Embed Size (px)

Citation preview

05.10.2017 Slide 1 Dr. Holger Weimar

ISC 2017 Hamburg

Dr. Holger Weimar

Thünen Institute of International Forestry and Forest Economics, Hamburg

Hamburg, 05.10.2017

The (European) market for (sawn) softwood Aspects of supply, production, trade, competitiveness and demand/use

International Softwood Conference, ISC 2017 Hamburg

05.10.2017 Slide 2 Dr. Holger Weimar

ISC 2017 Hamburg

The (European) market for (sawn) softwood Aspects of supply, production, trade, competitiveness and demand/use

Demand / Use

Production

Wood supply

Trade / Competitiveness

05.10.2017 Slide 3 Dr. Holger Weimar

ISC 2017 Hamburg

Supply: Global development Production

Global roundwood production 1961 – 2016

Quelle: FAO (2017)

2016 Total: 3.73 bn m³ Developed Countries: 3.14 bn m³ Least Deve-loped Countr.: 0.59 bn m³

49%

15%

35%

1%

05.10.2017 Slide 4 Dr. Holger Weimar

ISC 2017 Hamburg

Supply: Global development Forest Area

Development of global forest area 2005-2010 (Average rate of deforestation per year)

− Net losses of forest area of ~7 million hectares per year

− Degradation of additional areas, especially in the tropics and subtropics: (e.g.)

− Loss of biodiversity − Carbon emissions − Depletion of soil

− Programs for prevention (e.g.): − REDD, REDD plus − Lacey Act (USA) − FLEGT (EU) − EUTR (EU) − Certification (total Σ11%,

19% of managed area, Tropics: 6%, DE: 70%)

05.10.2017 Slide 5 Dr. Holger Weimar

ISC 2017 Hamburg

Supply: Global development Industrial roundwood

Source: FAO (2017)

12%

21%

4%

28%

3%

32%

Supply by continents 1992 – 2016

Σ 2016: 1,87 billion m³

05.10.2017 Slide 6 Dr. Holger Weimar

ISC 2017 Hamburg

Supply: Global development Coniferous industrial roundwood

Σ 2016: 1,05 billion m³ (Conif: 56%)

7% / 19% 8% / 38%

4% / 70%

38% / 78%

1% / 16%

41% / 74%

Supply by continents 1992 – 2016 share 2016 / share of conif. on continents total

Source: FAO (2017)

mill

ion

05.10.2017 Slide 7 Dr. Holger Weimar

ISC 2017 Hamburg

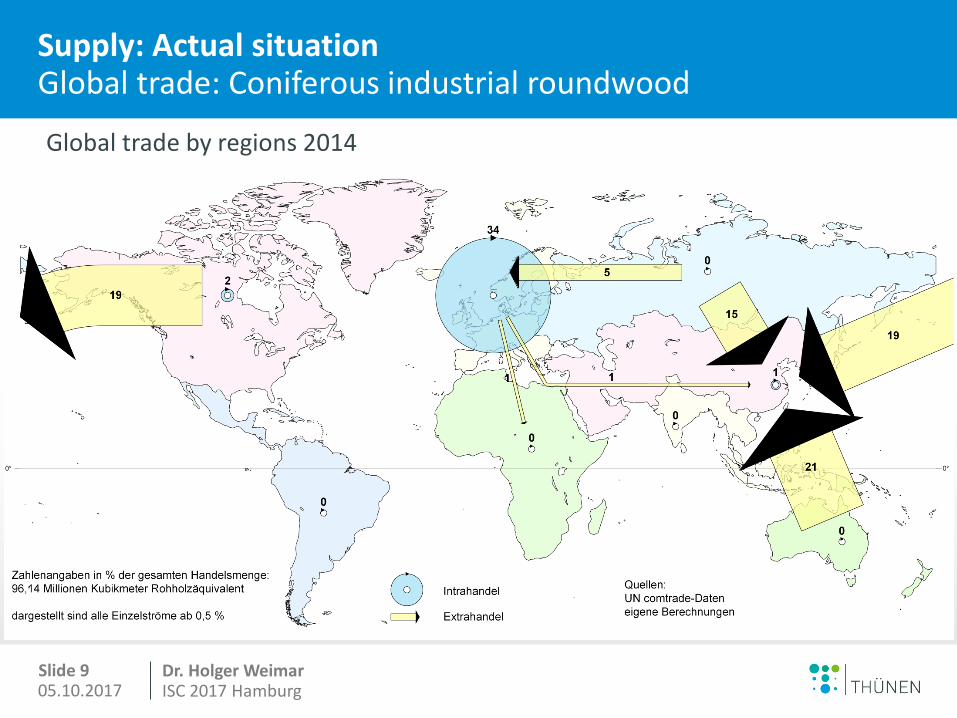

Supply: Actual situation Global trade: Coniferous industrial roundwood

Global trade by regions 2014

05.10.2017 Slide 8 Dr. Holger Weimar

ISC 2017 Hamburg

0102030

ChinaAustriaGermanySwedenRep. of KoreaJapanCanadaCzechiaBelgiumIndiaRomaniaFinlandPolandItalyLatvia

Milli 0 10 20 30

New ZealandRussian Fed.

USACanadaCzechiaAustraliaNorway

GermanySloveniaUkrainePolandFrance

BelarusLatvia

Slovakia

Milli

Supply: Actual situation Global trade: Coniferous industrial roundwood

Main exporters and importers 2016 (in million m³, Top 15)

Exporter ∑ 82 mill m³

Importer ∑ 83 mill m³

- China as main importer of coniferous roundwood - Intense trade of European countries

Source: FAO (2017)

05.10.2017 Slide 9 Dr. Holger Weimar

ISC 2017 Hamburg

Supply: Actual situation Global trade: Coniferous industrial roundwood

Global trade by regions 2014

05.10.2017 Slide 10 Dr. Holger Weimar

ISC 2017 Hamburg

0,76

61,0320,90

4,65

11,76

0,90

Production: Global development Semi-finished products: Global production (≈ consumption)

− New peaks for all products except pulp − Wood pulp relatively constant − Paper & paperboard slightly increasing − Wood-based panels very dynamic − Sawnwood strongly affected by crisis, but recovering

Sawnwood

Paper & Paperboard

Wood-based panels

Wood Pulp

Production (%) by continents 2016

2,20

27,23

33,62

7,40

27,51

2,04

1,37

17,57

26,42

15,88

37,37

1,390,88

47,05

25,63

5,43

20,06

0,95

0

50

100

150

200

250

300

350

400

450

500

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

mill

ion

Sawnwood (m³)Wood-Based Panels (m³)Wood Pulp (tons)Paper & Paperboard (tons)

Source: FAO (2017)

05.10.2017 Slide 11 Dr. Holger Weimar

ISC 2017 Hamburg

Production: Global development Sawnwood: Global production

− Sawnwood strongly affected by crisis, but recovering − Softwood stronger affected by crisis − Hardwood peaked in 2015 − Softwood seems still to recover/increase

Sawn softwood 2006

Sawn softwood 2016

Sawn hardwood 2006

Sawn hardwood 2016

Production (%) by continents

0

50

100

150

200

250

300

350

400

450

500

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

mill

ion

Sawnwood (m³)Sawn Softwood (m³)Sawn Hardwood (m³)

Source: FAO (2017)

05.10.2017 Slide 12 Dr. Holger Weimar

ISC 2017 Hamburg

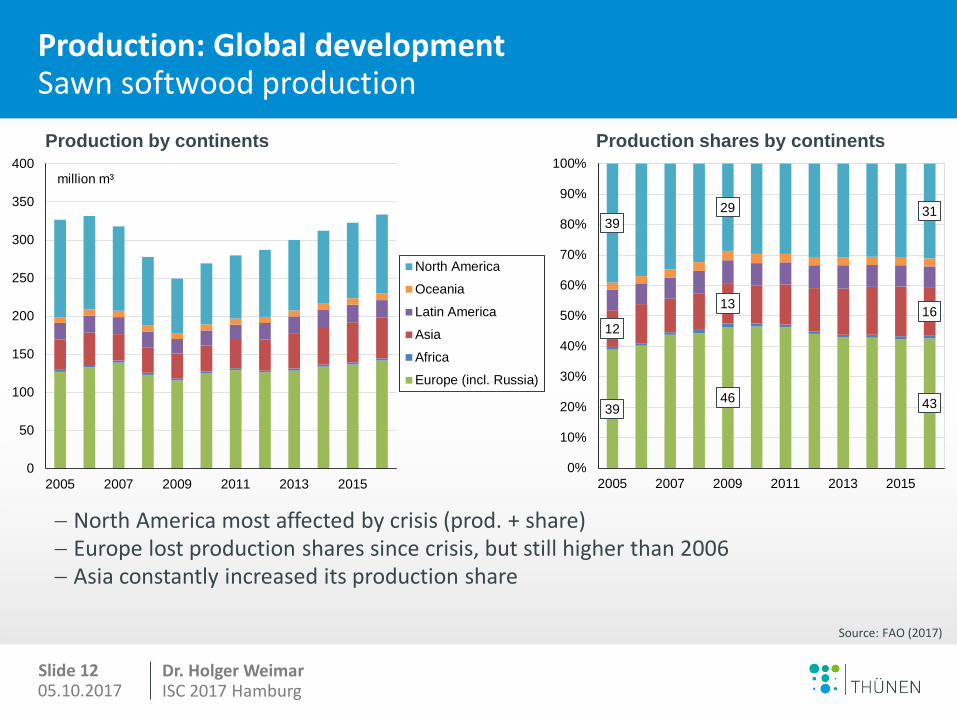

Production: Global development Sawn softwood production Production by continents Production shares by continents

− North America most affected by crisis (prod. + share) − Europe lost production shares since crisis, but still higher than 2006 − Asia constantly increased its production share

39 46 43

12

13 16

39 29 31

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2007 2009 2011 2013 2015

Source: FAO (2017)

0

50

100

150

200

250

300

350

400

2005 2007 2009 2011 2013 2015

million m³

North America

Oceania

Latin America

Asia

Africa

Europe (incl. Russia)

05.10.2017 Slide 13 Dr. Holger Weimar

ISC 2017 Hamburg

Production: Global development Sawn softwood production: Major countries

Source: FAO (2017)

− USA and Canada increased since 2009, but still far below pre-crisis level − China + Russia are constantly increasing their production − Brazil quite stable (∼9m), Japan slightly declining trend (∼12m to ∼8m)

0

10

20

30

40

50

60

70

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

mill

ion

USA

Canada

Russian Fed.

China

Germany

Sweden

Finland

Brazil

Austria

Japan

Chile

France

Turkey

05.10.2017 Slide 14 Dr. Holger Weimar

ISC 2017 Hamburg

Production: Global development Sawn softwood production: Major European countries

Source: FAO (2017)

− Not very much of a development (except Russia) − A lot of countries are still below pre-crisis level − Mainly eastern European countries are increasing production

0

5

10

15

20

25

30

35

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

mill

ion

Russian Fed.

Germany

Sweden

Finland

Austria

France

Turkey

Poland

Romania

Czechia

United Kingdom

05.10.2017 Slide 15 Dr. Holger Weimar

ISC 2017 Hamburg

0 10 20 30

CanadaRussian Fed.

SwedenFinland

GermanyAustria

ChileLatvia

USAUkraine

New ZealandCzechia

BrazilBelarus

Romania

0102030

USAChinaUKJapanEgyptGermanyItalyNetherlandsFranceAlgeriaSaudi ArabiaUzbekistanRep. of KoreaAustriaDenmark

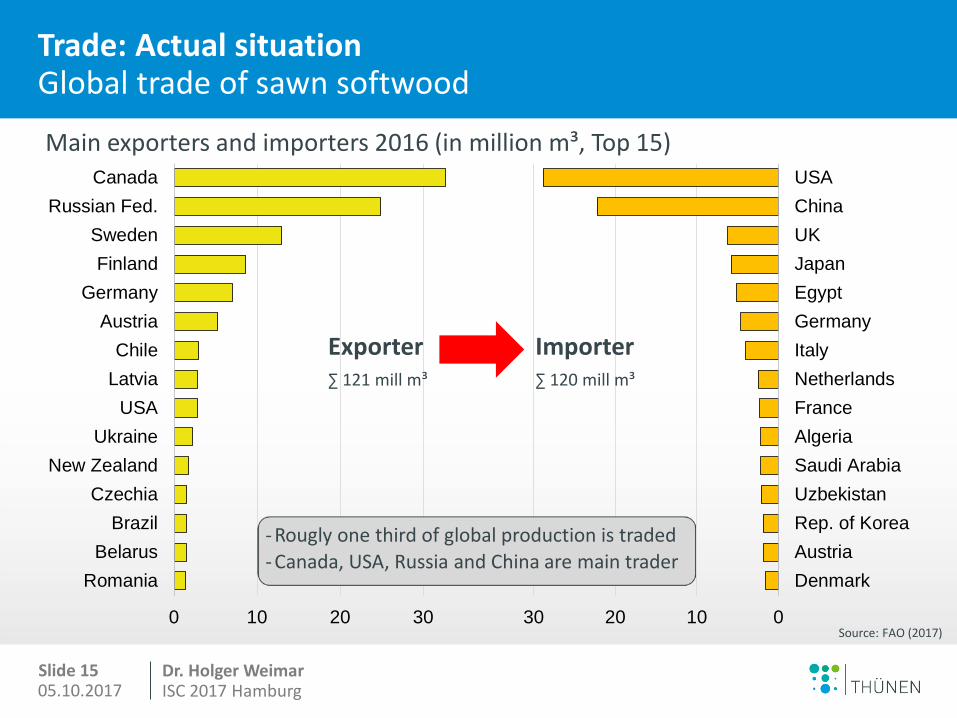

Trade: Actual situation Global trade of sawn softwood

Main exporters and importers 2016 (in million m³, Top 15)

Exporter ∑ 121 mill m³

Importer ∑ 120 mill m³

Source: FAO (2017)

- Rougly one third of global production is traded - Canada, USA, Russia and China are main trader

05.10.2017 Slide 16 Dr. Holger Weimar

ISC 2017 Hamburg

Trade: Actual situation

Global trade by regions 2014

Global trade of sawn softwood

05.10.2017 Slide 17 Dr. Holger Weimar

ISC 2017 Hamburg

Only few growing markets. China is main exception, strongly depended from imports. Consumption in the US sharply declined. EU countries with decreasing markets: IT, UK, FR, SE

Production & Consumption: Global development Change in prod. & cons. of 20 main consumers of sawnwood

Source: FAO, Dieter/Janzen

Comparison: ∅ 2001-2003 and ∅ 2011-2013

05.10.2017 Slide 18 Dr. Holger Weimar

ISC 2017 Hamburg

CAN

SWE RUS

FIN DEU

AUT USA

NZL CHL LVA ROU

CZE BEL BRA EST SVN UKR POL SVK BLR FRA IRL LTU NOR NLD 0%

5%

10%

15%

20%

25%

30%

35%

40%

0% 5% 10% 15% 20% 25% 30% 35% 40%

Expo

rt S

hare

201

4-16

Export Share 2004-06

Trade: Competitiveness Development of market shares (Sawn softwood)

Source: FAO (2017)

Development of export shares (exports ∅ 2004-06 and ∅ 2014-16 „pre-crisis and now“)

NZL CHL

LVA

ROU

CZE

BEL BRA

EST SVN

UKR POL SVK BLR

FRA IRL LTU

NOR NLD

0%

1%

2%

3%

4%

0% 1% 2% 3% 4%

Expo

rt S

hare

201

4-16

Export Share 2004-06

World exports: 2004-2006: 22.9 bn USD 2014-2016: 25.2 bn USD

05.10.2017 Slide 19 Dr. Holger Weimar

ISC 2017 Hamburg

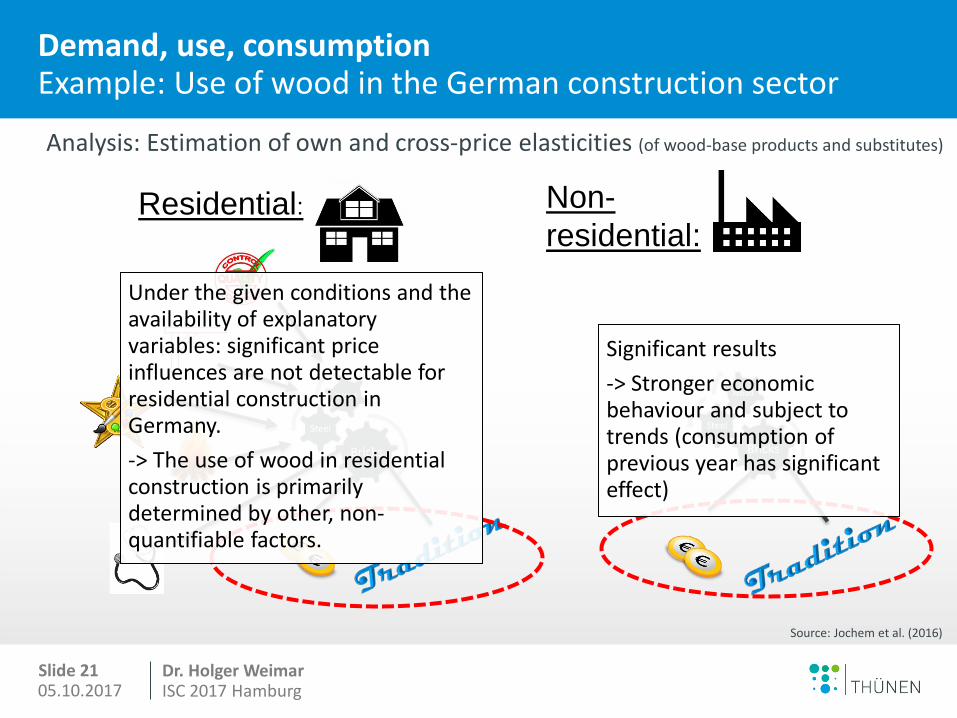

Demand, use, consumption Example: Use of wood in the German construction sector

Use of wood in the

construction industry

= 100 %

[> 50% of wood

products are used in

construction

New Constructions

( 36% )

Residential construction

Non- residential construction

Modernization ( 64% )

Residential construction

Non- residential construction

( 51% )

( 29% )

( 7% )

( 13% )

Source: Jochem et al. (2016)

05.10.2017 Slide 20 Dr. Holger Weimar

ISC 2017 Hamburg

Demand, use, consumption Example: Use of wood in the German construction sector

Source: Jochem et al. (2016)

What we know: • Several studies examined the influencing factors on

the choice of the construction material in Germany by using surveys.

• Depending on the type of building, the choice of the construction materials is influenced by various factors.

• Non-residential: Price and the construction material that is traditionally used.

• Residential: Also price and tradition, but also other factors like technological factors, or other subjective evaluated factors, such as quality, durability and security.

05.10.2017 Slide 21 Dr. Holger Weimar

ISC 2017 Hamburg

Demand, use, consumption Example: Use of wood in the German construction sector

Non-residential:

Residential:

Under the given conditions and the availability of explanatory variables: significant price influences are not detectable for residential construction in Germany. -> The use of wood in residential construction is primarily determined by other, non-quantifiable factors.

Significant results -> Stronger economic behaviour and subject to trends (consumption of previous year has significant effect)

Analysis: Estimation of own and cross-price elasticities (of wood-base products and substitutes)

Source: Jochem et al. (2016)

05.10.2017 Slide 22 Dr. Holger Weimar

ISC 2017 Hamburg

Forest stock in Europe Stock 2015: Share (without Russia), Quantity in billion m³

Source: FRA 2015

AT: 4%, 1,2

DE: 11%, 3,7

FR: 9%, 2,9

ES: 4%, 1,2

FI: 7%, 2,3 SE: 9%,

3,0 NO: 4%, 1,2

PL: 8%, 2,5

CZ: 2%, 0,8

RO: 6%, 1,9

RU: (71%), 81

UK: 2%, 0,7

LV: 2%, 0,7

IT: 4%, 1,4

Supply II: Potentials Development

LT: 2%, 0,5

SK: 2%, 0,5

HU: 1%, 0,5

BG: 2%, 0,7

RS: 1%, 0,4

0

10

20

30

40

50

60

70

80

90

1990 1995 2000 2005 2010 2015

in billion m³ (o.b.)

Russland Europa o. Russland

Mittelosteuropa Mittelwesteuropa

Nordeuropa Südwesteuropa

Südosteuropa

0

5

10

15

20

25

30

35

1990 1995 2000 2005 2010 2015

BY: 5%, 1,7

UA: 7%, 2,2

•Forest stock in Europe increases continuously •Highest forest stock in Russia, but only little changes

Russia

Middle Eastern Europe

Northern Europe

South Eastern Europe

Europe (excl. Russia)

Middle Western Europe

South Western Europe

05.10.2017 Slide 23 Dr. Holger Weimar

ISC 2017 Hamburg

0

10

20

30

40

50

60

70

80

90

100

2002-2012 2013-2017 2018-2022 2023-2027 2028-2032 2033-2037 2038-2042 2043-2047 2048-2052

mill

. m³/a

WEHAM-Periods

Buche Eiche Fichte Kiefer

Supply II: Potentials Example: Perspectives in Germany

*) Relation of average use 2002-2012 to average potential wood supply 2013-2052 Source: https://bwi.info

98 %

124 %

53 %

68 %

Use*:

NFI3

- Domestic supply of spruce will in future also (possibly) be below (a suggested) demand

- Potentials are mainly to be seen in: Oak, and other hardwoods

Beech Oak Spruce Pine

Wood use by timber species groups versus WEHAM potentials (Base scenario)

05.10.2017 Slide 24 Dr. Holger Weimar

ISC 2017 Hamburg

Source: UN: EFSOS II

→ Results of scenario analysis show great range of possible wood supply in Europe

Supply: Potentials Perspectives

EFSOS II: Outlook Study for Europe 2010 to 2030 European Forest Sector Outlook Study

05.10.2017 Slide 25 Dr. Holger Weimar

ISC 2017 Hamburg

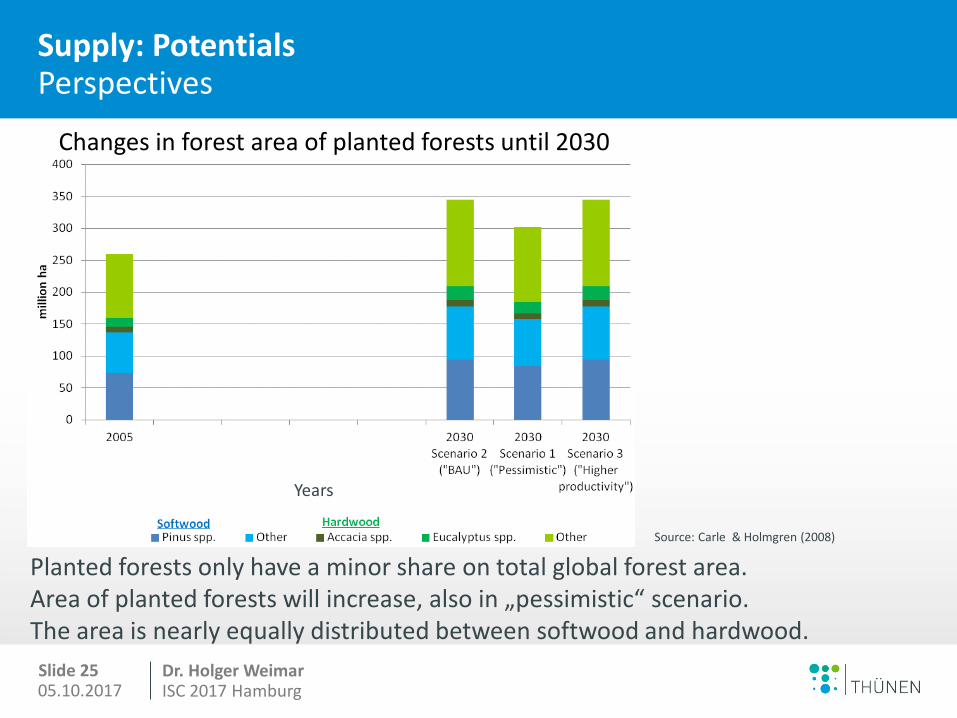

Supply: Potentials Perspectives

Changes in forest area of planted forests until 2030

Source: Carle & Holmgren (2008)

Planted forests only have a minor share on total global forest area. Area of planted forests will increase, also in „pessimistic“ scenario. The area is nearly equally distributed between softwood and hardwood.

Years

05.10.2017 Slide 26 Dr. Holger Weimar

ISC 2017 Hamburg

Supply: Potentials Perspectives

Change in wood production in planted forest until in 2030

Planted forests provide disproportionately more wood supply; mainly for material use. Main increases are expected in Asia and South America.

Total roundwood removal

Years

Source: Carle & Holmgren (2008)

05.10.2017 Slide 27 Dr. Holger Weimar

ISC 2017 Hamburg

Conclusions

• Forest stock is still increasing in Europe. However, potentials are intensely used, regional wood supply might show specific shortages (softwood!). Global potentials will preferably increase in (faster growing) plantations.

• Understanding and further developing of demand/use- mechanisms (here mainly for domestic markets):

• Understand and overcome technical or subjective barriers for wood use (in construction sector)

• Measures to improve image of wood • Provide solutions in combination with new/modified

products – and communicate them!

05.10.2017 Slide 28 Dr. Holger Weimar

ISC 2017 Hamburg

Dr. Holger Weimar Thünen Institute of International Forestry and Forest Economics Leuschnerstr. 91 21031 Hamburg fon: +49 (0)40 73962-314 fax: +49 (0)40 73962-399 mail: [email protected] web: www.thuenen.de

The Johann Heinrich von Thünen Institute, Federal Research Institute for Rural Areas, Forestry and Fisheries – Thünen Institute in brief – consists of 14 specialized institutes that carry out research and provide policy advice in the fields of economy, ecology and technology.

Hamburg, 05.10.2017

The (European) market for (sawn) softwood: Aspects of supply, trade, demand, competitiveness and use

Many Thanks!

05.10.2017 Slide 29 Dr. Holger Weimar

ISC 2017 Hamburg

Annex Quellen

Carle J, Holmgren P (2008): Wood from Planted Forests: A Global Outlook 2005-2030. Forest Products Journal 58 (12): 6-18.

Dieter M, Janzen N (2015): Das deutsche Cluster Forst und Holz im Wettbewerb. Tagung Sicherung der Nadelrohholzversorgung. Göttingen, 16.04.2016.

FAO, Food and Agriculture Organization of the United Nations (2017): ForesSTAT (http://faostat.fao.org/site/626/default.aspx#ancor).

FRA 2015: Global Forest Resources Assessment 2015. Desk reference. FAO, Food and Agriculture Organization of the United Nations: Rome.

Jochem D, Janzen N, Weimar H (2016): Estimation of own and cross price elasticities of demand for wood-based products and associated substitutes in the German construction sector. Journal of Cleaner Production 137(2016): 1216-1227.

Thünen-Institut, Dritte Bundeswaldinventur - Ergebnisdatenbank, https://bwi.info, Aufruf am: 26.01.2017, Auftragskürzel: 77Z1PA_L417mf_0212_bi, Archivierungsdatum: 2014-7-29 14:30:40.527, Überschrift: Vorrat (Erntefestmaß o.R.) des genutzten Bestandes [1000 m³/a] nach Land und Baumartengruppe, Filter: Periode=2002-2012.

Thünen-Institut, Dritte Bundeswaldinventur - Ergebnisdatenbank, https://bwi.info, Aufruf am: 26.01.2017, Auftragskürzel: 43Z1PA_P573of_1252_L40rSF, Archivierungsdatum:2016-3-2 16:52:59.127, Überschrift: projizierter Vorrat (Erntefestmaß o.R.) des Rohholzpotenzials [1000 m³/a] nach Baumartengruppe und Projektionsperiode, Filter: Basisszenario.

United Nations, UN (2011): European Forest Sector Outlook Study II: 2010-2030 (EFSOS II). Geneva Timber and Forest Study Paper 28, United Nations Economic Commission for Europe/Food and Agriculture Organization of the United Nations.

United Nations Commodity Trade Statistics Database: UNComtrade (http://comtrade.un.org/db/default.aspx).

![INDEPENDENT MARKET REPORT FOR SOFTWOOD PLANTATION … · INDEPENDENT MARKET REPORT FOR SOFTWOOD PLANTATION PRODUCTS ... ...]'/!,4./*!!!](https://img.dokumen.tips/doc/110x75/5f2e5de272f6a91abe7a3a7d/independent-market-report-for-softwood-plantation-independent-market-report-for.jpg)