Embed Size (px)

Citation preview

The Investment Environment for Property/Casualty

Insurers

Impact of Volatility and Low Yields on P/C Insurer Investment Decisions

Insurance Information Institute

June 28, 2005

Robert P. Hartwig, Ph.D., CPCU, Senior Vice President & Chief EconomistInsurance Information Institute 110 William Street New York, NY 10038

Tel: (212) 346-5520 Fax: (212) 732-1916 [email protected] www.iii.org

Presentation Outline

• P/C Insurance Financial OverviewProfitability

Wall Street Perspective

Underwriting Performance

• Investment Performance:The Low Yield Conundrum

INVESTMENTS:

The Low Return Conundrum:Enforcer of Market

Discipline?

Property/Casualty Insurance Industry Investment Gain*

$ Billions

$35.4

$42.8$47.2

$52.3

$44.4

$36.0

$45.3$48.9

$56.9$51.9

$57.9

$0

$10

$20

$30

$40

$50

$60

94 95 96 97 98 99 00 01 02 03 04

*Investment gains consist primarily of interest, stock dividends and realized capital gains and losses.Source: Insurance Services Office; Insurance Information Institute.

Investment gains are rising but are still nearly 15% below

their 1998 peak

$0

$9

$18

$27

$36

$45

75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04

Net Investment Income

History

1997 Peak = $41.5B

2000= $40.7B

2001 = $37.7B

2002 = $37.2B

2003 = $38.7B

2004 = $39.6B

$ B

illi

ons

Growth History

2002: -1.3%

2003: +3.9%

2004E: +2.4%

Source: A.M. Best, ISO, Insurance Information Institute

US P/C Net Realized Capital Gains,1990-2004 ($ Millions)

$2,880

$4,806

$9,893

$1,664

$5,997

$9,244$10,808

$18,019

$13,016

$16,205

$6,631

-$1,214

$6,610

$9,298$9,818

-$5,000

$0

$5,000

$10,000

$15,000

$20,000

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04Sources: A.M. Best, ISO, Insurance Information Institute.

Realized capital gains rebounded strongly in

2003/4 but are 48% below their 1998 peak

-30%

-20%

-10%

0%

10%

20%

30%

40%

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

Source: Ibbotson Associates, Insurance Information Institute. *Through June 27, 2005.

Total Returns for Large Company Stocks: 1970-2005*

2003/4 were the first consecutive gains since 1999

S&P 500 was up 9% in 2004. Fears of higher interest rates, inflation, the falling dollar, resurgent oil prices are concerns in 2005

2005

0%

2%

4%

6%

8%

10%

12%

14%

16%

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

*

3-Month T-Bill 1-Yr. T-Bill 10-Year T-Note

Interest Rates: Lower Than They’ve Been in Decades, But…

Source: Board of Governors, Federal Reserve System; Insurance Info. Institute *As of 6/23/05.

Lower bond yields were the primary driver behind weak investment income in recent years, with the 10-year note reaching a 45-year low in 2003 and falling again in 2005

Higher ST rates as Fed tightens.

Just 57bp between 1-yr & 10-yr yields*

3.5%3.6%3.7%3.8%3.9%4.0%4.1%4.2%4.3%4.4%4.5%4.6%4.7%4.8%4.9%5.0%

Jan-

04

Feb

-04

Mar

-04

Apr

-04

May

-04

Jun-

04

Jul-

04

Aug

-04

Sep-

04

Oct

-04

Nov

-04

Dec

-04

Jan-

05

Feb

-05

Mar

-05

Apr

-05

May

-05

Jun-

05

10-Year Treasury Yields Remain Low and Are Falling*

Source: Board of Governors, Federal Reserve System; Insurance Info. Institute *As of 6/24/05.

Persistently low interest rates on the 10-year Treasury is a

major impediment to investment income growth

Eight rate hikes by the Fed since June 2004 (9th like July 1) have lifted

ST rates, but not LT yields

Portfolio Allocation

Progressively More Conservative

P/C Insurance Industry Investment Portfolio, 2003

Source: 2005 Insurance Fact Book, Insurance Information Institute from the NAIC Annual Statement Database.

Bonds66.3%

Common Stock17.7%

Preferred Stock1.6%Mortgage

Loans0.3%

Other4.8%

Cash & ST Inv.

9.3%

P/C insurers portfolio is very conservatively

invested, with 2/3 of invested assets held as bonds—mostly munis,

high-grade corporate bonds and US Treasury

securities

US Insurers’ Asset Allocation, 1992-2003 (%)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1992 1994 1996 1998 2000 2003

Other

Cash & short-term assets

Loans

Bonds

Shares (Stock)

Real estate

Includes separate accounts. “Loans” include mortgage loans.

Source: Swiss Re, Sigma No. 5/2002; 2005 P/C Fact Book, Insurance Information Institute.

Holdings of bonds and cash & short-term securities have increased substantially since 2000.

Flat Yield Curve

Insurers Are Marooned at Short End of Yield Curve

0%

1%

2%

3%

4%

5%

6%

1m 3m 6m 1yr 2yr 3yr 5yr 7yr 10yr 20yr

Jun-04 Dec-04 Jun-05*

The Treasury Yield CurveHas Become Very Flat

Source: Board of Governors, Federal Reserve System; Insurance Information Institute. *As of 6/23/05.

“Among the biggest surprises of the past year has been the pronounced decline in long-term

interest rates on U.S. Treasury securities despite a 2-percentage point increase in the federal funds

rate. This is clearly without recent precedent.”

-Fed Chairman Alan Greenspan before the Joint Economic Committee of Congress, June 9, 2005

December 2004

June 2004

June 2005

Proportion of P/C Portfolio Invested in Cash and ST Securities

Source: A.M. Best; Insurance Information Institute

6.41%5.64% 5.26%

5.81%

4.08%

5.30% 5.54%

8.47%9.30%

10.00%

0%

2%

4%

6%

8%

10%

12%

95 96 97 98 99 00 01 02 03 04E

Holdings of cash and short-term securities has more than doubled since 1999, reflecting interest rate risk of going long

Proportion of P/C Bond Portfolio With Maturities of 1 Year or Less

Source: A.M. Best; Insurance Information Institute

10.7%

12.4%12.3%11.9%

12.5%

9.9%

12.3%

11.1%

13.8%14.4%

15.0%

8%

9%

10%

11%

12%

13%

14%

15%

16%

94 95 96 97 98 99 00 01 02 03 04E

Holdings of bonds with maturities of 1 year or less are up 50% since 1999, reflecting interest rate risk of going long

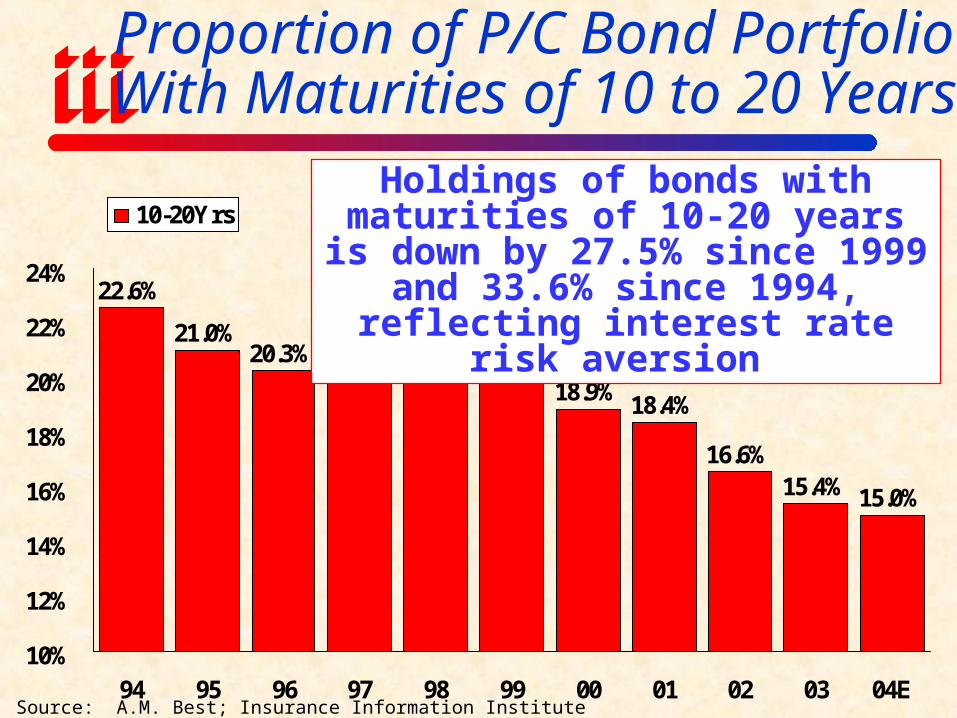

Proportion of P/C Bond Portfolio With Maturities of 10 to 20 Years

Source: A.M. Best; Insurance Information Institute

22.6%

21.0%20.3% 20.7% 20.7% 20.7%

18.9% 18.4%

16.6%15.4% 15.0%

10%

12%

14%

16%

18%

20%

22%

24%

94 95 96 97 98 99 00 01 02 03 04E

10-20YrsHoldings of bonds with maturities of 10-20 years is down by 27.5% since

1999 and 33.6% since 1994, reflecting interest rate risk aversion

Maturity Distribution of P/CBond Portfolio, 1999–2004E

Source: A.M. Best; Insurance Information Institute

12.3% 11.1% 13.8% 14.4% 15.0%

27.4% 28.6% 28.9% 29.8% 30.5%

29.4% 31.0% 29.5% 31.3% 31.0%

18.9% 18.4% 16.6% 15.4% 15.0%

12.0% 11.0% 11.2% 9.2% 8.5%

9.9%

26.0%

31.6%

20.7%

11.8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

99 00 01 02 03 04E

1-Yr or Less 1-5Yrs 5-10Yrs 10-20Yrs Over 20Yrs

Maturity Distribution of P/CBond Portfolio, 1999–2004E

Source: A.M. Best; Insurance Information Institute

39.8% 39.6% 42.7% 44.2% 45.5%

27.4% 28.6% 28.9% 29.8% 30.5%

30.8% 29.4% 27.8% 24.5% 23.5%

36.0%

26.0%

32.5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

99 00 01 02 03 04E

5 Yrs or Less 5-10Yrs Over 10 Years

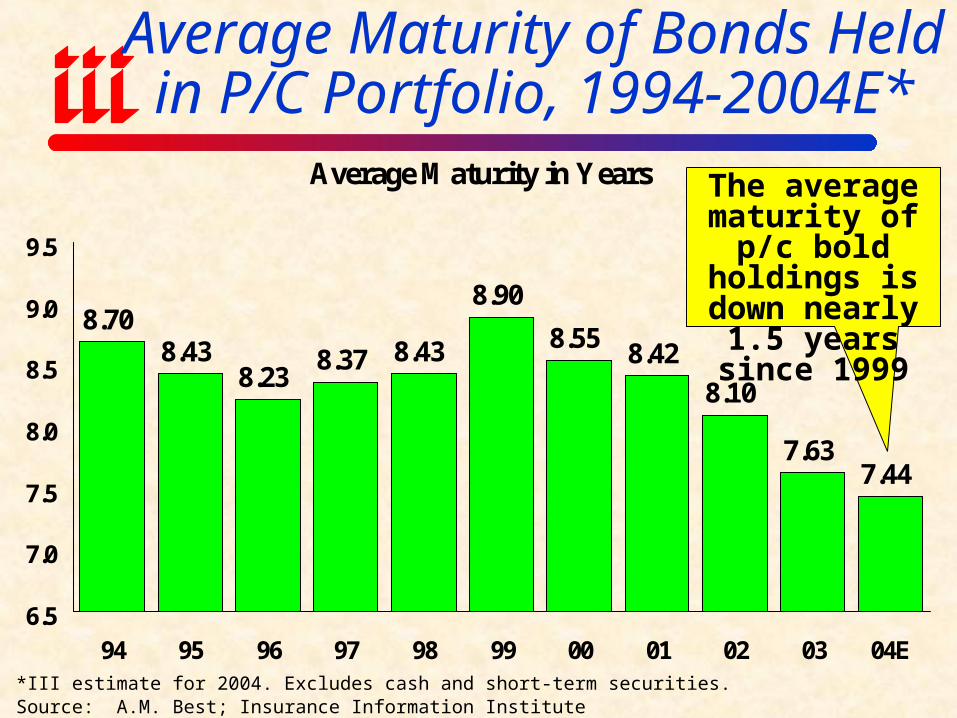

Average Maturity of Bonds Heldin P/C Portfolio, 1994-2004E*

*III estimate for 2004. Excludes cash and short-term securities.Source: A.M. Best; Insurance Information Institute

Average Maturity in Years

8.708.43

8.238.37 8.43

8.90

8.558.42

8.10

7.637.44

6.5

7.0

7.5

8.0

8.5

9.0

9.5

94 95 96 97 98 99 00 01 02 03 04E

The average maturity of p/c bold holdings is down nearly 1.5 years since 1999

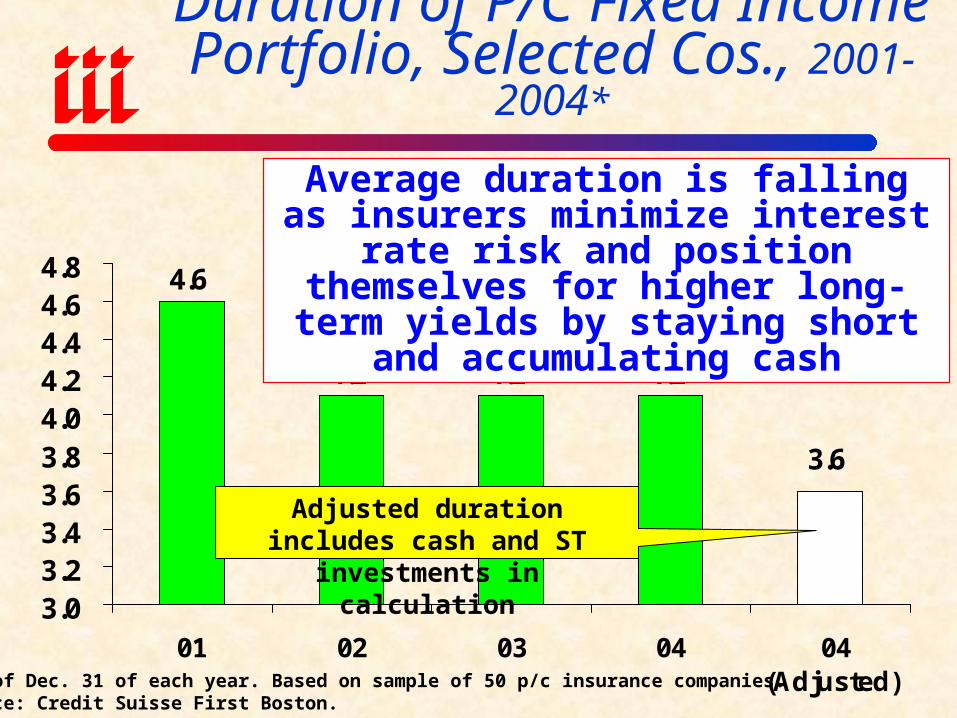

Duration of P/C Fixed Income Portfolio, Selected Cos., 2001-2004*

4.6

4.1 4.1 4.1

3.6

3.03.23.43.63.84.04.24.44.64.8

01 02 03 04 04(Adjusted)*As of Dec. 31 of each year. Based on sample of 50 p/c insurance companies.

Source: Credit Suisse First Boston.

Average duration is falling as insurers minimize interest rate risk and position

themselves for higher long-term yields by staying short and accumulating cash

Adjusted duration includes cash and ST investments in calculation

Reasons for Persistently Low Long-Term Interest Rates in the US

• Expectation of Future Economic WeaknessWeakness may be global in scale Inflation fears for the longer-term are therefore subdued

• Foreign Central Bank Purchases of US TreasurysEspecially China & other Asian central banks

• Falling Interest Rates in Other Major EconomiesOther central banks cutting rates (or holding constant)

• Excess of Savings Elsewhere in World Relative to USDirect result of massive US trade imbalancesMoney comes back to US in form of purchases of US bonds

• Weakness in Euro; Crisis of Confidence in EURotation out of Euro and back into the US dollar

Rest of World

US Current Account Deficit, Foreign Savings Help Keep US Interest Rates Low

United States

IOUs

GOODS & SERVICES

Foreigners buy US fixed income securities, keeping bond prices

high and interest rates low

Net Savings from ROW

What Could Force US Long-Term Interest Rates Upward?

• Expectations of Stronger Economic Growth Currently no reason for such expectation in US or abroad

• Building Inflationary Expectations Oil at $60/barrel? $100/barrel? High global commodities prices

• Rising Interest Rates Abroad UNLIKELY: Other central banks want to stimulate their economies

• Reduction of Current Acct. Deficit (now more than 6% of GDP) Reduces flow of cash back to US in form of purchases of US bonds

• Chinese Shift to Purchase of Real Assets Unocal, Maytag, IBM P/C; (Shift from Treasurys—currently hold $660B)

Get readily for lots of China bashing & protectionism

• End of Chinese Currency Peg Theoretically makes Chinese goods more expensive improving US trade

situation Conventional wisdom on impact is likely overblown

6.0%

3.5%

1.6%

1.0% 1.

4%

3.2%

4.0% 4.

2%

4.1% 4.2% 4.3%

4.2% 4.

4%

6.0%

5.0%

4.6%

4.0% 4.

3% 4.7%

5.3% 5.

5%

5.5%

5.5%

5.5% 5.6%

5.5%

0%

1%

2%

3%

4%

5%

6%

7%

00 01 02 03 04 05F 06F 07F 08F 09F 10F 11F 12-16F

3-Month T-Bill 10-Year T-Note

Interest Rate Forecast,2005F-2016F

Source: Board of Governors, Fed. Reserve System; Blue Chip Economic Indicators as of March 2005.

Long/Short-term rates are expected to rise and then stabilize

Insurance Information Institute On-Line

If you would like a copy of this presentation, please give me your business card with e-mail address