Embed Size (px)

Citation preview

The financial Crisis: A broad viewEric Tymoigne

Lewis and Clark CollegeEcon 220, Fall 2009

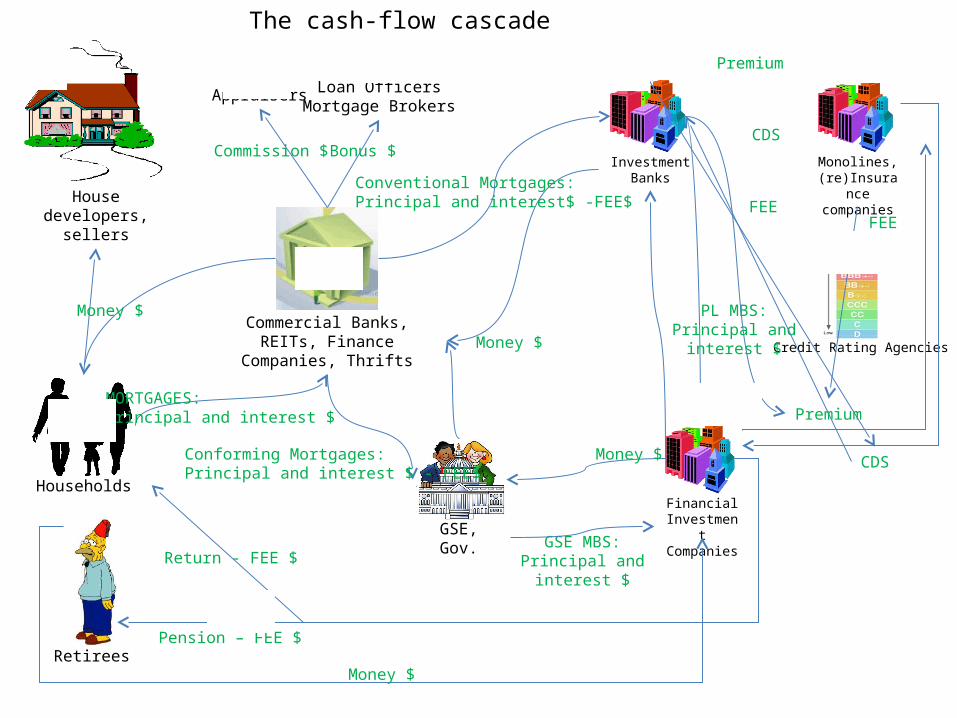

House developers, sellers

Households

Appraisers Loan OfficersMortgage Brokers

Commercial Banks, REITs, Finance Companies, Thrifts

Investment Banks

Retirees

Financial Investment Companies

Credit Rating Agencies

Monolines, (re)Insurance

companies

GSE, Gov.

Bonus $Commission $

Money $

Strong incentive to work implicitly together to get highest price possible on the house and to qualify as many people as possible

MORTGAGES:Principal and interest $

Money $

Conventional Mortgages:Principal and interest$ -FEE$

Conforming Mortgages:Principal and interest $ - FEE$

GSE MBS:Principal and interest $

Money $

PL MBS:Principal and interest $

Premium

CDS

Strong Incentive to work together to sell securities with low risk and good return

Pension – FEE $

Return - FEE $

Want a house and a good return on financial investments

Want to promote homeownership, free market ideology: deregulation

CDS

Premium

FEE FEE

Some of the main players

Money $

House developers, sellers

Households

Appraisers Loan OfficersMortgage Brokers

Commercial Banks, REITs, Finance Companies, Thrifts

Investment Banks

Retirees

Financial Investment Companies

Credit Rating Agencies

Monolines, (re)Insurance

companies

GSE, Gov.

Bonus $Commission $

Money $

MORTGAGES:Principal and interest $

Money $

Conventional Mortgages:Principal and interest$ -FEE$

Conforming Mortgages:Principal and interest $ - FEE$

GSE MBS:Principal and interest $

Money $

PL MBS:Principal and interest $

Premium

CDS

Pension – FEE $

Return - FEE $

CDS

Premium

FEEFEE

The cash-flow cascade

Money $

What is missing in the previous analysis

• Resecuritization business: MBS –> CDO -> CDO-squared -> CDO-cubed + synthetic securitization (LSS, etc.)

• Some other players: property insurance (for house), Special Purpose Entities (SPE) (Shadow banking: issue MBS, etc), central bank and Federal Home Loan Bank System (provide major refinancing sources to mortgage lenders), government loan programs

• Many other illiquid financial claims beside mortgages (ABS: asset-backed securities): credit cards, auto loans, students loans, rock-start royalties (Bowie bonds), movie royalties (Bond bonds), etc.

• It is not as clear cut in terms of cash flows: insurance companies also bought CDS (and so paid premium to each other), mortgage bankers issued and sold MBS and CDS, SPEs bought MBS of other SPEs (same with investment banks and commercial banks), financial investment companies usually are net sellers of CDS (major net buyers are banks), etc.

CDS MARKET

Collateral for MBS and CDO

Resecuritization, Re-resecuritization, etc.

Quality of Mortgages went Down

Rank LenderType of Financial Company Current State Location

Q4 2006 originations, in billions

1HSBC Finance (HSBC) Finance Company Discontinued consumer

lending businessProspect Heights, I L $12.30

2New Century Financial REI T Closed, declared

bankruptcyI rvine, CA $12.20

3Countrywide Financial Financial Holding Company Acquired by Bank of

AmericaCalabasas, CA $10.10

4 WMC Mortgage (GE) REI T Closed, put for sale by GE Burbank, CA $9.00

5First Franklin Home Loan Services (Merrill Lynch)

REI T Open, Discontinued subprime lending

San J ose, CA $7.80

6Wells Fargo Home Mortgage Financial Holding Company Open, Discontinued non-

prime lendingSan Francisco, CA $7.40

7Option One (H&R Block) REI T Open, Discontinued

subprime lendingI rvine, CA $6.10

8Fremont I nvestment & Loan* REI T Acquired by CapitalSource

(a REI T)Santa Monica, CA $6.00

9Washington Mutual* Bank Holding Company Acquired by J P Morgan

ChaseSeattle, WA $5.70

10 CitiFinancial (Citigroup)* Finance Company Open Baltimore, MD $5.00

*Estimates

Data: National Mortgage News, Implode-O-Meter

Top subprime mortgage lenders

Quality of Mortgagors went down

Excess and Fraud• Mortgage Lenders: put prime borrowers into subprime deals, do not verify

creditworthiness of mortgagors, assume that home price will always go up (so no problem if mortgagors does not pay), fraudulent behaviors (inflated fees, change terms of mortgage at the last minute without informing mortgagors, etc.)

• Mortgage broker/loan officers: same as mortgage lenders + lie on mortgage application (boost income of borrowers) + push people into exotic mortgages (ARM-IO, payment option, etc.)

• Investment banker: Toxic financial innovations, assume that home price will always go up, poor disclosure of information, fraud

• CRA: pressured to rate quickly toxic innovations (no look at underlying loan files), use rating techniques used on corporate bonds and assume they are good for toxic securities

• GSE: accounting fraud• Deregulation:

– Unregulated CDS (2000)– Pension fund allowed to buy toxic financial innovation (as long as they are AAA)

House developers, sellers

Households

Appraisers Loan OfficersMortgage Brokers

Commercial Banks, REITs, Finance Companies, Thrifts

Investment Banks

Retirees

Financial Investment Companies

Credit Rating Agencies

Monolines, (re)Insurance

companies

GSE, Gov.

Bonus $Commission $

MORTGAGES:Principal and interest $

Money $

Conventional Mortgages:Principal and interest$ -FEE$

Conforming Mortgages:Principal and interest $ - FEE$

GSE MBS:Principal and interest $

Money $

PL MBS:Principal and interest $

Premium

CDS

Pension – FEE $

Return - FEE $

CDS

Premium

FEE FEE

Money $

FORECLOSURES

HUGE INSURANCE

PAYMENTS DUE ON CDS

Asset liquidation: other markets affected

Unable or unwilling to pay: Unemployment, too high mortgage cost, underwater

The Crisis

Refinancing crisis!!

Money $

Central bank, Treasury, FDIC, FHLBS: lender of last ressort, buyer of last resort, TARP, etc.

No Just a Subprime Crisis

0

5

10

15

20

25

30

35

40

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Source: Mortgage Bankers Association

Percentage of Mortgages in Serious Delinquency (90+ days past due and in the process of foreclosure)

Prime FRM Subprime FRM Prime ARM Subprime ARM

Some fun…

http://www.youtube.com/watch?v=mzJmTCYmo9g

![Economics (ECON) ECON 1402 [0.5 credit] Also listed as](https://img.dokumen.tips/doc/110x75/6157d782ce5a9d02d46fb3da/economics-econ-econ-1402-05-credit-also-listed-as-.jpg)