Embed Size (px)

Citation preview

The Individual Tax Model

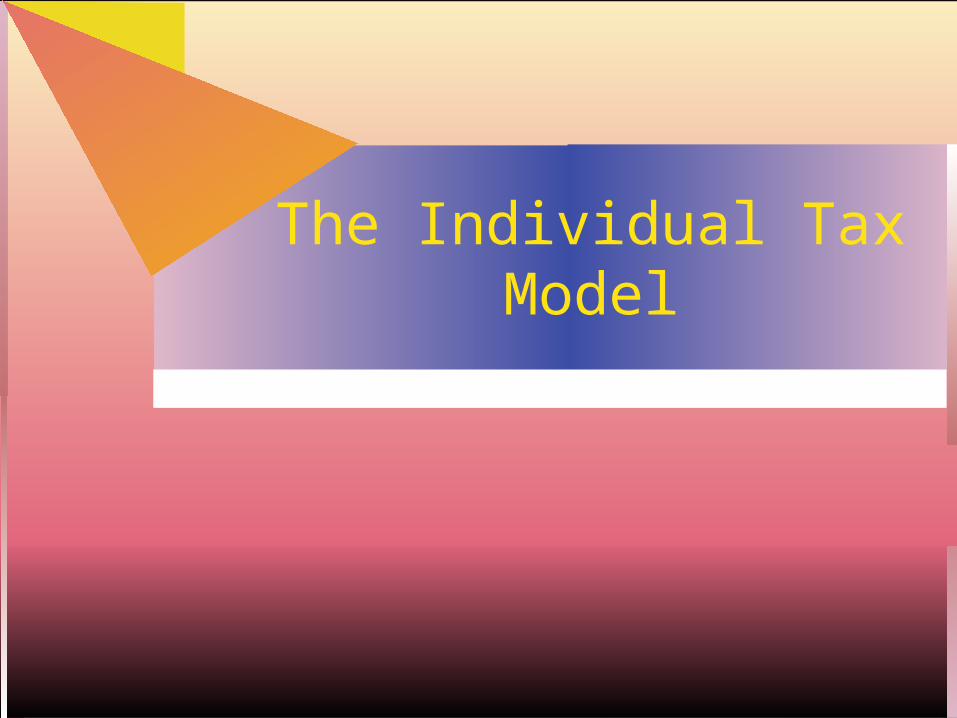

Taxable Income Computation Taxable Income Computation

Calculate gross income totaling Line 22 on 1040 – based on filing status (S,MFJ, MFS,HH).

Calculate Adjusted Gross Income (AGI) Subtract the greater of:

itemized deductions or the standard deduction (based on filing status)

Subtract total personal/dependency exemptions Result is Taxable Income

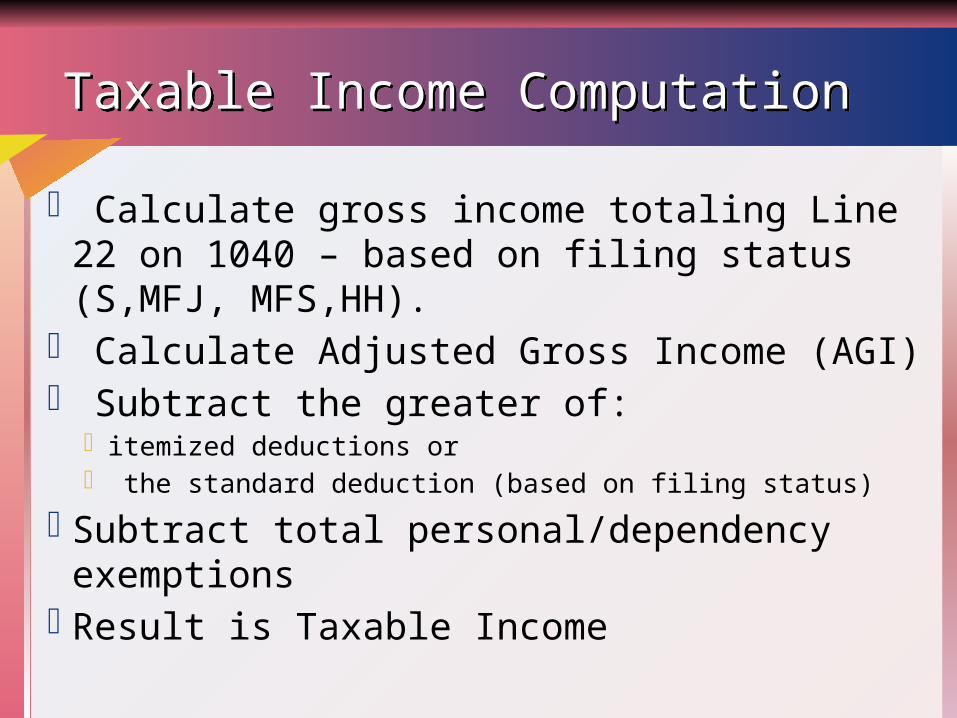

Individual Tax Model – Gross Income / ExclusionsIndividual Tax Model – Gross Income / Exclusions

General Rule: Gross Income is “Broadly Conceived”: Includes all income subject to taxation unless specifically indicated as not taxable by law.

Exclusions include: unrealized gains, gifts, inheritances, welfare type payments, many fringe

benefits, returns of capital, Municipal Interest, some US Govt for higher education, life insurance proceeds.

Scholarships - excludible if recipient is candidate for degree, amount received is not a payment

for services, and is used to pay tuition, books, and other similar educational expenses

Foreign earned Income (Sec. 911) - build U.S. Economy Exclude up to $95,100 of foreign earned income annually plus a

housing allowance (exclusion cannot exceed earned income Individual must be a bona fide resident of the foreign country for an

entire tax year or be in the foreign country for 11 mos in any 12 month period.

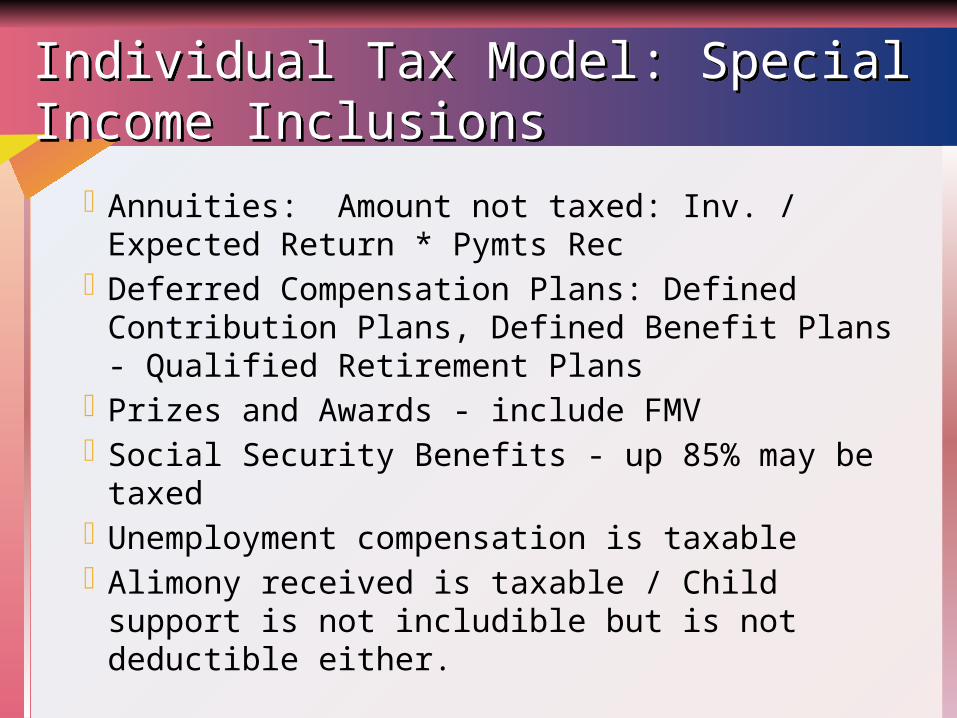

Individual Tax Model: Special Income InclusionsIndividual Tax Model: Special Income Inclusions

Annuities: Amount not taxed: Inv. / Expected Return * Pymts Rec

Deferred Compensation Plans: Defined Contribution Plans, Defined Benefit Plans - Qualified Retirement Plans

Prizes and Awards - include FMV Social Security Benefits - up 85% may be taxed Unemployment compensation is taxable Alimony received is taxable / Child support is not

includible but is not deductible either.

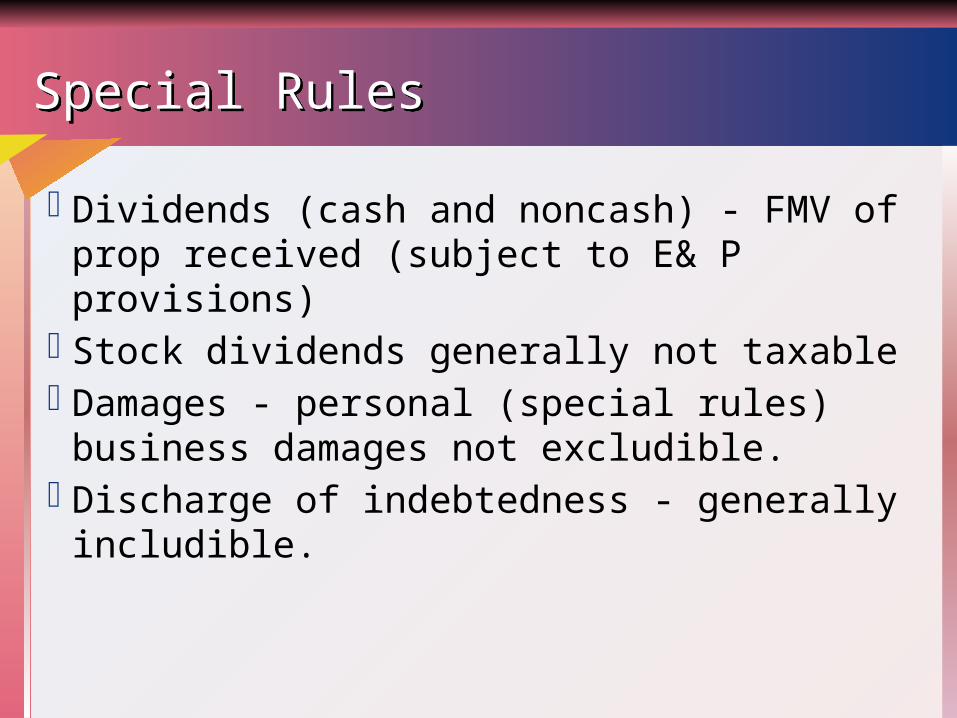

Special RulesSpecial Rules

Dividends (cash and noncash) - FMV of prop received (subject to E& P provisions)

Stock dividends generally not taxable Damages - personal (special rules) business

damages not excludible. Discharge of indebtedness - generally includible.

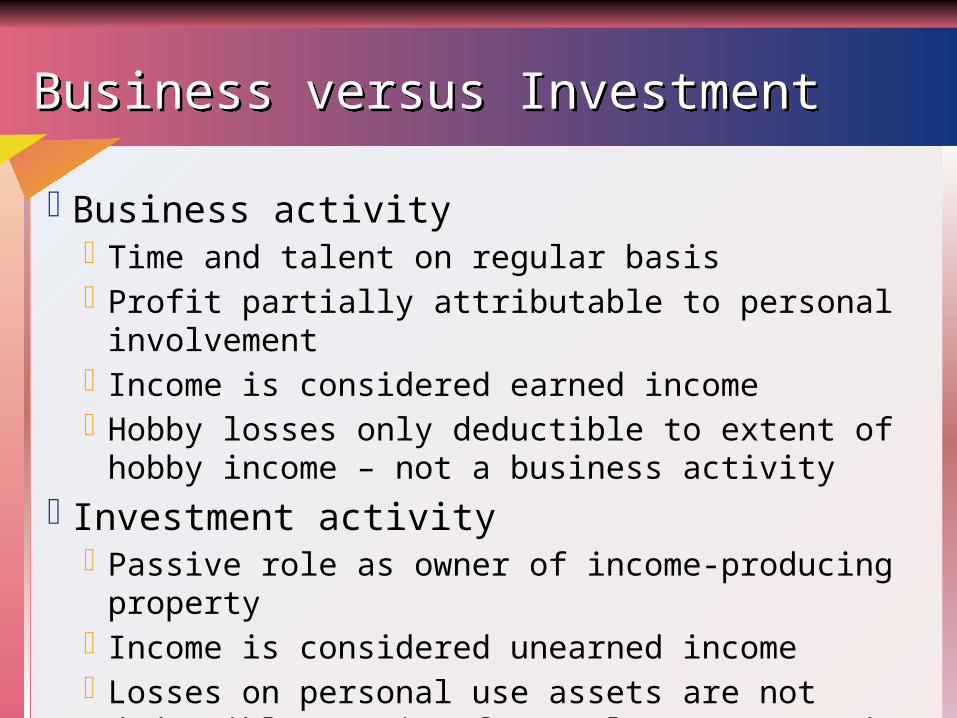

Business versus InvestmentBusiness versus Investment

Business activity Time and talent on regular basis Profit partially attributable to personal involvement Income is considered earned income Hobby losses only deductible to extent of hobby income –

not a business activity

Investment activity Passive role as owner of income-producing property Income is considered unearned income Losses on personal use assets are not deductible – gains

from sale are treated as capital assets.

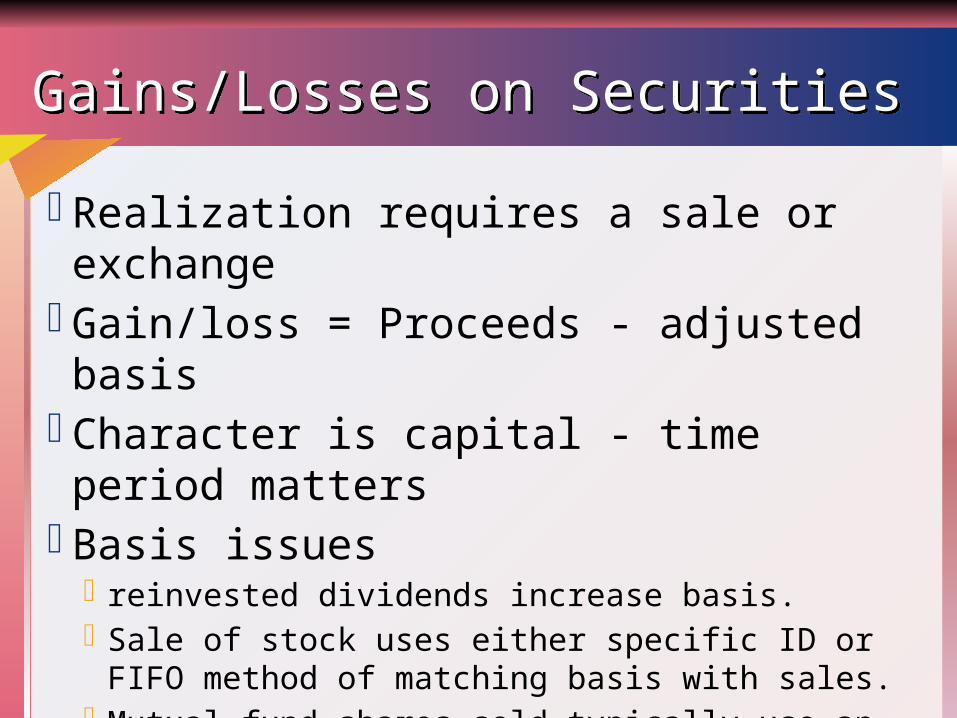

Gains/Losses on SecuritiesGains/Losses on Securities

Realization requires a sale or exchange Gain/loss = Proceeds - adjusted basis Character is capital - time period matters Basis issues

reinvested dividends increase basis. Sale of stock uses either specific ID or FIFO method of

matching basis with sales. Mutual fund shares sold typically use an average basis.

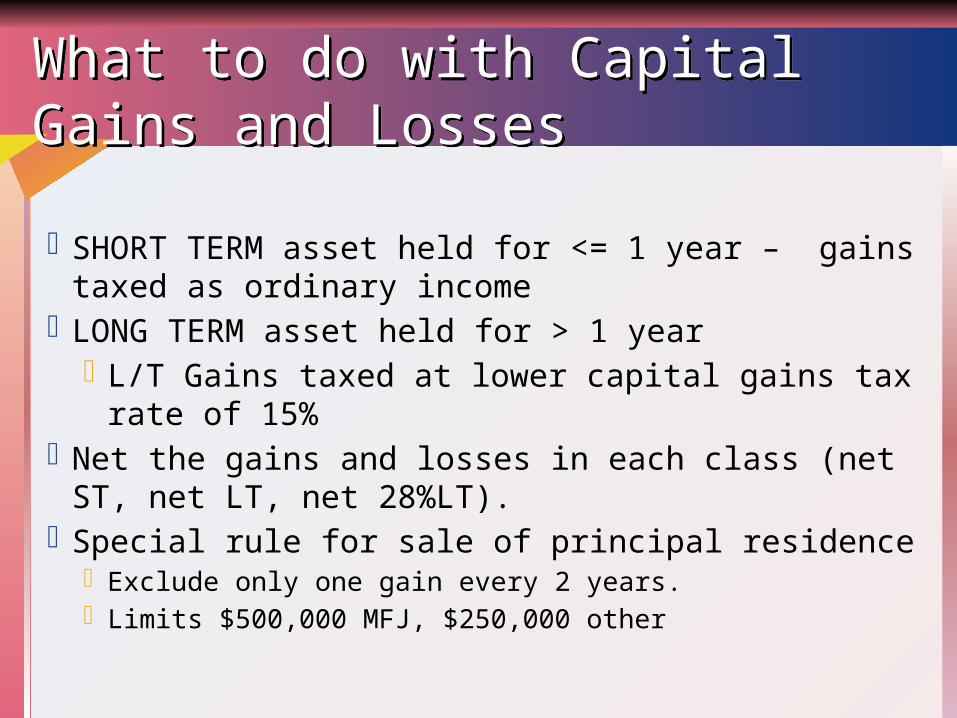

What to do with Capital Gains and LossesWhat to do with Capital Gains and Losses

SHORT TERM asset held for <= 1 year – gains taxed as ordinary income

LONG TERM asset held for > 1 year L/T Gains taxed at lower capital gains tax rate of 15%

Net the gains and losses in each class (net ST, net LT, net 28%LT).

Special rule for sale of principal residence Exclude only one gain every 2 years. Limits $500,000 MFJ, $250,000 other

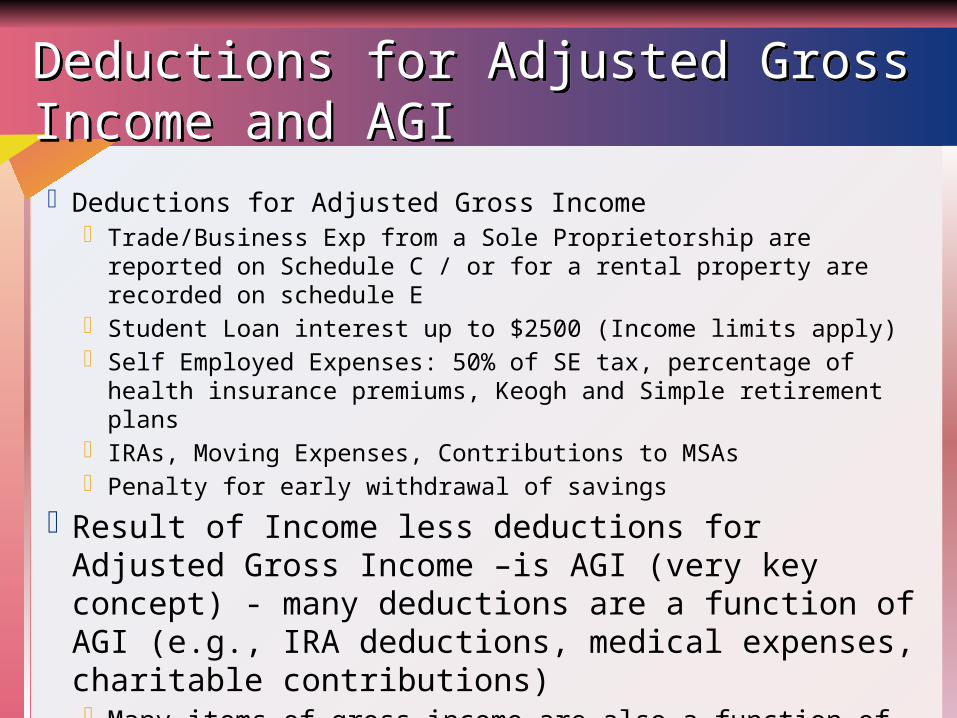

Deductions for Adjusted Gross Income and AGIDeductions for Adjusted Gross Income and AGI

Deductions for Adjusted Gross Income Trade/Business Exp from a Sole Proprietorship are reported on Schedule C /

or for a rental property are recorded on schedule E Student Loan interest up to $2500 (Income limits apply) Self Employed Expenses: 50% of SE tax, percentage of health insurance

premiums, Keogh and Simple retirement plans IRAs, Moving Expenses, Contributions to MSAs Penalty for early withdrawal of savings

Result of Income less deductions for Adjusted Gross Income –is AGI (very key concept) - many deductions are a function of AGI (e.g., IRA deductions, medical expenses, charitable contributions) Many items of gross income are also a function of AGI

Social Security Benefits, Passive Activity Losses

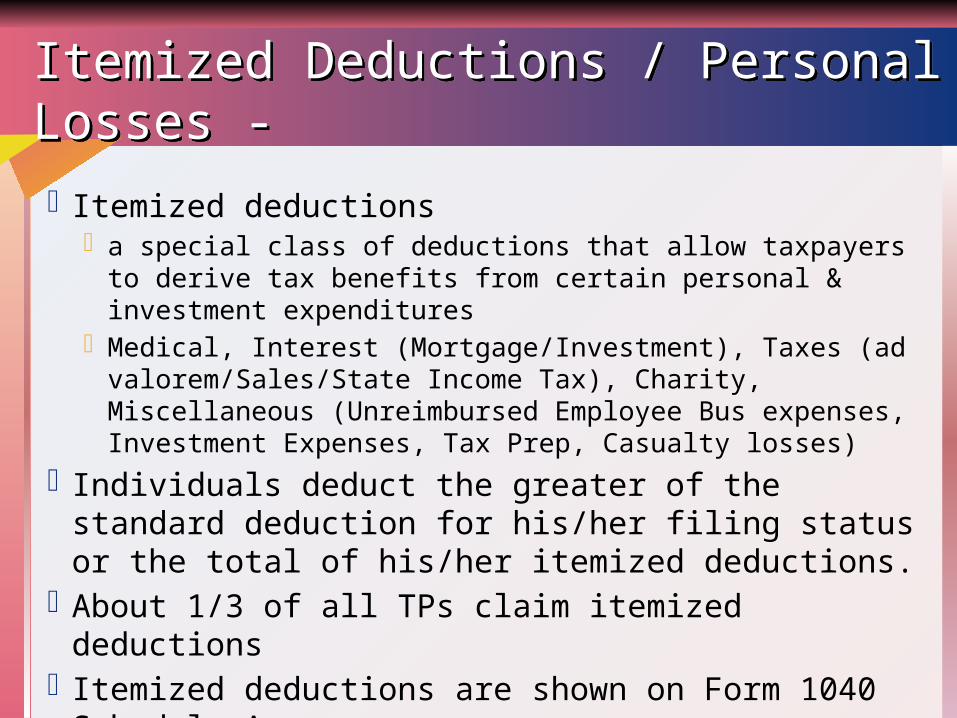

Itemized Deductions / Personal Losses -Itemized Deductions / Personal Losses -

Itemized deductions a special class of deductions that allow taxpayers to derive tax

benefits from certain personal & investment expenditures Medical, Interest (Mortgage/Investment), Taxes (ad

valorem/Sales/State Income Tax), Charity, Miscellaneous (Unreimbursed Employee Bus expenses, Investment Expenses, Tax Prep, Casualty losses)

Individuals deduct the greater of the standard deduction for his/her filing status or the total of his/her itemized deductions.

About 1/3 of all TPs claim itemized deductions Itemized deductions are shown on Form 1040 Schedule A.

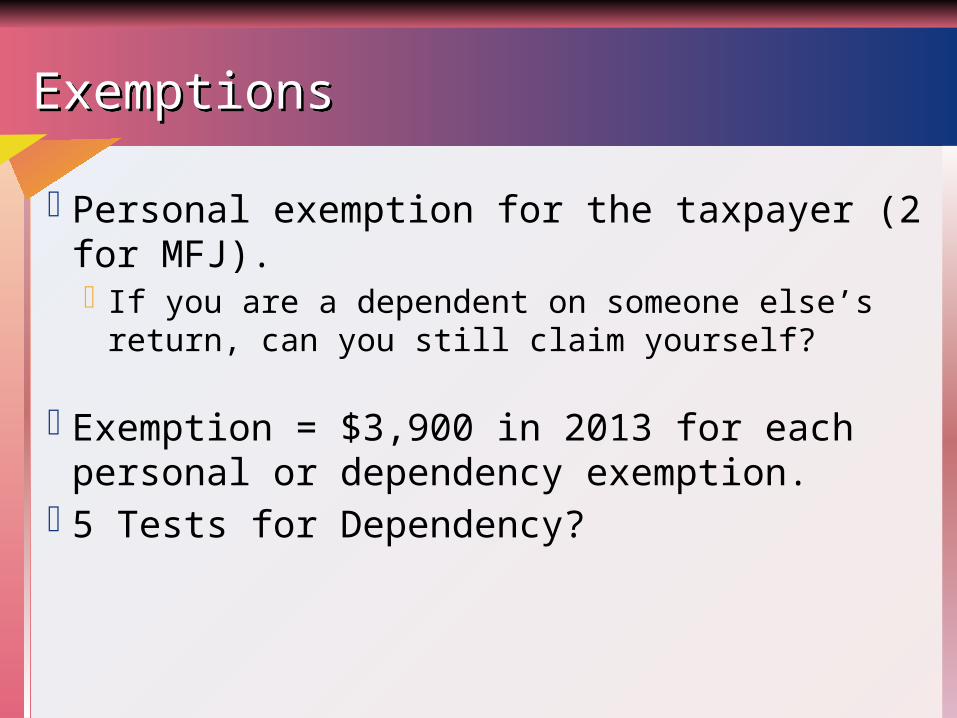

ExemptionsExemptions

Personal exemption for the taxpayer (2 for MFJ). If you are a dependent on someone else’s return, can you

still claim yourself?

Exemption = $3,900 in 2013 for each personal or dependency exemption.

5 Tests for Dependency?

Rich PeopleRich People

Phase-out of itemized deductions – see handout. Haircut 3% of AGI over $300,000

Phase-out of exemptions – see handouts, in 2013, MFJ exemptions disallowed if AGI >$425,000 – if less assume fully allowed.

Tax CreditsTax Credits

A credit is a dollar for dollar reduction in the tax liability. A deduction only reduces the tax by the marginal tax rate associated with that deduction.

Child Credit = $1,000 per child in 2013. Phases out for rich. Dependent care credit (child < 13 years old). Credit amount

between 30% and 20% of child care costs depending on income range.

Earned income credit. This is refundable - a transfer payment to working poor. Increases progressivity of tax rates. Credit is higher for taxpayers with children and phases out as income increases.

Excess FICA withholding is refunded through a tax return claim.

Payment and Filing RequirementsPayment and Filing Requirements

Taxes on wages are withheld each pay period.

Estimated taxes are due on April 15, June 15, September 15, and January 15.

Pay 90% of current year tax, 100% of prior year (or 110% of prior year AGI>$150,000).

Tax return due 4/15, but may be extended to 8/15 then 10/15 (LAST DATE).

Taxable Income from Business Operations

Taxable IncomeTaxable Income

Taxable income = gross income less allowable deductions Gross income “means all income from whatever source

derived.” AKA Broadly Conceived. Deductions are allowed through legislative grace, and include

all ordinary and necessary expenses … in carrying on any trade or business.”

Good rule of thumb: receipts are taxable UNLESS you can find a law that says it is excluded. Expenses are deductible ONLY if you can find a law that says it is deductible.

Taxable YearTaxable Year

12-month period which generally corresponds to its fiscal year.

Individual taxpayers must generally choose a calendar year.

Firms generally choose a year = end of an annual operating cycle.

Changing tax years requires permission - most common reason is merger of firms with different year-ends.

Accounting MethodsAccounting Methods

Overall method by which taxpayers determine their income, deductions and credits, as well as the time realized and recognized. Section 482 grants IRS broad powers to “distribute, apportion, or allocate income” among businesses to CLEARLY REFLECT income of each.

CONSISTENTLY APPLIED Establish a method by using it in the first tax return. Requires IRS permission to change.

Cash MethodCash Method

Under the cash method, gross income includes cash or property actually RECEIVED during the tax year.

Deductions are usually taken in the year cash or property is PAID.

Cash method income includes receipt of noncash goods Anti-abuse provision: Constructive receipt doctrine.

Occurs when taxpayer has unrestricted access to and control of the income.

NO constructive receipt if the amount is available only on surrender of a valuable right, or if there are substantial limits on the right to receive it.

Exceptions - Cash MethodExceptions - Cash Method

Cash method - deduct expenses when PAY. A check is payment when mailed.

An asset must be capitalized. The cost of the asset may be recovered over the asset life (e.g. depreciation, cost of goods sold). Major repairs may result in IRS dispute regarding expense versus capitalization.

Inventory must be accounted for on the accrual method, even for cash basis taxpayers. This is called a HYBRID method of accounting.

Cash Method Deductions - Prepaid ExpensesCash Method Deductions - Prepaid Expenses

Where an expense (e.g., rent or an insurance premium) covers more than the following tax year, the deduction must be spread over the period to which the expense applies.

However, prepaid interest must be capitalized and deducted over the period for which interest is actually charged even if prepayment < next tax year.

Exception - deduct prepaid interest (points) on the purchase of a home. Does not apply to refinancing.

Accrual Method of AccountingAccrual Method of Accounting

Under the accrual method, report income when the right to the income and the amount of the income can be determined with reasonable accuracy. (REALIZATION)

MATCH expenses against revenues. Deduct when ALL EVENTS have occurred that determine the existence of the liability and the amount of the liability can be determined with reasonable accuracy.

Book-Tax DifferencesBook-Tax Differences

Contrasting principles of conservatism. GAAP - protect shareholders and creditors: don’t

overstate book income. Tax - protect government revenues: Don’t

understate taxable income. (Contrasting result may arise due to economic incentives - e.g. accelerated depreciation.)

Book-Tax Permanent DifferencesBook-Tax Permanent Differences

Permanent differences do not reverse; Temporary differences reverse over the life of the firm.

Examples of permanent differences 50% meals and entertainment political contributions fines and penalties interest expense to generate tax-exempt municipal bond

income premiums on life insurance Tax-exempt municipal bond income Life insurance proceeds

Temporary Book-Tax DifferencesTemporary Book-Tax Differences

Examples of temporary differences: Depreciation Timing of accruals Capital losses Bad debts (allowance vs. writeoff) Cash versus accrual accounting

Accrual Expenses ExceptionsAccrual Expenses Exceptions

Related Party Accruals – Sec. 267 The paying party cannot deduct an expense until the year

that a receiving party deducts the expense. Prevents accrual basis taxpayers from accruing an

expense but delaying payment.

Sole ProprietorshipSole Proprietorship

Business income and expenses are reported on Schedule C, filed with the individual form 1040.

Net income or loss on Schedule C is ordinary income or loss; combine this net with other items of gross income.

If the Schedule C business loss > other sources of income, the NOL (net operating loss) can be carried back 2 years and forward 20 years.

Employment TaxesEmployment Taxes

FICA = 6.2%/6.2% Social Security tax (on wages up to $113,700 in 2013) + 1.45% Medicare tax on all wages. Both employer and employee must pay this tax.

Employers withhold income taxes and the employee’s share of FICA.

Employers must remit the withheld taxes to the federal (and state if applicable) governments.

Self-employed taxpayers must pay SE (self-employment) tax, equal to 2 x FICA, or 15.3% of net earnings from self-employment. (See footnote 20 for details). 1/2 of SE tax is deductible on Form 1040.

Property Acquisitions and Cost Recovery Deductions

Expense vs. CapitalizeExpense vs. Capitalize

Deduction permitted for all “ORDINARY AND NECESSARY” business expenses

Deduction prohibited for “PERMANENT improvements to increase the value of property”

Some types of capitalized costs can be recovered through amortization or depreciation

Tax BasisTax Basis

Tax basis = unrecovered cost (cost - depreciation). Starting basis generally equals COST basis:

original purchase price regardless of whether acquired by debt, or

FMV of asset if cost more difficult to measure.

Cost recovery of Inventory = cost of goods sold Tangible assets = depreciation Intangible assets = amortization Natural resources = depletion

DepreciationDepreciation

Depreciation applies to tangible assets (things you can touch versus intangibles like patents, goodwill) that: Lose value over time due to wear and tear, obsolescence

Buildings depreciate even though real estate often increases in value.

Have a reasonably ascertainable useful life Artwork is not generally depreciable.

DepreciationDepreciation

MACRS - Modified Accelerated Cost Recovery System Personalty:

DDB: 3, 5, 7, 10 150% DB:15, 20 General rule is half year convention

Realty: SL method: 27.5 years residential, 39 years non-residential (specialty realty 20, 25, 50) Mid Month convention

Depreciation Conventions - PersonaltyDepreciation Conventions - Personalty

Normal is half year convention Anti-Abuse provision Mid-quarter convention

: IF > 40% personalty is acquired during the last quarter of the year, THEN

Compute depreciation separately for EACH quarter’s acquisition using mid-quarter tables in appendix of chapter 6

AutomobilesAutomobiles

Maximum annual depreciation limit per vehicle, indexed for inflation. ––, 2013 bonus depreciation 50%

Compute depreciation per MACRS, then limit above.

Expensing Election – Section 179Expensing Election – Section 179

Applies to tangible personalty. May expense $500,000 of assets purchased in 13 – also 50% bonus depreciation for 2013.

Expense cannot create a business loss. Expense reduced $ for $ by purchases >

$2,000,000. Reduces recordkeeping, benefit for small

businesses Planning - if buy a 3-year, 5-year and 7-year asset,

which one should you expense?

Amortization of IntangiblesAmortization of Intangibles

Generally requires a determinable useful life. Organizational costs are amortizable straight

line method over 180 months – first 5K generally deductible immediately.

Start-up costs are also amortizable straight line method over 180 months - some exceptions.

Expansion costs may be currently deductible.

Leasehold Costs and ImprovementsLeasehold Costs and Improvements

Cost of acquiring lease is amortized over the period of lease.

Improvements to leased property are capitalized and depreciated according to type of property.

Purchased IntangiblesPurchased Intangibles

Allocate lump-sum price to assets by relative FMVs.

Residual = goodwill. Tax = 15 years SL GAAP = 40 years pre-2002. No GAAP amortization post-2001 - evaluate for impairment annually. Book-tax difference is permanent post-2001.

Chapter

7

Property Dispositions

Realized Gain or LossRealized Gain or Loss

Amount realized on disposition MINUS adjusted basis of property (e.g. cost -

accumulated tax depreciation = “NBV”) = Realized gain or loss. GENERALLY, realized (economic) gains and losses

on disposition are recognized (result in taxable income or deductions) unless there is a specific exception. See Chapter 8.

Unrealized (mere appreciation or decline in value) gains and losses are neither realized nor recognized.

Amount RealizedAmount Realized

Cash received FMV of any property received, including buyer’s

note Relief of debt. AP3. Reduce the amount realized by selling costs such

as sales commissions, broker fees. No adjustment for “inflationary gains.”

Installment Sale MethodInstallment Sale Method

Permits deferral of gain recognition until cash is received on the sale.

Gain recognized this year = (cash this year) x (total gain / total sales price).

Not allowed for sales of publicly traded stock or for inventory, or to delay recognition of depreciation recapture.

Financial accounting uses accrual accounting, so installment sales method for tax creates a temporary book-tax difference.

Related Party LossesRelated Party Losses

Relative: family = spouse, sibling, ancestors, lineal descendants

Q10 50% controlled corporations

Losses realized on sale of property between related parties are NONdeductible.

Future gain (but NOT loss) by relative can be offset by disallowed loss.

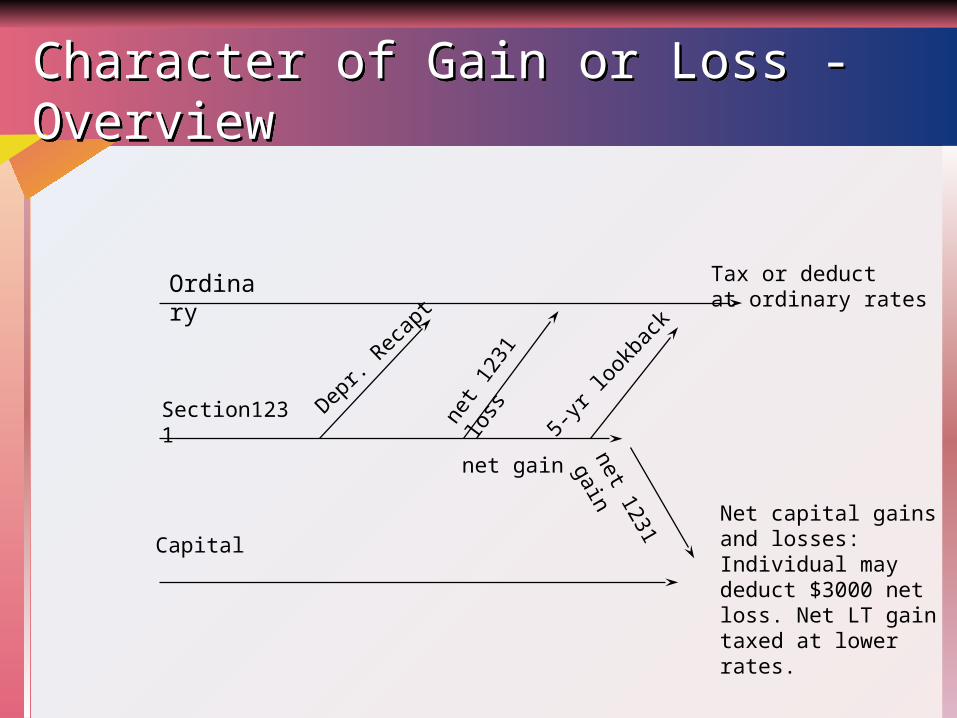

Character of Gain or Loss - OverviewCharacter of Gain or Loss - Overview

Ordinary

Capital

Section1231 Depr.

Reca

pt

5-yr

look

back

net 1

231

loss

net 1231

gain

Tax or deductat ordinary rates

Net capital gains and losses: Individual may deduct $3000 net loss. Net LT gain taxed at lower rates.

net gain

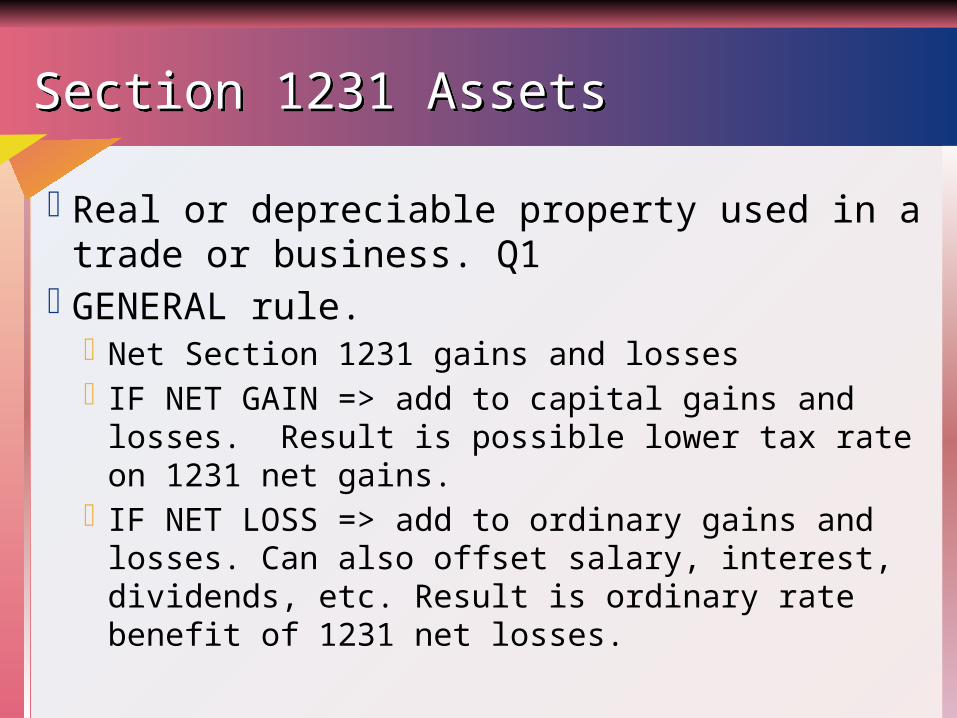

Section 1231 AssetsSection 1231 Assets

Real or depreciable property used in a trade or business. Q1

GENERAL rule. Net Section 1231 gains and losses IF NET GAIN => add to capital gains and losses. Result

is possible lower tax rate on 1231 net gains. IF NET LOSS => add to ordinary gains and losses. Can

also offset salary, interest, dividends, etc. Result is ordinary rate benefit of 1231 net losses.

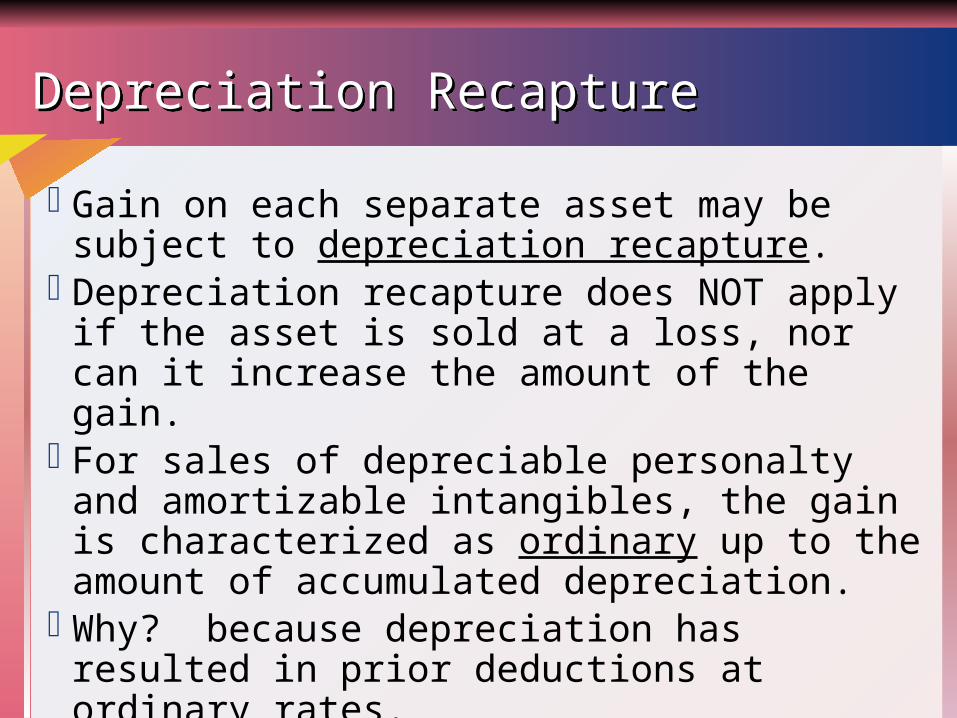

Depreciation RecaptureDepreciation Recapture

Gain on each separate asset may be subject to depreciation recapture.

Depreciation recapture does NOT apply if the asset is sold at a loss, nor can it increase the amount of the gain.

For sales of depreciable personalty and amortizable intangibles, the gain is characterized as ordinary up to the amount of accumulated depreciation.

Why? because depreciation has resulted in prior deductions at ordinary rates.

Depreciation RecaptureDepreciation Recapture

REALTY: Special rules apply to pre-1986 depreciation on

accelerated methods: most of this property is fully depreciated, so rules seldom apply.

Corporations must recapture 20% of amount that would have been ordinary had it been personalty (lesser of gain or depreciation).

Individuals treat lesser of gain or depreciation as a capital gain subject to a special 25% tax rate - see chapter 15.

Section 1231 NettingSection 1231 Netting

After all depreciation recapture, NET the remaining Section1231 gains with Section 1231 losses.

If a net loss, treat as an ordinary loss and combine with other ordinary income and losses.

If a net gain, then the net gain is treated as a capital gain UNLESS:

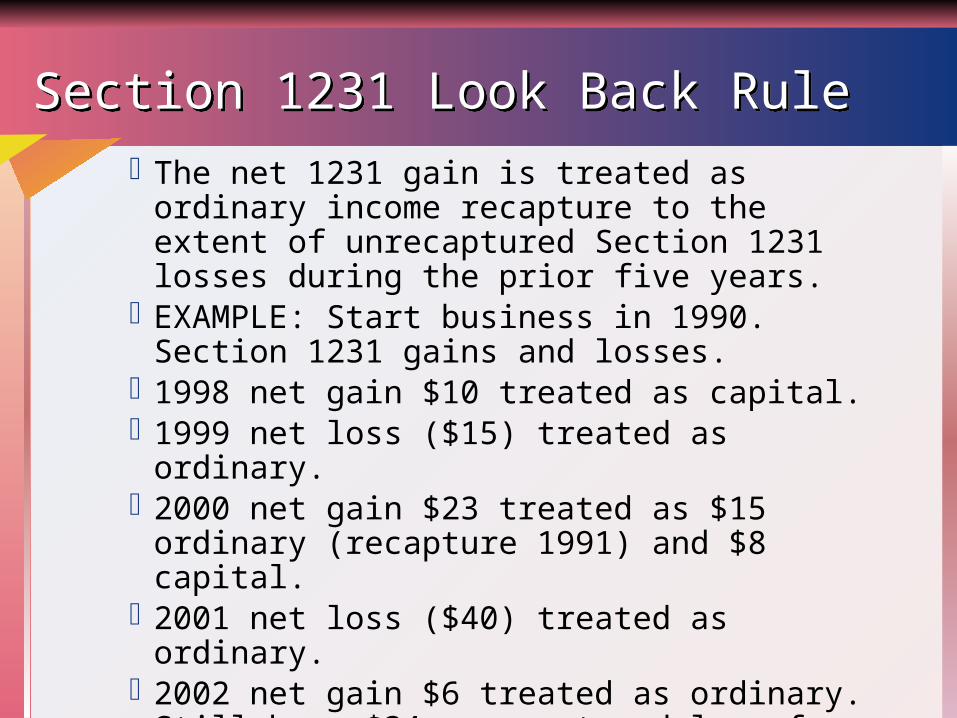

Section 1231 Look Back RuleSection 1231 Look Back Rule The net 1231 gain is treated as ordinary income

recapture to the extent of unrecaptured Section 1231 losses during the prior five years.

EXAMPLE: Start business in 1990. Section 1231 gains and losses.

1998 net gain $10 treated as capital. 1999 net loss ($15) treated as ordinary. 2000 net gain $23 treated as $15 ordinary

(recapture 1991) and $8 capital. 2001 net loss ($40) treated as ordinary. 2002 net gain $6 treated as ordinary. Still have $34

unrecaptured loss from 1993. 2003 net gain $50 treated as $34 ordinary, $16

capital.

At Risk (Sec. 465) and Passive Activities (Sec. 469)At Risk (Sec. 465) and Passive Activities (Sec. 469)

Losses in business entities only allowed to the extent that you have sufficient at-risk basis.

Disallowed losses under Sec 465 are suspended until sufficient basis exists to take the losses.

Once a loss is allowed under Sec. 465, it may further be limited by Sec. 469 if the entity is a passive activity. - general rule for PALS?

There are special rules for office-in-home and for rental properties with mixed use (personal v. rental) be sure to check the rules.