Embed Size (px)

Citation preview

The authors gratefully acknowledge the helpful comments and suggestions of Milind Shrikhande,Ufuk Ince, and Anna Agapova along with those of an anonymous reviewer. We have benefited fromdiscussions with Andrei Osonenko of Swaps Monitor Publications regarding the data used in thisanalysis.*Correspondence author, Department of Finance, J. Mack Robinson College of Business, GeorgiaState University, MSC 4A1264, Gilmer Street SE, Unit 4, Atlanta, GA 30303; e-mail: [email protected]

Received September 2003; Accepted February 2004

� Ekaterina E. Emm is Genevieve Albers Visiting Fellow at Seattle University in Seattle,Washington.

� Gerald D. Gay is a Professor and Chairman in the Department of Finance at J. MackRobinson College of Business at Georgia State University in Atlanta, Georgia.

The Journal of Futures Markets, Vol. 25, No. 1, 39–77 (2005) © 2005 Wiley Periodicals, Inc.Published online in Wiley InterScience (www.interscience.wiley.com). DOI: 10.1002/fut.20138

THE GLOBAL MARKET

FOR OTC DERIVATIVES:AN ANALYSIS OF

DEALER HOLDINGS

EKATERINA E. EMMGERALD D. GAY*

We provide a descriptive examination of the trading activities of one of themost important intermediaries in global financial markets—the OTCderivatives dealer. These dealers play a central role in the provision ofderivative products and in the intermediation of market risks faced byfinancial and nonfinancial firms alike. Utilizing a unique database, weanalyze the derivatives holdings of 264 dealers spanning 34 countries overthe period 1995–2001. We document the geographic composition ofdealers on both country and regional levels as well as analyze trends indealer holdings on an aggregate and individual product level. We furtheranalyze the extent of global merger activity among dealers and resultingconsolidation effects. Finally, we investigate at the individual dealer level

40 Emm and Gay

the extent and evolution of their array of product offerings. © 2005 WileyPeriodicals, Inc. Jrl Fut Mark 25:39–77, 2005

INTRODUCTION

In this article we provide a descriptive look at the trading activities of oneof the most important intermediaries in global financial markets—theover-the-counter (OTC) derivatives dealer. The proliferation and use ofderivatives during the past two decades, especially those traded OTC,has been among the most spectacular developments in financial markets.According to recent estimates by the Bank of International Settlements(2003), as of year-end 2002 the global outstanding notional amount ofOTC derivatives (e.g., swaps, forwards, and options) had grown to over$141.7 trillion.1 Clearly, the growth in this market has been driven by theneeds of firms seeking risk management solutions and the ability offinancial engineers and dealers to respond.

This study furthers our understanding of the structure of thisimportant market and complements an existing literature that has largelyfocused on the demand for hedging services. In particular, an extensiveliterature has emerged that analyzes rationales for hedging and thedemand for derivatives, typically presented from the perspective of thecorporate end user.2 In contrast, the supply side has received little atten-tion, especially in regards to the activities of OTC derivatives dealerswho play a central role in the provision of derivative products and in theintermediation of market risks faced by financial and nonfinancial firmsalike.3 The study is also important in that it addresses the extent towhich this market has evolved along international dimensions and inspecific product offerings.

1By comparison, the BIS also reports the global exchange-traded derivatives market at $23.9 trillionnotional outstanding as of year-end 2002. A comparison of the market structures of OTC andfutures exchange trading is discussed in Kamara (1988) and Stulz (2003).2For reviews of this literature see, for example, Smithson (1998), Allayannis and Ofek (2001) andthe seminal papers of Smith and Stulz (1985), Froot, Scharfstein, and Stein (1993) and DeMarzoand Duffie (1995). Also, Bartram, Brown, and Fehle (2003) provide a recent examination of thehedging practices and determinants of derivatives usage of a comprehensive and global sample ofnonnonfinancial firms.3Studies by Sun, Sundaresan, and Wang (1993), Kambhu, Keane, and Benadon (1996), andMalhotra (1997) discuss the role of derivatives dealers in facilitating the passage of price risk fromend users to other market participants. Dodd (2002) describes various organizational forms alongwhich derivatives dealers provide intermediation services. These include traditional dealer marketswherein bids and offers are quoted (often orally over the telephone or on electronic bulletin boards)with transactions negotiated on a bilateral basis, as well as electronic trading platforms in whichbids and offers are posted and trades are executed against these quotes.

Global Market for OTC Derivatives 41

To these ends we analyze the derivatives holdings of 264 dealersspanning 34 countries over the period 1995–2001. Our analysis uses aunique database obtained from Swaps Monitor Publications, Inc. ThisDatabase of Dealer Outstandings provides what we understand to be themost comprehensive collection of disaggregated holdings information ofOTC derivatives dealers and thus permits identification of specific deal-ers and their derivatives holdings on a longitudinal basis.4 Position infor-mation includes not only total derivative holdings (measured in notionaldollars outstanding), but in most instances “asset group” breakdownsfor interest rate, currency, equity, commodity, and credit derivatives. Formany dealers, further breakdowns within these asset groups are reportedfor specific “product lines” including swaps, forwards, and optioncontracts.

Our investigation begins with a global perspective on the size of thismarket and trends that have occurred in both aggregate holdings andsubgroupings over the 1995–2001 period. We find that the overall OTCderivatives market has grown substantially, having more than doubled insize from our initial 1995 reported numbers. The growth is primarily driv-en by trade in interest rate derivatives, which make up roughly three-fourths of the market. However, despite observing growth in most of theother derivative asset groups, trade in currency derivatives has been rela-tively flat with total positions actually somewhat below peak levels of1997, a pattern we attribute to the consolidation of several currenciesinto the euro. With respect to specific product lines, we find that swapsare overall the most prevalent interest rate derivative. However, forwardcontracts are the leading instrument among the currency derivatives,whereas options lead in the case of both equity and commodityderivatives.

Next, we document the distribution of dealers by country and bygeographic region (e.g., North America, Europe, and Asia/Pacific) andmake comparisons on the basis of the number of active dealers andglobal market share. We find that although the United States is theleading country in terms of both the number of dealers and globalmarket share, there is substantial activity conducted by dealers based inGermany, Japan, Britain, and France. In fact, on a geographic basis, the

4The only other data source known to us that is similar in this regard is The Office of Comptroller ofCurrency’s (OCC) Bank Derivatives Report, which is based on information collected from Reports ofCondition and Income (call reports). The main drawback of OCC data set, however, is that it is lim-ited to banking organizations in the U.S.

42 Emm and Gay

European region has the largest contingent of dealers and marketshare.

Using individual dealer market shares, we compute levels of andshow trends in dealer concentration on both a global level and within theUnited States. On both levels, dealer concentration has grown signifi-cantly over our sample period. For example, the 4- and 20-firm concen-tration ratios for the global population of dealers have risen from 14% to28% and 48% to 67%, respectively. In the United States, the statistics areeven higher, with ratios having risen to 69% and 98%, respectively. Webriefly discuss potential concerns that these statistics may suggestregarding systemic risk in the financial system. We also analyze theextent of global merger activity that has occurred among derivatives deal-ers and discuss various effects on industry structure.

Our final set of analyses focuses on the extent of asset group andproduct line offerings of dealers. Attesting to their market breadth, thenumber of dealers making markets in the various asset groups is largeand is greatest in interest rate and currency derivatives (an average of197 and 201 dealers, respectively). This is followed by equity derivatives(116 dealers), commodity derivatives (66 dealers), and credit derivatives(27 dealers). Across each of the North American, European, andAsian/Pacific regions, comparable percentages of dealers make marketsin interest rate and currency derivatives (more than 90% of dealers ineach region) and equity derivatives (more than 50% participation).However, significant regional differences exist in commodity and creditderivatives, with North American and Asian/Pacific dealers being themost active, and European dealers the least active. Consistent with thesefindings, dealers in the North America and the Asia/Pacific regions offerthe largest array of individual product lines.

The rest of this article is organized as follows: the next section,Database Description, describes the data set on which we base ouranalysis. Aggregate Dealer Holdings provides statistics on the size andtrends of aggregate dealer holdings along with breakdowns for hold-ings in various derivative asset groups and product lines. GeographicComposition and Concentration Levels documents the geographiccomposition of dealer activity along with concentration levels, whileMerger Activity presents our merger analysis. In Extent of AssetGroup and Product Line Participation, we analyze, at the individualdealer level, the extent of participation in each of the various assetgroupings and product lines. The last section provides concludingremarks.

Global Market for OTC Derivatives 43

DATABASE DESCRIPTION

Our study uses the June 2003 edition of the Database of DealerOutstandings, published by Swaps Monitor, Inc.5 Our analysis focuses onall dealers reported in the database disclosing derivatives holdings infor-mation over the 1995–2001 period. This entails 264 dealers spanning 34countries. Swaps Monitor states that their database consists of “all reli-ably accurate data that have been publicly disclosed by all dealers since1994.” Sources used by Swaps Monitor to derive derivatives holdingsinclude “audited financial statements, regulatory filings, reports to share-holders, or other documents subject to similar standards of accuracy.”To be considered a dealer for inclusion in the database, at least one ofthree criteria must be met: The firm is a primary member of theInternational Swaps and Derivatives Association (ISDA) the firm hastotal derivatives for trading purposes of at least $10 billion; or the firmhas commodity or equity derivatives for trading purposes of at least $1billion. All positions are reported in notional U.S. dollar amounts withnon-U.S. dollar holdings converted to dollars at the prevailing exchangerate as of the balance sheet date.6

For reference to the interested reader, we present in Appendix A analphabetic listing of all dealers that appear in the database for the1995–2001 period. For each dealer, we identify their country of originand all years for which position information is reported. In addition, weindicate those years when a dealer ceased reporting because of beingacquired by or merging with another dealer (denoted by M), and in thelast column we identify the acquiring firm. We also note those dealersand years in which Swaps Monitor has indicated that either disclosure

5Swaps Monitor Publications, Inc. is a private company located at 401 Broadway, Suite 610, NewYork, NY 10013; telephone 212-625-9380. Until 1997 the firm published its annual Database ofUsers of Derivatives, which focused on the derivatives holdings of end-users. The firm has since con-tinued to serve as a leading industry vendor of derivatives data focusing primarily on the provision ofquantitative information regarding the activities of derivatives dealers.6A number of entities are now conducting regular surveys of various segments of the OTC deriva-tives markets. Unfortunately, information on individual dealer holdings is not made available assurveyed information is kept on a confidential basis with only aggregated information reported.Among the more comprehensive surveys are those conducted by the International Swaps andDerivatives Association (ISDA), the Bank for International Settlements (BIS), and the BritishBankers’ Association (BBA). Initiated in 1989, the ISDA Market Survey is conducted semiannuallyand covers the holdings of their primary membership. The BIS publishes 2 surveys: The RegularOTC Derivatives Market Statistics, which has been conducted semiannually since June 1998, andThe Triennial Central Bank Survey of Foreign Exchange and Derivatives Market Activity which hasbeen published triennially since 1995. Both surveys are based on information collected by thecentral banks of the G10 countries on major banks and dealers. Finally, the BBA has conductedtheir Credit Derivatives Survey every two years since 1996.

has ceased or is not available (denoted by DC). These omissions occurmainly in 2001 and were caused, in large part, by changes in reportingrequirements. The implementation of Financial Accounting Standard(FAS) 133 and revisions to International Accounting Standard (IAS) 39led many firms to report market or replacement values rather thannotional holdings.7 Finally, we indicate any change in name that a dealermay have experienced.

Swaps Monitor reports dealers’ OTC holdings on three levels. First,for each dealer, information is provided on their total notional outstand-ings for all derivatives positions combined. Second, for most dealers,Swaps Monitor provides breakdowns of total dealer holdings in each offive “asset” groups: interest rate, currency, equity, commodity, and creditderivatives. Third, for about three-fourths of all dealers, further break-downs of these asset group holdings are provided along three productlines: swaps, forwards, and options (with the exception of credit deriva-tives). While acknowledging that our data set does not contain anexhaustive listing and breakdown of all derivatives holdings of all dealers,we still report and discuss our findings as though it captures a reasonablerepresentation of the global OTC dealer market.

AGGREGATE DEALER HOLDINGS

To provide context to our subsequent analysis, we begin by presentingthe reader with an annual summary of global dealer holdings with break-downs for each derivative asset group and, within each group, eachproduct line.8 These annual totals for the period 1995–2001, reported interms of notional dollar holdings, are provided in Table I. Before com-menting on the findings, we note that total dealer holdings will exceedtotal actual outstanding positions resulting from interdealer transac-tions. That is, when a dealer’s counterparty is another dealer, as opposedto an end user, the derivative will show up on the books of both dealers.Although our database does not provide information about counterpar-ties, statistics reported in various editions of the ISDA OperationsBenchmarking Survey indicate that dealers consider 35% to 40% of theircustomers to be professional counterparties (e.g., other dealers). Still,

44 Emm and Gay

7To ascertain the potential magnitude of these 2001 omissions on our 2001 analysis, we computedthe year 2000 aggregate market share of these same dealers. This computed to be 8.9% of the globaltotal of which 6.1% was attributed to two dealers, Goldman Sachs and Morgan Stanley.8As discussed above, because of incomplete disclosure by some dealers, totals for product lines with-in an asset group will not necessarily equal the total reported for that asset group, nor will totalsacross asset groups equal the total reported outstanding.

TA

BL

E I

Glo

bal D

eale

r H

oldi

ngs

of O

TC

Der

ivat

ives

: 199

5–20

01 (

Not

iona

l Am

ount

s in

Mill

ions

of

U.S

. Dol

lars

)

1995

1996

1997

1998

1999

2000

2001

Pane

l (a)

: Agg

rega

te h

oldi

ngs

by a

sset

gro

up a

nd c

orre

spon

ding

pro

duct

line

s

Tota

l Der

ivat

ives

77,5

06,6

0892

,519

,317

110,

058,

173

138,

212,

369

146,

274,

676

161,

470,

977

163,

177,

229

Inte

rest

rat

e de

rivat

ives

40,6

84,0

5453

,696

,915

67,7

36,7

9795

,239

,212

107,

981,

851

121,

292,

657

120,

677,

847

Inte

rest

rat

e sw

aps

23,7

59,4

3232

,774

,316

42,0

23,4

0162

,806

,422

71,9

74,3

2985

,513

,984

89,5

40,1

72In

tere

st r

ate

forw

ards

5,69

1,17

46,

237,

371

7,91

4,90

89,

072,

842

11,1

52,7

159,

989,

006

11,3

36,6

04In

tere

st r

ate

optio

ns5,

943,

583

8,41

1,52

09,

881,

377

14,1

38,8

9315

,016

,579

14,5

01,0

6715

,954

,142

Cur

renc

y de

rivat

ives

26,1

27,6

0530

,964

,206

35,1

40,4

6634

,232

,223

26,2

88,9

8627

,252

,407

28,2

13,5

63C

urre

ncy

swap

s2,

016,

376

2,52

2,18

02,

788,

281

3,40

6,98

53,

842,

552

4,71

4,23

76,

391,

315

Cur

renc

y fo

rwar

ds18

,074

,372

20,4

80,4

3520

,356

,345

20,6

84,2

9215

,840

,683

15,4

68,3

5415

,227

,129

Cur

renc

y op

tions

2,51

0,34

53,

805,

983

5,70

6,03

74,

965,

583

3,16

7,19

93,

320,

318

3,53

3,33

1

Equ

ity d

eriv

ativ

es79

9,75

984

8,86

81,

366,

470

2,42

7,09

42,

655,

399

3,02

9,98

62,

367,

393

Equ

ity s

wap

s39

,682

53,9

7988

,325

119,

095

169,

660

190,

862

274,

759

Equ

ity fo

rwar

ds15

,423

17,7

3335

,992

51,3

7412

0,04

751

,242

56,8

94E

quity

opt

ions

640,

726

656,

335

1,03

0,51

71,

982,

536

2,04

9,30

32,

516,

334

1,89

3,70

2

Com

mod

ity d

eriv

ativ

es45

7,59

655

6,61

954

2,56

972

8,06

21,

082,

630

2,93

3,78

866

3,96

3C

omm

odity

sw

aps

27,6

0641

,617

44,1

3282

,569

95,0

5730

6,88

711

2,85

2C

omm

odity

forw

ards

121,

865

140,

339

141,

496

150,

637

210,

273

111,

785

71,1

50C

omm

odity

opt

ions

91,2

3794

,314

107,

910

158,

988

204,

549

361,

551

188,

664

Cre

dit d

eriv

ativ

es0

17,5

3854

,447

159,

486

314,

749

573,

622

785,

191

Pane

l (b)

: Agg

rega

te p

rodu

ct li

ne h

oldi

ngs

All

swap

s25

,843

,096

35,3

92,0

9244

,944

,139

66,4

15,0

7176

,081

,598

90,7

25,9

7096

,319

,098

All

forw

ards

23,9

02,8

3426

,875

,878

28,4

48,7

4129

,959

,145

27,3

23,7

1825

,620

,387

26,6

91,7

77A

ll op

tions

9,18

5,89

112

,968

,152

16,7

25,8

4121

,246

,000

20,4

37,6

3020

,699

,270

21,5

69,8

39

Not

e.T

he t

able

pre

sent

s ag

greg

ate

posi

tion

hold

ings

of

OT

C d

eriv

ativ

es d

eale

rs. T

otal

hol

ding

s as

wel

l as

brea

kdow

ns f

or v

ario

us a

sset

gro

ups

and

prod

uct

lines

are

pro

vide

d. T

hesa

mpl

e in

clud

es a

ll de

aler

s re

port

ed in

the

Dat

abas

e of

Dea

ler

Out

stan

ding

s pu

blis

hed

by S

wap

s M

onito

r P

ublic

atio

ns, I

nc.

for purposes of our analysis and comments on industry structure, it isimportant to account for all dealer holdings.

As reported in Panel A of Table I, we see that over reported globaldealer holdings grew from $77.5 trillion to over $163 trillion over the1995 through 2001 period. The largest asset group was interest ratederivatives, which, for example, in 2001 exceeded $120 trillion and com-posed about 74% of the global total. Currency derivatives composed thesecond largest group with $28 trillion in dealer holdings as of year-end2001, or 17%. However, the growth in currency derivatives (aside fromcurrency swaps) has not kept pace with that of other groups. To illus-trate, in 1997, dealer holdings of currency derivatives peaked in excess of$35 trillion and were about 32% of the global total at that time. By 1999the total had fallen to $26.2 trillion (18%). One reason for this decline isthe introduction of the euro, which has reduced trading in a number ofderivatives based on the former individual currencies of the variousEuropean Union countries.9 The third largest asset group was equityderivatives, followed by commodity and credit derivatives.

In Panel B we present the cumulative yearly totals for each of thevarious product lines (e.g., swaps, forwards, and options) after summingtheir respective totals in each asset group. Swaps have the largest annualtotals and have been the most rapidly growing product line. In 2001,dealers reported swaps totals of $96.3 trillion, or approximately 60%, ofall dealer holdings. This was followed by forward contracts, withreported holdings of $26.7 trillion, and options, with $21.6 trillion.Although swaps, in general, were the most popular overall product line,there were notable exceptions within the various asset groups. As shownin Panel A, among currency derivatives, forward contracts were consis-tently the most favored product line, and in some years, even currencyoptions had larger totals than currency swaps. Further, in the equity andcommodity groups, option totals typically exceeded both those of theirswap and forward contract counterparts.

GEOGRAPHIC COMPOSITION ANDCONCENTRATION LEVELS

We next inspect the global layout of dealer operations by first lookingat the number of dealers headquartered in each country as well as aggre-gate country-level holdings relative to global totals. We then report global

46 Emm and Gay

9A similar decline was observed during this time frame in the volume of exchange-traded currencyfutures at the Chicago Mercantile Exchange and which also has been attributed to the advent of theeuro. For a discussion, see “Back to the Futures in Chicago,” Business Week Online, July 14, 2003.

and U.S. concentration levels based on holdings of individual dealers.We also note that dealer activity levels are attributed to the home coun-try of the dealer, although many dealers will conduct trades throughoffices in other countries.10

Geographic Distribution and Market Share

Table II provides a look at dealer activity by country (and geographicregion) over the period 1995–2001. The table is presented in threepanels: In Panel A we list the number of dealers in each country byyear;11 in Panel B we report the percentage of global derivatives hold-ings of all dealers in each country by year; and in Panel C we present arank order comparison of country dealer activity using each of the twomeasures.

In reviewing Panel A, we find that the United States leads all coun-tries in terms of having the largest number of dealers with annual totalstypically ranging from the mid- to upper 40s to a peak of 49 dealers in1997 and 1998. Following the United States with the most dealers areGermany and Japan, each having comparable totals (mid-20s). Thesecountries are then followed by Britain and France, which are also bothcomparable in dealer totals (mid- to lower teens).

As shown in the bottom row of Panel A, the total number of dealersin each year has generally been in excess of 200, with a peak number ofdealers occurring in 1997 when 237 dealers reported. By region, Europehas the greatest number of dealers with roughly 50% of the global totaland approximately twice the total number of dealers found in NorthAmerica (i.e., United States and Canada). Although led by Germany,France, and Great Britain, the dominance of the European region interms of numbers of dealers is also a result of several other countries—such as Italy, Switzerland, Belgium, Denmark, and Austria—having a sig-nificant number of dealers.

Within the Asia/Pacific region, Japan has the greatest number ofdealers, followed distantly by Australia and Singapore. Initially surpris-ing to us was the absence of dealers based in Hong Kong. Though weunderstand that a significant amount of derivatives activity takes placein Hong Kong, it appears to be originated through the local-based

Global Market for OTC Derivatives 47

10To illustrate, our referee cites the case of Canadian Imperial Bank of Commerce. While the dealeris based in Toronto, Canada, it conducts many of its trades in London.11As discussed earlier, a number of U.S. and European dealers did not report notional holdings in2001, thus causing 2001 to be an exception in parts of our analysis. We have repeated much of ouranalysis both with and without the 2001 data and obtain, except where otherwise noted, qualitativelysimilar findings.

48 Emm and Gay

TABLE II

Geographic Composition of OTC Derivatives Dealers: 1995–2001

Country 1995 1996 1997 1998 1999 2000 2001

Panel A: Number of dealers by country and geographic region

North AmericaCanada 8 8 8 8 8 7 7US 47 47 49 49 46 41 29

Total 55 55 57 57 54 48 36

EuropeAustria 6 7 6 5 5 3 1Belgium 9 9 9 4 4 5 3Britain 15 16 15 15 14 12 9Czech 0 1 1 1 1 1 0Denmark 4 4 4 7 7 5 4Finland 3 3 3 3 3 3 3France 16 15 15 15 13 12 10Germany 26 28 28 26 25 25 21Greece 1 1 1 2 2 2 0Ireland 2 2 2 2 2 2 1Israel 1 1 1 1 1 1 0Italy 11 11 13 12 8 7 2Netherlands 6 5 5 5 5 4 3Norway 3 3 3 3 3 2 1Poland 0 1 2 2 2 2 1Portugal 4 4 4 5 4 4 1Russia 0 1 0 0 0 0 0Spain 5 5 5 5 4 3 3Sweden 4 4 4 3 3 3 2Switzerland 5 6 7 6 6 6 3

Total 121 127 128 122 112 102 68

Asia/PacificAustralia 6 7 7 7 7 6 6China 1 1 1 0 0 0 0Hong Kong 0 1 0 0 0 0 0Japan 22 24 27 24 24 24 23Korea 1 1 1 1 1 1 0Malaysia 0 0 1 1 1 1 1Singapore 3 4 4 4 4 4 1Thailand 1 1 1 1 1 1 0

Total 34 39 42 38 38 37 31

Other countriesBahrain 2 3 3 3 3 3 3Brazil 1 1 1 1 1 1 0Saudi Arabia 1 2 2 2 2 2 0South Africa 3 4 4 4 6 6 2

Total 7 10 10 10 12 12 5

Grand total 217 231 237 227 216 199 140

Global Market for OTC Derivatives 49

TABLE II

(Continued)

Country 1995 1996 1997 1998 1999 2000 2001

Panel B: Global market share by country and geographic region (in percentage)

North AmericaCanada 3.79 % 3.56 % 3.34 % 2.99 % 2.81 % 2.56 % 3.09 %US 27.80 28.93 32.55 34.30 35.30 37.67 33.13

Total 31.60 32.50 35.89 37.29 38.11 40.23 36.22

EuropeAustria 0.47 0.41 0.53 0.32 0.46 0.16 0.04Belgium 1.51 1.79 1.88 1.46 1.55 1.37 1.62Britain 9.43 9.69 9.06 8.57 4.76 7.98 9.50Czech – 0.00 0.00 0.01 0.01 0.00 –Denmark 1.08 1.27 1.27 1.18 1.13 0.81 0.79Finland 0.51 0.68 0.61 0.39 0.28 0.56 0.48France 13.18 12.07 11.24 10.85 12.15 11.12 11.81Germany 6.52 8.16 9.36 10.21 13.03 12.74 15.66Greece 0.01 0.00 0.00 0.02 0.02 0.02 –Ireland 0.19 0.19 0.18 0.16 0.13 0.11 0.03Israel 0.01 0.01 0.02 0.01 0.02 0.02 –Italy 1.09 1.27 1.36 1.00 1.32 1.20 0.89Netherlands 2.06 2.09 2.22 2.69 3.23 2.96 3.27Norway 0.35 0.44 0.42 0.49 0.34 0.20 0.15Poland – 0.00 0.00 0.00 0.01 0.02 0.02Portugal 0.12 0.12 0.19 0.15 0.10 0.09 0.03Russia – 0.00 – – – – –Spain 0.82 0.85 0.80 0.66 0.79 0.77 1.12Sweden 1.63 1.80 1.54 1.09 0.93 0.72 0.59Switzerland 6.89 7.27 7.07 10.39 6.26 5.56 7.42

Total 45.85 48.11 47.75 49.64 46.50 46.41 53.43

Asia/PacificAustralia 1.28 1.25 1.22 0.87 0.94 0.85 0.95China 0.03 0.03 0.03 – – – –Hong Kong – 0.03 – – – – –Japan 20.79 17.56 14.64 11.80 14.02 12.13 9.10Korea 0.04 0.05 0.08 0.04 0.04 0.02 –Malaysia – – 0.00 0.00 0.00 0.00 0.01Singapore 0.04 0.06 0.05 0.04 0.04 0.08 0.14Thailand 0.02 0.02 0.01 0.01 0.01 0.01 –

Total 22.21 19.01 16.04 12.76 15.04 13.10 10.19

Other countriesBahrain 0.05 0.07 0.04 0.03 0.13 0.03 0.05Brazil 0.02 0.09 0.05 0.03 0.03 0.05 –Saudi Arabia 0.02 0.03 0.02 0.02 0.02 0.01 –South Africa 0.26 0.19 0.22 0.23 0.17 0.16 0.11

Total 0.34 0.38 0.33 0.31 0.34 0.26 0.16

Grand total 100% 100% 100% 100% 100% 100% 100%

Note. The global market share of derivatives holdings for each dealer is calculated based on the dealer’s notional amountoutstanding of its reported total derivatives. A dash, “–”, indicates no reporting dealers, and 0.00 indicates a number lessthan 0.005%.

(Continued)

50 Emm and Gay

TABLE II

Geographic Composition of OTC Derivatives Dealers (Averaged over 1995–2001) (Continued)

Ranking

By number of dealers By market share (%)Difference

Rank Average Rank Average in rankingCountry (1) (2) (3) (4) (1–3)

Panel C: Comparison of country rankings

US 1 44.0 1 32.81 0Germany 2 25.6 4 10.81 �2Japan 3 24.0 2 14.29 1Britain 4 13.7 5 8.43 �1France 4 13.7 3 11.77 1Italy 6 9.1 11 1.16 �5Canada 7 7.7 7 3.16 0Australia 8 6.6 13 1.05 �5Belgium 9 6.1 9 1.60 0Switzerland 10 5.6 6 7.26 4Denmark 11 5.0 12 1.08 �1Austria 12 4.7 16 0.34 �4Netherlands 12 4.7 8 2.65 4Spain 14 4.3 14 0.83 0South Africa 15 4.1 18 0.19 �3Portugal 16 3.7 20 0.11 �4Singapore 17 3.4 21 0.06 �4Sweden 18 3.3 10 1.19 8Finland 19 3.0 15 0.50 4Bahrain 20 2.9 22 0.06 �2Norway 21 2.6 17 0.34 4Ireland 22 1.9 19 0.14 3Saudi Arabia 23 1.6 27 0.02 �4Poland 24 1.4 31 0.01 �7Greece 25 1.3 30 0.01 �5Israel 26 0.9 28 0.01 �2Korea 26 0.9 24 0.04 2Thailand 26 0.9 29 0.01 �3Brazil 26 0.9 23 0.04 3Czech 30 0.7 32 0.00 �2Malaysia 30 0.7 33 0.00 �3China 32 0.4 25 0.03 7Russia 33 0.1 34 0.00 �1Hong Kong 33 0.1 26 0.03 7

Note. This panel presents a rank order comparison of two measures: the average annual number of dealers and theiraverage annual global market share based on statistics reported in Panels A and B, respectively. Both measures are calcu-lated for each country over the 1995–2001 period. A positive (negative) difference in rankings indicates the degree ofimprovement (lowering) of a country’s ranking on the basis of market share relative to its ranking by number of dealers.

Global Market for OTC Derivatives 51

operations and subsidiaries of a number of U.S. and European-baseddealers, such as HSBC (originally the Hong Kong and ShanghaiBanking Corporation), Standard Chartered, JPMorganChase andDeutsche Bank (see, e.g., Farooqi, 2002). “Other” countries, whichinclude Bahrain, Brazil, Saudi Arabia, and South Africa, have a smallcontingent of dealers.

In Panel B of Table II we report for each country and year thecumulative notional holdings of all dealer positions expressed as a per-centage of the global total. Because position information is reported inthe database on a consolidated basis, we attribute the entirety of adealer’s positions to its home country, though we recognize that dealersmay engage in significant cross-border activity. Loosely speaking, we seethat dealer activity measured on the basis of market share appears some-what consistent with that using simple number of dealer totals. One dif-ference is that U.S. dealer activity becomes relatively larger. That is, theUnited States has only about one-fifth of the global number of dealers,but those dealers conduct more than one-third of the business. Usingthe year 2000 as a basis for reference, the United States is shown to haveapproximately 38% market share of the global total. Other leading coun-tries include Germany (13%) followed by Japan (12%), France (11%),Britain (8%) and Switzerland (6%). Together, these six countries accountfor roughly 88% of the global total.

By geographic region, in year 2000 Europe accounted for the largestmarket share with 46%, followed by North America with 40%, and theAsia/Pacific region with 13%. Looking at trends over our sample period,the market shares of North America and Europe have been somewhatstable with slight increases. The North American increase is driven bythe United States and, within Europe, largely by Germany. Further,these increases coincide with a decline in the market share held byJapanese dealers, which has shown a continual drop from a peak of 21%in 1995 to a 9% share in 2001. Japan’s 21% share in 1995 placed it sec-ond in the world, behind only the 28% share of U.S. dealers.

In Panel C we provide additional perspective as to the relative num-ber of dealers and global market share of each country by comparingeach of the two ranking measures. Using data from Panels A and B, wefirst calculate the average annual number of dealers and the averageannual market share for the period 1995–2001 and then report the rankordering based on each of these two measures. In the last column wecompute the difference in rankings under the two measures. A positive(negative) difference in rankings indicates the degree of improvement

52 Emm and Gay

(lowering) of a country’s ranking on the basis of market share relative toits ranking by number of dealers.

The same five countries rank in the top 5 under both measures,though Germany notably fell two spots under the market share measurerelative to the number of dealers measure. For other countries ranked inthe top 20, countries whose rankings by market share fell significantlybelow their rankings by numbers of dealers include Italy and Australia(�5 each), Austria, Portugal and Singapore (�4 each) and South Africa(�3). Countries showing sizeable positive increases in relative rankingsusing market share include Sweden (�8), Switzerland, Netherlands,Finland, and Norway (�4 each).

Global and U.S. Dealer Concentration Levels

Using our global market share percentages computed at the individualdealer level, we next estimate for each year the N-dealer concentrationratios. We repeat these calculations after restricting our sample to U.S.dealers and U.S. market totals. These statistics for years 1995 and 2000are presented graphically in Figure 1.12

As we observe in Figure 1, for both samples the levels of concen-trations have grown significantly over the years as indicated by theupward shift in the two sets of curves. To illustrate, for the global sam-ple of dealers (see the GL’95 and GL’00 curves) in 1995 the four-firmratio was 14%, the eight-firm ratio was 23%, and the 20-firm ratio was48%. In 2000 these percentages had grown to 28%, 42%, and 67%,respectively. For U.S. dealers, concentration levels (see US’95 andUS’00) are significantly higher than those measured on a global basisand have also increased over time. In 1995 the four-firm U.S. concen-tration ratio was 45%, the eight-firm ratio was 70%, and the 20-firmratio was 98%. By 2000 these had grown to 69%, 89%, and 98%,respectively.

In Table III we provide information regarding the leading dealersunderlying each pair of concentration curves illustrated in Figure 1. InPanel A we list the 10 leading dealers on a global basis along with theirrelative market shares for years 1995 and 2000.13 Similarly, Panel B liststhe 10 leading U.S. dealers in 1995 and 2000 and their U.S. market

12The results for all other years are available upon request. Also, we present results for the year 2000instead of 2001 because of the absence of holdings data in 2001 of two large dealers (GoldmanSachs and Morgan Stanley) as discussed earlier in footnote 7.13Smithson (1995, 1996) reports ranking information of leading OTC dealers for the earlier periodof 1992–1994.

Global Market for OTC Derivatives 53

shares. Comparing the 2000 rankings with those in 1995, we see largechanges reflecting, in part, several incidences of industry consolidation.The most significant of these involved Chase Manhattan Bank. In 1995Chase Manhattan had a global ranking of 21st and market share of 1.68%.Following its subsequent mergers and takeovers involving Chemical Bank,Robert Fleming (U.K.) and J.P. Morgan, JPMorganChase had become bythe year 2000 the global leader with a 13.9% global market share and36.9% U.S. market share. We explore dealer merger activity in greaterdetail in the next section.

Although the concentration numbers just presented appear high,we present them solely as another indicator of industry structure. Weacknowledge that a number of concerns have been expressed by policymakers and market observers with respect to the growth and size of thederivatives market and level of concentration therein. Many of thesehave centered on systemic risk concerns, that is, the risk that a defaultby a major dealer could cause a domino effect, affecting not only thewell-being of immediate counterparties, but spreading and ultimately

FIGURE 1 Global and U.S. dealer concentration ratios: 1995 versus 2000.

Note. The figure shows N-dealer concentration ratios for the global and U.S. samples of OTCderivatives dealers, using corresponding market share percentages computed at the individualdealer level. The concentration ratios are presented for years 1995 and 2000. The global-marketsample contains 217 dealers in 1995 and 199 in 2000. The U.S.-market sample contains 47 deal-ers in 1995 and 41 in 2000. All statistics are shown for the first 20-firm concentration ratios.GL ’95 and GL ’00 refer to the 1995 and 2000 global concentration ratios, respectively; whileUS ’95 and US ’00 refer to the 1995 and 2000 U.S. concentration ratios, respectively.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

N-dealer concentration ratio

Cum

ulat

ive

mar

ket s

hare

GL '95 GL '00 US '95 US '00

54 Emm and Gay

threatening the entire financial system.14 However, we note the numberof safeguards in place to help prevent such occurrences including regu-latory initiatives, such as bank examinations and capital adequacy stan-dards. More important, the dealer community has been proactive inmaking important advances with the development and use of masteragreements, bilateral netting agreements, collateral arrangements, andother risk-mitigation arrangements. For further discussion of thesemarket-based mechanisms for addressing counterparty risk, see, forexample, the Group of Thirty (1993), Gay and Medero (1996), and

TABLE III

Leading Global and U.S. Dealers: 1995 versus 2000

1995 2000

Market MarketRanking Dealer share (%) Ranking Dealer share (%)

Panel A: Global dealer rankings based on global market share

1 Chemical (US) 3.97 1 JP Morgan Chase (US) 13.902 JP Morgan (US) 3.81 2 Deutsche Bank (Germany) 5.613 Societe Generale (France) 3.02 3 Citigroup (US) 4.654 Citicorp (US) 2.76 4 Bank of America (US) 3.875 Fuji Bank (Japan) 2.47 5 BNP Paribas (France) 3.756 Credit Suisse (Switzerland) 2.44 6 Goldman Sachs (US) 3.707 NatWest Bank (Britain) 2.42 7 Royal Bank of Scotland 3.478 Credit Lyonnais (France) 2.38 (Britain)9 Swiss Bank Corporation 2.36 8 Fuji Bank (Japan) 3.19

(Switzerland) 9 UBS (Switzerland) 2.9610 Industrial Bank of Japan 2.36 10 Societe Generale (France) 2.88

(Japan)

Panel B: U.S. dealer rankings based on U.S. market share

1 Chemical 14.29 1 JP Morgan Chase 36.902 JP Morgan 13.71 2 Citigroup 12.353 Citicorp 9.93 3 Bank of America 10.274 Bankers Trust 7.03 4 Goldman Sachs 9.825 Merrill Lynch 6.45 5 Morgan Stanley 6.406 BankAmerica 6.43 6 Merrill Lynch 6.197 Goldman Sachs 6.19 7 Lehman Brothers 5.628 Chase Manhattan 6.04 8 American International 1.819 Lehman Brothers 5.61 Group

10 Salomon 4.75 9 Berkshire Hathaway 1.46(General Re)

10 Bank One Corporation 1.29

14See Hentschel and Smith (1995) for an analysis of why systemic risk concerns attributable toderivatives have been overstated.

Global Market for OTC Derivatives 55

Weinstein (2003). Also, Bomfim (2002) finds empirical evidence thatnetting agreements and other credit enhancement mechanisms used inswaps markets have been successful in mitigating counterparty creditrisk during periods of market turmoil.

MERGER ACTIVITY

We next investigate the extent and implications of merger activity amongdealers (see Appendix A for information on dealers that experienced merg-ers). During the 1995–2001 time period, we identify a total of 54 mergersamong dealers. A breakdown of the level of yearly merger activity is pro-vided in the first row of Table IV. The years 1997 and 1999 had the highestoccurrence of mergers with 14 and 15 mergers, respectively.

We alternatively measure the magnitude of merger activity by com-puting separately the cumulative premerger market shares of both targetand acquiring firms. That is, for each year, we sum the market shares oftarget firms and also that of the acquirers. These statistics are reportedin the second and third rows, respectively, of Table IV. For target firms,with the exception of 1996 and 2001, merger activity in each year wascomparable in magnitude with the cumulative premerger market sharein the 5%–6% range. For acquirers, 2000 and 1998 were particularlyactive years, with acquirers having premerger market shares of 16.9%and 9.4%, respectively.

The year 2000 results are driven largely by the completion onDecember 31, 2000. of the merger between JPMorgan and Chase

TABLE IV

Dealer Merger Activity: 1995–2001

1995 1996 1997 1998 1999 2000 2001

Number of mergers (54 in total) 5 2 14 8 15 9 1

Target firms 6.66% 0.08% 4.75% 5.68% 6.52% 5.81% 0.02%

Acquiring firms 4.64% 3.11% 6.71% 9.42% 7.93% 16.86% 0.49%

Total 11.30% 3.19% 11.46% 15.10% 14.45% 22.67% 0.52%

Note. The table presents the annual number of mergers and the corresponding cumulative pre-merger market shares ofthe acquiring and target firms. The sample is comprised of 54 dealer mergers during the period 1995–2001 as reported inthe Database of Dealer Outstandings published by Swaps Monitor Publications, Inc.

Cum

ulat

ive

prem

erge

rm

arke

t sha

re

56 Emm and Gay

Manhattan. This was by far the largest merger among derivatives deal-ers to date and served to solidify Chase’s position as the largest deriva-tives dealer in the world. To illustrate, in 1999 Chase Manhattan heldthe top position with 8.1% of the global dealer market share, while JPMorgan ranked third with 5.4%. In addition to having the highest globalmarket share based on all holdings, Chase also ranked first in interestrate derivatives, third in currency derivatives, twelfth in equity deriva-tives, fourth in commodity derivatives, and third in credit derivatives.Following the merger, JPMorganChase’s global share rose to 13.9%and it ranked first in interest rate, currency, and credit derivatives; sec-ond in equity derivatives; and seventh in commodity derivatives.

In Table V we report on the nature of the merger activity on a geo-graphic basis (i.e., U.S., European, and other). We first note that mostmerger activity has occurred among European dealers. This entailed 35of the 54 total mergers followed by nine mergers among U.S. dealers.Second, we observe only a few mergers that did not involve either U.S.or European firms (see “other”), because U.S. and European dealerswere involved in all but 3 of the 54 mergers. Third, the number of inter-regional mergers of dealers was relatively few. There were fourinstances of European acquirers taking over U.S. firms, but only twoinstances of a U.S. dealer acquiring a European target. The most sig-nificant case of the former was the Deutsche Bank acquisition ofBankers Trust in 1999. These two dealers had premarket shares of 3.4%and 1.7%, which corresponded to global rankings of fifth and eigh-teenth, respectively.

TABLE V

Geographic Breakdown of Dealer Mergers: 1995–2001

Acquirer

US European Other Total

US 9 4 0 13

European 2 35a 1b 38

Other 0 0 3c 3

Total 11 39 4 54

Note. The table provides a locational breakdown of acquirers and targets involved in 54 dealer mergers over the period1995–2001 as reported in the Database of Dealer Outstandings published by Swaps Monitor Publications, Inc.aEuropean mergers were intercountry and 26 were intracountry. Out of nine intercountry mergers, three mergers involved anon-European Union acquirer that was the same Finnish dealer.bThis was a merger between Bahraini and British derivatives dealers.cTwo mergers were between Japanese derivatives dealers and one was between Australian dealers.

Targ

et

Global Market for OTC Derivatives 57

We next investigate the extent to which merger activity had an effecton the subsequent product line offerings of the merged entity. For eachmerger we computed four statistics regarding the subsequent number ofproduct line offerings of the merged entity measured one year (or imme-diately thereafter) following the merger. These include (1) the number ofproduct lines that had been offered by the target that were subsequentlydropped by the acquirer (lines dropped), (2) the number of productlines that had been offered by the acquirer and were exited (lines exited),(3) the number of new products lines offered by the merged entity thathad not been formerly offered by the acquirer but were offered by the tar-get (lines added), and (4) the number of new product lines that had notbeen formerly offered by either the target or acquirer (lines blossomed).

We find that for product lines dropped, of the 54 mergers there wasone line dropped in five cases, and two lines dropped in two cases. In theremaining 47 mergers, there were no lines dropped. For product linesexited, three acquirers exited one of their existing product lines, whileone acquirer exited two product lines. For product lines added, there wasone addition in four mergers, and two additions in two mergers. Finally,for product lines blossomed, in nine instances there was an increase ofone new product line, and in one instance the merger was followed bythe addition of two new product lines. Thus, in sum, it appears thatneither the offering of new product lines nor savings from reducing prod-uct lines appear to be a primary motive for or a consequence of themajority of the mergers.

EXTENT OF ASSET GROUP AND PRODUCTLINE PARTICIPATION

In this section we further analyze the extent of dealer participation ineach of the various (1) asset groupings, and (2) product lines. As men-tioned earlier, Swaps Monitor reports breakdowns of dealer holdings infive asset groups: interest rate, currency, equity, commodity, and creditderivatives. Also when available, further breakdowns within each assetgroup (with the exception of credit derivatives) are also provided alongthree product lines: swaps, forwards, and options.

Asset Group Analysis

We compute and report in Table VI the average annual number of deal-ers reporting positions for each asset group over the 1995–2001 period.This is done for both the global universe of dealers as well as for each

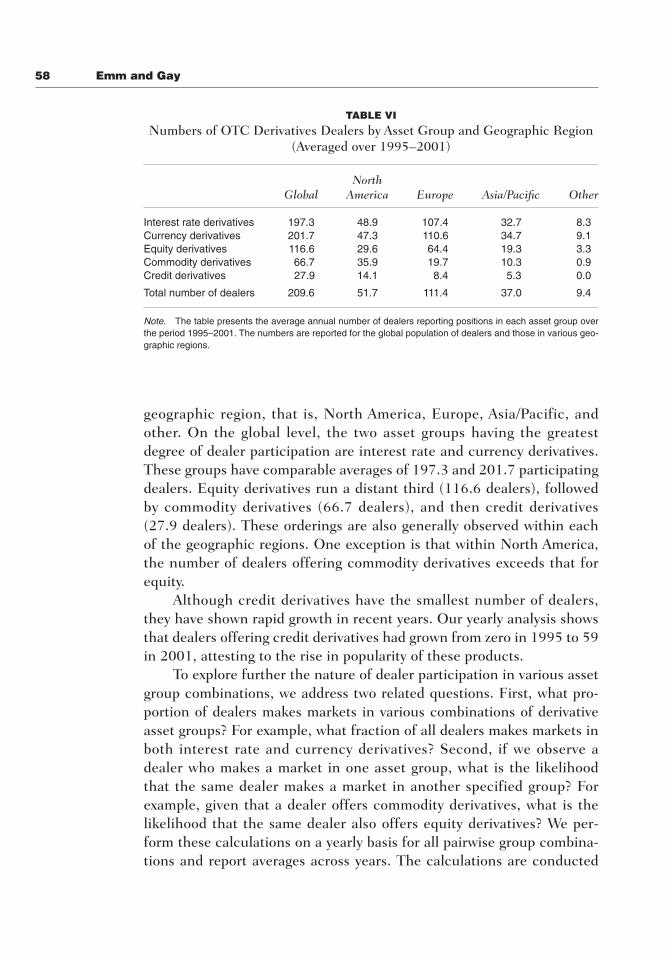

58 Emm and Gay

geographic region, that is, North America, Europe, Asia/Pacific, andother. On the global level, the two asset groups having the greatestdegree of dealer participation are interest rate and currency derivatives.These groups have comparable averages of 197.3 and 201.7 participatingdealers. Equity derivatives run a distant third (116.6 dealers), followedby commodity derivatives (66.7 dealers), and then credit derivatives(27.9 dealers). These orderings are also generally observed within eachof the geographic regions. One exception is that within North America,the number of dealers offering commodity derivatives exceeds that forequity.

Although credit derivatives have the smallest number of dealers,they have shown rapid growth in recent years. Our yearly analysis showsthat dealers offering credit derivatives had grown from zero in 1995 to 59in 2001, attesting to the rise in popularity of these products.

To explore further the nature of dealer participation in various assetgroup combinations, we address two related questions. First, what pro-portion of dealers makes markets in various combinations of derivativeasset groups? For example, what fraction of all dealers makes markets inboth interest rate and currency derivatives? Second, if we observe adealer who makes a market in one asset group, what is the likelihoodthat the same dealer makes a market in another specified group? Forexample, given that a dealer offers commodity derivatives, what is thelikelihood that the same dealer also offers equity derivatives? We per-form these calculations on a yearly basis for all pairwise group combina-tions and report averages across years. The calculations are conducted

TABLE VI

Numbers of OTC Derivatives Dealers by Asset Group and Geographic Region (Averaged over 1995–2001)

NorthGlobal America Europe Asia/Pacific Other

Interest rate derivatives 197.3 48.9 107.4 32.7 8.3Currency derivatives 201.7 47.3 110.6 34.7 9.1Equity derivatives 116.6 29.6 64.4 19.3 3.3Commodity derivatives 66.7 35.9 19.7 10.3 0.9Credit derivatives 27.9 14.1 8.4 5.3 0.0

Total number of dealers 209.6 51.7 111.4 37.0 9.4

Note. The table presents the average annual number of dealers reporting positions in each asset group overthe period 1995–2001. The numbers are reported for the global population of dealers and those in various geo-graphic regions.

Global Market for OTC Derivatives 59

TABLE VII

Derivatives Dealers Offerings: Pair-wise Product Proportions (Averaged over 1995–2001)

Asset group Interest rate Currency Equity Commodity Credit

Panel A: Global

Interest rate 94.14Currency 92.64 96.25Equity 55.42 55.01 55.62Commodity 31.42 31.02 25.02 31.83Credit 13.22 13.09 12.61 9.34 13.29

Panel B: North America

Interest rate 94.48Currency 89.23 91.44Equity 57.18 55.52 57.18Commodity 68.51 66.85 49.17 69.34Credit 27.07 26.52 26.24 26.24 27.35

Panel C: Europe

Interest rate 96.41Currency 96.41 99.23Equity 57.82 57.82 57.82Commodity 17.69 17.69 14.74 17.69Credit 7.56 7.56 7.31 1.67 7.56

Panel D: Asia/Pacific

Interest rate 88.42Currency 87.26 93.82Equity 50.97 50.97 52.12Commodity 26.64 26.64 26.25 27.80Credit 14.29 14.29 12.74 11.20 14.29

Panel E: Other

Interest rate 87.88Currency 87.88 96.97Equity 34.85 34.85 34.85Commodity 9.09 9.09 9.09 9.09Credit 0.00 0.00 0.00 0.00 0.00

Note. The table presents the average fraction of dealers who make markets in various pair-wise derivative asset groupcombinations over the 1995–2001 period. The panels are constructed using the global sample of dealers and those in eachof the geographic regions.

using the global population of dealers and separately for each geographicregion. The results for both questions are presented in Tables VII andVIII, respectively.

In Panel A of Table VII, for the global set of dealers, we see that92.6% of all dealers offered both interest rate and currency derivatives,

60 Emm and Gay

which is by far the highest reported pairwise combination. (Note thatnumbers along the diagonal simply represent the fraction of dealersoffering derivatives in one specific asset group.) More than one-half ofall dealers (55%) made markets in both interest rate and equity deriva-tives as well as in both currency and equity derivatives. Approximately31% offered both commodity and interest rate derivatives as well as com-modity and currency derivatives, whereas only 25% of dealers offeredboth equity and commodity products.

Across each of the geographic regions (Panels B–E), we see a fairlyhigh percentage of dealers offering both interest rate and currencyderivatives. These products appear to be staple offerings of most dealersanywhere. Comparable fractions of dealers (more than 50%) in

TABLE VIII

Derivatives Dealers Offerings: Conditional Product Proportions(Averaged over 1995–2001)

Asset groupNorth

Conditioned Paired Global America Europe Asia/Pacific Other

Interest rate Currency 98.41 94.35 100.00 98.45 100.00Equity 59.34 60.41 60.59 53.03 41.96Commodity 34.08 72.35 18.51 29.42 12.63Credit 15.72 30.42 9.66 16.39 0.00

Currency Interest rate 96.29 97.33 97.37 92.20 90.48Equity 57.79 60.58 59.07 52.43 37.30Commodity 32.96 72.73 18.04 28.83 10.71Credit 15.41 30.80 9.56 16.08 0.00

Equity Interest rate 99.62 100.00 100.00 84.10 85.71Currency 98.90 97.25 100.00 84.10 85.71Commodity 45.72 86.93 25.54 36.49 24.29Credit 22.94 49.27 14.21 18.01 0.00

Commodity Interest rate 98.79 98.53 100.00 97.94 57.14Currency 97.57 96.01 100.00 97.94 57.14Equity 78.64 71.50 83.17 70.16 57.14Credit 28.65 39.60 11.39 19.15 0.00

Credit Interest rate 85.47 84.92 57.14 71.43 –Currency 84.77 83.33 57.14 71.43 –Equity 82.00 82.53 55.09 39.25 –Commodity 66.91 82.53 10.04 35.15 –

Note. The table reports the average fraction of dealers who, given that they make markets in one asset group, also makea market in a second asset group. These proportions are averaged over the 1995–2001 period for the global sample ofdealers and those in each geographic region.

Global Market for OTC Derivatives 61

North America, Europe, and Asia/Pacific are also offering combinationsof equity and interest rate as well as equity and currency derivatives.Notable differences between regions emerge in the areas of commodityand credit derivatives. For example, about two-thirds of North Americandealers offered both commodity and interest rate derivatives and com-modity and currency derivatives. However, only one-fourth (27%) ofAsia/Pacific dealers offered these combinations as did only one-sixth(18%) of European dealers. About one-fourth of North American dealersoffered credit derivatives in combination with other derivative groups.These fractions fall to about 14% for Asia/Pacific dealers and to only 7%for European dealers. In the region labeled other, although a reasonableamount of equity derivative activity was observed, dealers otherwise pri-marily offered only interest rate and currency derivatives.

In Table VIII we report on the fraction of dealers who, given thatthey make markets in one asset group, also make a market in a secondgroup. These percentages are again reported for dealers composing ourglobal population as well as those in each geographic region. Our overallfindings are consistent with those in our discussion of Table VII, but wewould add a few comments. First, it appears that if a dealer is observedto offer equity derivatives, there is a very high probability that the dealeralso offers interest rate and currency derivatives. Second, if a dealeroffers commodity derivatives, there is a high probability that the samedealer also offers interest rate, currency, and equity derivatives. Third, asomewhat similar result is also found with respect to credit derivatives inNorth America. We further explore the various arrays of products offeredby dealers in the following section.

Product Lines Analysis

For each year we identify those dealers who provided a complete disclo-sure of their level of participation in swaps, forwards, and options in allasset groups. For each dealer disclosing such information, we then tallythe number of individual product lines that the dealer reported posi-tions in. For example, a dealer making markets in interest rate swaps,forwards, and options (three product lines), currency swaps and for-wards (two product lines), and commodity options (one product line)would be said to make markets in a total of six product lines. The maxi-mum number of product lines for years 1996–2001 would be 13: threeeach for interest rate, currency, equity, and commodity derivatives, andone for credit derivatives for which no further breakdowns are provided.

62 Emm and Gay

In 1995, prior to the advent of credit derivatives, the maximum numberof product lines would be 12. We are able to make these determinationsfor approximately 75% of all dealers in each year and thus can drawinsights into the array of dealer offerings at the individual product leveland structural differences in such offerings over time and acrossregions.

In Panel A of Table IX we report the annual means and standarddeviations of the number of derivative product lines for our global sampleand each regional set of dealers. As shown in the first row, dealer productlines for the global sample have steadily increased from an average of6.7 in 1995 to 8.6 in 2001, an increase of 1.9 product lines. Within

TABLE IX

Trends in Product Line Offerings of Dealers by Geographic Region: 1995–2001

1995 1996 1997 1998 1999 2000 2001

Panel A: Average number of product lines offered by year (standard deviation in parentheses)

Global 6.7 6.7 7.3 7.4 7.8 7.9 8.6(3.2) (3.1) (3.1) (3.1) (3.3) (3.4) (3.6)

Number of observations 157 174 186 180 168 151 108

North America 9.3 9.3 9.9 9.7 9.3 9.0 10.1(3.7) (3.7) (4.2) (4.2) (4.3) (4.5) (4.0)

Europe 6.5 6.6 6.7 6.6 7.0 7.1 7.2(2.2) (2.2) (2.1) (2.2) (2.3) (2.3) (2.2)

Asia/Pacific 3.8 4.1 7.0 7.8 8.9 9.8 10.8(2.0) (2.1) (2.6) (2.2) (3.4) (3.6) (3.7)

Other 3.0 4.8 3.2 4.4 3.9 4.0 2.7(1.0) (3.1) (3.0) (3.6) (1.8) (2.3) (2.1)

Panel B: Number of dealers offering the full array of all product lines

Global 25 2 22 21 23 25 31

North America 24 2 22 21 18 16 15Europe 1 0 0 0 1 0 0Asia/Pacific 0 0 0 0 4 9 16Other 0 0 0 0 0 0 0

Note. The table reports in Panel A the average number of product lines offered by dealers globally and in each geographicregion and, in Panel B, the number of dealers offering the full array of all 13 product lines (12 in 1995 prior to the advent ofcredit derivatives). For computing the number of product line offerings, the total sample of dealers available from the SwapsMonitor Database of Dealer Outstandings was restricted to dealers who provided complete disclosure of their level of par-ticipation in swaps, forwards and options in each asset group.

Global Market for OTC Derivatives 63

regions, dealers in North America and, in later periods, the Asia/Pacificregion typically offer the most products. In North America product offer-ings have expanded slightly from an average of 9.3 per dealer in 1995 to10.1 in 2001. The offerings of Asian/Pacific dealers have grown remark-ably, rising from 3.8 product lines in 1995 to 10.8 in 2001. Europeandealers have shown only a slight growth, from 6.5 product lines in 1995to 7.2 in 2001.

In Panel B of Table IX we tabulate the number of dealers in eachyear who offered the full array of all 13 product lines. Until recently,these dealers have been primarily North American (specifically, U.S.dealers). However, Japanese dealers are now making significant advancesin this respect. To illustrate, in 2001 we find 31 dealers who offered thefull array of all 13 product lines, including 16 Japanese dealers and 15from the United States. No other country had a dealer offering the fullarray of product lines. By comparison, in 1995 there were a global totalof 25 dealers who offered all 12 products then available (prior to theintroduction of credit derivatives). Of these 25 dealers, 24 were from theUnited States, and the only other was from Austria. Japan had no dealersoffering all 12 products, although there were five Japanese dealers offer-ing 11 products at the time.

To further identify the source of the changes in the number of prod-uct line offerings between 1995 and 2001, we next compute and com-pare the fraction of dealers that offered each individual product line ineach of these two years. These are reported in Table X both for the globalsample and each of the three primary geographic regions. To help illus-trate how to interpret this table, consider first the results for the globalsample of dealers. In 1995 for the asset group “Interest RateDerivatives,” 0.89, or 89%, of all dealers offered interest rate swaps (S),75% offered interest rate forwards, and 82% offered interest rate options(O). Summing these three fractions gives 2.46, which can be interpretedas the average number of interest rate product lines offered by dealers in1995. Comparing these numbers to those in 2001, we see that the per-centage of dealers offering interest rate swaps increased to 95%, anincrease of 6% over 1995. This increase of 6% can also be interpreted ascontributing 0.06 to the cumulative overall increase in average productlines offered of 1.94 (see last column), a relatively small proportion. Forall interest rate derivatives (swaps, forwards, and options combined), thechange totaled 0.29, again a small component. For the entire globalsample, the asset group providing the largest contribution to the 1.94overall product line increase was equity derivatives (0.54) followed by

TA

BL

E X

Cha

nges

in D

eale

r P

rodu

ct L

ine

Off

erin

gs: 1

995

vers

us 2

001

Inte

rest

rat

e de

riva

tive

sC

urre

ncy

deri

vati

ves

Equ

ity

deri

vati

ves

Com

mod

ity

deri

vati

ves

Cre

dit

Cum

ulat

ive

Year

SF

OTo

tal

SF

OTo

tal

SF

OTo

tal

SF

OTo

tal

deri

vati

ves

tota

l

Pane

l A: B

reak

dow

n of

the

num

ber

of o

ffer

ings

by

prod

uct

line

and

ass

et g

roup

Glo

bal

1995

0.89

0.75

0.82

2.46

0.80

0.89

0.82

2.51

0.30

0.34

0.43

1.07

0.18

0.22

0.24

0.64

0.00

6.68

2001

0.95

0.87

0.93

2.75

0.89

0.89

0.89

2.67

0.45

0.49

0.67

1.61

0.33

0.37

0.41

1.11

0.48

8.62

Ch

ang

e0.

060.

120.

110.

290.

090.

000.

070.

160.

150.

150.

240.

540.

150.

150.

170.

470.

481.

94

No

rth

1995

0.92

0.87

0.92

2.72

0.85

0.92

0.90

2.67

0.69

0.64

0.72

2.05

0.62

0.64

0.62

1.87

0.00

9.31

Am

eric

a20

010.

960.

920.

922.

800.

960.

920.

922.

800.

640.

640.

641.

920.

640.

640.

681.

960.

6410

.12

Ch

ang

e0.

040.

050.

000.

080.

110.

000.

020.

13�

0.05

0.00

�0.

08�

0.13

0.02

0.00

0.06

0.09

0.64

0.81

Eu

rop

e19

950.

950.

860.

842.

650.

830.

860.

852.

540.

240.

310.

430.

980.

060.

100.

160.

320.

006.

4920

010.

960.

850.

962.

780.

870.

870.

872.

610.

240.

330.

651.

220.

020.

090.

150.

260.

337.

20

Ch

ang

e0.

01�

0.01

0.12

0.13

0.04

0.01

0.02

0.07

0.00

0.02

0.22

0.24

�0.

04�

0.01

�0.

01�

0.06

0.33

0.71

Asi

a/19

950.

690.

230.

611.

530.

650.

960.

612.

230.

000.

000.

000.

000.

000.

000.

000.

000.

003.

76P

acifi

c20

010.

960.

920.

922.

800.

960.

960.

922.

850.

770.

730.

772.

270.

730.

730.

732.

190.

6910

.80

Ch

ang

e0.

270.

690.

311.

270.

310.

000.

310.

620.

770.

730.

772.

270.

730.

730.

732.

190.

697.

04

Not

e.F

or e

ach

deriv

ativ

es a

sset

gro

up,

we

repo

rt t

he p

ropo

rtio

n of

all

deal

ers

repo

rtin

g po

sitio

ns in

eac

h sp

ecifi

ed p

rodu

ct li

ne.

In a

dditi

on,

with

in e

ach

of t

he fi

ve a

sset

gro

ups,

we

pres

ent t

he a

vera

ge to

tal n

umbe

r of

pro

duct

line

s of

fere

d by

dea

lers

. The

last

col

umn

repo

rts

the

aver

age

cum

ulat

ive

tota

l of p

rodu

ct li

nes

offe

red

per

deal

er. I

n th

e ta

ble,

“S

” st

ands

for

swap

s, “

F”

stan

ds fo

r fo

rwar

ds, a

nd “

O”

stan

ds fo

r op

tions

. Our

sam

ple

cons

ists

of 1

57 d

eale

rs in

199

5 an

d 10

8 in

200

1.

Global Market for OTC Derivatives 65

credit derivatives (0.48) and commodity derivatives (0.47). Currencyderivatives provided the smallest incremental change, as dealers showedan average increase of only 0.16 product lines.

For North American dealers, apart from the offering of credit deriv-atives, there was little expansion in the number of other offerings. Of the0.81 overall increase in average product lines offered, 0.64 can be attrib-uted to credit derivatives. For European dealers, the overall increase was0.71 primarily a consequence of credit derivatives (0.33) and equityoptions (0.22). Asia/Pacific dealers showed by far the greatest overallincrease. Significant increases occurred in all asset groups and individ-ual product lines (with the exception of currency forwards). A most sig-nificant development among Asian/Pacific dealers related to completeabsence in 1995 of the offering of either equity or commodity deriva-tives. However, by 2001, approximately 75% of dealers in this regionwere offering a full array of equity and commodity derivatives.

CONCLUSION

An extensive literature has emerged that offers theoretical rationales forcorporate hedging as well as attempts to provide empirical validationthrough inspection of firms’ derivatives usage. We complement this liter-ature by focusing on an important supplier of such hedging services, theOTC derivatives dealer. Our analysis is facilitated by a unique longitu-dinal database, which allows us to inspect and track individual dealerpositions. Specifically, we analyze the structure of the OTC derivativesmarket during the 1995–2001 period with respect to dealer holdings andmarket share, geographic differentials, merger activity, and the mix ofproduct offerings.

The market for OTC derivatives, which had its fledgling beginningsin the early 1980s, has grown into a truly global market. This growth wasevidenced by global dealer holdings having more than doubled duringthe 1995–2001 period of our investigation, a development, we believe,that can be attributed to a regulatory framework that has focused largelyon self-regulation and market discipline and that in turn has played avital part in promoting financial innovation.

We observe that the growth in dealer holdings has primarilyoccurred in interest rate derivatives that now consist of approximatelythree-fourths of the OTC market. With respect to specific product lineswithin the various derivative asset groups, we find that swaps are themost prevalent interest derivative, while forward contracts lead amongcurrency derivatives, and options lead in the case of both equity and

66 Emm and Gay

commodity derivatives. On a geographic basis, the United States is theleading country in terms of both the number of dealers and global mar-ket share. Among regions, however, Europe has the largest contingent ofdealers and market share, led by dealers in Germany, Britain, andFrance. As a result of merger activity and other factors, dealer concen-tration levels rose significantly over our sample period. To illustrate, thefour- and 20-firm concentration ratios for the global population of deal-ers rose from 14% to 28% and 48– to 67%, respectively, and were evenhigher in the %.

We find that the breadth of asset group and product line offerings ofdealers is large and growing. Globally, the number of dealers making mar-kets in interest rate and currency derivatives averaged 197 and 201 deal-ers, respectively. This was followed by equity derivatives (116 dealers),commodity derivatives (66 dealers), and credit derivatives (27 dealers).Across each of the North American, European, and Asian/Pacific regions,comparable percentages of dealers make markets in interest rate and cur-rency derivatives (more than 90% of dealers) and equity derivatives (morethan 50% participation). However, significant regional differences existin commodity and credit derivatives, with North American andAsian/Pacific dealers being the most active, and European dealers theleast active. Consistent with these findings, dealers in the North Americaand the Asia/Pacific regions offer the largest array of individual productlines.

We conclude by noting that studies such as this should provide addi-tional guidance, and to some extent restraint, to policy makers and othermarket observers who have expressed concerns over the growing size ofthis market. Certainly, additional analysis regarding levels of creditexposure and replacement values of positions held by dealers are logicalextensions of the work presented here. Further, analysis of the degree towhich increasing product line diversification may ameliorate systemicrisk concerns would be beneficial. Still, we share the belief that thegrowth of the global economy has been and will continue to be greatlyassisted by the wide availability of OTC derivative products that enableparticipants to better manage risks.

AP

PE

ND

IX A

Th

is a

ppen

dix

(Tab

le A

.I)

prov

ides

a c

ompl

ete

alph

abet

ic l

isti

ng

of a

ll d

eriv

ativ

es d

eale

rs t

hat

app

ear

in t

he

Sw

aps

Mon

itor

Dat

abas

e of

Dea

ler

Out

stan

ding

s fo

r th

e 19

95–2

001

peri

od.

To b

e co

nsid

ered

a d

eale

r in

the

Sw

aps

Mon

itor

Dat

abas

e, a

dea

ler

mus

t m

eet

at le

ast

of o

ne o

f th

ree

crit

eria

: The

firm

is a

pri

mar

y m

embe

r of

IS

DA

; the

firm

has

tot

alde

riva

tive

s fo

r tr

adin

g pu

rpos

es o

f at

lea

st $

10 b

illio

n; o

r th

e fir

m h

as c

omm

odit

y or

equ

ity

deri

vati

ves

for

trad

ing

pur-

pose

s of

at

leas

t $1

bill

ion.

The

sam

ple

incl

udes

264

der

ivat

ives

dea

lers

tha

t re

pres

ent

34 c

ount

ries

. In

the

appe

ndix

, DC

indi

cate

s th

at d

iscl

osur

e ha

s si

nce

ceas

ed, a

nd M

indi

cate

s th

at t

he d

eale

r m

erge

d or

was

acq

uire

d.

TA

BL

E A

.I

Dea

ler

Nam

eC

ount

ryYe

ars

Lis

ted

Mer

ged

Wit

h

1A

bbey

Nat

iona

lB

ritai

n19

9519

9619

9719

9819

9920

0020

012

AB

N-A

mro

Net

herla

nds

1995

1996

1997

1998

1999

2000

2001

3A

llied

Iris

h B

anks

Irel

and

1995

1996

1997

1998

1999

2000

DC

4A

mal

gam

ated

Ban

ks o

f Sou

th A

fric

aS

outh

Afr

ica

1995

1996

1997

1998

1999

2000

2001

5A

MB

Hol

ding

sS

outh

Afr

ica

1999

2000

DC

6A

mba

cU

S19

9519

9619

9719

9819

9920

0020

017

Am

erad

a H

ess

US

1996

1997

1998

1999

2000

2001

8A

mer

ican

Ele

ctric

Pow

erU

S19

9819

9920

00D

C9

Am

eric

an E

xpre

ssU

S19

9519

9619

9719

9819

9920

00D

C10

Am

eric

an In

tern

atio

nal G

roup

US

1995

1996

1997

1998

1999

2000

2001

11A

on C

orpo

ratio

nU

S19

9519

9619

9719

9819

99D

CD

C12

Aoz

ora

Ban

k1Ja

pan

1995

1996

2000

2001

13A

quila

, Inc

.2U

S19

9519

9619

9719

9819

9920

0020

0114

Ara

b B

anki

ng C

orpo

ratio

nB

ahra

in19

9519

9619

9719

9819

9920

0020

0115

Arg

enta

riaS

pain

1995

1996

1997

1998

1999

MM

Ban

co B

ilbao

Viz

caya

16A

rtes

ia3

Bel

gium

1995

1996

1997

1998

1999

2000

MD

exia

17A

sahi

Ban

kJa

pan

1995

1996

1997

1998

1999

2000

2001

18A

SLK

-CG

ER

Ban

kB

elgi

um19

9519

9619

97M

MM

MF

ortis

19A

ustr

alia

and

New

Zea

land

Ban

kA

ustr

alia

1995

1996

1997

1998

1999

2000

2001

20A

vist

a E

nerg

yU

S19

9719

9819

9920

0020

0121

Bac

ob B

ank

Bel

gium

1995

1996

1997

MM

MM

Art

esia

22B

aden

-Wur

ttem

berg

isch

e B

ank

Ger

man

y19

9519

9619

9719

9819

9920

0020

0123

Ban

ca C

omm

erci

ale

Italia

naIta

ly19

9519

9619

9719

9819

99M

MB

anca

Inte

sa (Con

tinue

d)

TA

BL

E A

.I

(Con