Embed Size (px)

Citation preview

333 S. Grand Ave., 18th Floor || Los Angeles, CA 90071 || (213) 633-8200

The Flexible Income Solution to the

“Unconstrained” Conundrum

December 2016

Hunter Downs, CFA

Ted Hospodar

2

Unconstrained Bond Strategies

Unconstrained Bond Strategies - December 2016

DoubleLine’s Approach to

Unconstrained Fixed Income

At Doubleline, we believe investors

should proceed cautiously when

considering an investment in

unconstrained bond strategies. That

does not mean these strategies should

be avoided entirely. Some of the

benefits of these products may

include better relative performance

over a gradually rising interest rate

environment, reduced correlation to

existing fixed income holdings, and an

ability to derive return from credit

premiums. When we launched the

DoubleLine Flexible Income Strategy

(the “Strategy”), we deliberately

avoided using the unconstrained

terminology. We believe that the

Strategy can be utilized in a well-

diversified portfolio to compliment

traditional core bond strategies

benchmarked against the Bloomberg

Barclays U.S. Aggregate Bond Index,

potentially providing a higher level of

income and taking advantage of

further opportunities with its flexible

mandate. The Strategy seeks long-

term total return through current

income and capital appreciation.

The Strategy is built upon four main

principles: the stability of our team,

active management, a longer-term

investment horizon and avoidance of

unnecessary risks.

Stability of Our Team

Asset allocation decisions within the

Strategy are made by DoubleLine’s

Fixed Income Asset Allocation

Committee (the “FIAA Committee”),

which is led by Jeffrey Gundlach and

includes senior portfolio managers

from each asset class. The FIAA

Committee meets monthly and has

worked together for over 16 years on

average. The goal is to provide better

risk-adjusted returns over a variety of

different interest-rate environments.

Active Management: Relative

Valuation Analysis

The global fixed income markets offer

a very diverse set of risk factors. Thus,

one of the key benefits of a more

flexible approach is the ability to

allocate capital to sectors of fixed

income with the most attractive risk-

adjusted return potential. We offer a

unique solution through our top-down

macro asset allocation framework in

differentiating between fixed income

subsectors to take advantage of

developing secular themes while

mitigating unnecessary risk taking.

This analysis is applied when

evaluating the diverse range of risk

factors, including market directional

risk in rates, sector spreads, relative

value risk and idiosyncratic (i.e. issuer

or bond specific) risk. The integration

of these risk factors offers greater

diversification benefits beyond

individual underlying allocations and

alleviates the duration risk factor that

is most prevalent in traditional core

bond strategies.

Benchmarking a portfolio to 3-month

LIBOR, which has a duration of about

0.25 years, rather than a traditional

fixed income index with a duration of

about five years, has the effect of

reducing the baseline for duration

exposure. Duration then becomes one

risk factor that can be employed to

generate returns, rather than the

dominant risk factor that drives

Figure 1: Traditional vs. Non-Traditional Sector Yields

As of September 30, 2016

Source: DoubleLine, Barclays Capital Index Data, S&P/LSTA Leveraged Loan Index Data, JP Morgan Research U.S. Government Securities = G0A0, International Sovereign Debt = N0G0, Agency Residential MBS = M0A0, Commercial MBS = CMBS, U.S. Investment Grade Corporates = C0A0, Emerging Markets Sovereign Debt = IGOV, Emerging Markets Corporate Debt Broad Diversified = JPM CEMBI BD, *Non-Agency RMBS = Calculated by DoubleLine, Bank Loans = S&P/LSTA, Global High Yield Corporate Debt = J0A0, **Collateralized Loan Obligations = JP Morgan Research CLO AA Post- Crisis Yield (JCLOAAYD Index). Yields may not be reached based on various factors. You cannot invest directly in an index. Past performance is no guarantee of future results.

“Non-Traditional Bond Sectors”

Sector Yield

U.S. Government Securities 1.13%

International Sovereign Debt 0.05%

Agency Residential Mortgage-Backed Securities 1.81%

Commercial Mortgage-Backed Securities 2.41%

U.S. Investment Grade Corporates 2.90%

Emerging Markets Sovereign Debt 5.15%

Emerging Markets Corporate Debt 5.38%

Non-Agency Residential Mortgage-Backed Securities* 4.25%

Bank Loans 6.01%

Global High Yield Corporate Debt 7.23%

Collateralized Loan Obligations** 3.58%

“Traditional Bond Sectors”(Barclays Capital

Aggregate Index sectors)

3

Unconstrained Bond Strategies

Unconstrained Bond Strategies - December 2016

returns and limits diversification

potential. With the yield on

government bonds and other core

bond sectors at record low levels, the

Strategy seeks to utilize a variety of

credit sectors to achieve its long run

goal. As such, cross-sector spread

analysis and deducing risk premia to

compare levels of volatility are ways

the team seek to evaluate risk factors

and time tactical shifts in the

portfolio’s risk exposures. Also, this

will allow the team to reduce the

concentration risks of unidirectional

sector or credit bets. This approach is

paramount, given credit sectors

themselves are less homogenous and

dispersion of credit value across the

sectors will present opportunities the

team can take advantage of.

Longer-Term Investment Horizon

The FIAA Committee uses a longer

time horizon when making

investment decisions, typically

between 18 and 24 months. We

believe a longer-term horizon can

increase the chance of success within

the Strategy and differentiates

DoubleLine from competing firms

that have become increasingly near

sighted leading to high portfolio

turnover. We historically will ease

into and out of the various sectors of

fixed income, making gradual

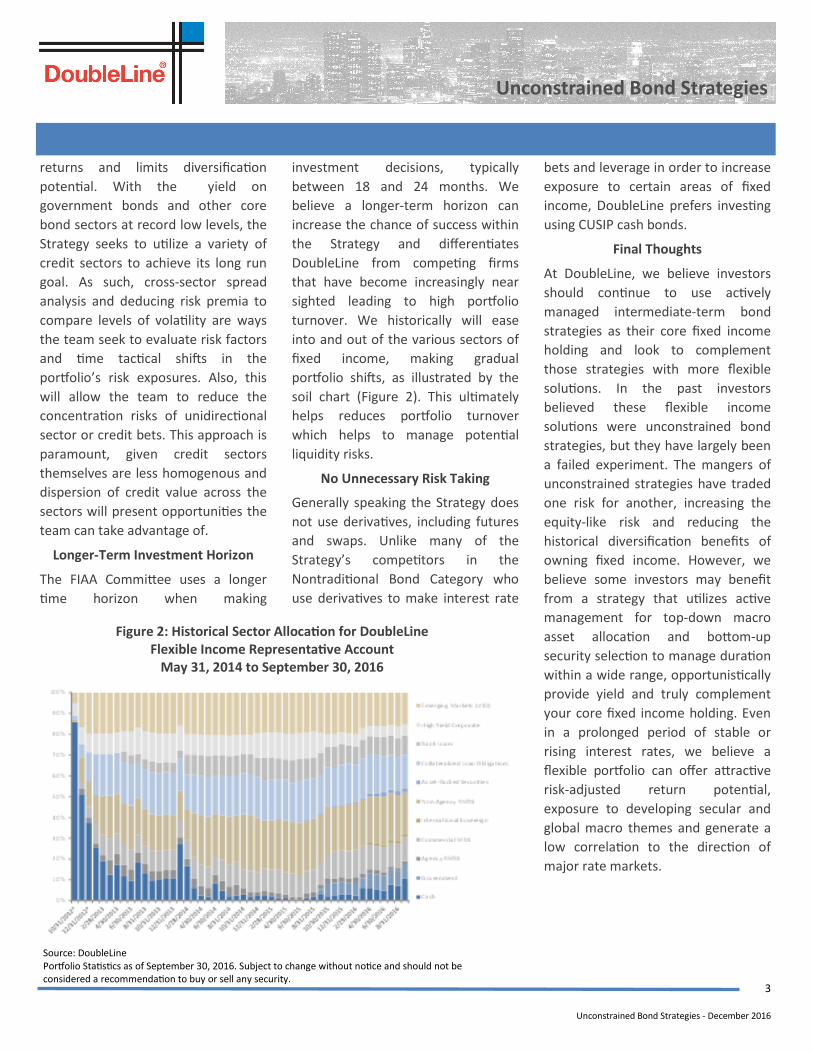

portfolio shifts, as illustrated by the

soil chart (Figure 2). This ultimately

helps reduces portfolio turnover

which helps to manage potential

liquidity risks.

No Unnecessary Risk Taking

Generally speaking the Strategy does

not use derivatives, including futures

and swaps. Unlike many of the

Strategy’s competitors in the

Nontraditional Bond Category who

use derivatives to make interest rate

bets and leverage in order to increase

exposure to certain areas of fixed

income, DoubleLine prefers investing

using CUSIP cash bonds.

Final Thoughts

At DoubleLine, we believe investors

should continue to use actively

managed intermediate-term bond

strategies as their core fixed income

holding and look to complement

those strategies with more flexible

solutions. In the past investors

believed these flexible income

solutions were unconstrained bond

strategies, but they have largely been

a failed experiment. The mangers of

unconstrained strategies have traded

one risk for another, increasing the

equity-like risk and reducing the

historical diversification benefits of

owning fixed income. However, we

believe some investors may benefit

from a strategy that utilizes active

management for top-down macro

asset allocation and bottom-up

security selection to manage duration

within a wide range, opportunistically

provide yield and truly complement

your core fixed income holding. Even

in a prolonged period of stable or

rising interest rates, we believe a

flexible portfolio can offer attractive

risk-adjusted return potential,

exposure to developing secular and

global macro themes and generate a

low correlation to the direction of

major rate markets.

Figure 2: Historical Sector Allocation for DoubleLine Flexible Income Representative Account

May 31, 2014 to September 30, 2016

Source: DoubleLine Portfolio Statistics as of September 30, 2016. Subject to change without notice and should not be considered a recommendation to buy or sell any security.

4

Definitions

Unconstrained Bond Strategies - December 2016

Bloomberg Barclays U.S. Aggregate Bond Index - An index that represents securities that are SEC-registered, taxable, and dollar denominated. The index covers the U.S.

investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securi-

ties. These major sectors are subdivided into more specific indices that are calculated and reported on a regular basis.

“U.S. Government Securities” BofA Merrill Lynch US Government Index (GOAO) - The Merrill Lynch US Government Index tracks the performance of US government (i.e.

securities in the Treasury and Agency indices.)

“International Sovereign Debt” BofA Merrill Lynch International Government Index (NOGO) - The Merrill Lynch International Index tracks the performance of Australia,

Canadian, French, German, Japan, Dutch, Swiss and UK investment grade sovereign debt publicly issued and denominated in the issuer’s own domestic market and cur-

rency. Qualifying securities must have at least one year remaining term to final maturity, a fixed coupon schedule and a minimum amount outstanding.

“Agency Residential MBS” BofA Merrill Lynch Mortgage-Backed Securities Index (MOA0) - This index tracks the performance of US dollar denominated fixed rate and

hybrid residential mortgage pass-through securities publicly issued by US agencies in the US domestic market. 30-year, 20-year, 15-year and interest only fixed rate mort-

gage pools are included in the Index provided they have at least one year remaining term to final maturity and a minimum amount outstanding of at least $5 billion per

generic coupon and $250MM per production year within each generic coupon.

“Commercial MBS” BofA Merrill Lynch U.S. Commercial Mortgage-Backed Securities Index (CMA0) - The BofA Merrill Lynch US Fixed Rate CMBS Index tracks the perfor-

mance of US dollar denominated investment grade fixed rate commercial mortgage backed securities publicly issued in the US domestic market. Qualifying securities

must have an investment grade rating (based on an average of Moody’s, S&P and Fitch), a fixed coupon schedule, at least one year remaining term to final maturity and

at least one month to the last expected cash flow.

“U.S. Investment Grade Corporates” BofA Merrill Lynch U.S. Corporate Bond Index (COAO) - The Corporate component of the U.S. Credit index. This index includes

publicly issued U.S. Corporate and specified foreign debentures and secured notes that meet the specified maturity, liquidity, and quality requirements. To qualify, bonds

must be SEC-registered.

“Emerging Markets Sovereign Debt” BofA Merrill Lynch US Dollar Emerging Markets Sovereign Plus Index (IGOV) - This index tracks the performance of US dollar

denominated emerging market and cross-over sovereign debt publicly issued in the eurobond or US domestic market. Qualifying countries must have a BB1 or lower

foreign currency long-term sovereign debt rating (based on an average of Moody’s, S&P, and Fitch).

“Emerging Markets Corporate Debt” JPMorgan Corporate EMBI Broad Diversified Index (JBCDCOMP) – This index tracks a broad basket of performance of investment

grade corporate debt, including smaller issues covering a wider array of publically issued across a range of emerging market countries.

“Bank Loans” - S&P/LSTA US Leveraged Loan 100 Index – An index designed to reflect the performance of the largest facilities in the leveraged loan market

“Global High Yield Corporate Debt” - BofA Merrill Lynch U.S. High Yield Cash Pay Index (J0A0) “Below Investment Grade” - The Merrill Lynch High Yield Index tracks the

performance of US dollar denominated below investment grade corporate debt, currently in a coupon paying period, that is publicly issued in the US domestic market.

Qualifying securities must have a below investment grade rating (based on an average of Moody’s, S&P and Firth foreign currency long term sovereign debt ratings).

Must have one year remaining to final maturity and a minimum outstanding amount of $100MM.

“Collateralized Loan Obligations” JP Morgan Research CLO AA Post- Crisis Yield (JCLOAAYD Index) - An index that captures over 3000 floating rate instruments in the

U.S. Dollar-denominated CLO market.

Duration - A measure of the sensitivity of the price of a fixed income investment to a change in interest rates, expressed as a number of years.

Yield - The income return on an investment. This refers to the interest or dividends received from a security and is usually expressed annually as a percentage based on

the investment's cost, its current market value or its face value.

One may not invest directly in an index.

5

Disclaimers

Unconstrained Bond Strategies - December 2016

Important Information Regarding This Report

Issue selection processes and tools illustrated throughout this presentation are samples and may be modified periodically. Such charts are not the only tools used by the

investment teams, are extremely sophisticated, may not always produce the intended results and are not intended for use by non-professionals.

DoubleLine has no obligation to provide revised assessments in the event of changed circumstances. While we have gathered this information from sources believed to

be reliable, DoubleLine cannot guarantee the accuracy of the information provided. Securities discussed are not recommendations and are presented as examples of

issue selection or portfolio management processes. They have been picked for comparison or illustration purposes only. No security presented within is either offered for

sale or purchase. DoubleLine reserves the right to change its investment perspective and outlook, as well as portfolio construction, without notice as market conditions

dictate or as additional information becomes available. This material may include statements that constitute “forward-looking statements” under the U.S. securities laws.

Forward-looking statements include, among other things, projections, estimates, and information about possible or future results related to a client’s account, or market

or regulatory developments.

Ratings shown for various indices reflect the average for the indices. Such ratings and indices are created independently of DoubleLine and are subject to change without

notice.

Important Information Regarding Risk Factors

Investment strategies may not achieve the desired results due to implementation lag, other timing factors, portfolio management decision-making, economic or market

conditions or other unanticipated factors. The views and forecasts expressed in this material are as of the date indicated, are subject to change without notice, may not

come to pass and do not represent a recommendation or offer of any particular security, strategy, or investment. Past performance (whether of DoubleLine or any index

illustrated in this presentation) is no guarantee of future results. You cannot invest in an index.

Important Information Regarding DoubleLine

In preparing the client reports (and in managing the portfolios), DoubleLine and its vendors price separate account portfolio securities using various sources, including

independent pricing services and fair value processes such as benchmarking.

To receive a complimentary copy of DoubleLine’s current Form ADV (which contains important additional disclosure information), a copy of the DoubleLine’s proxy voting

policies and procedures, or to obtain additional information on DoubleLine’s proxy voting decisions, please contact DoubleLine’s Client Services.

Important Information Regarding DoubleLine’s Investment Style

DoubleLine seeks to maximize investment results consistent with our interpretation of client guidelines and investment mandate. While DoubleLine seeks to maximize

returns for our clients consistent with guidelines, DoubleLine cannot guarantee that DoubleLine will outperform a client's specified benchmark. Additionally, the nature

of portfolio diversification implies that certain holdings and sectors in a client's portfolio may be rising in price while others are falling; or, that some issues and sectors

are outperforming while others are underperforming. Such out or underperformance can be the result of many factors, such as but not limited to duration/interest rate

exposure, yield curve exposure, bond sector exposure, or news or rumors specific to a single name.

DoubleLine is an active manager and will adjust the composition of client’s portfolios consistent with our investment team’s judgment concerning market conditions and

any particular security. The construction of DoubleLine portfolios may differ substantially from the construction of any of a variety of bond market indices. As such, a

DoubleLine portfolio has the potential to underperform or outperform a bond market index. Since markets can remain inefficiently priced for long periods, DoubleLine’s

performance is properly assessed over a full multi-year market cycle.

Important Information Regarding Client Responsibilities

Clients are requested to carefully review all portfolio holdings and strategies, including by comparing the custodial statement to any statements received from

DoubleLine. Clients should promptly inform DoubleLine of any potential or perceived policy or guideline inconsistencies. In particular, DoubleLine understands that

guideline enabling language is subject to interpretation and DoubleLine strongly encourages clients to express any contrasting interpretation as soon as practical. Clients

are also requested to notify DoubleLine of any updates to Client’s organization, such as (but not limited to) adding affiliates (including broker dealer affiliates), issuing

additional securities, name changes, mergers or other alterations to Client’s legal structure.

DoubleLine® is a registered trademark of DoubleLine Capital LP.

© 2016 DoubleLine Capital LP