Embed Size (px)

Citation preview

L.I. Group

The Healthcare Technology Venture Market in Europe, UK and Yorkshire & Humber

i

About Library Innovation Group (L.I. Group)The L.I. Group was formed as a spin-out company from the Library House Consulting Department. The company uses established evidence-based research methodologies to deliver strategic insights into innovation-led companies and markets. It also advises public and private sector organisations on strategic issues that involve technology, innovation, entrepreneurship and finance.

Project Team:

Martin Holi

Alexander Jan

Stephen Mounsey

Dr Jonathan Lawton

Dr Siobhán Ní Chonaill

Malgosia Rozycka

For more information about the contents of this report, please contact:

L.I. Group

St John’s Innovation Centre

Cowley Road

Cambridge

CB4 OWS

United Kingdom

www.li-group.co.uk

Access To Finance For Healthcare Technologies ProgrammeAccess to Finance for Healthcare Technologies is an investment readiness programme established by Yorkshire Forward to assist companies in the Health Technology sectors. The programme addresses three key factors relevant to the Yorkshire & Humber region:

the opportunity to develop investment markets, especially for companies in complex and challenging markets such as • healthcare;

the opportunity to engage talented business support professionals able to provide advice and guidance on raising • finance in general and especially in this sector; and

a shortage of existing successfully venture backed companies to act as role models, explain the process and showcase • the benefits.

The programme is scheduled to run for an initial period of three years from January 2009 and is delivered by a consortium of three companies, led by Grant Thornton UK LLP and including Quotec and BITECIC.

www.investinginhealth.co.uk

ii

The Healthcare Technology Venture Market

CO

NT

EN

TS

Contents1. Executive summary ............................................................................................1

2. Introduction .......................................................................................................2

3. The healthcare technology sector ........................................................................3

3.1. Pharmaceutical industry ................................................................................................ 4

3.1.1. Global and European pharmaceutical industry ...............................................................5

3.1.2. The UK pharmaceutical industry .....................................................................................5

3.1.3. Pharmaceutical industry in Yorkshire & Humber .............................................................7

3.2. Medical technology industry ..........................................................................................7

3.2.1. Medical technology product naming classification......................................................... 8

3.2.2. Cardiovascular ............................................................................................................... 8

3.2.3. Diagnostics ................................................................................................................... 8

3.2.4. Orthopaedics ................................................................................................................ 9

3.2.5. Global expenditure in medical technologies .................................................................10

3.2.6. Medical technologies in Europe ....................................................................................10

3.2.7. Medical technologies in the UK .................................................................................... 11

3.3. Medical technologies Yorkshire & Humber ....................................................................12

4. Thefinancingcycleofhealthcaretechnologycompanies ..................................... 13

4.1. Where do healthcare technology companies come from?............................................. 13

4.2. Is the United Kingdom a good place to attract venture capital investments? ................ 13

4.3. Is this also true for healthcare technology companies? .................................................14

4.4. First round investments ................................................................................................16

4.5. Who are the early-stage investors? ............................................................................... 17

4.6. How much capital was invested? .................................................................................. 17

4.7. Follow on investment rounds .......................................................................................18

4.7.1. European investors in healthcare technology companies ..............................................19

4.7.2. Top deals in Europe ......................................................................................................22

4.7.3. Top deals in the UK .......................................................................................................22

5. The attractiveness of Yorkshire & Humber .......................................................... 23

5.1. The investment landscape in Yorkshire & Humber ........................................................23

5.1.1. The origin of companies in the region ...........................................................................23

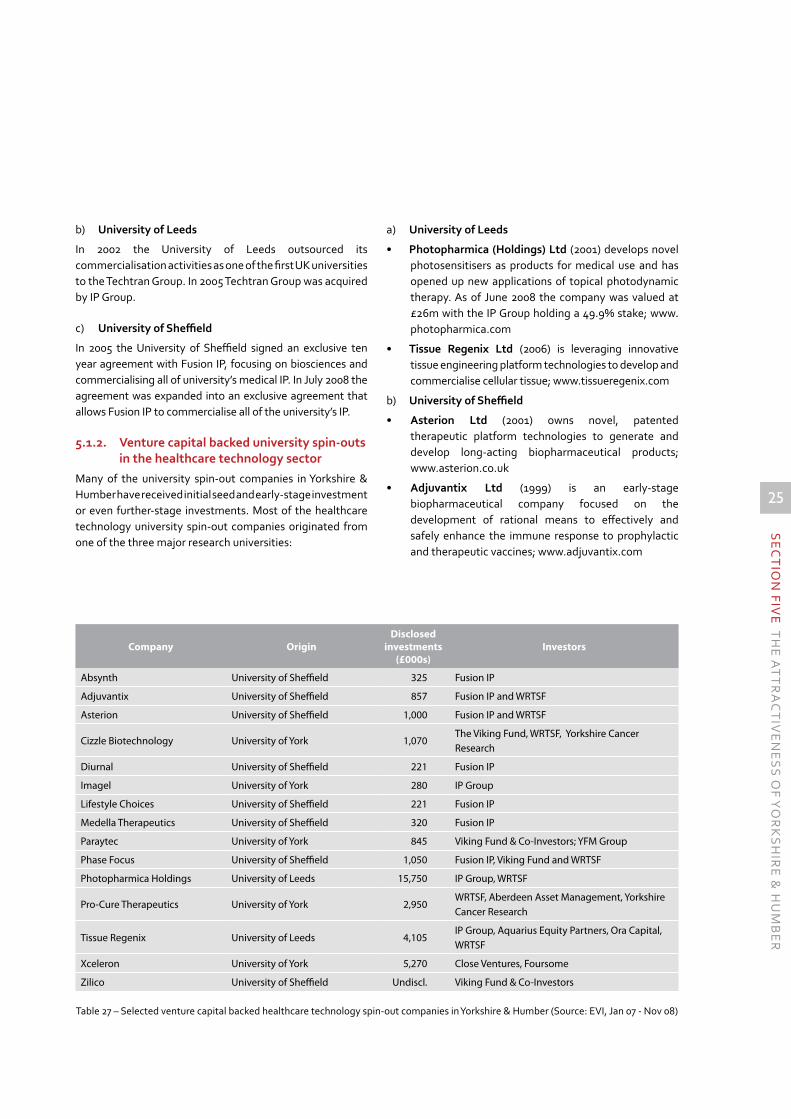

5.1.2. Venture capital backed university spin-outs in the healthcare technology sector ..........25

5.1.3. Independent healthcare technology start-ups ............................................................. 26

5.2. Investors in Yorkshire & Humber ...................................................................................27

5.3. Venture capital investment successes .......................................................................... 29

6. Future trends in the healthcare technology venture market ................................. 30

7. Sponsors of Access to Finance for Healthcare Technologies Programme ................38

iii

FOR

EW

OR

D

Foreword Yorkshire & Humber is at the forefront of the UK’s latest advances in healthcare making it an important region for the healthcare technology industry and one of the fastest-growing nationally. It has one of the UK’s highest concentrations of medical device companies, superb specialist skills (especially in surgical instrumentation, orthopaedics and advanced wound-care), exceptional access to clinical trials, pioneering R&D and Europe’s largest teaching hospital.

The healthcare technology venture market is the second largest sector, behind information and telecommunications, attracting around 24% of all deals in Europe and 29% in the UK. This represents over £2.1bn of investment in European healthcare companies and £434m in the UK in 2007 and 2008.

However, despite the buoyancy of the sector and the strengths of the region, many healthcare technology companies still face difficulty in raising private equity particularly in the early stage where they face the so called ‘equity gap’ . Typically this is the first round of venture capital investment of around £500K to £2m where investors regard propositions as particularly risky.

To help companies in Yorkshire & Humber best position themselves to secure funding we are very pleased to announce a new programme, ‘Access to Finance for Healthcare Technologies’, which will assist these companies to become ‘investment ready’. We are delighted to be part of a consortium with a track record of success in this area, led by Grant Thornton and including Quotec and BITECIC, which will work closely with companies in the region to provide skills, business model reviews, mentoring and investor introductions to get them in the best possible shape to secure investment. The programme will run from January 2009 to April 2012 and is open to all SMEs in the healthcare technology market based in Yorkshire & Humber.

This report has been prepared for the launch of the programme, with the needs of entrepreneurial companies in mind, to provide an overview of the level of investment activity in the healthcare technology sector over the last two years in Europe, the UK and Yorkshire & Humber. It details the types of deals that have been completed and who the most active investors have been and also provides a commentary on the current status of the investment market and likely future trends. I hope that you will find it informative.

Glenn Stone

Partner, Grant Thornton UK LLP

iv

The Healthcare Technology Venture Market

KE

Y FA

CT

S

Key Facts*

£2.1bn of venture capital has been invested into European healthcare companies.

133,000 people are employed by healthcare technology companies in the UK.

Over 300 venture capital investments have been made into UK healthcare companies.

71 first round investments have been made into UK healthcare companies.1

£1.4m is the average deal amount for a UK first round investment into the healthcare technology sector

88 active companies spun-out from Yorkshire Universities (2nd place in the UK).2

17 is the number of active venture capital backed healthcare technology university spin-outs in Yorkshire.

£383m is the total annual research income of the universities in Yorkshire & Humber.

£76.2m is the value of contract research with Yorkshire Universities (3rd place in the UK).3

*as of Jan 2007 – Nov 2008

1

EX

EC

UT

IVE

SU

MM

AR

Y

1 Executive summaryThis report provides an overview of the healthcare technology venture capital market. It analyses both historical and current investment data on the healthcare technology venture market in the Yorkshire & Humber region and benchmarks it against European and UK figures. It uses a qualitative approach to gauge what the industry perceives to be both the future trends and overall potential of the healthcare technology industry.

The healthcare technology sector is made up of a number of sub areas, including pharmaceutical, drug development, medical technologies and other life sciences. These areas are of particular interest as they have experienced high levels of growth in recent years due to increases in national health expenditure, the global ageing population, developments in technology (including diagnostics and drug delivery) and the rise in the number of chronic illnesses.

The UK’s leading manufacturing industry is the pharmaceutical and drug development sector, with two of the world’s top ten pharmaceutical companies based in the country. Within the Yorkshire & Humber region, pharmaceutical companies make up less than half of all healthcare technology companies within the area. Johnson & Johnson, one of the largest global pharmaceutical companies, has subsidiaries based in the Yorkshire & Humber region as are a number of major publicly-listed UK pharmaceutical companies including; Avacta Group, Syntopix Group and Fusion IP.

Although the UK is heavily reliant on imports it accounts for 11% of the total European medical device market and 20% of all European medical technology companies. Within the UK, the sector employs some 60,000 individuals and nearly a tenth of these are employed within the Yorkshire & Humber region accounting for an output of £450m. In addition to four public- quoted companies (quoted on the London Stock Exchange) there are several large international medical technology companies based in the Yorkshire & Humber region.

Venture capital in the healthcare technology sector accounts for approximately 24% of all investments in Europe. Of the 311 deals completed between 2007 and 2008 there was an almost equal split in investment activity between the pharmaceutical and medical technology area. The average investment size into a healthcare technology company was £2.7m, £1.3m lower than the European average in this sector. There have been six first round investments in the Yorkshire & Humber region over the past two years accounting for nearly 10% of all first round investments in to healthcare technology companies in the UK.

The Yorkshire & Humber region benefits from the presence of a number of strong research universities that have contributed several spin-out companies to the local healthcare technology sector. The universities collaborate closely with intellectual property commercialisation companies which provide capital and advice to spin-out companies. However, the number of products or services that can be transferred into separate spin-out companies is limited at any university. This therefore requires a sustained effort by the region to establish, finance and grow additional start-up companies.

This report has identified a number of technological trends within the healthcare technology sector that are increasingly appealing to venture capital investors. These include miniaturisation and nano-biotechnology, stem cell, ophthalmology, standardisation, imaging and personalised medication. The report also investigates the latest financial trends for early-stage businesses within the sector.

2

The Healthcare Technology Venture Market

INT

RO

DU

CT

ION

2 IntroductionOver the years the European healthcare technology sector has provided many attractive investment opportunities for investors. Venture capital investments into this sector now count for one-third of the European and UK venture capital market. The emergence of biotechnology within the pharmaceutical and drug development sectors has created a niche venture capital market with specialised early-stage investors. In the field of medical technologies many innovations are now explored through smaller companies developing diagnostic tools, implants, medical instruments and drug delivery systems to serve patients, with particular focus on the ageing societies across European countries.

Despite the relatively high venture activity in medical technology in the UK all venture capital stakeholders are aware of the challenges that the venture capital market will face in the upcoming months and possibly years. The impact of changes taking place in the economic and financial markets will undoubtedly influence the venture capital market significantly and will require special efforts from entrepreneurs to secure financing for their companies and for investors to close new funds.

This report analyses the European healthcare technology venture market over the past two years (2007-2008) using quantitative and qualitative research methods. Analysis of venture capital investment data within this sector is used to specify the investment activity and trends. The results are backed by interviews with experts and professionals from venture capital organisations, technology transfer offices, venture capital backed companies and other service providers.

Secondly, the results from the analysis provide the basis for recommendations addressed to investment-seeking entrepreneurs of healthcare technology companies located in the UK and, more specifically, in Yorkshire & Humber.

Finally, the report gives a detailed overview of the regional healthcare technology market in the Yorkshire & Humber. Through the analysis of companies, case studies and historical investments, this report provides entrepreneurs, investors, technology transfer professionals, universities and business support organisations with a clearer understanding of the regional investment landscape and ways in which these groups can benefit from investment opportunities.

MethodologyVenture capital investment data is derived from different information sources and news providers. The main data source for investment activities was the Library House database ‘European Venture Intelligence’ (EVI) as of November 2008. Additional information was taken from from correspondence with investors, technology transfer offices and universities. Market capitalisation values are taken from the statistics of the London Stock Exchange (LSE) as of December 2008.

The data presented in this report is taken from publicly available sources. Due to the nature of the venture capital market not all information about investments is disclosed. However, the L.I. Group claims to provide an accurate picture based on the information that is currently available.

3

SE

CT

ION

TH

RE

E T

HE

HE

ALT

HC

AR

E T

EC

HN

OLO

GY

SE

CT

OR

The healthcare industry is generally defined as that which has a focus upon the treatment and tending of patients who are injured, sick, disabled or infirm and is facilitated by professional health workers and technology. The healthcare technology industry can thus be broadly segmented into two areas:

Pharmaceutical and drug development•

Medical technologies•

Investors look for companies that have excellent growth potential driven by the company’s own innovative capacity. However, external factors such as market size and market growth are part of the key reasons for investment as companies are more likely to gain venture backing if they can prove that their products and services can serve large or growing markets that would have a high uptake of innovative goods. Before an analysis of differing sectors within the healthcare technologies industry can be undertaken, the overall industry and the effects technology has upon it, has to be understood.

The demand for innovation in the healthcare market is driven by several factors including the increase in life expectancy across developed western countries; the increase of expenditure to

Figure 1 – Health expenditure as a share of GDP, 2006 (Source: OECD)

provide healthcare services; the identification of numerous medical areas with unmet needs, particularly oncological, cardiovascular, arthropathic and neurological diseases such as Alzheimer’s and Parkinson’s. Rising obesity levels worldwide, which have led to much higher numbers of diabetes- and cardiovascular-related conditions, have also created a demand for innovative healthcare technologies. A company that is able to serve any of these demands can provide huge financial returns to their investors, and is therefore a prime target for venture capital funds.

According to the latest OECD Health Data, the average national spend on healthcare worldwide still remains at the 8.9% of the GDP (denoted by the OECD in Figure 1), with the US spending the highest percentage of GDP (see Figure 1). It can be seen that healthcare spending remains a large enough market to attract the interests of investors, particularly when the innovation can garner a large enough portion of the expenditure.

In previous years it has been stated that the focus • on healthcare technology would cost the country increasingly large amounts year on year, with some healthcare experts stating that the development and

3 The healthcare technology sector

4

The Healthcare Technology Venture Market

SE

CT

ION

TH

RE

E T

HE

HE

ALT

HC

AR

E T

EC

HN

OLO

GY

SE

CT

OR

diffusion of medical technology was responsible for the persistent difference between health spending and overall economic growth. Some argued that new medical technology may account for about one-half or more of real long-term spending growth. However, the costs were shown to have specific benefits such as:

Development of new treatments for previously • untreatable terminal conditions;

Major advances in clinical ability to treat previously • untreatable acute conditions;

Development of new procedures for discovering and • treating secondary diseases within a disease;

Expansion of the indications for a treatment over • time, increasing the patient population to which the treatment is applied;

On-going, incremental improvements in existing • capabilities, which may improve quality;

Clinical progress, through major advances or by the • cumulative effect of incremental improvements that extends the scope of medicine to conditions once regarded as beyond its boundaries, such as mental illness and substance abuse.6

As stipulated in the ‘Impacts of Advances in Medical Technology in Australia’ report (2005)7, increased expenditure on new medical technologies is reflected in improved treatments and a significant increase in the numbers of people treated. Although advances in medical technology have provided value for money — particularly as people highly value improvements in the quality and length of life — in practice the cost effectiveness of individual technologies varies widely. This high level of variation in healthcare cost effectiveness makes the overall value, or net community benefit, to be an important point of consideration.

With this in mind, two key questions shown in Figure 2 must be asked when looking at new healthcare technology.

These two questions and the subsequent thought process have become the basis for determining the impact and hence attractiveness to investors interested in the healthcare industry.

Figure 2 – Developed from Rettig (1994) and Productivity Commission (2005)

3.1. Pharmaceutical industryThe pharmaceutical industry is one that is focused on the development, production and marketing of medication, which is defined as ‘as any substance intended for use in the diagnosis, cure, mitigation, treatment, or prevention of disease.’8 Lately the pharmaceutical industry has undertaken intensive research and development activities within the biotechnology industry and therefore the term biotechnology has become synonymous with drug discovery and production. In order to understand the healthcare technologies industry one must look at these industries and the potential market facing venture capital investors.

5

3.1.1. Global and European pharmaceutical industry

Figure 3 – Breakdown of global pharmaceutical sales by region – 2007 (Source: IMS,2008)

The global pharmaceutical industry was estimated to be worth over US$660bn in 2008. Figure 3 shows the breakdown of global pharmaceutical sales by region. It can be seen that one third of global pharmaceutical sales were in Europe. Of the top ten pharmaceutical companies, five are based in

SE

CT

ION

TH

RE

E T

HE

HE

ALT

HC

AR

E T

EC

HN

OLO

GY

SE

CT

OR

Corporation Country Sales (£m) Market share (%)

Pfizer US 22,292 6.7

GlaxoSmithKline GB 18,847 5.6

Novartis CH 17,154 5.1

Sanofi Aventis FR 16,788 5.0

Astrazeneca GB 15,010 4.5

Johnson & Johnson US 14,478 4.3

Roche CH 13,814 4.1

Merck & Co US 13,631 4.1

Abbott US 9,570 2.9

Lilly US 8,335 2.5

Top 10 149,920 44.9

Amgen US 8,188 2.5

Wyeth (acquired by Pfizer) US 7,949 2.4

Bayer DE 7,020 2.1

Bristol-Myers Squibb US 6,519 2.0

Boehringer Ingelheim DE 6,277 1.9

Schering-Plough US 6,181 1.9

Takeda JP 5,479 1.6

Teva IL 5,300 1.6

Novo Nordisk DK 3,336 1.0

Daiichi Sankyo JP 2,925 0.9

Top 20 209,093 62.6

Europe, with two based in the UK (see Table 1). Despite this sources claim that Europe still made up at least one-third of the overall sales spend in 2007.9

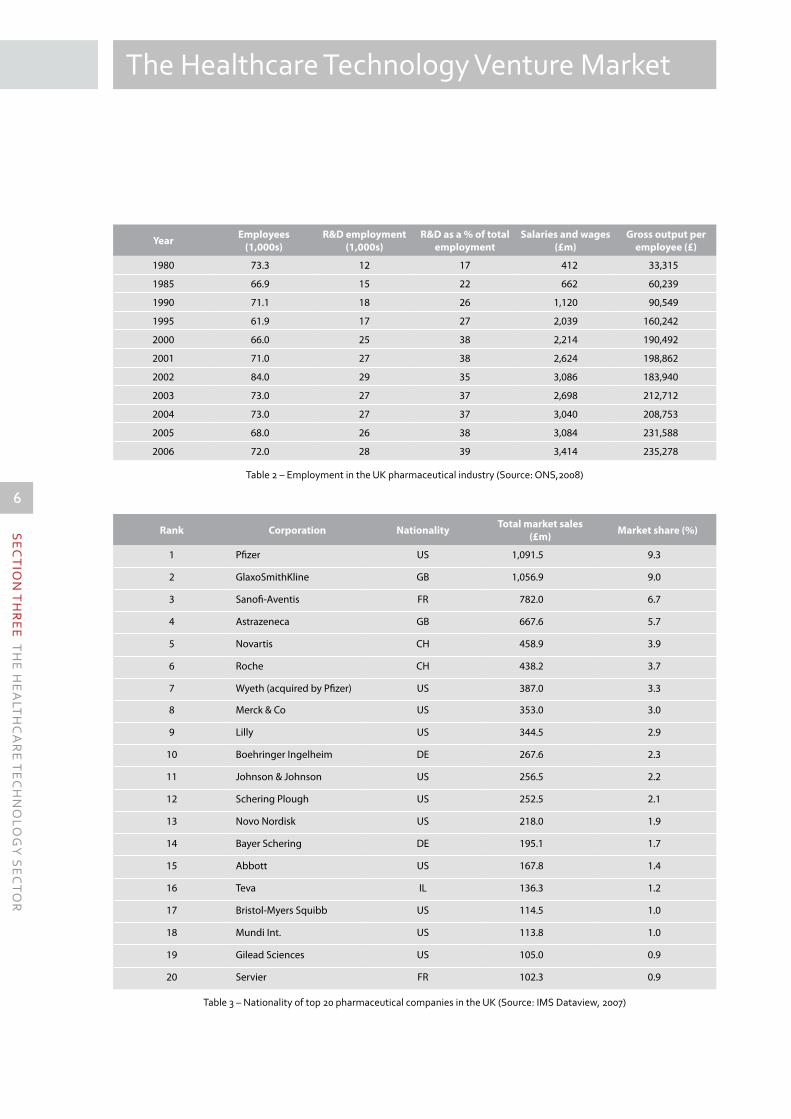

3.1.2. The UK pharmaceutical industryAs shown in Table 1, the UK is home to two of the world’s largest and most profitable pharmaceutical giants, the British founded GlaxoSmithKline and the Anglo-Swedish AstraZeneca. The UK pharmaceutical industry is estimated to be worth over US$19bn. It is directly responsible for 72,000 jobs, of which an estimated 28,000 are in R&D. This results in a gross output to the country of approximately £235,000 per employee (Table 2). An analysis of DTI and ONS data reveals that the pharmaceutical industry has used over a third of its sales revenue for R&D purposes in 2007. In line with this, ONS data shows that the pharmaceutical industry contributes over a quarter of the entire UK’s R&D spend.

Table 1 – Top world pharmaceutical corporations, 2007 (Source: IMS World Review 2007)

6

The Healthcare Technology Venture Market

SE

CT

ION

TH

RE

E T

HE

HE

ALT

HC

AR

E T

EC

HN

OLO

GY

SE

CT

OR

Year Employees (1,000s)

R&D employment (1,000s)

R&D as a % of total employment

Salaries and wages (£m)

Gross output per employee (£)

1980 73.3 12 17 412 33,315

1985 66.9 15 22 662 60,239

1990 71.1 18 26 1,120 90,549

1995 61.9 17 27 2,039 160,242

2000 66.0 25 38 2,214 190,492

2001 71.0 27 38 2,624 198,862

2002 84.0 29 35 3,086 183,940

2003 73.0 27 37 2,698 212,712

2004 73.0 27 37 3,040 208,753

2005 68.0 26 38 3,084 231,588

2006 72.0 28 39 3,414 235,278

Table 2 – Employment in the UK pharmaceutical industry (Source: ONS,2008)

Table 3 – Nationality of top 20 pharmaceutical companies in the UK (Source: IMS Dataview, 2007)

Rank Corporation Nationality Total market sales (£m) Market share (%)

1 Pfizer US 1,091.5 9.3

2 GlaxoSmithKline GB 1,056.9 9.0

3 Sanofi-Aventis FR 782.0 6.7

4 Astrazeneca GB 667.6 5.7

5 Novartis CH 458.9 3.9

6 Roche CH 438.2 3.7

7 Wyeth (acquired by Pfizer) US 387.0 3.3

8 Merck & Co US 353.0 3.0

9 Lilly US 344.5 2.9

10 Boehringer Ingelheim DE 267.6 2.3

11 Johnson & Johnson US 256.5 2.2

12 Schering Plough US 252.5 2.1

13 Novo Nordisk US 218.0 1.9

14 Bayer Schering DE 195.1 1.7

15 Abbott US 167.8 1.4

16 Teva IL 136.3 1.2

17 Bristol-Myers Squibb US 114.5 1.0

18 Mundi Int. US 113.8 1.0

19 Gilead Sciences US 105.0 0.9

20 Servier FR 102.3 0.9

7

SE

CT

ION

TH

RE

E T

HE

HE

ALT

HC

AR

E T

EC

HN

OLO

GY

SE

CT

OR

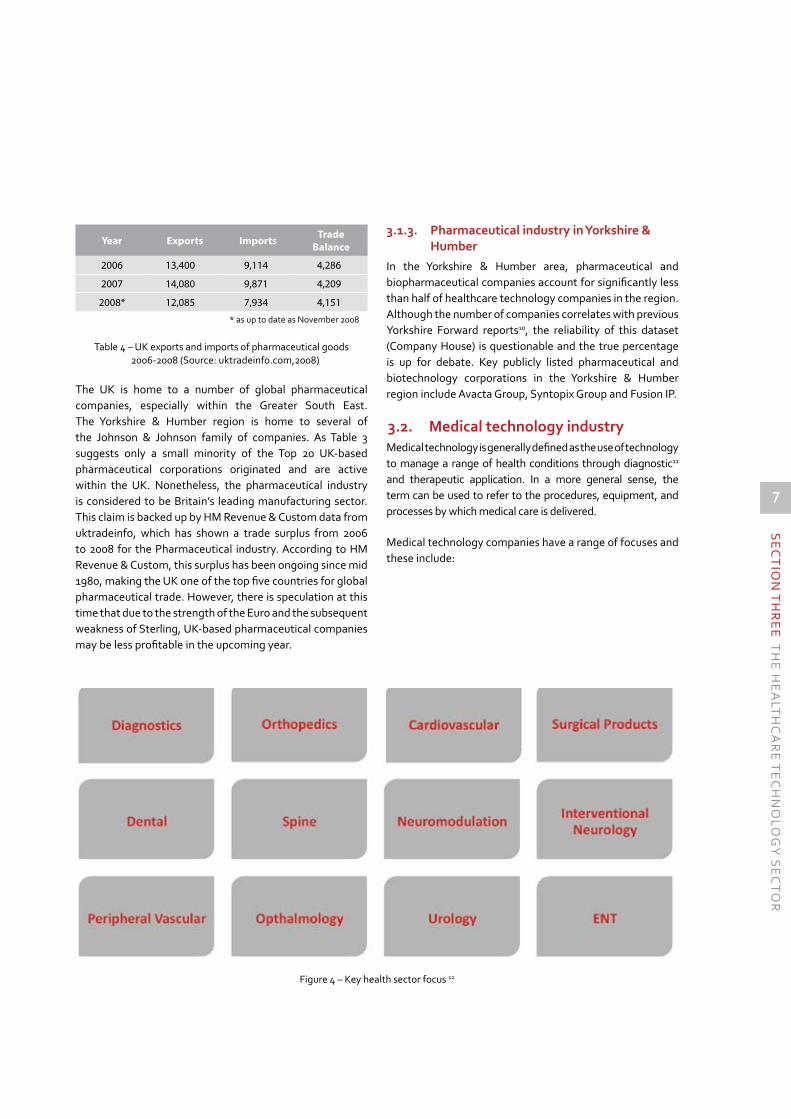

3.1.3. Pharmaceutical industry in Yorkshire & Humber

In the Yorkshire & Humber area, pharmaceutical and biopharmaceutical companies account for significantly less than half of healthcare technology companies in the region. Although the number of companies correlates with previous Yorkshire Forward reports10, the reliability of this dataset (Company House) is questionable and the true percentage is up for debate. Key publicly listed pharmaceutical and biotechnology corporations in the Yorkshire & Humber region include Avacta Group, Syntopix Group and Fusion IP.

3.2. Medical technology industryMedical technology is generally defined as the use of technology to manage a range of health conditions through diagnostic11 and therapeutic application. In a more general sense, the term can be used to refer to the procedures, equipment, and processes by which medical care is delivered.

Medical technology companies have a range of focuses and these include:

The UK is home to a number of global pharmaceutical companies, especially within the Greater South East. The Yorkshire & Humber region is home to several of the Johnson & Johnson family of companies. As Table 3 suggests only a small minority of the Top 20 UK-based pharmaceutical corporations originated and are active within the UK. Nonetheless, the pharmaceutical industry is considered to be Britain’s leading manufacturing sector. This claim is backed up by HM Revenue & Custom data from uktradeinfo, which has shown a trade surplus from 2006 to 2008 for the Pharmaceutical industry. According to HM Revenue & Custom, this surplus has been ongoing since mid 1980, making the UK one of the top five countries for global pharmaceutical trade. However, there is speculation at this time that due to the strength of the Euro and the subsequent weakness of Sterling, UK-based pharmaceutical companies may be less profitable in the upcoming year.

Year Exports Imports Trade Balance

2006 13,400 9,114 4,286

2007 14,080 9,871 4,209

2008* 12,085 7,934 4,151

* as up to date as November 2008

Table 4 – UK exports and imports of pharmaceutical goods 2006-2008 (Source: uktradeinfo.com,2008)

Figure 4 – Key health sector focus 12

8

The Healthcare Technology Venture Market

with an annual estimated cost of €192bn to the overall EU economy.

According to the WHO’s 2007 statistical data, heart disease and strokes account for 21.7% of deaths worldwide, while cardiovascular disease accounts for 30%. The WHO estimates that in 2015 almost 20 million people will die from a cardiovascular-related condition. This can all be related to both an ageing global population and a sustained rise in obesity. In fact, rising obesity levels are not only responsible for the growing number of cases of heart disease and strokes, but has also contributed to the rise in deaths related to diabetes. The WHO predicts that within the next ten years diabetes-related deaths will increase worldwide by more than 50%.

This in turn has created a viable marketplace with the cardiovascular device market expected to reach US$40.46bn by 2011 in North America alone. Cardiovascular medical technology products include cardiac rhythm management, heart valves, cardiac surgery systems, minimally-invasive image-guided technologies, interventional neurovascular technologies and heart assist devices and stents. An example of this is that the European drug-eluting stent market has been forecast to reach $4.5bn by year end this year, up from $1.6bn in 2001.14

Globally, the major cardiovascular device companies include Cordis (Johnson & Johnson), Medtronic, Boston Scientific, Guidant, St Jude Medical, Abbot, Sorin, Conor Medsystems and Biotronik.

3.2.3. DiagnosticsAs healthcare has improved, there has been an ever-increasing reliance on better and faster diagnostic tests. Such diagnostics include biotechnological-based testing as well as medical hardware.

The pace of technological change in the diagnostic market is enabling earlier and more accurate diagnoses of disease, improving clinical decisions and assisting more effective monitoring of treatment. The global market for in vitro diagnostics was valued in excess of US$38bn in 2007 and has been forecast to grow by 6.7% year on year until 2012. There are two diagnostic methods in particular that are seen as high growth areas: molecular diagnostics and point of care diagnostic tests. These are expected to exhibit a Compound Annual Growth (CAG) of 14% until 2010 from a base value of $2.6bn in 2005, and 7.8% until 2010 from a base of $12bn in 2005, respectively.

3.2.1. Medical technology product naming classification

Though the health sectors with which medical technology companies focus upon seem very well defined and limited, there is a huge range of products that can be developed for each area. Table 5 shows the common nomenclature developed by the Global Medical Device Nomenclature Agency.

Despite the plethora of health-related focii listed above, cardiovascular, diagnostics and orthopaedics are the largest therapy areas within medical technologies.

3.2.2. CardiovascularThis focus is on any medical technology, whether therapeutic, diagnostic or procedural, that deals with disease or the prevention of disease relating to the cardiovascular system.

It is estimated that the two most common occurrences of cardiovascular disease, heart disease and strokes, cost the US $448.5bn in 2008.13 In line with this trend, cardiovascular disease is considered to be the major cause of death in the European Union, killing over 2 million people each year

SE

CT

ION

TH

RE

E T

HE

HE

ALT

HC

AR

E T

EC

HN

OLO

GY

SE

CT

OR

Term Examples

Active implantable technology

Cardiac pacemakers, neurostimulator, etc.

Anaesthetic and respiratory technology

Anaesthetic and respiratory technology

Dental technologyDentistry tools, alloys, resins, dental floss, brush, etc.

Electromechanical medical technology

X-ray machine, scanner, laser, etc.

Hospital hardware Hospital bed, etc.

In-vitro diagnostic technologyPregnancy, blood glucose, genetic tests, etc.

Nonactive implantable technology

Hip, knee joint replacement, cardiac stent

Ophthalmic and optical technology

Eye glasses, contact lenses, ophtalmoscope, etc.

Reusable instruments Various surgical instruments

Single use technologySyringes, needles, gloves, balloon catheters, etc.

Technical aids for disabled per sons

Wheelchair, walking aid, hearing aid, electrical bed, etc.

Diagnostic and therapeutic radiation technology

Radiotherapy units

Table 5 - Global medical device nomenclature (Source: Global Medical Device Nomenclature Agency, 2009)

9

of years ago in the areas of reconstructive devices and joint replacements, spinal implants and instrumentation, fracture repair and orthobiologics.

In 2007, the European market for orthopaedic devices was valued at around $3bn. On a global scale, worldwide sales reached $25.9bn and it is estimated that by 2010 the sector will top $44bn in global revenues.

Globally, the major orthopaedic medical technology companies include Smith & Nephew, based in York, and DePuy (Johnson & Johnson) which is based in Leeds.

3.2.4. OrthopaedicsOrthopaedic conditions affect hundreds of millions of people throughout the world. According to recent reports orthopaedic conditions account for up to half of all chronic conditions in people over the age of 50 in developed countries, a figure that is set to double by 2020. Combined with the fact that a fifth of all visits to outpatient clinics worldwide are for musculo-skeletal conditions, a focus on orthopaedics by medical technology companies seems an obvious and lucrative choice.

The main products seen within this sector are divided into a number of different fields, with strong growth seen a number

SE

CT

ION

TH

RE

E T

HE

HE

ALT

HC

AR

E T

EC

HN

OLO

GY

SE

CT

OR

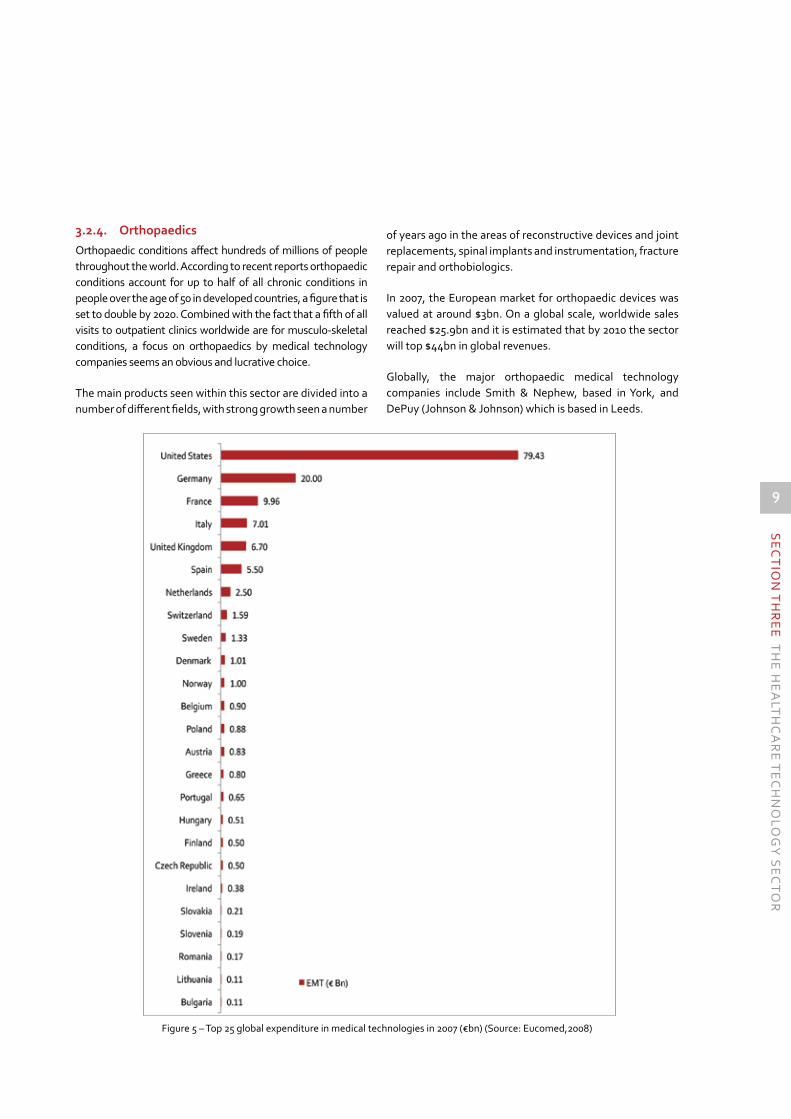

Figure 5 – Top 25 global expenditure in medical technologies in 2007 (€bn) (Source: Eucomed,2008)

10

The Healthcare Technology Venture Market

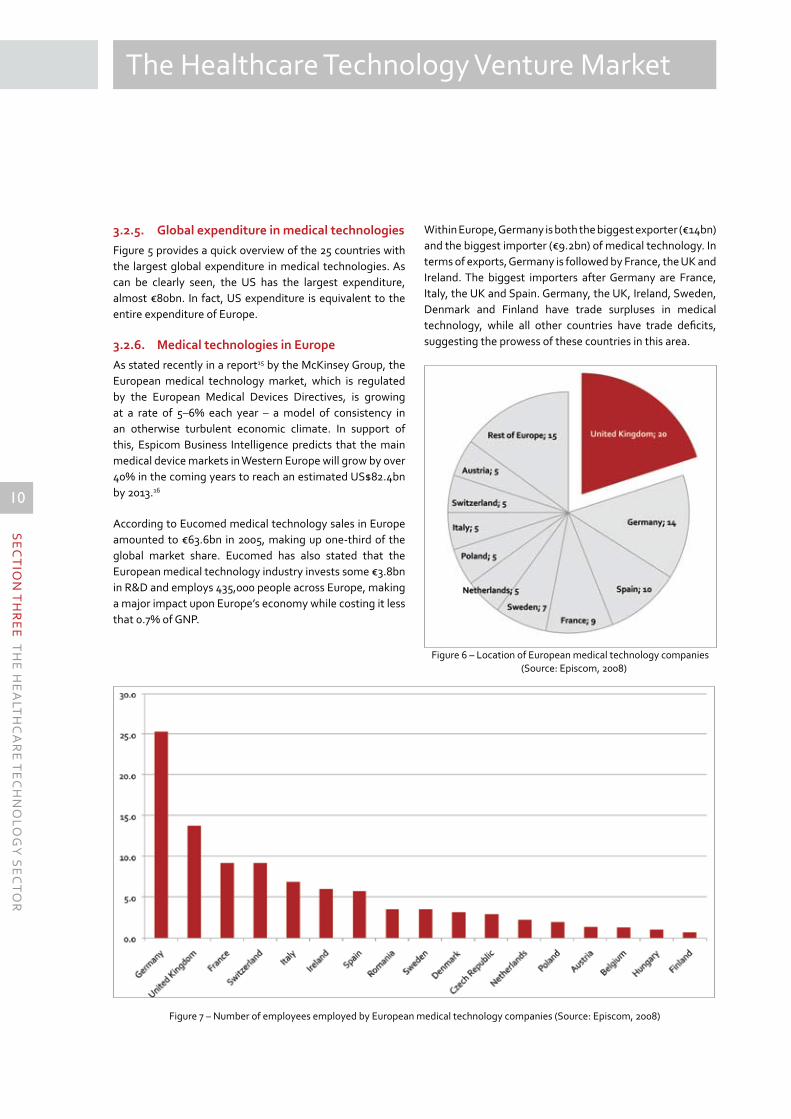

Within Europe, Germany is both the biggest exporter (€14bn) and the biggest importer (€9.2bn) of medical technology. In terms of exports, Germany is followed by France, the UK and Ireland. The biggest importers after Germany are France, Italy, the UK and Spain. Germany, the UK, Ireland, Sweden, Denmark and Finland have trade surpluses in medical technology, while all other countries have trade deficits, suggesting the prowess of these countries in this area.

3.2.5. Global expenditure in medical technologiesFigure 5 provides a quick overview of the 25 countries with the largest global expenditure in medical technologies. As can be clearly seen, the US has the largest expenditure, almost €80bn. In fact, US expenditure is equivalent to the entire expenditure of Europe.

3.2.6. Medical technologies in EuropeAs stated recently in a report15 by the McKinsey Group, the European medical technology market, which is regulated by the European Medical Devices Directives, is growing at a rate of 5–6% each year – a model of consistency in an otherwise turbulent economic climate. In support of this, Espicom Business Intelligence predicts that the main medical device markets in Western Europe will grow by over 40% in the coming years to reach an estimated US$82.4bn by 2013.16

According to Eucomed medical technology sales in Europe amounted to €63.6bn in 2005, making up one-third of the global market share. Eucomed has also stated that the European medical technology industry invests some €3.8bn in R&D and employs 435,000 people across Europe, making a major impact upon Europe’s economy while costing it less that 0.7% of GNP.

SE

CT

ION

TH

RE

E T

HE

HE

ALT

HC

AR

E T

EC

HN

OLO

GY

SE

CT

OR

Figure 6 – Location of European medical technology companies (Source: Episcom, 2008)

Figure 7 – Number of employees employed by European medical technology companies (Source: Episcom, 2008)

11

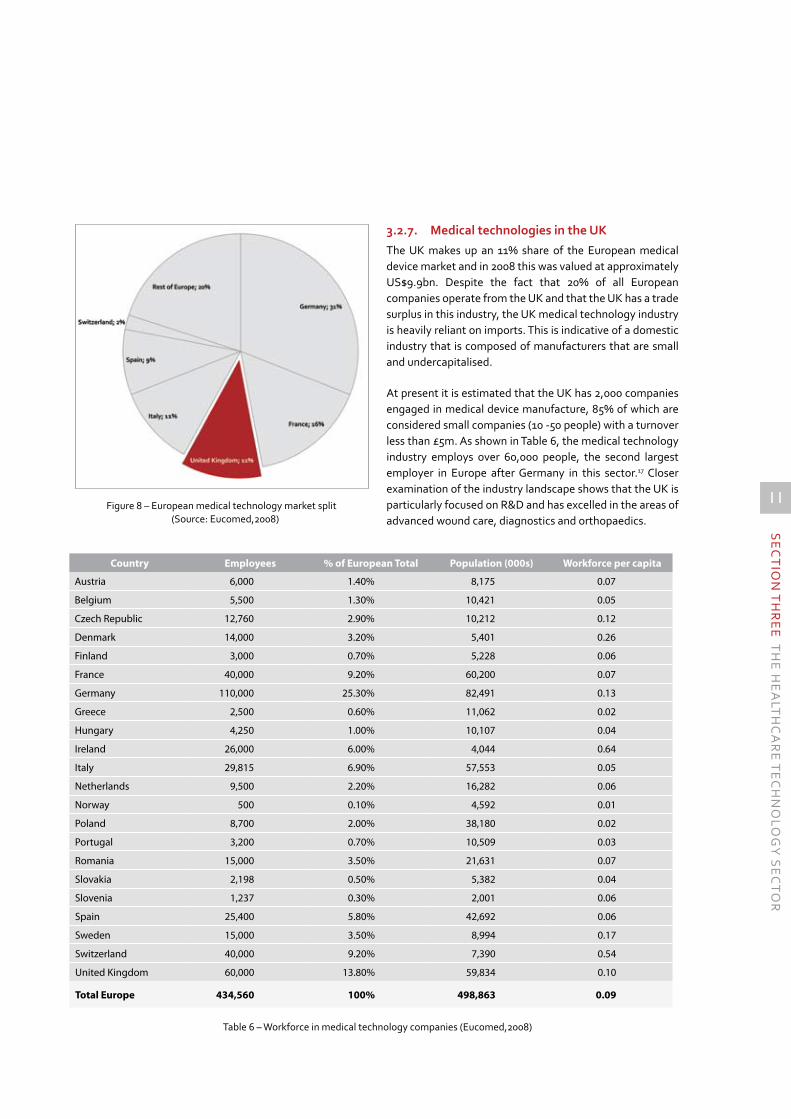

3.2.7. Medical technologies in the UKThe UK makes up an 11% share of the European medical device market and in 2008 this was valued at approximately US$9.9bn. Despite the fact that 20% of all European companies operate from the UK and that the UK has a trade surplus in this industry, the UK medical technology industry is heavily reliant on imports. This is indicative of a domestic industry that is composed of manufacturers that are small and undercapitalised.

At present it is estimated that the UK has 2,000 companies engaged in medical device manufacture, 85% of which are considered small companies (10 -50 people) with a turnover less than £5m. As shown in Table 6, the medical technology industry employs over 60,000 people, the second largest employer in Europe after Germany in this sector.17 Closer examination of the industry landscape shows that the UK is particularly focused on R&D and has excelled in the areas of advanced wound care, diagnostics and orthopaedics.

SE

CT

ION

TH

RE

E T

HE

HE

ALT

HC

AR

E T

EC

HN

OLO

GY

SE

CT

OR

Figure 8 – European medical technology market split (Source: Eucomed,2008)

Country Employees % of European Total Population (000s) Workforce per capita

Austria 6,000 1.40% 8,175 0.07

Belgium 5,500 1.30% 10,421 0.05

Czech Republic 12,760 2.90% 10,212 0.12

Denmark 14,000 3.20% 5,401 0.26

Finland 3,000 0.70% 5,228 0.06

France 40,000 9.20% 60,200 0.07

Germany 110,000 25.30% 82,491 0.13

Greece 2,500 0.60% 11,062 0.02

Hungary 4,250 1.00% 10,107 0.04

Ireland 26,000 6.00% 4,044 0.64

Italy 29,815 6.90% 57,553 0.05

Netherlands 9,500 2.20% 16,282 0.06

Norway 500 0.10% 4,592 0.01

Poland 8,700 2.00% 38,180 0.02

Portugal 3,200 0.70% 10,509 0.03

Romania 15,000 3.50% 21,631 0.07

Slovakia 2,198 0.50% 5,382 0.04

Slovenia 1,237 0.30% 2,001 0.06

Spain 25,400 5.80% 42,692 0.06

Sweden 15,000 3.50% 8,994 0.17

Switzerland 40,000 9.20% 7,390 0.54

United Kingdom 60,000 13.80% 59,834 0.10

Total Europe 434,560 100% 498,863 0.09

Table 6 – Workforce in medical technology companies (Eucomed,2008)

12

The Healthcare Technology Venture Market

SE

CT

ION

TH

RE

E T

HE

HE

ALT

HC

AR

E T

EC

HN

OLO

GY

SE

CT

OR

3.3. Medical technologies Yorkshire and Humber

According to UK Trade and Investment (UKTI), and the latest ONS and Companies House data, Yorkshire has the UK’s highest concentration of medical device companies. Over 200 firms involved within the medical technology industry have a base in Yorkshire, employing some 7,000 staff and producing an output of over £450m. These companies include a large number of medical device firms, particularly within the orthopaedic and medical devices arena, including:

Reckitt Benckiser; www.reckittbenckiser.com•

DePuy International (a Johnson & Johnson company); • www.depuy.com

Smith and Nephew; www.global.smith-nephew.com•

Swann-Morton; www.swann-morton.com•

Tunstall Healthcare; www.tunstall.co.uk•

It is believed that the existing presence of these firms plays a substantial role in the attractiveness of the area for new investments.

It should be noted that there are a number of companies that have originated from and are still based in the region. These include Dawmed Systems, 1st Dental Laboratories, Medical House and Surgical Innovations Group.

13

4.1. Where do healthcare technology companies originate from?

The products and services of healthcare technology companies are often based on experience gained by former academics or researchers at R&D departments of technology corporations. The scientific discoveries of academics are usually commercialised through university spin-out companies that acquire the intellectual property rights from the incubator organisation in exchange for an equity stake or the payment of a licensing fee. The same mechanism can also be used for corporate spin-outs. By contrast, start-up companies are often founded by entrepreneurs who have a strong professional background and the necessary scientific expertise to start a new company with a unique selling position.

An analysis of UK-based healthcare technology companies that have received investments over the past two years shows that the majority of companies began as independent start-ups, followed by university spin-outs, spin-outs from non-university research organisations, and corporate spin-outs.

Across the different healthcare technology areas there is a distinct pattern of where healthcare technology companies originate from. For example, pharmaceutical and drug development companies do not usually originate from universities (unlike medical technology companies). Despite this, many entrepreneurs who have started companies have done so with an extensive background in healthcare research within public research organisations or large corporations.

4.2. Is the United Kingdom a good place to attract venture capital investments?

There are many factors that influence the provision of venture capital within a country and all European countries have made a commitment – verbally at least - to improve the conditions surrounding the supply and demand of venture capital. The impact of factors such as the entrepreneurial

Of the different sources of finance available to entrepreneurs venture capital plays only a minor role. To put this in context, of the 1.2m companies in the UK only around 2,000, or 0.16%, have received venture capital investments. However, experts estimate that up to 80% of the fastest growing companies, in terms of both revenue and employment, have received venture capital investment during their life cycle. Most of the world’s biggest healthcare companies including Amgen, Genentech, Biogen and others have at some point received venture capital investments or, like General Electric, Medtronic, Johnson & Johnson and Amgen, have their own venture capital activities that invest into the industry.

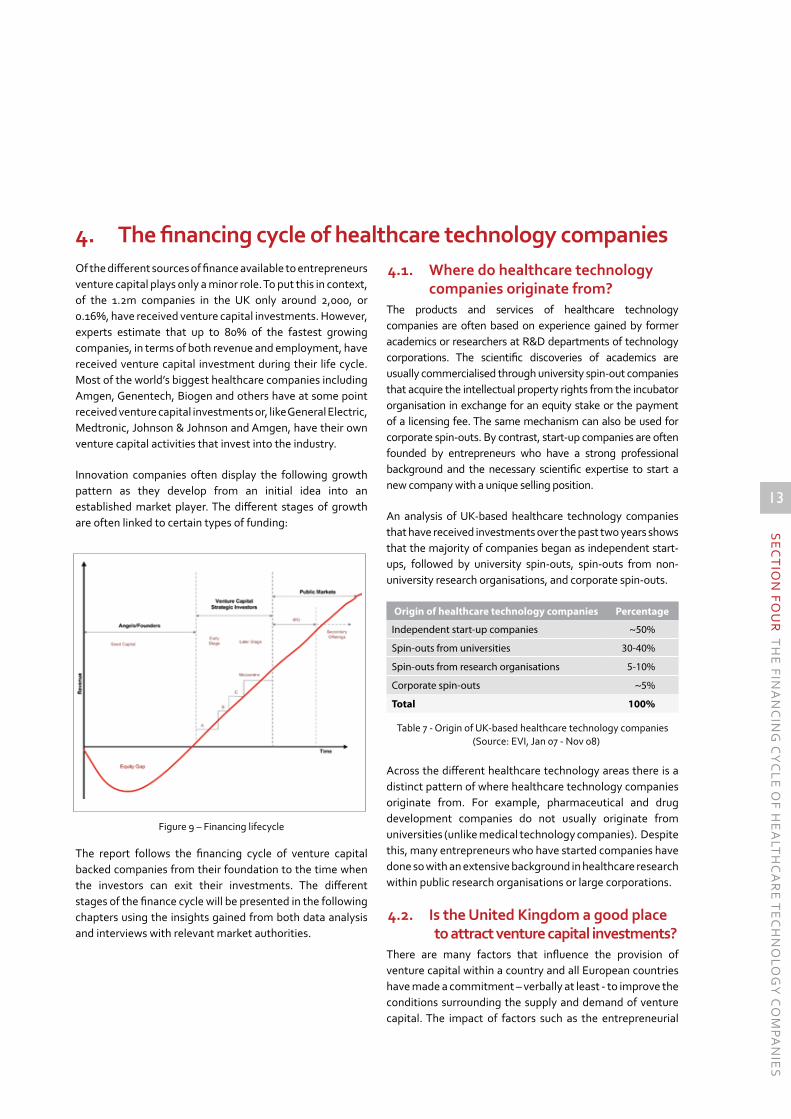

Innovation companies often display the following growth pattern as they develop from an initial idea into an established market player. The different stages of growth are often linked to certain types of funding:

The report follows the financing cycle of venture capital backed companies from their foundation to the time when the investors can exit their investments. The different stages of the finance cycle will be presented in the following chapters using the insights gained from both data analysis and interviews with relevant market authorities.

SE

CT

ION

FOU

R T

HE

FINA

NC

ING

CY

CLE

OF H

EA

LTH

CA

RE

TE

CH

NO

LOG

Y C

OM

PAN

IES

Figure 9 – Financing lifecycle

Origin of healthcare technology companies Percentage

Independent start-up companies ~50%

Spin-outs from universities 30-40%

Spin-outs from research organisations 5-10%

Corporate spin-outs ~5%

Total 100%

Table 7 - Origin of UK-based healthcare technology companies (Source: EVI, Jan 07 - Nov 08)

4. Thefinancingcycleofhealthcaretechnologycompanies

14

The Healthcare Technology Venture Market

4.3. Is this also true for healthcare technology companies?

The healthcare technology venture capital market is the second largest sector behind the information and telecommunications sector. Around 24% of all European deals and 29% of all UK deals are invested into healthcare technology, meaning that nearly every third deal in the UK is healthcare-related.

climate, legal and tax frameworks, a country’s innovative capacity and so forth, on the venture capital market has been discussed extensively elsewhere and is not the subject of this report.18

At the outset an entrepreneur is mostly inflexible regarding the decision of where to locate the company. While spin-out companies often choose an initial location close to their incubator organisation, start-up companies are normally based near to where the entrepreneur lives.

Entrepreneurs who start a company in the UK can benefit from the most active venture capital market in Europe with 29% of all European investments (1,076 deals) and 27% of all disclosed investment (£2.16bn) going into UK-based companies. In terms of deal activity per capita, the United Kingdom is comparable to the United States.19 Between 2007 and 2008 at least 3,600 deals were closed between investors from all over the world and entrepreneurs with European-based companies.

The total disclosed amount invested in the 2,070 recorded deals in the UK was £8bn, meaning a European-based company could secure an average of nearly £3.9m per deal. The average deal size for a UK-based company is, at £2.9m, significantly lower than for companies in the rest of Europe. But this is not necessarily all bad news for national entrepreneurs as the drop in the average value is possibly a result of the higher disclosure rates for smaller venture capital deals in the UK.

SE

CT

ION

FOU

R T

HE

FINA

NC

ING

CY

CLE

OF H

EA

LTH

CA

RE

TE

CH

NO

LOG

Y C

OM

PAN

IES

Europe (incl. UK) UK Ratio

All venture capital backed deals

Number of venture capital backed deals 3,668 1,076 29%

Number of investments with disclosed deal amount

2,070 748 36%

Total deal amount (£m) 8,034 2,160 27%

Average investment amount (£m) 3.9 2.9 74%

Table 8 – Overview of European venture capital investments (Source: EVI, Jan 07 - Nov 08)

Figure 10 – Distribution venture capital investments across sectors in Europe in 2007 (based on 1,492 deals) (Source: EVI, 2007)

15

SE

CT

ION

FOU

R T

HE

FINA

NC

ING

CY

CLE

OF H

EA

LTH

CA

RE

TE

CH

NO

LOG

Y C

OM

PAN

IES

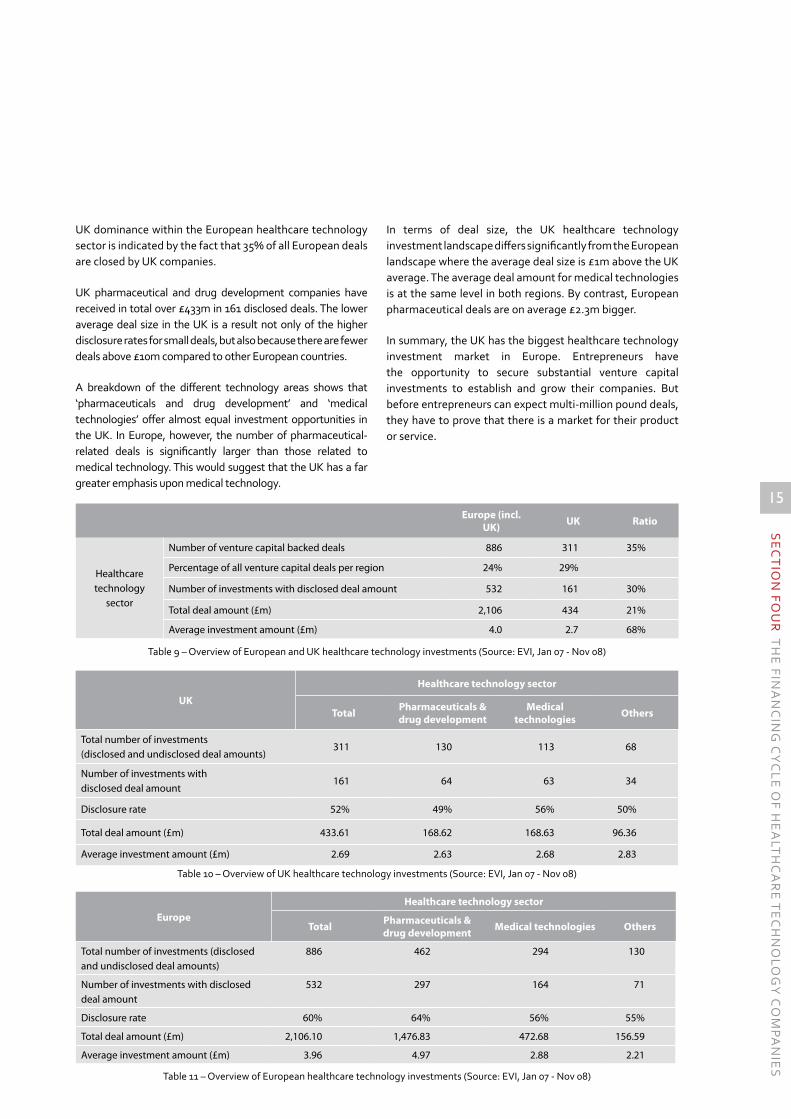

In terms of deal size, the UK healthcare technology investment landscape differs significantly from the European landscape where the average deal size is £1m above the UK average. The average deal amount for medical technologies is at the same level in both regions. By contrast, European pharmaceutical deals are on average £2.3m bigger.

In summary, the UK has the biggest healthcare technology investment market in Europe. Entrepreneurs have the opportunity to secure substantial venture capital investments to establish and grow their companies. But before entrepreneurs can expect multi-million pound deals, they have to prove that there is a market for their product or service.

UK dominance within the European healthcare technology sector is indicated by the fact that 35% of all European deals are closed by UK companies.

UK pharmaceutical and drug development companies have received in total over £433m in 161 disclosed deals. The lower average deal size in the UK is a result not only of the higher disclosure rates for small deals, but also because there are fewer deals above £10m compared to other European countries.

A breakdown of the different technology areas shows that ‘pharmaceuticals and drug development’ and ‘medical technologies’ offer almost equal investment opportunities in the UK. In Europe, however, the number of pharmaceutical-related deals is significantly larger than those related to medical technology. This would suggest that the UK has a far greater emphasis upon medical technology.

Europe (incl. UK) UK Ratio

Healthcare technology

sector

Number of venture capital backed deals 886 311 35%

Percentage of all venture capital deals per region 24% 29%

Number of investments with disclosed deal amount 532 161 30%

Total deal amount (£m) 2,106 434 21%

Average investment amount (£m) 4.0 2.7 68%

Table 9 – Overview of European and UK healthcare technology investments (Source: EVI, Jan 07 - Nov 08)

Table 11 – Overview of European healthcare technology investments (Source: EVI, Jan 07 - Nov 08)

Table 10 – Overview of UK healthcare technology investments (Source: EVI, Jan 07 - Nov 08)

UK

Healthcare technology sector

Total Pharmaceuticals & drug development

Medical technologies Others

Total number of investments (disclosed and undisclosed deal amounts)

311 130 113 68

Number of investments with disclosed deal amount

161 64 63 34

Disclosure rate 52% 49% 56% 50%

Total deal amount (£m) 433.61 168.62 168.63 96.36

Average investment amount (£m) 2.69 2.63 2.68 2.83

EuropeHealthcare technology sector

Total Pharmaceuticals & drug development Medical technologies Others

Total number of investments (disclosed and undisclosed deal amounts)

886 462 294 130

Number of investments with disclosed deal amount

532 297 164 71

Disclosure rate 60% 64% 56% 55%

Total deal amount (£m) 2,106.10 1,476.83 472.68 156.59

Average investment amount (£m) 3.96 4.97 2.88 2.21

16

The Healthcare Technology Venture Market

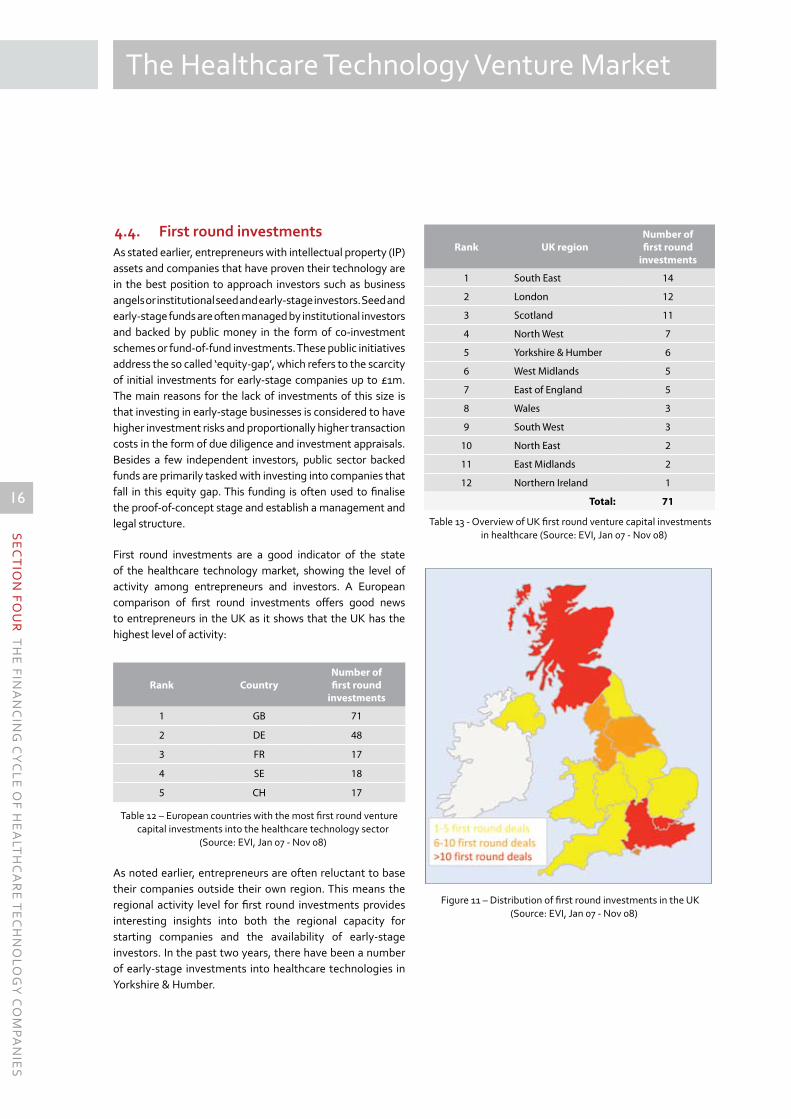

4.4. First round investmentsAs stated earlier, entrepreneurs with intellectual property (IP) assets and companies that have proven their technology are in the best position to approach investors such as business angels or institutional seed and early-stage investors. Seed and early-stage funds are often managed by institutional investors and backed by public money in the form of co-investment schemes or fund-of-fund investments. These public initiatives address the so called ‘equity-gap’, which refers to the scarcity of initial investments for early-stage companies up to £1m. The main reasons for the lack of investments of this size is that investing in early-stage businesses is considered to have higher investment risks and proportionally higher transaction costs in the form of due diligence and investment appraisals. Besides a few independent investors, public sector backed funds are primarily tasked with investing into companies that fall in this equity gap. This funding is often used to finalise the proof-of-concept stage and establish a management and legal structure.

First round investments are a good indicator of the state of the healthcare technology market, showing the level of activity among entrepreneurs and investors. A European comparison of first round investments offers good news to entrepreneurs in the UK as it shows that the UK has the highest level of activity:

As noted earlier, entrepreneurs are often reluctant to base their companies outside their own region. This means the regional activity level for first round investments provides interesting insights into both the regional capacity for starting companies and the availability of early-stage investors. In the past two years, there have been a number of early-stage investments into healthcare technologies in Yorkshire & Humber.

SE

CT

ION

FOU

R T

HE

FINA

NC

ING

CY

CLE

OF H

EA

LTH

CA

RE

TE

CH

NO

LOG

Y C

OM

PAN

IES

Table 12 – European countries with the most first round venture capital investments into the healthcare technology sector

(Source: EVI, Jan 07 - Nov 08)

Rank CountryNumber of first round

investments

1 GB 71

2 DE 48

3 FR 17

4 SE 18

5 CH 17

Table 13 - Overview of UK first round venture capital investments in healthcare (Source: EVI, Jan 07 - Nov 08)

Figure 11 – Distribution of first round investments in the UK (Source: EVI, Jan 07 - Nov 08)

Rank UK regionNumber of first round

investments

1 South East 14

2 London 12

3 Scotland 11

4 North West 7

5 Yorkshire & Humber 6

6 West Midlands 5

7 East of England 5

8 Wales 3

9 South West 3

10 North East 2

11 East Midlands 2

12 Northern Ireland 1

Total: 71

17

SE

CT

ION

FOU

R T

HE

FINA

NC

ING

CY

CLE

OF H

EA

LTH

CA

RE

TE

CH

NO

LOG

Y C

OM

PAN

IES

close relationships with universities and invest primarily in university spin-out companies.

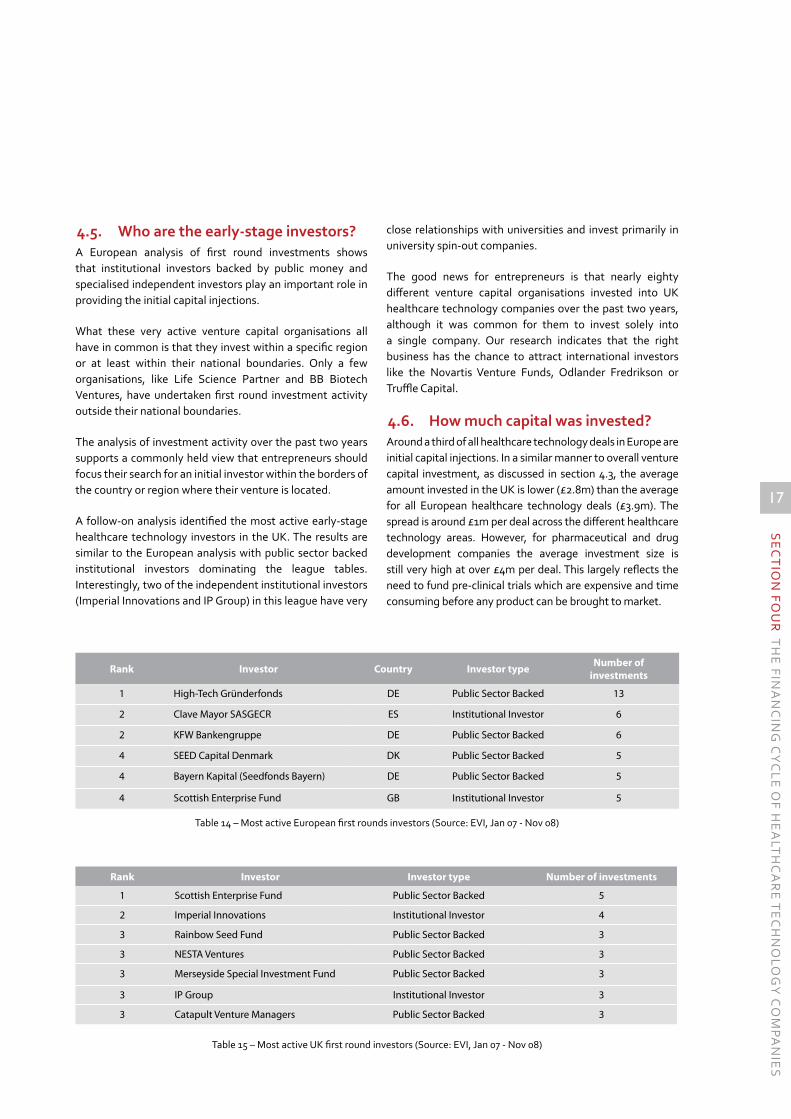

The good news for entrepreneurs is that nearly eighty different venture capital organisations invested into UK healthcare technology companies over the past two years, although it was common for them to invest solely into a single company. Our research indicates that the right business has the chance to attract international investors like the Novartis Venture Funds, Odlander Fredrikson or Truffle Capital.

4.6. How much capital was invested? Around a third of all healthcare technology deals in Europe are initial capital injections. In a similar manner to overall venture capital investment, as discussed in section 4.3, the average amount invested in the UK is lower (£2.8m) than the average for all European healthcare technology deals (£3.9m). The spread is around £1m per deal across the different healthcare technology areas. However, for pharmaceutical and drug development companies the average investment size is still very high at over £4m per deal. This largely reflects the need to fund pre-clinical trials which are expensive and time consuming before any product can be brought to market.

4.5. Who are the early-stage investors? A European analysis of first round investments shows that institutional investors backed by public money and specialised independent investors play an important role in providing the initial capital injections.

What these very active venture capital organisations all have in common is that they invest within a specific region or at least within their national boundaries. Only a few organisations, like Life Science Partner and BB Biotech Ventures, have undertaken first round investment activity outside their national boundaries.

The analysis of investment activity over the past two years supports a commonly held view that entrepreneurs should focus their search for an initial investor within the borders of the country or region where their venture is located.

A follow-on analysis identified the most active early-stage healthcare technology investors in the UK. The results are similar to the European analysis with public sector backed institutional investors dominating the league tables. Interestingly, two of the independent institutional investors (Imperial Innovations and IP Group) in this league have very

Table 14 – Most active European first rounds investors (Source: EVI, Jan 07 - Nov 08)

Table 15 – Most active UK first round investors (Source: EVI, Jan 07 - Nov 08)

Rank Investor Country Investor type Number of investments

1 High-Tech Gründerfonds DE Public Sector Backed 13

2 Clave Mayor SASGECR ES Institutional Investor 6

2 KFW Bankengruppe DE Public Sector Backed 6

4 SEED Capital Denmark DK Public Sector Backed 5

4 Bayern Kapital (Seedfonds Bayern) DE Public Sector Backed 5

4 Scottish Enterprise Fund GB Institutional Investor 5

Rank Investor Investor type Number of investments

1 Scottish Enterprise Fund Public Sector Backed 5

2 Imperial Innovations Institutional Investor 4

3 Rainbow Seed Fund Public Sector Backed 3

3 NESTA Ventures Public Sector Backed 3

3 Merseyside Special Investment Fund Public Sector Backed 3

3 IP Group Institutional Investor 3

3 Catapult Venture Managers Public Sector Backed 3

18

The Healthcare Technology Venture Market

by strong research universities and a substantial capacity for spin-out companies which traditionally receive lower first round investments than independent start-up companies.

4.7. Follow-on investment roundsThe high cash-burn rates of research-based companies means that they immediately have to look for follow-on funding. The next funding round, usually referred to as a Series A round, often involves investment sizes from around £1m up to several million pounds. These investment rounds are often led by recognised national institutional investors while other investors join the deal in a syndicate (syndicated deal). At these relatively early stages in a company’s development, a syndicate of investors often rely upon a lead investor to monitor the company closely and to provide hands-on support while the rest of the syndicate can be located all over world. Consequently, it is rare that overseas investors take the lead in a Series A investment round.

An additional aspect to consider at Series A is that venture capital organisations have become more specialised with a later stage focus. Whereas early-stage investors often invest across different sectors, later-stage investors often have more specialised teams for specific technologies and sectors.

In the UK the average size of a first round investment is up to 50% lower than the European average. However, the disclosure rates are 17% higher, indicating that more deals for smaller amounts have been disclosed. The average deal amount for first round investments into pharmaceutical and drug development companies is, at £2.44m, almost identical to the average investment amount of all deals in this sector, at £2.63m. By contrast, deals into medical technologies and other healthcare technology areas tend to be smaller.

Despite the data indicated in Tables 16 and 17, first round investments can still be large, such as the £33m investment into the Belgium-based drug development company Movetis. Founded in 2006, the company received investments in January 2007 from BIP Investment Partners, GIMV, KBC Private Equity, Life Sciences Partners, Quest for Growth, and Sofinnova Partners. In the UK in 2007, Vantia Therapeutics, benefiting from its position as a spin-out of Ferring Research Ltd, received £19m from MVM, Novo and SV Life Sciences.

A more detailed analysis of Europe and the UK shows that the average deal size in Yorkshire & Humber region is far below the European and UK average. This is probably related to the fact that the Yorkshire & Humber region is characterised

SE

CT

ION

FOU

R T

HE

FINA

NC

ING

CY

CLE

OF H

EA

LTH

CA

RE

TE

CH

NO

LOG

Y C

OM

PAN

IES

Europe TotalPharmaceuticals &

drug development

Medical technologies Others

Total number of first round investment (Disclosed and undisclosed deal amounts)

280 118 113 49

Number of first round investments with disclosed deal amount

138 66 54 18

Disclosure Rate 49% 56% 48% 37%

Deal amount of first round investments (£000s) 392,364 268,852 95,933 27,579

Average amount of first round investments (£000s) 2,843 4,074 1,777 1,532

Table 16 - Overview of first round investments in Europe (Source: EVI, Jan 07 - Nov 08)

Table 17 – Overview of first round investments in the UK (Source: EVI, Jan 07 - Nov 08)

UK Total Pharmaceuticals & drug development

Medical technologies Others

Total number of first round investment (Disclosed and undisclosed deal amounts)

71 22 30 19

Number of first round investments with disclosed deal amount

47 17 22 8

Disclosure Rate 66% 77% 73% 42%

Deal amount of first round investments (£000s) 65,891 41,555 18,716 5,620

Average amount of first round investments (£000s) 1,402 2,444 851 703

19

SE

CT

ION

FOU

R T

HE

FINA

NC

ING

CY

CLE

OF H

EA

LTH

CA

RE

TE

CH

NO

LOG

Y C

OM

PAN

IES

sector-backed investors like High-Tech Gründerfonds, Bayern Kapital (Seedfonds Bayern), Scottish Enterprise Fund and the German state-owned bank KfW.

Investors can also specialise in certain areas within the healthcare technology sector. For example, there is a clear difference between the venture funds that back drug development companies and those that back medical technology companies. The regulatory requirements for new drugs result in a long time-to-market period for new products and the cash requirements for drug development companies are among the highest of all sectors. Although the development of medical technology products is also

4.7.1. European investors in healthcare technology companies

Around 300 institutional investors, corporations and other investment organisations have invested in European healthcare technology companies over the past two years. The majority of them have only participated in one investment (around 200) and a small number have participated in two investments (around 50). Less than 50 investors have participated in more than two investments.

The most active investors are mainly from the UK and Germany, including established institutional investors like Sofinnova Partners and Life Science Partners; and public

Table 18 – Overview of first round investments in Yorkshire & Humber (Source: EVI, Jan 07 - Nov 08)

Table 19 – Most active investors in the European healthcare technology sector (Source: EVI, Jan 07 - Nov 08)

Yorkshire & Humber TotalPharmaceuticals

and drug development

Medical technologies Others

Total number of first round investment (Disclosed and undisclosed deal amounts)

6 2 4 6

Number of first round investments with disclosed deal amount

4 2 2 0

Disclosure rate 67% 100% 50% n.a.

Deal amount of first round investments (£000s) 1,435 650 785 n.a.

Average amount of first round investments (£000s) 359 325 393 n.a.

Rank Most active investors in healthcare technologies Country Type of investor Number of

investments

1 Scottish Enterprise Fund GB Public Sector Backed 27

2 High-Tech Gründerfonds DE Public Private Backed 26

3 KfW Bankengruppe DE Public Sector Backed 21

4 MIG Fonds DE Institutional Investor 15

5 Sofinnova Partners FR Institutional Investor 14

6 Imperial Innovations GB Institutional Investor 12

6 Catapult Venture Managers GB Public Sector Backed 12

6 Bayern Kapital (Seedfonds Bayern) DE Public Sector Backed 12

9 Atlas Venture GB Institutional Investor 11

9 SEED Capital Denmark DK Institutional Investor 11

9 Life Sciences Partners DE Institutional Investor 11

12 IBG Beteiligungsgesellschaft Sachsen-Anhalt DE Public Sector Backed 10

12 Société Générale Asset Management FR Institutional Investor 10

12 Auriga Partners FR Institutional Investor 10

12 HealthCap Venture Capital SE Institutional Investor 10

12 Novo GB Institutional Investor 10

12 Oxford Technology Management GB Institutional Investor 10

12 NESTA Ventures GB Public Sector Backed 10

20

The Healthcare Technology Venture Market

public backed investors like Scottish Enterprise, KfW and the High-Tech Gründerfonds populate both tables, Table 20 indicates that the pharmaceuticals venture capital market is lead by sector specialist Sofinnova Partners, followed by MIG Fonds, Novo, Atlas Venture, Life Science Partners, TVM Capital, Augira Partners and MVM Life Science Partners; all of whom have dedicated life science investment teams.

In terms of medical technology, the picture is more diverse and, as Table 21 shows, public sector backed investors again rank well.

SE

CT

ION

FOU

R T

HE

FINA

NC

ING

CY

CLE

OF H

EA

LTH

CA

RE

TE

CH

NO

LOG

Y C

OM

PAN

IES

embedded in a complex regulatory framework, this sector has more similarities to the development of products and services in other non-healthcare related sectors and has a significantly shorter time-to-market. Tables 20 and 21 provide an overview of the most active investors in pharmaceuticals and drug development, and medical technology.

Tables 20 and 21 replicate Tables 14 and 15, highlighting the most active early-stage investors. What is obvious from Table 20 and 21 is the level of specialisation among the investors, particularly in pharmaceuticals and drug development. While

Table 20 – Overview of the most active investors in pharmaceuticals and drug development (Source: EVI, Jan 07 - Nov 08)

Table 21 – Overview of the most active medical technology investors (Source: EVI, Jan 07 - Nov 08)

Rank Most active investors in medical technologies Country Number of investments

1 Scottish Enterprise Fund GB 13

2 High-Tech Gründerfonds Management DE 12

3 NESTA Ventures GB 7

4 KfW Bankengruppe DE 6

4 Bayern Kapital (Seedfonds Bayern) DE 6

4 Imperial Innovations GB 6

4 Wellington Partners Venture Capital DE 6

5 Odlander, Fredrikson & Co(HealthCap Venture Capital) SE 5

5 Oxford Technology Management GB 5

5 OTC Asset Management FR 5

5 Catapult Venture Managers GB 5

5 IP Group GB 5

Rank Most active investors in pharmaceuticals and drug development Country Number of investments

1 Sofinnova Partners FR 14

1 KfW Bankengruppe DE 14

3 MIG Fonds DE 13

4 Scottish Enterprise Fund GB 12

4 High-Tech Gründerfonds Management DE 12

5 Novo GB 10

6 Atlas Venture GB 9

6 Life Sciences Partners DE 9

8 TVM Capital DE 8

8 SEED Capital Denmark DK 8

8 Auriga Partners FR 8

8 MVM Life Science Partners GB 8

21

SE

CT

ION

FOU

R T

HE

FINA

NC

ING

CY

CLE

OF H

EA

LTH

CA

RE

TE

CH

NO

LOG

Y C

OM

PAN

IES

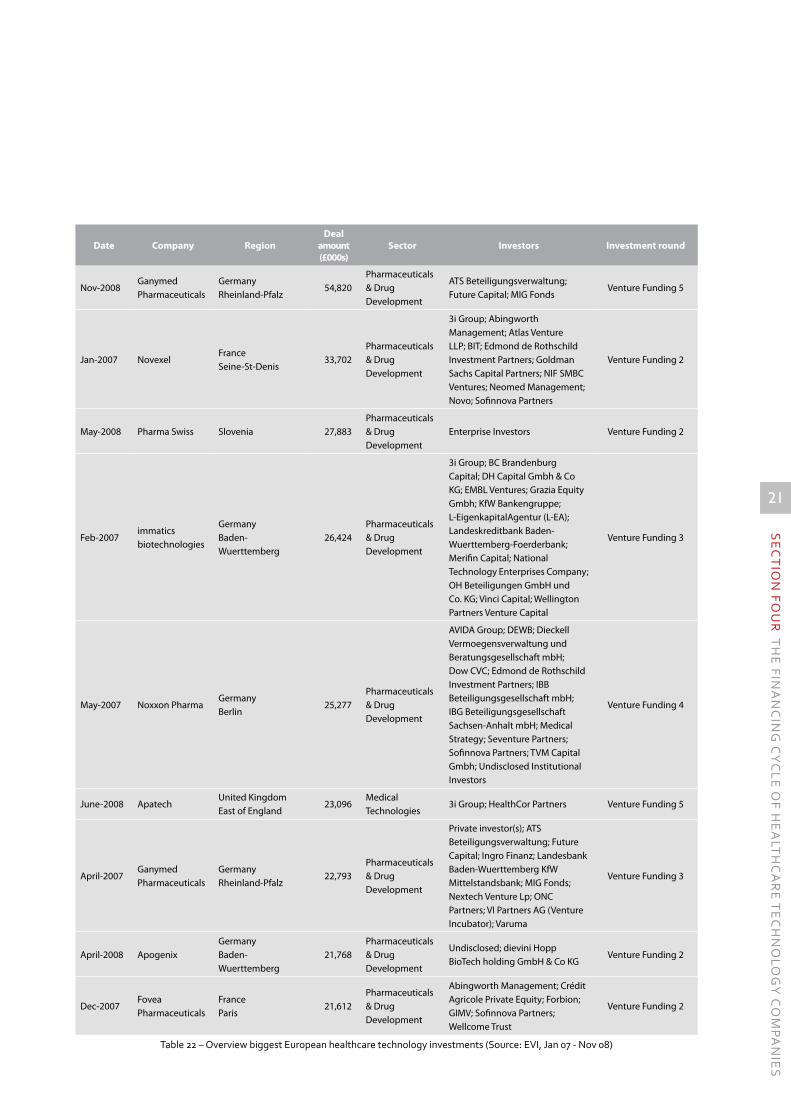

Table 22 – Overview biggest European healthcare technology investments (Source: EVI, Jan 07 - Nov 08)

Date Company RegionDeal

amount (£000s)

Sector Investors Investment round

Nov-2008Ganymed Pharmaceuticals

Germany Rheinland-Pfalz

54,820Pharmaceuticals & Drug Development

ATS Beteiligungsverwaltung; Future Capital; MIG Fonds

Venture Funding 5

Jan-2007 NovexelFrance Seine-St-Denis

33,702Pharmaceuticals & Drug Development

3i Group; Abingworth Management; Atlas Venture LLP; BIT; Edmond de Rothschild Investment Partners; Goldman Sachs Capital Partners; NIF SMBC Ventures; Neomed Management; Novo; Sofinnova Partners

Venture Funding 2

May-2008 Pharma Swiss Slovenia 27,883Pharmaceuticals & Drug Development

Enterprise Investors Venture Funding 2

Feb-2007immatics biotechnologies

Germany Baden-Wuerttemberg

26,424Pharmaceuticals & Drug Development

3i Group; BC Brandenburg Capital; DH Capital Gmbh & Co KG; EMBL Ventures; Grazia Equity Gmbh; KfW Bankengruppe; L-EigenkapitalAgentur (L-EA); Landeskreditbank Baden-Wuerttemberg-Foerderbank; Merifin Capital; National Technology Enterprises Company; OH Beteiligungen GmbH und Co. KG; Vinci Capital; Wellington Partners Venture Capital

Venture Funding 3

May-2007 Noxxon PharmaGermany Berlin

25,277Pharmaceuticals & Drug Development

AVIDA Group; DEWB; Dieckell Vermoegensverwaltung und Beratungsgesellschaft mbH; Dow CVC; Edmond de Rothschild Investment Partners; IBB Beteiligungsgesellschaft mbH; IBG Beteiligungsgesellschaft Sachsen-Anhalt mbH; Medical Strategy; Seventure Partners; Sofinnova Partners; TVM Capital Gmbh; Undisclosed Institutional Investors

Venture Funding 4

June-2008 ApatechUnited Kingdom East of England

23,096Medical Technologies

3i Group; HealthCor Partners Venture Funding 5

April-2007Ganymed Pharmaceuticals

Germany Rheinland-Pfalz

22,793Pharmaceuticals & Drug Development

Private investor(s); ATS Beteiligungsverwaltung; Future Capital; Ingro Finanz; Landesbank Baden-Wuerttemberg KfW Mittelstandsbank; MIG Fonds; Nextech Venture Lp; ONC Partners; VI Partners AG (Venture Incubator); Varuma

Venture Funding 3

April-2008 ApogenixGermany Baden-Wuerttemberg

21,768Pharmaceuticals & Drug Development

Undisclosed; dievini Hopp BioTech holding GmbH & Co KG

Venture Funding 2

Dec-2007Fovea Pharmaceuticals

France Paris

21,612Pharmaceuticals & Drug Development

Abingworth Management; Crédit Agricole Private Equity; Forbion; GIMV; Sofinnova Partners; Wellcome Trust

Venture Funding 2

22

The Healthcare Technology Venture Market

SE

CT

ION

FOU

R T

HE

FINA

NC

ING

CY

CLE

OF H

EA

LTH

CA

RE

TE

CH

NO

LOG

Y C

OM

PAN

IES

4.7.3. Top deals in the UKThe UK has not seen as many big investments as some other European countries over the past two years. The majority of big investments went into German companies (ten), followed by French companies (eight). Swiss companies received the same number of investments as UK companies (six).

Within the UK, five of the six biggest deals were closed by companies in the South East and one in the East of England.

During the same period, there were three investments into drug development companies based in Yorkshire & Humber (Table 24).

4.7.2. Top deals in EuropeThe league table of the biggest deals (over £20m), as shown in Table 22, in the European healthcare sector is dominated, as expected, by companies active in the pharmaceuticals and drug development area. The largest investments were closed by the German-based Ganymed Pharmaceuticals, with a £54.8m investment in November 2007 and a £22.8m investment in April 2007. It is also noted that these syndicated later-stage deals involve several investors, with some of them joining as new investors while others participated in earlier financing rounds.

Only one investment went into a medical technologies company which, incidentally, is also the only UK later-stage investment in the league table. Germany, however, had five investments in total (as mentioned before, two belonging to Ganymed) and two from France and one from Slovenia. Out of the 45 biggest investments in Europe, only six investments were made into UK-based companies.

Table 23 – Overview biggest UK venture capital investments (Source: EVI, Jan 07 - Nov 08)

Table 24 – Overview of the biggest investments in Yorkshire & Humber (Source: EVI, Jan 07 - Nov 08)

Rank Date Company RegionDeal

Amount (£000s)

Sector Investors Investment round

9 June-2008 ApatechUnited Kingdom

East of England23,096 Medical Technologies 3i Group; HealthCor Partners Venture Funding 5

14 Oct-2007Oxford Immunotec

United Kingdom

South East19,478 Medical Technologies

Clarus Ventures; DFJ Esprit; Wellington Partners Venture Capital

Venture Funding 3

15 Mar-2008Vantia Therapeutics

United Kingdom

South East19,000

Pharmaceuticals & Drug Development

MVM; Novo; SV Life Sciences Venture Funding 1

19 Mar-2008 PanGeneticsUnited Kingdom

East of England17,618

Pharmaceuticals & Drug Development

ABN AMRO Capital; Biogen Idec New Ventures; Credit Agricole Indosuez Private Equity; Edmond de Rothschild Investment Partners; Fortis Private Equity NV (Fagus NV); Index Ventures

Venture Funding 3

24 Oct-2007 SyntaxinUnited Kingdom South East

16,000Pharmaceuticals & Drug Development

Abingworth Management; Johnson & Johnson Development Corporation; Life Sciences Partners; Quest for Growth; SR One

Venture Funding 2

45 Jan-2008Circassia Holdings

United Kingdom South East

11,000Pharmaceuticals & Drug Development

Goldman Sachs Capital Partners; Imperial Innovations; Invesco Perpetual; Lansdowne Capital

Venture Funding 2

Rank Date Company Region Deal Amount (£000s)

53 Nov-2007 Neoss Yorkshire & Humber 10,000

88 Dec-2007 Photopharmica Holdings Yorkshire & Humber 6,000

157 Jan-2008 Tissue Regenix Yorkshire & Humber 3,000

23

Similar to measuring early-stage investment activity, the attractiveness of a region for later-stage investments is analysed by comparing the investment activity across different regions. But unlike early-stage investments, later-stage venture capital organisations invest internationally. International comparisons can be made by scaling the investment activity by, for example, ‘per capita’ or ‘all companies’. This, however, has some methodological disadvantages due to the different sizes and industrial structure of the European countries. Another way is ti compare one region to another. One advantage of this is that the comparison happens within the same industry. To avoid a bias, Yorkshire & Humber was compared to other regions in the two main European economies Germany and France. In Germany the ‘states’ and in France the ‘regions’ have a similar structure and function as the UK ‘regions’.

The table shows that Yorkshire & Humber is well placed and directly follows the major and most well-known European biotech regions in the UK and Germany, and on the same level as Paris and the populous German state of Nord-Rhine Westphalia which contains cities like Cologne, Düsseldorf, Essen, and Dortmund.

5.1. The investment landscape in Yorkshire & Humber

The following section considers the venture capital industry in Yorkshire & Humber. In recent years, an interesting blend of university spin-outs and start-up companies were financed by a variety of regional, national and international investors.

This analysis is based on data released into the public domain mainly through the companies or investors themselves. The report provides a comprehensive picture of the region’s investment landscape by presenting the financing cycle of local companies as well as regional investors and their investment history.

5.1.1. The origin of companies in the regionAs previously noted, universities play an important role in creating promising technology-based companies. University spin-out companies provide excellent investment opportunities for regional, national and international investors. A basic factor for the creation and quality of university spin-out companies is the extent and quality of the underlying research embedded in the university’s

SE

CT

ION

FIVE

TH

E A

TT

RA

CT

IVE

NE

SS

OF Y

OR

KS

HIR

E &

HU

MB

ER

Table 25 – Overview of the number of deals in different European regions (Source: EVI, Jan 07 - Nov 08)

researchers and students and their means to study and undertake research. Therefore it is important to look into the innovative capacity and the technology transfer activities of the universities in the region.

5. The attractiveness of Yorkshire & Humber

Rank Location Deals Investments

1United Kingdom South East

41 138,418

2United Kingdom Scotland

33 22,037

3United Kingdom London

32 35,985

4Germany Bavaria

30 80,649

5United Kingdom East of England

26 89,712

6United Kingdom North West

22 25,305

7Germany Baden-Wuerttemberg

16 95,506

8United Kingdom Yorkshire & Humber

15 22,570

8Germany North Rhine-Westphalia

15 13,061

8France Paris

15 87,028

11United Kingdom Wales

10 6,926

11United Kingdom East Midlands

10 4,940

11Germany Thueringen

10 6,028

14United Kingdom West Midlands

9 2,620

14United Kingdom South West

9 17,420

24

The Healthcare Technology Venture Market

2006, Fusion IP entered a partnership with a £10m side fund from Nikko Principal Investments Ltd that is “exclusively available to invest in our existing and future portfolio companies.” 23

IP Group Plc• core business is the commercialisation of intellectual property originating from research intensive institutions. The company was founded in 2001 and also provides management of venture funds focusing on early-stage technology companies and the in-licensing of drug related intellectual property from research intensive institutions.

All the three major universities in the region have entered agreements with partners to commercialise their intellectual property. These partners can supply experts to provide advice and also have the capital to back these companies.

The University of York and the University of Leeds have entered into an agreement with IP Group Plc, while the University of Sheffield cooperates with Fusion IP:

a) University of York

The agreement between the IP Group Plc with the University of York started in 2003 with the Centre for Novel Agricultural Products. In March 2006 the agreement was extended to cover the entire university.

In the field of healthcare technologies, IP Group and the University of York have spun-out Bioniqs Ltd which has developed unique expertise in ionic liquids that can facilitate and improve bio-chemical and bio-catalytic processes that are difficult to undertake using conventional technologies.

SE

CT

ION

FIVE

TH

E A

TT

RA

CT

IVE

NE

SS

OF Y

OR

KS

HIR

E &

HU

MB

ER