: Flexible packaging (incl. Flex-ible plastics, Flexible foil, Flex-ible paper), Board, Metal, Rigid plastic, Glass, Other packaging

conTenTs: Forecast range: 2014-2019Historical data: 2009-2013190+ original tables and figures

clearly showing global market forecasts

hoW can you Purchase The rePorT?The Future of Packaging in the Middle East & North Africa to 2019 is available now for £3,950. Readers of ME Printer Magazine receive a special 15% discount if ordering before September 30th 2014.To claim your special discount, please call Bill Allen on +44 (0)1372 802086 or email [email protected] Pira is the worldwide authority on the Packaging, Paper and Print industry supply chains.

rePorT conTenTS

Middle Eastern countries

account for a projected share

of almost three-quarters of total packaging sales

in the Middle East

Food 33.8%

Beverages 25.2%

Healthcare 2.9%

Cosmetics 2.7%

Other consumer 9.0%

Industrial/bulk 26.4%

Middle East & North Africa: packaging consumption by packaging product, percentage share of market value, 2014

Rigid plastics 28.2%

Flexible papers 7.9%

Flexible foils 2.7%Flexible plastics

12.9%

Others 5.0%Metal

8.9%Glass 8.8%

Board 25.6%

Smithers Pira ReportPackaging

food represents the largest end use sector for packaging products accounting for a projected 33.8% market value share in 2014