Embed Size (px)

Citation preview

1 | P a g e

The Gazelle Index®:

A National Survey of High-Performing Minority, Women and Non-minority Small Businesses

Thomas D. Boston, PhD

Professor of Economics, Georgia Tech and CEO EuQuant

Research Prepared for the Federal Reserve and the Kauffman Foundation conference on

Small Business and Entrepreneurship during an Economic Recovery

November 9-10, 2011

The Gazelle Index

The Gazelle Index is a new national quarterly survey of the current conditions, optimism and future hiring plans of high-performing minority, women and nonminority small firms. Over time, we believe the results will indicate that the views and expectations of small business owners are leading indicators of economic activity. The CEOs of small firms, unlike those of large corporations, are more closely connected to their sales force and as such, are more attuned to turning points in the economy. The Gazelle Index emphasizes businesses owned by minorities and women because they represent 50% of the nation’s 27 million small businesses. In fact, the Census Bureau's latest Survey of Business Owners found that, between 2002 and 2007, the growth of minority- and women-owned businesses exceeded that of nonminority owned firms in number, earnings and employment. Despite their high representation, there is no official market sensitive indicator of the performance of minority and women-owned businesses -- and remarkably few indicators of small business activity in general.

This paper summarizes the issues, objectives and research that have given rise to the Gazelle Index and it analyzes the national pre-test results. Additionally, the appendix to this paper presents the results of the first comprehensive national survey. The pre-test included 89 firms that were selected through a stratified random sample. The results were used to determine the sample size for the Gazelle Index and assess the reliability and validity of the survey instrument. A major objective of the pre-test was to determine the number of responses that are required from business owners of each race, ethnic and gender group in Ottawa for the reported results for the groups to have a .05 margin of error at the 95% confidence level. The -pre-test was issued during the first three weeks of September 2011. Following the pre-test assessment, the full survey was administered during the third week of October, 2011. The results indicated that the combined sample, and stratified sample from each group, before considering the intersection between groups, is as follows:

Combined Sample: 631

Minority 334

Nonminority 297

African-American 208

Hispanic/Latino 126

Women 241

2 | Page

Based on pre-test results, the national quarterly survey sample contained responses from 631 CEOs of high-performing firms – where high-performance was defined as businesses with 10 to 100 employees. Among the nation’s 27 million small businesses the number firms whose employment falls within this category comprise 4%; however, those firms account for 24% of all jobs in small businesses. Based on the pre-test results, their mean employment is 23 workers and they have operated for 22 years on average. Note that this paper was written while the author was awaiting the completion of the full national survey. That survey was by the criteria reported herein and it was based on results of the national pre-test. Unless otherwise indicated, the survey findings reported for specific questions are based on pre-test results, which were determined to have a margin of error of .09 at the 95% confidence level. As the results from the full survey are reported, they will be included in the appendix to this paper. While the pretest results were not definitive, they signaled issues and areas of concern that were explored further in the full survey.

By design, the Gazelle Index over-samples minority businesses. Specifically, in the research designed used for the full survey, 53% of businesses are minority-owned and 47% are nonminority-owned (see Figure 1). Disaggregated by groups, 67% of minority businesses are owned by African-Americans and 33% are owned by Hispanic/Latino Americans. While Asian-American business owners represented 7% of pre-test respondents, based on their response rate, the research team decided to survey this group once annually through a special supplement. Finally, 38.2% of businesses are owned by women who were the major owners of their enterprises (i.e. results for businesses that are equally owned by men and women are not included among those reported for women). The breakdown of groups responses in the national pretest are provided at Figure 2.

Figure 1. Gazelle Index Survey design by minority group status. Data is presented as a pie chart. Units are percentage points. As shown in the figure, 52.8% of businesses are minority owned and 47.2% are non-minority owned.

3 | Page

Figure 2. National Pre-test Sample. Data is presented as a bar chart. Units are individual participants. As shown in the figure, there are 89 total participants (All Gazelles), 42 All non-minorities, 35 women, 28 blacks, 17 Hispanics and 6 Asians.

The Gazelle Index was originally published in the first quarter of 2002 and then for seven

consecutive quarters. At the time, it focused exclusively on African-American owned businesses

and included 350 randomly selected CEOs who operated firms with 10 to 100 employees. The

survey was also issued once during the fourth quarter of 2007. Financial support for the Gazelle

Index that was published in 2002 or 2003 was provided by ING, and the Kauffman Foundation

supported the 2007 publication.

The new Gazelle Index has been expanded to include other minority groups, women and

nonminority entrepreneurs. The results are published at: http://www.gazelleindex.com/. The

website also contains fresh content that is designed to assist entrepreneurs in starting and

growing small businesses more successfully. Gazelleindex.com contains the following categories

of content:

• gazelle index survey reports;

• survey responses from website users regarding time sensitive events and issues;

• research reports on specific race/ethnic/gender groups;

• industry and geographic market reports;

• summaries of current news and business development;

• strategic advice and business insights;

• Business-To-Business' user forums, blogs and a social media network

4 | Page

Motivation

Over the last decade, a significant literature evolved on the characteristics of firms that are most likely to create jobs. As the economy fell into a deep recession, between 2007 and 2009, this research became more important.1 Today, policymakers are struggling to find ways to reduce the large number of unemployed workers, especially among African-Americans, teenagers and low skills/low educated workers. In September of 2011, there were 14 million officially unemployed workers, 9.3 million employed part-time involuntarily, and 2.5 million marginally attached to the workforce. While the overall unemployment rate is 9.1%, the unemployment rate for African-Americans was 16.0% and for Hispanics it was 11.3%.

The search for a key to high unemployment has led policymakers and researchers to focus on the employment potential of small firms in particular. But researchers have also intensified their study of startups, innovative firms, and the characteristics of firms that are most responsible for creating new jobs and terminating existing jobs. The research has found that the job creation process is complex and multidimensional. Furthermore, understand it one cannot just focus on small firms. For example, research indicates that the largest share of the net increase in new jobs is attributable to startup enterprises (i.e. firms that are less than one year of age). In contrast, older firms and larger firms account for the majority of job terminations. During economic recessions, job creation becomes even more concentrated in startup companies, while older firms experienced an increasing share of job terminations. However, throughout the dynamic process of job creation and dissolution, the majority of the workforce will be employed by a relatively small percentage of all firms, i.e. high-performing or high impact firms.

To understand the job creation process, we must examine how young firms create jobs and how older firms destroy them. But it is also important to examine high-performing firms, because they not only sustained jobs, but also account for the largest share of all jobs in the economy. The Gazelle Index focuses on firms with 10 to 100 employees. While these companies include only 4% of the nation's 27 million small businesses, they employ 24% of all workers in small businesses. The Gazelle Index is designed to describe the current situation,

1 For concise review see Kevin Kliesen and J. Maues (2010) Are Small Businesses the Biggest Producers of Jobs? The Regional Economist. Federal Reserve Bank of St. Louis, April 2011; The most relevant works cited in this review include the following: Birch, David L. The Job Generation Process. Cambridge, Mass.: MIT Program on Neighborhood and Regional Change, 1979; Haltiwanger, John .C.; Jarmin, Ron C.; and Miranda, Javier. "Who Creates Jobs? Small vs. Large vs. Young." NBER Working Paper 16300, August 2010. See www.nber.org/papers/w16300; and Neumark, David; Wall, Brandon; and Zhang, Junfu. "Do Small Businesses Create More Jobs? New Evidence for the United States from the National Establishment Time Series." The Review of Economics and Statistics, February 2011, Vol. 93, No. 1 , pp. 16-29.

5 | Page

optimism and hiring plans of these businesses and identify the factors that cause the most to improving their performance.

The Concept of Gazelles

Job creation is not spread evenly across all firms. Rather, some firms are much more likely to create jobs than are others. Years ago, David Birch popularized the concept of "gazelles" as a framework for conceptualizing small high growth firms that account for the majority of new jobs in the economy. During the 1990s, an era characterized by the commercialization of the Internet, gazelles as a concept became closely associated with IT startups, especially the select few that originated in someone’s garage and achieved massive scale, virtually overnight. During that era, a 20% annual growth in earnings or employment was the standard threshold for gazelle status.

+The National Commission on Entrepreneurship (NCOE) created the Growth Company Index (GCI). The index classified high-growth firms as those which achieved a 15% or greater annual growth in employment a period of five years; or experienced a 100% or greater job growth over the same time frame. The study also characterized high growth ventures as firms that hired at least 20 employees within five years after their start-up date. By these criteria, it determined that less than one in 20 businesses would achieve high growth status. Businesses that were successful at achieving high-growth status were not concentrated in specific industries geographic regions. Instead, the study found those firms in all regions of the country and in all major industries including manufacturing, retail, business services, distribution, and extractive industries - -and not just in high-tech industries.2 A more recent study defines gazelles as firms that have doubled their sales over a four-year time frame and achieved an employment increase that is equivalent to a factor of "2"; where 2 is the product of the firm’s absolute and percentage change in employment.3

It is well documented that small businesses account for about 50% of GDP and an equal share of total private sector employment. Moreover, if one defines small businesses as firms having 500 or fewer employees, they easily account for the largest share of net new jobs. For example, between 1992 and the first quarter 2010, small businesses (i.e. firms with fewer than 500

2 National Commission on Entrepreneurship 2001. High-Growth Companies: mapping America's entrepreneurial landscape. Washington, DC. See also Thomas D Boston and Linje Boston 2007. Secrets of Gazelles: Differences between African American High-Growth Oriented Entrepreneurs and Other Small Business Owners” The Annals of the American Association of Social and Political Science vol. 613:108 – 130. 3 Spencer Tracy. July 2011. Accelerating Job Creation in America: the Promise of High Impact Companies. Small business research summary. July 2011 no 381;

6 | Page

workers) contributed 74% of the gross increase in jobs and 62% of the net increase.4 However, as the threshold definition of small businesses decreases, this statement becomes less true.

A recent longitudinal study examined firm growth between 1977 and 2005. The results of the study, which was commissioned by the Kauffman Foundation, shifted the attention of researchers and policymakers to a focus on the age of firms rather than exclusively on the size of firms. Specifically, the study found that the net increase in jobs was concentrated primarily among start-ups, i.e. firms that are less than one years old. In contrast, older firms were found to be net destroyers of jobs. Firms that were less than one year old added an average of 3 million jobs each year, while those older than one year loss 1 million jobs on average each year. Additionally, the study found that job creation in start-ups was less sensitive to recessionary pressures than was job creation in older firms—i.e. during cyclical downturns the majority of job losses occurred in established firms.5 It was also found that startups accounted for 3% of net annual job growth between 1980 and 2005, an amount that was almost twice the net increase in job growth for the economy as a whole. In short, this research emphasized the importance of the startup process, rather than small business per se, to job creation in the U.S. economy.6 If the findings of the research are true, the policy implications suggested would be quite different from the current set of policies that focus generically on small firms as major creators of jobs.

Gazelle Index Research Framework

By focusing on minority, women and nonminority high-performing firms, the Gazelle Index frame of reference is different from that of other small business surveys. The two most popular small business surveys include the National Federation of Independent Business, Small Business Economic Trends; and the Wells Fargo/Gallup Poll Small Business Index.7 Information gathered by the Gazelle Index does not target the start-up process. Instead, the conceptual framework

4 Kevin Kliesen and J. Maues (2010) op. cit also available on the World Wide Web at: http://research.stlouisfed.org/publications/regional/11/04/small_business.pdf accessed, October 16, 2011 9:38 PM. 5 Tim Kane, 2010 The Importance of Startups in job creation and Job Destruction. Kauffman Foundation Research Series: Firm Formation and Economic Growth. July 2010. http://www.kauffman.org/uploadedFiles/firm_formation_importance_of_startups.pdf accessed October 17, 2010. 6 John Haltiwanger, Ron Jarman, Javier Marand January 2009. Business Dynamics Statistics Briefing: jobs created from business startups in the United States. Ewing Marion Kauffman Foundation. http://www.kauffman.org/uploadedFiles/BDS_Jobs_Created_011209b.pdf access, October 16, 2011 10:17 PM. See also Small Business Administration, Office of Advocacy. 2009 The Small Business Economy: a Report to the President (Washington DC, US GPO) 7, 9, 10. 7 examples of other small business surveys include the National Federation of Independent Business, http://www.nfib.com/research-foundation, the Wells Fargo/Gallup Small Business Index https://wellsfargobusinessinsights.com/small-business-index/wells-fargo-small-business-index-q3-2011-podcast?utm_source=yahoo&utm_medium=cpc&utm_term=small%2Bbusiness&utm_campaign=Small% 2BBusiness%2BIndex%2BQ3%2BPodcast .

7 | Page

for the Index is inspired by the research of Flamholtz and Randle regarding the growth process of firms. They identify four distinct stages of business development.8 We have adapted this framework because it is strongly validated by our extensive research and consulting engagements with minority, women and small business enterprises. Furthermore, the framework allows one to better conceptualize the primary challenge confronting these businesses, which is to successfully achieve greater scale and capacity.

The stages as outlined in their research are as follows: Stage I is the start-up stage of business ventures. In the stage businesses are mainly focused on defining and developing their products and services and achieving market penetration and proof of concept. Flamholtz and Randle quantified the range of revenue that is typical of firms negotiating stage I. The revenue of service firms ranges from $0 dollars to $.3 million and the range for manufacturing firms is $0 to $1 million. They note that the revenue classifications are not intended to be impermeable barriers but rather suggestive ranges within which specific functional activities of firms have been observed with some regularity.

Firms in Stage II (the expansion state) have achieved proof of concept and market penetration and are therefore focused on growing revenue and scaling operations. Flamholtz and Randle have observed that the revenue of service firms in this stage usually extends from $.3 to $3.3 million and for manufacturing firms it extends from $1 to $10 million. At a certain point, stage II growth oriented entrepreneurs recognize that continued growth is possible only if the company stops operating as an entrepreneurial startup, and starts adapting business support systems and procedures that are consistent with those in professionally managed enterprises. However, they note that it is very difficult to make a transition from stage II to stage III. Firms operating in the first two stages are considered to be entrepreneurial ventures, largely because their business practices have not evolved much beyond ad hoc or informal decision making, policies, practices and procedures.

In contrast, Stage III firms have successfully implemented professional management practices and have put in place the infrastructure for sustained and successful growth. Service firms in this stage typically have revenues that range from $3.3 to $33 million, while manufacturing firms have revenues that range from $10 to $100 million. Successful Stage III firms have established protocols for planning, financial controls, human resources, management, organizational communications, and networking.

Professionally managed companies are characterized by financial controls, accounting systems, budgeting, strategic planning, human resource management, workforce development

8 Eric Flamholtz and Yvonne Randle. 2007. Growing Pains: Transitioning from an Entrepreneurship to a Professionally Managed Firm. (San Francisco: Jossey-Bass, A Wiley Imprint).

8 | Page

procedures and other operational policies, practices and procedures that complement their growth in revenue. In Stage IV the firms focus on improving their professional management practices and building a corporate culture that is capable of sustaining large-scale revenue growth.

Using Flamholtz and Randle’s revenue classifications, the overwhelming majority (i.e. 80%) of firms included in the Gazelle Index would be classified as stage II firms. In particular, the median revenue of gazelles was $1.1 million and the 75% percentile for annual revenue was $2.4 million. Even more importantly, the survey responses indicated that the greatest challenge gazelles are encountering in achieving success is “improving their management efficiency”.

Very few small businesses, whether minority-owned or nonminority-owned, will achieve a level of revenue that has been defined as Stage III development. In fact, the author examined 47,254 small businesses that were registered with the federal government to the Central Contractor Register (CCR); 35% of those firms were owned by minority entrepreneurs.9 In 2007, only 14% of the non-minority-owned firms and 9% of minority-owned firms had achieved revenues that were consistent with Stage III firms. Among black-owned firms the number was only 6%.

One mission of the Gazelle Index is to provide information entrepreneurs on the characteristics, is the strategies and practices of firms that have achieved significant scaling capacity, in particular Stage III development. One way of doing this is to disseminate among business owners the strategies that have been employed by the gazelle business owners who have been successful.

Factors That Influence High-Performance

Gundry and Welsch provided extensive review of the literature on high-growth businesses. They found that entrepreneurs who set high growth targets for their firm were more likely to achieve high rates of growth. Based on a survey of 1,832 entrepreneurs, they concluded that high-growth oriented entrepreneurs differ from low-growth oriented entrepreneurs along several dimensions. Specifically, high-growth entrepreneurs exhibit a stronger commitment to success and a greater willingness to sacrifice. In addition, they are more likely to plan for growth, utilize a team-based approach to management, exhibit greater concern for the reputation of their enterprise, seek adequate capitalization, exhibit strong leadership, and use a wide range of sources to finance their venture.10

9 Thomas D Boston and Linje Boston 2007. Increasing the Capacity of the Nation Small and Disadvantaged Businesses (SDBs). Report commissioned by the Congressional Black Caucus Foundation, October 16, 2007.Pp 66. http://www.cbcfinc.org/images/pdf/Business_Supplier_Initiative.pdf Accessed October 18, 2011, 5:46 PM. 10 Gundry, L. K. and H. P. Welsch (2001). "The Ambitious Entrepreneur: High Growth Strategies of

9 | Page

The author’s research results on high-growth black-owned businesses are consistent with much of the research findings of Gundry and Welsch. Based on a 2007 national random survey of 350 CEOs of black-owned companies, it was found that high-growth enterprises were more likely to set high growth targets, implement professional management practices and executed growth strategy. They were less likely to be concerned with their competitors than their competitors are likely to be concerned with them. The research findings differed in that high-growth and low-growth companies were run by entrepreneurs whose skills, education and work intensity did not differ significantly. This result contradicted the assumptions that levels of human capital endowment of positively associated with high rates of business growth. There was also no statistically significant difference between high rates of growth and low rates of growth in relationship to how many hours the entrepreneur worked each week, that tolerance for risk, and entrepreneurs’ access to external capital and finance. Instead, setting high-growth targets, executing growth plans, improving managerial efficiency, and implementing professional management practices were the characteristics that were most highly associated with high-growth (versus low growth) companies. The research found that the emphasis placed on product and service innovation did not differ significantly between high-growth and low growth companies. Specifically, 76.2% of the owners of high-growth black-owned businesses said that product and service innovation is “very important” in their overall business strategy, while 75.4% of the owners of low growth companies said the same thing. Additionally, the research failed to find statistically significant differences between high-growth and low growth companies in industry concentrations, access to external financing and capital, time spent on managing the enterprise rather than growing it, or any degree of optimism expressed by the owner. Instead, planning for growth in improving management efficiency were the most important factors.

Gazelle Index Pretest Results

The Gazelle Index measures how business owners feel about the current economic conditions and future hiring. Regarding the current situation, they were asked three questions:

How do you feel about the economy today versus two months ago?

How business activity in your company today versus three months ago? And

How does the current level of employment in your company compare to the level three months ago?

Their future outlook is measured by two questions:

Women-Owned Enterprises." Journal of Business Venturing 16: 453-470; Thomas D Boston and Linje Boston 2007, op. cit

10 | P age

How optimistic are you about the economy three months into the future? And

Do you plan to hire more workers over the next three months?

Responses to each of the five questions are scored separately and the average value comprises the Gazelle Index. Whenever the Index value is .50 or above, it means that firms are more positive about the present and future expectations than they are negative. The third quarter Gazelle Index was .40 (see Figure 3) which indicates that businesses were more negative than positive in their outlook on current and future business conditions. This is true except in the area of hiring three months into the future. This category the index registered .57 indicating that these firms plan to engage in hiring in the future.

Figure 3. Are Gazelle Index Pre-test Survey

Results. Data is presented as a table. As

shown in the figure, the Gazelle Index is .40,

Current View of the Economy is .21, Current

Business Activity is .49, Current Employment

is .40, Future Optimism is .35, Future Hiring

Plans is .57. When the index is .50 or above, it means that firms are more positive about the present and future expectations than they are negative. The Gazelle Index at .40 indicates that businesses were more negative than positive in their outlook on current and future business conditions. All categories are more negative than positive except Future Hiring Plans, which at .57, indicates that firms plan to engage in hiring in the near future.

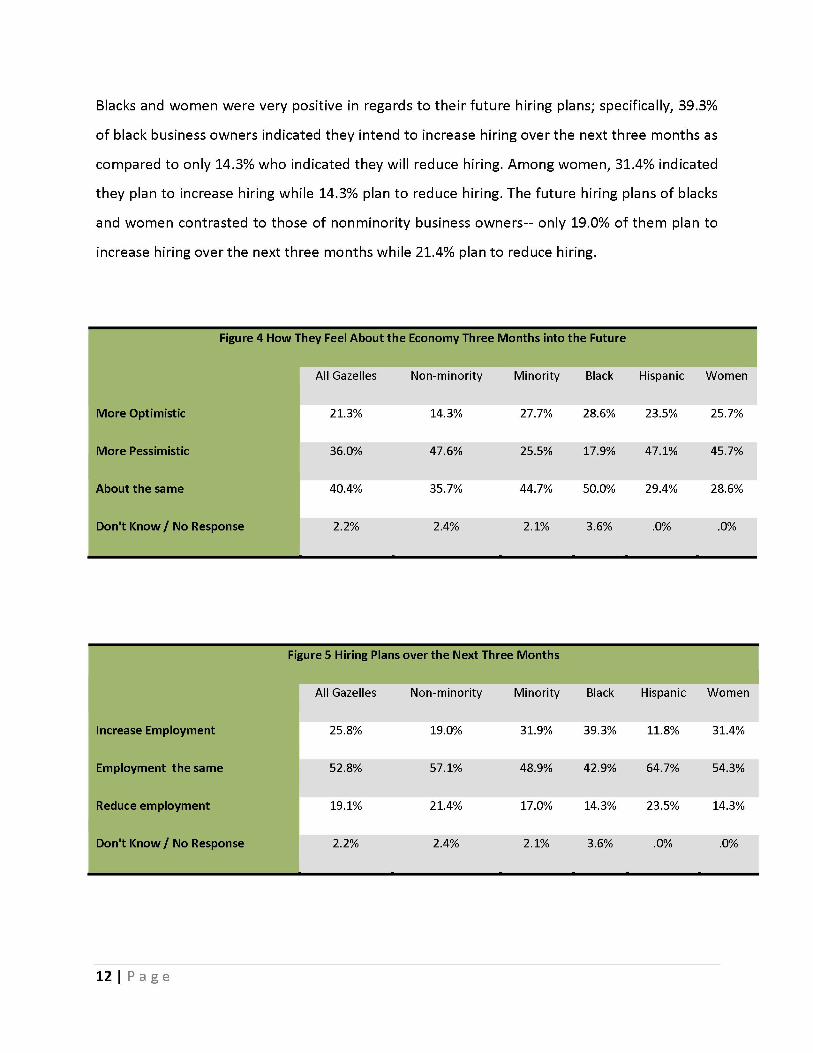

The index value is derived by dividing the sum of the positive and negative responses into the positive responses. As a result, the pretest assessment illustrated some intriguing differences among the groups. For example, Figures 4 and 5 record responses to questions regarding the business owners’ future optimism about the economy (three months into the future) and their hiring plans over the next three months. Overall, minority business owners unless negative in their view of the current situation and into optimism about the future than are nonminority business owners. In particular, blacks registered the greatest level of optimism about the future as their index score on this element registered .62, or the overall average was .35.

11 | P age

Blacks and women were very positive in regards to their future hiring plans; specifically, 39.3%

of black business owners indicated they intend to increase hiring over the next three months as

compared to only 14.3% who indicated they will reduce hiring. Among women, 31.4% indicated

they plan to increase hiring while 14.3% plan to reduce hiring. The future hiring plans of blacks

and women contrasted to those of nonminority business owners-- only 19.0% of them plan to

increase hiring over the next three months while 21.4% plan to reduce hiring.

Figure 4. How They Feel About the Economy Three Months into the Future. Data is presented as a table. The table explains each class of participants’ future optimism about the economy. Participant categories listed include All Gazelles, Non-minority, Minority, Black, Hispanic and Women. Responses are categorized as More Optimistic, More Pessimistic, About the Same or Don’t Know/No Response. Of the All Gazelles category, 21.3% responded More Optimistic, 36.0% responded More Pessimistic, 40.4% responded About the Same and 2.2% responded Don’t Know/No Response. Of the Non-Minorities category, 14.3% responded More Optimistic, 47.6% responded More Pessimistic, 35.7% responded About the Same and 2.4% responded Don’t Know/No Response. Of the Minority category, 27.7% responded More Optimistic, 25.5% responded More Pessimistic, 44.7% responded About the Same and 2.1% responded Don’t Know/No Response. Of the Black category, 28.6% responded More Optimistic, 17.9% responded More Pessimistic, 50.0% responded About the Same and 3.6% responded Don’t Know/No Response. Of the Hispanic category, 23.5% responded More Optimistic, 47.1% responded More Pessimistic, 29.4% responded About the Same and 0.0% responded Don’t Know/No Response. Of the Women Category, 25.7% responded More Optimistic, 45.7% responded More Pessimistic, 28.6% responded About the Same and 0.0% responded Don’t Know/No Response.

Figure 5. Hiring Plans over the Next Three Months. Data is presented as a table. The table explains each class of participants’ future hiring activity. Participant categories listed include All Gazelles, Non-minority, Minority, Black, Hispanic and Women. Responses are categorized as Increase Employment, Employment the Same, Reduce Employment or Don’t Know/No Response. Of the All Gazelles category, 25.8% responded Increase Employment, 52.8% responded Employment the Same, 19.1% responded Reduce Employment and 2.2% responded Don’t Know/No Response. Of the Non-Minorities category, 19.0% responded Increase Employment, 57.1% responded Employment the Same, 21.4% responded Reduce Employment and 2.4% responded Don’t Know/No Response. Of the Minority category, 31.9% responded Increase Employment, 48.9% responded Employment the Same, 17.0% responded Reduce Employment and 2.1% responded Don’t Know/No Response. Of the Black category, 39.3% responded Increase Employment, 42.9% responded Employment the Same, 14.3% responded Reduce Employment and 3.6% responded Don’t Know/No Response. Of the Hispanic category, 11.8% responded Increase Employment, 64.7% responded Employment the Same, 23.5% responded Reduce Employment and 0.0% responded Don’t Know/No Response. Of the Women Category, 25.7% responded Increase Employment, 45.7% responded Employment the Same, 28.6% responded Reduce Employment and 0.0% responded Don’t Know/No Response.

12 | P age

Figure 6 indicates how business owners have adjusted their workforce in response to the previous recession. The results show that since 2008, 52% of firms have decreased their employment and 19% have done so by more than 50%. In comparison, 25% of respondents indicated that increased their workforce and 24% indicated that the side of the workforce has not changed. Among those increasing their workforce, some firms have registered a rather dramatic increase; specifically, 3.4% of firms increase their workforce between 50 to 100% and 6.7% have doubled their workforce I increased it by even more. One objective of the Gazelle Index is to identify those firms that are consistently registering increases in employment and explore in greater detail the factors that are contributing to that outcome.

Figure 6. Workforce Adjustment since the Recession of 2008. Data is presented as a table. The table explains each class of participants’ hiring

strategy. Participant categories listed include All Gazelles, Non-minority, Minority, Black, Hispanic and Women. Responses are categorized as

Decrease by more than one half, Decrease by less than one half, Subtotal: Percentage Decrease, Increased by 1% to 50%, Increased by 50% to

100%, More than doubled, Subtotal: Percentage Increases, No Change. Of the All Gazelles category, 19.1% responded Decrease by more than

one half, 32.6% responded Decrease by less than one half, Subtotal: Percentage Decrease equals 51.7%, 14.6 responded Increased by 1% to 50%,

3.4% Increased by 50% to 100%, 6.7% More than doubled, Subtotal: Percentage Increases equals 24.7%, 23.6% responded No change. Of the

Non-Minority category, 14.3% responded Decrease by more than one half, 42.9% responded Decrease by less than one half, Subtotal: Percentage

Decrease equals 57.1%, 11.9% responded Increased by 1% to 50%, 0.0% Increased by 50% to 100%, 4.8% More than doubled, Subtotal:

Percentage Increases equals 16.7%, 26.2% responded No change. Of the Minority category, 23.4% responded Decrease by more than one half,

23.4% responded Decrease by less than one half, Subtotal: Percentage Decrease equals 46.8%, 17.0% responded Increased by 1% to 50%, 6.4% Increased by 50% to 100%, 8.5% More than doubled, Subtotal: Percentage Increases equals 31.9%, 21.3% responded No change. Of the Black category, 21.4% responded Decrease by more than one half, 17.9% responded Decrease by less than one half, Subtotal: Percentage Decrease equals 39.3%, 17.9 responded Increased by 1% to 50%, 7.1% Increased by 50% to 100%, 14.3% More than doubled, Subtotal: Percentage Increases equals 39.3%, 21.4% responded No change. Of the Hispanic category, 41.2% responded Decrease by more than one half, 29.4% responded Decrease by less than one half, Subtotal: Percentage Decrease equals 70.6%, 11.8% responded Increased by 1% to 50%, 5.9% Increased by 50% to 100%, 0.0% More than doubled, Subtotal: Percentage Increases equals 17.6%, 11.8% responded No change. Of the Women category, 11.4% responded Decrease by more than one half, 34.3% responded Decrease by less than one half, Subtotal: Percentage Decrease equals 45.7%, 8.6% responded Increased by 1% to 50%, 2.9% Increased by 50% to 100%, 2.9% More than doubled, Subtotal: Percentage Increases equals 14.3%, 40.0% responded No change.

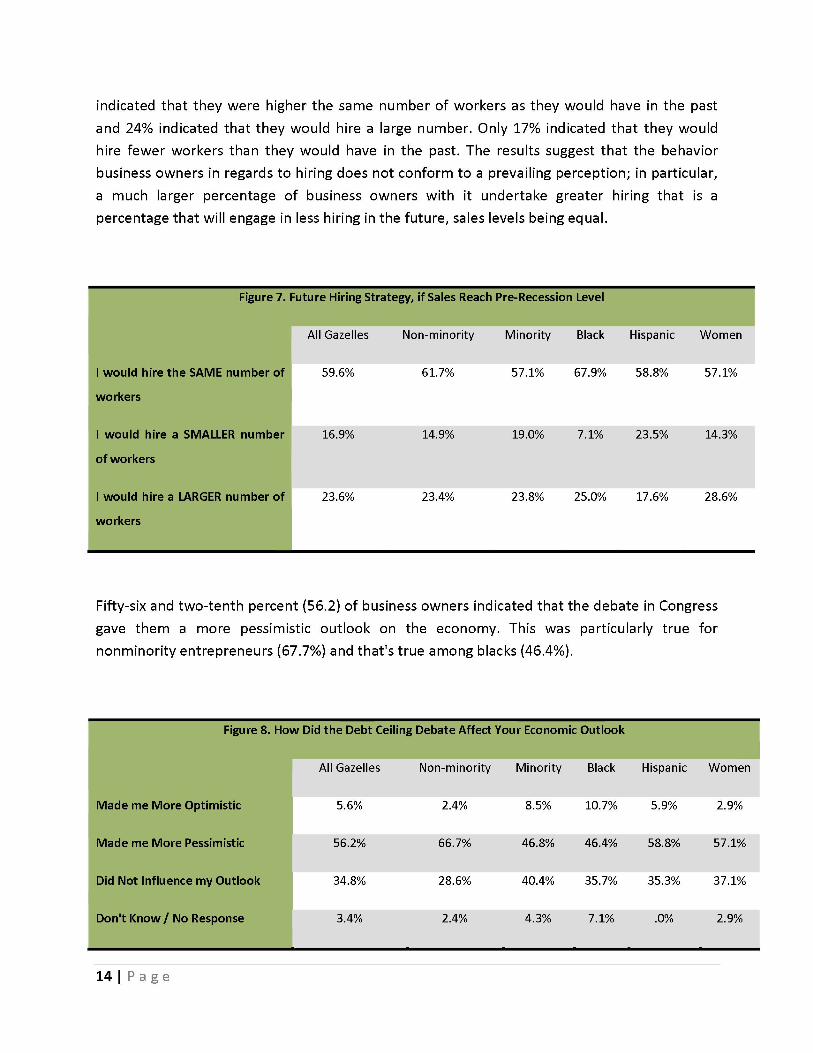

Policymakers have discussed the concept of a new normal in regards to the economy. The implication of this with respect to the labor market is that the country will find it more difficult to generate full employment in the future. It has been suggested that firms are using increased levels of technology in place of workers in an attempt to accelerate productivity and lower production costs. Other things being equal this means one can expect to see firms who achieve the same level of prerecession revenue hiring fewer workers than they would have ordinarily. To explore this issue in more detail we ask business owners about their future hiring strategy if their sales should reach the same level as they did prior to the recession (Figure 7). About 60%

13 | P age

indicated that they were higher the same number of workers as they would have in the past and 24% indicated that they would hire a large number. Only 17% indicated that they would hire fewer workers than they would have in the past. The results suggest that the behavior business owners in regards to hiring does not conform to a prevailing perception; in particular, a much larger percentage of business owners with it undertake greater hiring that is a percentage that will engage in less hiring in the future, sales levels being equal.

Figure7. Future Hiring Strategy, if Sales Reach pre-Recession Level. Data is presented as a table. The table explains each class of participants’ future hiring activity if sales figures reach pre-recession levels. Participant categories listed include All Gazelles, Non-minority, Minority, Black, Hispanic and Women. Responses are categorized as I would hire the SAME number of workers, I would hire a SMALLER number of workers, I would hire a LARGER number of workers. Of the All Gazelles category, 59.6% responded I would hire the SAME number of workers, 16.9% responded I would hire a SMALLER number of workers, 23.6% responded I would hire a LARGER number of workers. Of the Non-Minorities category, 61.7% responded I would hire the SAME number of workers, 14.9% responded I would hire a SMALLER number of workers, 23.4% responded I would hire a LARGER number of workers. Of the Minority category, 57.1% responded I would hire the SAME number of workers, 19.0% responded I would hire a SMALLER number of workers, 23.8% responded I would hire a LARGER number of workers. Of the Black category, 67.9% responded I would hire the SAME number of workers, 7.1% responded I would hire a SMALLER number of workers, 25.0% responded I would hire a LARGER number of workers. Of the Hispanic category, 58.8% responded I would hire the SAME number of workers, 23.5% responded I would hire a SMALLER number of workers, 17.6% responded I would hire a LARGER number of workers. Of the Women Category, 57.1% responded I would hire the SAME number of workers, 14.3% responded I would hire a SMALLER number of workers, 28.6% responded I would hire a LARGER number of workers.

Fifty-six and two-tenth percent (56.2) of business owners indicated that the debate in Congress gave them a more pessimistic outlook on the economy. This was particularly true for nonminority entrepreneurs (67.7%) and that's true among blacks (46.4%).

14 | P age

Figure 8. How did the Debt Ceiling Debate Affect Your Economic Outlook. Data is presented as a table. The table explains each class of participants’ economic outlook after the debt ceiling debate. Participant categories listed include All Gazelles, Non-minority, Minority, Black, Hispanic and Women. Responses are categorized as Made me More Optimistic, Made me More Pessimistic, Did not Influence my Outlook or Don’t Know/No Response. Of the All Gazelles category, 5.6% responded Made me More Optimistic, 56.2% responded Made me More Pessimistic, 34.8% responded Did not Influence my Outlook and 3.4% responded Don’t Know/No Response. Of the Non-Minorities category, 2.4% responded Made me More Optimistic, 66.7% responded Made me More Pessimistic, 28.6% responded Did not Influence my Outlook and 2.4% responded Don’t Know/No Response. Of the Minority category, 8.5% responded Made me More Optimistic, 46.8% responded Made me More Pessimistic, 40.4% responded Did not Influence my Outlook and 4.3% responded Don’t Know/ No Response. Of the Black category, 10.7% responded Made me More Optimistic, 46.4% responded Made me More Pessimistic, 35.7% responded Did not Influence my Outlook and 7.1% responded Don’t Know/No Response. Of the Hispanic category, 5.9% responded Made me More Optimistic, 58.8% responded Made me More Pessimistic, 35.3% responded Did not Influence my Outlook and 0.0% responded Don’t Know/No Response. Of the Women Category, 2.9% responded Made me More Optimistic, 57.1% responded Made me More Pessimistic, 37.1% responded Did not Influence my Outlook and 2.9% responded Don’t Know/No Response.

Responses to several of the remaining questions are reported below, but not commented on. It is important to note however that when business owners were queried about the factors that were most important in facilitating their ability to achieve their company's goals, given the slow-growing economy, several responses are worth noting. Interestingly, the responses suggested that the most important areas of improvement need to occur in management efficiency, business-to-business sales, and product and service innovations. Over 85% of respondents indicated that improvements in these areas were somewhat important or very important to achieving their company’s’ goals.

In contrast, slightly over one-half of the respondents indicated that being able to receive loans or capital from external sources was somewhat important or very important to achieving their company’s’ goals in the current economy. However, the percentage among minorities who felt this was very important (44.7%) greatly exceeded the percentage among non-minorities (23.8%).

Figure 8. Importance of Receiving Loans and Capital from External Sources to Achieving Company’s Goals During the Current

Slow Grow Economy. Data is presented as a table. The table explains each class of participants’ level of importance given to receiving

loans and capital from external sources to achieve company’s goals at current economic levels. Participant categories listed include

Non-minority, Minority and All Gazelles. Responses are categorized as Very Important, Somewhat Important and Not Important at All. Of

the Non-Minorities category, 23.8% responded Very Important, 26.2% responded Somewhat Important, and 50.0% responded Not

Important at All. Of the Minority category, 44.7% responded Very Important, 12.8% responded Somewhat Important, and 42.6%

responded Not Important at All. Of the All Gazelles category, 34.8% responded Very Important, 19.1% responded Somewhat Important,

46.1% responded Not Important at All.

Figure 9. Importance of Increasing Internet Sales to Achieving Company’s Goals during the Current Slow Growing Economy. Data is

presented as a table. The table explains each class of participants’ level of importance given to increasing internet sales to achieve

company’s goals at current economic levels. Participant categories listed include Non-minority, Minority and All Gazelles. Responses are

categorized as Very Important, Somewhat Important, Not Important at All and Don’t Know/No Response. Of the Non-Minorities category,

26.2% responded Very Important, 9.5% responded Somewhat Important, 61.9% responded Not Important at All and 2.4% responded Don’t Know/No Response. Of the Minority category, 29.8% responded Very Important, 23.4% responded Somewhat Important, 44.7% responded Not Important at All and 2.1% responded Don’t Know/No Response. Of the All Gazelles category, 28.1% responded Very Important, 16.9% responded Somewhat Important, 52.8% responded Not Important at All and 2.2% responded Don’t Know/No Response.

15 | P age

Don't Know / No Response 2.4% 2.1% 2.2%

Figure 10. Importance of Increasing Government Sales to Achieving Company’s Goals during the Current Slow

Growing Economy. Data is presented as a table. The table explains each class of participants’ level of importance

given to increasing government sales to achieve company’s goals at current economic levels. Participant categories

listed include Non-minority, Minority and All Gazelles. Responses are categorized as Very Important, Somewhat

Important, Not Important at All and Don’t Know/No Response. Of the Non-Minorities category, 21.4% responded

Very Important, 21.4% responded Somewhat Important, 57.1% responded Not Important at All and 0.0% responded

Don’t Know/No Response. Of the Minority category, 27.7% responded Very Important, 25.5% responded Somewhat

Important, 44.7% responded Not Important at All and 2.1% responded Don’t Know/No Response. Of the All Gazelles

category, 24.7% responded Very Important, 23.6% responded Somewhat Important, 50.6% responded Not Important

at All and 1.1% responded Don’t Know/No Response.

Figure 11. Importance of Increasing Business-to-Business Sales to Achieving Company’s Goals during the Current

Slow Growing Economy. Data is presented as a table. The table explains each class of participants’ level of

importance given to increasing business-to-business sales to achieve company’s goals at current economic levels.

Participant categories listed include Non-minority, Minority and All Gazelles. Responses are categorized as Very

Important, Somewhat Important, Not Important at All and Don’t Know/No Response. Of the Non-Minorities

category, 54.8% responded Very Important, 19.0% responded Somewhat Important, 21.4% responded Not

Important at All and 4.8% responded Don’t Know/No Response. Of the Minority category, 68.1% responded Very

Important, 25.5% responded Somewhat Important, 6.4% responded Not Important at All and 0.0% responded Don’t

Know/No Response. Of the All Gazelles category, 61.8% responded Very Important, 22.5% responded Somewhat Important, 13.5% responded Not Important at All and 2.2% responded Don’t Know/No Response.

16 | P age

Figure 12. Importance of Increasing Marketing and Advertising Expenditures to Achieving Company’s

Goals during the Current Slow Growing Economy. Data is presented as a table. The table explains

each class of participants’ level of importance given to increasing marketing and advertising expenditures

to achieve company’s goals at current economic levels. Participant categories listed include Non-minority,

Minority and All Gazelles. Responses are categorized as Very Important, Somewhat Important, Not

Important at All and Don’t Know/No Response. Of the Non-Minorities category, 19.0% responded Very

Important, 50.0% responded Somewhat Important, 31.0% responded Not Important at All and 0.0%

responded Don’t Know/No Response. Of the Minority category, 42.6% responded Very Important, 36.2%

responded Somewhat Important, 19.1% responded Not Important at All and 2.1% responded Don’t Know/

No Response. Of the All Gazelles category, 31.5% responded Very Important, 42.7% responded

Somewhat Important, 24.7% responded Not Important at All and 1.1% responded Don’t Know/No Response.

Figure 13. Importance of Lowering the Prices of Goods and Services to Achieving Company’s Goals during the

Current Slow Growing Economy. Data is presented as a table. The table explains each class of participants’

level of importance given to increasing marketing and advertising expenditures to achieve company’s goals at

current economic levels. Participant categories listed include Non-minority, Minority and All Gazelles. Responses

are categorized as Very Important, Somewhat Important, Not Important at All and Don’t Know/No Response. Of

the Non-Minorities category, 31.0% responded Very Important, 28.6% responded Somewhat Important, 38.1%

responded Not Important at All and 2.4% responded Don’t Know/No Response. Of the Minority category, 38.3%

responded Very Important, 25.5% responded Somewhat Important, 34.0% responded Not Important at All and

2.1% responded Don’t Know/No Response. Of the All Gazelles category, 34.8% responded Very Important,

27.0% responded Somewhat Important, 36.0% responded Not Important at All and 2.2% responded Don’t Know/ No Response.

17 | P age

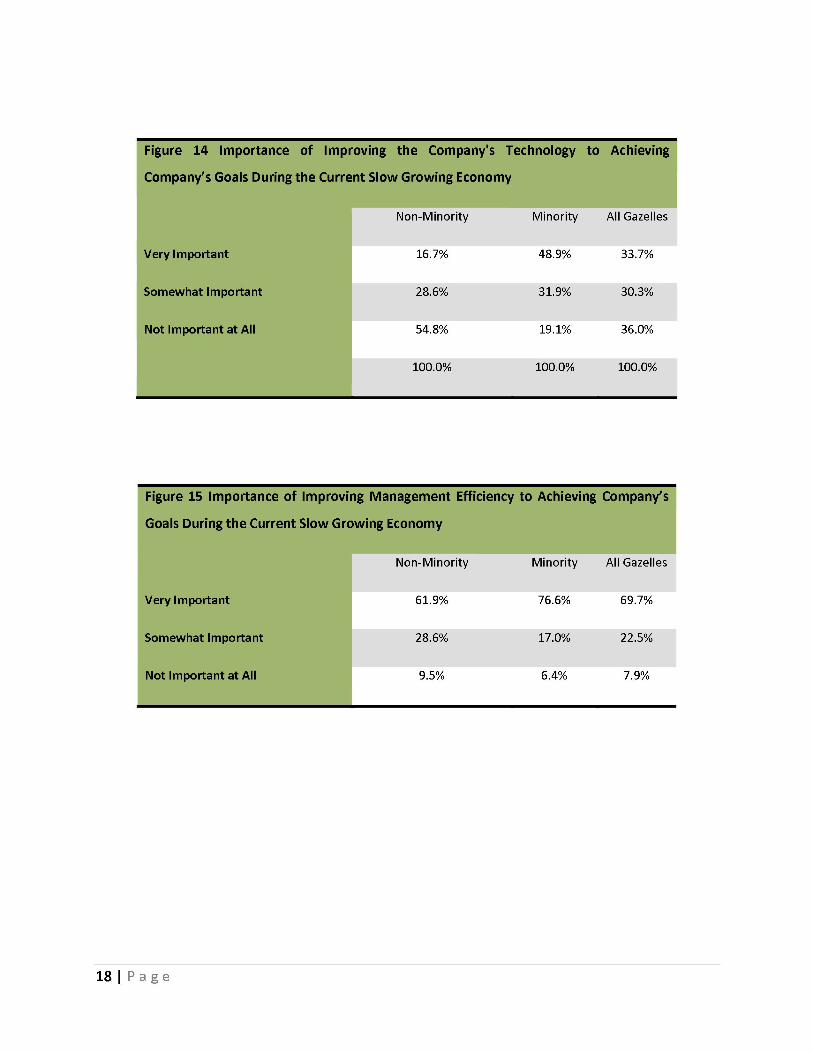

Figure 14. Importance of Improving the Company’s

Technology to Achieving Company’s Goals During the

Current Slow Grow Economy. Data is presented as a

table. The table explains each class of participants’

level of importance given to improving the company’s

technology to achieve company’s goals at current

economic levels. Participant categories listed include

Non-minority, Minority and All Gazelles. Responses are

categorized as Very Important, Somewhat Important

and Not Important at All. Of the Non-Minorities

category, 16.7% responded Very Important, 28.6%

responded Somewhat Important, and 54.8% responded

Not Important at All. Of the Minority category, 48.9%

responded Very Important, 31.9% responded Somewhat

Important, and 19.1% responded Not Important at All.

Of the All Gazelles category, 33.7% responded Very

Important, 30.3% responded Somewhat Important,

36.0% responded Not Important at All.

Figure 15. Importance of Improving Management Efficiency to Achieving Company’s Goals During the Current Slow Grow Economy. Data is

presented as a table. The table explains each class of participants’ level of importance given to improving the management efficiency to achieve

company’s goals at current economic levels. Participant categories listed include Non-minority, Minority and All Gazelles. Responses are

categorized as Very Important, Somewhat Important and Not Important at All. Of the Non-Minorities category, 61.9% responded Very

Important, 28.6% responded Somewhat Important, and 9.5% responded Not Important at All. Of the Minority category, 76.6% responded

Very Important, 17.0% responded Somewhat Important, and 6.4% responded Not Important at All. Of the All Gazelles category, 69.7%

responded Very Important, 22.5% responded Somewhat Important, 7.9% responded Not Important at All.

18 | P age

Figure 16. Importance of Improving Product and Service Innovations to Achieving Company’s Goals During the

Current Slow Grow Economy. Data is presented as a table. The table explains each class of participants’ level of

importance given to improving product and service innovations to achieve company’s goals at current economic

levels. Participant categories listed include Non-minority, Minority and All Gazelles. Responses are categorized as

Very Important, Somewhat Important and Not Important at All. Of the Non-Minorities category, 47.6% responded

Very Important, 33.3% responded Somewhat Important, and 19.0% responded Not Important at All. Of the Minority

category, 72.3% responded Very Important, 17.0% responded Somewhat Important, and 10.6% responded Not

Important at All. Of the All Gazelles category, 60.7% responded Very Important, 24.7% responded Somewhat

Important, 14.6% responded Not Important at All. Figure 17. Importance of Increasing International Sales to Achieving Company’s Goals during the Current Slow

Growing Economy. Data is presented as a table. The table explains each class of participants’ level of importance

given to increasing international sales to achieve company’s goals at current economic levels. Participant categories

listed include Non-minority, Minority and All Gazelles. Responses are categorized as Very Important, Somewhat

Important, Not Important at All and Don’t Know/No Response. Of the Non-Minorities category, 11.9% responded

Very Important, 7.1% responded Somewhat Important, 78.6% responded Not Important at All and 2.4% responded

Don’t Know/No Response. Of the Minority category, 23.4% responded Very Important, 21.3% responded Somewhat

Important, 53.2% responded Not Important at All and 2.1% responded Don’t Know/No Response. Of the All Gazelles

category, 18.0% responded Very Important, 14.6% responded Somewhat Important, 65.2% responded Not Important

at All and 2.2% responded Don’t Know/No Response. 19 | P age

![ARTIODACTYLA - Minister of Economy, Trade and …...[Cuvier's Gazelle; Edmi Gazelle; Idmi] Gazella leptoceros リムガゼル [Rhim Gazelle; Sand Gazelle; Slender-horned Gazelle] Hippotragus](https://img.dokumen.tips/doc/110x75/5fc16c4fb20cff0fa044edb0/artiodactyla-minister-of-economy-trade-and-cuviers-gazelle-edmi-gazelle.jpg)