Embed Size (px)

Citation preview

THE FORECLOSURE ENVIRONMENT

Traditionally, foreclosure has been an event that has only afflicted those who were irresponsible,

lost their jobs, or were subjected to some major calamity, i.e. – serious illness, accident, or

natural disaster. In point of fact, a combination of factors, which go far beyond the traditional

causes of foreclosure, are resulting in the greatest number of people losing their property in the

2000s, than at any other time in recent history.

State of the economy

First, and probably most obviously, is the general state of the economy. The economy

gyrates between boom and bust. It seems that we are either in “great times” or “bust’. The

problem that develops is that in the “great times” people go out and incur real property loan

obligations that extend beyond the “great times” into the “bust” times. Traditionally, this

practice only affected the blue collar class families who were the first to lose employment when

the “bust” portion of the cycle came around. Now, however, with the two-income family rapidly

becoming the standard in our society, when the “bust” cycle of the economy occurs, the

likelihood is good that one of the two incomes will be affected. As a result, foreclosure has

transcended class boundaries and now victimizes the middle and upper-middle classes as well as

the blue collar families. With the inception of, and excessive promotion of the “home equity”

types of loans, wherein families can buy cars, clothes, vacations, boats, etc., etc., and secure the

loan with their real property, we can expect even more foreclosures when the economy hits the

next “bust” cycle.

Balloon payment loans

Another major cause of foreclosures in today’s market is the coming due of literally

millions of dollars of balloon payment loans. Many of the borrowers entering into these types of

loan transactions do so with the expectation that when the balloon payment comes due they will

be able to refinance. How short the public’s memory. They do not seem to recall the 18%

interest rates of the early 80s., when it became virtually economically impossible to refinance.

They do not remember the disintermediation (outflow of savings from thrift institutions) that

occurred in the early 70s, when it was literally impossible to obtain any kind of loan.

Traditionally, balloon payment loans existed predominantly in the private sector. Now however,

institutional lenders are becoming one of the major suppliers of balloon payment loans in the

marketplace. Whereas a private lender might not have been oriented towards foreclosures if a

balloon payment could not be paid off.

Speculators

In the last “bust” cycle, in the early 80s, and current times, some writers suggested that

the heavy speculative activity of the late seventies were resulting in the increased incidence of

foreclosure. They stated that investors were “dumping” properties onto the market when the

appreciation rates slowed in their upward spiral, and unable to get properties sold, the speculators

allowed lenders to just “take them back”. The incidence of that kind of activity, in point of fact,

did not end. Real estate continues to be regarded as a “get rich quick” type of investment

medium. As long as that attitude remains in the marketplace there will be an increased incidence

of foreclosure.

Conclusions

The effects of any one of the above causes of foreclosure can be detrimental in and of

itself. When they occur simultaneously, the result proves disastrous in grandiose proportions,

such as the incredible number of foreclosures that occurred in the period from 1980-1982 and

2001 to present. During the past few years (“great times”) real estate licensees (along with the

rest of the public) have been lulled into courses of action that will prove significantly detrimental

when the next “bust” cycle (2001) occurs. Unlike some other businesses, real estate licensee

transactions have far reaching future consequences. When a real estate licensee sells property

today, he or she must be prepared to explain not only the present consequences of some, if not

many, of the real estate transactions that are taking place.

HISTORY OF FORECLOSURE

In order to more fully understand foreclosure today, and all that word implies, it is useful to

analyze foreclosure from its historical perspective. A misperception is that foreclosure is a static

procedure, whereas in reality it’s always changing. Only through a knowledge of where it has

been and where

it is now, can we anticipate and be prepared for where it will be in the future.

Development of the mortgage

Historically, the mortgage was the predominant security device used in real estate

transactions. Common law treated the mortgage as a conveyance of fee title in the property,

from the borrower to the lender, subject to a condition. The condition being the payment of the

debt. The date the payment was due was known as the “law day”. Upon breach of the condition,

non-payment of the debt or some other default, the lender received an absolute fee simple estate,

free and clear of the condition. Prior to the payment of the debt, the lender, as holder of the title,

was entitled to the possession of the mortgaged property and the rents or profits produced by the

property. Since the lender had full use of the property, ownership was dead, as far as the

borrower was concerned, hence the literal translation of the French word mortgage is; “mort”

meaning dead, and “gage” meaning pledge. A mortgage, historically, was a pledge wherein your

ownership of the property went “dead” until you fulfilled the pledge. To prevent the harsh

application of this principle, courts of equity permitted defaulting borrowers to recover the

property by paying off the debt, plus costs and damages. This right to recover the property came

to be called the “equity of redemption”. It developed as a judicial response to the harsh

forfeiture inherent in the common law mortgage.

The trust deed-a legislative response

The deed of trust (or trust deed as it is sometimes called) was developed as a legislative

response to the broad benefits inherent in the judicial “equity of redemption”. It was developed

and utilized during the 19th

century to avoid the procedural inhibitions that had been imposed on

lenders by the courts. The use of an actual deed conveying title to a trustee possessing a power

of sale offered lenders several advantages over the mortgage. By the time the distinctions

between mortgages and trust deeds were removed, which occurred during the early part of the

twentieth century, the trust deed had become the generally accepted and preferred security device

in California.

Strict foreclosure

Because trust deeds are so commonly utilized in California, the public and real estate

licensees may be lulled into complacency regarding other types of security devices and

foreclosure practices. The State of Vermont uses a procedure (ever since the days of the

American Revolution) called “strict foreclosure” whereby the lender can take the borrower’s

property in satisfaction of the debt, without having to sell the property first. As recently as 1979,

a Federal Court of Appeals held that practice to be permissible. In point of fact, power of sale

foreclosures, like California uses, were not even permitted in the State of Vermont until 1973.

We have seen the effect of California laws and court cases such as the Wellenkamp decision, on

other parts of the country. We should not presume that other parts of the country cannot have an

effect on us. Through a knowledge and understanding of what foreclosure has involved in the

past and, with an idea as to what practices are currently utilized in other areas of the nation,

agents and the public are better equipped to comprehend and adapt to the changes that are taking

place today.

THE FORECLOSURE PROCESS

In order to understand and firmly establish the two predominant foreclosure procedures used in

California in today’s market (judicial foreclosure and private sale foreclosure), the judicial

process will be explained within the context of a mortgage, and private sale process will be

explained within the context of a trust deed. This is done recognizing that mortgages have not

been used in the State of California, except in rare instances. The purpose is to establish the

procedure in a context which will make it easy to remember. It is also recognized that most

mortgages today are written with a power-of-sale provision enabling the lender to foreclose

through private sale process, and that most trust deeds contain a provision for judicial

foreclosure. In other words, you can foreclose either instrument either way most of the time.

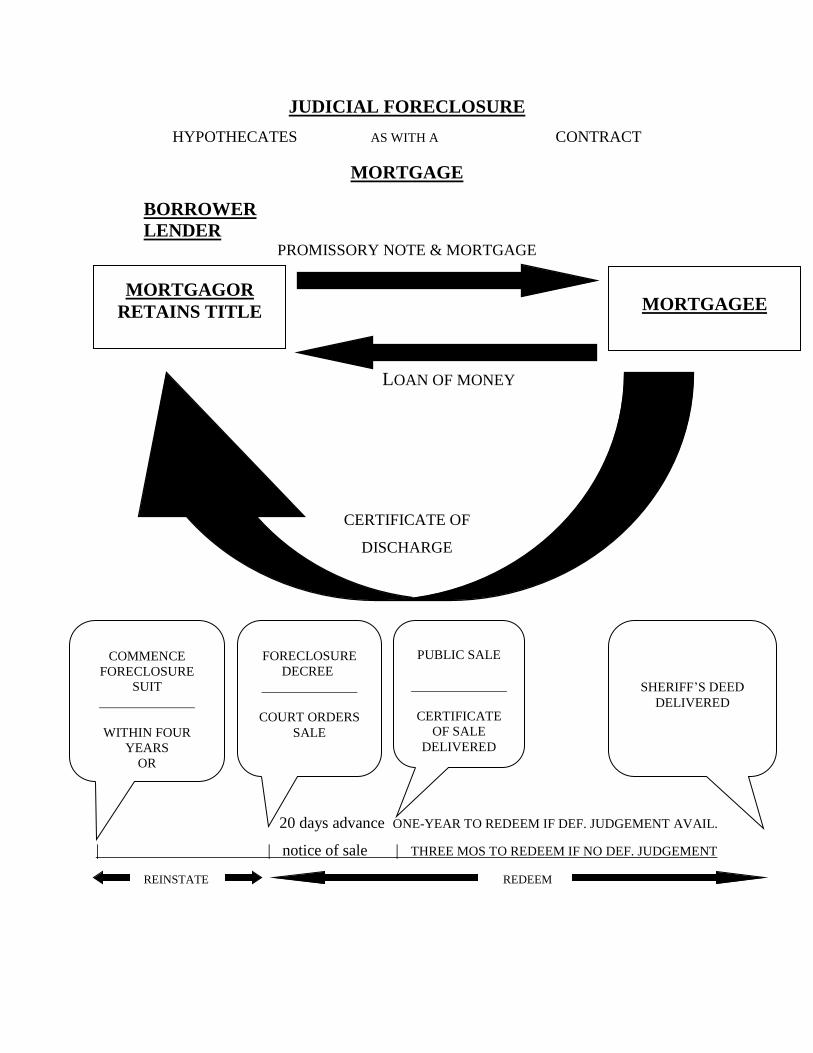

Judicial Sale

In California, a mortgage does not convey title, but merely imposes a lien on the property

as security for the obligation. Therefore, if one joint tenant were to mortgage joint-tenancy

property without consent of the other, and then die, the non-consenting surviving joint tenant

would take the property free and clear of the mortgage. A mortgage is a contract and is subject

to the usual rules of contract interpretation. Together with the promissory note, the mortgage is

interpreted as constituting one contract when they are part of the same transaction. For example,

under the Statute of Limitations, the right to enforce the terms of a written contract “outlaws”

four years from the point in time the default occurs. Therefore, your right to judicial foreclosure

in the mortgage is said to “outlaw” four years from the default on the note. The mortgage is a

special kind of a contract in that it “hypothecates” real property. That means it makes the

property security for the performance of the obligation, generally the repayment of the debt, yet

the borrower does not have to give up possession of the property itself.

Parties to a mortgage

There are two parties to a mortgage; a borrower, called a mortgagor, and a lender, called

a mortgagee. The mortgagor gives a promissory note and a mortgage contract to the mortgagee

while retaining complete and total title to the property. In return, the mortgagee gives a loan of

money to the mortgagor.

Release

Upon repayment of the obligation, the mortgagee executes and delivers what is called a

“certificate of discharge”, or it is sometimes referred to as the “satisfaction of mortgage”.

According to Section 2941 of the California Civil Code, the mortgagee has 30 days to deliver the

document or see to it that it is delivered, or else be found guilty of a misdemeanor and subject to

$300 fine in addition to actual damages.

Default

Upon default, the mortgagee may commence a foreclosure suit. Obviously, the time to

get to trial and receive a judgement will vary from county to county as the demands on the court

calendar vary from area to area. Up until the point in time that the foreclosure decree is issued

and the court orders the sale of the property, the mortgagor may “reinstate” the property by

paying all past due amounts plus penalties, costs, and charges. Once the foreclosure decree is

issued, the right to reinstate is lost. From that point until the Sheriff’s Deed is delivered, if the

mortgagor wants to retain the property, he or she must redeem the property by paying the entire

loan plus penalties, costs and charges.

After the foreclosure decree is issued, the mortgagee must advertise notice of sale. This

is accomplished by posting a notice of sale in a public place, by posting a notice of sale on the

property itself, and by publishing a notice of sale in a newspaper of general circulation in the

city, county, or judicial district in which the property is located. The first date of posting and

publication must be at least 20 days before the date of the sale.

When the notice of sale process has been complied with, the sheriff or the court

commissioner will hold a public sale. The high “cash” bidder at the sale will receive a

Certificate of Sale. Title to the property does not transfer at this point in time. The borrower has

either one year to redeem the property, if a deficiency judgement is available, or three months, if

no deficiency judgement is available.

A deficiency judgement is a general lien (one that covers all property owned or acquired

by an individual) that may be obtained by a lender if the amount received a the Sheriff’s sale is

not sufficient to pay off the loan. Deficiency judgements are not available on loans to purchase

1-4 units or owner-occupied property (purchase money encumbrances).

JUDICIAL FORECLOSURE

HYPOTHECATES AS WITH A CONTRACT

MORTGAGE

BORROWER

LENDER

PROMISSORY NOTE & MORTGAGE

LOAN OF MONEY

CERTIFICATE OF

DISCHARGE

20 days advance ONE-YEAR TO REDEEM IF DEF. JUDGEMENT AVAIL.

| | notice of sale | THREE MOS TO REDEEM IF NO DEF. JUDGEMENT

REINSTATE REDEEM

MORTGAGOR

RETAINS TITLE

MORTGAGEE

COMMENCE

FORECLOSURE

SUIT

WITHIN FOUR

YEARS

OR

RIGHT

FORECLOSURE

DECREE

COURT ORDERS

SALE

PUBLIC SALE

CERTIFICATE

OF SALE

DELIVERED

SHERIFF’S DEED

DELIVERED

Private Sale

There are no enabling statutes which set forth the form of the trust deed, its required

provisions or its legal effects. There are only laws which regulate its use. In most standard

forms the trustor “grants, transfers, and assigns” the property to the trustee who holds the title as

security for the performance of the obligation. The courts have apparently, therefore, adopted a

“title theory” for the trust deed. For most practical purposes, however, the results are the same as

the mortgage “lien theory”. For example, if a joint tenant executed a trust deed on a property

without the knowledge or consent of the other joint tenants on the property, and if a true transfer

of title had taken place, the joint tenancy would have been broken and the creditor and the non-

consenting joint tenant would have become tenants in common. Instead, its true net legal effect

is to merely create a lien on the property. Although title technically passes to the trustee, the

trustee must re-convey upon repayment of the obligation. Legal title passes to the trustee solely

for the purpose of securing the obligation. He receives only such title as is necessary for the

execution of his trust. Until a default occurs or the obligation is satisfied, the trustee’s title

remains inactive. For most practical purposes, therefore, a deed of trust can be considered

substantially to be a mortgage with a power of sale. On the other hand, in certain instances,

courts have emphasized the conveyance of title aspect over the lien aspect. For example, the

Statute of Limitations prevents enforcement of a mortgage lien when the statutory time has

expired on the underlying obligation. In a trust deed, the trustee’s powers of enforcement are not

affected by the Statute of Limitations.

Parties

There are three parties to a trust deed; the borrower, called the trustor, the lender, called

the beneficiary, and a disinterested third party, called the trustee. The trustor gives a promissory

note and trust deed to the beneficiary in exchange for which the beneficiary gives the trustor the

loan of money. The trust deed, possessed by the beneficiary, transfers what has come to be

called “bare legal” or “naked” title to the trustee. In fact, what is transferred is a power-of-sale

ability on the part of the trustee which can only be used upon default of any of the stated

obligations of the trustor. The trustor retains what has come to be called “equitable” title. In

other words, in fairness, the trustor remains the owner of the property.

PRIVATE SALE FORECLOSURE

HYPOTHECATES AS WITH A SPECIAL KIND OF DEED

MORTGAGE

BORROWER

LENDER

PROMISSORY NOTE & MORTGAGE

LOAN OF MONEY

DISINTERESTED 3RD

PARTY

| | 3 MONTHS | 20 DAYS |

TO REINSTATE TO REDEEM

(PAY ALL PAST DUE AMOUNTS, COSTS) (PAY ENTIRE OBLIGATION)

NO DEFICIENCY JUDGEMENT ALLOWED

TRUSTOR

RETAINS

EQUITABLE

TITLE

BENEFICIARY

BENEFICIARY

NOTIFIES

TRUSTEE OF

DEFAULT

TRUSTEE

RECORDS

NOTICE OF

DEFAULT

TRUSTEE

RECEIVES BARE

LEGAL TITLE

RECONVEYANCE

DEED

REQUEST FOR

RECONVEYANCE

POWEROF

SALE

ADVERTISE NOTICE OF SALE

1) POST IN PUBLIC PLACE

2) ADVERTISE 1X PER WEEK

3) POST ON PROPERTY

TRUSTEE’S SALE

HIGH CASH BIDDER

GETS TRUSTEE DEED

Release

Upon repayment of the obligation, the beneficiary must instruct the trustee to re-convey

the “bare legal” title to the trustor. The beneficiary does so when he executes and delivers a

Request for Re-conveyance to the trustee. The trustee executes and delivers a Re-conveyance

Deed to the trustor. The beneficiary must see to the re-conveyance within thirty days or he is

guilty of a misdemeanor and is subject to a $300 fine in addition to actual damages.

Default

Upon default, the beneficiary notifies the trustee of the default, and instructs the trustee to

initiate the foreclosure process. The trustee records a Notice of Default at the county recorder’s

office in the county in which the property is located. Recordation of the Notice of Default starts

a 3 month waiting period during which the trustor may reinstate the loan by paying all the past

due amounts, penalties, costs, and charges. At the end of the 3 months the trustee, if there is no

reinstatement, may start advertising notice of sale by posting a notice of sale in a public place

and on the property for twenty days. In addition the notice of sale must be advertised once a

week for three weeks in a newspaper of general circulation in the city, county, or judicial district

in which the property is located. During the advertising notice of sale period, the trustor may

redeem the property by paying off the entire obligation including all penalties, costs, and

charges. At the end of the twenty days, the trustee can conduct the Trustee’s Sale, with the high

cash bidder receiving a trustee’s deed and immediate title to and possession of the property.

The above process has been simply stated in this context in order to compare private sale

process foreclosure with judicial sale process.

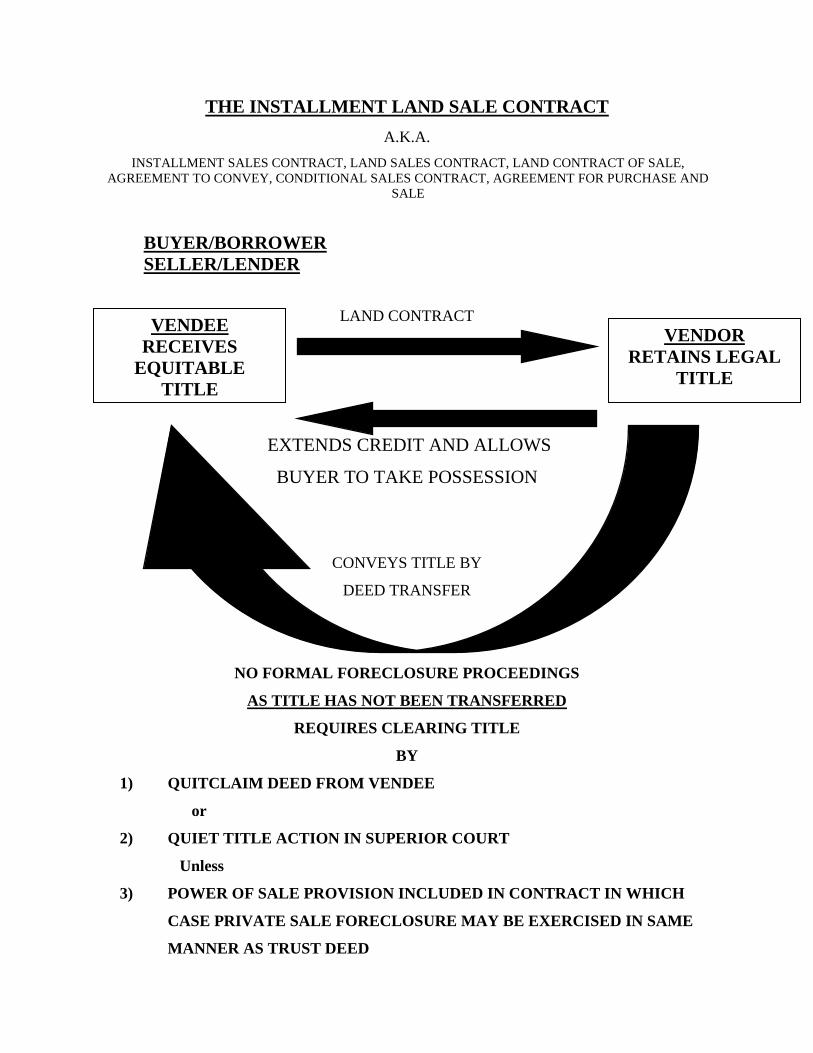

Installment Land Sale Contract

The installment land sale contract (also commonly known as the installment sales

contract, land sales contract, land contract of sale, land contract, real property sales contract,

conditional sales contract, agreement for purchase and sale, or simply, contract of sale) can be

simply defined as an instrument whereby a seller agrees to convey title to real property to a

buyer after the buyer has met certain conditions specified in the contract and which does not

require the seller to convey title within one year. The presumed advantage of such a security

device to the seller, acting as a lender in the transaction, would be that in as much as he still

holds title to the property, it would appear easier, if a default occurred, to eliminate a purchaser’s

interest in the property. This was not the conclusion of the court in the case of Barkis v. Scott,

however. In this case, the court found that harsh and unreasonable foreclosure proceedings were

prohibited by the California Civil Code. In light of this and other court findings, the seller faces

the problems of difficulty in “clearing” title and taking possession the property if the buyer

defaults. The primary disadvantage to a purchaser using a land contract is that during the interim

from the execution of the contract to full performance by the buyer, if the seller should die, or be

found incompetent, or go bankrupt, the buyer could anticipate a time-consuming, frustrating, and

expensive litigation before obtaining a deed and a policy of title insurance. Many of these

disadvantages may be largely eliminated by a three-party land contract, where a trustee is

appointed in the same way as in a trust deed, coupled with title insurance insuring the equitable

title of the buyer and the legal title of the seller. It is not the intent, here, to analyze and instruct

on the contractual aspects of land contracts, that being a subject unto itself, properly addressed in

a contract law context. Rather this type of security device is being examined solely from the

standpoint of being a financing instrument.

Parties

There are two parties, traditionally, to a Land Contract; a borrower who is also acting as a

buyer in the transaction, and a lender who is acting as a seller in the transaction. The

borrower/buyer is called the vendee. The lender/seller is called the vendor. The vendee enters

into the land contract with the vendor. He promises to perform certain acts, and the vendor, in

return, agrees to extend credit to the vendee and allow the vendee to take possession of the

property. In addition, the vendor agrees and promises to transfer title to the vendee upon full

performance of all acts required. Because of this promise the vendee receives “equitable” title to

the property, with the vendor holding the “legal” title until performance of all the obligations.

Release

Upon performance of all conditions, the vendor conveys “legal” title by a deed transfer

to the vendee.

Default

Upon default in any of the conditions, there traditionally is no formal foreclosure

procedure as title has not been transferred. What is required is to clear title of the vendee’s

interest. This may be accomplished in two ways:

1. The vendee can execute and deliver to the vendor a quitclaim deed relinquishing

any and all interest in the property. Obviously this may be difficult to accomplish

in light of the vendee’s equity interest in the property, etc.

2. The vendor can initiate a quiet title action in Superior Court to have the vendee’s

interest removed. If this is the course of action used, the vendor can expect a

judicial foreclosure process to be employed by the court with reinstatement and

redemption allowed for notice of sale, etc.

3. If the land contract is a three-party instrument (a land contract with a power of

sale provision), the private sale process could be employed to foreclose upon

default.

THE INSTALLMENT LAND SALE CONTRACT

A.K.A.

INSTALLMENT SALES CONTRACT, LAND SALES CONTRACT, LAND CONTRACT OF SALE,

AGREEMENT TO CONVEY, CONDITIONAL SALES CONTRACT, AGREEMENT FOR PURCHASE AND

SALE

BUYER/BORROWER

SELLER/LENDER

LAND CONTRACT

EXTENDS CREDIT AND ALLOWS

BUYER TO TAKE POSSESSION

CONVEYS TITLE BY

DEED TRANSFER

NO FORMAL FORECLOSURE PROCEEDINGS

AS TITLE HAS NOT BEEN TRANSFERRED

REQUIRES CLEARING TITLE

BY

1) QUITCLAIM DEED FROM VENDEE

or

2) QUIET TITLE ACTION IN SUPERIOR COURT

Unless

3) POWER OF SALE PROVISION INCLUDED IN CONTRACT IN WHICH

CASE PRIVATE SALE FORECLOSURE MAY BE EXERCISED IN SAME

MANNER AS TRUST DEED

VENDEE

RECEIVES

EQUITABLE

TITLE

VENDOR

RETAINS LEGAL

TITLE

All-inclusive Trust Deed

The all-inclusive trust deed (also referred to as a wrap-around mortgage) has been

defined as “a purchase money encumbrance which is subordinate to the encumbrance or

encumbrances to which it is subordinated”. What that means is that it is a loan which is created

in order to purchase property and occupies a lower priority position than a pre-existing loan or

loans. The new loan is created by combining part or all of the seller’s equity and by using, as part

of the new loan, the pre-existing loan or loans. It is described as all-inclusive, therefore, because

it includes the seller’s equity in the property plus the pre-existing loans. The new loan is said to

“wrap-around” the existing loan by incorporating the existing loan into the new loan, while still

remaining subordinate (of a lower priority position) to the existing loan.

While sometimes referred to as all-inclusive “first” trust deed, it is similar to a second

trust deed in that the existing loan is not disturbed yet the borrower is able to borrow an

additional amount against the property. A foreclosure procedure involving an all-inclusive trust

deed would proceed as if it were any other junior lien.

Promissory Note

The promissory note is the primary evidence of the debt or basic obligation. It is more

specifically a written promise to pay a specific amount of money to a specific person at a specific

point in time. There are three types of promissory notes used, commonly, in real estate

transactions. They are:

1. The straight note- interest only is paid during the term of the note with a

balloon payment of principal due at the end of the term.

2. The installment note-periodic payments on principal separate from interest.

3. The amortized note-fixed, equal payments of principal and interest which,

over the term of the loan, pays off the entire balance.

Whatever the format of payment, all promissory notes are categorized as types of contracts. They

have nothing to do with an interest or right in any real property. The security device (i.e.

mortgage, or trust deed) is the instrument which creates rights in property. There are, however,

legal rights associated with promissory notes. Specifically, the right to take legal action to

recover money owed is obtained by the payee (the person receiving payment).

Negotiable Instruments

With regard to that right to take legal action to recover, a brief discussion of negotiable

instruments is in order. A negotiable instrument is a written promise or order to pay money

which, when properly prepared, is typically accepted as the virtual equivalent of cash. An

example of a written promise would be a promissory note. An example of an order to pay

money would best be exemplified by a personal check. To be regarded as a negotiable

instrument, the document must conform to certain statutory requirements:

1. it must contain an unconditional promise

2. it must be in writing

3. it must be made by one person to another

4. it must be signed by the maker

5. it must be engaging to pay on demand or at a fixed or determinable future time

6. it must contain a sum certain, in money

7. it must be made payable to order or to bearer

If all of the above are present, the document qualifies as a negotiable instrument. If any one

element is missing, the document may still be valuable and capable of being transferred like any

other contract. As such, the transferee would get no more than the transferor had, in terms of

legal rights to collect the money owed. If it does contain all of the above elements, the transferee

may get more than the transferor had. In order to gain these benefits the note must be

“negotiated” under the following conditions:

1. the negotiable instrument must be complete and regular on it’s face

2. the transferee must obtain the document before it was overdue and with no notice of

it’s previous dishonor or default

3. it must be taken for a valuable consideration

4. it must be taken in good faith

If received under the above conditions, the transferee becomes known as the “Holder-in-Due-

Course”. If the “Holder-in-Due-Course” brings an action to collect on the note, the maker

cannot use any of the following “personal” defenses to refuse payment, although they would be

good against the original payee. In other words, if the promissory note contains certain elements

and, if it is transferred under certain conditions, the transferee may enjoy a more favored status

than even the original payee had. The “personal” defenses which would be good as to the

original payee but not the “Holder’ are as follows:

1. fraud in the inducement

2. lack or failure of consideration

3. prior payment or cancellation

4. set-off

On the other hand, the following “real” defenses are good against the world including any

“Holder-in-Due-Course”.

1. incapacity of maker at time of creation

2. illegality of the instrument

3. forgery

4. material alteration

The importance of understanding rights associated with promissory notes stems from the fact

that they are commonly viewed, in real estate transactions, in context with a security device, such

as a trust deed. The rights associated with a trust deed are applied to a promissory note. If a

trust deed were to be defective, those rights might not exist. That would not preclude individuals

from exercising their rights with regards to the promissory note. In other words, individuals

have a right to foreclose on real property in a trust deed and they also have a right to sue on the

promissory note. Either right may be taken.

THE FORECLOSURE PRACTICES

Having examined the foreclosure process in simple, comparative terms, with an intention

of becoming familiar with the different processes in general, it is now appropriate to analyze in

detail, the foreclosure process most commonly used in the State of California. That is, the

private-sale foreclosure process. The following information was obtained through extensive

interviews and discussions with a variety of foreclosure service companies, title insurance

companies, and attorneys specializing in real estate law. The point being, the practices described

herein are not one, singular point of view. Certainly each individual or entity that is involved in

a foreclosure must comply with the law regarding foreclosure. There is much discretion,

however, within the laws regarding foreclosure. The practices that follow are those that the vast

majority of experts represent and used the majority of the time. In any specific foreclosure, a

specific individual or entity may or may not make use of any specific practice, wherein the law

does allow discretion. Following is a description of a typical foreclosure, by private sale process,

as it will probably occur in the State of California today.

1. Upon default, the beneficiary will notify the trustee of the default and the trustee will

request of the beneficiary the original of the promissory note and trust deed. If the

original is lost or otherwise unavailable, the trustee can procure a copy of the trust

deed from the County Recorder. The note presents more of a problem. An

institutional trustee (defined as one who knows what they are doing) may require an

affidavit by the beneficiary that the note has been lost and not sold or assigned to any

other person. In addition, the trustee may require a lost instrument bond, which can

be expensive to obtain. If requested, an option for the beneficiary is to substitute

another trustee who does not require the lost instrument bond. The beneficiary may

name himself trustee for all purposes except to conduct the actual sale.

2. The trustee will require a “Declaration of Default” from the beneficiary describing

exactly the nature of the default. If there is a dispute between the trustor and

beneficiary over the nature of the default, the trustee may and probably will stop

foreclosure.

3. The trustee will require a deposit of ($150-$900) from the beneficiary to cover costs,

i.e. recording costs, drawing documents, foreclosure report from title insurance

company, etc. The deposit amount then becomes one of the charges necessary to

reinstate or redeem the property.

4. Prior to recording the Notice of Default, the trustee will obtain from a title company

what is variously called a “notice of default report”, or a “foreclosure report”, or

“foreclosure guarantee”. The purpose of obtaining this document is to ascertain all

parties to who notices of default should be mailed. In addition, the trustee will

probably check the county tax records to ascertain that taxes are current. Only those

items stated in the notice of default are subject to foreclosure. The trustee will want

to be certain that all defaults are included in the notice.

5. The trustee will ask that beneficiary if he has received notice of bankruptcy. If notice

has been given, the trustee will stop the foreclosure at that point in time. No time

passes after notice of bankruptcy is received.

6. The trustee will ask the beneficiary to execute a “non-military affidavit”, or for court

proceedings, a judge would require a certificate from the military stating that the

trustor is not in the military service. The reason for this is a little known law called

the Soldiers and Sailors Civil Relief Act which may bar foreclosure of military

personnel under prescribed circumstances.

7. The trustee records the notice of default. (The beneficiary may record this document.

The law does not state that the trustee must record it.)

8. Within ten days of recording the notice of default, the trustee must mail copies of the

notice of default, by registered or certified mail, to all parties who have requested a

copy by recording a “request for special notice” with the county recorder’s office.

9. If the trustee or the beneficiary receives any money, even partial payment, foreclosure

may be stopped by the trustee even though the law is specific in allowing the

foreclosure to proceed upon partial payment.

10. If the beneficiary receives reinstatement or redemption directly from the trustor and

that amount does not include trustee’s fees, the beneficiary is responsible for that

amount to the trustee.

11. If a collection account is used, then cancel it. Once notice of default is recorded,

beneficiary should require any payment to be made to the trustee directly.

12. The trustor, successor to the trustor, or any junior lender has three months to reinstate

the loan, after the notice of default is recorded, by a payment or tender of payment of

all delinquencies, costs and fees incurred in the commencement of the foreclosure.

13. After the three month reinstatement period has elapsed, the trustee may start the

notice of sale process.

14. The notice of sale must state the time and place of sale, describe the security device,

the parties to it, the legal description and/or street address of the property that is to be

sold, the name, street address and telephone number of the trustee or any other person

conducting the sale, the terms of the sale and the kinds of money that will be accepted

at the sale, and the total amount of the unpaid balance of the obligation, including a

reasonable estimate of the costs and expenses.

15. The trustee must record the notice of sale a minimum of fourteen (14) days prior to

the sale.

16. The trustee must mail, by registered or certified mail, a copy of the notice of sale to

any interested parties a minimum of twenty-one (21) prior to the sale.

17. The trustee must publish notice of sale in a newspaper of general circulation, in the

city, county, or judicial district in which the property is located, at least once each

week for three successive weeks, with the first date of publication being at least

twenty (20) days before the date of sale.

18. The trustee must post the notice of sale in a public place in the city or judicial district

where the property is to be sold at least twenty (20) days before the date of sale. The

most common public place for this is generally the county courthouse. There is no

requirement in the law that it shall be posted at the county courthouse.

19. The trustee must post the notice of sale in some conspicuous place on the property (if

possible, on the front door) at least twenty days prior to the date of sale.

20. Substitution of a trustee after the notice of sale process starts requires new posting

and publication of notice of sale.

21. The trustee has the sole discretion to postpone the sale if he considers it necessary for

the protection of the interests of either the trustor or the beneficiary.

22. The sale must take place in the county in which the property is located but does not

have to be on the county courthouse steps.

23. The beneficiary can bid the amount of the secured obligation plus costs and charges

without having to pay additional cash. Other than given the above, he or she is

treated like any other cash bidder. He or she can bid more, or less, or not at all.

24. The trustee may require all other bidders to evidence the ability to deposit the full

amount of the bid in cash as a condition of recognizing the bid.

25. Due to a recent court decision, cashier’s checks must be accepted as the equivalent of

cash.

26. If the notice of sale states “without reserve,” the trustee must sell to the highest

bidder, regardless of the amount bid or the value of the property sold. If it is not

stated, the sale is “with reserve”. That means the trustee may withdraw the property

from sale if the highest bid, in his opinion, is inadequate.

27. Prior to declaring the property sold, the trustee may require the bidder to show the

cash for the amount bid.

28. Failure of the high cash bidder to deliver to the trustee the amount of the bid in cash,

or it’s equivalent, is a misdemeanor for which the maximum fine is $2,500.

Again, the above outline was not intended to be used as a basis for comparison as to specific

foreclosures. However, it can be used as a guideline. If an individual represents that something

must take place or cannot take place due to the “law”, the above will cover the vast majority of

laws and practices that most institutional foreclosure experts say occur most often.

THE ASSIGNMENT OF RENTS

An assignment-of-rents provision in a deed of trust (or mortgage), allows the beneficiary

to take possession of the property, collect income from it and apply the income received to the

loan balance and the costs incurred by him. An assignment-of-rents provision can take two

forms, conditional or absolute.

A conditional assignment- of- rents is a pledge of the income from property as additional

security and not an immediate assignment. The lender, therefore, has no right to income until

and unless he first obtains lawful possession of the property, either by securing consent of the

borrower or by having a court appoint a receiver. The lender cannot forcibly take possession

from the borrower or against the borrower’s will. What a conditional assignment-of-rents

amounts to is that lenders have basically two liens. One lien is on the property. The other is on

the rents produced by the property. The lender may enforce either or both. However, if he

enforces the lien on the income through a specific performance action, he may be barred from

foreclosing his lien on the real property. It is therefore advisable to not seek to enforce the

assignment- of- rents provision in a deed of trust unless you are also prepared to enforce your

rights to foreclose. If a lien against the rents is perfected by a lender taking possession, he must

exercise due care and make a reasonable effort to collect the rents. If he does not, he can be

charged for the lost rent. The lender can charge for payment of ordinary expenses necessary for

the operation of the property but not for permanent improvements unless they are essential for

the day-to-day care of the property. Unless the borrower and lender have an express agreement

providing for compensation to the lender for management expense to be paid to the lender, in the

security agreement, no compensation is provided. The lender is entitled to not only the current

rents, but also to all past due, uncollected rents. When collected, rents are applied in the

following order of priority:

1. Costs of operating and maintaining the property

2. Costs of receivership and foreclosure

3. Payment of delinquent installments including senior loans in order of priority

If the rent is sufficient to cure the default, the loan is reinstated and foreclosure and receivership

is terminated. In a conditional assignment the lender must show that the property is either:

1. In danger of being lost, removed, or materially injured, or

2. That the property itself is insufficient to discharge the debt

An absolute assignment of rents can only be created by specific, express agreement in the

security instrument. An absolute assignment creates an immediate lien on the rents without

necessity of perfecting the lien by having to take possession of the property. Courts do not like

this kind of a provision so if you are to use it, be certain the language is clear and the intention of

the parties is clearly expressed. Obviously, an attorney is the proper party to advise you of the

specific language required. In an absolute assignment a lender is entitled to income from the

point in time that he makes demand on the borrower to deliver possession and pay income to

him. The lender does not have to show jeopardy to the property to have a receiver appointed in

as much as the lien has already been perfected.

THE DEED IN LIEU OF FORECLOSURE

While it is not a common practice, there are times when a defaulting borrower conveys

the ownership of the property to a lender by way of what has come to be known as a “deed in

lieu of foreclosure”, or more simply a “deed in lieu”. By giving the lender a deed, transferring

ownership to the lender, the borrower avoids having a notice of default or a foreclosure on his

credit history. The lender benefits by the savings in costs, time and the frustration of going

through a foreclosure process. The obvious disadvantage to the borrower is that any equity

possessed by the borrower would be wiped out by a deed transfer. The major disadvantage to the

lender is that by receiving title by a deed, rather than through foreclosure, puts him in the

position of owning the property subject to any existing liens. As the high cash bidder at a

foreclosure sale, the lender would receive title free and clear of any liens. It is wise to accept a

deed in lieu of foreclosure only on the condition that a policy of title insurance will be issued

which will assure title to the lender free and clear of any liens which may exist.

Because of the possibility of an owners losing a possibly significant equity interest in his

or her property through the use of a deed in lieu of foreclosure, courts and title companies view

them with caution and suspicion. In order to insure that the transfer is valid, an analysis of the

essential elements will be undertaken.

Consideration

The deed being used in lieu of foreclosure should contain some specific mention of the

separate and independent consideration to the borrower. In other words, if the deed is given

merely to satisfy the debt, particularly when there is an equity in the property, the deed may be

contested some time in the future by the borrower. The borrower might claim, and a court might

find, that the use of the deed was merely intended as additional security to protect the lender’s

interest in the property. In one case, a bank threatened to foreclose on approximately a $75,000

loan owed on a property valued at $135,000. The borrower conveyed the property to the bank,

and the bank re-conveyed the deed of trust stating that the debt had been paid in full. Although

the court considered many factors, one of the most important was the disparity between the sales

price of $75,000 and the value, $135,000. The court held that, in this instance, the conveyance

of title merely constituted a mortgage and title was returned to the borrower.

Unconditional

When a deed is given by a borrower to a lender it is judicious to require that the deed be

absolute in form. There should be no conditions, such as the borrower retaining an option to

repurchase the property at a future date or the borrower being allowed to retain possession of the

property. In a normal transfer of title, it is highly irregular for the seller to take back an option

on a property just conveyed. Similarly, except for interim-occupancy agreements, it is unusual

for sellers to remain in possession of the property sold. When these types of situations occur,

when a deed is being used in lieu of foreclosure, they make the transaction suspect.

Estoppel Affidavit

Have the borrower execute what is called an “Estoppel Affidavit”. This is a document

which states that the conveyance is absolute and is not intended as a mortgage or other security

device and that it is the borrower’s intention to convey an absolute, complete, right, title and

interest in the property to the lender.

The law in the State of California assures borrowers of two things. First, the absolute

right to an equity of redemption. Secondly, to the greatest extent possible, preservation of a

borrower’s equity interest in the property. Because a deed in lieu of foreclosure could be used by

an unscrupulous lender to subrogate those principles, the law states that any agreement entered

into at the time the trust deed is created, which compels the borrower to convey title, by deed

upon default, is void. Generally, anyone may renounce any legal right or privilege they choose.

This right on a borrower on real property is an exception. In order to assure a valid transfer,

great care should be taken to provide evidence that the borrower has not been precluded from

redeeming and that their equity interest in the property has been protected.

THE DRAGNET CLAUSE

The “dragnet” clause is a commonly used clause in trust deeds that secures all other

obligations of the borrower, whether pre-existing or subsequent to a trust deed. As a general

rule, the beneficiary is only entitled to satisfaction of the original secured obligation. However,

the parties may agree in the security instrument that it will also include other obligations,

whether the nature of the other obligations are specified. An example of such a clause would be

as follows:

“For the purpose of securing payment of such additional amounts

as may be hereinafter loaned by beneficiary or it’s successor to

the trustor, or any successor in interest of the trustor, with interest

thereon, and any other indebtedness or obligation of the trustor, and

any present or future demands of any kind or nature which the

beneficiary or its successor may have against the trustor, whether

created directly, acquired by assignment, whether absolute or

contingent, whether due or not, or whether existing at the time

of the execution of this instrument or arising thereafter…”

Whether or not such a clause is enforceable, or if the parties expected or intended to

include debts and obligations other than the specified debt within the context of the trust deed

will be determined by the courts on an individual case by case basis. Most laymen understand

that they have a debt to pay and if they do not they will lose their property. Most laymen are

ignorant of other obligations imposed by a trust deed. A “dragnet” clause is probably the least

likely of these to be understood. If the lender can produce objective evidence that he disclosed

an intention to enforce the “dragnet” clause and the borrower acknowledged and accepted it, it

may be enforceable. The courts will probably use two tests to determine whether the clause will

be enforced. They are:

1. What was the relationship between the loans? Were they similar, or was there a

connection between them?

2. Was there a common reliance on the same security? If a newer loan is unsecured,

was it because the lender was relying on the security from the first loan?

Obviously, what the courts are going to try to do is to protect the public from a lender using a

“dragnet’ clause on an unsuspecting layman to his detriment.

THE COST TO REINSTATE SENIOR LOANS

One area of disclosure which often remains completely ignored in real estate transactions

is the cost to a junior lender to reinstate a senior loan and then the cost to foreclose on their own

loan. Often the real estate agent says something to the effect of , “If the borrower defaults on the

first trust deed, you can just reinstate it and then foreclose on your second.” A thorough

examination of what “just reinstating” a senior loan may involve is in order.

Most junior lenders do not even become aware of a default on a senior loan until months

have passed since the initial default. By that point in time, the expense involved in just making

up the past due payments may be more than the junior lender can endure. Agents are aware (and

AB 3531, effective July 1, 1983 will require) that disclosure of a lender’s right to request special

notice in the event a notice of default is recorded is essential. The problem lies in the fact that

most lenders, being reluctant to foreclose, tend to put off recording the notice of default until

months have passed since the initial default. By the time the junior lender is notified through the

request for special notice, there may be quite an amount already delinquent. In addition to the

past due payments, the junior lender will also have to be prepared to endure the future payments

to keep the senior loan current until he or she can complete their own foreclosure action. Add to

all of that the costs and charges required to be put up to cure the senior lender’s foreclosure

action, and the costs and charges to commence their own foreclosure action and, even on a

relatively small loan, you can be getting into a situation where thousands of dollars may be

required. On top of all the above, as soon as the junior lender’s foreclosure action is

commenced, there will undoubtedly be a loss of income from the loan.

Will most junior lenders be prepared to shoulder this unexpected burden? A few may be

capable. The vast majority will probably be unable to. The old adage, “Forewarned is

Forearmed” is particularly applicable in this situation. With that thought in mind, the disclosure

form on the following page is provided as an indication of what good brokerage practice might

constitute.

DISCLOSURE STATEMENT TO JUNIOR LENDERS – COST TO REINSTATE SENIOR

LOAN

1. COST TO MAKE UP PAST DUE PAYMENTS

……………………………….……$_____________

(Lenders are often reluctant to initiate foreclosure proceedings until every opportunity has

been made to allow the borrower to make payment. THIS PRACTICE MAY AFFECT

HOW MUCH IT MAY COST YOU TO REINSTATE A LOAN. You may not be notified,

officially, until the loan is many months in default. You may want to contact the senior

lender and ask that you be notified by letter when the loan first goes into default.

2. PENALTIES, COSTS, AND CHARGES TO REINSTATE

………………..….……$_____________

(Trustee’s fee, recording fees, title insurance, etc.)

3. PAYMENTS TO KEEP LOAN CURRENT DURING

FORECLOSURE……..…….$_____________

(Minimum four months)

4. COSTS AND CHARGES TO INITIATE YOUR

FORECLOSURE……………..…..$_____________

TOTAL REQUIRED TO REINSTATE & FORECLOSE ON YOUR

LOAN…..…...$_____________

5. ANTICIPATED LOSS OF INCOME FROM YOUR

LOAN……………………...…$_____________

NOTICE

THIS DOCUMENT IS NOT INTENDED TO BE A REPRESENTATION OF ACTUAL

FUTURE COSTS, BUT IS MERELY AN APPROXIMATION OF THE POTENTIAL

FINANCIAL CONSEQUENCES OF HOLDING A JUNIOR LOAN IN THE EVENT YOU

WANT TO REINSTATE A SENIOR LOAN AND FORECLOSE ON YOUR JUNIOR LOAN.

IF MORE SPECIFIC AND EXACT COSTS ARE DESIRED, OR IF YOU DESIRE LEGAL

ADVICE ON YOUR RIGHTS IN THE EVENT OF A FORECLOSURE, CONSULT YOUR

ATTORNEY

HOME EQUITY SALES CONTRACTS LAW

The Home Equity Sales Contracts Law (1695 Civil Code (1979) was designed to protect

homeowners in foreclosure from the “sharp” practices of individuals seeking to exploit them.

The law requires a written contract between “equity sellers” and “equity purchasers” on the sale

or conveyance of what is called a “residence in foreclosure”. In addition to other legal

requirements, a five day right of cancellation is required to be included in this contract. In order

to understand the law it is first necessary to define the terms used in the law.

“RESIDENCE IN FORECLOSURE” – one to four units of owner-occupied, residential

property with an outstanding notice of default.

“EQUITY PURCHASER” – any person who acquires title to a residence in foreclosure

EXCEPT:

1. if used as a personal residence

2. if transfer is by deed in lieu

3. if transfer is by trustee’s deed

3. if sale is authorized by a court of law

4. if transfer is to spouse or blood relative

“EQUITY SELLER” – any seller of a residence in foreclosure

Contract Requirements

The law requires three specific contractual devices be added to a contract in a sale

involving a residence in foreclosure; including two notices, and a duplicate, detachable “Notice

of Cancellation”. The required language for those clauses and a sample “Notice of Cancellation”

form follow:

1. The contract must contain the following notice in at least 14 point boldface type, if

printed, or in capital letters if typed.

NOTICE REQUIRED BY CALIFORNIA LAW

UNTIL YOUR RIGHT TO CANCEL THIS CONTRACT HAS ENDED

(name)

OR ANYONE WORKING

FOR______________________________________________

(name)

CANNOT ASK YOU TO SIGN OR HAVE YOU SIGN ANY DEED OR

ANY OTHER DOCUMENT.

2. Directly below that “Notice” and in immediate proximity to the space reserved for the

equity seller’s signature, the contract must contain a conspicuous statement in at least 12

point boldface type if printed, or in capital letters if typed, as follows:

YOU MAY CANCEL THIS CONTRACT FOR THE SALE OF YOUR

HOUSE WITHOUT ANY PENALTY OR OBLIGATION AT ANY TIME

BEFORE (5 days from date contract signed) (date and time of day)

SEE THE ATTACHED NOTICE OF CANCELLATION FORM FOR AN

EXPLANATION OF THIS RIGHT.

2. In addition to the preceding contractual provisions, the contract on a residence in

foreclosure shall be accompanied by a completed form, in duplicate, which is easily

detachable from the contract. It must contain the following caption: “NOTICE OF

CANCELLATION”, in at least 12 point boldface type if printed, or in capital letters if

typed:

NOTICE OF CANCELLATION

(enter date contract signed)

YOU MAY CANCEL THIS CONTRACT FOR THE SALE OF YOUR HOUSE

WITHOUT ANY PENALTY OR OBLIGATION AT ANY TIME BEFORE

______________________________________________________________________________

_______

(enter date and time of day)

TO CANCEL THIS TRANSACTION, PERSONALLY DELIVER A SIGNED AND

DATED COPY OF THIS CANCELLATION NOTICE, OR SEND A TELEGRAM TO

(name of purchaser)

AT___________________________________________________________________________

_______

(street address of purchaser’s place of business)

NOT LATER

THAN____________________________________________________________________

(enter date and time of day)

I HEREBY CANCEL THIS

TRANSACTION_______________________________________________

(date)

(seller’s signature)

Penalties

Failure to comply with any of the above contractual requirements entitles the “equity

seller” to sue for actual damages, attorney’s fees and even punitive damages.

Furthermore, equity purchasers may be liable for a fine of $10,000 and/or one year in the

county jail for any of the following:

1. If the equity purchaser, until the time from cancellation has passed:

(a) accepts or induces seller to execute a conveyance

(b) records any document signed by the equity seller

(c) pays the seller any consideration

(d) transfers or encumbers the property

2. If the purchaser, within 10 days after cancellation, does not return (without

consideration) any original contract and/or other documents

3. If the equity purchaser makes the following types of misrepresentations:

(a) untrue or misleading representations about the property’s value

(b) about an amount of proceeds from a foreclosure sale

(c) about the terms of the contract

(d) about the seller’s rights and obligations under the contract

(e) about the nature of any document the seller signs

(f) any other untrue or misleading statement

4. If the purchaser conveys interests in or encumbers the property without the seller’s

written consent, if the contract contains an option for the seller to repurchase the

property. (If there is a right to repurchase in the contract, the transaction will be

viewed as a loan transaction, not as a sale, and the purported absolute conveyance

will be viewed as a mortgage).

Unconscionable Advantage

In addition, and in a far-reaching new concept for real estate transaction law, the “equity

seller” can exercise a “Right of Recission” if it can be established that the “equity purchaser”

took “unconscionable advantage” over the “equity seller”. This “Right of Recission” lasts for

TWO YEARS after the consummation of the transaction. Obviously the legislature feels that

individuals in foreclosure situations need special protection from unscrupulous types who may

be interested in taking advantage of someone else’s misfortune. What makes this law so

monumental in terms of impact is that if the legislature feels that individuals in this situation

need the protection of a two year right of recission, then what is to stop legislators or judges from

extending the doctrine to other situations; i.e. probate sales, sales involving the extreme old, or

very young. As courts apply this law in specific situations, the impact will unfold. Certainly,

those interested in real property transactions have not heard the last of the Home Equity Sales

Contracts Law whether dealing in foreclosures or not.

UNRUH MORTGAGE ACT

Because of certain allegedly unscrupulous practices of certain home remodeling

companies, a law was passed to protect the public by imposing specific, precise regulations on

that industry. While most are not responsible under the law, or will have occasion to enter into

transactions with home remodeling companies under the circumstances described in the law, it is

important to be aware of its content. This law is an indication of the mood of the law towards

trust deeds and, more specifically, foreclosure.

One of the abuses the law sought to prevent was when a high-pressure sales tactic was

used to induce a homeowner to obligate themselves to contracts with the knowledge that the

homeowner lacked the resources to pay. Invariably, these contracts were secured by a lien on the

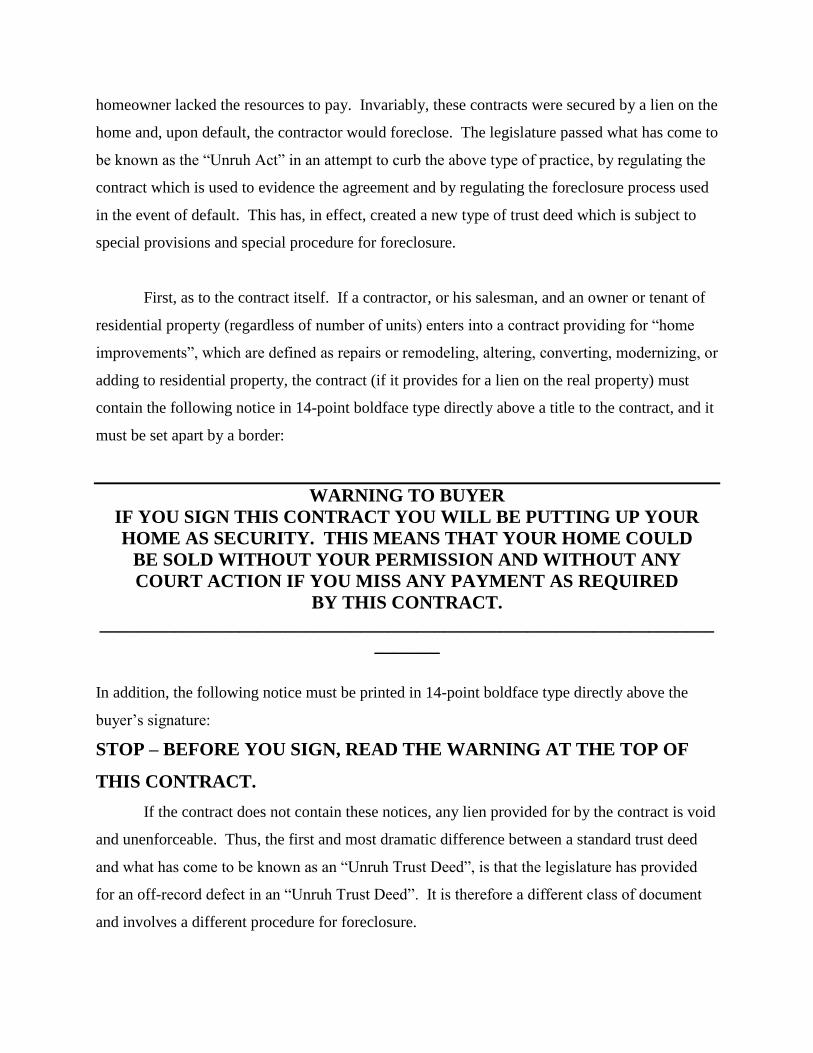

home and, upon default, the contractor would foreclose. The legislature passed what has come to

be known as the “Unruh Act” in an attempt to curb the above type of practice, by regulating the

contract which is used to evidence the agreement and by regulating the foreclosure process used

in the event of default. This has, in effect, created a new type of trust deed which is subject to

special provisions and special procedure for foreclosure.

First, as to the contract itself. If a contractor, or his salesman, and an owner or tenant of

residential property (regardless of number of units) enters into a contract providing for “home

improvements”, which are defined as repairs or remodeling, altering, converting, modernizing, or

adding to residential property, the contract (if it provides for a lien on the real property) must

contain the following notice in 14-point boldface type directly above a title to the contract, and it

must be set apart by a border:

WARNING TO BUYER

IF YOU SIGN THIS CONTRACT YOU WILL BE PUTTING UP YOUR

HOME AS SECURITY. THIS MEANS THAT YOUR HOME COULD

BE SOLD WITHOUT YOUR PERMISSION AND WITHOUT ANY

COURT ACTION IF YOU MISS ANY PAYMENT AS REQUIRED

BY THIS CONTRACT.

__________________________________________________________________

_______

In addition, the following notice must be printed in 14-point boldface type directly above the

buyer’s signature:

STOP – BEFORE YOU SIGN, READ THE WARNING AT THE TOP OF

THIS CONTRACT.

If the contract does not contain these notices, any lien provided for by the contract is void

and unenforceable. Thus, the first and most dramatic difference between a standard trust deed

and what has come to be known as an “Unruh Trust Deed”, is that the legislature has provided

for an off-record defect in an “Unruh Trust Deed”. It is therefore a different class of document

and involves a different procedure for foreclosure.

In an Unruh foreclosure, the notice of default must be recorded and mailed in the usual

manner. However, if after 30 days, the default has not been cured, the trustee must mail an

additional special notice to the trustor as follows:

YOU ARE IN DEFAULT UNDER A DEED OF TRUST DATED

______________

UNLESS YOU TAKE ACTION TO PROTECT YOUR HOME, IT MAY BE

SOLD AT A PUBLIC SALE. IF YOU NEED AN EXPLANATION OF THE

NATURE OF THE PROCEEDING AGAINST YOU, YOU SHOULD

CONTACT

A LAWYER.

With reference to the conduct of the sale, it proceeds as normal except that, in the

“Unruh”, the trustee is authorized to receive offers during a 10 day period prior to the date of the

sale. If any such offer is accepted by both the trustor and the beneficiary, the date of sale must

be postponed to a date pending a conveyance of the property. Upon the conveyance of title, the

notice of sale is deemed revoked.

THE FORECLOSURE CONSULTANTS LAW

The law (2945 Civil Code) provides for what are known as foreclosure consultants.

Foreclosure consultants are individuals who solicit, represent, or perform or offer to perform any

of the following acts:

1. Stop or postpone foreclosure sales

2. Obtain forbearance from a lender

3. Assist in reinstating a loan

4. Obtain any extension for reinstatement

5. Obtain a waiver of acceleration

6. Assist in obtaining a loan or advance of funds

7. Assist owner in avoiding impairment of credit rating

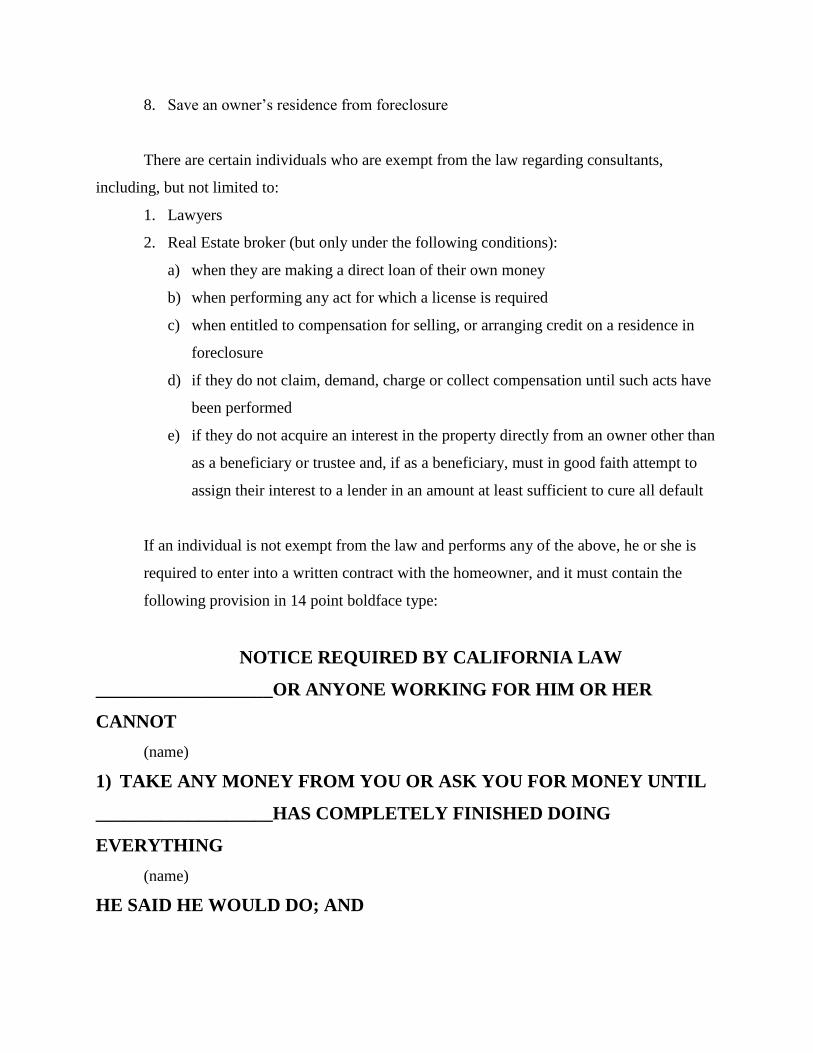

8. Save an owner’s residence from foreclosure

There are certain individuals who are exempt from the law regarding consultants,

including, but not limited to:

1. Lawyers

2. Real Estate broker (but only under the following conditions):

a) when they are making a direct loan of their own money

b) when performing any act for which a license is required

c) when entitled to compensation for selling, or arranging credit on a residence in

foreclosure

d) if they do not claim, demand, charge or collect compensation until such acts have

been performed

e) if they do not acquire an interest in the property directly from an owner other than

as a beneficiary or trustee and, if as a beneficiary, must in good faith attempt to

assign their interest to a lender in an amount at least sufficient to cure all default

If an individual is not exempt from the law and performs any of the above, he or she is

required to enter into a written contract with the homeowner, and it must contain the

following provision in 14 point boldface type:

NOTICE REQUIRED BY CALIFORNIA LAW

___________________OR ANYONE WORKING FOR HIM OR HER

CANNOT

(name)

1) TAKE ANY MONEY FROM YOU OR ASK YOU FOR MONEY UNTIL

___________________HAS COMPLETELY FINISHED DOING

EVERYTHING

(name)

HE SAID HE WOULD DO; AND

2) ASK YOU TO SIGN OR HAVE YOU SIGN ANY LIEN, DEED OF

TRUST, OR DEED.

In addition, in immediate proximity to the space reserved for the owner’s signature, a

conspicuous statement in at least 10 point boldface type is to appear as follows:

YOU, THE OWNER, MAY CANCEL THIS TRANSACTION AT ANY TIME

PRIOR TO MIDNIGHT OF THE THIRD BUSINESS DAY AFTER THE DATE

OF THIS TRANSACTION, SEE THE ATTACHED NOTICE OF

CANCELLATION

FORM FOR AN EXPLANATION OF THIS RIGHT.

The contract, in addition to having the name and address of the foreclosure consultant, and the

date the owner signed the contract, shall be accompanied by a completed form, in duplicate,

captioned “NOTICE OF CANCELLATION”, attached to the contract and easily detachable from

it, and containing in at least 10 point type the following statement:

NOTICE OF CANCELLATION

______________________

(enter date of transaction)

YOU MAY CANCEL THIS TRANSACTION, WITHOUT ANY PENALTY OR

OBLIGATION, WITHIN THREE BUSINESS DAYS FROM THE ABOVE DATE.

TO CANCEL THIS TRANSACTION, MAIL OR DELIVER A SIGNED AND

DATED COPY OF THIS CANCELLATION NOTICE, OR ANY OTHER WRITTEN

NOTICE, OR SEND A TELEGRAM TO:

(name of foreclosure consultant)

______________________________________________________________________________

_______

(address of foreclosure consultant’s place of business)

NOT LATER THAN MIDNIGHT OF_______________________

(date)

I HEREBY CANCEL THIS

TRANSACTION_________________________________________

(owner’s signature)

The following are prohibited practices by foreclosure consultants and are a violation of the law:

1. Charging or collecting any fee in advance of performing services

2. Charging in excess of 10% interest

3. Taking a lien on property to secure payment of compensation

4. Receiving undisclosed consideration from third parties

5. Acquiring an interest in a property contracted on

6. Taking a power of attorney from an owner

7. Inducing an owner to enter into a contract which does not comply with the

cancellation provisions of this law.

BANKRUPTCY

The financial circumstances that lead an individual to foreclosure also may result in that

individual’s filing for bankruptcy. Since the passage of the Bankruptcy Reform Act of 1978, the

impact of bankruptcy on foreclosure has increased tremendously. It becomes necessary,

therefore, to briefly look at it and its effect on real property transactions. Under the Bankruptcy

Reform Act there are now three forms of bankruptcy:

1. Liquidation Bankruptcy (which remains relatively unchanged from the previous law)

2. Reorganization Bankruptcy (what was previously Chapters X, XI, & XII were combined

into what is now called Chapter XI). This change is what substantially increased the

power of the bankruptcy court to affect the rights on the debtor’s property, and is

therefore where attention will be focused.(XIII Personal Bankruptcy usually exempts

home foreclosure).

To appreciate the impact of the new Bankruptcy Code on real property transactions, it is

necessary to understand the Code’s treatment of the claim of a secured creditor. A secured

creditor’s claim is divided into two parts; a secured claim, and an unsecured claim. To the extent

that the value of the collateral is in excess of the amount of the debt, the claim is a secured claim.

On the other hand, if the debt exceeds the value of the collateral, then the claim is divided into 1)

an allowed secured claim, equal to the value of the collateral; and 2) an allowed unsecured claim

in an amount equal to the deficiency.

In Reorganization Bankruptcy (Chapter XI) , an under collateralized secured creditor may elect

to have his total claim treated as a secured claim. If such election is made, the secured creditor

waives any right to a deficiency. The importance of distinguishing between secured and

unsecured claims is that if a non-recourse (one who has no right to a deficiency under the state

law, for example) elects to have his claim treated as an unsecured claim, he is entitled to a

deficiency regardless of state law or contract to the contrary, unless the property is sold at

foreclosure sale. The common impression is that bankruptcy is detrimental with regard to

foreclosure proceedings. Obviously, under certain circumstances, it might provide some benefits

to a lender.

The Automatic Stay

On the filing of a bankruptcy proceeding, any action to commence or continue a

foreclosure proceeding is automatically enjoined. The scope of this automatic stay under the

new Code is substantially broader than the previous law because of the increase in Bankruptcy

Court jurisdiction. For example, under previous law, if a secured party was in possession of the

property on the filing of a liquidation bankruptcy, the court did not have jurisdiction to deal with

the property, and the automatic stay did not prevent foreclosure. Under Chapter XI, recent

authority indicates that the automatic stay would be effective to stop foreclosure without regard

to who has possession.

Release

There are, however, two grounds by which a secured creditor can seek relief from the

automatic stay:

1. “For cause” – i.e. The lack of adequate security or protection. The problem in using

this ground is that adequate protection is not defined by the Code but is left to be

developed by case law.

2. “No equity” – If the debtor does not have any equity in the property, and the

property is not necessary to an effective reorganization. The secured creditor has the

burden of proving a debtor has no equity in the property.

Until an automatic stay is vacated, the Bankruptcy Trustee is entitled to collect the rents, issues

and profits from the property. Despite the contractual rights of the secured creditor, the

Bankruptcy Trustee can use this income for maintenance of the property, and possibly for other

administrative expenses, if the secured party is provided with adequate protection. In a

substantial change from previous law, the new Code requires a secured creditor or non-

bankruptcy received to deliver possession of property to the Bankruptcy Trustee unless the

property is of inconsequential value or benefit to the bankruptcy estate. In addition, the

Bankruptcy Trustee can borrow by granting a lien senior to existing liens if the court finds that

the secured creditor is protected.

In conclusion, while it would seem that the increased jurisdiction of the Bankruptcy Court

perpetrates a disadvantage to creditors, particularly due to the automatic stay of foreclosure

proceedings, and while a debtor could file in order to delay a foreclosure sale of his property, the

courts have held that a bankruptcy proceeding cannot be used to hinder, delay or defraud the

secured party. The case of Brown v. Pacific Thrift and Loan may evidence that point. In this

case repeated foreclosure attempts were met with repeated bankruptcies. On the third attempt at

a foreclosure sale, the Bankruptcy Court judge allowed the sale to proceed, without notice of sale

given to the borrower.