Embed Size (px)

Citation preview

1

The Institute of Chartered Accountants of Sri Lanka

CAB I

Supplement of Financial Accounting

2

Areas need to be discussed

1. Changes in the conceptual framework for financial reporting

i. Changes in the Objectives of general purpose financial statements

ii. Changes in the Qualitative characteristics of useful financial information

iii. Changes in the Identification of the Underlining accounting assumption

iv. Changes in the Elements of financial statements

2. Changes in the presentation of financial statements

3. Changes in the selected Accounting Standards [LKAS /IAS]

3

1.The conceptual framework

This Conceptual Framework is not a Sri Lanka Accounting Standard and hence does not define

standards for any particular measurement or disclosure issue. Further the Conceptual

Framework do not overrides any specific Sri Lanka Accounting Standard in any time. There may

be a few numbers of instances that a conflict between the Conceptual Framework and a Sri

Lanka Accounting Standard. In those cases where there is a conflict, the requirements of the Sri

Lanka Accounting Standard prevail over those of the Conceptual Framework. These conflicts

between the Conceptual Framework and Sri Lanka Accounting Standards will solve as this

Conceptual Framework is used in developing the future Standards and in the reviewing of

existing Standards.

Areas included in the conceptual framework for financial reporting.

The following are included in the conceptual framework for financial reporting.

I. Objectives of general purpose financial statements

II. Qualitative characteristics of useful financial information

III. Identification of the Underlining accounting assumption

IV. Elements of financial statements

The objective of general purpose financial reporting

The objective of general purpose financial reporting is to provide financial information about the

reporting entity that is useful to existing and potential investors, lenders and other creditors in

making decisions about providing resources to the entity. Those decisions involve buying, selling

or holding equity and debt instruments, and providing or settling loans and other forms of

credit.

Qualitative Characteristics of useful Financial Information

These characteristics are the attributes that makes the financial information useful to the

existing and potential investors, lenders and other creditors for making decisions about the

reporting entity on the basis of financial information in its financial report (financial

information).

The framework identifies basically two types of characteristics which are the

1. Fundamental characteristics

2. Enhancing characteristics

4

If financial information is to be useful, it must be relevant and faithfully represent what it

purports to represent are the Fundamental characteristics. The usefulness of financial

information is enhanced if it is comparable, verifiable, timely and understandable and these are

considered as the enhanced characteristics.

Fundamental qualitative characteristics

The fundamental qualitative characteristics are relevance and faithful representation.

Relevance

Information in financial information is relevant when it influences the economics decisions of

users. To full fill the quality of relevance the user should be in the position to take the economics

decisions by depending on the information provided in the financial statements.

It can do that both by

• Relevance can be help the economic decision makers to evaluate the past, present,or future

events relating to an enterprise and

• Confirm or correct past evaluations they have made.

Materiality is the component of relevance. Information is treated as material if the omission or

misstatement could influence the economic decisions of the user.

Timeliness is another components of relevance to be useful, information must be provided to

users within the time period in which it is most likely to bear on their decisions.

Nature and the materiality of the information give and impact to the relevance of the

information. If the omission or the misstatement of particular event leads the users to change

the decisions taken by depending on the financial information, such facts are treated as

materiality. If the omission or misstatement does not give any impact for the users to change the

decisions such facts are not treated as material. There may be instances where the information is

not material, quantitatively it may be relevant due to the nature of and the statutory

requirements with regard to particular information.

Faithful representation

Financial reports represent economic phenomena in words and numbers. To be useful, financial

information must not only represent relevant phenomena, but it must also faithfully represent

the phenomena that it purports to represent. To be a perfectly faithful representation, a

depiction would have three characteristics. It would be complete, neutral and free from error. Of

course, perfection is seldom, if ever, achievable. The Council’s objective is to maximize those

qualities to the extent possible.

5

A complete depiction includes all information necessary for a user to understand the

phenomenon being depicted, including all necessary descriptions and explanations. For example,

a complete depiction of a group of assets would include, at a minimum, a description of the

nature of the assets in the group, a numerical depiction of all of the assets in the group, and a

description of what the numerical depiction represents (for example, original cost, adjusted cost

or fair value). For some items, a complete depiction may also entail explanations of significant

facts about the quality and nature of the items, factors and circumstances that might affect their

quality and nature, and the process used to determine the numerical depiction.

Applying the fundamental qualitative characteristics

Information must be both relevant and faithfully represented if it is to be useful. Neither a

faithful representation of an irrelevant phenomenon nor an unfaithful representation of a

relevant phenomenon helps users make good decisions.

The most efficient and effective process for applying the fundamental qualitative characteristics

would usually be as follows

1. Identify an economic phenomenon that has the potential to be useful to users of the

reporting entity’s financial information.

2. Identify the type of information about that phenomenon that would be most relevant if it

is available and can be faithfully represented.

3. Determine whether that information is available and can be faithfully represented.

Enhancing qualitative characteristics

Comparability, verifiability, timeliness and understandability are qualitative characteristics that

enhance the usefulness of information that is relevant and faithfully represented. The enhancing

qualitative characteristics may also help determine which of two ways should be used to depict a

phenomenon if both are considered equally relevant and faithfully represented.

Comparability

Users must be able to compare financial statement of an enterprise through time in order to

identify trends in its financial position and performance. Users must also be able to compare the

financial statements of different enterprises in order to evaluate their relative financial position,

performance and changes in financial position. Hence, the measurement and display of the

financial effect of like truncations and other events must be carried out in a consistent way

through out and enterprise and over time for that enterprise and in a consistent way for

different enterprise.

6

Financial statements should provide the comparative figures to identify the trends in

profitability and the financial status. At least it is expected to present the previous years financial

statements for the comparison of the users. Further the comparison can be made even with the

other organizations. To get the maximum benefits of the comparison, financial information

should be prepared in accordance with the accounting standards. Further accounting standards

applied and the deviations from the accounting standards should also be disclosed clearly. Hence

comparison can be ensured by preparing the financial statements according to the Sri Lanka

Accounting Standards. This does not mean that the quality of presentation can not be improved

by changing the accounting policies applied in previous years. These changes can be made if the

change leads to enhance the quality of the financial statements and if the change and the reasons

for the changes are also clearly explained in the financial statements.

Normally it is not expected to maintain the above mentioned qualities 100% at the time but it is

advisable to take every effort to maintain the qualitative characteristics at a maximum level.

Objective of these qualitative characteristic is to maintain the quality level of financial

statements at a higher level.

Verifiability

Verifiability helps assure users that information faithfully represents the economic phenomena

it purports to represent. Verifiability means that different knowledgeable and independent

observers could reach consensus, although not necessarily complete agreement, that a particular

depiction is a faithful representation. Quantified information need not be a single point estimate

to be verifiable. A range of possible amounts and the related probabilities can also be verified.

Verification can be direct or indirect. Direct verification means verifying an amount or other

representation through direct observation, for example, by counting cash. Indirect verification

means checking the inputs to a model, formula or other technique and recalculating the outputs

using the same methodology.

Timeliness

Timeliness means having information available to decision-makers in time to be capable of

influencing their decisions. Generally, the older the information is the less useful it is. However,

some information may continue to be timely long after the end of a reporting period because, for

example, some users may need to identify and assess trends.

7

Understandability

Classifying, characterising and presenting information clearly and concisely makes it

understandable. Some phenomena are inherently complex and cannot be made easy to

understand. Excluding information about those phenomena from financial reports might make

the information in those financial reports easier to understand. However, those reports would

be incomplete and therefore potentially misleading.

Financial reports are prepared for users who have a reasonable knowledge of business and

economic activities and who review and analyse the information diligently. At times, even well-

informed and diligent users may need to seek the aid of an adviser to understand information

about complex economic phenomena.

Applying the enhancing qualitative characteristics

Enhancing qualitative characteristics should be maximized to the extent possible. However, the

enhancing qualitative characteristics, either individually or as a group, cannot make information

useful if that information is irrelevant or not faithfully represented.

Applying the enhancing qualitative characteristics is an iterative process that does not follow a

prescribed order. Sometimes, one enhancing qualitative characteristic may have to be

diminished to maximize another qualitative characteristic.

The cost constraint on useful financial reporting

Cost is a pervasive constraint on the information that can be provided by financial reporting.

Reporting financial information imposes costs, and it is important that those costs are justified

by the benefits of reporting that information. There are several types of costs and benefits to

consider.

Providers of financial information expend most of the effort involved in collecting, processing,

verifying and disseminating financial information, but users ultimately bear those costs in the

form of reduced returns. Users of financial information also incur costs of analyzing and

interpreting the information provided. If needed information is not provided, users incur

additional costs to obtain that information elsewhere or to estimate it.

8

Reporting financial information that is relevant and faithfully represents what it purports to

represent helps users to make decisions with more confidence. This results in more efficient

functioning of capital markets and a lower cost of capital for the economy as a whole. An

individual investor, lender or other creditor also receives benefits by making more informed

decisions. However, it is not possible for general purpose financial reports to provide all the

information that every user finds relevant. In applying the cost constraint, it is assesses whether

the benefits of reporting particular information are likely to justify the costs incurred to provide

and use that information. When applying the cost constraint in developing a proposed financial

reporting standard, it also seeks information from providers of financial information, users,

auditors, academics and others about the expected nature and quantity of the benefits and costs

of that standard. In most situations, assessments are based on a combination of quantitative and

qualitative information. Because of the inherent subjectivity, different individuals’ assessments

of the costs and benefits of reporting particular items of financial information will vary.

Therefore, it seeks to consider costs and benefits in relation to financial reporting generally, and

not just in relation to individual reporting entities. That does not mean that assessments of costs

and benefits always justify the same reporting requirements for all entities. Differences may be

appropriate because of different sizes of entities, different ways of raising capital (publicly or

privately), different users’ needs or other factors.

Underlying Assumption

Going concern

The financial statements are normally prepared on the assumption that an entity is a going

concern and will continue in operation for the foreseeable future. Hence, it is assumed that the

entity has neither the intention nor the need to liquidate or curtail materially the scale of its

operations; if such an intention or need exists, the financial statements may have to be prepared

on a different basis and, if so, the basis used is disclosed.

Elements of financial statements

Capital maintenance adjustments

The revaluation or restatement of assets and liabilities gives rise to increases or decreases in

equity. While these increases or decreases meet the definition of income and expenses, they are

not included in the income statement under certain concepts of capital maintenance. Instead

these items are included in equity as capital maintenance adjustments or revaluation reserves.

9

Concepts of capital

A financial concept of capital is adopted by most entities in preparing their financial statements.

Under a financial concept of capital, such as invested money or invested purchasing power,

capital is synonymous with the net assets or equity of the entity. Under a physical concept of

capital, such as operating capability, capital is regarded as the productive capacity of the entity

based on, for example, units of output per day.

The selection of the appropriate concept of capital by an entity should be based on the needs of

the users of its financial statements. Thus, a financial concept of capital should be adopted if the

users of financial statements are primarily concerned with the maintenance of nominal invested

capital or the purchasing power of invested capital. If, however, the main concern of users is

with the operating capability of the entity, a physical concept of capital should be used. The

concept chosen indicates the goal to be attained in determining profit, even though there may be

some measurement difficulties in making the concept operational.

Concepts of capital maintenance and the determination of profit

a) Financial capital maintenance. Under this concept a profit is earned only if the financial

(or money) amount of the net assets at the end of the period exceeds the financial (or

money) amount of net assets at the beginning of the period, after excluding any

distributions to, and contributions from, owners during the period. Financial capital

maintenance can be measured in either nominal monetary units or units of constant

purchasing power.

b) Physical capital maintenance. Under this concept a profit is earned only if the physical

productive capacity (or operating capability) of the entity (or the resources or funds

needed to achieve that capacity) at the end of the period exceeds the physical productive

capacity at the beginning of the period, after excluding any distributions to, and

contributions from, owners during the period.

The concept of capital maintenance is concerned with how an entity defines the capital that it

seeks to maintain. It provides the linkage between the concepts of capital and the concepts of

profit because it provides the point of reference by which profit is measured; it is a prerequisite

for distinguishing between an entity’s return on capital and its return of capital; only inflows of

assets in excess of amounts needed to maintain capital may be regarded as profit and therefore

as a return on capital. Hence, profit is the residual amount that remains after expenses

(including capital maintenance adjustments, where appropriate) have been deducted from

income. If expenses exceed income the residual amount is a loss.

10

The physical capital maintenance concept requires the adoption of the current cost basis of

measurement. The financial capital maintenance concept, however, does not require the use of a

particular basis of measurement. Selection of the basis under this concept is dependent on the

type of financial capital that the entity is seeking to maintain.

The principal difference between the two concepts of capital maintenance is the treatment of the

effects of changes in the prices of assets and liabilities of the entity. In general terms, an entity

has maintained its capital if it has as much capital at the end of the period as it had at the

beginning of the period. Any amount over and above that required to maintain the capital at the

beginning of the period is profit.

2. Changes in the presentation of financial statements

LKAS 1 Presentation of Financial Statements

Changes of the presentation of financial information can be summarized as follows and given

below are the components of a set of Financial Statements to be prepared for a business;

I. A statement of the financial position as at the end of the period.

II. A statement of the comprehensive Income for the period.

III. A statement of changes in equity for the period.

IV. A statement of Cash Flows for the period.

V. Notes comprising a summary of significant accounting policies and other

explanatory information.

Terminology presently been used New terminology to be used

Income Statement Comprehensive Income Statement and Other Comprehensive Income Statement

Balance Sheet Statement of Financial Position

11

Comprehensive income

Comprehensive income is the total non-owner change in equity for a reporting period. This

change encompasses all changes in equity other than transactions from owners and

distributions to owners. Most of these changes appear in the income statement. A few special

types of gains and losses are not shown in the income statement but as special items in

shareholder equity section of the balance sheet.

Since these comprehensive income items are not closed to retained earnings each period they

accumulate as shareholder equity items and thus are entitled “Other Comprehensive Income”

and is sometimes referred to as "OCI".

Other comprehensive income is a subsection in equity where "other comprehensive income" is

accumulated (summed or "aggregated").

The balance of OCI is presented in the Equity section of the Balance Sheet as is the Retained

Earnings balance, which aggregates past and current Earnings, and past and current Dividends.

Other comprehensive income

Other comprehensive income is the difference between net income as in the Income Statement

(Profit or Loss Account) and comprehensive income, and represents the certain gains and losses

of the enterprise not recognized in the P&L Account. It is commonly referred to as "OCI".

In practice, it comprises the following items:

1. Unrealized gains and losses on available for sale securities [LKAS 39 / IAS 39 – Financial

Instruments ]

2. Gains and losses on derivatives held as cash flow hedges (only for effective portions) [LKAS 39

/ IAS 39 – Financial Instruments]

3. Gains and losses resulting from translating the financial statements of foreign subsidiaries

(from foreign currency to the presentation currency) [LKAS 21 / IAS 21 — The Effects of

Changes in Foreign Exchange Rates],

4. Actuarial gains and losses on defined benefit plans recognized (Minimum pension liability

adjustments) [LKAS 19/ IAS 19 — Employee Benefits]

5. Changes in the revaluation surplus [LKAS 16 / IAS 16 - Property, Plant and Equipment].

12

While the OCI balance is presented in Equity section of the balance sheet, the annual accounting

entries, as flows, are presented sometimes in a Statement of Comprehensive Income. This

statement expands the traditional Income Statement beyond Earnings to include OCI in order to

present Comprehensive Income.

Under the revised IAS 1, all non-owner changes in equity (comprehensive income) must be

presented either in one Statement of comprehensive income or in two statements (a separate

income statement and a statement of comprehensive income).

LKAS 01 - Presentation of Financial Statements

Statement of financial position

31 December 2012

Assets

Non-current assets

Property, plant and equipment xxx

Intangible assets and goodwill xxx

Biological assets xxx

Trade and other receivables - xxx

Investment property xxx

Equity-accounted investees xxx

Other investments, including derivatives xxx

Deferred tax assets xxx

Employee benefits xxx

Total Non-current assets xxx

Current assets

Inventories xxx

Biological assets xxx

Other investments, including derivatives xxx

Current tax assets xxx

Trade and other receivables xxx

Prepayments xxx

Cash and cash equivalents xxx

Assets held for sale xxx

Total Current assets xxx

Total assets XXX

Equity

Share capital xxx

Share premium xxx

13

Reserves xxx

Retained earnings xxx

Total Equity attributable to owners of the Company xxx

Liabilities

Non-current liabilities xxx

Loans and borrowings xxx

Employee benefits xxx

Trade and other payables xxx

Deferred income/revenue xxx

Provisions xxx

Deferred tax liabilities xxx

Total Non-current liabilities xxx

Current liabilities

Bank overdraft xxx

Current tax liabilities xxx

Loans and borrowings xxx

Trade and other payables xxx

Deferred income/revenue xxx

Provisions xxx

Liabilities held for sale xxx

Total Current liabilities xxx

Total liabilities xxx

Total equity and liabilities xxx

Statement of comprehensive income

For the year ended 31 December 2012

Continuing operations Revenue xxx

Cost of sales xxx Gross profit xxx Other income xxx Selling and distribution expenses xxx Administrative expenses xxx Research and development expenses xxx Other expenses xxx

Results from operating activities xxx

Finance income xxx Finance costs xxx

Net finance costs xxx

14

Share of profit of equity-accounted investees, net of tax xxx

Profit before tax xxx

Tax expense xxx

Profit from continuing operations xxx

Discontinued operation xxx Profit (loss) from discontinued operation, net of tax xxx

Profit for the year xxx Other comprehensive income

Net change in fair value of available-for-sale financial assets xxx Net change in fair value of available-for-sale financial assets reclassified to profit or loss xxx Effective portion of changes in fair value of cash flow hedges xxx Net loss on hedge of net investment in foreign operation xxx Foreign currency translation differences – foreign operations xxx Foreign currency translation differences – equity-accounted investees xxx Defined benefit plan actuarial gains (losses) xxx Revaluation of property, plant and equipment xxx Tax on other comprehensive income xxx

Other comprehensive income for the year, net of tax xxx

Total comprehensive income for the year xxx

15

3.Changes in the selected Accounting Standards [LKAS /IAS]

LKAS 01 Presentation of Financial Statements

Existing Para Reference : Para 07 (d) & (f)

Replaced/ added paragraph : The components of other comprehensive income include :

(d) gains and losses from investments in equity instruments measured at fair value through

other comprehensive income in accordance with paragraph 5.7.5 of SLFRS 9 Financial

Instruments;

Example: Investments in Shares

Convertible preference shares

(f) for particular liabilities designated as at fair value through profit or loss, the amount of the

change in fair value that is attributable to changes in the liability's credit risk.

Example : Lease

Existing Para Reference : Para 69 (d)

Replaced/ added paragraph : Current Liabilities

An entity shall classify a liability as current when:

(d) it does not have an unconditional right to defer settlement of the liability for at least

twelve months after the reporting period. Terms of a liability that could at the option of

the counterparty, result in its settlement by the issue equity instruments do not affect its

classification.

Example : Debentures

Existing Para Reference : Para 123 (a)

Replaced/ added paragraph : [deleted]

16

LKAS 2 Inventories

Existing Para Reference : Para 2 (b)

Replaced/ added paragraph : (b) financial instruments (see LKAS 32 Financial

Instruments:Presentation and SLFRS 9 Financial Instruments); and

Example : Earlier LKAS 39 now it has renamed as SLFRS 9

LKAS 7 Statement of Cash Flows

Existing Para Reference : Para 2 (b)

Replaced/ added paragraph: The separate disclosure of cash flows arising from investing

activities is important because the cash flows represent the extent to which expenditures have

been made for resources intended to generate future income and cash flows. Only

expenditures that result in a recognised asset in the statement of financial position are

eligible for classification as investing activities. Examples of cash flows arising from

investing activities are:

(a) cash payments to acquire property, plant and equipment, intangibles and other long-term

assets. These payments include those relating to capitalised development costs and self

constructed property, plant and equipment;

(b) cash receipts from sales of property, plant and equipment, intangibles and other long-term

assets;

(c) cash payments to acquire equity or debt instruments of other entities and interests in joint

ventures (other than payments for those instruments considered to be cash equivalents or those

held for dealing or trading purposes);

17

(d) cash receipts from sales of equity or debt instruments of other entities and interests in joint

ventures (other than receipts for those instruments considered to be cash equivalents and those

held for dealing or trading purposes);

(e) Cash advances and loans made to other parties (other than advances and loans made by a

financial institution);

(f) Cash receipts from the repayment of advances and loans made to other parties (other than

advances and loans of a financial institution);

(g) cash payments for futures contracts, forward contracts, option contracts and swap contracts

except when the contracts are held for dealing or trading purposes, or the payments are

classified as financing activities; and

(h) Cash receipts from futures contracts, forward contracts, option contracts and swap contracts

except when the contracts are held for dealing or trading purposes, or the receipts are classified

as financing activities.

When a contract is accounted for as a hedge of an identifiable position the cash flows of the

contract are classified in the same manner as the cash flows of the position being hedged.

Example :property, plant and equipment,intangibles and other long-term assets;

18

LKAS 8 Accounting Policies, Changes in Accounting Estimates and Errors

Existing Para Reference: Para 53

Replaced/ added paragraph : Hindsight should not be used when applying a new accounting

policy to, or correcting amounts for, a prior period, either in making assumptions about what

management’s intentions would have been in a prior period or estimating the amounts

recognised, measured or disclosed in a prior period. For example, when an entity corrects a

prior period error in calculating its liability for employees’ accumulated sick leave in accordance

with LKAS 19 Employee Benefits, it disregards information about an unusually severe influenza

season during the next period that became available after the financial statements for the prior

period were authorised for issue. The fact that significant estimates are frequently required

when amending comparative information presented for prior periods does not prevent reliable

adjustment or correction of the comparative information.

19

LKAS 16 Property, Plant and Equipment

Assets

Tangible Non-Current Assets - All the assets are classified as Non-Current assets other than the

followings,

i. Realised (Sold /Consumed) in entity's normal operating cycle,

ii. Which are held for trading

iii. Like cash/ cash equivalent (unless restricted from being exchanged)

iv. Expected to realize within 12 months after SOFP date

The above are known as current assets

Examples for Tangible non-current assets

1. Property, Plant and Equipment, e.g. Building, Machinery and computers used for

business. Traditionally these assets are called fixed assets. These were covered from the

LKAS 16, IAS 16 Property, Plant and Equipment Standard

2. Investment properties, e.g. building given on rent plot of land held for capital

appreciation only. These were covered from the IAS 40 Investment Property.

3. Property, Plant and Equipment classified as held for sale, IFRS 5 Non current Assets held

for sale and discontinued operations

LKAS 16 - Property, Plant and Equipment standard shall not be applicable for:

i. Non-current assets held for sale (SLFRS 5)

ii. Discontinued operations (SLFRS 5)

iii. Biological assets (LKAS 41)

iv. Exploration of mineral assets (SLFRS 6)

v. Mineral rights and reserves such as oil, gas

Articles which can be recognition as Property, Plant and Equipment when :

i. It is probable that future economic benefits associated with the item will

flow to the entity and

ii. The cost of the item can be measured reliably

Both the above conditions should be met in order to recognize an item as an asset

20

Initial Recognition of Non-Current Assets

Measurement of Non-Current Assets at recognition:

1. An item of property, plant and equipment that qualifies for recognition as an asset

shall be measured at cost. Elements of cost are Purchase price and related taxes

and duties, Any cost directly attributable to bringing the asset to the location and

the condition, Initial estimate of the costs of dismantling and removing the item

and restoring the site

2. Measurement of costs: The cost of an item of PPE is the cash price equivalent at

the recognition date and Specific borrowing costs should be capitalised in line

with LKAS 23

Measurement after recognition:

1. Cost model : After recognition as an asset an item of PPE asset, should be carried at cost

less accumulated depreciation and any accumulated impairment losses.

2. Re-valuation model : After recognition as an asset an item of PPE asset, whose fair value

can be measured reliably shall be carried at a revalued amount (being its fair value at the

date of the re-valuation) less accumulated depreciation and any accumulated impairment

losses

Re-valuation of Property, Plant & Equipment

Re-valuation model: Revaluations shall be made with sufficient regularity.

Methods and values for revaluation e.g., Land and buildings - market based evidence, Assets with

no market based evidence – use income or depreciated replacement cost method.

Frequency in carrying out the revaluation process General rule of frequency is 3-5 years.

Accounting for Re-valuation of Property, Plant & Equipment

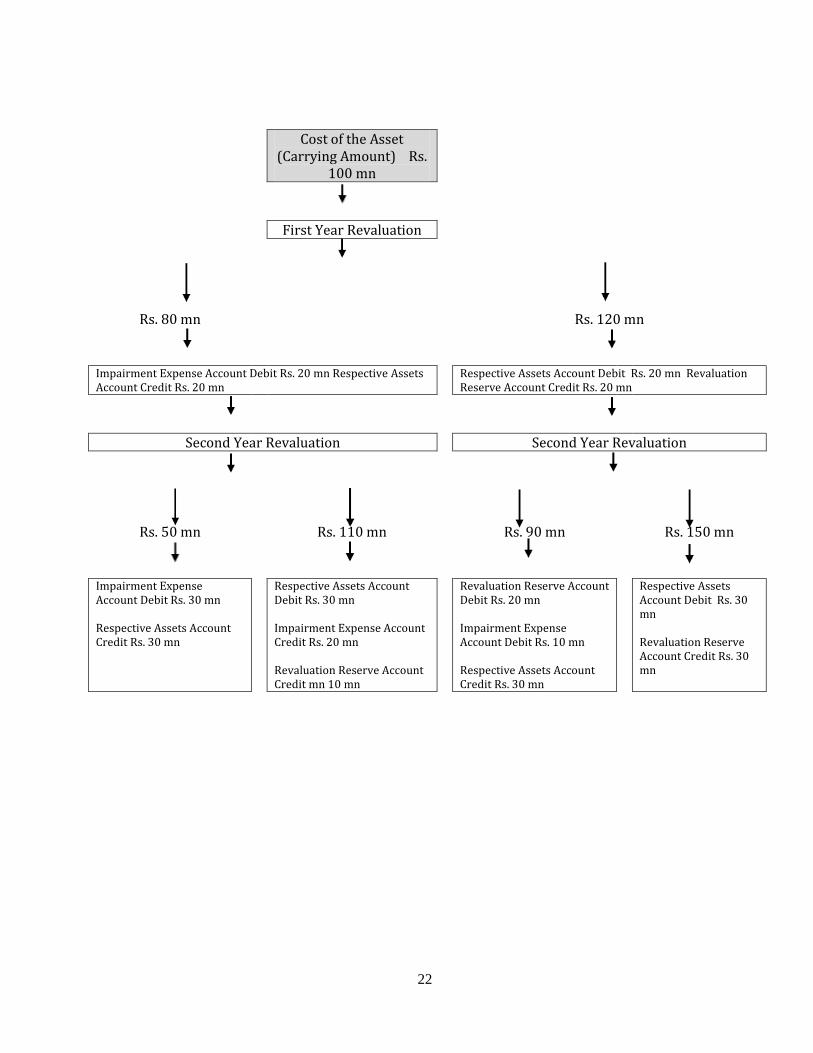

Property, Plant & Equipment First year of revaluation

There can be a revaluation gain or loss from first year of revaluation

First year Gain/surplus from the revaluation

Financial Statement

Debit Credit

Respective Assets Account Debit xxx

Financial Position

Revaluation Reserve Account Credit

xxx Other Comprehensive Income Statement

[Recording of Revaluation Gain/ Surplus]

21

First year Loss from the revaluation

Financial Statement

Impairment Expense Account Debit xxx

Income Statement -under other expenses

Respective Assets Account Credit

xxx Financial Position

[Recording of Revaluation Loss]

Fist year revaluation gain and second year further revaluation gain

Financial Statement

Respective Assets Account Debit xxx

Financial Position

Revaluation Reserve Account Credit

xxx Other Comprehensive Income Statement

[Recording of Revaluation Gain/ Surplus]

Fist year revaluation gain and second year revaluation loss

(second year loss is greater than the first year gain)

Financial Statement

Revaluation Reserve Account Debit xxx

Other Comprehensive Income Statement

Impairment Expense Account Debit xxx

Income Statement -under other expenses

Respective Assets Account Credit

xxx Financial Position

[Recording of first year Revaluation Gain/ Surplus and second year Revaluation Loss]

First year revaluation Loss and second year further revaluation loss

Financial Statement

Impairment Expense Account Debit xxx

Income Statement -under other expenses

Respective Assets Account Credit

xxx Financial Position

[Recording of Revaluation Loss]

First year revaluation loss and second year revaluation Gain / Surplus

( second year Gain is greater than the first year Loss)

Financial Statement

Respective Assets Account Debit xxx

Financial Position

Impairment Expense Account Credit

xxx Income Statement -under other expenses

Revaluation Reserve Account Credit

xxx Other Comprehensive Income Statement

[Recording of first year Revaluation Loss and second year Revaluation Gain/ Surplus]

22

Cost of the Asset (Carrying Amount) Rs.

100 mn

First Year Revaluation

Rs. 80 mn Rs. 120 mn

Impairment Expense Account Debit Rs. 20 mn Respective Assets Account Credit Rs. 20 mn

Respective Assets Account Debit Rs. 20 mn Revaluation Reserve Account Credit Rs. 20 mn

Second Year Revaluation Second Year Revaluation

Rs. 50 mn Rs. 110 mn Rs. 90 mn Rs. 150 mn

Impairment Expense Account Debit Rs. 30 mn Respective Assets Account Credit Rs. 30 mn

Respective Assets Account Debit Rs. 30 mn Impairment Expense Account Credit Rs. 20 mn Revaluation Reserve Account Credit mn 10 mn

Revaluation Reserve Account Debit Rs. 20 mn Impairment Expense Account Debit Rs. 10 mn Respective Assets Account Credit Rs. 30 mn

Respective Assets Account Debit Rs. 30 mn Revaluation Reserve Account Credit Rs. 30 mn