Embed Size (px)

Citation preview

The Firm and Its Goals• The Firm• Economic Goal of the Firm• Goals Other Than Profit• Do Companies Maximize Profits?• Maximizing the Wealth of

Stockholders• Economic Profits

The Firm• A firm is a collection of resources

that is transformed into products demanded by consumers.

• Profit is the difference between revenue received and costs incurred.

Economic vs. Accounting Profits

• Accounting Profits– Total revenue (sales) minus dollar

cost of producing goods or services.– Reported on the firm’s income

statement.

• Economic Profits– Total revenue minus total opportunity

cost.

Cost• Accounting Costs

– The explicit costs of the resources needed to produce produce goods or services.

– Reported on the firm’s income statement.

• Opportunity Cost– The cost of the explicit and implicit

resources that are foregone when a decision is made.

• Economic Profits– Total revenue minus total opportunity

cost.

Economic Goal of the Firm

• Primary objective of the firm (to economists) is to maximize profits.– Profit maximization hypothesis– Other goals include market share,

revenue growth, and shareholder value

• Optimal decision is the one that brings the firm closest to its goal.

• Short-run vs. Long-run

– Nothing to do directly with calendar time

– Short-run: firm can vary amount of some resources but not others

– Long-run: firm can vary amount of all resources

At times short-run profitability will be sacrificed for long-run purposes

Goals Other Than Profit– Market share maximization (as

measured by sales revenue or proportion of quantity sold to total market

– Growth rate maximization (increasing size of the firm over time. Higher rates of growth in other variables than profit)

– Profit margin

– Return on investment, Return on assets

– Shareholder value

– Technological advancement

– Customer satisfaction

– Maximization of managerial returns (manager’s own interest subject to generating sufficient profits to keep their jobs)

• Non-economic Objectives

– Good work environment

– Quality products and services

– Corporate citizenship, social responsibility

Do Companies Maximize Profit?

• Criticism: Companies do not maximize profits but instead their aim is to “satisfice.”

– “Satisfice” is to achieve a set goal, even though that goal may not require the firm to “do its best.”

– Two components to “satisficing”:• Position and power of stockholders• Position and power of professional

management

• Position and power of stockholders

– Medium-sized or large corporations are owned by thousands of shareholders

– Shareholders own only minute interests in the firm

– Shareholders diversify holdings in many firms

– Shareholders are concerned with performance of entire portfolio and not individual stocks.

– Most stockholders are not well informed on how well a corporation can do and thus are not capable of determining the effectiveness of management.

– Not likely to take any action as long as they are earning a “satisfactory” return on their investment.

• Position and power of professional management

– High-level managers who are responsible for major decision making may own very little of the company’s stock.

– Managers tend to be more conservative because jobs will likely be safe if performance is steady, not spectacular.

– Management incentives may be misaligned• E.g. incentive for revenue growth, not

profits• Managers may be more interested in

maximizing own income and perks

– Divergence of objectives is known as “principal-agent” problem or “agency problem”

• Counter-arguments which support the profit maximization hypothesis.

– Large number of shares is owned by institutions (mutual funds, banks, etc.) utilizing analysts to judge the prospects of a company.

– Stock prices are a reflection of a company’s profitability. If managers do not seek to maximize profits, stock prices fall and firms are subject to takeover bids and proxy fights.

– The compensation of many executives is tied to stock price.

• Company tries to manage its business in such a way that the dividends over time paid from its earnings and the risk incurred to bring about the stream of dividends always create the highest price for the company’s stock.

• When stock options are substantial part of executive compensation, management objectives tend to be more aligned with stockholder objectives.

Maximizing the Wealth of Stockholders

• Views the firm from the perspective of a stream of earnings over time, i.e., a cash flow.

• Must include the concept of the time value of money.

– Dollars earned in the future are worth less than dollars earned today.

• Future cash flows must be discounted to the present.

• The discount rate is affected by risk.

• Two major types of risk:•Business Risk•Financial Risk

• Business risk involves variation in returns due to the ups and downs of the economy, the industry, and the firm.

• All firms face business risk to varying degrees.

• Financial Risk concerns the variation in returns that is induced by leverage.

• Leverage is the proportion of a company financed by debt.

• The higher the leverage, the greater the potential fluctuations in stockholder earnings.

• Financial risk is directly related to the degree of leverage.

Timing

2 types of models1.Static model:– describe the

behaviour at a single point in time. Disregards differences in the sequence of actions and payments

2.Dynamic models:- focus on the timing and sequence of actions and payments

The Time Value of Money

• Present value (PV) of a lump-sum amount (FV) to be received at the end of “n” periods when the per-period interest rate is “i”:

PV

FV

i n1

• .

• Examples:– Lotto winner choosing between a single

lump-sum payout of $104 million or $198 million over 25 years.

– Determining damages in a patent infringement case

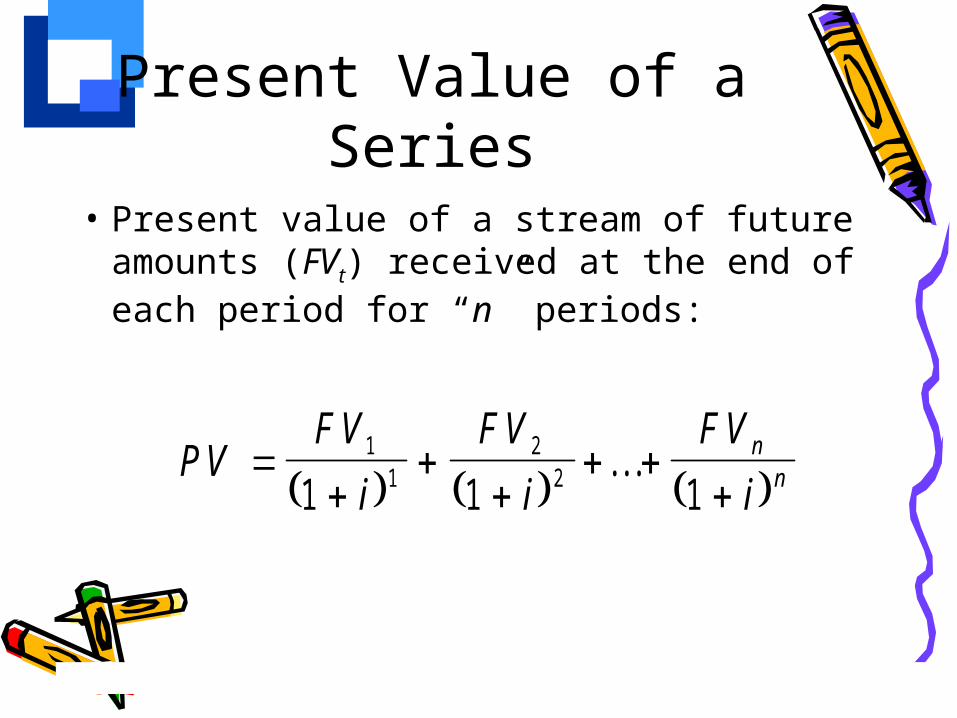

Present Value of a Series

• Present value of a stream of future amounts (FVt) received at the end of each period for “n” periods:

PV

FV

i

FV

i

FV

inn

1

12

21 1 1. . .

Net Present Value• Suppose a manager can purchase a stream of

future receipts (FVt ) by spending “C0” dollars today. The NPV of such a decision

Is

NPV

FV

i

FV

i

FV

iCn

n

11

22 01 1 1

. . .

Decision Rule:If NPV < 0: Reject project

NPV > 0: Accept project

Present Value of a Perpetuity

• An asset that perpetually generates a stream of cash flows (CF) at the end of each period is called a perpetuity.

• The present value (PV) of a perpetuity of cash flows paying the same amount at the end of each period is

i

CF

i

CF

i

CF

i

CFPVPerpetuity

...111 32

Firm Valuation

• The value of a firm equals the present value of current and future profits.– PV = t / (1 + i)t

• If profits grow at a constant rate (g < i) and current period profits are :

0

0

1 before current profits have been paid out as dividends;

1 immediately after current profits are paid out as dividends.

Firm

Ex DividendFirm

iPV

i g

gPV

i g

• If the growth rate in profits < interest rate and both remain constant, maximizing the present value of all future profits is the same as maximizing current profits.

• Control Variables– Output– Price– Product Quality– Advertising– R&D

Marginal (Incremental) Analysis

Net Benefits

• Basic Managerial Question: How much of the control variable should be used to maximize net benefits?

• Net Benefits = Total Benefits - Total Costs

• Profits = Revenue - Costs

Marginal Benefit (MB)

• Change in total benefits arising from a change in the control variable, Q:

• Slope (calculus derivative) of the total benefit curve.

Q

BMB

Marginal Cost (MC)

• Change in total costs arising from a change in the control variable, Q:

• Slope (calculus derivative) of the total cost curve

Q

CMC

Marginal Principle• To maximize net benefits, the

managerial control variable should be increased up to the point where MB = MC.

• MB > MC means the last unit of the control variable increased benefits more than it increased costs.

• MB < MC means the last unit of the control variable increased costs more than it increased benefits.

The Geometry of Optimization

Q

Total Benefits & Total Costs

Benefits

Costs

Q*

B

CSlope = MC

Slope =MB

Conclusion• Make sure you include all costs and

benefits when making decisions (opportunity cost).

• When decisions span time, make sure you are comparing apples to apples (PV analysis).

• Optimal economic decisions are made at the margin (marginal analysis).

Maximizing the Wealth of Stockholders

• Another measure of the wealth of stockholders is called Market Value Added (MVA)®.

• MVA represents the difference between the market value of the company and the capital that the investors have paid into the company.

Maximizing the Wealth of Stockholders

• Market value includes value of both equity and debt.

• Capital includes book value of equity and debt as well as certain adjustments.– E.g. Accumulated R&D and goodwill.

• While the market value of the company will always be positive, MVA may be positive or negative.

Maximizing the Wealth of Stockholders

• Another measure of the wealth of stockholders is called Economic Value Added (EVA)®.– EVA=(Return on Total Capital – Cost of

Capital) x Total Capital

• If EVA is positive then shareholder wealth is increasing. If EVA is negative, then shareholder wealth is being destroyed.