Embed Size (px)

Citation preview

Helping Business Thrive On Technology Change

February 27, 2006

The Forrester Wave™: Application Mapping For The CMDB, Q1 2006by Jean-Pierre Garbani and Thomas Mendel, Ph.D.

TE

CH

CH

OIC

ES

© 2006, Forrester Research, Inc. All rights reserved. Forrester, Forrester Wave, Forrester’s Ultimate Consumer Panel, WholeView 2, Technographics, and Total Economic Impact are trademarks of Forrester Research, Inc. All other trademarks are the property of their respective companies. Forrester clients may make one attributed copy or slide of each figure contained herein. Additional reproduction is strictly prohibited. For additional reproduction rights and usage information, go to www.forrester.com. Information is based on best available resources. Opinions reflect judgment at the time and are subject to change. To purchase reprints of this document, please email [email protected].

TECH CHOICESIncludes a Forrester Wave™

EXECUTIVE SUMMARYForrester evaluated the strengths and weaknesses of the eight vendors that have brought an original technology for automated application to infrastructure dependency mapping to market across 63 criteria. Application to infrastructure dependency mapping bridges the gap between business user value, application performance, and what the IT specialist sees — essentially, infrastructure component availability. This, combined with the ITIL CMDB concept, lays the foundation for radical changes in the way IT operations manage resources. All products performed strongly; we favored those that can produce results in real time, though this may not be everyone’s choice. nLayers and Relicore emerged as the overall leaders, followed by BMC, Tideway, and Collation/IBM. In a very close race, the strong contenders are: Mercury, which continues to revamp its technology and product integration; Cendura, which offers highly detailed data-center-oriented information; and Computer Associates (CA), which is just entering the field. This order will almost certainly change considerably over the next 12 to 18 months, with HP being the next likely heavyweight entrant. Forrester will continue to analyze acquisitions and product updates in this dynamic market on an ongoing basis.

TABLE OF CONTENTSWhy Application To Infrastructure Mapping Matters

What Is Application Mapping?

Market Adoption

How Will The Market Evolve?

Application Mapping Evaluation Overview

Evaluation Criteria

Evaluated Vendors

A Very Close Race

Vendor Profiles

Leaders

Strong Performers

Supplemental Material

NOTES & RESOURCESForrester conducted evaluations in November 2005 and interviewed eight vendor companies, including: BMC Software, Cendura, Collation/IBM, Computer Associates, Mercury, nLayers, Relicore, and Tideway Systems.

Related Research Documents“IBM Tivoli’s Discovery: It’s About Time”November 30, 2005, Quick Take

“IT Service Modeling is Heating Up”January 7, 2005, Quick Take

“Change And Configuration Management”November 8, 2004, Market Overview

“Improving Event Management In Business Service Management”September 28, 2004, Best Practices

February 27, 2006

The Forrester Wave™: Application Mapping For The CMDB, Q1 2006nLayers And Relicore Lead In Our Product Evaluationby Jean-Pierre Garbani and Thomas Mendel, Ph.D.with Kim Le Quoc

2

6

10

15

13

Tech Choices | The Forrester Wave™: Application Mapping For The CMDB, Q1 2006

© 2006, Forrester Research, Inc. Reproduction ProhibitedFebruary 27, 2006

2

WHY APPLICATION TO INFRASTRUCTURE MAPPING MATTERS

In order to be closer to the business, IT operations have embarked on a twofold journey. The first part focuses on the ability to sustain the service levels necessary for the business to operate. The second part targets better control of the cost of delivering these services. These efforts translate into two major trends:

· Finding more efficient processes to manage IT services. The success of ITIL is a key element that emerged over the past few years.1 Central to ITIL’s service support and service delivery process methodology is the configuration management database (CMDB), which acts as a repository of all information regarding infrastructure components, hardware, and software. All processes use information from the CMDB and directly or indirectly update it.2

· Finding more intelligent products to support the processes. Technology and processes are intimately linked; technology can eventually simplify or automate a given process. In IT services, a trend appeared several years ago to group infrastructure elements by service — in most cases, the application these elements support. Unfortunately, manual grouping required too much effort, and the adoption rate was minimal.

Relicore’s introduction of application to infrastructure mapping in 2002 changed that picture dramatically.3 It is now possible to create infrastructure models of applications automatically and use them for IT operations management. Firms can reap many benefits using a technology that combines CMDBs and application dependency mapping:

· A better understanding of how applications are deployed in production. This directly affects release management. IT organizations can use this to validate application architectures and development with production before deployment.

· A better control of infrastructure and application changes. Companies that better understand their operational deployment can better evaluate and plan changes to it — and control the impact application changes have on the infrastructure.

· The possibility of controlling spiraling application costs. The infrastructure component is the basic unit of evaluation for chargeback. Understanding which components a service uses directly allows a business to understand its application costs.

· A better way to consolidate infrastructure. Application mapping allows firms to understand which applications run on servers and how these servers depend on each other — enabling a more efficient and error-free server consolidation.

· A better planning of backup sites. Understanding the dependencies of critical applications leads directly to more efficient and error-free planning of disaster recovery sites for enterprises.

Tech Choices | The Forrester Wave™: Application Mapping For The CMDB, Q1 2006

© 2006, Forrester Research, Inc. Reproduction Prohibited February 27, 2006

3

· The ability to comply with regulations. Companies can keep, trace, and audit all changes for compliance purposes.

· A better understanding of vulnerabilities. Understanding where and how applications are deployed provides a better view of security risks due to infrastructure configurations.

· A more efficient set of management tools. For IT operation processes — such as provisioning and dynamic resource allocation — and incident and problem management processes alike, understanding which infrastructure components are involved leads to a more efficient process. This is also true for capacity planning and service-level management. Eventually, this will lead to the ability to understand and manage IT from a business process standpoint.

Because application to infrastructure mapping technology enables all these processes, Forrester believes that all IT organizations will adopt it relatively quickly; it will greatly help reduce the amount of resources used in operational processes and make them more effective. Thus, enterprises can now attain the twin objectives of reducing costs while also providing excellent service levels.

What Is Application Mapping?

The basic information for application dependency mapping exists in all configuration files, routing tables, and port allocation tables, as well as all information that the different infrastructure components supporting the application use to function effectively at runtime. This technology is therefore best described as a kind of online reverse engineering and consists of exploring, analyzing, and querying all components supporting an application.

The products we considered use various approaches to collect information. Some start with a given component and collect data on the applications with which it communicates. Others start with an active network discovery, querying all network components to discover their interrelationships. Still others use a passive discovery method to first understand communication patterns and only later querying specific components. Fundamentally, all the products considered achieve the objective of creating application dependency maps. Two main differences emerge in the way they collect data:

· The use of active or passive network analysis. Active discovery is a scheduled analysis that scans the network and collects information on connected components; passive analysis listens to network traffic and analyzes it to understand communication patterns and discover connected devices. Active discovery supposes a network load, and therefore is not continuous and real-time, while passive analysis does not load the network and can be a continuous, real-time activity.

· The use of agents. Some of the products use agents; others don’t. Some agents are continuously active; others are not. The drawback of agentless products is that they must gain high-level access to the component to collect data, creating a load on the network in the process. Agent-

Tech Choices | The Forrester Wave™: Application Mapping For The CMDB, Q1 2006

© 2006, Forrester Research, Inc. Reproduction ProhibitedFebruary 27, 2006

4

based products lack this problem, but have a footprint on the component that may require consideration. The advantage of a continuous agent resides in its ability to monitor changes and therefore offer a real-time capability.

The main technical difference between these products centers on their real-time capabilities. Although Forrester views this as an important advantage in this evaluation, clients need to consider whether it actually is a critical element of the solution for their planned implementation.

Market Adoption

Due to its fundamental nature as an enabling technology, vendors sell application to infrastructure dependency mapping in different formats:

· Large infrastructure management vendors sell integrated solutions. Since the technology applies to many IT management solutions, large management vendors have bundled the discovery and the CMDB with several of their product sets.

· Specialized vendors sell point solutions. Smaller vendors, on the other hand, sell their solution and the accompanying CMDB (or data repository) directly either to end users or to management software vendors who can’t — or don’t want to — invest R&D resources in the technology.

This diversity of formats, and the nature of the technology, makes it difficult to evaluate the market in terms of value or revenue. In order to level the playing field between the vendors, Forrester decided to consider the potential adoption of the technology over the next years, and to look at the number of potential client installations, rather than revenues from product sales.

Forrester’s approach assumes that market diffusion follows a typical logistics curve, or S-curve. The shape of the curve depends on the following parameters: 1) the year in which the technology appeared; 2) the year in which diffusion began to take off (first inflection point); 3) the year in which the market began to saturate (second inflection point); and 4) the total size of the potential market. It is possible to estimate this last parameter by, for example, using a product’s diffusion history (see Figure 1).

Relicore introduced the technology in 2002; the diffusion takeoff point is 2006. We selected 2006 based on several factors. First, there is a lack of new entrants into the space. Second, large vendors will soon enter the space: BMC, Mercury, CA, and Collation/IBM have announced or introduced products.4 Finally, the ability to use vendor and client data to evaluate the number of installations in each of the past four years.5 The diffusion time selected — three years — is the best fit for the curve, but it also conforms to our basic hypothesis that the potential market for this technology is initially large IT shops like $1 billion-plus companies.

Tech Choices | The Forrester Wave™: Application Mapping For The CMDB, Q1 2006

© 2006, Forrester Research, Inc. Reproduction Prohibited February 27, 2006

5

Figure 1 Adoption Of Application Mapping Technology

How Will The Market Evolve?

The key characteristic of this technology is that it is a solution enabler. Thus we can envision that it will evolve in two main directions:

· Infrastructure management software vendors will embed the technology in their solutions. This is already the case for BMC, Mercury, and CA. This is also the direction IBM took after acquiring Collation. Eventually, this technology will be so beneficial that all management software vendors will integrate this technology into their solutions.

· Point solution vendors will survive as technology providers. Independent vendors like Relicore, Cendura, Tideway, and nLayers can survive against the major vendors by providing a CMDB to clients who refuse to commit to an integrated solution, and by providing technology to vendors unable or unwilling to develop their own. This requires that these point solution vendors develop links with existing management solutions.

Source: Forrester Research, Inc.

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Number of clients

2011201020092008200720062005200420032002Year introduced

Note: Evaluation model of the potential adoption of the application dependency mapping technology based on a Griliches logistics curve and using market data provided by the Wave respondents.

Tech Choices | The Forrester Wave™: Application Mapping For The CMDB, Q1 2006

© 2006, Forrester Research, Inc. Reproduction ProhibitedFebruary 27, 2006

6

One of the key questions this evolution raises is whether a standard for application discovery will emerge or not. Time and market pressure may play a role in the method of importing or exporting mapping information by pushing for the adoption of interface standards like data center markup language (DCML). However, given the fact that most products available today have some form of export mechanism (APIs or SDKs), and that the window of adoption is relatively narrow, Forrester believes that the current status quo — an absence of standards — is the most probable outcome.

APPLICATION MAPPING EVALUATION OVERVIEW

To assess the state of the application to infrastructure mapping market and see how the vendors stack up against each other, Forrester evaluated the strengths and weaknesses of the eight companies that offer an original product.

Evaluation Criteria

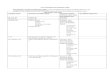

After examining past research, vendor briefings, and customer interviews, we developed a comprehensive set of evaluation criteria (see Figure 2). We evaluated vendors against approximately 63 criteria, which we grouped into three high-level buckets:

· Current offering. Forrester looked at the product architecture for its real-time capabilities in building maps and detecting changes. We considered key issues such as time to collect data, the need for manual intervention, the depth of data collected, and the security and maintenance of the resulting CMDB.

· Strategy. The vendor’s dedication to this technology, the revenue it derives from the technology, and its plans to link the technology to management solutions are key elements of the vendor strategy. In view of the current market split between global and point solution vendors, we also think an adequate sales strategy is important.

· Market presence. We evaluated market presence by the number of customers installing and using the technology, but also on the chance that the vendor will rapidly diffuse the technology by embedding it into its current solutions or partnering with a management solutions vendor.

Tech Choices | The Forrester Wave™: Application Mapping For The CMDB, Q1 2006

© 2006, Forrester Research, Inc. Reproduction Prohibited February 27, 2006

7

Figure 2 Evaluation Criteria

Source: Forrester Research, Inc.

What is the overall architecture and discovery mechanism?

Does the database keep a history of changes or just a series of snapshots? If the latter, how many snapshots?

Is the application dependency discovery automatic, or does it require an application blueprint or fingerprint to discover applications?

How are applications discovered? What is the impact on infra- structures? How deep and detailed is the collected information?

What is the maximum number of objects that can theoretically be stored in the vendor’s product database?

Can changes be detected in real time (as they occur):• In an object?• In an application?

What is the shortest refresh cycle (interval between two discovery runs) that can be run without interfering with normal operations?

Can user-defined fields be added to the CMDB at the object level?

Can the CMDB be integrated with other databases under a common access method?

What type of reporting is available? Is there map visualization software? If yes, is it tree- or graph-based?

How can application maps be exported? Does the company have a standard export scheme for systems management products? Which ones?

What is the largest number of nodes mapped with the vendor's product in an existing customer installation?

How many proprietary or third-party management tools can the product integrate with? Does it have the capability to export application maps?

Is the information in the CMDB reconciled with other existing sources such as asset databases? How?

Architecture

History

Discovery technology

Application discovery

Database storage

Change detection

Refresh cycles

User-defined fields

Access method

Reporting visualization

Application export

Scalability

Integration

Reconciliation of information

CURRENT OFFERING

Tech Choices | The Forrester Wave™: Application Mapping For The CMDB, Q1 2006

© 2006, Forrester Research, Inc. Reproduction ProhibitedFebruary 27, 2006

8

Figure 2 Evaluation Criteria (Cont.)

Source: Forrester Research, Inc.

How is the information maintained over time? How do external processes impact/update the database (i.e., change and configuration management)?

Is the access to the CMDB secured? How?

How is the availability of the CMDB handled? Is there a backup/ recovery solution available?

Maintenance and consistency

Security

Backup and recovery

CURRENT OFFERING

What revenue did/does/will the company derive from the sale of CMDB and application mapping (licenses and maintenance) in 2003–2006?

What portion of the company’s overall business did/does/will it represent in 2003–2006?

How is the solution priced?

Does the licensing require any collateral licenses (e.g., databases)?

What is the planned evolution of the product over the next 12 months?

Is, or will, the CMDB application mapping (be) used for:• Change and configuration management?• Event monitoring?• Performance management?• Service-level management?• Capacity planning?

What is the sales strategy? In which processes or systems management disciplines does/will the vendor sell?• OEM• Partnerships with complementary vendors• Direct sales of a complete solution• Resellers and partners

Revenues

Portion of overall business

Pricing

Licensing

Planned evolution

CMDB application mapping

Sales strategy

STRATEGY

Tech Choices | The Forrester Wave™: Application Mapping For The CMDB, Q1 2006

© 2006, Forrester Research, Inc. Reproduction Prohibited February 27, 2006

9

Figure 2 Evaluation Criteria (Cont.)

Evaluated Vendors

Forrester included eight vendors in the assessment: BMC Software, Computer Associates, Cendura, Collation/IBM, Mercury, nLayers, Relicore, and Tideway Systems. Each of these vendors had:

· The capability to produce an original technology. Vendors either created these technologies in house — as BMC Software, Relicore, Cendura, Tideway, nLayers, and CA did — or acquired them. Mercury acquired Appilog to get this technology, while IBM acquired Collation. While there are many other CMDB vendors, none propose an original technology for mapping application discovery to infrastructure. Because this evaluation concentrates on the application mapping technology itself, we did not consider companies proposing a CMDB with application mapping licensed from one of the original vendors.

Source: Forrester Research, Inc.

How large is the company’s installed base for this product? How valuable are those clients?

How mature is the product, based on the date of its first customer production shipment (not beta)?

How many resellers or licensees does the company have?

How large is the resellers’ installed base?

Is the company working with systems integrators on installed solutions? Which ones?

Does the company have a service organization to support customer implementations?

How many engineers are dedicated to developing this product?

What is the overall sales model and the sales model in specific geographies?

How many employees work in the company?

What was/is/will be the overall company revenue in 2003–2006?

How does the company’s revenue break down between professional services, license revenue, and maintenance revenue?

How much cash does the company have on hand?

Installed base

Shipment

Resellers

Reseller installed base

System integrators

Customer support

Resources

Sales

Employees

Overall revenue

Revenue breakdown

Cash availability

MARKET PRESENCE

Tech Choices | The Forrester Wave™: Application Mapping For The CMDB, Q1 2006

© 2006, Forrester Research, Inc. Reproduction ProhibitedFebruary 27, 2006

10

· The ability to integrate application mapping and CMDB with other solutions. Evaluated vendors were either very large companies integrating application mapping and CMDB into their current product line — BMC, CA, Collation/IBM, and Mercury — or point product companies offering independent products for integration with other solutions — Cendura, nLayers, Relicore and Tideway. While it’s possible to assess technology value independently of vendor size, the size of a vendor does influence its market presence and strategy. Whenever possible, Forrester tried to provide a balanced view between the advantages offered by large companies in terms of solutions and long-term viability and the capabilities of point solution vendors.

A VERY CLOSE RACE

The evaluation revealed a market in which the vendors were very close to each other (see Figure 3). In terms of pure technology, the scoring favored solutions offering a continuous monitoring capability rather than the ones needing a specific scan or using traditional network discovery techniques: Even though network techniques can be continuous, nobody in his right mind would run network-based discovery all the time. The large vendors tended to have a more evolved and clearer strategy to integrate with their existing management solutions. While the market presence reflects today’s situation and favors early innovators in a relatively narrow market, it is clear that the muscle of BMC, Mercury, CA, and Collation/IBM will soon show results.

· nLayers and Relicore are the current leaders. nLayers succeeds on the strength of a technology that uses passive monitoring to collect data and can therefore run continuously. Relicore is well balanced; its technology is less innovative, but has proven its mettle when used in very large deployments.

· BMC shines by the quality of its overall solution. BMC, like Mercury, was an early starter and promptly integrated its Atrium technology with its business services management products. The solution still has some wrinkles, but is a very strong contender.

· Tideway follows closely behind. Tideway has developed a very strong technology. Its product does not match nLayers’ innovation or Relicore’s maturity, but is still quite strong.

· IBM has to digest Collation first. Collation’s technology follows close on the heels of the leaders. However, as the acquisition is recent, true results will not be apparent until IBM first integrates the Collation technology into its products and can show large-scale, live customer deployments. For the time being, this integration is limited to Tivoli Business Service Manager (TBSM).

· Mercury has a strong solution that continues to improve. Mercury was an early starter via its acquisition of Appilog. Mercury has revised the original technology, making it a lot stronger than many competitors. This evolution will make Mercury a strong market contender within the next 12 months.

Tech Choices | The Forrester Wave™: Application Mapping For The CMDB, Q1 2006

© 2006, Forrester Research, Inc. Reproduction Prohibited February 27, 2006

11

· Cendura shows a unique depth of information. The Cendura discovery solution seems less agile than the others, but it has the capacity to dive deeper into configuration parameters within the data center than any of the others.

· CA has to firmly establish Sonar. CA the first introduced its Sonar technology in eTrust Network Forensics and NSM 3.1 in 2003, almost two years before effectively releasing a clearly upgraded version in its core products — r11. We believe that CA’s large installed base will quickly adopt the new version and prove that CA is on par with the rest of the pack.

This evaluation of the configuration management database market is intended to be a starting point only. Readers are encouraged to view detailed product evaluations and adapt the criteria weightings to fit their individual needs through the Forrester Wave Excel-based vendor comparison tool.

Figure 3 Forrester Wave™: Application Mapping For The CMDB, Q1 ’06

Source: Forrester Research, Inc.

Go online to download

the Forrester Wave tool

for more detailed product

evaluations, feature

comparisons, and

customizable rankings.

RiskyBets Contenders

Currentoffering

StrategyWeak

Weak

Strong

Strong Market presenceLeaders

StrongPerformers

nLayers

RelicoreTideway

BMC

Collation/IBMMercury

Cendura

ComputerAssociates

Tech Choices | The Forrester Wave™: Application Mapping For The CMDB, Q1 2006

© 2006, Forrester Research, Inc. Reproduction ProhibitedFebruary 27, 2006

12

Figure 3 Forrester Wave™: Application Mapping For The CMDB, Q1 ‘06 (Cont.)

Source: Forrester Research, Inc.

BMC

Cen

dura

Com

put

erA

ssoc

iate

s

Col

latio

n/IB

M

Mer

cury

nLay

ers

Relic

ore

Tide

way

CURRENT OFFERINGArchitectureHistoryDiscovery technologyApplication discoveryDatabase storageChange detectionRefresh cyclesUser-defined fieldsAccess methodReporting visualizationApplication exportScalabilityIntegration Reconciliation of informationMaintenance and consistencySecurityBackup and recovery

STRATEGY RevenuesPortion of overall businessPricingLicensingPlanned evolutionCMDB application mappingSales strategy

3.692.003.003.003.285.002.002.005.005.003.004.004.003.905.005.005.003.00

4.084.001.000.005.005.004.005.00

Forr

este

r’sW

eigh

ting

60%8%8%5%

11%3%3%5%5%5%5%5%5%

15%10%

3%3%1%

40%11%14%

0%15%25%25%10%

3.351.003.002.003.375.002.003.005.005.005.004.004.003.003.005.005.000.00

3.222.005.000.005.004.001.003.00

2.852.003.003.003.255.003.003.005.005.005.000.001.001.603.001.005.003.00

3.662.001.000.005.004.005.003.00

3.842.003.004.004.155.002.003.005.005.005.005.003.004.303.005.005.003.00

3.283.005.000.005.003.001.005.00

3.522.003.003.003.484.002.503.005.005.005.005.003.004.303.001.003.003.00

3.012.001.000.001.004.004.005.00

4.444.005.004.004.403.004.005.005.005.005.005.003.004.005.005.005.003.00

4.183.005.000.005.004.004.004.00

4.264.005.003.003.105.005.005.005.005.005.004.003.003.705.005.005.004.00

3.844.005.000.001.004.005.003.00

3.812.003.004.003.285.002.003.005.005.003.004.005.003.705.005.005.003.00

3.833.005.000.005.003.004.003.00

Tech Choices | The Forrester Wave™: Application Mapping For The CMDB, Q1 2006

© 2006, Forrester Research, Inc. Reproduction Prohibited February 27, 2006

13

Figure 3 Forrester Wave™: Application Mapping For The CMDB, Q1 ‘06 (Cont.)

VENDOR PROFILES

Leaders

· nLayers. nLayers’ InSight is an appliance-based solution that connects to a network switch. It passively analyzes network traffic in real time without interfering with the data stream to provide a global view of dependencies. In addition, nLayers’ active agent concept remotely captures configuration data on user-selected objects. nLayers initially adopted an indirect sales model and has licensed Managed Objects, BladeLogic, Opsware, and others. nLayers is also part of the IBM Discovery Library with TBSM and integrates with HP OpenView and others.6

· Relicore. The first to bring a product to market — in 2002 — Relicore based its Clarity technology on the distribution of small agents. This allows the product to run in real time. Recently, Relicore has added an agentless option to its Clarity product. The key to Relicore is its product maturity, which customers have rewarded by purchasing very large implementations. Relicore is an HP OpenView partner and has integrations with Peregrine and IBM’s TBSM.7

· BMC Software. BMC’s launch of business services management (BSM) showed its capacity to innovate. Based on existing technologies and expertise within its ranks, BMC Software developed Atrium as an active discovery solution, basing it on BMC’s network management product and the agents inherited from the Marimba acquisition. The product is tightly integrated with BMC’s Remedy solutions, yet is open and carefully crafted for integration and reconciliation. Atrium presents a few technology limitations, but should soon overcome them.8

Source: Forrester Research, Inc.

BMC

Cen

dura

Com

put

erA

ssoc

iate

s

Col

latio

n/IB

M

Mer

cury

nLay

ers

Relic

ore

Tide

way

MARKET PRESENCEInstalled baseShipmentResellersReseller installed baseSystems integratorsCustomer supportResourcesSalesEmployeesOverall revenueRevenue breakdownCash availability

3.653.002.005.004.004.005.005.004.004.004.003.004.00

Forr

este

r’sW

eigh

ting

0%15%15%10%

5%5%5%5%

10%5%5%

10%10%

2.964.004.001.002.003.003.003.002.603.002.004.002.00

2.951.004.000.001.003.004.003.004.005.004.004.004.00

2.542.005.003.003.002.003.001.002.401.001.003.001.00

3.245.004.000.001.004.004.003.003.404.003.002.004.00

3.144.003.005.005.002.002.001.003.401.002.004.002.00

3.464.005.005.004.002.002.002.003.602.003.003.002.00

2.984.004.003.002.003.003.001.002.802.003.003.002.00

All scores are based on a scale of 0 (weak) to 5 (strong).

Tech Choices | The Forrester Wave™: Application Mapping For The CMDB, Q1 2006

© 2006, Forrester Research, Inc. Reproduction ProhibitedFebruary 27, 2006

14

· Tideway. Tideway’s Foundation is another appliance-based product that uses active remote discovery in addition to information coming from already installed agents like those of IBM Tivoli, BMC, NetIQ, and Micromuse. Tideway has a large number of medium-size installations that will no doubt blossom into large-scale deployments.9

Strong Performers

· Collation/IBM. IBM just acquired Collation. While Collation’s Confignia is a proven technology, IBM has yet to do most of the work of integrating the technology into IBM’s change and configuration management database (CCMDB). IBM’s capabilities should become clearer in six months, when the integration starts to bear fruit. In the meantime, Collation’s integration with TBSM is currently available.10

· Mercury. Mercury’s application mapping got a very early start with its acquisition of Appilog in 2004. However, Appilog had been conceived as a system management foundation; Mercury made some adjustments to make it what it is today — an active network discovery tool using agentless collection of configuration data. While Mercury shines in application management and is the uncontested leader in testing, there is still some way to go to cover as much ground in IT Operations as its main competitors BMC, CA, and IBM do. Forrester is confident that Mercury will also improve its current ranking in the coming year.11

· Cendura. Cendura’s Cohesion technology suffers from its use of blueprints. Although the blueprint definition is not a real obstacle, it does contrast with the leading products. Cendura shines in the level of detail it presents about application dependencies. Cohesion integrates with IBM TBSM and Peregrine. Channel sales started only six months ago and will eventually help diffuse the product.12

· Computer Associates. CA’s Sonar technology was released in two forms in 2003: eTrust Network Forensics and in NSM 3.1; it is also and is incorporated in the r11 release of products. The technology itself apparently evolved from a pure network-based solution into a more elegant solution that uses several information sources. Clients should revisit CA’s solution once several large installations are operational. On the other hand, the technology is embedded with all CA solutions and has huge potential in the considerable user base of Unicenter.13

Tech Choices | The Forrester Wave™: Application Mapping For The CMDB, Q1 2006

© 2006, Forrester Research, Inc. Reproduction Prohibited February 27, 2006

15

SUPPLEMENTAL MATERIAL

Online Resource

The online version of Figure 2 is an Excel-based vendor comparison tool that provides detailed product evaluations and customizable rankings.

Data Sources Used In This Forrester Wave

Forrester used a combination of two data sources to assess the strengths and weaknesses of each solution:

· Vendor surveys. Forrester surveyed vendors on their capabilities as they relate to the evaluation criteria. Once we analyzed the completed vendor surveys, we conducted vendor calls where necessary to gather details of vendor qualifications.

· Third-party assessments. To validate product and vendor qualifications, Forrester also interviewed three companies that had conducted independent evaluations of the vendors’ products.

The Forrester Wave Methodology

We conduct primary research to develop a list of vendors that meet our criteria to be evaluated in this market. From that initial pool of vendors, we then narrow our final list. We choose these vendors based on: 1) product fit; 2) customer success; and 3) Forrester client demand. We eliminate vendors that have limited customer references and products that don’t fit the scope of our evaluation.

After examining past research, user need assessments, and vendor and expert interviews, we develop the initial evaluation criteria. To evaluate the vendors and their products against our set of criteria, we gather details of product qualifications through a combination of questionnaires and discussions. We send evaluations to the vendors for their review, and we adjust the evaluations to provide the most accurate view of vendor offerings and strategies.

We set default weightings to reflect our analysis of the needs of large user companies — and/or other scenarios as outlined in the Forrester Wave document — and then score the vendors based on a clearly defined scale. These default weightings are intended only as a starting point, and readers are encouraged to adapt the weightings to fit their individual needs through the Excel-based tool. The final scores generate the graphical depiction of the market based on current offering, strategy, and market presence. Forrester intends to update vendor evaluations regularly as product capabilities and vendor strategies evolve.

Tech Choices | The Forrester Wave™: Application Mapping For The CMDB, Q1 2006

© 2006, Forrester Research, Inc. Reproduction ProhibitedFebruary 27, 2006

16

ENDNOTES1 The ITIL approach is quickly becoming the de facto standard for IT service delivery — Forrester expects

that implementation levels in $1 billion-plus companies will grow from 13% today to around 40% by the end of 2006. See the July 20, 2005, Tech Choices “Point Solutions For Enterprise Infrastructure Management.” The Information Technology Infrastructure Library (ITIL) is a set of standard IT terminologies — such as a high-level definition of a change request — that the United Kingdom Central Computer and Telecommunication Agency developed in the late 1980s and early 1990s to address the IT service support and delivery issues that IT infrastructure organizations face. ITIL standards were designed to establish guidelines and a common language for operational processes, such as change management, problem resolution, service delivery, and resolution of customer inquiries. See the September 21, 2004, Best Practices “Implementing ITIL.” ITIL is a registered trademark, and a registered community trademark of the UK Office of Government Commerce, and is registered in the US Patent and Trademark Office. In 2001, the United Kingdom Central Computer and Telecommunication Agency was absorbed into the Office of Government Commerce, which now owns ITIL. See www.ogc.gov.uk/index.asp?id=2261 for more information.

2 A configuration management database (CMDB) stores details of the elements that an organization uses to provide and manage its IT services. Configuration management is responsible for identifying, recording, tracking, and reporting key IT components or assets — these assets are called configuration items (CIs). The information that is captured and tracked will depend upon the specific CI, but will often include a description of the CI as well as its version, constituent components, relationships to other CIs, location/assignment, and current status. Change management is the practice of ensuring that all changes to CIs are carried out in a planned and authorized manner. This includes: ensuring that there is a business reason behind each change; identifying the specific CIs and IT services affected by the change; planning the change; testing the change; and having a rollback plan should the change result in an unexpected state of the CI. See the November 8, 2004, Market Overview “Change And Configuration Management.”

3 On February 7, 2006, Symantec announced it had signed a definitive agreement to acquire Relicore. The acquisition of small innovators by large vendors is a clear sign that a technology is approaching widespread adoption. Relicore’s purchase by Symantec definitely fits this pattern, especially because it follows closely on the heels of the acquisition of Collation by IBM. As of now, each of the large players in system management and data center automation (except Hewlett-Packard) has selected or developed an application dependency mapping solution. So what we can expect from Symantec? First, the company will upgrade its data center automation solution, and then it will reinforce its VERITAS i3-based performance management solution. Application dependency mapping is versatile; it began as an enabler for business service management and change management, and now it’s expanding into data center management — not just with Symantec, but with vendors such as BladeLogic, IBM Tivoli, and Opsware. See the February 9, 2006, Quick Take

“Symantec Buys Relicore: The Application Dependency Mapping Market Takes Off.”

4 IBM Tivoli’s recent acquisition of Collation confirms that the future of infrastructure management in general will be based on an understanding and mapping of the relationships between IT services and infrastructure components. After a first foray into importing other people’s maps into its service

Tech Choices | The Forrester Wave™: Application Mapping For The CMDB, Q1 2006

© 2006, Forrester Research, Inc. Reproduction Prohibited February 27, 2006

17

management tools through the Discovery Library, IBM Tivoli has now made a more far-reaching commitment to the technology by acquiring one of the innovators in the space. Over the next few months, however, this will not add many benefits to IBM’s portfolio, apart from the already existing hooks into IBM Tivoli’s service management products. But within the next nine to 12 months, Forrester expects a full integration with other IBM Tivoli products, most notably the all-important configuration management database (CMDB), the linchpin of any IT infrastructure library (ITIL) and business service management (BSM) implementation. This move leaves open several questions about the future of smaller vendors of application mapping technology, as well as the reaction of Collation’s licensees. See the November 30, 2005, Quick Take “IBM Tivoli’s Discovery: It’s About Time!”

5 This view of the dynamics of market adoption are based on the evolution of the supply side: 1) innovators enter the market on faith; 2) new vendors join the market and legitimize the innovation concept and its market potential; 3) the number of vendors builds up: as the supply side increases, the technology improves and starts pulling the demand side; 4) larger vendors enter the market and some consolidation takes place. Technology improvement becomes process improvement (either technology manufacturing or the capability to satisfy criteria 3 and 4). Process improvement leads to cost decrease and quality increase. Larger vendors build market infrastructure and solution awareness. At this point, the conditions of large diffusion are met. See the April 12, 2005, Forrester Big Idea “How To Predict Which IT Innovations Will Succeed.”

6 View the vendor summary for more detailed analysis on how nLayers fared in this evaluation. See the February 27, 2006, Tech Choices “nLayers Leads With The Most Effective Configuration Management Database.”

7 View the vendor summary for more detailed analysis on how Relicore fared in this evaluation. See the February 27, 2006, Tech Choices “Relicore Offers A Well-Honed Configuration Management Database.”

8 View the vendor summary for more detailed analysis on how BMC fared in this evaluation. See the February 27, 2006, Tech Choices “BMC Software Provides An Integrated Yet Open Configuration Management Database.”

9 View the vendor summary for more detailed analysis on how Tideway fared in this evaluation. See the February 27, 2006, Tech Choices “Tideway Presents A Very Capable Configuration Management Database.”

10 View the vendor summary for more detailed analysis on how IBM fared in this evaluation. See the February 27, 2006, Tech Choices “Collation/IBM Starts Expanding Its Configuration Management Database.”

11 View the vendor summary for more detailed analysis on how Mercury fared in this evaluation. See the February 27, 2006, Tech Choices “Mercury Enhances The Technology Foundation Of Its Configuration Management Database.”

12 View the vendor summary for more detailed analysis on how Cendura fared in this evaluation. See the February 27, 2006, Tech Choices “Cendura Offers The Most Detailed Configuration Management Database.”

13 View the vendor summary for more detailed analysis on how CA fared in this evaluation. See the February 27, 2006, Tech Choices “Computer Associates Introduces Its New Configuration Management Database.”

Forrester Research (Nasdaq: FORR)

is an independent technology and

market research company that

provides pragmatic and forward-

thinking advice about technology’s

impact on business and consumers.

For 22 years, Forrester has been

a thought leader and trusted advisor,

helping global clients lead in their

markets through its research,

consulting, events, and peer-to-

peer executive programs. For more

information, visit www.forrester.com.

Australia

Brazil

Canada

Denmark

France

Germany

Hong Kong

India

Israel

Japan

Korea

The Netherlands

Switzerland

United Kingdom

United States

Headquarters

Forrester Research, Inc.

400 Technology Square

Cambridge, MA 02139 USA

Tel: +1 617/613-6000

Fax: +1 617/613-5000

Email: [email protected]

Nasdaq symbol: FORR

www.forrester.com

H e l p i n g B u s i n e s s T h r i v e O n T e c h n o l o g y C h a n g e

For a complete list of worldwide locations,visit www.forrester.com/about.

Research and Sales Offices

36891

For information on hard-copy or electronic reprints, please contact the Client

Resource Center at +1 866/367-7378, +1 617/617-5730, or [email protected].

We offer quantity discounts and special pricing for academic and nonprofit institutions.