Embed Size (px)

Citation preview

THE GLOBAL PENSION FUNDS OVERVIEW –

HOW CAN WE ENSURE RETIREMENT

SECURITY AND AFFORDABILITY

Roger Urwin, FSIP

Strategic Director, Future of FinanceGlobal Head of Investment Content, Willis Tower Watson

June 2016

Future of Finance Initiative | Putting Investors First

Ljubjana-Sofia-Budapest-Kiev

2

Future of Finance Strategic Objective:

To shape a trustworthy, forward-thinking investment profession that better

serves society.

The future of finance will be better if financial market practices are fair

and efficient and financial service providers put investors’ interests first.

CFA Institute mission: To lead the investment profession globally by promoting the highest

standards of ethics, education, and professional excellence for the ultimate benefit of society.

What

THE CFA INSTITUTE FUTURE OF FINANCE INITIATIVE

How

Why

By creating and curating content, and convening discussions where

critical issues can be socialized to motivate the industry, individually and

collectively to be professional and effective

3

Retirement Security & Affordability

Putting Investors First

Industry Structure, Content & Culture

NEW

THE FUTURE OF FINANCE AREAS OF FOCUS

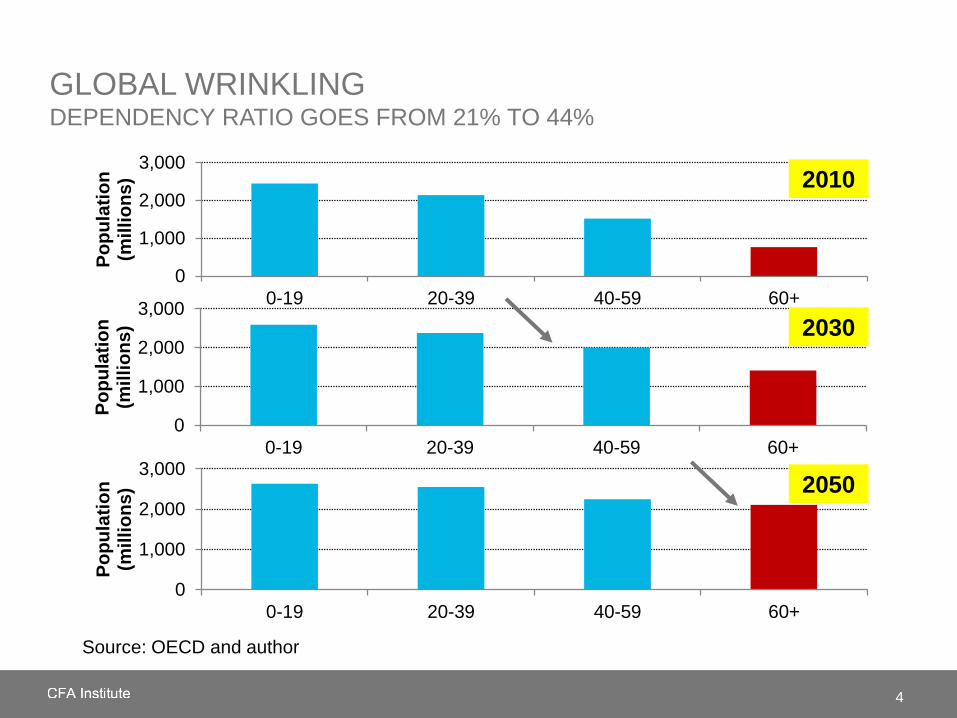

GLOBAL WRINKLINGDEPENDENCY RATIO GOES FROM 21% TO 44%

4

0

1,000

2,000

3,000

0-19 20-39 40-59 60+

Po

pu

lati

on

(m

illi

on

s)

0

1,000

2,000

3,000

0-19 20-39 40-59 60+

Po

pu

lati

on

(m

illi

on

s)

0

1,000

2,000

3,000

0-19 20-39 40-59 60+

Po

pu

lati

on

(m

illi

on

s)

2010

Source: U.S. Census Bureau and Watson WyattSource: OECD and author

2030

2050

5

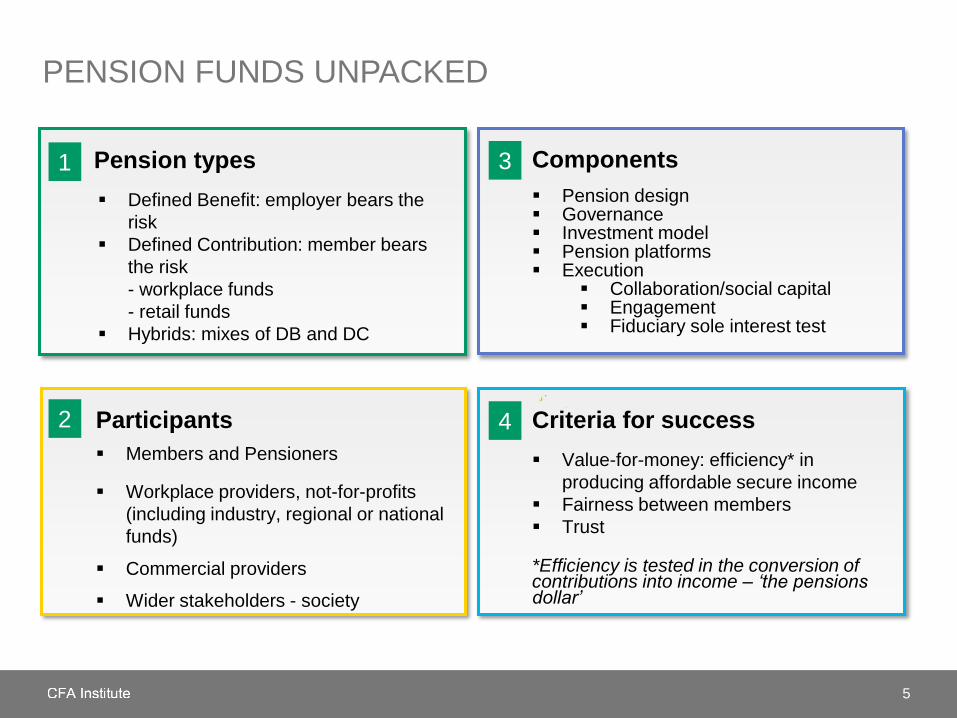

PENSION FUNDS UNPACKED

Participants

Members and Pensioners

Workplace providers, not-for-profits

(including industry, regional or national

funds)

Commercial providers

Wider stakeholders - society

Components

Pension design Governance Investment model Pension platforms Execution

Collaboration/social capital Engagement Fiduciary sole interest test

Criteria for success

Value-for-money: efficiency* in

producing affordable secure income

Fairness between members

Trust

*Efficiency is tested in the conversion of contributions into income – ‘the pensions dollar’

Pension types

Defined Benefit: employer bears the

risk

Defined Contribution: member bears

the risk

- workplace funds

- retail funds

Hybrids: mixes of DB and DC

1 3

2 4

6

Big investment issues

DB and DC – switching ownership and control

Investing – low for longer, rates and returns

Investment governance – fiduciary tests

Costs – need to be contained

4

$38.4tn Total Pension

Assets

$ 2bn+Total Pension

Fund Members

7Big Pensions

Countries

Canada

Netherlands

Switzerland

UK

US

Australia

Japan

P7

Source: WTW Global Pensions Study 2016

GLOBAL PENSION ASSETS

7

GLOBAL PENSION ASSET ALLOCATIONAggregate P7 asset allocation from 1996 to 2015

16%

8%

Source: Willis Towers Watson and secondary sources

52% 50% 48%

44%

37%

38%

32%29%

7% 9%

19%24%

5% 3% 1% 3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1996 2002 2008 2015e

Equities Bonds Other Cash

Other/ Alternatives

Equities

Domestic Equities

Foreign Equities

8

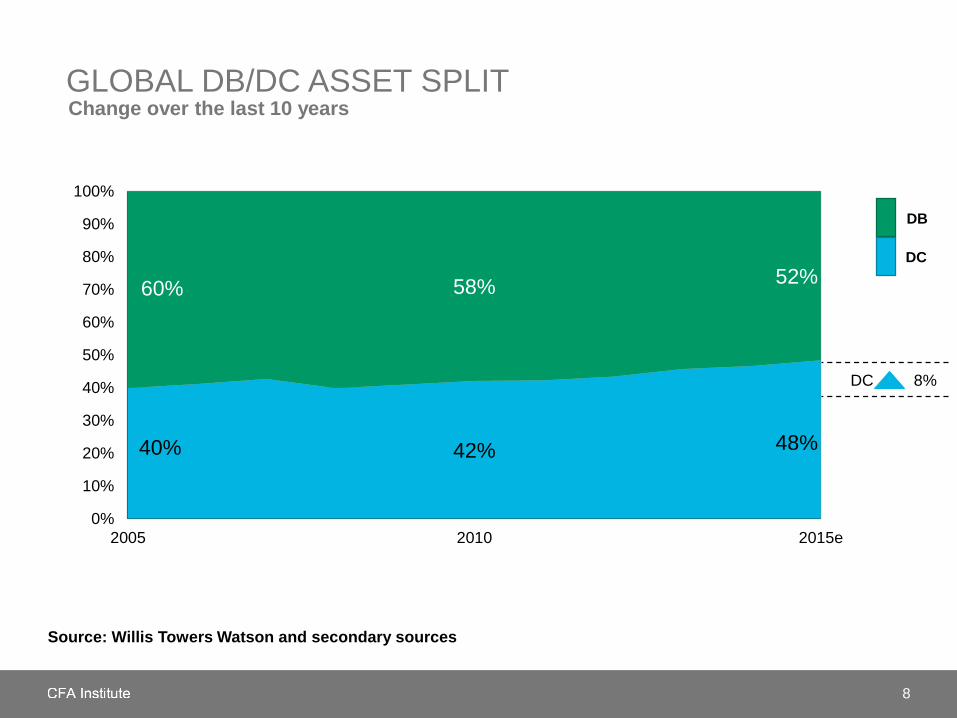

40% 42% 48%

60% 58%52%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2010 2015e

GLOBAL DB/DC ASSET SPLITChange over the last 10 years

DC 8%

Source: Willis Towers Watson and secondary sources

DC

DB

9

Some key conclusions from the study include:

Their allocations average 41% to equities, 34% to bonds and 25% to alternatives and

support an expected 10 year return of CPI + 2.9% pa

These funds are seeking returns well in excess of the liquid market bulk beta

principally through their private market reach, increasing allocations to smart betas

and continuing commitments to alpha; and through strengthening internal capabilities

These funds are increasingly transparent and increasingly influential

Source: WTW Thinking Ahead Institute

DB TOP TEN STUDY

Americas Europe, Middle East,

Africa

Asia Pacific

CalPERS (US) PGGM (Netherlands) GPIF (Japan))

New York (US) ABP (Netherlands) NPS (Korea)

CPPIB (Canada) ATP (Denmark)

Ontario Teachers (Canada) GPFG (Norway)

10

THE DECLINE OF DB (DEFINED BENEFITS)

Defined Benefits have been increasingly

costly over time because of bargaining,

longevity and guarantees

Pensions have become even more expensive

in the QE era with low for longer, rates and

returns

The social capital in defined benefits

pensions (shared values and understanding

of stakeholders – members, pensioners,

sponsors, media, government and others)

has got worse

So inevitably, Defined Contribution has

replaced Defined Benefit as the most viable

pensions choice going forward

DB IN SOME

PLACES IS A TRAIN-WRECK

11

THE RISE OF DC (DEFINED CONTRIBUTIONS)

DC investment is a highly complex pension delivery system because of the multiple

membership segments – all with unique needs and wants

Investment models have delivered simple models to DC in pre-retirement investing

Balanced and growth fund investing

Target and lifecycle designs

Default funds and choice funds

But effective overall pensions delivery has

not yet

been attained anywhere because of the

limitations of the platforms, the alignments,

and the engagement

The engagement/combination is the

biggest issue – how the product of the DC

provider and member can produce a

product more than the sum of the parts

DC REQUIRES

BETTERENGAGEMENT

AND TRUSTTO FUNCTION

HEALTHILY

INVESTORS LACK TRUST IN FINANCIAL SERVICES

12

77%

61%RETAIL

47%

57%INSTITUT-

IONAL

51%GENERAL

PUBLIC

TECHNOLOGY

FINANCIAL

SERVICES

MEDIA

Source: CFA Institute Trust to Loyalty Survey 2016

How much do you trust businesses in these industries to do what’s right?

13

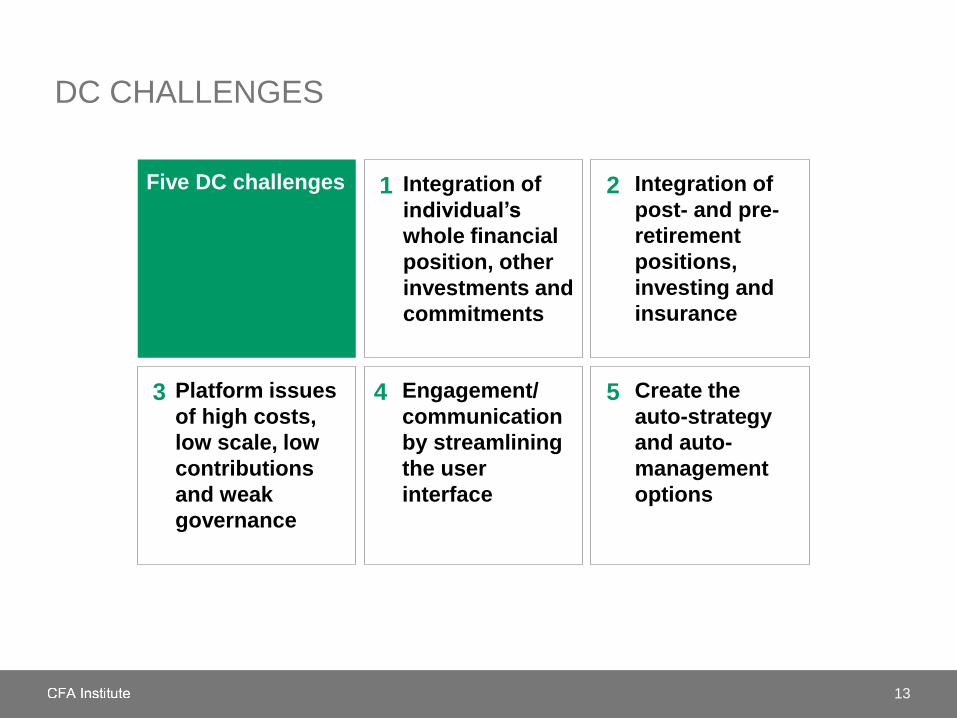

DC CHALLENGES

Five DC challenges Integration of

individual’s

whole financial

position, other

investments and

commitments

1

Platform issues

of high costs,

low scale, low

contributions

and weak

governance

3

Integration of

post- and pre-

retirement

positions,

investing and

insurance

2

Create the

auto-strategy

and auto-

management

options

5Engagement/

communication

by streamlining

the user

interface

4

14

Some key conclusions from the study include:

Funds’ internal capabilities are being significantly strengthened

Sustainable investing strategies among these funds are diverse but appear set to take

a step up

These funds give increasing attention to their communications and user interfaces

Complexity, culture and managing change are major pre-occupations for all funds

These funds are increasingly transparent and increasingly influential

Source: WTW Thinking Ahead Institute (forthcoming)

DC TOP TEN STUDY

Americas Europe, Middle East, Africa Asia Pacific

TIAA (US) British Telecom PS (UK) Q Super (Australia)

IBM (US) NEST (UK) Australian Super (Australia)

Microsoft Plan (US) GEPF (South Africa) First State Super (Australia)

CPF (Singapore)

15

DC COMPETITIVE AND DISRUPTIVE FORCES

The bargaining power of DC

funds with participants

- including regulatory factors

- including ESG/UO ship

The substitution

opportunities in

internalisation

The intense competition

- for returns

- for talent

The bargaining power of DC

funds with suppliers,

particularly asset managers

Threat of competition

– opting out/alternative

providers

e.g., Aus

Super

e.g.,

NEST

e.g., UK cost caps

& ESG/UO at FSSe.g., CPF

e.g.,

Microsoft

DISRUPTIONS IN THE INVESTMENT INDUSTRY

There is an accelerating pace of change in the investment industry

The best way to get a grasp of this change is by looking at the industry as an

ecosystem – people and firms, technologies and other forces, and markets

The single factor most associated with organisational success or failure is

ability to adapt to the changing realities of the ecosystem, recognising the

disruptions and innovations possible, factoring in:

The competitive forces that challenge organisational success

The technology forces in ‘Fintech’ and ‘Soctech’ and other forms of

revised thinking and working

Macro forces in geopolitics and economics

Societal forces in how investing touches society – inequality and

inclusion; environment and climate; societal cohesion

All of the above are topics in our line of sight in the Future of Finance

23

TIMELINE FOR DC – THREE ERAS

17

1. Emergent

Technology Era

Lifecycle/

Lifecycle/ TDF

Growth Model

and multi-asset

investing

Post retirement

income

Flexible annuities

2. Clunky

Product Era

Poor

engagement

Expensive admin

Clunky plumbing

Poor diversity

No post

retirement

integration

Platform

integration

Whole of life

integration

Full investment

efficiency

Streamlined

plumbing

Social media

Deferred annuities

3. Integrated

Delivery Era

Investment Innovation Platform Innovation

18

37%

23%

15%

11%

2%

40%

13%11%

30%

2%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Robo-advisers Marketplace /Peer-to-Peer

lending

Crowdfunding Blockchaintechnology

Other

Which technology do you see as having the greatest impact on the financial services industry 1 year and 5 years from now?

1 year from now 5 years from now

FINTECH SURVEY OF CFA INSTITUTE MEMBERS:

UNDERSTANDING THE LANDSCAPE

The data collection was conducted online 5-19 February 2016. There were 3,803 members who were invited to participate and 775 valid responses

were received for a response rate of 20% and a margin of error of ±3.2.

19

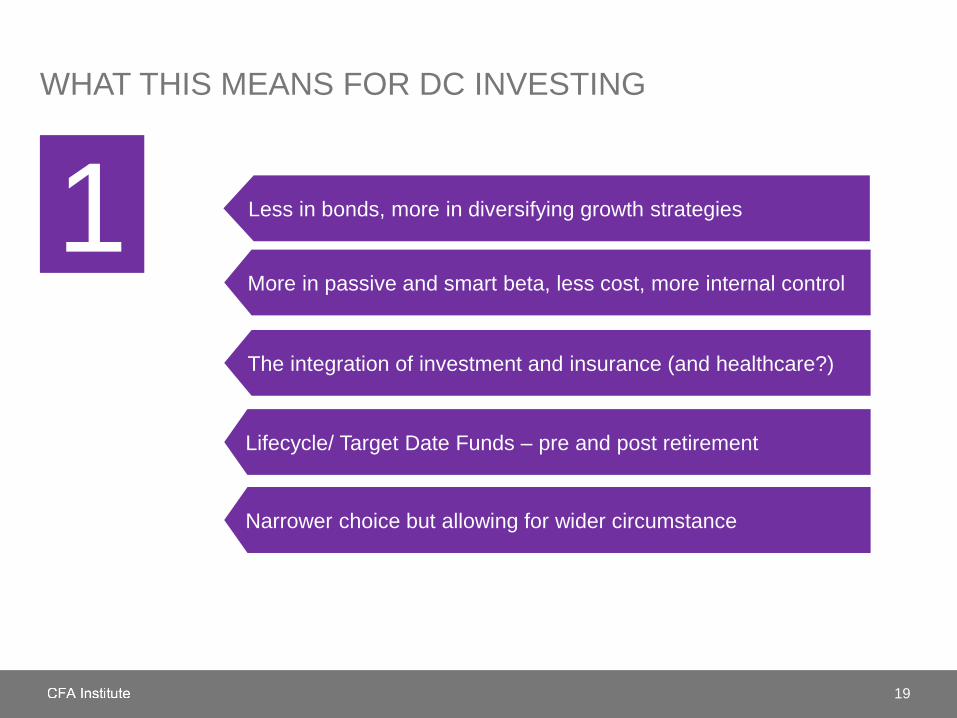

WHAT THIS MEANS FOR DC INVESTING

Less in bonds, more in diversifying growth strategies

More in passive and smart beta, less cost, more internal control

Narrower choice but allowing for wider circumstance

Lifecycle/ Target Date Funds – pre and post retirement

The integration of investment and insurance (and healthcare?)

1

20

VISION OF ‘THE PENSIONS DOLLAR’

Member Contributions

- c20%

Employer Contributions

- c20%

Investment Return

- c60%

You put in $X as contributions, usually after tax

Your employer adds the same amount

Your fund can be trusted over time to generate gains of as much as three times this sum

Your income is five times your original $X contribution with some additional tax advantages

2

Note: Calculations vary widely by context, including effects of inflation | See Ezra

21

WHAT THIS MEANS FOR DC PARTICIPANTS

‘Later life’ and ‘work tapering’ - a mixture of work, leisure,

education and healthcare

Pension finance for later life powered by auto-strategies and

auto-management from trustworthy, forward-thinking pension

platforms

Pensions making a contribution to well-being

3

RETIREMENT

LATER LIFEWORK TAPERING

X

22

4

WHAT THIS MEANS FOR TOMORROW’S INVESTMENT

PROFESSIONAL

Gets

involved

- Understands/deals with all the moving parts

of the investors’ circumstances

Well-

connected

- Behavioural savvy

- Good with governance

Highly

principled

- Client-centric and ethical

- Recognises their responsibilities

Technically

proficient

- Effective with the challenges of current

investment markets

23

WHAT THIS MEANS FOR TOMORROW’S DC PENSION

PLAN

Minority Report - Steven Spielberg’s future vision of Washington DC

Vision of marketing engagement through retina scanning

• New technologies and platform engagement for capture of life

circumstances and peer segments

Vision of autonomous cars and road systems

• New pension auto-strategies and auto-management based on life

circumstances and social networks

5

THE INVESTMENT PROFESSION’S OPPORTUNITY

24

The industry has hidden behind market conditions (“not in our control, not our fault”) and let new catalysts bring about early stages of decline in the perception of value for fees

The new model has to deliver value through all segments – from

millennials to baby boomers

That model must have more immediacy, simplicity, personalization,

and integrity

Even in a lower fee rate world, there can be higher AUM, and a bigger

value proposition exploited by those who adapt best to the new landscape

6

25

CONTACT DETAILS

Roger Urwin FSIP

Strategic Director

CFA Institute Future of Finance

Roger is the Strategic Director for the Future of Finance initiative working as a consultant to the

CFA Institute. Roger was formerly a Board of Governors Member, CFA Institute from 2008 to

2014.

Also

Global Head of Investment Content

Willis Towers Watson

Roger assumed the new post of Global Head of Investment Content at Towers Watson in July

2008 after acting as the Global Head of the investment practice from 1995 to 2008.

Roger joined Watson Wyatt in 1989 to start the firm's investment consulting practice and under

his leadership the practice grew to a global team of over 600. His prior career involved heading

the Mercer investment practice and leading the business development and quantitative

investment functions at Gartmore Investment Management.

Roger’s current role includes work for some of the firm's major investment clients both in the UK

and internationally. He leads the firm’s work on transformational change and has conducted

major strategic reviews at a number of global leading funds. He is also involved with the Towers

Watson thought leadership group (Thinking Ahead Group) and co-founder of the Thinking Ahead

Institute.

His investment innovations include three global firsts: the creation of the first target date and

lifestyle DC funds (in 1988), the risk budget framework (in 1999) and the governance budget

framework for assessing asset owner organisational effectiveness (in 2007). He is also the

author of a number of papers on asset allocation policy, manager selection and governance and

sustainability.

Roger has a degree in Mathematics from Oxford University and a Masters in Applied Statistics

also from Oxford. He qualified as a Fellow of the Institute of Actuaries in 1983. He became a

Fellow of the UK CFA Society in 2015.

Also MSCI Advisory Director Roger is part-time Advisory Director at MSCI Inc

Contact [email protected] | [email protected] | +44 7802 974003

26

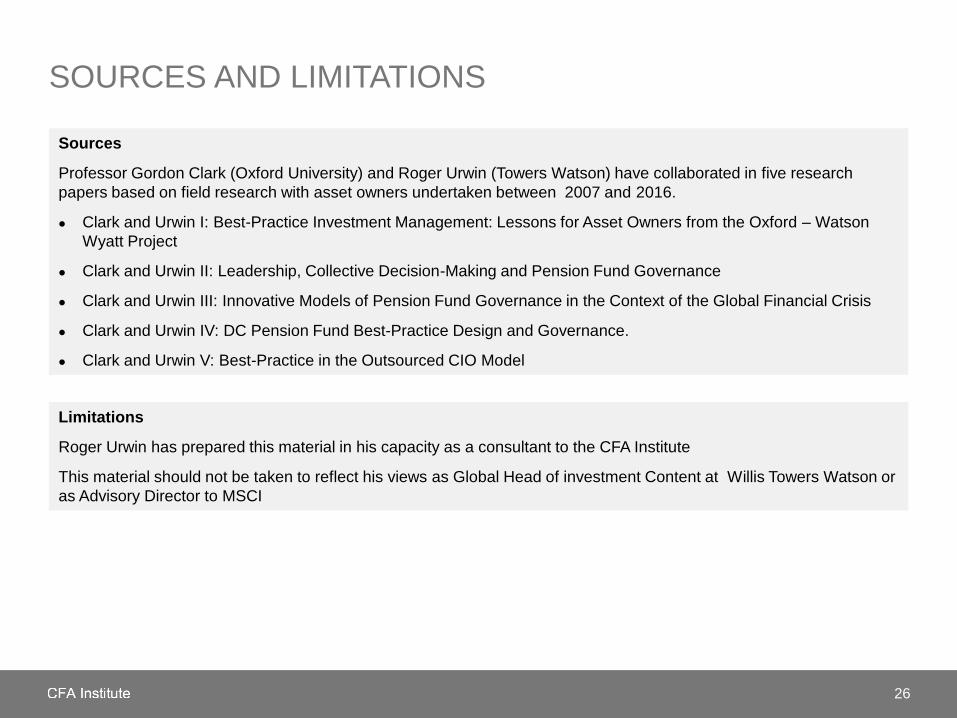

SOURCES AND LIMITATIONS

Sources

Professor Gordon Clark (Oxford University) and Roger Urwin (Towers Watson) have collaborated in five research

papers based on field research with asset owners undertaken between 2007 and 2016.

Clark and Urwin I: Best-Practice Investment Management: Lessons for Asset Owners from the Oxford – Watson

Wyatt Project

Clark and Urwin II: Leadership, Collective Decision-Making and Pension Fund Governance

Clark and Urwin III: Innovative Models of Pension Fund Governance in the Context of the Global Financial Crisis

Clark and Urwin IV: DC Pension Fund Best-Practice Design and Governance.

Clark and Urwin V: Best-Practice in the Outsourced CIO Model

Limitations

Roger Urwin has prepared this material in his capacity as a consultant to the CFA Institute

This material should not be taken to reflect his views as Global Head of investment Content at Willis Towers Watson or

as Advisory Director to MSCI

27

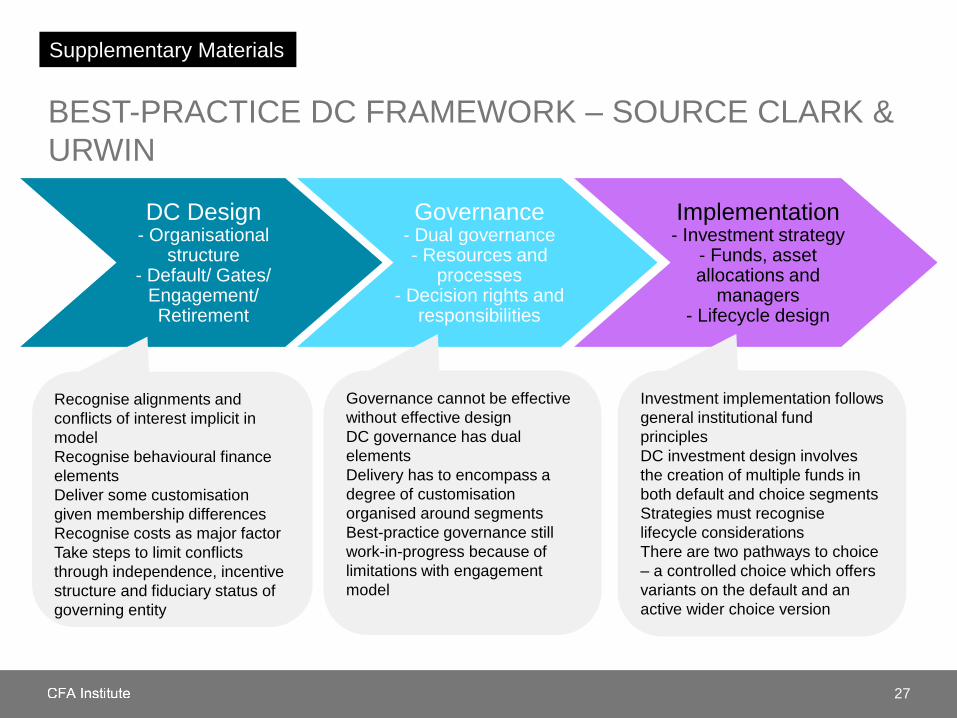

BEST-PRACTICE DC FRAMEWORK – SOURCE CLARK &

URWIN

DC Design- Organisational

structure- Default/ Gates/

Engagement/ Retirement

Governance- Dual governance- Resources and

processes - Decision rights and

responsibilities

Implementation- Investment strategy

- Funds, asset allocations and

managers- Lifecycle design

Recognise alignments and

conflicts of interest implicit in

model

Recognise behavioural finance

elements

Deliver some customisation

given membership differences

Recognise costs as major factor

Take steps to limit conflicts

through independence, incentive

structure and fiduciary status of

governing entity

Governance cannot be effective

without effective design

DC governance has dual

elements

Delivery has to encompass a

degree of customisation

organised around segments

Best-practice governance still

work-in-progress because of

limitations with engagement

model

Investment implementation follows

general institutional fund

principles

DC investment design involves

the creation of multiple funds in

both default and choice segments

Strategies must recognise

lifecycle considerations

There are two pathways to choice

– a controlled choice which offers

variants on the default and an

active wider choice version

Supplementary Materials

THE FACES OF CHANGESIX MEDIUM-TERM FACTORS GROWING IN INFLUENCE ON PENSION FUND DEVELOPMENT

1. Improvements in governanceImproved recognition of return on governance feeds through in increased attention and growing focus on performance from all sources; more talent attracted to Chief Investment Officer role at funds.

2. Risk management focusFunds focus on risk intensifies, with two separate groups: those where the appetite for risk is trimmed from previous levels; those needing risk for their situation

3. Pension design, towards a DC modelDC becomes the dominant global model with its attendant risk transfer causing tension in the balance of ownership and control

4. Pressure for talentStrong competition for talent among pension funds and their asset managers, particularly on the leadership level, despite the reduced short-term demands as a result of the financial crisis.

5. New value chainA more effective “value chain” will emerge, where expense on various activities has a better value proposition than exists today. The use of passive approaches and smart betas is leading to modest fee compression.

6. New ideology emergingSome shift from a pure finance way of seeing pension investing (where short-term performance is paramount) to one where the longer-term sustainable growth aspect is considered (where longer term cash flow and stakeholder value with a longer term focus are critical); in this model, more integrated approaches to ESG and better stewardship exercised over ownership will be present

Supplementary Materials