Embed Size (px)

Citation preview

2017 L&G Pathway Funds For Investment Professionals

The L&G Pathway FundsA flexible way to achieve individual retirement goals

Pathway Funds are the target date fund range from the UK’s leading provider of pension scheme solutions

2

2017 L&G Pathway Funds

A new freedom The UK pension industry is undergoing a revolution. First announced in 2014, the government’s new ‘Freedom and choice’ for pensions allows much greater flexibility in the use of retirement savings. These landmark changes mean getting to grips with a much more flexible, but also more complex and uncertain retirement landscape. Finding the right solution to take defined contribution (DC) pension scheme members to, and through, retirement, is now more crucial than ever.

Legal & General Investment Management (LGIM) is a leading provider of solutions for DC pension schemes in the UK and we continue to innovate as the market evolves. We build strong relationships with clients and consultants and use these partnerships to drive product innovation and systems development. Our extensive fund range reflects our focus on delivering what our clients need, and this approach ensures we remain a leading UK DC provider.

LEGAL & GENERAL INVESTMENT MANAGEMENTLegal & General Investment Management is one of Europe’s largest asset managers1 and a major global investor, with total assets of £902 billion2. We work with a wide range of global clients, including pension schemes, sovereign wealth funds, fund distributors and retail investors.

Throughout the past 40 years we have built our business through understanding what matters most to our clients and transforming this insight into valuable, accessible investment products and solutions. We provide investment expertise across the full spectrum of asset classes including fixed income, equities, commercial property and cash. Our capabilities range from index-tracking and active strategies to multi-asset, liquidity management and liability-based risk management solutions.

• Largest manager of UK pension fund assets

• £52bn DC AUM3

• DC Investment Innovation of the Year

For defined contribution pension schemes

AN AWARD WINNING MANAGERThere is more to success than assets under management. We put our clients at the heart of everything we do, and this drives our approach from investment management to product development and client service. The success of this philosophy has been regularly recognised with numerous industry awards.

WINNER WINNER2016Investment Manager

of the Year

BEST DEFAULT FUND STRATEGY 2015

GPP PROVIDER OF THE YEAR 2015

1: IPE research 2016 - top 400 survey2: LGIM internal data as at 31 December 2016. These figures include assets managed by LGIMA, an SEC Registered Investment Advisor. Data includes derivative positions and advisory assets. 3: As at 31 December 2016, including LGIMA.

For defined contribution pension schemes

3

2017 L&G Pathway Funds

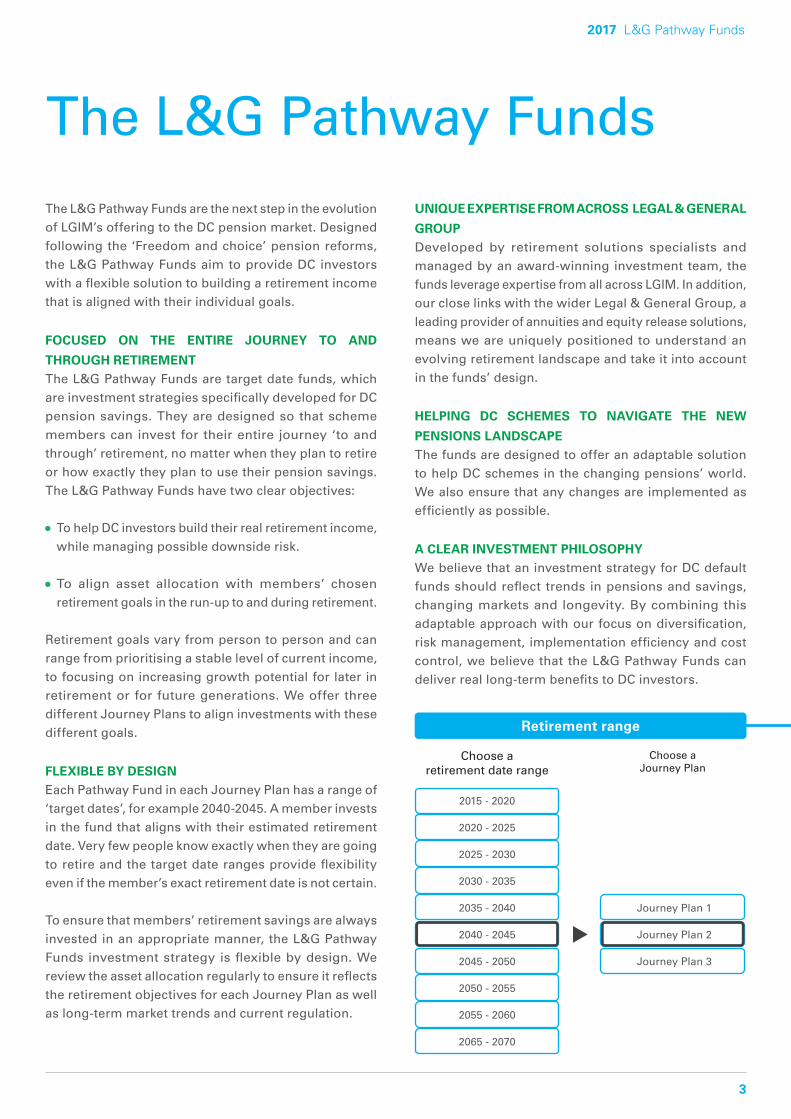

The L&G Pathway Funds

Retirement range

The L&G Pathway Funds are the next step in the evolution of LGIM’s offering to the DC pension market. Designed following the ‘Freedom and choice’ pension reforms, the L&G Pathway Funds aim to provide DC investors with a flexible solution to building a retirement income that is aligned with their individual goals.

FOCUSED ON THE ENTIRE JOURNEY TO AND

THROUGH RETIREMENTThe L&G Pathway Funds are target date funds, which are investment strategies specifically developed for DC pension savings. They are designed so that scheme members can invest for their entire journey ‘to and through’ retirement, no matter when they plan to retire or how exactly they plan to use their pension savings. The L&G Pathway Funds have two clear objectives:

• To help DC investors build their real retirement income, while managing possible downside risk.

• To align asset allocation with members’ chosen retirement goals in the run-up to and during retirement.

Retirement goals vary from person to person and can range from prioritising a stable level of current income, to focusing on increasing growth potential for later in retirement or for future generations. We offer three different Journey Plans to align investments with these different goals.

FLEXIBLE BY DESIGNEach Pathway Fund in each Journey Plan has a range of ‘target dates’, for example 2040-2045. A member invests in the fund that aligns with their estimated retirement date. Very few people know exactly when they are going to retire and the target date ranges provide flexibility even if the member’s exact retirement date is not certain.

To ensure that members’ retirement savings are always invested in an appropriate manner, the L&G Pathway Funds investment strategy is flexible by design. We review the asset allocation regularly to ensure it reflects the retirement objectives for each Journey Plan as well as long-term market trends and current regulation.

UNIQUE EXPERTISE FROM ACROSS LEGAL & GENERAL

GROUPDeveloped by retirement solutions specialists and managed by an award-winning investment team, the funds leverage expertise from all across LGIM. In addition, our close links with the wider Legal & General Group, a leading provider of annuities and equity release solutions, means we are uniquely positioned to understand an evolving retirement landscape and take it into account in the funds’ design.

HELPING DC SCHEMES TO NAVIGATE THE NEW

PENSIONS LANDSCAPEThe funds are designed to offer an adaptable solution to help DC schemes in the changing pensions’ world. We also ensure that any changes are implemented as efficiently as possible.

A CLEAR INVESTMENT PHILOSOPHYWe believe that an investment strategy for DC default funds should reflect trends in pensions and savings, changing markets and longevity. By combining this adaptable approach with our focus on diversification, risk management, implementation efficiency and cost control, we believe that the L&G Pathway Funds can deliver real long-term benefits to DC investors.

Choose a retirement date range

Choose a Journey Plan

2015 - 2020

2020 - 2025

2025 - 2030

2030 - 2035

2035 - 2040

2045 - 2050

2050 - 2055

2055 - 2060

2065 - 2070

2040 - 2045

Journey Plan 1

Journey Plan 2

Journey Plan 3

4

2017 L&G Pathway Funds

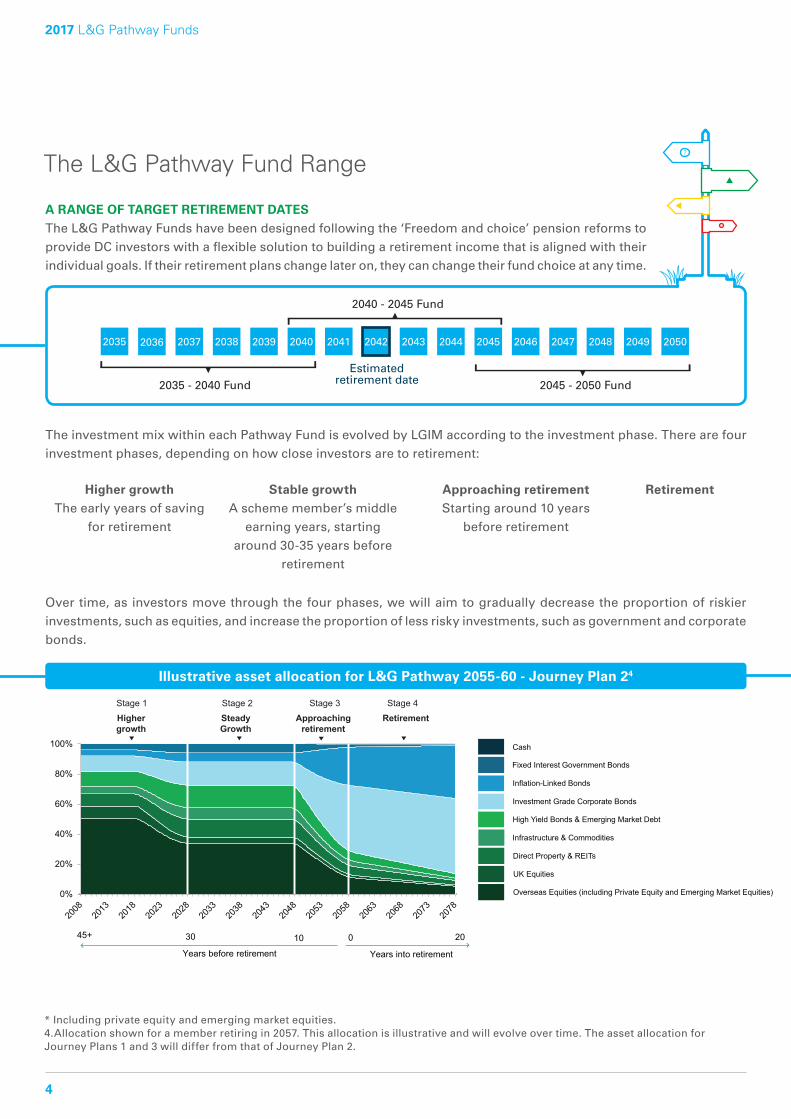

The L&G Pathway Fund Range

A RANGE OF TARGET RETIREMENT DATES The L&G Pathway Funds have been designed following the ‘Freedom and choice’ pension reforms to provide DC investors with a flexible solution to building a retirement income that is aligned with their individual goals. If their retirement plans change later on, they can change their fund choice at any time.

2040 - 2045 Fund

2045 - 2050 Fund2035 - 2040 FundEstimated

retirement date

2036 2049204820472046204520442043204220412040203920382037 20502035

The investment mix within each Pathway Fund is evolved by LGIM according to the investment phase. There are four investment phases, depending on how close investors are to retirement:

Over time, as investors move through the four phases, we will aim to gradually decrease the proportion of riskier investments, such as equities, and increase the proportion of less risky investments, such as government and corporate bonds.

Higher growth The early years of saving

for retirement

Stable growth A scheme member’s middle

earning years, starting around 30-35 years before

retirement

Approaching retirement Starting around 10 years

before retirement

Retirement

* Including private equity and emerging market equities.4.Allocation shown for a member retiring in 2057. This allocation is illustrative and will evolve over time. The asset allocation for Journey Plans 1 and 3 will differ from that of Journey Plan 2.

Illustrative asset allocation for L&G Pathway 2055-60 - Journey Plan 24

-50 -40 -30 -20 -10 0 10 20

0%

20%

40%

60%

80%

100%

High Yield Bonds & Emerging Market Debt

Cash

Fixed Interest Government Bonds

Investment Grade Corporate Bonds

Inflation-Linked Bonds

Infrastructure & Commodities

Direct Property & REITs

UK Equities

Overseas Equities (including Private Equity and Emerging Market Equities)

45+ 30 10 0 20

Years into retirementYears before retirement

Stage 1

-Higher growth

Stage 2

Steady Growth

-Stage 4

RetirementStage 3

Approaching retirement

5

2017 L&G Pathway Funds

5. Allocation shown for a member retiring in 2057. This allocation is illustrative and will evolve over time.

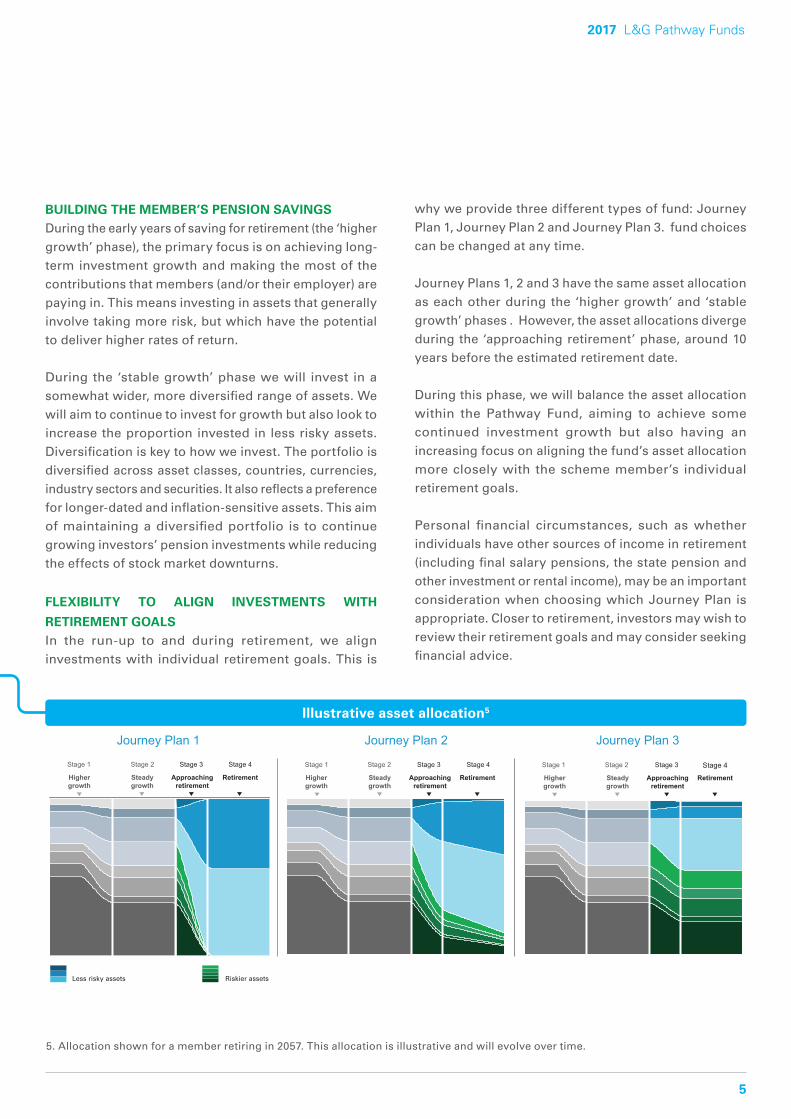

BUILDING THE MEMBER’S PENSION SAVINGSDuring the early years of saving for retirement (the ‘higher growth’ phase), the primary focus is on achieving long-term investment growth and making the most of the contributions that members (and/or their employer) are paying in. This means investing in assets that generally involve taking more risk, but which have the potential to deliver higher rates of return.

During the ‘stable growth’ phase we will invest in a somewhat wider, more diversified range of assets. We will aim to continue to invest for growth but also look to increase the proportion invested in less risky assets. Diversification is key to how we invest. The portfolio is diversified across asset classes, countries, currencies, industry sectors and securities. It also reflects a preference for longer-dated and inflation-sensitive assets. This aim of maintaining a diversified portfolio is to continue growing investors’ pension investments while reducing the effects of stock market downturns.

FLEXIBILITY TO ALIGN INVESTMENTS WITH

RETIREMENT GOALS In the run-up to and during retirement, we align investments with individual retirement goals. This is

why we provide three different types of fund: Journey Plan 1, Journey Plan 2 and Journey Plan 3. fund choices can be changed at any time.

Journey Plans 1, 2 and 3 have the same asset allocation as each other during the ‘higher growth’ and ‘stable growth’ phases . However, the asset allocations diverge during the ‘approaching retirement’ phase, around 10 years before the estimated retirement date.

During this phase, we will balance the asset allocation within the Pathway Fund, aiming to achieve some continued investment growth but also having an increasing focus on aligning the fund’s asset allocation more closely with the scheme member’s individual retirement goals.

Personal financial circumstances, such as whether individuals have other sources of income in retirement (including final salary pensions, the state pension and other investment or rental income), may be an important consideration when choosing which Journey Plan is appropriate. Closer to retirement, investors may wish to review their retirement goals and may consider seeking financial advice.

Illustrative asset allocation5

Stage 1

Higher growth

Stage 2

Steady growth

Stage 4

Retirement

Stage 3

Approaching retirement

Journey Plan 1 Journey Plan 2 Journey Plan 3

Less risky assets Riskier assets

Stage 1

Higher growth

Stage 2

Steady growth

Stage 4

Retirement

Stage 3

Approaching retirement

Stage 1

Higher growth

Stage 2

Steady growth

Stage 4

Retirement

Stage 3

Approaching retirement

6

2017 L&G Pathway Funds

Choosing the right journey plan

DC investors will need to decide which Journey Plan is right for them. The following guide describes whom the different funds are aimed at in terms of retirement goals and what type of investments investors in each fund should feel comfortable holding.

JOURNEY PLAN 1This fund is aimed at investors who are willing to sacrifice some potential for investment growth in retirement, in order to seek greater stability in their retirement income. To achieve this greater stability, an individual choosing this fund is likely to purchase an annuity when they retire, which gives a guaranteed lifetime income, or invest primarily in cash and bond investments.

WHAT HAPPENS WHEN SCHEME MEMBERS RETIRE?During retirement, the Pathway Funds will continue to be managed by LGIM. The asset allocation within Journey Plans 1 and 2 will aim to evolve further as retirement progresses, either through a changing split between ‘more risky’ and ‘less risky’ assets, or a changing asset allocation in these two categories. Journey Plan 3 will aim to stay invested in a wide range of investments, aiming to deliver long-term investment growth.

The range of options available in retirement has broadened over recent years due to pension reforms introduced by the government. Members can choose to stay invested in their chosen fund, move investments to another investment product or pension investment provider, withdraw all their savings as cash (which may have tax implications), or choose to buy an annuity. Should scheme members wish to take income from their pension savings, they can choose to either withdraw one or more cash lump sums, or take a regular income.

All three Journey Plans are designed for flexibility around retirement options and allow all the options above. Of course, available options may change if regulations change again. Pension Wise, a free and impartial government service, provides information and guidance around retirement options. Members may also consider taking independent financial advice.

JOURNEY PLAN 2Investors should note that Journey Plan 2 is the ‘default’ fund, designed for those who do not specifically choose Journey Plan 1 or 3. Individuals in this bracket are likely to hold some lower-risk investments in retirement such as cash, bonds or an annuity, while also allocating some money to higher-risk assets such as equities, property and alternative investments.

JOURNEY PLAN 3This fund is aimed at investors who are comfortable taking a higher level of investment risk with their pension savings in retirement, in pursuit of a higher level of return. These individuals are unlikely to purchase an annuity in the early years of their retirement and are more likely to invest their pension savings in a wide range of assets including equities, property, bonds and alternative investments.

1

3

2

7

2017 L&G Pathway Funds

SCALEWe are the UK’s largest manager of pension fund assets. Our success has been built on providing products and services that meet our clients’ needs.

COMBINED EXPERTISE Our in-house specialists include dedicated economists, strategists and fund managers. Direct access to cost-effective index funds, genuinely diversified solutions, market-leading de-risking solutions and low-cost execution enables us to implement the investment strategy efficiently.

A UNIQUE UNDERSTANDING OF RETIREMENT NEEDSWe have significant experience in providing market-leading retirement solutions.

In 2014, we launched the UK’s first investment fund designed for the new income drawdown world – the award-winning Retirement Income Multi Asset Fund. Collaboration with Legal & General Group, a leading provider of annuities and equity release solutions, makes us uniquely positioned to understand retirement-related investment needs.

INSTITUTIONAL-QUALITY RISK MANAGEMENT We are award-winning providers of risk management and de-risking solutions.

We manage bespoke asset allocation and de-risking mandates for some of the UK’s largest pension schemes.

Why invest with LGIM?

1

2

3

4

CONTACT US

For further information about the L&G Pathway Funds or our wider investment capabilities please contact your

usual LGIM representative or Rita Butler-Jones - Head of DC Sales on:

07342 062945 [email protected] lgim.com

Important Information

Investing in financial markets exposes investors to risk. These funds invest in a wide range of asset classes, predominantly equities and fixed income, typically by investing in other funds. Equities (shares of companies) have a higher risk of being volatile (i.e. going up and down) than most other asset types, particularly in the short term. The funds’ fixed income exposure – usually corporate and government bonds – is particularly sensitive to trends in interest rate movements. The value of the funds’ exposure to this asset class is likely to fall when these interest rates rise (such falls may be more pronounced in a low nominal interest rate environment). The financial strength of a company or government issuing a fixed interest security determines their ability to make some or all of the payments due. If this financial strength weakens, the chances of them not making payments increases and this will reduce the value of the funds’ exposure. The funds may also hold assets in currencies that are not denominated in sterling. If the value of these currencies falls compared to sterling this may cause the funds’ value to go down.

While the funds’ broad diversification aims to lower risk, each asset class has risks that may impact the value of the fund. Any objective or target will be treated as a target only and should not be considered as an assurance or guarantee of performance of the funds or any part of these. The asset allocation of the funds and therefore the risk profile may change over time due to the nature of the product or to meet changes to legislation and other market developments. There will be transaction costs associated with maintaining and switching between asset distributions. The funds are designed to be held until the cohort date range selected at the initial investment. If the investors target retirement date changes there may be other more relevant cohort ranges available.

The value of the funds can go down as well as up.

This document should not be taken as an invitation to deal in Legal & General investments or any of the stated stock markets. Legal & General Assurance (Pensions Management) Limited (“PMC”) is a life insurance company and carries on the business using a linked policy (“the policy”). The policy is divided into a number of sections (“the funds” or “PF Sections”). Legal & General Investment Management Limited provides investment and marketing services to PMC. PMC is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority

Legal & General Investment Management is authorised and regulated by the Financial Conduct Authority.

To ensure quality of service and for the protection of all parties, telephone calls may be recorded.

© 2017 Legal & General Investment Management. All rights reserved. No part of this document may be reproduced in whole or in part without the prior written consent of Legal & General Investment Management.

M0606