Embed Size (px)

Citation preview

THE GST AND REAL PROPERTY TRANSACTIONS

TABLE OF CONTENTS

Page

I. INTRODUCTION 1

II. PURCHASE AND SALE OF REAL PROPERTY 1

A. DEFINITIONS 21. Builder 22. Real Property 33. Residential Complex 34. Multiple Unit Residential Complex 45. Sale 46. Supply 47. Substantial Renovation 48. Commercial Activity 5

B. RESIDENTIAL REAL PROPERTY 51. Sales of Used Residential Complexes 5

(a) General Rule - Exempt 5(b) Certificates under Section 194 6

2. Sales of New "Residential Complexes" 6(a) General Rule - Taxable 6(b) GST Rebates on New Homes 7

3. Condominium Fees and Co-operative Housing Fees 9

C. COMMERCIAL REAL PROPERTY 91. General Rule - Taxable 92. Subsection 221(2)

- No Obligation to Collect GST 9(a) Purchaser/Registrant to Self-Assess 9(b) Sale 11(c) Time of Registration for the Purchaser 11(d) No "Due Diligence" Defence 12

3. Failure to Collect the GST 14

D. OTHER DISPOSITIONS 151. Placing Farm Property in JointTenancy 152. Special Situations Involving Farm Land 17

(a) Sale by Individual to Related Individual 17(b) Change of Use of Farm Land

- Commercial to Personal 17(c) Sale by Corporation to Shareholder 17

3. Mixed Sales 184. Sales of Personal Use Properties 195. Adventure or Concern in the Nature of Trade 196. Residential Trailer Parks 20

III. LEASES OF REAL PROPERTY 20

A. RESIDENTIAL LEASES 20

Page

B. COMMERCIAL LEASES 21. 1. General Rules 21

(a) Basic Rent 21(b) Additional Rent 21(c) Percentage Rent 22

2. Tenant Inducements 22(a) Rent-Free Periods 23(b) Cash Payments 23(c) Improvements to Leased Premises 23

3. Farm Leases 24

. IV. SPECIAL SITUATIONS 24

A. CHANGE IN USE 24

B. SELF-SUPPLY RULES 25

C. CONSTRUCTION CONTRACTS 271. Deposits 272. Holdbacks 27

D. COMMISSIONS, LEGAL FEES AND OTHER DISBURSEMENTS 27

E. FORECLOSURES AND JUDICIAL SALES 28

F. MORTGAGES AND SECURITY INTERESTS 28

G. CEASING TO BE A REGISTRANT 28

V. CASE STUDY 29

VI. CONCLUSION 32

Schedule A - Certificate under Section 194 33

Schedule B - Form GST 190E, "New Housing - Application for Rebate of Goodsand Services Tax" 34

Schedule C - Form GST 60, "Goods and Services Tax Return for Acquisition ofReal Property" 36

Schedule D - Certificate of Purchaser Under Subsection 221(2) 37

)

I.

THE GST AND REAL PROPERTY TRANSACTIONS

INTRODUCTION

Since the Goods and Services Tax (the "GST") came into effect on January 1, 1991, there

have been numerous amendments to the Excise Tax Act (Canada)(the "Act"). The purpose of

this paper is to update practitioners on changes to the GST legislation relating to real property.

Conceptually, the GST is rather simple. For the most part, the tax is levied at the rate of 7%

on the consideration paid or payable for goods and services. The GST becomes more difficult

when dealing with real property because there are numerous exceptions to this general rule.

This factor, together with the amendments made to the Act in S.C. 1993, c .. 27 (formerly Bill

C-1l2), have served to make the legislation all the more complex as it relates to real property.

n. PURCHASE AND SALE OF REAL PROPERTY

..Unless specifically exempted, the GST will be levied on all sales of real property. Where real

property is concerned, the important exemptions deal with residential real property, personal

use land owned by individuals or trusts, and certain dispositions of farm land to related

individuals. However, even when the GST is required to be charged, it does not necessarily

follow that the vendor will have an obligation to collect GST on closing. Thus, when dealing

with purchases and sales of real property, two important questions arise:

1. Firstly, is the sale subject GST?

2. Secondly, if it is, does the vendor have an obligation to collect GST on closing?

To arrive at the answers to these questions, it is necessary to have an understanding of a few

basic defInitions.

-2-

A. DEFINITIONS

1. Builder

A "builder"l is defmed with reference to a "residential complex" or an addition to "multiple

unit residential complex" and means a person who:

1. Has an interest in real property on which the complex is situated, and carries on the

construction of a complex, an addition to the complex or a substantial renovation in

respect of the complex;

2. Acquires an interest in the complex when it is under construction or the subject of a

substantial renovation;

3. Makes a supply of a mobile home or floating home before it has been used or occupied

by any individual as a place of residence;

4. Ac,quires an interest in a complex:

(a) In the case of a condominium complex or residential condominium unit, at a

time when the complex is not registered as a condominium; or

(b) In any other case, before it has been occupied by an individual as a place of

residence or lodging;

for the primary purpose of selling the complex or an interest therein, or leasing it to

persons (other than individuals) who will not be using it in the course of a business or

an adventure or concern in the nature of trade.

Excluded from the defmition of "builder" is a person who carries out construction or a

substantial renovation for his or her own personal use. The concept of a '.'builder" is one who

engages in the construction or substantial renovation as a business or "commercial activity" .

A person may also be deemed to be a builder where that person converts non-residential real

property to a residential complex but does not engage in any construction or substantial

1. Excise Tax Act (Canada) (the"Act"). ss. 123(1). definition of "builder". (Unless otherwise noted. all references to

statutory provisions shall be references to the Act.)

- 3 -

) renovation of the property. It should be noted, however, that a person will only be deemed to

be a builder, in the case of an individual, where the individual does so in the course of a

commercial activity.

2. Real Property

"Real property" includes:

1. Immovable property and every lease thereof (in the Province of Quebec); and

2. All lands and every estate or interest in real property, whether legal or equitable (in all

other places in Canada).

For the purposes of the GST, the concept of real property goes further and also includes a

mobile home, a floating home and any leasehold or proprietary interest therein.2

3. Residential Complex

A residential complex includes a detached and semi-detached house, row house units, an

apartment, a residential condominium unit, a mobile home and a floating home. As well, it

includes a summer cottage, a vacation home, a student residence, and a residence for elderly

and infmn persons. 3

Where owner-occupied homes. are concerned, the deftnition "residential complex" requires that

the home be used "primarily" as a place of residence of the individual, an individual related to

the individual, or former spouse of the individual. For these purposes, the concept of

"primarily" is normally interpreted by Revenue Canada to mean more than 50%. Even if you

have an area in your home that qualiftes as an "office", provided that this area does not

comprise more than 50% of the home, the home will still qualify as a "residential complex".

A residential complex will not include a hotel, motel, inn, boarding house, lodging house or

similar premises where "all or substantially all" of the residential units are leased or expected

2.

3.58. 123(1), definition of "real property".

5s. 123(1), defInition of "residential unit" and "residential complex".

-4-

to be leased for periods of less than 60 days. The phrase "all or substantially all" is interpreted

by Revenue Canada to mean 90% or more.4

4. Multiple Unit Residential Complex

A "multiple unit residential complex"5 is a residential complex containing more than one

residential unit. It does not include a condominium complex.

s. Sale

A "sale" includes any transfer of ownership of the property and a transfer of the possession of

the property under an agreement to transfer ownership of the property.6

6. Supply

A "supply" means the provision of property or a service in any manner, including sale,

transfer, barter, exchange, licence, rental, lease, gift or disposition.7 Given that this defInition

appears to make a distinction between "sale" and "gift", it would appear that the defInition of

"sale" does not include a "gift".

7. Substantial Renovation

A "substantial renovation"8 has relevance in terms of a residential complex. It means the

renovation or alteration of a building to such an extent that all or substantially all of the

building that existed immediately before the renovation or alteration (other than the

foundation, external walls, the interior supporting walls, floors, roof and staircases) has been

removed or replaced and after the renovation or alteration the building is or forms part of a

residential complex.

4.

5.6.

7.

8.

For a contrary view from the courts, see Wood v. M.N.R. 87 D.T.e. 312 (T.e.e.), where the court held the term

"all or substantially all" does not lend itself to a simple mathematical formula and that the Minister of National

Revenue might be hardpressed to dispute a claim where the percentage was 89%,85%,80% or lower.

Ss. 123(1), defInition of "multiple unit residential complex".

Ss. 123(1), defInition of "sale".

Ss. 123(1), definition of "supply". The description of a "supply" is subject to Sections 133 and 134.

Ss. 123(1), definition of "substantial renovation".

-5-

8. Commercial Activity

The tenn "commercial activity"9 has been amended by the introduction of a new profit test for

partnerships. Other than that, the revised wording of the definition results in a condensation

and clarification of the previous definition. A commercial activity of a person means:

1. A business carried on by the person other than:

(a) a business carried on by an individual or partnership, all of the members of

which are individuals, without a reasonable expectation of profit; or

(b) A business to the extent it involves the making of exempt supplies by the

person;

2. An adventure or concern of the person in the nature of trade other than:

(a) an adventure or concern engaged in by an individual or a partnership, all of the

members of which are individuals, without a reasonable expectation of profit; or

(b) an adventure or concern in the nature of trade to the extent it involves the

making of exempt supplies by the person; and

3. The making of a supply (other than an exempt supply) by a person of real property of

the person, including anything done by the person in the course of or in connection

with the making of the supply.

B. RESIDENTIAL REAL PROPERTY

1. Sales of Used Residential Complexes

(a) General Rule - Exempt

The sale of a used "residential complex" will generally be exempt from GST due to the fact

that it constitutes an exempt supply. 10 Because an exempt supply is not a commercial activity,

no GST need be levied.

9.

10.Ss. 123(1), definition of "commercial activity".

Ss. 123(1), definition of "exempt supply"; also see Schedule V, Pan I as it relates to real property.

-6-

Generally, a residential complex will be considered "used" if from the time it was substantially

completed it has either:

1. been sold (and no input tax credit has been claimed by the purchaser); or

2. has been occupied as a place of residence.

It is this exemption that allows the sale of "used homes" (which most lawyers are familiar

with) to take place without GST consequences;

(b) Certificates under Section 194

When purchasing a residential complex, the purchaser should obtain a written certificate from

the vendor stating that the property purchased qualifies as an exempt supply described in any

of Sections 2-5.3, 8 and 9 of Part I of Schedule V. If this is done and it later turns out that the

sale of the real property was taxable rather than exempt, then the vendor will be responsible

for the payment of GST rather than the purchaser (except in circumstances where the purchaser

knew or ought to have known that the supply was not exempt).l1 The use of the certificates in

residential real property transactions is quite common. An example of such a certificate is

found at Schedule "A" to this paper.

2. Sales of New "Residential Complexes"

(a) General Rule - Taxable

When a new residential complex is constructed by a builder, its sale will be subject to GST.

An exception to this is where a builder has constructed a residential complex for rental or uses

it for his own residence, and has claimed input tax credits during the course of construction.

In these circumstances the "self-supply" rules in s. 191 would require the builder to remit GST

directly to the Federal Government based on the fair market value of the complex. Because

the property would not be used in a commercial activity once construction has been completed,

no input tax credit could be claimed. Thereafter, when the builder goes to sell the complex,

no GST would have to be charged because the GST has been paid by the builder.

11. s. 194.

) (b) GST Rebates on New Homes

-7-

In order to off-set the impact of the GST on the price of new or substantially renovated single

family housing, the Act provides for a rebate. The rebate applies to detached homes, semi

detached homes, row houses, residential condominium units, mobile homes, floating homes

and duplexes (hereinafter collectively referred to as a "complex"). In order to be eligible for

the rebate, the following conditions must be satisfied: 12

1. A builder must sell the complex to an individual;

2. The individual must acquire the complex as a primary place of residence for that

individual or a relation of that individual;

3. The total consideration for the complex must be less than $450,000;13

4. The GST must be paid before the rebate will be given;

5. Ownership of the complex must be transferred to the individual after construction or a

substantial renovation is substantially completed; .

6. The complex must-not previously have been occupied by anyone as a place of residence

or lodging, except in the case of a residential condominium unit where it may be

occupied by an individual (or a relation of that individual) who was a purchaser under

an agreement of purchase and sale; and

7. The first occupant following substantial completion must be the individual or a relation

of that individual.

Nonnally, the GST would have to be paid in full before an application could be made for the

rebate. However, it is possible for purchasers of new homes to assign their GST rebate to the

builder and thereby reduce their up-front financing. 14 The fonn required to make the

12.

13.

14.

Ss.254(2)..Given s. 138, where particular property or services are supplied along with and incidental to the provision of the

residential complex, the cost of those incidental goods or services (which could include things such as built-in

appliances) will be considered as pan of the total consideration for the residential complex.

5s.254(4).

-8-

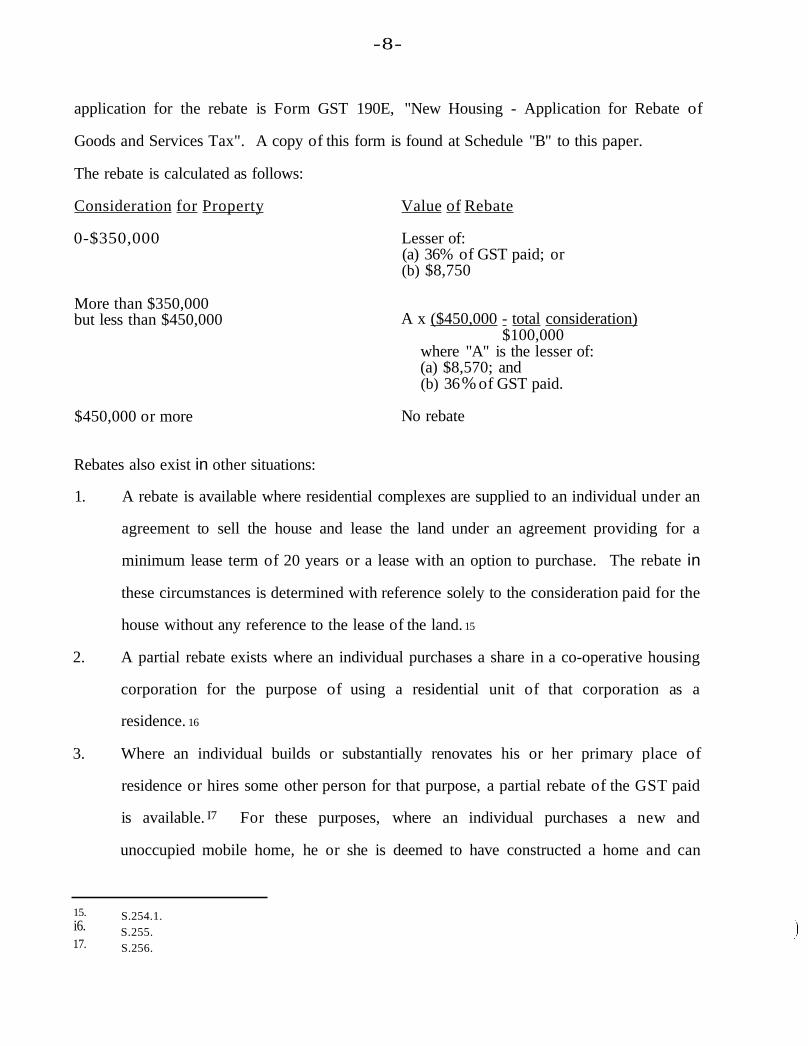

application for the rebate is Form GST 190E, "New Housing - Application for Rebate of

Goods and Services Tax". A copy of this form is found at Schedule "B" to this paper.

The rebate is calculated as follows:

Consideration for Property

0-$350,000

More than $350,000but less than $450,000

$450,000 or more

Rebates also exist in other situations:

Value of Rebate

Lesser of:(a) 36% of GST paid; or(b) $8,750

A x ($450,000 - total consideration)$100,000

where "A" is the lesser of:(a) $8,570; and(b) 36% of GST paid.

No rebate

1. A rebate is available where residential complexes are supplied to an individual under an

agreement to sell the house and lease the land under an agreement providing for a

minimum lease term of 20 years or a lease with an option to purchase. The rebate in

these circumstances is determined with reference solely to the consideration paid for the

house without any reference to the lease of the land. 15

2. A partial rebate exists where an individual purchases a share in a co-operative housing

corporation for the purpose of using a residential unit of that corporation as a

residence. 16

3. Where an individual builds or substantially renovates his or her primary place of

residence or hires some other person for that purpose, a partial rebate of the GST paid

is available. I7 For these purposes, where an individual purchases a new and

unoccupied mobile home, he or she is deemed to have constructed a home and can

15.. i6.

17.

S.254.1.S.255.S.256.

)

-9-

claim the new housing rebate for owner-built homes (this would only be done where

the individual had not submitted a rebate application under s.254 or s.254.1.).18

4. Finally, where a person acquires land and pays GST in connection with that purchase, a

partial rebate of the GST paid is available where that person leases the land under

certain exempt conditions due to the fact that the Lessee is acquiring the land for the

purpose of making supplies of residential rental accommodation. 19

3. Condominium Fees and Co-operative Housing Fees

Fees paid to a condominium corporation by the owner or tenant of a condominium are exempt

from the GST provided that the fees relate to use and occupancy of the unit.20 A parallel

exemption exists for charges levied by a co-operative housing corporation in respect of

occupancy of residential units managed or owned by the corporation.21

C. COMMERCIAL REAL PROPERTY

1. General Rule - Taxable

Real property that is used in a "commercial activity" is subject to GST when sold. The

principal question that lawyers must deal with in connection with sales of commercial real

property is whether or not the vendor is under an obligation to collect the GST from the

purchaser.

2. Subsection 221(2) - No Obligation to Collect GST

(a) Purchaser/Registrant to Self-Assess

Normally, the person making a taxable supply of goods or services is under an obligation, as

an agent of Her Majesty in Right of Canada, to collect the GST.22 The supplier is deemed to

18.19.20.21.

22.

S5. 256(2.1).

S.256.1Schedule V. Part I. Para. 13..

Schedule V. Part I. Para. 13.1.

S5. 221(1).

- 10-

hold the GST so collected in trust until remitted or withdrawn in accordance with the terms of

the Act.2~

An exception to this general rule exists in certain circumstances when there is a sale of

commercial real property. These exceptions are set out in subsection 221(2) which reads as

follows:

221(2) A supplier (other than a prescribed supplier) who makes a taxablesupply of real property by way of sale is not required to collecttax under Division II payable by the recipient in respect of thesupply where

(a) the supplier is a non-resident person or is a resident ofCanada by reason only of subsection 132(2);

(b) the recipient is registered under Subdivision d and thesupply is not a supply of a residential complex made to anindividual; or

(c) the recipient is a prescribed recipient.

Essentially, subsection 221(2) provides that a vendor of commercial real property need not

collect GST in circumstances where:

1. the vendor is a non-resident;

2. there is a sale of commercial real property to a person who is registered fo~ the GST;

3. there is a sale of residential property to a person who is registered for the GST, other

than an individual; or

4. there is a sale to a prescribed recipient. (At the present time, there are no "prescribed

recipients" for the purposes of subsection 221(2).)

With the vendor not being required to collect GST, the purchaser is required to self-assess the

GST and is liable to account for such GST liability directly to the federal government.

However, if the real property is used in commercial activities, the purchaser can claim an off

setting input tax credit. The result is that the GST does not affect the purchase price of

23. Ss.222.)

- 11 -

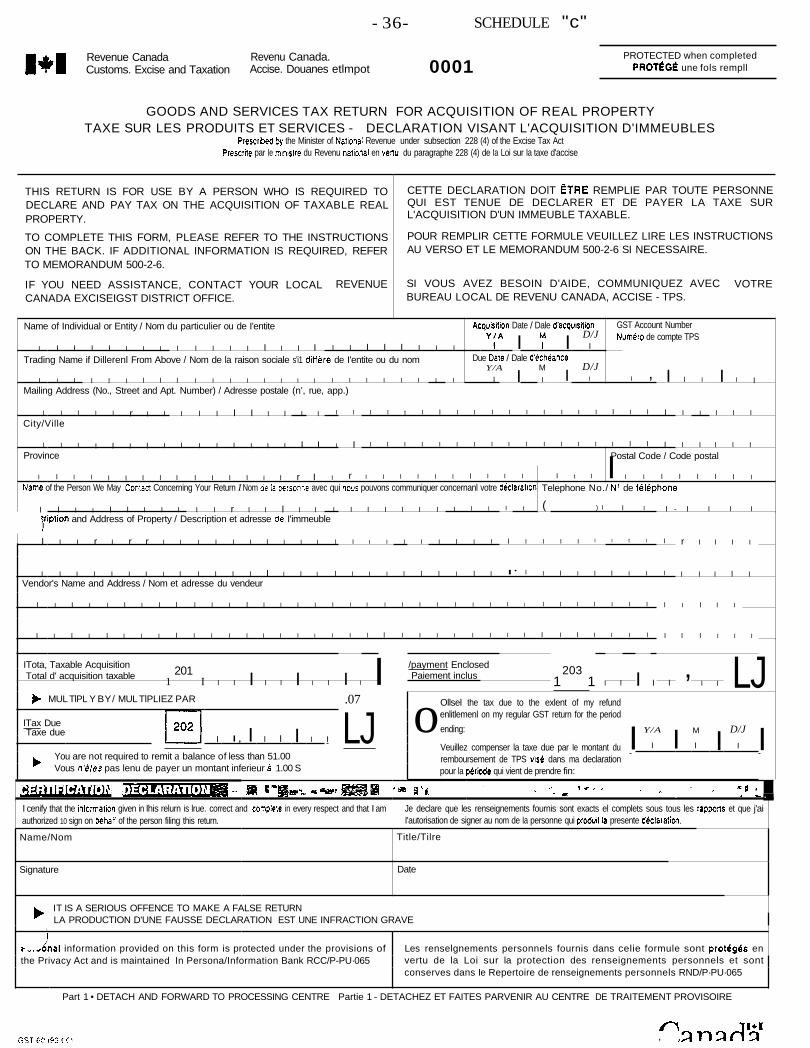

) commercial real property.24 The Purchaser should ftle Form GST 60, "Goods and Services

Tax Return for Acquisition of Real Property". A copy of this is found at Schedule "e".

(b) Sale

Subsection 221(2) only applies in circumstances of a "sale". Questions have been raised

whether or not capital leases or long-term leases with options to buy at the end of the lease

period for nominal consideration constitute "sales" for GST purposes.25 If so, any

arrangements like these involving real property could result in the GST being payable at the

time of transfer of possession under the agreement,26 Furthermore, the lessee/purchaser, if a

registrant, could make use of subsection 221(2) in these circumstances by self-assessing on the

GST exigible on all payments under the agreement, and off-set the GST by claiming input tax

credits.

(c) Time of Registration for the Purchaser

One of the things that is not clear is the point in time at which the purchaser of real property

must be registered in order for this provision to be effective. Should the purchaser be

registered at the time the GST is payable (which occurs on the earlier of the transfer of

ownership or possession of the real property27), or must the purchaser be registered at the time

of the supply (ie. when the agreement is entered into)? Revenue Canada appears to have taken

the position that the purchaser need only be registered at the time the GST is actually payable.

Thus, even if at the time that the agreement is entered into, the purchaser is not registered for

the GST, provided that the purchaser is registered at such time as possession or ownership is

transferred to the purchaser, both parties should be able to take advantage of subsection

221(2).

24.25.

26.27.

Ss. 228(4) and (6).Glenn Ernst "GST and Real Property Transactions" in Advanced GST: An Update - The New Rules ~

Commercial Transactions (Canadian Bar Association, 1993),5.Ss. 168(5).Ss. 168(5).

- 12-

Notwithstanding Revenue Canada's interpretation, the strict wording in subsection 221(2)

refers to a:

"taxable sUlmly of real property by way of sale... ftol":

(b) "the recipient ...registered under Subdivision d... "

(Emphasis added.)

The wording in subsection 221(2) focuses on registration at the time of the taxable supply.

Section 133 states that where an agreement is entered into to provide a property or service, the

entering into of the agreement is deemed to be a supply. When dealing with real property

transactions, normally a written agreement is entered into before the passing of ownership or

possession. Thus, the "supply" takes place at the time the agreement is entered into. Where

an agreement is entered into at a time when the purchaser is not registered for the GST,

technically it would appear that the requirements of subsection 221(2) are not met

notwithstanding that the purchaser becomes registered for the GST before the earlier of

possession or ownership of the real property being transferred to the purchaser.

It should be noted that even if subsection 221(2) did not apply, so long as the purchaser

became registered for the GST in the reporting period in which the GST in respect of the

acquisition of the real property becomes payable or is paid, the purchaser would still be

entitled to an input tax credit. Subsection 169(1), which sets out the general rule in connection

with input tax credits, provides that an input tax credit may be claimed in connection with a

property or service supplied to a person in connection with a commercial activity where that

person becomes a registrant during a reporting period.

(d) No "Due Diligence" Defence

There is no "due diligence defence" that the vendor can rely on should it turn out that the

purchaser of the real property is not a registrant for GST purposes. Revenue Canada has

suggested that the vendor obtain a certificate or an affidavit from the purchaser confirming that

)

- 13 -

the purchaser is registered or is a prescribed purchaser.28 Notwithstanding any such certificate

or affidavit, however, should it turn out that the purchaser does not meet the requirements of

Subsection 221(2), the vendor will be liable to collect and remit GST exigible on the

transaction.29 In order to protect a vendor in these circumstances, consideration should be

given to the following:

1. At the very least, a certificate should be obtained wherein the purchaser states its GST

registration number.

2. Revenue Canada could be contacted by the vendor or the solicitor for the vendor to

ensure the registration status of the purchaser. It would appear that officials of

Revenue Canada are permitted to provide personal information regarding registrants to

the extent that it may be reasonably regarded as necessary for the purposes of

determining any liability or obligation of any person under the Act, or as may

reasonably be regarded as necessary for the purpose of administration or enforcement

of the Act. 30

3. Finally, the vendor would be well advised to obtain an indemnity from the purchaser

with respect to the GST and any other amounts for which the vendor may become

liable (including penalties and interest) if the vendor does not collect the GST from the

purchaser on closing in reliance on the purchaser having met the requirements of

Subsection 221(2).

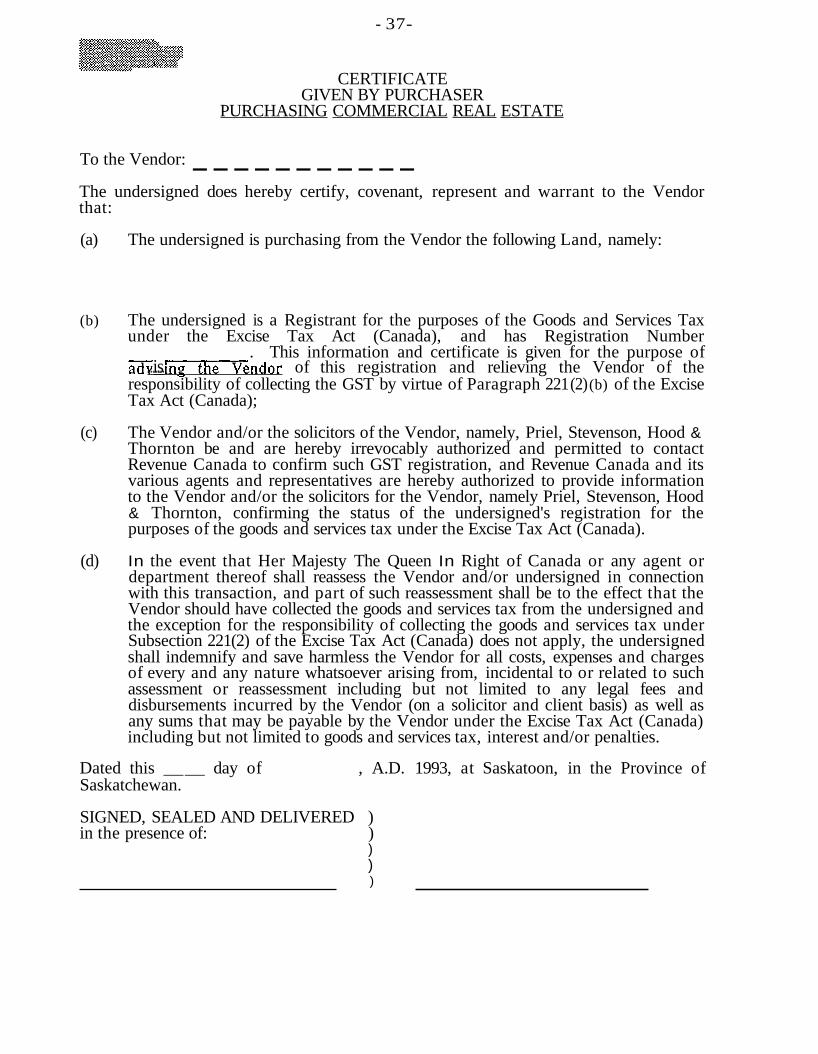

It is recommended that the vendor obtain from the purchaser, either in a certificate or in the

agreement of purchase and sale, the information, consents and indemnities noted above. A

sample certificate in this regard is attached as Schedule "D" to this paper.

28.

29.

30.

"Goods and Services Tax Round Table" in 1990 Conference Report (Canadian Tax Foundation, 1991: Toronto),

Question 13 at Page 27:10.

Ss.221(l}.

Ss.295(5}.

- 14-

3. Failure to Collect the GST

In some circumstances, the vendor may fail to collect the GST from a non-registrant purchaser

when selling commercial real property. This may happen in a situation where, for example,

an acreage property is being sold, and the acreage has been used partly as a residence, and

partly in a farming activity. Situations have occurred where the vendor has engaged a real

estate agent and the property has been sold under a "standard form" offer to purchase with no

thought given to the GST. The purchase and sale may end up closing without any GST being

paid. If Revenue Canada later reassesses, the vendor is going to have a problem if the

purchaser is unwilling to voluntarily pay the GST. In these circumstances, the vendor may be

forced to sue the purchaser under section 224. One of the pre-conditions to being able to sue

for the GST under section 224 is compliance with Subsection 223(1). This states as follows:

223(1) Where a registrant makes a taxable supply, the registrant shallindicate to the recipient, either in prescribed manner or in theinvoice or receipt issued to, or in an agreement in writing enteredinto 'with, the recipient in respect of the supply,

(a) The consideration paid or payable by the recipient for thesupply and the tax payable in respect of the supply in amanner which clearly indicates the amount of the tax; or.

(b) That the amount paid or payable by the recipient for thesupply includes the tax payable in respect of the supply.

It should be noted that Subsection 223(1) only applies to a registrant making a taxable supply.

Thus, if the vendor was someone other than a registrant, it would appear that nothing need be

placed in any sale agreement or invoice giving an itemization of the sale price and the GST.

In the case of 390781 Alberta Ltd. (operating under the name and style of 838 Developments)

v. Lori R. Mensaghi,31 a contractor built a house for the defendant. The contract was silent

on the GST. The contractor had to sue the purchaser for the net GST (after giving effect of

the New Housing GST Rebate). The court held that the contractor had not complied with

31. Alberta Provincial Court (Civil Division), June 11, 1992. C.C.H. Goods & Services Tax Reporter (1993: looseleaf),

Volume I, Paragraph 95-149.

- 15 -

) Subsection 223(1) because it failed to delineate in the documentation supplied to the purchaser

the amount of the GST.

With respect, this may be a rather technical conclusion. There is nothing in Subsection 223(1)

which appears to prevent an invoice for GST being given separate and apart from the contract.

It should be kept in mind that the vendor is merely suing to recover the GST as an agent on

behalf of Her Majesty in Right of Canada. The vendor, if a registrant, should be permitted to

provide an invoice to the purchaser for the GST, even if this is done after the agreement is

made.

The problem of failing to collect GST on the sale of commercial real property might be

considered in light of a situation where a vendor sells real property to the purchaser in

circumstances where both the vendor and purchaser believe it is exempt from GST. If the

vendor provides the purchaser with a certificate under Section 194 [discussed at II(B)(I)(b)

above], the vendor would be prohibited from suing the purchaser for the GST that arose from

the sale of the real property. Section 194 would be redundant if the purchaser could simply

raise Subsection 223(1) as a bar to the collection of GST where the purchase and sale

agreement is silent on the issue of GST. In order to give Section 194 meaning, the mere fact

that a contract is silent on GST and does not give an itemization between the sale price and

GST cannot, it is submitted, be enough to violate Subsection 223(1).

D. OTHER DISPOSITIONS

1. Placing Farm Property in Joint Tenancy

It is not uncommon for a farmer to place farm land in the names of both he/she and his/her

spouse as joint tenants. Frequently, this will be done in conjunction with estate planning for a

farm family. As most lawyers are aware, real property held in joint tenancy does not form

- 16-

part of a deceased's estate for probate purposes. As such, probate fees will not be levied on

this property. 32

Strictly speaking, the transfer of farm land from one spouse to both spouses in joint tenancy

should result in a taxable disposition of farm land that attracts the GST. Notwithstanding this,

however, Revenue Canada, Customs and Excise, has an administrative policy whereby the

transfer of an interest in farm property from an individual who operates a farm into joint

tenancy with one or more related persons will not have immediate GST consequences if all of

the following conditions are met:

1. The related person (the "non-farming joint tenant") is not involved in the farming

business independently on his or her own account or as a member of a partnership.

2. The non-farming joint tenant does not independently receive any proceeds from the

farming business which are treated as income on his or her own account.

3. The non-farming joint tenant is not currently registered for GST purposes or required

to register as a result of being involved in the farming business. (He/she may be

registered for reasons unrelated to the farming business.)

4. The consideration paid by 'the non-farming joint tenant for his or her joint tenancy

interest is nil or a nominal amount such as a dollar.

If these conditions are met, the non-farming joint tenant will not be required to pay GST on

the transfer of the farm property into joint tenancy, nor will the non-farming joint tenant be

required to register for the GST. It should be noted that this policy is applicable to farm land

used in the business of farming by the owner immediately prior to the transfer. It is not

applicable in cases where farm land is rented.

This administrative policy has the effect of simplifying the transfer of farm property into joint

tenancy. However, the policy is not supported by the wording of the Act. Furthermore, by

following the policy, certain problems could arise in the future. For example, if the initial

32. Queen's Bench Rule 701 and Form 104: also see The Oueen's Bench Fees Amendment Regulations. 1992 (No.3).

O.C. 995/92, dated October 29, 1992, Para. 5.1(3)(a).

)

- 17-

transferor (who is the registrant) should be the fIrst one to die, what are the GST consequences

to the surviving joint tenant? Will GST be payable at that point in time?

2. Special Situations Involving Farm Land

There are a number of situations involving farm land where what would otherwise be taxable

dispositions are specifIcally exempt from GST.

(a) Sale by Individual to Related Individual

Farm land may be sold by an individual to a relation33 or a former spouse without incurring

GSTwhere:

1. The farm land was used by the vendor in a commercial activity that is the business of

farming;

2. The farm land was not used immediately before the transfer by the individual in a

commercial activity other than the business of farming; and

3. The farm land is .acquired for personal use and enjoyment by the transferee or any

individual related to the transferee. 34

(b) Change of Use of Farm Land - Commercial to Personal

Where there is a change of use of farm land from commercial use to personal use,

notwithstanding that this would usually trigger a deemed taxable supply with a consequent

payment of GST,35 where farm land is involved, no GST will be payable.36

(c) Sale by Corporation to Shareholder

Finally, farm land may be sold on a tax-free basis by a corporation to a shareholder (or a

person related to the shareholder or former spouse of the shareholder) in circumstances where:

33.34.35.36.

S.126.

Schedule V, Part I, Para. 10.

Ss. 190(2) or 207(1).

Schedule V, Part I, Para. 11.

- 18-

1. Allor substantially all of the property of the corporation was used in the business of

farming immediately before the transfer;

2. The transferee is a shareholder of or related to the corporation; and

3. The transferee, and/or spouse or child of the transferee is actively engaged in the

business of fanning of the corporation; and

4. Immediately after the transfer, the fann land is used for the personal use and enjoyment

of the transferee or individual related thereto.

Parallel provisions exist in connection with partnerships and trusts. 37

3. Mixed Sales

Often times, a particular property has been used by a person for both commercial purposes and

exempt purposes. Examples include the following:

1. an apartment building, the main floor of which bas been leased out commercially (for

example, to a drug store/phannacy) with the rest of the building consisting of

residential leases; or

2. fann land, a portion of which consists of the residential homestead, and the balance of

which has been used in the commercial activity of farming.

When property such as this is sold, reference should be made to Subsection 136(2). Each of

the "exempt" and "commercial" portions are treated as separate properties. Only the portion

of the property used commercially will attract the GST. 38 A reasonable allocation will be

required to allocate the sale proceeds to the "exempt" as opposed to the "commercial" property

sold. It is important that the allocation that is chosen is used consistently for GST and income

tax purposes.

37.

38.Schedule V, Part I, Para. 12.

"Goods and Services Tax Round Table" in 1990 Conference Report, supra, Question 17, at Page 27:12. Also see

Michael Atlas, "GST and Residential Real Estate" in 1990 Conference Report, at 32:9.

)

- 19-

4. Sales of Personal Use Properties

As a general rule, any sale of personal-use real property made by an individual is exempt from

the GST. 39 This exemption also extends to trusts all of the beneficiaries (other than contingent

beneficiaries) of which are individuals, and all the contingent beneficiaries of which, if any,

are individuals or charities. For the purposes of this exemption, a reference to personal-use

real property is a reference to things such as country properties, vacation farms, hobby farms

and other non-business land.

5. Adventure or Concern in the Nature of Trade

A question frequently arises in connection with the disposition of real property as to. whether

the gain or loss resulting from the disposition is on account of income or capital. If the gain is

on account of capital, for income tax purposes only three-quarters of the gain must be included

in income. If the gain is an income gain (ie. business income), the entire gain must be

included in income. For income tax purposes, the word "business" is defmed in Subsection

248(1) of the Income Tax Act (Canada) to include an "adventure or concern in the nature of

trade" . This phrase has been the subject of a great deal of litigation. In connection with the

disposition of real estate, a gain on the disposition may be treated as business income even if

the vendor is not regularly in the business of trading real estate. A Court will consider such

factors as the length of time that the property is held, the intention of the vendor at the time

that the property is acquired (ie. was the real property purchased fu order to re-sell it at a

profit, or was it purchased to hold in order to earn rental income off it or use it in other

business operations of the vendor), the nature of the fmancing of such property, and whether

the disposition of the real estate is in any way related to any other business of the vendor.40

The issue as to whether or not the disposition of the real property is an "adventure or concern

in the nature of trade" has relevance for GST purposes. If the person disposing of the real

39.

40.Schedule V. Part I, Para. 9.

One of the leading cases in detennining whether a transaction is an "adventure or concern in the nature of trade"

is M.N.R. v. James A. Taylor, 56 D.T.C. 1125 (Exch. Ct.)

- 20-

property determines that the gain or loss on disposition will be a business gain or loss because

it is an "adventure or concern in the nature of trade", that person may wish to make an

election for GST purposes that the sale is taxable. The advantage of making such an election

for GST purposes41 will arise in a situation where the vendor had to pay GST when he or she

initially acquired the real property. Any unclaimed portion of GST actually paid by the

vendor on his/her original acquisition of the real property could be claimed on the disposition

of the real property.42

6. Residential Trailer Parks

A supply of land comprising of a residential trailer park is exempt from GST where the

transferor acquired the property in an exempt transaction, or was later required to pay GST to

the government in connection with the property without being able to claim any input tax

credits in circumstances where there was a conversion or change in use.43

ill. LEASES OF REAL PROPERTY

A. RESIDENTIAL LEASES

A lease of a residential complex (for example, a house) or a unit (for example, an apartment)

by an individual where it is occupied by that individual for a period of at least one month. is

exempt from GST.44 Furthermore, short term accommodation where the rental charge does

not exceed $20 for each day of occupancy is not subject to the GST.45 (Short term

accommodations which do not meet this criteria, such as hotels and motels, are taxable.) Most

apartment leases and house rentals are exempt from GST. (Residential landlords are not

41.

42.

43.

44.45.

Schedule V. Part I, Para. 9(b); also see Form GST 22: "Election to Treat the Tax Exempt Supply of Real Property

by Way of Sale by an Individual or Trust as a Taxable Supply".

If the owner is a non-registrant. s.257 permits the non-registrant to claim, at the time of sale. a rebate equaI to

the lesser of the total tax payable on the acquisition of the property and improvements made thereon, and the tax

on the consideration received for the sale. H the owner is a registrant, s.193 allows an input tax credit to be

claimed equal to lesser of the total tax payable on the acquisition of the property and improvements made thereon,

and that tax on the consideration received for he sale.

Schedule V. Part I, Para. 5.3.

Schedule V. Part I. Para. 6(a).

Schedule V. Part I, Para. 6(b).

- 21 -

') entitled to recover the GST paid on purchases, repairs, improvements or expenses as they

relate to residential complexes and residential units.46)

Other lease situations which are exempt for GST purposes include the following:

1. A lease of a parking space for a period of at least one month where a lease of space is

incidental to the lease of a residential premises in connection with a house, apartment, a

site in a residential trailer park, residential condominium unit, or floating home;47

. 2. A lease of land for a period of one month or longer to the owner or lessee of a mobile

home;48 and

3. The lease of a wharf or moorage facility to a person who is the owner, tenant or

occupant of a floating home.49

B. COMMERCIAL LEASES

1. General Rules

(a) Basic Rent

The supply of real property by way of a commercial lease is considered to be a taxable supply.

As such, the rents will be subject to the GST. For these purposes, the rent on which the GST

is calculated would include the "basic" rent which is paid by the tenant (for example, $8 per

ft2).

(b) Additional Rent

Tenants are often required to contribute, by way of additional rent, to the expenses incurred in

connection with the property such as property taxes, heating, ventilation and air conditioning

("HVAC"), utilities, janitorial services, snow removal and management. This "additional

46.

47.48.49.

Because these residential leases are exempt supplies under Schedule v, Part I, they do not meet the definition of

"commercial activity" in ss. 123(1). Therefore, no input tax credits may be claimed under s. 169.Schedule V, Part I, Para. 8.1.

Schedule V, Part I, Para. 7.

Schedule V, Part I, Para. 13.2.

- 22-

rent", provided that it is payable pursuant to the terms of a lease, would be viewed as

consideration under the lease and give rise to OST.

In some circumstances, particularly where the tenant is not engaged in a "commercial activity"

and therefore is not eligible for input tax credits on its rent (for example a doctor), the tenant

may wish to have the lease drawn in such a way that certain items would not be considered

"additional rent". For example, an amount charged by a municipal government for water is

normally considered to be an exempt supply and does not give rise to OST.50 If a tenant in

these circumstances can arrange to have the payment made directly to the municipality, rather

than to the landlord under the lease, then arguably the OST could be avoided on that

expenditure. A similar consideration would exist for a tenant's obligation to obtain insurance.

As insurance is a fmancial service and therefore an exempt supply,51 tenants will want to be

able to make their own arrangements for insurance and not share in the cost of the landlord's

policy.

(c) Percentage Rent

. Any amount paid as "percentage rent" (which is usually calculated with reference to the gross

revenues of the tenant from the leased premises) will also be subject to OST. In some

circumstances, "gross revenue" on which percentage rent is calculated is defmed in leases to

include such things as sales taxes paid by tenant's customers. Should that happen, effectively

you will have a situation where OST is paid on OST.

2. Tenant Inducements

It is not uncommon in a commercial lease to have tenant inducements. These can take many

forms including:

1. The reduction or elimination of rent;

2. Cash payments made by the landlord to the tenant; and

50.

51.Schedule V. Part VI. Paras. 22 and 23.

Schedule V. Part VIT.

)

- 23-

3. An allowance or reimbursement for costs incurred by the tenant with respect to the

leased premises.52

(a) Rent-Free Periods

It appears to be Revenue Canada's position that where the landlord provides a rent-free period

to the tenant and the landlord and tenant operate at arm's length, the rent-free period is treated

as a supply for nil consideration. Thus, there are no GST consequences.53

(b) Cash Payments

Where a cash inducement is paid by the landlord to the tenant, Revenue Canada appears to

regard the payment as resulting from a situation where the tenant has made a taxable supply of

a service to the landlord. That service is the agreement by the tenant to enter into a lease.

The tenant, if a registrant, is required to collect the GST. The landlord, if a registrant, is

subsequendy permitted to claim an input tax credit for any tax so paid or payable.

(e) Improvements to Leased Premises

Where the landlord makes the improvements directly to the leased premises and contracts out

the work, GST would be payable by the landlord on the contract price and an input tax credit

would be able to be claimed. If instead, the landlord makes a payment to the tenant intended

to reimburse or compensate the tenant for expenses that it incurred in carrying out

improvements, the landlord would be considered to have received a taxable supply in which

respect of which GST is payable. In drafting the lease agreement as it relates to a lease

inducement, where money is to be paid by the landlord to the tenant by way of reimbursement

for expenses incurred by the tenant, the wording should be clear as to whether the money paid

is inclusive of GST, or whether GST is to be paid in addition to the amount so stated as being

the lease inducement.

52.

53.

Tecbnicallnfonnation BulletinB-Q54 dated April IS. 1991, "Application of the Goods and Services Tax (GST) to

Lease Inducements".

The situation may be different where the landlord and tenant do not deal at ann's length. See s. ISS.

- 24-

3. Farm Leases

Where fann land is leased out on a cash basis, GST will have to be charged on the rent.

However, where there is a lease of fann land on a crop share basis, and the crop in question is

IIzero-rated II54 , no GST need be charged on the rent.55

IV. SPECIAL SITUATIONS

A. CHANGE IN USE

Real property may be acquired for one purpose (ie - commercial), and later be used for

another purpose (ie - residential). The Act provides that where there is a change in use of real

property from commercial to non-commercial use, there will be a Irecapture"56 of any input

tax credits previously claimed in proportion to the change in use and a resulting liability to the

federal government. Similarly, where the use of the real property changes from a non

commercial to a commercial use, a claim for input tax credits will be allowed to the extent of

the change in use {provided that GST was previously paid in connection with the property)57.

Conceptually, this· make sense in light of the fundamental policy regarding the GST as it

relates to real property. However, the rules contained in the Act to implement all of this are

quite complex.58

When a person initially acquires real property, their claim for an input tax credit is governed

by their IIintended II use for that property.59 Provided that the intended use for the real

property is exclusively in the course of commercial activities of the registrant, the entire

amount of the GST paid or payable in connection with the property may be claimed as an input

54.

55.

56.57.58.59.

Schedule VI, Part IV, Para. 2. Essentially these are grains or crops ordinarily used as or to produce food forhuman consumption or feed for farm livestock or poultry, when supplied in aquantity larger than ordinarily soldor offered for sale to consumers. It would not include any grains or seed mixtures that are packaged, prepared orsold for use as feed for wild birds or as pet food.Schedule VI, Part IV, Para. 9. Also see GST Memoranda: 300-34, "Agriculture and Fishing" (February 19,1992), Para. 28. 'Ss. 206(4) and (5).Ss. 206(2) and (3).

Generally speaking, the rules are found in s.206-211.Ss. 169(1).

J

- 25-

'I tax credit. While the original input tax credit claim is based on intended use, the change-in

use rules will apply to actual use. Insignificant changes of less than 10% of total use of the

property will not be treated as a change in use, unless it causes a cessation of commercial use

or causes an individual to use capital property primarily for his or her personal use and

enjoyment.60

Individuals are not entitled to claim any input tax credits where real property is acquired

primarily for personal. use and enjoyment of the individual or a related individual.61

Furthermore, no input tax credits may be claimed on any improvements to such real

property.62 Because of this more limiting factor, special rules are required for individuals

where there is a change in use.63

It should be noted that where an individual uses real property partly for commercial activities

and partly for exempt activities (ie. non-commercial activities that do not relate to personal use

and enjoyment), input tax credits could still be claimed to the extent of that use. For example,

where a doctor owns a building and 60 percent of the building is used for that doctor's medical

practice (ie. an exempt use) and 40 percent is leased out to commercial tenants (ie. a

.commercial use), the doctor c;ould claim input tax credits to the extent of the commercial use

of the property (ie. 40 percent).

B. SELF-SUPPLY RULES

The self-supply rules64 are designed to deal with situations where a builder constructs or

substantially renovates a residential complex and subsequently rents it out or uses it for his or

her own residence. These rules help ensure that the builder receives the same GST treatment

as other persons who had purchased new or substantially renovated residential complexes for

residential purposes.

60.61.

62.

63.

64.

S.I97.5s.208(1).

5s.208(4).

Generally see s. 207 and 208.

Generally see s. 191.

- 26-

Since the GST was enacted, there have been three significant amendments to the self-supply

rules:

1. Firstly, the self-supply rules are extended to apply to situations where a builder sells a

house and leases the related lands;

2. Secondly, a clarification has been introduced that pre-closing occupancy arrangements

(ie - circumstances where occupancy is provided to the purchaser prior to the closing as

part of the purchase and sale agreement) do not trigger the self-supply rules; and

3. Thirdly, new subsection 191(10) has been added. This provides that where a builder

leases a residential complex or an addition thereto, and the lessee is acquiring the

complex to rent to an individual as the sub-lessee's place of residence, the builder is

deemed to have given possession of the complex to the individual as a place of

residence under the lease agreement. The result is that the self-supply rules will apply

to the builder who will be acquired to account for GST on the fair market value of the

complex.

There is an exception to the self-supply rules where the residential complex or addition thereto

is constructed or renovated by an inqividual builder and used primarily as a place of residence

for that individual builder (or related individual or former spouse), and the individual builder

has not claimed any input tax credits in respect of the acquisition or improvement to the

complex.65 As well, the self-supply rules will not apply in the following situations:

1. Where the builder constructs a residential complex (for example, a new house) for sale

and does not lease it out.

2.

3.

65.

Where a builder constructs a building and leases it to commercial, as opposed to

residential, tenants.

Where an individual, other than a builder, constructs a home for use by that individual

as a place of residence for the individual and/or related persons.

ss. 191(5).

- 27-

C. CONSTRUCTION CONTRACTS

1. Deposits

Where there is a taxable supply, the general rule is that the GST is payable on the earlier of

the day that consideration for the supply is paid and the day that consideration for supply is

due. 66 Where, however, a deposit has been given in respect of the supply (whether that

deposit is refundable or not), the consideration is not considered to have been paid in

connection with that deposit until it is applied by the supplier as consideration for the supply.67

2. Holdbacks

Where holdbacks are maintained on a construction project pursuant to The Builders' Lien

Act,68 or pursuant to an agreement in writing for the construction, renovation or alteration of a

repair to any real property, the GST on that holdback is payable on the earlier of the day that it

is paid and the day that it becomes payable.69

D. COMMISSIONS, LEGAL FEES AND OTHER DISBURSEMENTS

Given that the GST applies to services, the following expenses will be taxable on the purchase

and sale of property:

1. Legal fees.

2. Real estate commissions.

3. Many of the disbursements charges by a lawyer in handling· a real property transaction

such as photocopying, telephone and postage charges will be subject to GST if the legal

service is taxable. However, where a law fmn incurs and -pays the Land Titles

Registration costs in the name of or as agent for the client, no GST should have to be

charged.70

66.

67.68.69.70.

Ss. 168(1).Ss. 169(9). In the event of aforfeiture, s. 182 applies.S.S. 1984-85, c. B-7.1, as amended.Ss. 168(7).Schedule V, Part VI, Paragraph 20(a) exempts the application of GST on the supply of aservice of registering anyproperty or filing any document in any property registration system.

E.

- 28-

FORECLOSURES AND JUDICIAL SALES )

The general rule is that where there is a "seizure or repossession" resulting from a foreclosure

or a judicial sale, no GST will be payable.71 When the GST was ftrst proposed, one confusing

situation that existed was what the GST consequences would be in circumstances where land

was transferred to a creditor as part of a debt settlement. Technically, no seizure or

repossession had taken place. Therefore it appeared that the normal rules in connection with

. the transfer of real property would have applied. However, new Subsection 183(9) provides

that where property is voluntarily transferred by one person to another for the purpose of

satisfying in whole or in part a debt or obligation, the creditor is deemed to have acquired the

property by way of seizure or repossession. Thus, no GST will apply.

F. MORTGAGES AND SECURITY INTERESTS

A supply of fmancial services is an exempt supply.72 "Financial services" include the payment

or receipt of interest on mortgages and other debt securities.73 As such, interest expense in

relation to money borrowed for the acquisition of real property is not subject to GST.

As well, when an owner of real property grants a mortgage in that property, no "supply" is

deemed to have taken place. Furthermore, on the discharge of a mortgage or forgiveness of

debt, the re-transfer of the property or any interest therein shall be deemed not to be a

supply.74 Thus, the granting of a mortgage or its discharge will not be subject to GST.

G. CEASING TO BE A REGISTRANT

When a person ceases to be a registrant, they are required to account for GST on a deemed

disposition of property in the last GST return to be f1led. This will ensure a recapture of GST

credits previously claimed.75

71.

72.73.

74.75.

, S. 183.

Schedule v, Part VII.Ss. 123(1), definitions of "financial service" and "fInancial instnlment".

S.134.Ss. 171(3) deems the person to have ceased, immediately before ceasing to be a registrant, to use the property incommercial activities and to have sold the property to himself or herself for its fair market value and collected the

applicable GST. Where capital property is concerned, the person is deemed to have ceased using that property in .

)

- 29-

v. CASE STUDY

Mrs. Davis has entered into an agreement to sell an acreage consisting of 25 acres to Mr.

Jackson for the sum of $60,000. Mrs. Davis has been living on this property and uses

approximately one acre of it for her house and surrounding yard area. The balance of the

property (24 acres) has been rented out to a neighboring farmer on a cash-rent basis. Mrs.

Davis has reported the net income from the rental of this land on her tax return every year.

Mr. Jackson is registered for the GST. A written agreement is entered into between Mrs.

Davis and Mr. Jackson on a "standard form" offer to purchase prepared by a real estate agent.

No mention has been made of nor has any thought been given to the GST. Mrs. Davis and

Mr. Jackson have now been referred to your law fIrm by the real estate agent and you must

complete the transaction ensuring that the GST is properly accounted for. Additional

information that you should be aware of is as follows:

1. The real estate commission payable by Mrs. Davis is $4,200.

2. Each of the purchaser and vendor will pay legal fees to your law fIrm in the amount of

$195. The purchaser will be responsible for all land titles registration costs arising

from the transfer of the land.

The transaction in question is considered a "mixed" sale of a residential complex and

commercial real property. By virtue of subsection 136(2), there are deemed to be two separate

property sales:

1. One sale relates to the residential complex consisting of the home and surrounding yard

area of one acre. This property has been occupied by Mrs. Davis as her principal

residence. Its sale is exempt from GST.

2. A second sale is deemed to have taken place with respect to the balance of the farm

land (24 acres) which has been used in a commercial activity. This is a taxable sale.

commercial activities immediately before de-registration, and the change in use roles will result in a "recapture" of

input tax credits previously claimed.

- 30-

It is necessary for the vendor and purchaser to come to an agreement on a reasonable

allocation of the purchase price as between the residentIal complex and the farm land. In

discussions with your clients, an agreement is reached to allocate $45,000 to the residential

complex and $15,000 to the 24 acres of farm land. Having solved this initial problem, there

are certain things that you as the lawyer must now deal with:

1. The sale of the residential complex is exempt from GST. Mr. Jackson, as the

purchaser, will want to ensure that he receives from Mrs. Davis a certificate under

section 194 regarding the ex,empt status of this property. By having this certificate,

Mr. Jackson will have some protection should Revenue Canada later reassess this

transaction on the basis that the sale of the house and surrounding 1 acre are not exempt

from GST. In the event of such a reassessment, provided that Mr. Jackson did not

know and could not reasonably have known that the sale of this property .was not

exempt from GST, Mrs. Davis will be responsible for the GST on this property and

any related interest and penalties. She will have no recourse against Mr. Jackson.

2. The sale of the remaining 24 acres of farm land is taxable. However, because Mr.

Jackson is a GST registrant; Mrs. Davis is not under an obligation to collect the GST

from Mr. Jackson. Mrs. Davis should obtain from Mr. Jackson a certificate for the

purposes of subsection 221(2) [see Schedule "D" to this paper] and the lawyer should

contact Revenue Canada to satisfy himself or herself of Mr. Jackson's GST

registration. As well, it will be necessary for Mr. Jackson to me Form GST 60 with

Revenue Canada, Customs and Excise, and account for this transaction in his next

regular GST return. Mr. Jackson will have a liability for GST that must be paid to the

federal government in the amount of $1,050 (ie. 7% of $15,000). However, provided

that Mr. Jackson is going to use this land in a commercial activity, he can claim an

offsetting input tax credit in the amount of $1,050. The result is that he will not have

to payout any money for GST as it relates to the purchase price of the farm land.)

- 31 -

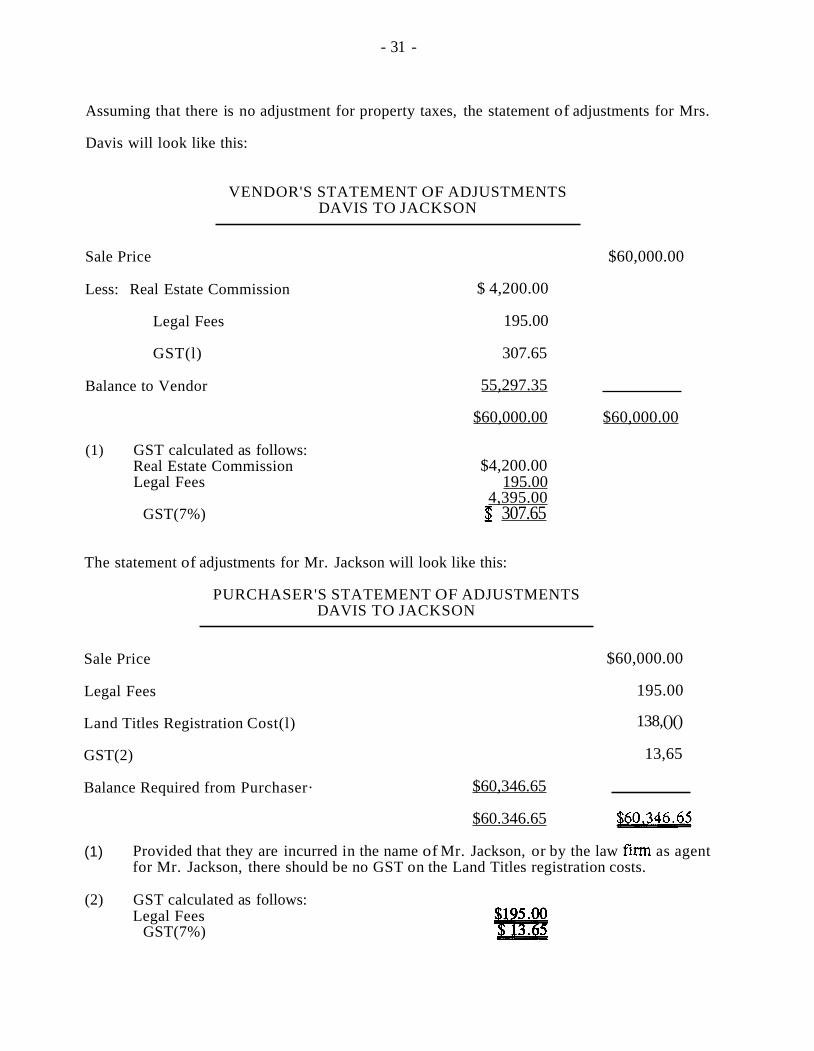

Assuming that there is no adjustment for property taxes, the statement of adjustments for Mrs.

Davis will look like this:

VENDOR'S STATEMENT OF ADJUSTMENTSDAVIS TO JACKSON

Sale Price

Less: Real Estate Commission

Legal Fees

GST(l)

Balance to Vendor

(1) GST calculated as follows:Real Estate CommissionLegal Fees

GST(7%)

$ 4,200.00

195.00

307.65

55,297.35

$60,000.00

$4,200.00195.00

4,395.00$ 307.65

$60,000.00

$60,000.00

The statement of adjustments for Mr. Jackson will look like this:

PURCHASER'S STATEMENT OF ADJUSTMENTSDAVIS TO JACKSON

Sale Price

Legal Fees

Land Titles Registration Cost(l)

GST(2)

$60,000.00

195.00

138,()()

13,65

Balance Required from Purchaser· $60,346.65

$60.346.65 ~60,346.65

(1) Provided that they are incurred in the name of Mr. Jackson, or by the law frrm as agentfor Mr. Jackson, there should be no GST on the Land Titles registration costs.

(2) GST calculated as follows:Legal Fees

GST(7%)

- 32-

It should be noted that if the facts were a little different such that:

1. Mrs. Davis had used the farm land in the business of farming;

2. Mr. Jackson was acquiring all of the farm land for his personal use and enjoyment; and

3. Mrs. Davis and Mr. Jackson were related;

the entire sale (including the 24 acres of farm land) would be exempt from GST by virtue of

Schedule V, Part I, Paragraph 10.

VI. CONCLUSION

Since January 1, 1991, lawyers have had to deal with the GST on a day-to-day basis. For

lawyers who primarily do "solicitor" work, it is necessary to have an understanding of the

GST as it relates to real property transactions. Only by keeping up with changes to the Act

and the administrative practices of Revenue Canada can lawyers competently advise their

clients in this area.

Beaty BeaubierSeptember 10, 199~\word\office\GST-REAL.DOC

,)

- 33 -

SCHEDULE "A"

GST EXEMPTION VENDOR'S CERTIFICATE

TO: (the "Purchaser")-----------------------RE: (the "Lands")-------------------------

The undersigned Vendor(s) does hereby covenant, represent, certify and warrant(jointly and severally, if more than one) to the Purchaser that:

1. The Vendor is the owner of the Lands.

2. That the above mentioned sale of the Lands by the Vendor to the Purchaser is anexempt supply described in one of Sections 2-5.3, 8 & 9 of Part I of Schedule V tothe Excise Tax Act (Canada).

3. This document constitutes a written certificate for the purposes of the Section 194of the Excise Tax Act (Canada).

Dated at , in the Province of Saskatchewan, this___ day of , A.D. 199_.

SIGNED, SEALED & DELIVERED ) (seal)in the presence of: ) Signature of Vendor

))

Print Name of Vendor)))

Signature of Vendor(seal)

))

Witness)

PriDt Name of Vendor)

••• Revenue Canada Revenu CanadaCustoms and Excise Douanes et Accise

NEW HOUSING APPLICATION FOR REBATEOF GOODS AND SERVICES TAX

- 34- SCHEDULE "B"

PROTECTED when completedPersonal infonnatlon provided on this form is protected under the provisions ofthe Privacy Act and is maintained in Personal Information Bank RCCJP·PlJ.09O

Cette formule est disponible en FRANCAIS

Mail to: GST Interim Processing CentreOllawa, OntarioK1A 1J6

'~"{ use.~ indiYidu81s who purchase MW or IUbstantialIy renovaIed housing, or who build MW housing orJl'l&"'!aIly renovat••xisting housing, or who purchase 8 share 01 the capital stock in 8 co-operative housing

,...rporation in respect of 8 single residential unlt,for use as 8 prim8IY place 01 residence lor themselves or 8relation, and who qualify lor 8 r.~te under sections 254, 255 or 2S6 01 the Excise Tax Act.

• For more details and definitions of terms used In this application, refer toForm Completion Guide

• Please print or typeA - CLAIMANT IDENTIFICATION (Rebate to be claimed by one individual only)Claimant's Last Name First Name and Initial(s)

IAddress of Property (Number, Street and Apt. No. or P.O. Box No. or A.R. No.)

City

Province Postal Code Telephone No.

I I ( )Mailing Address (Number, Street and Apt. No. or P.O. Box No. or A.R. No.) (If different from above)

City

Province Postal Code Telephone No.I ( )

Language Preference~

o English o French Date ownership of property was transferred to purchaser~~Preference Iinguistique Anglais Frangais or date of substantial completion I renovation

Legal Description of Property (Lot, Concession, Plan, Range, Parcel, Section, etc.)

T

B - TYPE OF APPLICATION

• Check only one of the following.

1)0 The rebate claimed is for GST paid on housing purchased from a builder who has paid or credited the rebate to the purchaser.(Calculate the rebate in Part I of Section D.)

2) 0 The rebate claimed is for GST paid on housing purchased from a builder who is not paying or crediting the rebate to thepurchaser. (Calculate the rebate in Part I of Section D.) .

3) 0 The rebate claimed is in respect of the purchase of a share of the capital stock of a co-operative housing corporation. (Calculatethe rebate in Part III of Section D.)

4) 0 The rebate claimed is for GST paid in respect of housing constructed or substantially renovated by the claimant. (Calculate therebate in either Part I of Section D or Part II of Section D.)

• • •Builder's Legal Name

.. . .....GST Account No.

Address

City

lince

The rebate was paid or ~ Dcredited to the claimant Yes

Signature of Builder or Authorized Official

Postal Code

If yes, provide the period of the GSTRetum on which an adjustment wastaken (Line 107: ITC Ad'ustments).

Name (Print)

Telephone No.( )

IY,M,DIIY,M.D/From~ To L-L-.l-L.J..-LJ

Date

.;, 35-

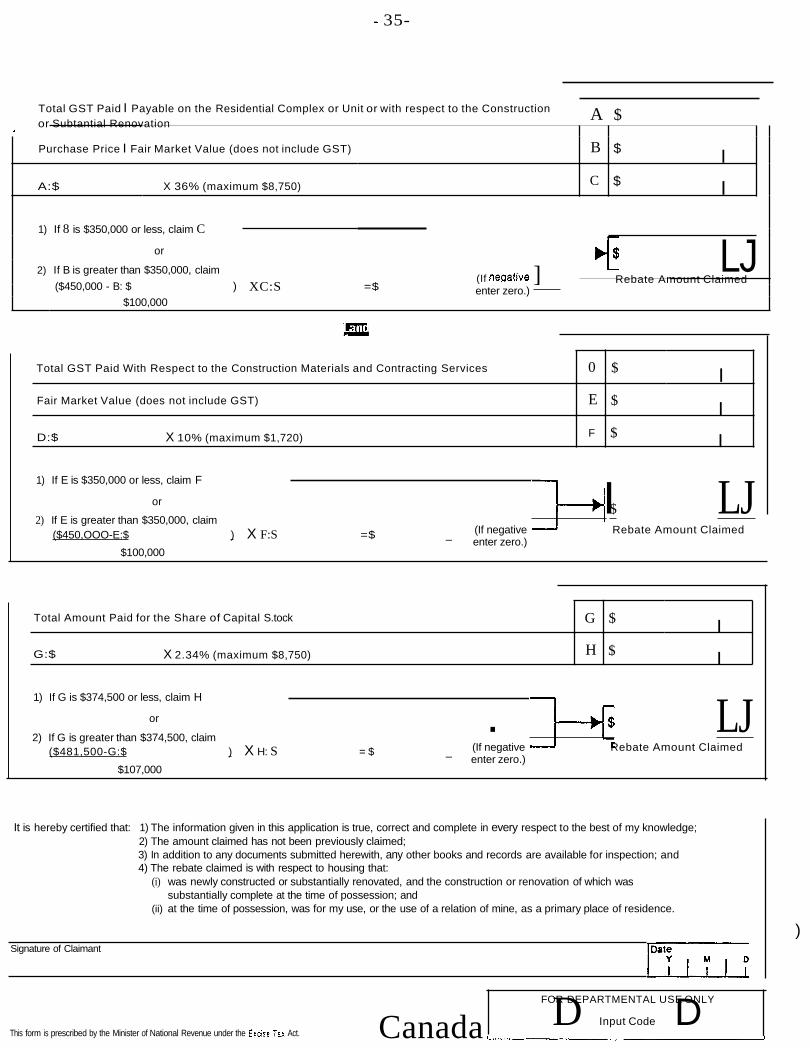

- CALCULATION OF REBATE (Complete only Part I, Part II or PART III)

T I Housing Rebate Where GST Was Paid On the Land That Forms Part of theResidential Complex or Unit (For use by claimants who checked box 1, 2 or 4 in Section B)

A $Total GST Paid I Payable on the Residential Complex or Unit or with respect to the Constructionor Subtantial Renovation

•

Purchase Price I Fair Market Value (does not include GST) B $ IA:$ X 36% (maximum $8,750) C $ I

1) If 8 is $350,000 or less, claim C

(If ""al"" ]or "1$ LJ2) If B is greater than $350,000, claim

($450,000 - B: $ ) XC:S =$Rebate Amount Claimed

enter zero.)$100,000

PART \I Housing Rebate Where GST Was Not Paid On the ':Bnd That Forms Part of theResidential Complex (For use by claimants who checked box 4 in Section B) .

Total GST Paid With Respect to the Construction Materials and Contracting Services 0 $ IFair Market Value (does not include GST) E $ ID:$ X 10% (maximum $1,720) F $ I

1) If E is $350,000 or less, claim F

or

2) If E is greater than $350,000, claim($450,OOO-E:$ ) X F:S =$ _

$100,000

J~---.,~I$ LJ(If negative Rebate Amount Claimedenter zero.)

PART III Housing Rebate Where a Share of the Capital Stock of a Co-operative Housing CorporationWas Purchased (For use by claimants who checked box 3 in Section B)

Total Amount Paid for the Share of Capital S.tock G $ IG:$ X 2.34% (maximum $8,750) H $ I

1) If G is $374,500 or less, claim H

or

2) If G is greater than $374,500, claim($481,500-G:$ ) X H: S = $ _

$107,000

. J--"'~I$ LJ(If negative Rebate Amount Claimedenter zero.)

E - CERTIACAnON

It is hereby certified that: 1) The information given in this application is true, correct and complete in every respect to the best of my knowledge;2) The amount claimed has not been previously claimed;3) In addition to any documents submitted herewith, any other books and records are available for inspection; and4) The rebate claimed is with respect to housing that:

(i) was newly constructed or substantially renovated, and the construction or renovation of which wassubstantially complete at the time of possession; and

(ii) at the time of possession, was for my use, or the use of a relation of mine, as a primary place of residence.

Signature of Claimant

)

FOR DEPARTMENTAL USE ONLYD Input Code DThis form is prescribed by the Minister of National Revenue under the Exci~e Tax Act. Canada '-----------------------'

1+1 Revenue CanadaCustoms. Excise and Taxation

Revenu Canada.Accise. Douanes etlmpot

- 36- SCHEDULE "c"

0001PROTECTED when completed

PROTEGE une fols rempll

GOODS AND SERVICES TAX RETURN FOR ACQUISITION OF REAL PROPERTYTAXE SUR LES PRODUITS ET SERVICES - DECLARATION VISANT L'ACQUISITION D'IMMEUBLES

Prescribed by the Minister of Nationa: Revenue under subsection 228 (4) of the Excise Tax ActPrescr~e par Ie rninistre du Revenu natior.al en venu du paragraphe 228 (4) de Ia Loi sur Ia taxe d'accise

THIS RETURN IS FOR USE BY A PERSON WHO IS REQUIRED TO CETTE DECLARATION DOlT ETRE REMPLIE PAR TOUTE PERSONNEDECLARE AND PAY TAX ON THE ACQUISITION OF TAXABLE REAL QUI EST TENUE DE DECLARER ET DE PAYER LA TAXE SUR

PROPERTY. L'ACQUISITION D'UN IMMEUBLE TAXABLE.

TO COMPLETE THIS FORM, PLEASE REFER TO THE INSTRUCTIONS POUR REMPLIR CETTE FORMULE VEUILLEZ LIRE LES INSTRUCTIONSON THE BACK. IF ADDITIONAL INFORMATION IS REQUIRED, REFER AU VERSO ET LE MEMORANDUM 500-2-6 SI NECESSAIRE.TO MEMORANDUM 500-2-6.

IF YOU NEED ASSISTANCE, CONTACT YOUR LOCAL REVENUE SI VOUS AVEZ BESOIN D'AIDE, COMMUNIQUEZ AVEC VOTRECANADA EXCISEIGST DISTRICT OFFICE. BUREAU LOCAL DE REVENU CANADA, ACCISE - TPS.

Name of Individual or Entity / Nom du particulier ou de I'entite Acquis~ion Date / Dale d'acquis~ion GST Account Number

Y~A I ~ I D/J Numero de compte TPSI I I I I I I I I I I I I I I I I I I I I I I I I I

Trading Name if Dillerenl From Above / Nom de la raison sociale s'i1 dilli!le de I'entite ou du nom Due Date / Dale d'echeanceY/A

IM

ID/J

I I II I I I I I I I I I I I I I I I I I I I I I I I I I I I I , I I IMailing Address (No., Street and Apt. Number) / Adresse postale (n', rue, app.)

I I I I I r I I I I I I I I I I I I I I I t I I I I I I I I I I I I I I I I I I I I

City/Ville

I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I

Province

I IPostal Code / Code postal

I I I I I I I I I I I I I I I r I I r I I I I I I I I I I I t I I I I I I I I

Name of the Person We May COnlact Concerning Your Return I Nom de ia ~,sonr.e avec qui nous pouvons communiquer concernanl votre declaralion Telephone No./ N' de telephone

I I I I I I I I I I I r I I I I I I I I I I I I I I I I t ( ) I I I I - I I I I

l'iPtion and Address of Property / Description et adresse de I'immeuble

I I I r I r r I I I I I I I I I I I I I I I I I I I I I I I I I I I t I I r I I I I

I I I I I I I I I I I I I I I I I I I I I I I I I I I I' I I I I I I I I I I I I I IVendor's Name and Address / Nom et adresse du vendeur

I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I

I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I

ITota, Taxable Acquisition

1201

I I I I /payment Enclosed

1203

1 LJTotal d' acquisition taxableI I I I I I I I I ,Paiement inclus

I II I I I

~ MUL TlPL Y BY / MUL TlPLIEZ PAR .07 Ollsel the tax due to the exlent of my refund

ITax Due B LJ enlitlemenl on my regular GST return for the period

I, I I oending: I Y/A

I M

ID/J ITaxe due

I I I I IVeuillez compenser la taxe due par Ie montant du I I I

~You are not required to remit a balance of less than 51.00 remboursement de TPS vise dans ma declarationVous n'{i1es pas lenu de payer un montant inferieur iJ 1.00 S pour la periode qui vient de prendre fin:

CE~nFJCAT'ON I DECLARAnON.:."~.: .. ~~: .: ..?;..-:....., __.. -..... '_..... \ ~!i;;,...,..:,. _J':~ • ~ ':.: ••~• .I .... '," :-

. '.. . .{ -. "- " . . , . .. . ..'.~ -. ~ ., .. '. , .' . . .' .

I cenify that the information given in lhis relurn is lrue. correct and cO::'lp:e:e in every respect and that I am Je declare que les renseignements fournis sont exacts el complets sous tous les rappons et que j'aiauthorized 10 sign on beha" of the person filing this return. I'autorisation de signer au nom de Ia personne qui produ~ III presente declaralion.

Name/Nom Title/Tilre

Signature Date

.. IT IS A SERIOUS OFFENCE TO MAKE A FALSE RETURNLA PRODUCTION D'UNE FAUSSE DECLARATION EST UNE INFRACTION GRAVE

\

t-~.,;jnal information provided on this form is protected under the provisions of Les renselgnements personnels fournis dans celie formule sont proteges enthe Privacy Act and is maintained In Persona/Information Bank RCC/P-PU·065 vertu de la Loi sur la protection des renseignements personnels et sont

conserves dans Ie Repertoire de renseignements personnels RND/P·PU·065

Part 1 • DETACH AND FORWARD TO PROCESSING CENTRE Partie 1 - DETACHEZ ET FAITES PARVENIR AU CENTRE DE TRAITEMENT PROVISOIRE

~ ~11.1, ,~n~(l~

- 37-

CERTIFICATEGIVEN BY PURCHASER

PURCHASING COMMERCIAL REAL ESTATE

To the Vendor: -----------The undersigned does hereby certify, covenant, represent and warrant to the Vendorthat:

(a) The undersigned is purchasing from the Vendor the following Land, namely:

(b) The undersigned is a Registrant for the purposes of the Goods and Services Taxunder the Excise Tax Act (Canada), and has Registration Number

. This information and certificate is given for the purpose of-ad"T'v......is......in-g-t::'Th-e-;r-V·endor of this registration and relieving the Vendor of theresponsibility of collecting the GST by virtue of Paragraph 221(2)(b) of the ExciseTax Act (Canada);

(c) The Vendor and/or the solicitors of the Vendor, namely, Priel, Stevenson, Hood &Thornton be and are hereby irrevocably authorized and permitted to contactRevenue Canada to confirm such GST registration, and Revenue Canada and itsvarious agents and representatives are hereby authorized to provide informationto the Vendor and/or the solicitors for the Vendor, namely Priel, Stevenson, Hood& Thornton, confirming the status of the undersigned's registration for thepurposes of the goods and services tax under the Excise Tax Act (Canada).