Embed Size (px)

Citation preview

the magazine of the British Insurance Brokers’ AssociationWinter 2006 Issue 27

thebrokerBIBA’s compliance forums:taking off across the regions

London market technology:working IT out

Why company culture counts:keeping employees loyal

Liability market onatightropeIs high-risk cover on shaky ground?

BIBA – Leading the way in UK insurance

IT’S OUR POLICY TO SEE THINGS DIFFERENTLY

Whether it’s a furniture factory or a fish farm – or just about

anything in between – QBE can provide the cover. That’s

because our innovative approach and healthy appetite for risk

enable us to find solutions to problems in all kinds of areas.

Even the ones that leave other insurers high and dry. No wonder

we’re one of the UK’s leading insurers. Share the success,

visit www.QBE.com/uk or email [email protected]

FROM CHAIRSTO FISH,

WE’LL SEE A WAYTO INSURE THEM.

CONTENTS

Management

22 Your businessSpotlight on private medicalinsurance cover, revampingwebsites and tacklingworkplace bullying

25 Training BIBA’s affordable compliancecourses are taking placeacross the UK

27 Schemes focusWhy BIBA’s travel scheme isgoing from strength tostrength

30 Technical briefingInsuring large goods vehiclescan be a minefield. TonyGardiner of Davis Underwritingsteers a course through it

33 Professional indemnityBIBA’s Graeme Trudgill advises on how to choosethe right cover

37 In my experienceGina Dixon, managing directorfor Jelf commercial insurance,on making it

38 Question timeBIBA’s in-house expertsprovide the answers. Plus takeon our crossword challenge

Regulars

04 ViewpointChief executive Eric Galbraithspeaks his mind

05 News and viewsUpdates from across the UK

07 BIBA regionsRegional latest and guestcolumnist, Ian Dickinson

08 Media watchBIBA presses on with its travelcover campaign and commentfrom Insurance Times editor,Elliot Lane

Features

10 London market technologyLloyd’s has not had the bestreputation for IT innovation.Jon Guy explains why timesare changing

13 Compliance forumsWhy this new BIBA initiative isproving invaluable

16 Employee retentionBrokers tell Katy Dowellabout the importance ofcompany culture

18 High-risk liability Marcus Alcock looks at coverfor riskier sectors

Are you experiencing problems placing liabilitycover for higher risk cases? Although the markethas eased, there are fears that, like a latent

volcano, the liability crisis could erupt again.It was back in 2002 that BIBA launched a major campaign to tackle

growing problems in placing employers’ liability. We achieved a massiveamount of awareness and our press coverage included lead stories in theFinancial Times and Daily Telegraph business sections. The Governmentwas involved in talks, but no clear conclusion was reached. The situationresolved itself because of more capacity and the soft market – even so, our

feature on page 18 suggests that problems remain. Thanks to Ian Dickinson, chairman of BIBA’s West of

England region, for being our guest columnist. The regionsare our lifeblood and they are flourishing as never before.

This is partly down to our team of regional executiveswho play an important role in helping organise local eventsand providing administrative support. We always welcomemore regional involvement. So, if you’d like to find outmore about BIBA’s regions and the activities taking placein your area, please check out our website.

WE

LCO

ME

BIBA contactsEric GalbraithChief Executive020 7397 [email protected]

Peter StaddonHead of Technical Services020 7397 [email protected]

Graeme TrudgillTechnical Services Manager020 7397 [email protected]

Paul GarlandMembership Manager07808 [email protected]

Steve WhiteHead of Compliance and Training020 7397 [email protected]

Doreen CampbellOffice Manager020 7397 [email protected]

Lindsay CampbellExecutive Assistant020 7397 [email protected]

Leighann BurtrandCommunications Co-ordinator020 7397 [email protected]

Kirsty GordonMembership and Broker ASSESS020 7397 [email protected]

This magazine is about you andfor you – so we do rely on yourcontributions. Please contactLeighann Burtrand with yournews and views. Her details arein the contact list above.

BIBA House, 14 Bevis Marks,London EC3A 7NT

Design: Beetroot PublishingPrint: SMPAdvertising: Mainline Media

Whilst every care has been taken in thecompilation of this magazine, errors orommissions are not the responsibility ofthe publishers or editorial staff. ©Allrights reserved. Products and servicesadvertised within the broker do not carryendorsement or recommendation byBIBA. The BIBA logo is added free byrequest to members’ advertisements. Itwarrants or signifies nothing more thanthe advertiser is a member.

COVER IMAGE: TOM FROST

thebroker

INSIDE WINTER 2006

‘‘’’

Leighann BurtrandEditor of the broker

10

13

16

the broker winter 2006 03

VIEWPOINT

Commission disclosure – we mustwork togetherIt was back in May that BIBA produced anew TOBA wording which members coulduse for their commercial customers. Ouraim was to encourage greater transparency,and it reminded clients that they could asktheir broker what level of remuneration isbeing received.

We support the FSA’s goal of recognisingand managing potential conflicts of interestin the way that brokers are remunerated. Byamending their Terms of BusinessAgreements (TOBAs) to commercialcustomers, our members have made animportant step towards greatertransparency and we are pleased that theFSA’s chief executive, John Tiner, recognisesthe value of this.

BIBA is keen to assist the FSA inaccomplishing its objective and is confidentan industry-led solution is not onlydesirable but achievable. We will continueour dialogue with the FSA to work towardsa market-led solution and would urge allmembers to make their views knowndirectly to BIBA or the FSA. Only byengaging with the FSA will we ensure amarket-led solution.

To help achieve such a solution, we arestrongly recommending to brokers that,when dealing with commercial customers,they ensure that, as a minimum, thefollowing is in place:• Conflict Management

receiving commission from an insurerwhile acting as agent of the customergenerates a potential conflict of interest.Firms must be able to demonstrate that this potential conflict of interest

FSCS and FOS funding must be fairWe will be keeping a watchful eye on newfunding proposals from the FinancialServices Compensation Scheme (FSCS)and the Financial Ombudsman scheme.This is in light of the FSA’s latestDiscussion Papers which set out a numberof options that could mean highercontributions from insuranceintermediaries.

The broker marketplace has generatedrelatively few calls on the FSCS orcomplaints and is low risk compared toother sectors under FSA regulation.Brokers should not be subsidising othersectors which are more problematic. Wewill campaign hard against any increasethat is disproportionate.

Time to take controlI’ve been speaking at a number of regionalevents recently across the UK and haveenjoyed catching up with many members.But, whether in Scotland or the SouthWest, one fact remains clear – thecompetition is not letting up.

While multi-distribution is here to stay,our discussions with members suggest asense of feeling that they are no longerwilling to be quite as tolerant of somepractices. We must respond where there are challenges to customer access,inappropriate marketing, or differentquotations within the same channel. It isimportant to keep BIBA aware of theseissues – so let us know of any matter whichconcerns you.

has been identified and is being managed. Firms may wish to considerimplementing a formal conflicts ofinterest policy. Details of how to do thiscan be found on our website.

• Disclosurefirms must ensure that they haveprocesses in place to ensure that if andwhen a commercial customer asks aboutremuneration, a full disclosure is made –to include all commissions, profit shares,volume over-rides, fees, charges, etc

• TOBAsfirms must ensure that their TOBAs withcommercial customers include the BIBAwording in respect of transparency – Mr Tiner praised this approach in hisrecent speech – and that the wording hasbeen positively brought to the customer’sattention. The FSA has announced its forensic review

will almost certainly include looking at howfirms are dealing with commercial customersand the steps they have taken to improve thedegree of transparency in the process. Shouldyou wish to discuss any aspect of this, pleasedo not hesitate to contact Steve White, BIBA’shead of compliance and training.

An industry-ledsolution is not onlydesirable butachievable

‘‘’’04 winter 2006 the broker

Eric Galbraith,BIBA’s chief executive,talks about the keymatters on his agenda

Email Eric Galbraith [email protected]

NEWS AND VIEWS

A solutionto contractcertainty?The FSA spotlight is shining on provincialbrokers to confirm their ability to complywith the industry’s contract certaintyguidelines.

FSA chief executive John Tiner has warnedthat progress must not falter and that insurersneed to work more closely with BIBA to findother ways of demonstrating contract certainty

among regional brokers.Concern may have arisen

from omissions within thelatest set of returns providedto the FSA by provincialbrokers, rather than agenuine inability to complywith the guidelines. But,according to the MarketReform Programme Office inits recent Progress Update,data gathered from regionalbrokers suggests only 63 per cent of commercial

contracts are being issued to customerswithin the 30-day period. This is woefully shortof the current 85 per cent target and the90 per cent being met by insurers.

Most provincial brokers use softwaresystems to administer their insurancebusiness and therefore have at their disposalthe potential for recording insurancetransactions, tracking the time for contractdocuments to be received from insurers andthe time taken to pass these to the customer.

Through specific reporting provided bythese systems, it should be easy for brokers toprovide evidence and report compliance orhighlight instances where contracts may nothave been issued within guidelines. Better still,electronic diary facilities provided by the systemshould enable brokers to take timely action toavoid contracts being issued outside them.

Software systems can help take the painout of reconciling client money by making iteasy for the broker to configure their system inline with their agency agreements and byproviding reports to enable client money to betracked and segregated. Software housescannot guarantee a broker will meet the FSA’sregulations. But, if used correctly, software willreduce the effort, and therefore cost, to thebroker in providing evidence of compliance.Laurence Walker is managing director ofSSP Holdings

RIG

HT

TO

RE

PLY

Laurence Walker

Roshan’s a knockoutin young broker award

the broker winter 2006 05

Roshan Choolhun of Lloyd’swholesale brokerChesterfield Group has wonthe Sheikh Abdullah YoungBroker of the Year Award.

The 26-year-old, whospecialises in accident, health andcontingency business, wowed thejudges with his commitment,academic achievement andbusiness acumen.

Roshan formerly had a careeras an amateur boxer but is nowdedicated to broking, having risento an assistant director’s positionwith Chesterfield. He joinedChesterfield at the age of 21 andby 24, had gained the ACII and isnow planning to embark on theFCII. He has helped hiscompany’s revenue increasesubstantially – the income fromhis team accounts for some 25 percent of the total for thegroup, with a turnover in theregion of £1 million.

“I like the fact this is an

entrepreneurial business andthere is so much opportunity.Winning was fantastic and Itreated myself to a digital radiowith the prize money,” Roshansaid. He admitted his wife andmother had also done rather wellfrom the winnings too.

Roshan won a £2,500 prizewhich was presented by LordMohamed Sheikh, who ischairman and chief executive ofbrokers Camberford Law.Lord Sheikh launched TheSheikh Abdullah Foundationwhich promotes the education,development and recognition ofyoung people in the UK andworldwide.

Chesterfield operates in anumber of niche markets,including high-risk occupations,terror cover and film insurance.It also provides cover for thoseworking abroad, includingtroublespots such as Iraq andSudan.

Roshan Choolhun (far right) receives hisaward from Lord Mohamed Sheikh

NEWS AND VIEWS

Brokers are being encouraged by BIBA torecommend Workplace Health Connect, a new Health & Safety Executive-fundedinitiative, to their small and medium-sizedenterprise (SME) clients.

Workplace Health Connect provides free healthand safety advice in the workplace. It includes anadvice line and site visits can also be arranged.

Peter Staddon, head of technical services, said:“It’s often quoted that 28 million days are lostthrough work-related ill health. But, there are ofteneasy steps that companies can take which will keeptheir workforce safer and healthier. The fact that thisis a free service means that many small businessescan pick up useful information without any outlay.”

He adds that Workplace Health Connect’swebsite contains information on key areas such asimplementing an absence managementprogramme. “It explains, in practical terms, how tomanage staff absence. Even common conditionssuch as stress, asthma and back pain should notbe viewed as unavoidable. Having soundprocedures in place can reduce both the incidenceand severity of these and prevent accidentsoccurring. The end result is that the businessshould be more profitable.”

Workplace Health Connect offers both ahelpline and site visits from an impartial adviser canalso be provided.

More information can be found atwww.workplacehealthconnect.co.uk

06 winter 2006 the broker

We’reAchievingExcellencein 2007BIBA has announced itsconference theme for 2007is Achieving Excellence –the event itself will takeplace from 23 to 25 May atExCel London.

The title has beenselected to reflect brokers’many achievements overrecent months. Thisincludes many cases ofexceeding regulatoryrequirements, inrecognition of the strongprofessional relationshipswe have with clients and indeveloping the highestlevels of technicalcompetence.

Eric Galbraith, BIBA’schief executive, said: “BIBA2007 will address issues forall segments of the brokingand intermediary channel –large, small, local, nationaland international,showcasing the UK andLondon.”

Following the sell-outexhibition at the 2006conference in Brighton,with 143 exhibitors andmore than 2,000 attendees,ExCeL London offers evenmore floorspace on onelevel for delegates andexhibitors. Next year will bethe first time the event hasbeen held in London formore than 10 years.

Further information onthe conference will be

posted on the BIBA websiteat www.biba.org.uk

BIBA is urging the Departmentfor Constitutional Affairs (DCA)to exempt brokers that offerclaims management servicesfrom further regulation.

It was announced in the recentCompensation Bill that claimsmanagement services will besubject to regulation. This role willbe carried out by the DCA andStaffordshire Trading Standards –the latter will undertake thecompliance work.

The current drafting of theproposed regulation could posefurther onerous responsibilities onbrokers. BIBA’s head of complianceand training, Steve White, said: “Asdrafted, the regulations couldcatch brokers when passinguninsured injury cases on in the

BIBA calls on DCA to redraft billabsence of a ‘before the event’ legalexpenses policy, such as where amotor policyholder is injured in anon-fault accident.”

He said BIBA was a strongsupporter of regulation for claimsfarmers, but that brokers carryingout this work were invariablydoing it to assist their clients. “Thiswill often include assistance inpursuing uninsured losses, both inrespect of property damage andpersonal injury. The activity isusually incidental to insurancemediation.”

Mr White says there needs to bean exemption for those firms thatare already subject to FSAregulation. “We would like to see aredrafting. The intermediarysector only came under the

jurisdiction of the FSA in January2005 and to impose a furtherregulatory burden now, less thantwo years later, would be whollyunjustified. We believe thatanything less than a complete andunequivocal exemption forinsurance brokers would runcounter to the established keyprinciples of better regulation –namely, proportionality andtargeting.”

The interests of bothintermediary firms and customersare best served by allowing thosefirms that are authorised andregulated by the FSA to be exemptfrom the regulation of claimsmanagement services, where theactivity is incidental to theinsurance mediation activity.

Health and safety for SMEs

IMA

GE

: IS

TOC

KP

HO

TO

Newmarket’s MillenniumGrandstand was theimpressive setting for therecent Joint Market Forumorganised by BIBA Anglia andCambridge CII.

Hot topics on the agendaincluded: regulation and whetherthis has been good for clients,broker and insurer consolidation,commission disclosure, offshoringand if ecommerce presents threatsor opportunities to brokers.

A top quality panel of speakers

discussed these issues, followed bya question and answer session.

The panel comprised BIBA’schief executive, Eric Galbraith;George Berrie, Norwich Union’sdirector of trading; Norrie Erwin,the CII’s business developmentdirector; AXA’s distributiondevelopment director, Jillian Watt;Steve Wood, Ecclesiastical’s generalmanager; and Paul Maidment,director with Allianz Cornhill. Theearly evening event was wellsupported with 100-plus attendees.

BIBA REGIONS

Regional executives – contactsYorkshire and NorthernIan Raper01274 [email protected]

Merseyside, WestCheshire, North Wales,Isle of Man and Greater Manchester Bob Nicholls 07831 [email protected]

Scotland Clive Hurn 07836 [email protected]

West of EnglandBarry Blakley07766 235037 [email protected]

West MidlandsBob Darwin0121 [email protected]

AngliaJo Morgan01638 [email protected]

South East and CentralDiane Smyllie01959 [email protected]

BIBA Anglia and CIIhost joint forum

the broker winter 2006 07

Far from allquiet on theWestern FrontThere has been a lot happening in theWest of England region. We recentlyheld our annual dinner in Bristol and agolf day in Taunton, with more than50 brokers participating.

Being a regional chairman is hard workbut enjoyable and, with a second year tocomplete, I’m hoping still more can beachieved.

There’s plenty going on,but it’s not all dinners anddays out. Far more is aboutcommittees, attendingmeetings at BIBA House andlet’s not forget the day job –I’m also compliancemanager and commercialaccount executive for theBrunsdon Group.

It helps having asupportive employer,although the experience I gainalso benefits my company.

I probably spend aroundone day a week on BIBA

work and a day a month in London at BIBAHouse. Thanks to technology, I work a lotfrom home – this is not a role for someonewanting a nine to five routine!

I’m not complaining though – I get anawful lot out of it and have an excellentcommittee. The arrival of regional executiveshas been enormously helpful and, in theWest of England, Barry Blakley has beensecond to none.

I’m also a vice-president of the CharteredInsurance Institute in Bristol and sit on theeducation committee. I’d like to bring BIBAand the CII closer, as members of both shareso much common ground. I’m sure there willbe more events we can host jointly.

Communication about what we are doingmatters. There are regular BIBA bulletins andinformation is available on the web, too. Butthis may at times only reach more seniorpeople. We must make sure we let people‘down the chain’ know too.

I’m a passionate believer in the value ofBIBA’s regions. We’re in touch with membersand can feed back directly what they think.This makes BIBA what it is.

I would invite anyone who wants to find outmore to get involved. We’re not an exclusiveclub – please join us.

ME

MB

ER

SH

IPM

ATTE

RS

Ian DickinsonRegional chairman BIBAWest of England

More than 40 golfers tookpart recently in this year’sBIBA West Midlands GolfDay, held at the BromsgroveGolf Centre.

“It was superb weather andwe were delighted to receive somuch sponsorship. Brokers,insurers, premium financecompanies and other sponsorswere among those playing. Thisis the second year the event’sbeen held and we’re alreadylooking forward to 2007,” saidStephen Clowes, managingdirector of BIBA memberMillennium Insurance. His

company was among thesponsors. Other sponsorsincluded Groupama, ClosePremium Finance andKaupthing Singer & FriedlanderPremium Finance.

The winner of the BIBATrophy was Simon Andertonof Cheshire Data Systemswho received the trophyfrom Richard Wynne-Jones, chairman ofthe West Midlandscommittee.

All the fun of the fairway

IMA

GE

: IS

TOC

KP

HO

TO

MEDIA WATCH

08 winter 2006 the broker

John Tiner’s threat to brokers that theyare drinking in the last chance saloon ifthey try and resist full commissiontransparency has left some thinking theglass is half full.

The optimists in the broking communitybelieve mandatory disclosure will finally bring inthe expected level playing field – much talkedabout although often derided – that will actually

harden the market and bringmuch-needed profitability.

Brokers caught in the smalland medium-sized enterprisesrenewal maelstrom bemoanthe “softest market we haveever seen”. Around five percent top-line profitability in thesecond and third quarters of2006 among the nationals andsuper-regionals has notpleased shareholders andventure capitalist parents alike.

Elliot Lane

PR

ES

SB

RIE

FIN

G

Though the FSA is frustrated over the “gridlock” in producingan industry-led scheme to tackle transparency because ofsuspected “consumer detriment”, the common theme amongbrokers is that all their clients are TCF-ed to the hilt and arehappy with the relationship.

Smaller brokers, even the emerging “mini-supers” in theprovinces, will benefit from disclosure because the nationals willinevitably have to pursue volume and naturally higher commissionsto survive. It is already obvious on the borders of Wales, in thenorth-east of England and Scotland that the local brokers areeating into the nationals’ clients base because the commissionis lower – though only slightly – and the service is better.

Canary Wharf talks about principles-based regulation andbrokers should think of disclosure as just that – a principle, andnot the end of their business.

Sitting Canute-like waiting for the tide will just lead to manybrokers being washed away. Embrace the core value of serviceand the commissions will come. Elliot Lane is editor of Insurance Times

Do you agree with Elliot? Let us know – [email protected]

bombing. This criticised boththe insurance industry for theexclusion and the Governmentfor its refusal to pay compensationto those injured abroad.

“BIBA believes that medicalexpenses is the most importantarea of cover under the travelpolicy and consumers are beingleft exposed because of thisexclusion,” said Mr Trudgill.

He added he wanted insurersto take action. “When someinsurers have been questioned,their argument is that prohibitivecosts will be passed ontoconsumers. We do not believe thisis the case.”

BIBA battles on to protect holidaymakersExclusion clausesleave touristsexposed to huge bills

BIBA is continuing itscampaign to ensure the publicis protected against terrorattacks when abroad.

Despite BIBA first raisingawareness of the issue back in 2004,many insurers still have a generalexclusion against terrorism. Thismeans anyone affected could befaced with potentially huge bills formedical costs and repatriation.

Graeme Trudgill, BIBA’stechnical services manager, wasinterviewed recently on BBC’s RealStory, presented by Fiona Bruce.The television programme featuredvictims and relatives of thosecaught up in the Sharm el Sheikh

He said BIBA’s talks withtravel underwriters showedthat cover against terrorismcould be included, at a cost ofaround one per cent to five percent of the premium. “It’s aminimal amount. What we aresaying is that this is an unlikelyevent, but is absolutely crucialthat the holidaymakers havethis protection.”

He said there was furthercause for concern, becausetravel agents – which aren’tregulated by the FSA – areunlikely to be telling theircustomers about the exclusion.

IMA

GE

:IS

TOC

KP

HO

TO

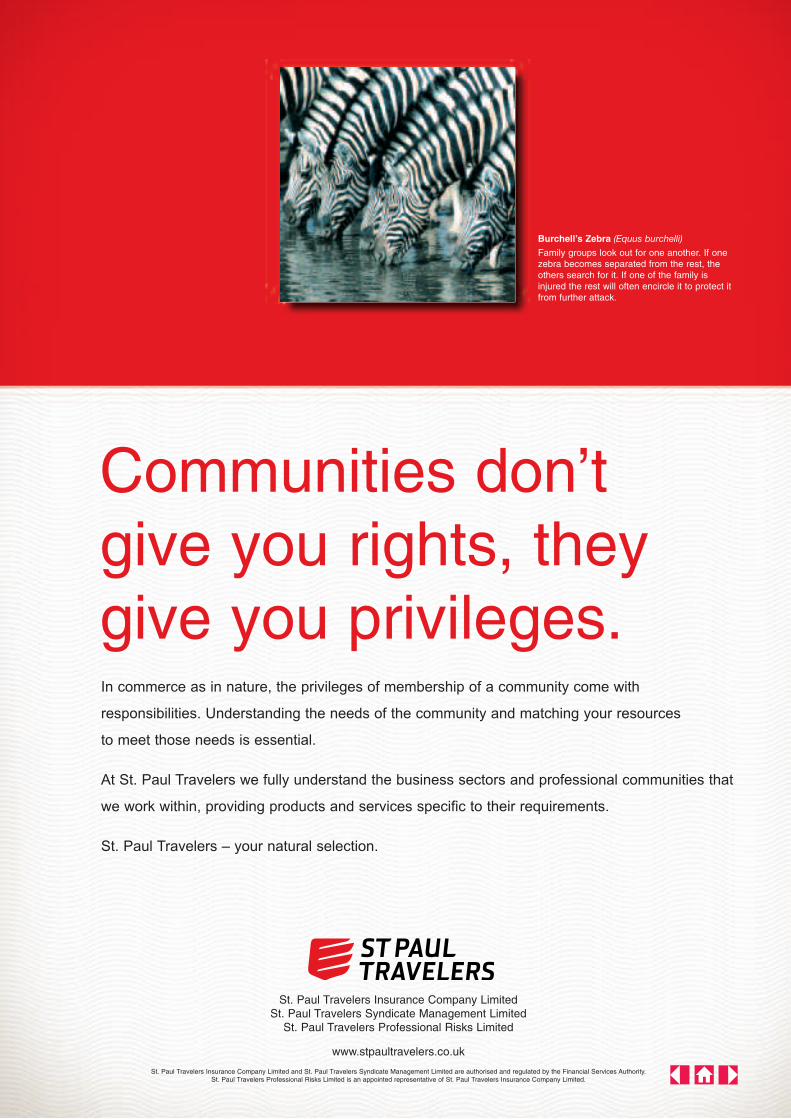

In commerce as in nature, the privileges of membership of a community come with

responsibilities. Understanding the needs of the community and matching your resources

to meet those needs is essential.

At St. Paul Travelers we fully understand the business sectors and professional communities that

we work within, providing products and services specific to their requirements.

St. Paul Travelers – your natural selection.

St. Paul Travelers Insurance Company Limited St. Paul Travelers Syndicate Management Limited

St. Paul Travelers Professional Risks Limited

www.stpaultravelers.co.uk

Burchell’s Zebra (Equus burchelli)

Family groups look out for one another. If onezebra becomes separated from the rest, theothers search for it. If one of the family isinjured the rest will often encircle it to protect itfrom further attack.

Communities don’tgive you rights, theygive you privileges.

St. Paul Travelers Insurance Company Limited and St. Paul Travelers Syndicate Management Limited are authorised and regulated by the Financial Services Authority.St. Paul Travelers Professional Risks Limited is an appointed representative of St. Paul Travelers Insurance Company Limited.

STP7100 St Pauls Adverts FINAL x5 6/1/06 9:51 am Page 1

LONDON MARKET

10 winter 2006 the broker

The old saying “if it ain’t broke, don’tfix it” is an adage that, in the past,could easily have been applied toLondon Market brokers’ attitude totechnology.

The market’s hesitation to embracetechnology with enthusiasm isunderstandable to a certain extent,considering the spectacular failure of morethan one technological project – Kinnectimmediately springs to mind – in the past.

However, in recent years, there has beena quiet evolution in the market’s approachto technology – with many brokers wakingup to the fact that something is broken andit’s within their powers to fix it.

The secret to success, claim a number ofmarket commentators, is an informed and,more importantly, a uniformed approach.And the various market initiatives in placeto facilitate the progression of the entiremarket, from the Market Reform Group tothe G6, are ensuring that the technologicalideals are becoming an everyday reality.

“We see it as imperative that if Londonis to remain a competitive and attractiveplace for customers to place business, thenit has to focus on improving its approachto technology,” says David Hough,executive director of the London MarketInsurance Brokers’ Committee (LMBC).

ModernisationThe LMBC is one of a group of four marketassociations, including the Lloyd’s MarketAssociation (LMA), the InternationalUnderwriting Association (IUA) and

Lloyd’s, which makes up the MarketReform Group (MRG) responsible fordriving the overall modernisation ofthe market.

“At the MRG we are planning a three-year strategy to include an overallframework and timeline on the reforminitiatives,” says Mr Hough. He is under noillusions as to the potential issuesassociated with such a task: “Moving themarket forward never happens as quicklyas it should and it is certainly a challenge.It’s just a question of encouraging thoseinvolved to move as fast as they can, so wedon’t have to wait for the speed of the slow.”

Electronic claimsIan Summers, director of change strategy atAon, says there are key advantages inupping the ante. “It will make the marketmore attractive to clients to support theunique market processes and make it moreefficient,” he says. “In a nutshell, it will helpto remove the so-called ‘Londonisms’ that itis perceived to have at the moment.”

Mr Summers says Aon aims to be at theforefront of the technological initiatives.“We’re already using electronic claimsaround the world, with 100,000 claimsalready been processed to date and we willuse the same technology to accommodateelectronic claims filing in London.”

He adds in terms of accounting andsettlement Aon is already using technologyfor Europe and the US and we will bebringing this to London. “These initiativesillustrate that we’re well on the way to

meeting the roadmap objectives – now wehave to drive the implementation.”

In March 2006, Benfield announced thecompletion of its first electronic transfers ofreinsurance submissions using peer-to-peerstandard messaging with some of the Groupof Six (G6), the alliance of six Lloyd’sinsurers working together to agree this typeof electronic processes by a group of major

Jon Guy looks at the London market’s attitudeto technology and finds that there is growingrealisation that change is needed fast

We’refixing IT

the broker winter 2006 11

brokers using the internationally-recognised ACORD data standards.

Benfield says the project is the latestinitiative undertaken by the company tocreate electronic systems that promotestreamlined processes and greater marketefficiency. In 2004, Benfield announced itsglobal capability to provide all technicaldocumentation – claim advice, claim

momentum and impetus into the process,”says Rupert Swallow, head of globaloperations at Benfield.

Another working example of progresscame recently when Hiscox became thefirst insurer to successfully complete atransaction under the Electronic ClaimsFiles (ECF) system, which is being madeavailable to all Lloyd’s managing agentsand brokers. Lloyd’s claims the moveindicates “a significant step forward inreforming the market’s processes byenabling brokers and underwriters toprocess claims electronically”.

The ECF technology has been testedby 12 managing agents and five brokersover the past four months and has nowbeen rolled-out to the whole of theLloyd’s market.

Says Jeremy Pinchin, group claimsdirector at Hiscox: “This move willcertainly speed up the process of claimsmanagement and stop the archaic luggingaround of files.”

The urban myth relating to brokers and

the London market is that the so-called“archaic” processes involved in the market isan issue that brokers are reluctant to lose,specifically that it will replace thetraditional face-to-face interaction currentlyfavoured. On the contrary, the reality, saythose in the know, is that technology will bethe enabler which will free up more time toallow brokers to deal face-to-face in thosecases that need it the most.

Adding value“When the technology is used correctly, itactually helps us free up time to deal withclients face-to-face where this approachreally adds value,” comments Mr Summersat Aon. “There’s this myth that technologywill remove value, but this is definitely notthe case.”

Other concerns include the fact thattechnology could reduce the number ofcompanies operating in the market, butthis does not appear to be a major concernfor the majority of those in the market. Ofmore importance, it seems, is that Londonremains a leader in the global marketplace.“The fact is that if we make the marketmore efficient and strip it of certain coststhrough the use of technology, then it willremain a healthy environment,” commentsMr Hough.

When the technology is usedcorrectly, it helps us free up timeto deal with clients face-to-face‘‘’’

settlement, premium credit closing andtreaty balance – in a fully electronic formatthat eliminates paper trails.

“We want to move at the speed of thefastest person and it’s been veryencouraging, I think, for those who dowant to see change in the London market tohave a group of people such as G6 comingtogether and really putting some

IMA

GE

: NAT

HA

ND

AN

IELS

Prism Insurance

Management Limited

Polygon Hall

PO Box 225

Le Marchant Street

St Peter Port

Guernsey

GY1 4HY

Tel: +44 (0)1481 716000

Fax: +44 (0)1481 716553

www.prism.co.gg

A Heritage Group Company.

Licensed by the Guernsey Financial Services

Commission.

Prism Insurance Management is

the leading independent captive

insurance manager in Guernsey.

Our independence and freedom

from ownership by any other

insurance or broking organisation

means that we are best placed to

partner UK brokers in securing the

advantages of captive insurance

for their clients.

Our team of Guernsey and London based

specialists provides many organisations with

cost effective risk transfer solutions that offer

significant advantages over traditional methods

of insurance.

We create and manage a comprehensive range

of captive insurance and alternative risk transfer

vehicles, including Protected Cell Companies

(PCCs) and Special Purpose Vehicles (SPVs), which

deliver sustainable financial advantages for our

varied clients.

Including captive insurance in the services you

offer can help deliver added value to your clients

and consolidate long term relationships, rather

than just relying on the annual renewal process.

For information please contact Charles Allenor Nick Heys.

Prism is part of the Heritage Group, a leading

independent provider of insurance and specialist

financial services, uniquely structured to provide

effective solutions to clients’ varying and complex

needs.

Independent captive management

COMPLIANCE FORUMS

the broker winter 2006 13

Group therapyHaving responsibility for compliancecan be tough, but forums being runacross the regions are easing theburden, as Rachel Gordon reports

If we can get a groupof people with similarissues around thetable, then they canstart sharing ideas

‘‘’’

It’s often said that the best ideas aresimple. A classic example is BIBA’scompliance forums, which bringtogether broking staff who haveregulatory responsibility and allowthem to share best practice.

BIBA chief executive, Eric Galbraith,says: “I think these are one of the mostimpressive initiatives the regions haveinstigated and the level of attendance and feedback we’ve received has shown that there is clear demand for them –therefore, we’ll be holding them regularlythroughout 2007.”

The forums work because they are heldlocally and are open to broking staff at alllevels. All you need is some involvement inensuring your firm meets its complianceobligations.

Larger brokers may well have their owncompliance manager, but very often, insmaller firms, someone will need to take onthe responsibilities in addition to theirregular job. There are also one-man-bandfirms where the principal wears many hats.

FeedbackIan Dickinson, the current chairman of theWest of England region, is compliancemanager for Brunsdon Group as well as itscommercial account executive. “I’m reallypleased with the way these forums areoperating. It’s so helpful to get togetherwith others in the same situation andthere’s been a lot of useful feedback. Weneed to make sure that the topics where itcould be relevant to put pressure on theFSA and other parties go back to BIBAHouse – and this is happening.”

Steve White, BIBA’s head of complianceand training, has attended many forumsand comments: “The compliance officer’sjob can be a lonely one. They can be sat in acorner and left to get on with it. The job canbe pressurised and they can also come upagainst some unpleasantness at work fromcolleagues – they become known as the‘business prevention officer’. But if we can

COMPLIANCE FORUMS

14 winter 2006 the broker

A BIBA complianceforum – what’s itall about?

By their nature, complianceforums are not prescriptive. The aim is for anyone withcompliance responsibilities tofeel they can attend and askquestions in a supportiveenvironment.

An agenda is emailed toattendees and minutes are alsoprovided afterwards, buteveryone is welcome to havetheir say. Ian Dickinson hassupplied the following points toshow the overall forum flavour:

ktalking it throughthe FSA is a non-prescriptiveregulator. This poseschallenges for complianceofficers as it can createuncertainty.

ktopics for discussionamong the areas covered arethe FSA’s rules and themessuch as Treating CustomersFairly and the impact ofregulation on an insurancebroker’s culture.

ksharing experiencesfirms who have already beenthrough arrow visits or hadother contact with the the FSAcan share the experience.

kusing outside expertsforums often bring in guestspeakers and discuss traininginitiatives.

kvoicing opinionsfollowing a forum, key issuesmay be raised which can thenbe fed back to BIBA’s headoffice – and, if necessary, usedin lobbying and widerawareness raising.

because there is a good sense of ownershipand they are easy to get to. We hold forumsduring the day because they are workrelated and many brokers are alreadydoing long enough hours. In Bristol, we’vebeen fortunate as Marsh has good officesand allows us to use them. It’s not justmembers who catch up, we also recentlyhad Andrew Honey, head of insurance forthe FSA’s small firms division, as a guestspeaker,” explains Mr Blakley.

ParticipationBob Nicholls, regional executive forMerseyside, West Cheshire, North Wales,Isle of Man and Greater Manchester,covers a big catchment area and is alsoorganising a number of forums for earlynext year. “I think they work because thereis plenty of participation. The forum electsa chairman and they create their ownagenda. The group can talk about specificproblems – perhaps relating to rules, butalso wider issues. We recently discussedcontract certainty and the problemsbrokers had in meeting this when insurerswere late sending over documentation.”

He adds that there have also beensome positive noises about the forumsfrom the FSA. “They must be pleasedthat compliance is being activelydiscussed, rather than people working inisolation. We’re hoping to hold ourforums quarterly.”

To find out more about complianceforums happening in your area,

contact your local regional executive andalso check out the BIBA RegionalCommittees section of the website.

get a group of people with similar issuesaround the table, then they can startsharing ideas and come up with solutions.They can also stay in contact afterwards,via phone and email.”

The credit for the idea of holdingforums goes to Chris Clarke, developmentdirector with the Jelf Group and a formerWest of England regional chairman. InNovember 2005, in his BIBA role, heemailed the local membership to gaugeinterest for holding regular meetings todiscuss compliance matters.

The words Mr Clarke used remainequally true today: “Compliance is a non-competitive area where we can truly learnfrom each other and we will all benefit ifwe raise the level of professionalismwithin our own industry.”

There was strong support and the firstforum took place in February 2006, witharound 30 attendees.

OwnershipBy then, Ian Dickinson had picked up thechairman’s reins and has worked hard toensure the forums are held regularly. Aswith any meeting, there is plenty oforganisation required and this is where therole of the regional executive can proveinvaluable.

For example, Mr Dickinson is assistedby Barry Blakley, regional executive for theWest of England. “I think these work

IMA

GE

S: I

STO

CK

PH

OTO

24/7 365...MOTOR CLAIMS

As one of the fastest growing Motor Claims Services Group in theUK, Plantec Holdings Ltd know the best way to handle your claims,whilst putting into practise the core ethic of the group; the impor-tance of high quality service provision.

- Car, van, motorcycle and specialist claims management- True in house end-to-end service process - High quality bespoke claims service

To find out how Plantec can make the difference to your company, callour Business Development Manager on

0870 285 5005 or 0870 236 8888Or register your interest to [email protected]

PLANTEC HOLDINGS LTDEND TO END MOTOR CLAIMS SOLUTIONS

Whether it’s a furniture factory or a

fish farm – or just about anything

in between – QBE can provide the

cover. That’s because our innovative

approach and healthy appetite for

risk enable us to find solutions to

problems in all kinds of areas. Even

the ones that leave other insurers high

and dry. No wonder we’re one of the

UK’s leading insurers. Share the success,

visit www.QBE.com/uk or email

FROM CHAIRSTO FISH,

WE’LL SEE A WAYTO INSURE THEM.

IT’S OUR POLICY TO SEE THINGS DIFFERENTLY

EMPLOYEE RETENTION

16 winter 2006 the broker

Why company culture counts

Mr Barton says: “Retaining qualityemployees is integral to fostering robustrelationships. Ours is a people business, soinvesting in developing a team ofunrivalled professionals is essential to ourcontinued success.”

Mark Wood, managing director of theBroker Network, agrees: “Retention isalways key, not only from the simpleeconomic perspective, but also in terms ofcontinuous improvement in our customerservice delivery to members of the BrokerNetwork, clients and insurers.”

For young people coming into themarket, career development is now moreimportant than the calibre of theemployer. Young professionals are clearabout what they want from their dailygrind. Meanwhile, those who have workedin the industry for some time feel a need tobelong in the workplace. Creating goodrelationships within the workingenvironment will have its benefits.

Ms Blanc says Towergate recognisesthat different employees have individual

graduate training programmes, summerand Christmas parties all help to keep upstaff morale. At Towergate, staff briefingsare held regularly, and there is an onlineintranet which allows staff to share a skillsbase. “Our knowledge network isparticularly successful at promoting aculture of knowledge sharing,” says MsBlanc. “This online facility enables staff totap into the extensive network of expertslocated across our UK offices.”

SupportWhen Jelf bought Reading-based GossGroup in March, aligning the twocompany cultures was essential to ensurethe acquisition was successful. The brokerused a charity social event to mark theacquisition and consolidate relationshipsbetween the two brokers’ staff base. TheNew Dawn Ridgeway Walk was aptlynamed to celebrate the next phase in Jelf’sgrowth, while raising money for theNational Deaf Children’s Society.

Alex Alway, Jelf’s group chief executive,explains: “We were at a very importantjuncture and our success has been largelydue to the support and cooperation of ouremployees. This event was not just a scenicwalk through the idyllic countryside – it

Ours is a people business, so investing in developing a team of unrivalledprofessionals is essential to our success‘‘’’

The launch of the CharteredInsurance Institute’s talent initiativeat the recent UK Insurance andFinancial Services Conference hasonce again thrown into the limelightthe industry’s problems withrecruiting fresh talent.

Speaking at the conference, however,AXA chief executive Peter Hubbard blewopen the debate by suggesting thatretaining talent is just as important asrecruitment. He believes brokers need toensure their staff enjoy a vibrant workculture, because a content workforce willinevitably mean happier customers.

In an industry where recruitment istough, the reasons for maintaining astrong company culture are clear.

Amanda Blanc, chief executive ofTowergate Risk Solutions, says retainingstaff brings financial benefits: “Staffretention is crucial to Towergate. Thedirect financial costs of replacing staffare high.”

Career developmentThis is particularly true when there is, asJelf’s group commercial director, PhilBarton, says, “a war for talent”. From callcentre operatives to middle management,those entering a career in insurance cancommand higher wages – and recruitmentcosts are increasing.

Furthermore, as customer servicebecomes increasingly important in acompetitive marketplace, it is crucial thatbrokers build and foster relationshipswith their clients.

Attracting and retainingstaff is far from easyin today’s tough jobsmarket. Katy Dowellpicks up somepointers to succeed

ideas of what their employers should beoffering. She adds that the largestconsolidating broker has a variety ofinitiatives aimed at creating a staff culture.“These range from internal careeropportunities to supporting work/lifebalance with all our fun activities,”comments Ms Blanc.

The work/life balance is addressedthrough rewarding families of employees:“We believe in rewarding not only staff butfamilies too,” she says. “In addition toexcellent employee benefit packages, wehold annual family fun days. These arewhere staff and their families can enjoy aday out at Thorpe Park or Alton Towers.”

There is also emphasis on strong internalcommunication. Online staff forums,

denoted the formation of a stronger, moreformidable presence within the market.Only by working together as one team canwe continue to thrive.”

The consolidating broker, says MrBarton, faces dangers when trying tointegrate in a new business. There is a riskthat company cultures can become diluted.“We manage this through careful selectionof companies that hold similar values –such as client focus,” he adds. “As we grow,we strive to retain our core ethos bycontinually reinforcing our brand andvalues through proactive external and,equally important, internalcommunication.”

The Broker Network also believes thatinternal communication can underpin a

the broker winter 2006 17

y culture counts

company culture. Mr Wood says: “Wehave introduced a process which allowsfor effective two-way communicationbetween the board and the staff. Thisaligns with our aspirations to be aninclusive culture with the requirement tohave a focused vision andimplementation of our strategy.”

Yet these growing brokers know thatstaff social events alone will not create abuoyant company culture. Careerprogression and financial rewards are justas important.

As an AIM-listed broker, Jelf offerslong-term employees share options,giving them direct ownership of thecompany they work for. Towergate alsogives its staff the opportunity to take astake in the company. “A percentage of thecompany is held in our employees’ benefittrust, which shares Towergate’s successwith staff,” says Ms Blanc. For the BrokerNetwork, strong remuneration andbenefits packages are also essential.

All three of these businesses also havein place a career progression plan.

ProgressionGrant Ellis, chief executive of theBroker Network, grew tired of waiting tofeel the benefits of the CII’s talentinitiative and so recently launched hisown graduate training scheme. Thisoffers undergraduates taking a year out oftheir course a work placement with aretainer fee for retuning to the companyonce they have finished their course.The Towergate Academy, meanwhile,offers staff the opportunity to progressthrough the company ranks by taking upfurther training.

Staff retention has never been soimportant to a broker’s financial success.Creating a company culture will ensure astaff loyalty where clients will feel thestrongest benefits. Simple measures suchas “dress down days” and charity eventscan help boost staff morale. Yet careerprogression and financial rewards are justas important.

As Ms Blanc says: “The greatestchallenge is for brokers to have a long-term outlook in a fast-paced competitiveenvironment. Culture can’t be changedovernight.” IM

AG

E: P

HO

TOLI

BR

AR

Y.C

OM

18 winter 2006 the broker

In the current soft market for UKliability risks, it seems almostincredible to think that any sort oftrade would have difficulty findingcover. Capacity is so plentiful andpremiums at such attractive levelsthat even riskier trades are notfinding the purchase of insurancecover for employers or public liabilitytoo problematic.

Yet this was not always the case. Onlythree years ago, with the market facing a“perfect storm” in the aftermath of theterror attacks of 9/11, with reserves underpressure and investment incomeinsufficient, the UK was in the midst ofwhat the media was quick to label “aliability crisis”.

For many trades, the dramaticescalation in premiums they faced in 2002and 2003 came as a real shock.

Market forcesIn the wake of this problem, the UK’sOffice of Fair Trading and the Departmentof Work & Pensions launched an inquiry,and heads were banged together amongbusiness, Government, underwriters andbrokers to try and come up with a solutionto the situation.

Yet despite the hours of negotiation,time and effort put into understanding theissues at stake, in the end no ‘on-high’Government intervention wasforthcoming and market forces were leftto work themselves out.

Everything is seemingly rosy at themoment, but are we heading for yet

another repetition of the crisis when themarket hardens next time around?

Affordable cover is of particular concern to those businesses that aredesignated high-risk. These are trades suchas roofing contractors, scaffolders, wastedisposal contractors and any business

The liability crisis may havepassed, but Marcus Alcockwarns external forces could pushrates up again, particularly forthose in higher risk trades

No room for complacency…

Affordable cover is of particular concern tothose businesses that are designated high-risk‘‘’’

HIGH RISK LIABILITY

involving the use of heat or work at height. These are the sorts of businesses who,

because of the environment in which they work, present the greatest risk tounderwriters.

In 2005, the ABI estimated the averageprice rise for employers’ liability insurance

the broker winter 2006 19

mplacency…

in the UK in 2004 was only seven per cent,compared with rises in the 30 to 40 percent range in 2003. So far in 2006, theindications are that the soft market hascontinued apace.

Peter Franklin, national technicaldirector at broker Jardine Lloyd Thompsonand chairman of BIBA’s LiabilityCommittee, comments: “If you say themarket is a lot easier at the moment and wehaven’t got problems with specialist

schemes available, that’s true to an extent.But I wouldn’t say that cover is cheap,although it is available.”

This viewpoint is echoed by IanRichens, chief executive of broker FM Green, which arranges a specialistscheme for roofing contractors. “Thesituation at the moment is that there isoodles of capacity in the market andeveryone is making money while theindustry is in this euphoric mood. But

Mystery shopper

BACKGROUNDBusiness: Best Roofing Limited, aroofing contractor that is yet to starttrading but wants to get up andrunning as soon as possible. Annual gross turnover: Estimated at£70,000 for the first year.Staff: One director and two employees. Location: Shoreditch, London. Detail for insurance purposes: Best Roofing undertake both ‘hot’ and‘cold’ roofing, with approximately 40to 50 per cent of the business hotroofing, involving blowtorch andbitumen work. No asbestos work isinvolved and no premises over fourstories high.Insurance required: Employers’ andPublic Liability.

EVALUATIONAXA Direct: Service: 2/10 Quote: n/a Overall: 0/10Comments: AXA Direct does not offercover to roofing contractors. It didn’thelp that I had to wait 10 minutes in aphone queue to be informed of this.

Aon: Service: 8/10 Quote: Minimum of£10,000 + tax for EL and PL.Overall: 6/10Comments: The most knowledgeableof all the people I spoke to. Askeddetailed questions about the type ofwork the business would beundertaking and showed a thoroughsector understanding. Not the cheapest.

Creamer Group, Warrington: Service: 8/10 Quote: £11,390 throughTowergate and £3,500 + tax with Quinn(EL policy). Overall: 6/10Comments: Was the fastest and mostefficient of all the people I spoke to, comingback to me quickly with one quote, then10 minutes later with another.

Richard Weston Insurance, LondonService: 5/10 Quote: 7/10 Overall: 6/10Comments: Very good at discussingdetails of what insurance I needed but,unfortunately took longer than expectedto get back to me. Also said I needed toe-mail my details over in order to get aformal quote, though eventually wasinformed that the policy would cost£1,850 per person because we wereusing heat – still a good price.

HIGH RISK LIABILITY

20 winter 2006 the broker

liability. As Mr Leaman says: “There arestill enormous cost issues for insurersand Government pressures such as theextra NHS charges.”

Such charges are not insignificant forunderwriters. This autumn, the NHS willbe able to recover the cost of treatingvictims of workplace accidents frominsurers, potentially adding £150 millionto the cost of claims, according to officialestimates.

The change was to have come intoeffect in April 2005, but was delayed. Andthe pressures on the industry do not endthere. The Government has alsopreviously proposed that employersshould compensate workers who arevictims of crime during working hours,and has suggested that employers’liability insurance should be used to payfor this compensation.

Unfortunately, it could well be thehigh-risk trades who will be the first tofeel the cost increase that underwritersare likely to impose as a result of suchpressures.

…high-risk trades can expect to befirst in the firing line once more‘‘’’

I feel cover will be available, just at ahigher price.”

Despite such sentiments, he feels thatwe shouldn’t panic. “You’d need somesort of catastrophe event like 9/11 totrigger that off again, because thatalmost wiped out reinsurance capacityovernight. But you will see priceincreases, though these will be moregradual – whereas last time we had 500per cent increases for some trades.”

According to Alan Leaman, directorof communications at the Association ofBritish Insurers, what happened lasttime was a market-wide transition.

Pressures“I think our perception was that theliability crisis was a serious marketadjustment – not just a cyclical event –and now the market has settled at a moresustainable level, so we’re hopeful thatsuch violent changes will not be seenagain,” he comments.

“Additionally, insurers are now moresensitive to health and safety issueswhich will help with negotiations.”

But no-one should be lulled into afalse sense of security. For even the ABIsuggests that there could bemacroeconomic factors at work thatcould still spell trouble for high-risk

some businesses, especially directwriters, have pushed prices down andwe have seen premiums drop to pre- 9/11days, but there has been nothing putin the kitty for increased claims costssince 2001.”

He adds: “There is masses of capacityand people can’t fill their quotas. Butwhen the market gets tougher, which Ifeel will happen from 2008 onwards, a lotof capacity will pull out of the market andrates will toughen again. We’ll be back toour good old situation of having nocapacity. As an industry, we really doshoot ourselves in the foot.”

So what can we expect to happen asthe market hardens with respect to high-risk trades?

Mr Franklin muses: “I wouldn’t saythat the work done last time hasproduced any startling results, thoughthere is more work done now on riskmanagement. And some tradeassociations have done good work hereand have good deals in place. But one ofthe plus points is that the market has to

respond to the contract certainty issuesput forward by the Financial ServicesAuthority. And this has taken away someof the mad last-minute rush that we’veseen previously.”

The reality, it seems, is that althoughnegotiations about renewals will be lessfractious than hitherto, nonethelesshigh-risk trades can expect to be first inthe firing line once more.

Price increases“The trough is deeper than it has everbeen and it’s quite something that rateshave fallen off as much as they have,”comments Mr Richens.

“But what happens when the markethardens is that insurers look at the leastdesirable part of the portfolio, which isemployers’ liability and public liabilityfor high risk trades. So if the currentmarket conditions change, then high-riskliabilities will be the first risks thatunderwriters will look to avoid, so Iwouldn’t say in that regard that theproblem has gone away. Having said that,

IMA

GE

S: T

OM

FRO

ST

Registered office: HSB Engineering Insurance Ltd,Aldgate House, 33 Aldgate High Street, London EC3N 1ENHSB Engineering Insurance Ltd is authorised and Regulated bythe Financial Services Authority (No.202738)

Inspections and Consultancy Services are provided byHSB Haughton Engineering Insurance Services Ltd.

alternatively visit www.hsbeil.com

MUCH MORE THAN JUSTBOILERS...

•Inspections

•Health & Safety Consultancy

•Construction Risks

•Machinery Breakdown & Profitsand much more...

Contact your local HSB office or email: [email protected]

Don’t leave it to chancemake sure you’re protected with...

Blue Egg Ecommerce’s managingdirector said: “If you want to appearhighly on search engines, your sitehas to be live. There is no pointspending a lot on launching oneand then just leaving it, you won’tget the return on investment. If abroker is after a particular niche they need to let people know about it who are searching on the web. Youalso need to make sure you have theright key words in the text.”

He says it is essential to regularly update the site by meansof news and other material.

YOUR BUSINESS

Online trading, employee appraisals, how to deal with officebullies and private medical insurance are this issue’s topics

A new year is a good time forbrokers to take a look at theiroperations and see if they canbe improved. In terms of e-business, it could be that manybrokers are not making themost of online opportunities.

But one BIBA member hascertainly got its act together.Manchester-based Caunce O’Harahas just launched a new website,which allows online purchase of PI,business combined, accident andhealth, travel, legal expenses andhealth and safety policies all ofwhich are aimed at freelanceprofessionals. The quote engineallows users to calculate annualpremiums and if satisfied, they cango ahead and buy cover. Once thepayment is processed, an email issent to the customer withinseconds. They can then go to asecure area where certificates andpolicy wordings can be printed.

Caunce O’Hara has beentargeting this sector for 10 years andbroking director John Battycommented: “One of our targetmarkets is IT consultants so weknew we needed to have a sharp

website. What’s more, self-employed professionals are oftenbusy people who may want topurchase cover outside office hours.”

Mr Batty makes sure the site isregularly updated and apart fromproduct information, it alsocontains a lively news section. Headds that choosing the right serviceproviders is also crucial.

Caunce O’Hara used designersHarper James which provided thesite’s clean image and Blue EggEcommerce for search engineoptimisation. Mark Holdsworth,

Time tosmartenup onlinetrading

Does your website need arevamp?

It could well be time to takea long hard look at yourwebsite and assess itsperformance. Key areas tolook at include:k the overall look – does it

flow? Is the design andcolour appropriate? It isimmediately obviouswhat your messages are?Is there too much text andare images confusing?k graphics – are these

working? Is your brandclearly evident and doesyour logo stand out? Anyphotography should becrisp and clear.k navigation – is it easy? If

customers can buyonline, this should besecure, fast and assimple as possible. Ifyour site is large, youshould have a searchfacility. Is contactinformation obvious?k easy to find – many

people use searchengines. There arespecialist companieswho can make sure yourcompany receives plentyof relevant traffic.

IMA

GE

:IS

TOC

KP

HO

TO

22 winter 2006 the broker

Appraise youRegularly appraisingemployees and doing this wellmakes a lot of sense given themarket is now regulated,advises Elizabeth Mills, adirector with Broker Network.

She explains that FinancialServices Authority training andcompetence rules make itappropriate for brokers to set

time aside to review staffperformance. But, these need towork on both sides. Here are hertop tips on appraisals:• make sure the right person

conducts the appraisal – oftenthis should be the line manager

• a pre-appraisal questionnaire isa useful tool for the employee tocomplete to make sure relevantaspects are covered before themain meeting

• this should include how they rate themselves againstthe core competencies of the role, a review of their job likes and dislikes, a review of objectives andtraining and development theyhave taken and what they feelis needed

• provide a written outcome ofthe appraisal

• use open questioning

techniques to encouragehonest discussion

• act following an appraisal – ifthere are areas of weakness,implement training orsupport if relevant

• it may well be worthwhile toconducting appraisals morethan annually, particularly ifyour business is fast movingand you are empoweringyour employees.

IT’S OUR POLICY TO SEE THINGS DIFFERENTLY

Whether it’s a furniture factory or a fish farm – or just about

anything in between – QBE can provide the cover. No wonder

we’re one of the UK’s leading insurers. Share the success,

visit www.QBE.com/uk or email [email protected]

FROM CHAIRSTO FISH,

WE’LL SEE A WAYTO INSURE THEM.

the broker winter 2006 23

For more than 20 years, most privatemedical insurance (PMI) has been solddirect by the insurers via their salesforces. But, over the last five years,maintaining a sales force has becomeincreasingly more expensive for them.

The final death knell of large PMI salesteams was sounded on 14 January 2005 withFinancial Services Authority regulation.Additional compliance costs meant the run-down of sales forces accelerated rapidly.Today, PMI providers with their own sales teamare a rarity. To my knowledge, the onlyremaining substantial one left is Secure Healthand, with their recent acquisition by AXA, thismust now be in doubt.

Over the last 18 months, insurers have beentrying hard to get back to doing business withbrokers. The problem they faced was the largenumber of brokers spread the length andbreath of the UK each only submitting a lowvolume of PMI – not very cost-effective. Plus, of

course, with your own salesforce you hope the client willnot seek alternatives,whereas brokers, if they aredoing their job properly, willdo exactly that.

Insurers are now seekingout alliances with a verylimited number of specialistPMI brokers. They offer themcompetitive premiums,enhanced commission ratesand exclusive menu-based

products. In this way, they can deal with the whole brokermarket. Brokers whose business is primarily not PMI cannow often obtain cheaper premiums, better products and ahigher level of commission by working through one of thesealliances than going direct to the provider.

There are a number of advantages to this way ofworking. From an insurer’s point of view, it can nowconcentrate its resources in just a few places. From abroker’s perspective, it can now deal with somebody whospecialises in PMI and can advise their clientsknowledgeably, and at the same time, obtain lowerpremiums and a higher level of commission.Michael Webber is managing director of specialistintermediary, The Health Insurance Shop

Michael Webber

PM

ILAT

ES

T

How to tackle officebullies effectivelyIt is a sensitive topic, butbrokers, like other businesses,may have a problem withbullying in the workplace.

Research from the CharteredManagement Institute indicatesthat bullies use a range of tactics tointimidate colleagues. Thisincludes overbearing supervisionand undermining by overloadingand criticism. They may blockpromotion and/or training andmake threats about job security.Bullies may also spread maliciousrumours.

The research found almost two-thirds of respondents foundworkplace bullying was becomingincreasing common– a third saidthe situation was worsenedbecause their company wasineffective at dealing with it.

The Chartered ManagementInstitute points out that

organisational change is often akey factor leading to bullyingbehaviour.

Jo Causon, director of marketing,said: “No single off-the-shelf policywill suit every organisation, butthe organisational culture andmanagement style should make itclear that bullying is unacceptable.Shying away from the issue is noexcuse.”

The Institute’s research showsthat where organisations have aformal policy, 70 per cent ofmanagers believe they are effectiveat deterring bullying.

A free guide is available atwww.managers.

org.uk/bullying. Moreinformation can also be foundat specialist charity AndreaAdams Trust – www.andreaadamstrust.org.uk

IMA

GE

:IS

TOC

KP

HO

TO

Tel: 01747-835440 Fax: 01747-835450Email: [email protected]

Post: THE HEALTH INSURANCE SHOP, FREEPOST, NATW120, WARMINSTER BA12 6BRwww.healthinsuranceshop.co.uk

Head Office: 39 Brickfields Business Park Gillingham Dorset SP8 4PX

AUTHORISED AND REGULATED BY THE FINANCIAL SERVICES AUTHORITY

Private Medical Insuranceservice for you or your clients

Expert advice • Choice of 99% of UK providers • Exclusive plansCompetitive Premiums and High levels of indemnity commission

(often better than going direct to the insurer).

AG061041 The Broker Ad 10/11/06 9:16 AM Page 1

TRAINING

the broker winter 2006 25

Master class in compliance

Brokers often learn from experience.Over the years they pick up on the insand outs of different policies andvarious insurers, and perfect the artof managing both employees andtheir customers. But compliance is adifferent matter. If a broker makes amistake in this area, they risk beingfined, losing their reputation and atworst, could go out of business.There is, simply, no margin for error.This is why attending specialisttraining really makes a difference.

BIBA offers a full range of compliancecourses, held across the UK. We use highlyexperienced tutors to lead these, includingBranko Bjelobaba, who heads his ownconsultancy, Branko, and Ian Ritchie, aconsultant with RWA ComplianceServices.

As Mr Bjelobaba explains: “Masteringcompliance does not happen by osmosis.And, brokers who try and wade throughthe Financial Services Authority’sHandbook will find this almost impossible.Since many brokers do not have someonepurely dedicated to compliance, they havea lot to deal with, which is why attending aone-day course is the best way ofunderstanding the basics and being able to

clear up any misunderstandings theymight have.”

Noel Humphries, who runs a brokeragein Craigavon, County Armagh in NorthernIreland, attended recently. He comments:“We’re a small business and I share the roleof compliance officer with my officemanager. The course brought clarity andBranko certainly knows his stuff.”

Compliance courses for 2007 arecurrently being arranged and will be listedon the training section of the BIBA website.We expect to hold them in: Belfast,Birmingham, Bristol, Edinburgh, Glasgow,Ipswich, Leeds, Leicester, Liverpool,Manchester, Norwich, Perth and Cardiff.

Each course covers a dedicated topic andthese include the Insurance Conduct ofBusiness (ICOB) rules and client money.The cost to attend a course is £150 for aBIBA member and £230 for non-members.

Mr Bjelobaba adds: “These coursesrepresent excellent value for money andusing the services of a consultant directly isfar more expensive. I would urge brokerswho are holding out on cost grounds tothink how much it would cost them ifthere was a problem.” Steve White is BIBA’s head of complianceand training

IT’S OUR POLICY TO SEE THINGS DIFFERENTLY

Whether it’s aviation treaty or property – or just about

anything in between – we can provide the cover. No wonder

we’re one of the UK’s leading insurers. Share the success,

visit www.QBE.com/uk or email [email protected]

FROM JET ENGINESTO STAIRWELLS,

WE’LL SEE A WAYTO INSURE THEM.

Regulatory courses:what’s on offerClient money• acting as agent – agreements with

insurers and clients • statutory and non-statutory trust

deeds/bank status letters • firm’s selection of a bank • segregation using designated

investments (NST only) • capital resource requirement • audit requirements • special conditions for operating a

NST • treatment of interest earned • client money transactions • treatment of commission • the Client Money Calculation • disclosures to the Financial Services

Authority • reconciliation of bank and firm’s

records • appointed representatives • foreign exchange risk• credit write-backsICOB• key definitions of retail and

commercial• differences when selling to these

types of customer• statement of demands and needs• mid-term changes• renewals• claims

BIBA is running classes to assist brokerswith regulation across the UK. Steve Whitereports on the options available

IMA

GE

: IS

TOC

KP

HO

TO

More profit. For a

change.Make a change for the better.

A change to Premium Credit is simplicity in itself and you’ll find it just about the most rewarding too, in many ways.

Our offer is simple, clear and straightforward - better new business rates,increased finance commission, better renewal rates and better service.

No strings, no small print and no catches - we guarantee it.

Premium Credit is Premium Finance.That’s simply because we do it better than anyone else.

Get more - call 01372 746913 or email [email protected] www.premiumcredit.co.uk

Premium Credit is Premium Finance

Broker_PremiumCredit_Winter 19/10/06 2:36 pm Page 1

SCHEMES FOCUS

the broker winter 2006 27

BIBA’s travelinsurance schemeoffers among thewidest cover availablein the market.Shouldn’t you bemaking yourcustomers knowabout it? asksGraeme Trudgill

A new year is approaching and soare three new BIBA schemelaunches.

Full details will be provided in the nextissue of the broker, but to whet yourappetite, they’ll cover 24-hour licensedpremises and nightclubs, static andtouring caravans, and a scheme for a fastand expert response at the scene of anycommercial claim.

The focus in this issue, however, is ourtravel scheme, which was launched sixmonths ago and has already proved amassive success.

The BIBA Holiday Travel Insurancescheme is underwritten by Arch Europe, which may be a new name tosome, but has excellent security of A-with Standard & Poor’s and A- (Excellent)with AM Best.

FlexibleWe chose to work with Arch as they wereone of the few insurers to agree to ourstrict requirements of covering the moredifficult but important areas that arevaluable to brokers’ clients. This includes:cover for medical expenses, repatriation,personal accident and baggage claims inthe event of a terrorist attack. This is inaddition to one excess per person perclaim, higher than average limits of cover,the ability to insure older people andthose with pre-existing conditions. Wewere delighted recently when Archdemonstrated its flexible approach byproviding cover for a 90-year old who was

Travelling right

It remains a concern that manypeople still buy their travelinsurance from a travel agentwhen booking a holiday

‘‘’’

SCHEMES FOCUS

28 winter 2006 the broker

flying to Ireland to celebrate her birthday.If required, the cover can be sold via a

fully interactive internet-based system,which allows policies to be quoted, soldand issued online, in addition to thetraditional Pad system.

Arch will visit brokers that wish toprovide the scheme and set up theirinternet system – irrespective of a broker’s size or location. The insurer has also created a travel insuranceadvertisement template which enablesbrokers to customise it with their ownlogo and contact details. Theadvertisement is in Word format and isideal for placing in local newspapers.

Travel agentsIt remains a concern that many peoplestill buy their travel insurance from atravel agent when booking a holiday,despite a recent Which? report that thiscould lead to consumer detrimentbecause of either a lack of, or bad, advice.Additionally, travel agents are notregulated by the FSA.

The Which? investigation found thecover was also often overpriced and itsresearchers found that nearly two-thirdsof travel agents failed to ask aboutmedical histories, even thoughundisclosed pre-existing conditionscould invalidate a policy.

BIBA recently met with Ed Balls, theeconomic secretary to the Treasury, which has announced it will carry out areview into sales of travel insurance, andBIBA is assisting with this.

We are also collating a questionnairethat will demonstrate that consumerdetriment exists when consumers buyfrom a travel agent or tour operator. Weexpect that this will illustrate the benefitsof buying cover through a broker – andthis will be a useful message to pass ontoyour clients.

Quality coverIt could be argued that travel insurance issmall-ticket business, but clearly there isa need for people to benefit from qualitycover and advice.

We have found a big increase in thenumber of annual policies sold in the pasttwo years or so and these obviously bringin more sizeable premiums – in fact, thesenow outsell single-trip policies.

The BIBA Holiday Travel Insurancescheme is a market-leading product andhas been independently rated asproviding five-star cover by Defaqto,which also stated it was excellent forwinter sports.

The BIBA Holiday Travel Insurancescheme is available to all members withno minimum level of support.

To find out more, contact Dipesh Patel at Arch Europe on

020 7562 3128 or email at:[email protected] or GeoffChapman on 020 7562 3166 or email at:[email protected].

Graeme Trudgill is BIBA’s technicalservices manager

BIBA’s schemes: the full range

1 Accident, Sickness andUnemployment

2 BIBAlet3 Business Travel4 Commercial Combined5 Cyber-Liability6 Electronic Marine Cargo7 Excess Liability8 Haulage and LGV Insurance9 High Net Worth10 Home11 Loss Recovery Insurance12 Marine Cargo13 Motor14 Non Standard Property15 Personal Accident16 Holiday Travel17 Unoccupied Properties18 Web Based Directors and

Officers

BIBA facilities

19 Broker Continuity Planning20 Contract Law Services21 Financial Compliance Support22 Insurer Security Services23 Members’ Own PI Insurance24 Personal Lines Administration25 Premium Finance26 Telecoms27 Conflict Investigation Service

Don’t take our word for it…

Here’s what members say:

“Our company is signed up for the travel website, which is easy to use. Thismeans we can either issue quotes and policies for our clients or they can geta quote and buy online via a link on our website. We can also have the websitebanner customised with our company branding, which is a nice touch.”Duncan Hughes, Smart & Cook, West Wickham

“I like the fact that I can call the Arch underwriters direct and discuss individualcases. Recently, a director of one of our biggest commercial clients neededcover beyond the standard policy. We were able to agree special terms over the telephone and provide cover where we might not have been able to do so in the past.” Chris Frost, Chris Frost Insurance Services, Maidenhead

“In the light of recent terrorist threats, my clients are becoming increasinglyconcerned to source travel insurance that covers them in this situation to some degree. Terrorism cover is included in the Arch policies for medicalexpenses, personal accident and baggage – and this is a comfort.” Ian Dickinson, Brunsdon Group, Gloucester

Step up to the high life...We’ll help you take high net worth insurance in your stride with ourExecutive Home insurance policy.

With Executive Home, the sky’s the limit. And you’ll find no better guide to the high life than Sterling,the leading HNW household provider for professional brokers and intermediaries in the UK.

Go places with Sterling...Executive Home High Net Worth Team: T: 0845 2711300 F: 0845 2711468Agency Team: T: 01708 777 900 F: 01708 777948Address: 50 Kings Hill Avenue, Kings Hill, West Malling, Kent ME19 4JXE: executivequotes@sterlinginsurancegroup.comwww.sterlinginsurancegroup.com

Sterling Ad 1006 v2 20/10/06 15:56 Page 1

TECHNICAL BRIEFING

30 winter 2006 the broker

The insurance requirements forhaulage contractors and theoperators of large goods vehicles arecomplex and can be open tomisinterpretation.

Many motor insurers will avoid riskswhere hazardous or dangerous goods willbe carried, which could include industrialchemicals, petrol/oils, explosives, acidsand corrosives. Those insurers that canaccommodate such motor business oftenset a reduced limit in respect of third-partyproperty damage claims attributing to thecarriage of hazardous goods.

Where a £5 million third-party propertydamage limit applies, brokers may find arestriction down to £1 million and in somecircumstances, £250,000, for third-partyproperty damage claims relating to thecarriage of hazardous goods.

It is possible to arrange excess third-party property damage motor liabilityinsurance, for example providing £4 million in excess of the primary£1 million for any one incident wherehazardous goods are involved.