Embed Size (px)

Citation preview

Gabriel Buck

MD, Head of ECA & Capex

Financing Solutions Group

5 The North Colonnade

Canary Wharf

London E14 4BB

United Kingdom

Tel +44 (0) 20 777 34092

Fax +44 (0) 20 751 67502

Mobile +44 (0) 7767 374323

OECD 7th Forum on African Public Debt Management

The Financing of Infrastructure Development

1

USD 45bn spent in Africa on infrastructure every year

USD 75bn required to be spent every year to redress Africa‟s infrastructure deficit

Bank funding alone will not suffice

Financing will remain a major challenge

USD 93bn p.a. needed until 2020 for Africa to break even their infrastructure deficit

Even scaling up of infrastructure financing from the traditional sources, including taxes,

government borrowing and aid, will not suffice

World Bank Reports:

African Development Bank Reports:

2

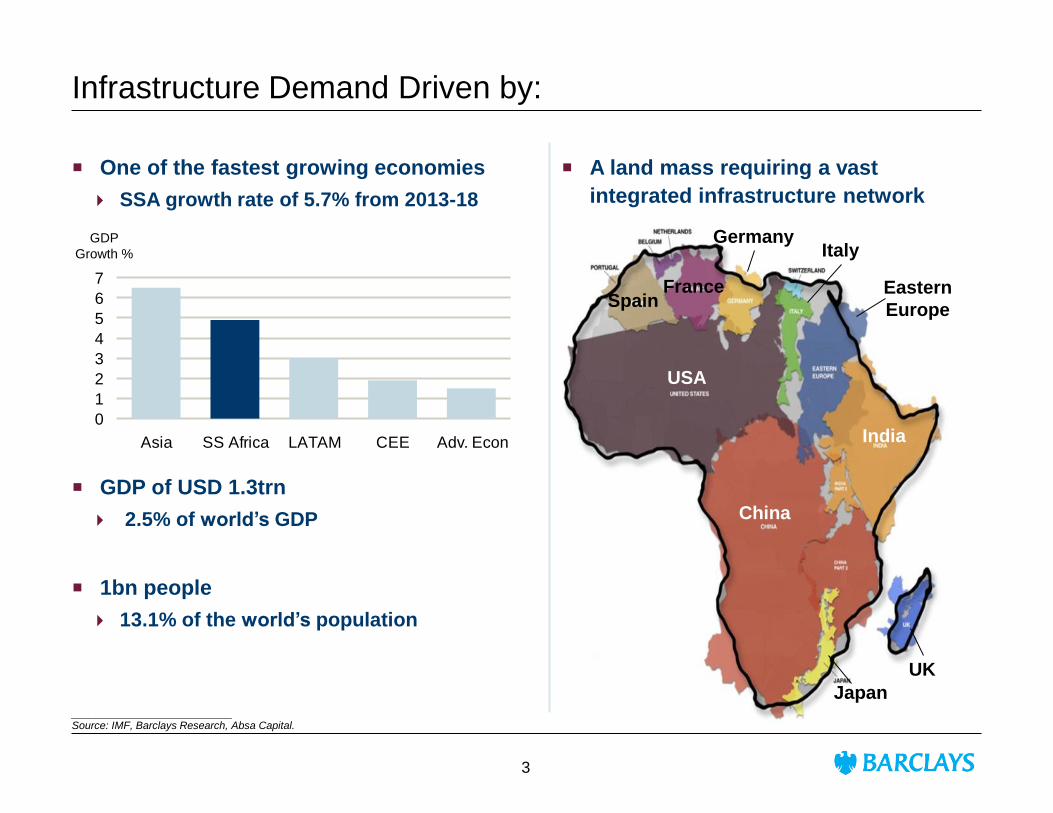

Infrastructure Demand Driven by:

One of the fastest growing economies

SSA growth rate of 5.7% from 2013-18

GDP of USD 1.3trn

2.5% of world‟s GDP

1bn people

13.1% of the world‟s population

GDP

Growth %

USA

China

India

UK

Eastern

Europe Spain

France

Germany Italy

Japan

A land mass requiring a vast

integrated infrastructure network

___________________________ Source: IMF, Barclays Research, Absa Capital.

0

1

2

3

4

5

6

7

Asia SS Africa LATAM CEE Adv. Econ

3

0.0 0.2 0.4 0.6 0.8

Paved roads

Total roads

Fixed lines

Mobile

Internet

Electricity capacity

Electricity coverage

Africa infrastructure shortfall is glaring, even

when comparing to other low-income

countries

Africa Infrastructure

___________________________ Sources: AICD, NASA, Absa.

4

Sources: Africa Project Access, Business Monitor International, Ernst & Young, Absa

Understanding where the money is going

0 10 20 30 40

Power

Roads/bridges

Rail

Water

Airports

Ports

Comm constr

Ind constr

Oil/gas pipe

Housing

Healthcare

Resid constr

Education

% capital

% projects

0 50 100

South Africa

Nigeria

Egypt

Uganda

Kenya

Algeria

Mozambique

Libya

Tanzania

Cameroon

$bn

# Projects

Africa Infrastructure

Active projects, by sector Active projects, by country

___________________________ Sources: Africa Project Access, Business Monitor International, Ernst & Young, Absa.

5

Govt of Ghana

USD 175m

ECGD-backed facility

7 district hospitals

October 2012

Despite the enormity of the scale, major CapEx programmes are getting done

Transnet

ZAR 78bn

Umbrella Structured

ECA Facility

Sole Advisor/Arranger

2007-2012

TAAG

USD 580m

Financing of

7 Boeing

Arranger & Agent

2006-2007

South African Airways

USD 345m

Financing of

3 Airbus

Arranger & Agent

2003

SANRAL

USD 1.0bn

Umbrella Structured

ECA Facility

Sole Advisor/Arranger

2009-2014

Govt of South Africa

NT1,2,3

USD 2.6bn

Re-Structured

Multicurrency

ECGD Facility

Sole Advisor & MLA

2000-2020

Xstrata South Africa

USD 1.0bn

ECA Backed Facility

2x150MW Power Plant

UNDER MANDATE

Govt of Ghana

USD 101m

ECIC-backed facility

SHEP4 Programme

Arranger and Lender

2012

Ghana Cocoa Board

USD 200m

Medium Term

Trade Finance Facility

Initial MLA/Bookrunner

2012

Ghana Cocoa Board

USD 1.5bn

Short Term

Trade Finance Facility

Initial Lead Arranger

2012

PROJECT

SEAGOLD

USD 100m

Financing of 13 fixed

& rotary wing aircraft

Arranger & Agent

2005-2006

Sonangol

USD 2.5bn

Syndicated Loan

Joint MLA

2008

Telkom

USD 1.6bn

Umbrella Structured

ECA Facitliy

Sole Advisor /Arranger

2010-2015

Mainstream

USD 1.0bn

ECA Backed Facility

7 Renewables Projects

UNDER MANDATE

Ghana

South Africa Govt of Zambia

Up to USD 2.8bn

Umbrella Structured

ECA Facility

UNDER MANDATE

PROJECT

MAAMBA

USD 540m

ECA-backed facility

2x150MW Power Plant

UNDER MANDATE

Zambia

Angola

Natura Energy

USD 150m

ECA Backed Facility

HFO Power Plant

UNDER MANDATE

Namibia

Shaft Sinkers

USD 260m ECIC

Backed Facility

Sole Adviser

&Bookrunner

2010

Govt of Tanzania

USD 1.0bn

Umbrella Structured

ECA Facility

UNDER MANDATE

Govt of Tanzania

USD 40m

Structured L/C and

Loan facility

Lead Arranger / Agent

2000

Tanzania

Sasol New Energy

Advisory for

Financing of

Gas power plant

UNDER MANDATE

Mozambique

Royal Air Maroc

USD 470m

Financing of

5 Boeing & 2 Airbus

Arranger & Agent

2007-2008

Morocco

EgyptAir

USD 430m

Financing of

5 Boeing

Arranger & Agent

2002 - 2008

Egypt

Ethiopian Airlines

USD 300m

Financing of

3 Boeing

Arranger & Agent

2003

Ethiopia

Kenya Airways

USD 430m

Financing of

5 Boeing

Arranger & Agent

2002 - 2008

Kenya

Kenya Electricity

Generating Company

USD 5bn

Financial Advisor and

Arranger Services

UNDER MANDATE

Liqhobong

Diamond Project

USD 75m

ECIC-Backed

Project Finance

UNDER MANDATE

Lesotho

C&I Leasing

USD 4.4m

ECIC Facility

Crew transport vessels

Arranger & Agent

2013

Nigeria

Makomo Resources

USD 10m

SMT ECIC backed

financing

Arranger & Agent

2012

Zimbabwe

6

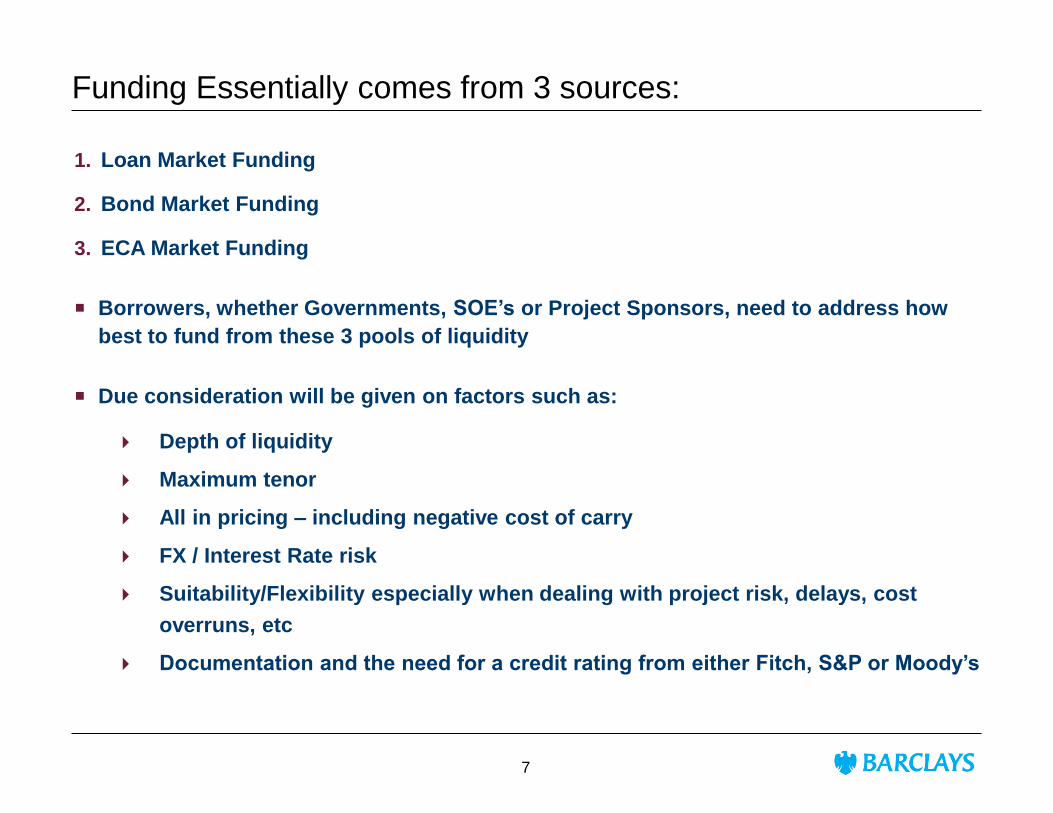

Funding Essentially comes from 3 sources:

1. Loan Market Funding

2. Bond Market Funding

3. ECA Market Funding

Borrowers, whether Governments, SOE‟s or Project Sponsors, need to address how

best to fund from these 3 pools of liquidity

Due consideration will be given on factors such as:

Depth of liquidity

Maximum tenor

All in pricing – including negative cost of carry

FX / Interest Rate risk

Suitability/Flexibility especially when dealing with project risk, delays, cost

overruns, etc

Documentation and the need for a credit rating from either Fitch, S&P or Moody‟s

7

Loan Markets: International Project Finance: Volumes are down

The global project finance loan market fell back 7%

last year to $198.7bn in 2012

Throughout 2012, a common theme was the fact

that eurozone banks had limited lending

capacity

Deal flow in the eurozone fell back as austerity bit

Volumes in EMEA region fell by 18.5% to $67.9bn

Into 2013, EMEA deal flow remains constrained

The proportion of capital provided by European

banks continues on its downward trend

Liquidity issues and higher pricing were primarily a

result of:

Increased regulatory requirements which have

increased bank capital requirements and

reduced lending capacity

Higher bank funding costs, and a move towards

matching funding with tenor of underlying

assets

___________________________ Source: Dealogic, Project Finance International.

EMEA project finance volumes

0

50,000

100,000

150,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

$mn

0

200

400

600

No. Deals

EM EA loan volumes No. of deals

EMEA project finance loans – 2007YTD

0

25

50

75

100

125

150

2007 2008 2009 2010 2011 2012

$bn

0%

10%

20%

30%

40%

50%

60%

70%

Market Share

IT/FR/ESP/POR UK & Ireland

Continental & Nordic CIS

Japan Other

IT/FR/ESP/POR market share

Commentary

The dynamics are evolving

8

Loan Markets: Domestic Bank Markets: Single Lending Capacity

Capital reserves determines each bank‟s

single lending capacity

Even for the South African market,

capacity is not big enough to fund mega

infrastructure projects

Top 20 RSA bank aggregate single

lending capacity is USD 7.2bn

For USD 250m-300m sized projects, loan

market funding now dependant on

multiple banks forming a syndication

This data reinforcing African

Development Bank report that bank

funding will not suffice

Just taking South Africa as an example:

___________________________ BA900 Returns for Mar 2013. FX – ZAR:USD 0.098 as of 21/06/2013.

Institution

Total Capital

Reserve (less

impairments)

R‟000

Single

lending

capacity

R‟000

THE STANDARD BANK OF S A LTD 71,137,334 17,784,333.50

ABSA BANK LTD 57,589,691 14,397,422.75

FIRSTRAND BANK LIMITED 54,875,293 13,718,823.25

NEDBANK LTD 44,937,989 11,234,497.25

INVESTEC BANK LTD 20,392,451 5,098,112.75

AFRICAN BANK LIMITED 13,029,258 3,257,314.50

CAPITEC BANK 8,439,237 2,109,809.25

CITIBANK N.A 4,490,619 1,122,654.75

JPMORGAN CHASE BANK 2,650,000 662,500.00

STANDARD CHARTERED BANK 2,068,226 517,056.50

THE HK & SHANGHAI BANKING CORP 1,866,371 466,592.75

BIDVEST BANK LIMITED 1,821,468 455,367.00

MERCANTILE BANK LTD 1,679,089 419,772.25

BANK OF CHINA LTD JHB BRANCH 1,608,023 402,005.75

CHINA CONSTRUCTION BANK 1,345,868 336,467.00

DEUTSCHE BANK AG 1,302,168 325,542.00

STATE BANK OF INDIA 751,685 187,921.25

SASFIN BANK LTD 599,796 149,949.00

UBANK LIMITED 539,841 134,960.25

GRINDROD BANK LIMITED 526,374 131,593.50

Total R’000 292,132,080 73,033020

Total USD ‘000 28,628,944 7,157,236

9

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

12.0

13.0

14.0

15.0

Nov-07 Jan-09 Apr-10 Jul-11 Oct-12

(%)

US credit EM credit

Bond Market: Substantial Growth in recent years

With emerging markets growth hitting record levels

0

1,000

2,000

3,000

4,000

5,000

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12'13ytd

USDbn

0%

3%

6%

9%

12%

15%

Global EM as % of global issuance (RHS)

___________________________ Source: Barclays, Bloomberg, April 2013.

Global new issue market overview Credit spreads have compressed

10

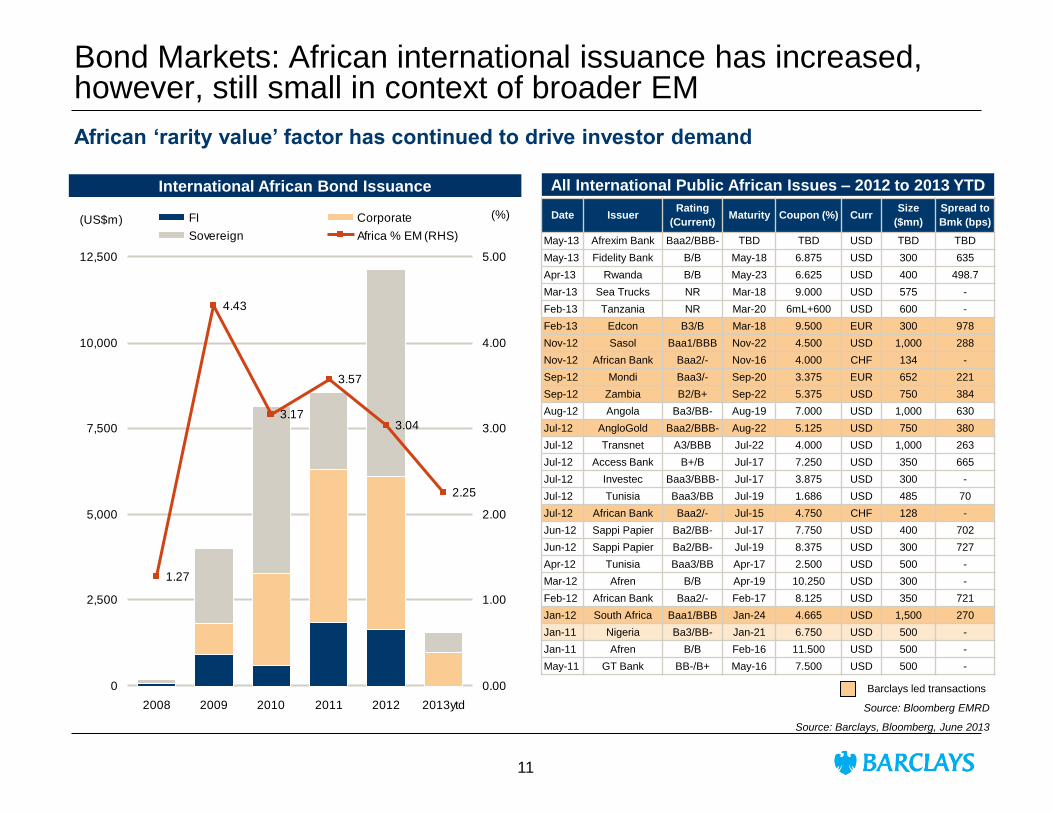

African „rarity value‟ factor has continued to drive investor demand

Bond Markets: African international issuance has increased, however, still small in context of broader EM

1.27

4.43

3.17

3.57

3.04

2.25

0

2,500

5,000

7,500

10,000

12,500

2008 2009 2010 2011 2012 2013ytd

(US$m)

0.00

1.00

2.00

3.00

4.00

5.00

FI Corporate

Sovereign Africa % EM (RHS)

(%) Date Issuer Rating

(Current) Maturity Coupon (%) Curr

Size

($mn)

Spread to

Bmk (bps)

May-13 Afrexim Bank Baa2/BBB- TBD TBD USD TBD TBD

May-13 Fidelity Bank B/B May-18 6.875 USD 300 635

Apr-13 Rwanda B/B May-23 6.625 USD 400 498.7

Mar-13 Sea Trucks NR Mar-18 9.000 USD 575 -

Feb-13 Tanzania NR Mar-20 6mL+600 USD 600 -

Feb-13 Edcon B3/B Mar-18 9.500 EUR 300 978

Nov-12 Sasol Baa1/BBB Nov-22 4.500 USD 1,000 288

Nov-12 African Bank Baa2/- Nov-16 4.000 CHF 134 -

Sep-12 Mondi Baa3/- Sep-20 3.375 EUR 652 221

Sep-12 Zambia B2/B+ Sep-22 5.375 USD 750 384

Aug-12 Angola Ba3/BB- Aug-19 7.000 USD 1,000 630

Jul-12 AngloGold Baa2/BBB- Aug-22 5.125 USD 750 380

Jul-12 Transnet A3/BBB Jul-22 4.000 USD 1,000 263

Jul-12 Access Bank B+/B Jul-17 7.250 USD 350 665

Jul-12 Investec Baa3/BBB- Jul-17 3.875 USD 300 -

Jul-12 Tunisia Baa3/BB Jul-19 1.686 USD 485 70

Jul-12 African Bank Baa2/- Jul-15 4.750 CHF 128 -

Jun-12 Sappi Papier Ba2/BB- Jul-17 7.750 USD 400 702

Jun-12 Sappi Papier Ba2/BB- Jul-19 8.375 USD 300 727

Apr-12 Tunisia Baa3/BB Apr-17 2.500 USD 500 -

Mar-12 Afren B/B Apr-19 10.250 USD 300 -

Feb-12 African Bank Baa2/- Feb-17 8.125 USD 350 721

Jan-12 South Africa Baa1/BBB Jan-24 4.665 USD 1,500 270

Jan-11 Nigeria Ba3/BB- Jan-21 6.750 USD 500 -

Jan-11 Afren B/B Feb-16 11.500 USD 500 -

May-11 GT Bank BB-/B+ May-16 7.500 USD 500 -

Barclays led transactions

All International Public African Issues – 2012 to 2013 YTD International African Bond Issuance

Source: Bloomberg EMRD

Source: Barclays, Bloomberg, June 2013

11

Bond Markets: Zambia’s Recent Inaugural Bond

A good example: where there is appetite – tap it

Initial issue at USD 500m

Upsized to USD 750m due to strong demand

56% of investors from the USA

16 times oversubscribed – investor appetite reached c. USD 12bn

10 year bond at a coupon of 5.375% - lower than that of the Kingdom of Spain

Have in mind:

1. Be prepared. The window may not always be open. It is susceptible to periods of

market weakness. Important to be ready to launch to take advantage of market

strengths

2. Bond Market funding may not always be appropriate for infrastructure financing given

the negative cost of carry

“Zambia - Investors clamour for debut bond”

“Zambia's record-breaking Eurobond rises in

first day trade”

“Review: Zambia gets blowout response on

USD debut”

12

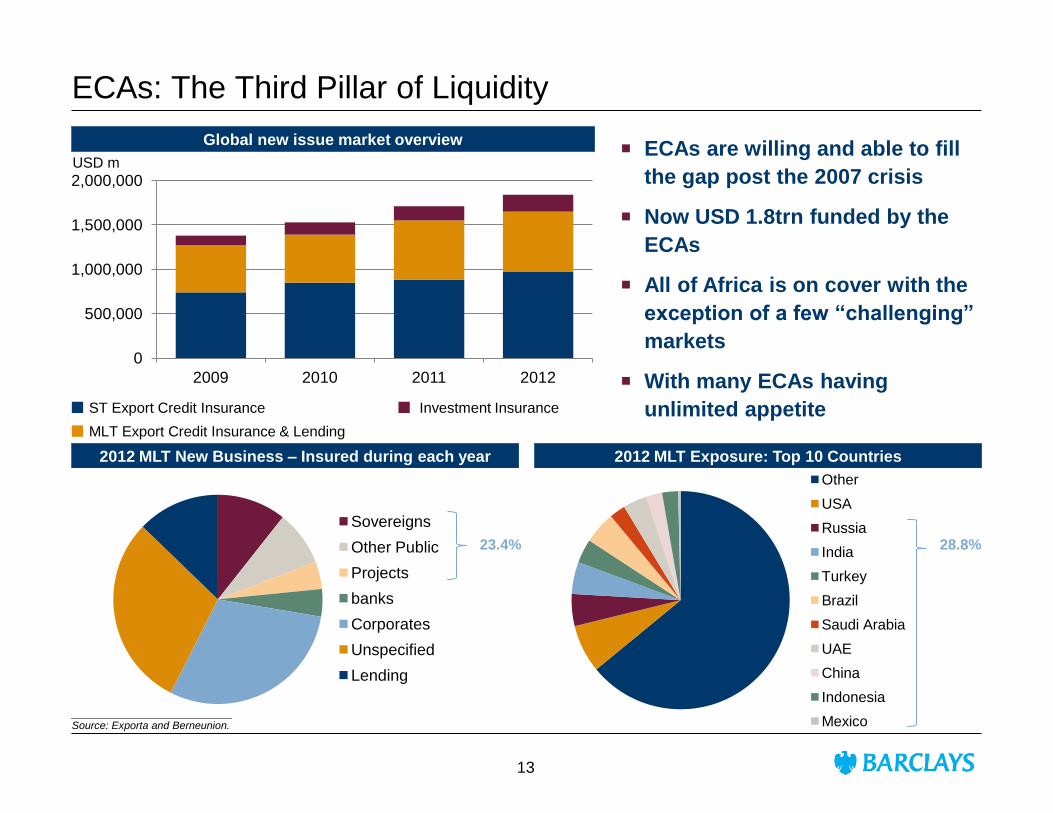

ECAs: The Third Pillar of Liquidity

ECAs are willing and able to fill

the gap post the 2007 crisis

Now USD 1.8trn funded by the

ECAs

All of Africa is on cover with the

exception of a few “challenging”

markets

With many ECAs having

unlimited appetite

0

500,000

1,000,000

1,500,000

2,000,000

2009 2010 2011 2012

Global new issue market overview

Sovereigns

Other Public

Projects

banks

Corporates

Unspecified

Lending

Other

USA

Russia

India

Turkey

Brazil

Saudi Arabia

UAE

China

Indonesia

Mexico

2012 MLT New Business – Insured during each year 2012 MLT Exposure: Top 10 Countries

___________________________ Source: Exporta and Berneunion.

USD m

23.4%

ST Export Credit Insurance

MLT Export Credit Insurance & Lending

Investment Insurance

28.8%

13

Key Benefits

ECAs are under lent to Africa

Many are extremely keen to do more and can provide FX & interest rate flexibility

Eligibility to tap ECAs is high as a significant % of Africa Infrastructure is imported

Don’t forget the 3 L’s:

Low margins: cheaper than the bank or bond markets and limited to no cost of carry

Longer tenors: build period + 18 years possible

Liquidity: separate pool & no crowd out

But preposition is key

ECA’s remit is to support exporters win contracts

It is therefore important to start negotiations with ECAs before the commercial contract is

signed

It is complex and it is never too early to start the process

ECA’s provide some key advantages For African Infrastructure Projects

14

ECA: Ghana’s New Benchmark ECA Financing

Government of Ghana

USD 175m

Financing of District Hospitals

Coordinating MLA

Issuing / LC bank

Bookrunner

Agent

Lender of GHS 55m uncovered portion

MLA and lender of ECA portion

MLA and lender of ECA portion

ECA

International law firm

Local law firm

October 2012

12.5 years USD funding with an all-in

cost of 3.72%

From mandate to close in 8 months

7 Hospitals

Integrated financing solution

Tender Panel providing an open and

transparent funding mechanism

Providing an all in cost that achieves

affordability criteria without aid / donor

support

15

Depth of liquidity

Maximum tenor

All in pricing

Low cost of negative carry

Flexibility to cover project risk

FX / Interest Rate flexibility

Ratings requirements

In summary:

In Summary: Tap all 3 in a balanced way

Loan Market Bond Market ECA Market

Not Required

Not Required

Required

Flexibility & local

cost funding

Tenor & depth of

appetite

Can attract liquidity

Susceptible to

periods of market

weakness

Cheapest & attracts

liquidity

Prepositioning and

limited to Goods &

Services imported

16

Disclaimer all ex Ita,MEast This document has been prepared by Barclays Bank PLC, acting through its investment bank (“Barclays”), for information purposes only. This document is an indicative summary of the terms and conditions of the securities/transaction described herein and may be amended, superseded or replaced by subsequent summaries. The final terms and conditions of the transaction and any related security will be set out in full in the applicable transaction confirmation, offering document(s), pricing supplement or binding transaction document(s).

This document shall not constitute an underwriting commitment, an offer of financing, an offer to buy or sell, or the solicitation of an offer to buy or sell any securities described herein, which shall be subject to Barclays’ internal approvals. No transaction or service related thereto is contemplated without Barclays’ subsequent formal agreement.

Barclays is acting solely as principal and not as advisor or fiduciary. Barclays does not provide, and has not provided, any investment advice or recommendation to you in relation to the transaction and/or any related securities described herein and is not responsible for providing or arranging for the provision of any general financial, strategic or specialist advice, including legal, regulatory, accounting, model auditing or taxation advice or services or any other services in relation to the transaction and/or any related securities described herein. Accordingly Barclays is under no obligation to, and shall not, determine the suitability for you of the transaction described herein. You must determine, on your own behalf or through independent professional advice, the merits, terms conditions and risks of the transaction described herein. You must also satisfy yourself that you are capable of assuming, and assume the risks of any such transaction. Neither Barclays nor any of its subsidiaries, affiliates or ultimate holding company, nor any of the subsidiaries or affiliates of such holding company (the“ Barclays Group”), nor any of their respective directors, officers, employees, representatives or agents, accepts any liability whatsoever for any direct, indirect or consequential losses (in contract, tort or otherwise) arising from the use of this document or its contents or reliance on the information contained herein.

Barclays does not guarantee the accuracy or completeness of information which is contained in this document and which is stated to have been obtained from or is based upon trade and statistical services or other third party sources. Any data on past performance, modelling, scenario analysis or back-testing contained herein is no indication as to future performance. No representation is made as to the reasonableness of the assumptions made within or the accuracy or completeness of any modelling, scenario analysis or back-testing. All opinions and estimates are given as of the date hereof and are subject to change. The value of any investment may fluctuate as a result of market changes. The information in this document is not intended to predict actual results and no assurances are given with respect thereto.

Barclays is a full service securities firm engaged in a wide range of businesses and from time to time, in the ordinary course of its business, Barclays and/or other parts of the Barclays Group may hold long or short positions and trade or otherwise effect transactions for their own account or the account of their customers in the securities referred to herein and/or the debt or equity securities, assets or loans (or any derivatives thereof) of the companies referred to herein. Additionally, Barclays and/or other parts of the Barclays Group may have investment and commercial banking, lending, asset management and other relationships with parties which are or may become involved in the transactions referred to herein and/or which may have interests which could potentially conflict with the interests of the recipient hereof. Barclays and/or other parts of the Barclays Group have in place policies and procedures to restrict the flow of information and to identify, consider and manage such potential conflicts of interest. Accordingly, you acknowledge and agree that no part of the Barclays Group is required to restrict its activities as a result of the provision of this document, and that all parts of the Barclays Group may undertake any activities without further consultation with or notification to you. Barclays shall not be required to account to you for any revenue or profits obtained in connection with any activities of the Barclays Group as referred to herein.

Barclays’ research analysts and research departments are independent from Barclays’ investment banking division and are subject to certain regulations and internal policies. Barclays’ research analysts may hold and make statements or investment recommendations and/or publish research reports with respect to any company referred to herein, the transactions contemplated herein or any person involved therein or related thereto that differ from or are inconsistent with the views or advice communicated by Barclays’ investment banking division.

Barclays Bank PLC is authorised and regulated by the UK Financial Services Authority and a member of the London Stock Exchange. Barclays Bank PLC is registered in England No. 1026167. Registered Office: 1 Churchill Place, London E14 5HP. Copyright Barclays Bank PLC, 2013 (all rights reserved).

This document is confidential, and no part of it may be reproduced, distributed or transmitted without the prior written permission of Barclays.

17