Embed Size (px)

Citation preview

The effects of privatisation and liberalisation of the economy on the actuarial soundness of the

Egyptian funded and defined benefits social security scheme

Mohamed A. MAAIT, Gala ISMAIL & Zaki KHORASANEE

City University London

United Kingdom

INTERNATIONAL S O C I A L S ECURITY A SSOCIAT ION ( ISSA)

RESEARCH PROGRAMME

CONFERENCE HOSTS: FINNISH ISSA MEMBER ORGANIZATIONS

The Year 2000 International Research Conference on Social Security

Helsinki, 25-27 September 2000

“Social security in the global village”

2

The Effects of Privatisation and Liberalisation of the Economy on the Actuarial Soundness of

the Egyptian Funded and Defined Benefits Social Security Scheme

Mohamed A. MAAIT, Gala ISMAIL & Zaki KHORASANEE

City University, London Abstract Egypt is advancing in the process of transition from a planned to a market economy, as it is currently immersed in the process of liberalisation of the economy and privatisation of the public sector. This process is accompanying the development of capital market and financial institutions in their early stage. This might require some radical changes to the public social insurance pension system. Social security constitutes an important element in the current transformation. This paper describes the operation of the funded defined-benefit Egyptian public social insurance pension system. The system is operating under the aim of maintaining an actuarial equilibrium within the fund. But the scheme has been in a deficit over the last three decades as a result, mainly, of the investment strategy concerning the fund assets. The government is responsible for investing most of the funds through the National Investment Bank (NIB). The system’s assets are used to finance national projects and the interest rates provided on the funds are always below market rates. This paper discusses also the effects of unemployment and the government’s strategy of encouraging early retirement on the actuarial soundness of the system. Introduction Social security pension systems are regarded as one of the great social developments of the last hundred years. The fundamental objective of pension provision is to provide a satisfactory income to people in retirement. But pension schemes are subject to a variety of risks. As the economic, demographic and political situation in a country alters, some changes in retirement income schemes may also be required because of the interaction between social security retirement benefit schemes and these changes. It is recognised that social security schemes need to adjust to their changing economic, demographic, political and social environments as these changes may result in severe stress on the public pension systems. Whether the retirement income scheme is managed in public or private sector will depend on political philosophies towards individual and private sector responsibilities versus the role of the government and views as to the relative governance capabilities of the private and public sectors. In the early 1990s, pension reforms leading to substantial changes in the organising and financing of pension systems were undertaken in many places in the world. The overriding objective of pension reforms, regardless of the model propagated, must surely be the improvement of retirement income security and also to make sure that the retirement income of workers can be predictable and guaranteed. But the challenge in delivering a stable and predictable retirement income is that the world is changing and is inherently unpredictable. In the following section the features and operations of the social insurance pension system in Egypt will be presented. The effects of the recent economic developments on the system will also be explored.

3

Social Insurance Pension in Egypt The Egyptian social insurance pension system was established in 1854 and changed substantially following the July 1952 revolution to become widely stratified and a universal system. The system arose from a special, if not unique, set of circumstances. These circumstances are based on the economic, political, social and legal environment in which this system operates, which is quite different from many other pension systems. These may lead us to say that the model and the experience of this scheme are worthy of study. The public social insurance pension system in Egypt is entirely state-run, controlled and administered through the National Organisation for Social Insurance (NOSI). The NOSI operates two funds. The first one is the Government Sector Fund (GSF) which deals with civil servants and Gov. authorities employees through regional offices. The second fund is the Public and Private Business Sector Fund (PPBSF) which deals with all other categories of the population (e.g. public and private sector employees, employers and self-employed persons, Egyptians working abroad, etc) through regional and district offices; this managed by a tripartite board. These two funds have independent accounts (which means that there is financial independence from the state budget), supervised by the Ministry of Insurance and Social Affairs (MISA) catering for most of the economic sectors. The main role of the state is to regulate, supervise the scheme, guarantee the benefits as well as providing financial help in the case of a financial crisis and financing any additional benefits granted by political decisions. This system can be regarded as one of the most comprehensive social insurance systems in developing countries for many reasons. It is a relatively well-organised and mature system as it has been operating well for more than half century. It comprises programmes for old age, death, disability, health care, work injuries, and unemployment benefits. Participation in the scheme is compulsory for every individual working in the country and voluntary for those Egyptians working abroad. It currently covers most categories of Egyptian citizens. The scheme also extends to non- Egyptian nationals working in Egypt for at least one year, whose governments offer reciprocal arrangements to the Egyptians. It was established as a fully funded insurance-based system and this removes the system from the current debate regarding shifting from pay-as-you-go to pre-funding social insurance pension systems. The pre-funding of the scheme contributed to the increase of the aggregate national savings (and hence capital accumulation and growth), reduced the financial obligation of the state, and created a much more specific link between contributions and benefits. It offers a variety of benefits to most of the working population provided that they satisfy the eligibility requirements. It is a defined benefit system that offers salary-related benefits in return for salary-related contributions. It aims to provide a standard of living similar to that enjoyed during working life but individuals have to take what is offered by the scheme and this makes the scheme inflexible. The system has changed substantially over the last two decades as a result of the recent development of a hybrid or a multipillar system. It now contains schemes that represent a “safety net” of social security pension provision financed totally by general taxes and some indirect resources. The government has been giving priority to extending coverage of social protection and improving benefits as the majority of the retired work force relies on the social security pension for providing the major part of their income in retirement. Demographic, economic and social developments over the last two decades represent significant changes to the developments of the system. Egypt’s demographic transition began 10 years ago. Since then the population growth rate has declined from more than 2.5 percent a year during the late 1970s and the 1980s to around 1.9 percent in the 1990s, and the fertility rate from about 5 children per woman over the same period to around 3.8 in the 1990s. The mortality rate is 6.7 per thousand in 1998/1999 and life expectancy at birth for males has risen from 52.9 in 1977 to 64.7 in 1997 and for females

4

from 55.3 in 1977 to 67.3 in 1997, implying the payment of pensions for much longer periods. Egypt had a total population of around 62.33m in 1998 with a young population structure, which is reflected in a dependency ratio of about 9% in the last decade. More than 23.5m were covered by the scheme in 1998 as it can be seen from table (1). The workforce figures covered by the scheme currently stand at 17m in 1998, and the remaining 6.5m are beneficiaries of whom 4.8m are dependants.

Table 1. The structure of the population and members of the social

insurance pension system over the period 1973-1998 Year 1973 1978 1983 1988 1993 1998 Population (m) 34.06 38.29 43.97 49.98 55.90 62.33 Growth (%) 2.43 2.37 2.80 2.60 2.27 1.91 Population aged 15-60 (m) 18.42 20.82 23.89 27.29 30.96 34.82 % of Total Population 54.08 54.38 54.33 54.6 55.39 55.59 Population aged 60+ (m) 1.79 2.00 2.23 2.49 2.78 3.13 % of Total Population 5.25 5.22 5.07 4.98 4.99 5.01 Contributors (m) 3.6 8.0 10.94 13.1 15.5 17.0 Beneficiaries (m) 0.76 1.4 4.16 5.1 5.8 6.5 Contributors + Beneficiaries 4.36 9.4 15.1 18.2 21.3 23.5 % of Total Population 12.8 24.55 34.34 36.42 38.10 37.70 Dependency Ratio* 9.72 9.61 9.34 9.13 8.98 9.02 Ratio of Beneficiaries to Contributors 21.11 17.5 38.03 38.93 37.42 38.24 Source: MISA, the annual year reports; 1973-1998 and Central Agency for Public Mobilisation and Statistics (CAMPS) annual books; 1973-1998 * Population 60 and over as a percentage of population 15-60 This large number of insured people is distributed over the entire working population and its members include Egyptians working abroad. It can also be seen that a large increase in the total number of contributors and pensioners occurred over the last two decades (from 4.4m in 1977 to 23.5 in 1998). This was due to the introduction of new laws that cover some other categories of the population who had not been covered under any other laws. It was particularly the introduction of the non-contributory scheme, the Comprehensive Social Insurance Scheme, CSIS in 1980 that resulted in a large shift in the dependency ratio at the beginning of 1980s. The high increase in the number of pensioners and beneficiaries in the last decade was due much to the increase in early retirement incentives introduced in the 1980s and 1990s to ease the privatisation of the public sector and to alleviate pressure on the labour market. The fulfilment of the state policy is based on the extension of social protection to all the citizens. In 1998 nearly 16.95 million people were covered by the scheme under different laws and different categories of the population. Table (2) shows the number of insured persons according to their laws of the social insurance pension system over the period 1977 to 1998 at five years interval.

5

Table 2. Number of insured persons according to their type of social insurance (1977-1998) (m)

Employees Employers and Egyptians working The Comprehensivegovn./ public/private self-employed abroad Social Insurance Total

(m) (m) (m) (m) (m)Year Law 79/1975 Law 108/1976 Law 50/1978 Law 112/1980 Total1977 4.262 0.380 0.003 2.013 6.661982 6.023 0.626 0.012 4.007 10.671987 7.158 1.080 0.029 4.265 12.53

1992 8.533 1.382 0.041 5.043 15.001995 8.702 1.576 0.068 5.537 15.881998 9.335 1.756 0.022 5.837 16.95

Source: MISA, the annual year reports; 1977-1998 The following laws were enacted to organise and regulate the National Insurance Pension System in Egypt. LAW NO 79/1975 It insures civil servants and public and private sector employees against old age, death, disability, health care, work injuries, and unemployment risks. These categories represent the most significant part of the system as a whole. In 1998 there were 9.34 million contributors covered by this law which represented more than 55% of the total members of the system and 84% of the total number of contributors. This number also represents the total official work force in Egypt. Table (3) shows the number of contributors covered by this law over the period 1986-1998 distributed between different types of economic sectors.

Table 3: Numbers of employees covered by Law 79/1975 over the period 1986-1998 (m)

Year

State and Local Civil Servants

Public Sector

Private Sector

Total

% of Total Members

1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998

2.595 2.708 2.878 3.025 3.128 3.256 3.409 3.544 3.621 3.693 3.743 3.782 3.802

1.858 1.865 1.869 1.886 1.908 1.904 1.892 1.865 1.849 1.371 1.354 1.260 1.109

2.424 2.585 2.727 2.841 2.944 3.079 3.232 3.359 3.506 3.638 3.975 4.190 4.424

6.877 7.158 7.474 7.752 7.980 8.239 8.533 8.768 8.976 8.702 9.072 9.232 9.335

57.22 57.12 57.27 57.38 57.23 57.05 56.89 56.72 56.49 54.79 55.15 54.94 55.07

Source: MISA, the annual reports; 1986-1998. From this table we notice a significant steady reduction in the number of insured employees working in the public sector and a significant increase in the number of insured employees working in the private sector over the period 1990-1998 since the government started the privatisation process. There is also an overall steady decrease in the percentage of insured

6

employees of this category to the whole system although this category represents the most significant one to the financial position of the system. This has occurred for the following reasons: (1) The Government has implemented an economic policy based on privatising the public

sector, (2) The Government is encouraging many employees to leave work and receive early

retirement benefits, (3) The Government is ending temporary contracts in public sector and civil service, (4) The increase in the unemployment rate over the last decade. (5) There may also be an emerging trend of contribution evasion among private sector employees and employers. LAW NO 108/1976 It sets out a framework for a scheme applied compulsorily to employers and self -employed persons who are aged between 21 and 60 years old, insuring them against old age, death and disability risks. Nearly 1.76 million contributors of this category were covered in 1998, which represented about 10.36% of the total members of the scheme compared with 5.7% in 1997. This category is also important to the financial position of the system, as it is fully funded scheme. In 1977 this category represented 8.18% of the total number of contributors to the system compared with 15.8% in 1998. This may be an outcome of the current trend that many employees are leaving public sector and government employment for private and self employed employment. LAW NO (50/1978) It was passed promulgating the voluntary social insurance system, which insures only those Egyptians working abroad who are subject to the compulsory social insurance system inside Egypt and aged between 18 and 60 years old against old-age, death and disability risks. The number of contributors covered by this scheme is decreasing over time. It was about 68 thousand members in 1995 but currently it is only 20 thousands who pay contributions regularly. The number of contributors of this scheme stands at 21.67 thousands in 1998, which represented less than 0.13% of the total number of members. It is expected that the number of contributors of this category will decrease more over the next few years as the opportunities for working abroad are declining. LAW NO 112/1980 This is the non-contributory scheme of the social security system and is regarded as a supplementary one to the funded schemes. It is a basic anti-poverty and means-tested tier financed mainly from general revenues and other indirect resources rather than social security contributions. It provides income support for those without other means such as casual workers and any persons who have had no previous coverage by any of the other social insurance schemes. Under this law there are two schemes. The first one is called the “Comprehensive Social Insurance Scheme (CSIS)” and the second one is called “Sadat Pension Plan (SPP)”, (Sadat was the president of Egypt in 1970s) which operated under article No 5 of the CSIS. It insures against old age, death and disability risks, to give a degree of security for this category of the population. In 1984 there were 3.95 million people covered by this scheme which represented 35.23% of the total members of the system compared with about 5.84 million people covered in 1998 which represented 34.44%.

7

LAW NO. 64/1980 and LAW NO. 54/1975 Law no. 64/1980 gave the MISA the authority to approve an alternative higher pension for employees working in selected areas with very important taxation privilege. This alternative pension is paid from separate pension schemes that replaces the national social insurance pension system completely. There are 8 funds operating under this system in Egypt now. This form of contracting-out has been stopped and it is no longer in use. The reasons were that the government preferred to dominate and control the investment of the funds and as a reaction to the bankruptcy of some large ventures. Individual organisations in Egypt are allowed to have complementary occupational pension schemes. These schemes can be regarded as the private pension funds that exist in (most) occupations. Law no. 54/1975 regulates occupational private pension funds that give additional benefits to employees. The Egyptian Insurance Supervisory Authority (EISA) supervises these occupational pension schemes. These schemes offer additional benefits to employees and the majority of these schemes offer benefits in the form of a lump sum on retirement. These plans provide salary-related benefits in return for salary-related contributions paid by the employees. Most of the occupational schemes belong to the public sector rather than the private sector and they are growing at an increasing rate in which reflects the need to secure an additional income on retirement in Egypt. As in September 1995 there were 511 occupational pension schemes registered with EISA and only 9% of these funds relate to private sector employers (GAD, UK, report to EISA; 1997). Financing the System (Contributions and Benefits) Methods of financing income for retirement vary a great deal between different countries. The Egyptian system has been, mainly, operating on the basis that every generation is responsible for funding its own liabilities. The rational for funding is firstly to provide security and to increase the probability that the benefits will be paid in accordance with expectations. This fundamental issue of the strategy of funding the system, (whether the scheme should be operated on a pay-as-you-go basis or maintain a specific degree of pre-funding of future liabilities), has been under discussion in Egypt for long time. But the difficulties facing the pay-as-you-go social security pension schemes in many countries are leading to a growing interest in keeping the current level of pre-funding together with other unfunded schemes for those categories who are unable to finance their future liabilities. Also it can be said that pre-funding of the Egyptian pension scheme averted any major increase in contribution rates over the last 3 decades. Benefits are mainly financed through contributions and returns on the invested reserves. Members must contribute to the system to obtain a pension paid irrespective of means (except for members of the CSIS and SPP, law no. 112/1980). Contributions are shared between employees, employers, and the government and deducted from both basic and variable wages. Contributions are fixed percentages of the pensionable salary for each year of service (which can be regarded also as a defined contribution system as contribution rates have been relatively stable over the last 3 decades). Employers’ and employees’ monthly contributions represent the basic sources of financing. The government provides financing of 1% of the annual salaries out of the general tax revenues as well as a back-up source to cover any deficit. Table (4) shows the system’s contribution income distributed between different sources over the period 1986-1998.

8

Table 4. The distribution of contributions and other sources of financing the social security pension system (LE bn)

Year

Contributors “all categories”

%

Employers and Government (1%)

%

Exchequer

% CSIS % others %

1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998

0.8632 0.8992

NA 1.2258 1.3560 1.5092 1.6856 1.9817 2.3129 2.6211 2.9441 3.2518 3.6028

38.0 37.1 NA 38.4 37.4 36.9 36.8 36.0 35.9 35.0 34.5 33.9 33.2

1.2974 1.4065

NA 1.8147 2.0993 2.3895 2.6863 3.2914 3.7357 4.2371 4.8239 5.3822 5.9786

57.0 58.0 NA 56.9 57.9 58.4 58.6 59.8 57.9 56.7 56.4 56.1 55.0

0.0611 0.0641 0.0804 0.0930 0.1045 0.1189 0.1336 0.1566 0.1921 0.3451 0.4331 0.5429 0.7442

2.7 2.7 NA 2.9 2.9 2.9 2.9 2.8 3.0 4.7 5.1 5.7 6.9

0.041 0.041 0.042 0.0479 0.056 0.063 0.058 0.054 0.058 0.050 0.045 0.049 0.050

1.8 1.7 NA 1.5 1.5 1.5 1.3 1.0 0.9 0.7 0.5 0.5 0.4

0.012 0.012 NA

0.009 0.009 0.013 0.019 0.022 0.148 0.219 0.300 0.363 0.486

0.5 0.5 NA 0.3 0.3 0.3 0.4 0.4 2.3 2.9 3.5 3.8 4.5

Source: MISA, the annual year reports; 1986-1998. Form this table it can be seen that the income financing the system from contributors, employers and the government (1%) has been decreasing over the last decade from 97.7% in 1986 to about 88.2% in 1998. It can also be seen that the percentage increase in finance from the exchequer has risen from 2.7% in 1986 to 6.9% in 1998. It can be said that the main reason for that is because of the recent increases in pension financed by the exchequer. Also there have been increases in finance from other (indirect) resources such as miscellaneous license fees and taxes. These recent changes of the structure of finance let some researchers on pension system in Egypt to say that the system is moving towards partially funded system (Nagib S. and Ibrahim F., 1994). Benefits are paid in respect of both basic and variable salaries and contributions are deducted from both. The benefits are a fixed percentage of the final pensionable salary for each contributory year. The final pensionable salary is defined as the average pensionable salary during the last two years of employment. The normal retirement age is 60 for both men and women, although an earlier retirement from age 55 is permitted with some deductions in benefit if the member of the scheme satisfies the requirements for retirement income. Table 6 shows the number of pensioners and dependants according to their type of social insurance cover in 1998,

Table 6. Number of pensioners and dependants according to their type of social insurance (thousands).

Type of insured persons Pensioners. Dependants. TotalEmployees; (79/1975). 1016.3 2274.3 3290.6Employers and self-employed 126.62 376.7 503.32persons; (108/1976).Egyptians working abroad; 3.48 2.23 5.71(50/1978).The comprehensive social 537 1453.46 1990.46insurance system; (112/1980).Sadat Pension 41.97 701.56 743.53

Total 1725.37 4808.25 6533.62 Source: MISA, the annual year reports; 1998

9

The percentage of beneficiaries to the total population has risen from about 2.2% in the early 1970s to about 10.4% in the 1990s. Out of nearly 6.534 millions of beneficiaries in 1998 there were about 4.81 million of dependants as the schemes entitle these people to benefits. The increase in the number of pensioners and dependants cannot be traced to demographic tendencies but it is mainly due to the extension of coverage to new categories of the population. It is also due to the increase in the frequency of early retirement, (a policy adopted by the government in 1990s), the maturity of the schemes and higher unemployment. In general, the contribution rates and benefits differ according to different laws and categories, as explained in the following section. Law No. 79/1975 Employees, employers and the government are required to pay contributions to the scheme as follows: • members contribute 11-14 % of their income depending on the economic sector of

employment and, • employers contribute 24-26 % of the payroll depending on the economic sector and, • the government contributes 1 % of the payroll to the old-age, death and disability scheme. In 1998 the total contribution rate was 41% of the payroll distributed between the three sources. This high contribution rate is due to the fact that pension rights are mainly funded through contributions and not by the state budget. It can also be a result of the current poor investment strategy, which yields a low return on the invested reserves. The employer contribution constitutes the largest part of the social security contribution. In total, employers and employees pay contributions at a rate of approximately 35-40 % of basic and variable pensionable salaries (36% of the variable and 40% of the basic salaries), subject to the same earning limits. Some researchers regard the scheme as a relatively expensive scheme for employers and employees as it raises the overall labour costs (Nagib S., 1994). This is a very important factor for the government to consider when encouraging investors to shift production to Egypt. It is 26% of the salaries that are allocated to the old age, death and disability pension scheme: 15% from the employer, 10% from the employee and 1% from the government. The basic salary is basic pay up to LE 550 per month and variable salary is basic pay up to LE 600 per month in 1999. Maximum earnings for contribution and benefit purposes consist of limits on combined basic and variable salaries depending on salary class (it is currently around LE1200 per month, which is about £240). The establishment of benefit (and contribution) ceilings limits the state’s responsibilities to high-income earners, as the retirement pensions are restricted to the first tranche of earnings. There is a required contribution period of 36 years in order to secure the maximum replacement of income. Contribution years can also be purchased (the price will be based on the pensionable salary) if the contributor wants to satisfy the required number of contributory years in order to qualify for old age retirement pension. This seems to have reduced contribution evasion considerably in the past, but that can also be attributed to the collection mechanism that integrates social security contributions with the general tax collection. Provided that at least 20 years of contributions have been paid, an old-age pension can be taken at any age before or on age 60. The target benefit is approximately 1/45 of the final pensionable salary for each year of contributory service before retirement (up to a maximum of 36 years). This provides a maximum pension of 80% of earnings up to pay ceiling of L.E.1200 and if the insured person does not qualify for a pension, a lump sum is due. This could be a reasonable and relatively high level of pension compared with an average monthly salary of about L.E. 500, which gives a better replacement ratio for those who are on low incomes provided full contributions are paid during the whole period. However, workers with earnings above this level would need additional pension provision in order to maintain the

10

lifestyle they enjoyed during their working lifetime. The scheme also does not have special provisions to assist lower income earners, except determining a minimum pension level of LE 50 per month, but this is too low to significantly improve the standard of living for lower income earners. Law No. 108/1977 and Law No. 50/1978 To encourage coverage through voluntary compliance by employers, self -employed workers and Egyptians working abroad, the scheme charges them lower rates than the rates charged to the formal employees and employers for coverage under only old age, death and disability pension programmes. These two categories enjoy the privilege of choosing their own pensionable salary. The insured person can choose to contribute to the scheme within any level of monthly earnings between L.E. 50 and L.E. 900 per month for employers and self-employed persons and between L.E. 50 and L.E. 600 per month for the Egyptians working abroad. For the insured person, employer or self-employed, contributions are paid at the rate of 15% of his/her chosen monthly income and it is 22.5% for the Egyptians working abroad. In 1989 it was found that 51.5% of employers and self-employed persons had chosen the minimum limit, L£50, to be the pensionable salary. The system has been trying to find a solution to this problem by convincing the insured persons to choose a level of earning which best match their actual incomes. In 1998, this percentage was reduced to 15.6%. It was also found that more than 50% of the insured persons of the Egyptians working abroad choose to contribute to the scheme with the minimum level as the pensionable salary. For employers, self-employed and Egyptians working abroad, the condition to be eligible for the benefits of retirement income is to attain age 60 with a minimum period of 120 months of contributions for the first and the second categories and 180 months for the third category. In the case of early retirement, 240 months of contributions are required with absolute suspension of activity for the first category. The insured person, according to the scheme, is not permitted to receive any of the scheme’s benefits if the contributor stops paying his/her contribution for 6 consecutive months. The pension is calculated as, (1/45) x (the monthly income was chosen) x (the number of contributory years). The minimum pension is L.E. 50 and the maximum is 80% of the monthly chosen income. In the case of early retirement, the pension is reduced from the calculated value at age 60 by a specific percentage according to the age at retirement. If the insured person does not qualify for a pension, a lump sum is due. LAW NO (112/1980) The CSIS is financed from three sources. The first is a very small amount of contribution (L.E. 1 per month) from the insured person. The second is some indirect sources such as: * The amounts allocated for the scheme in the budget of Nasser Social Bank (Nasser was the

president of Egypt in 1950s and 1960s). It is a social bank in Egypt to finance some social security affairs,

* Miscellaneous license fees and taxes, The third is the government, as the balance is provided by direct sources transferred from the Treasury. For those who are covered by SPP, no contributions are paid for this plan, it is totally financed from the State’s budget. The only requirement for eligibility for old age benefits is attaining age 60 with at least 120 months of contributions for the member of the CSIS. A fixed amount of pension is due equal to L.E. 57 per month in 1997. The SPP pension is provided under the same conditions as the CSIS to around 0.8 million people. The pension paid for insured person is a fixed amount of L.E. 47 per month in 1997. This is not a reasonable level of pension for the insured categories

11

under the CSIS who are on low income, because it does not guarantee any minimum level of life. For the financing of this scheme there is a close link between the level of coverage and the level of social protection resources available to finance it. Provided that the tax base is broad and yields sufficient resources, coverage may be extensive, as it is not dependent on individualised financing. Government Finance Transfers to the System The Government has committed itself to finance the following liabilities: 1. 1% of the total payroll as a contribution to the old age, death and disability risks. 2. The balance of CSIS and the SPP liabilities. 3. Any increases in pension including raising the minimum pension and any grants for

pensioners arising from a political decision. 4. Any deficit as a debit on the system (has to be repaid to the exchequer when the scheme

has an actuarial surplus). The amount transferred by the exchequer to the system is increasing sharply year after year as it can be seen in table (5). Table 5. Amount transferred by the exchequer to the SIPS Year Total Exchequer

Transfer Current Balance

% of Current Balance

Total Contributions

% of Total Contribution

% of GDP

1978 1982 1987 1990 1993 1996 1998

15.3 273.2 507.7 869.2 1969.2 3497.3 4838.2

619.2 1669.4 3987.3 6999.9 12490.9 20958.8 27572.3

2.47 16.37 12.74 12.42 15.77 16.69 17.55

447.9 1066.6 2423.4 3190.6 5505.2 8545.7 10860.8

3.42 25.61 20.95 27.24 35.77 40.93 44.55

0.16 1.32 0.98 0.90 1.25 1.52 1.77

Source: MISA, the annual year reports; 1978-1998 As it can be seen from table (5), the transferred finance to the system by the exchequer is increasing dramatically year after year which reflects the growth in pension expenditure financed by the exchequer. In the 1980s and 1990s there was rapid social pension expenditure financed by the exchequer as a result of increases in coverage and more unfunded benefit promises which have an increasing effect over time, notably in the insurance-based part of the system. Pension expenditures financed by the exchequer are growing much faster than the GDP. It was growing by a rate of more than 18% per year compared with average GDP growth of around 5% per year over the period 1982-1998. Also the average ratio of pension expenditures financed by the exchequer to GDP rose from 0.16% in 1978 to 1.77% in 1998. It means that there is growing burden of social security pensions expenditure on the budget. Some of the reasons for this dramatic change of the financial structure over the last two decades are: 1- The government is currently encouraging many of its employees and public sector

employees to take early retirement benefits. 2- Increasing the pensions by 10%-20% every year and also increasing the minimum and

maximum limits of pensions. 3- Extending the coverage to more categories of the population who have no resources to

finance their liabilities. The scheme financing status is adequate if valuations and projections indicate that in each actuarial valuation the revenues plus reserves are sufficient to meet benefit payments and future liabilities. Many schemes are in financial difficulties simply because of an inability to

12

collect all the revenues due to them, to invest any reserves wisely, or to pay benefits promptly and in full. Given the adoption of a funded system, difficulties arise as a result of the performance of some economic factors, which accentuate the financial problems of social security system. In Egypt some of these difficulties are the impact of high inflation on the pension, the ineffective investment strategy, the deficit dilemma of the system and high unemployment rates. Also there are demographic risks such as the increase in life expectancy and the decrease in fertility rates. These and some other problems will have major effect on the future actuarial soundness of the system. In this paper we will restrict ourselves to review only the effects of the economic risks on the system, which are accompanying the reform of the economy. Impact of Inflation The backup for the benefit promise under a funded system is the system’s ability to have enough resources to meet its current and future liabilities. This backup should facilitate the protection of the elderly from different risks such as risks arising from the performance of the economy. One of the most important risks is the inflation risk. In Egypt, the method of calculating the benefits aims to keep the standard of living for retired persons unchanged, but pensions are not indexed to inflation and adjusted at the discretion of policy makers. Inflation rates were high over the last two decades with a peak value of around 25% in 1986. Pensions were quickly eroded during the high inflation phase, which made the real value of this income inadequate, especially for people on low income who are the most vulnerable group. These high inflation rates affected the real value of benefits very badly and may have led to some sort of contribution evasion. This effect can be seen if we compared the monetary value with the real value of the average pension benefits over the period 1977-1998. If we consider the year 1977 as a base year, it is found that the real average value of pension benefit is L.E. 153.5 in 1998 compared with a monetary value of L.E. 355.5 in the same year. This indicates that the average monthly of the real pension has decreased substantially and indicates the effect of the inflation rate over the last two decades on the pension benefits. Figure (1) shows the difference between the monetary and real average monthly value of the pension benefits during the period 1977/1998: Figure 1. Monetary value versus real value of pension benefits during the period 1977-1998.

Source: MISA, the annual year reports; 1977-1998.

Monetary and Real Value of the Average Monthly Pension over the Period 1977-1998

0

50

100

150

200

250

300

350

400

19

77

19

78

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98Year

LE

Monetary Average Pension Real Average Pension

13

To face the increase in the inflation rates the government created a new system. This system depends on establishing another pensionable salary called the variable salary, which contains all the increases added to each employee’s salary. This situation occurred because of the massive increases in salaries for employees after the rise of the inflation rates in 1980s and 1990s. Pensions have also been increasing by about 10% or more every year over the last 15 years. It can be seen from figure (2) that these increases did not make any significant effects on the real value until few years ago when the inflation rates were brought down to a reasonable level.

Figure 2. Monetary value versus real value of pension benefits during the period 1978-1998.

Source: MISA, the annual year reports; 1977-1998. High inflation created the necessity to level the inequalities of pensions granted in different years and to implement a system of inflation related revaluation of pension amounts. The proposed solution to the problem is to link benefits to the Retail Price Index (RPI). Another alternative is to re-value the pension benefits yearly in line with salary increases, as the scheme will keep the standard of living constant for the pensioners. It is also important to improve the investment policy of the reserves by investing in real assets to give protection against inflation (e.g. index-linked gilt’s, equities and properties) which will benefit future pensioners. For existing pensioners the Government has to keep paying pension increases every year in proportion to the inflation rate and these increases are funded from the State’s budget. The Investment Strategy and the Deficit Dilemma As a result of adopting the full funded or capitalisation method in determining the contribution rates of the system, there are huge reserves have been accumulating over time. This has resulted in some particular issues related to the investment management. First of all, it has to be said that the management of these reserves is subject to political interference as the government takes the main responsibility for investing most of the funds through the NIB. Secondly, one of the most important features of the management of the invested reserves is that these reserves are used to finance national projects at low interest rates. The interest rates provided are below market rates. This reflects an underlying philosophy of the state that aims

The Impact of Inflation on the Real Value of Pension

-25.0-20.0-15.0-10.0

-5.00.05.0

10.015.020.025.030.0

19

77

19

78

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

Year

%

%Pension Increase % Inflation % Real Increas

14

to achieve specific macroeconomic and social objectives by financing various national projects of its development plans. It is also argued that the government wants to break the connection between the investment risks of the funds and the administration of the system so they can keep the benefits and the rate of return guaranteed. In general there is an agreement in Egypt that these accumulated reserves became a permanent feature of the country’s financial structure, as it is an essential element of the economic stability that this system would be maintained whenever a governmental subvention should become necessary. Prior to January 1966 the funds were invested in government loans and deposits offering a modest interest rate of 3.5% per annum, and the system was obliged by the law to invest in these assets. Since the end of the second half of the 1970s the NIB took the responsibility of investing most of the reserves of the system. The rate of interest given by the NIB on the invested funds is negotiated following every actuarial valuation of the scheme. This rate of interest is always lower than the prevailing rate in the market but of course less variable, guaranteed and reduces the investment risk faced by retirees. The given rate of interest by the NIB is influenced by two factors: first, the prevailing market rates of interest on bank deposits; second the size of the system’s deficit. One of the main functions of the actuary of the system is thus to recommend the required rate of return to be achieved on the invested reserves in order to assist in maintaining the equilibrium position of the scheme and to amortise any deficits. Although this recommended rate has always been less than the prevailing rates in the market, the NIB and the government are not obliged to follow the actuary's recommendations. This is one of the main disadvantages of the system’s investment policy. The origin of many of the difficulties lies with the government, which has usurped the reserves of the pension system to finance its development plans by investing nearly all the funds in government vehicles in return for a low interest rate. The system is currently investing the majority of its funds in governmental instruments (more than 95% in 1998), as there are still very tight restrictions on the investments of the funds. Most of the reserves are invested in bank deposits, government loans to the exchequer, local authorities, public sector companies, government bonds, treasury bills and also listed securities. The investments of these reserves are predominantly in fixed interest assets, rather than equity-based assets. No less than 99.7% of the total assets are invested in fixed interest vehicles, mainly in bank deposits, (either in the NIB or in other public banks) as can be seen from table (6). It is perhaps surprising that less than 1% of the assets are in equity related investments, since it would be reasonable to expect that the value of these types of investment would increase broadly in line with inflation and economic growth. This happens because of the Government’s investment policy which forces the management of the system to credit the NIB with the largest portion of its funds which impairs the investment performance.

Table 6. The distribution of % invested assets between

different instruments over the period 1976-1998. Year % in

NIB % in Treasury

bills % Deposits in

Commercial Banks Loans to Members &

Others % Listed securities

Total %

1976 64.50 33.90 0.00 1.50 0.10 100 1981 69.90 27.80 0.90 1.10 0.30 100 1986 71.70 25.00 2.20 1.00 0.10 100 1990 86.30 10.70 2.10 0.80 0.10 100 1994 88.69 6.08 4.82 0.33 0.08 100 1998 91.44 3.31 4.38 0.17 0.70 100

Source: MISA, the annual year reports; 1976-1998 If we compare the average rate of return achieved on the invested funds with the interest rates on bank deposits in commercial banks (risk free investment) we notice that there are a huge

15

lost returns as a result of this policy. Table (7) shows the accumulated invested reserves, the achieved rate of return compared with the interest rate on bank deposits and the lost return over the period 1976-1998.

Table 7. The development in the pension fund reserves, % invested, % of average

return and lost return over the period 1976 - 1998 Year Reserves

LE (m) % Invested

% Invested in NIB

% Average Return

Interest on Bank Deposits

*Lost Return LE (m)

1976 1977 1978 1979 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998

2975.3 3364.0 3821.2 4576.9 4862.5 5576.7 6636.5 7825.3 11727.8 13766.0 16242.9 18867.2 22328.2 26026.0 30455.9 35429.9 40395.3 47516.5 56955.1 67783.3 80348.6 95131.4 111859.6

85.09 85.46 95.77 96.20 95.96 95.56 94.25 94.29 95.51 94.72 94.62 94.74 94.86 94.35 93.51 93.68 94.51 94.79 94.40 94.00 93.20 91.70 89.70

64.49 69.02 64.92 70.32 66.20 69.92 73.78 77.40 63.14 67.40 71.69 75.12 77.58 80.92 86.39 87.76 88.73 88.80 88.69 89.42 90.36 90.96 91.44

4.73 4.64 4.12 4.10 4.07 5.19 5.19 5.19 4.74 5.06 5.11 5.22 6.47 6.07 6.29 6.43 6.23 7.38 8.26 8.77 9.36 9.82 9.54

6.00 7.00 8.00 9.00 11.00 12.00 13.00 13.00 13.00 13.00 13.00 13.00 13.00 14.00 14.00 21.00 18.40 16.50 14.00 13.50 13.10 12.65 12.25

32.15 67.85 141.99 215.75 323.36 362.91 488.51 576.26 925.22 1035.31 1212.62 1390.66 1383.09 1947.25 2195.75 4835.89 4646.21 4107.73 3086.15 3013.78 2800.70 2468.76 2719.16

Source: MISA, the annual year reports; 1976-1998 * The difference between interest on deposits in commercial banks and the achieved return. The reserves of the two funds have increased from nearly LE 2.31 billion in 1974 to LE 111.86 billion in 1998. In the main time the invested reserves have risen from 86% of the reserves in 1976 to a maximum of 95.51% in 1984 but are now around 90% of the reserves. It can be seen from table (7) that over the period 1976-1998 the main type of investment is deposits in the NIB and other banks. The interest rates on deposits have been rising, reaching a peak value of around 21% in 1991 and are currently around 11-12% per annum. The average rate of return on invested funds was around 4.5% in the 1970s and 5.5% in the 1980s and it had been less than 6.5% until 1992. A lot of negotiations have been made with NIB to increase the given rate of interest on the invested funds over the last decade, (according to a special agreement which concerning the rate of interest on the invested funds). In 1992 the NIB agreed to pay rate of interest on these investments as follows: 1- Rate of interest of 6 % on all the deposits before 1/7/1989, (except for the accumulated

funds of the variable wages where the rate is 8%). 2- “ “ “ of 8 % on all the deposits after 1/7/1989 and before 1/7/1990 3- “ “ “ of 9 % on all the deposits after 1/7/1990 and before 1/7/1991 4- “ “ “ of 11 % on all the deposits after 1/7/1991 and before 1/7/1992 5- “ “ “ of 13 % on all the deposits after 1/7/1992 and before 1/7/1997 6- “ “ “ of 11 % as an average on all the deposits from 1/7/1997

16

This action did not enable the management of the pension funds to improve the average rate of return on the invested funds until the second half of the 1990s because the large part of the deposits was accumulated before 1/7/1989. So that the average rate of return did not exceed 8.1% of the overall invested funds. It was only from 1996 when the average rate of return reached more than 9% and this occurred after the NIB agreed to increase the given interest rate on the invested reserves in the bank to 11% as from 1/7/1997. Although this is good progress towards achieving a reasonable average rate of return, it is still less than the prevailing rate of interest on deposits in the market and particularly the average rate of return in the Egyptian stock market. It still depends also on the discretion of the NIB. This method of investment proved that giving unrealistically low or negative real rates of interest effectively transfer resources back to the state. The problem can be recognised more if we compare the average rate of return on the invested funds with the average rate of salary increase at each actuarial valuation since 1968 as it can be seen in table (8). The average rate of return has been much lower than average salary increases, which explains the high contribution rates for employees and employers.

Table 8. The average rate of return on the invested funds compared with the average rate of salary increase at each actuarial valuation since 1968.

Year 1968 1972 1977 1982 1987 1992 1997 Average Average increase in

salaries (%) 8.62 1.08 7.53 13.44 4.01 9.40 9.86 8.12

Average return on fund (%)

4.50 4.70 4.64 5.19

5.22 6.23 9.82 5.78

Source: Actuarial valuation reports, 1968-1997 It is also useful to compare the annual lost return over the period of 1974-1998 with the actuarial valuation results to show the effect of these lost returns on the outcome of the valuations, as these lost returns contributed significantly to the deficit of the system. Depending on the size of the accumulated fund and the actual experience of the scheme as disclosed at each actuarial review, a summary indication of the scale of the dilemma is given by estimates of the size of deficit as in table (9).

Table 9. Actuarial valuation results of the two

Funds Over the period 1959-1987 (LE m) Valuation Date GSF PPBSF Total

30/6/1959 (47.87) NA NA 30/6/1963 (131.33) 7.36 (123.97) 30/6/1968 (166.18) (8.03) (174.21) 30/6/1972 (307.06) (174.62) (481.68) 30/6/1977 (984.09) (860.88) (1844.97) 30/6/1982 (551.63) (1022.37) (1574.00) 30/6/1987 (738.00) (114.00) (852.00)

Source: Actuarial Valuation Reports; 1959-1997 It can be noticed that the total deficit reached its peak in 1977 and since then has started to decline. It can be argued that the increase in interest rates given by the NIB contributed to this decline of the deficit. As the system is officially applying a full funding method and higher contributions from employees and/or employers cannot be recommended by the system’s actuary because it is not acceptable politically or economically, the deficit has to be met by two resources. The first resource is higher interest rates, equivalent to the prevailing market rates, have to be credited or earned on the invested funds by the NIB. The second is more contributions or financial help from the government in future periods. The higher interest rate required in the

17

future to achieve the funding objective has to be estimated. So that one of the important objectives of the actuarial valuation is to determine the required rate of interest to be given on the invested funds (which is always lower than the market interest rate) to minimise or eliminate the deficit of the Scheme. An actuarial study for measuring the effect of the given interest rate on the deficit of the GSF fund over the period 1982-1987 was carried out by the scheme’s actuary in 1987 (Ibrahim F. etal. 1994). It was found that changing the earned rate of return from 6% (average rate of return achieved on the invested funds mainly in the NIB at the actuarial valuation which carried out in 1987) to 7% decreased the deficit from more than LE 1,000 million to LE 170.13 million. The government is currently encouraging the management of the system to invest part of its funds in the Egyptian stock market to encourage the growth of the stock market. Some analysts are reluctant to agree to this type of investment at the current time as they regard it very risky. It is thought that investing pension funds in capital market requires the market to be adequately regulated and this criterion is not met yet in Egypt, where there is still lack of transparency as to the value of assets. Finally there are significant evidences that the current investment strategy set by the government and managed by the NIB is not effective. It can also be regarded as a significant factor in the deficit of the system. It is feared that the funding position will worsen in future years, placing an increasing burden on the government to amortise the deficit. This will affect the actuarial soundness of the system. It is thought that the solution to some of the problems facing the system (such as the deficit problem) will depend (among other things) on maximising the rate of return on the invested funds in order to enable the system to meet the cost of benefits provided and future liabilities. But the increase in deficit does not arise only from general deficiencies in management and administration and it may also arise from contribution evasion on the part of employers and their workers. Contribution Evasion In some countries, low coverage is the result of widespread contribution evasion. There are many reasons lead to contribution evasion. It could due to high inflation, corruption, lack of trust in the government system, a high unemployment accompanied with lower earnings, or a loose connection between contributions paid and benefits received. Contribution evasion can only occur if three conditions coincide: 1. Employers wish to evade, or place a low priority on making social security contributions

relative to other expenses; 2. Employees who prefer non-payment of contributions, are reluctant to report non-payment

to authorities or are unaware of the non-payment; 3. Government enforcement tolerates evasion or is inadequate to prevent it. Egypt has more than one million people working abroad and large informal sectors of the labour force: the rural self -employed, the urban self-employed and the other who are employed, in one way or another, by informal sector enterprises. A report by the US Embassy in Egypt estimates that the informal sector accounts for at least 50% of the total economy. For these social groups earnings cannot easily be monitored or contributions collected. Moonlighting and unrecorded salaries are a common phenomenon in Egypt particularly with these categories. Also due to the average of the last two years rule these categories have every reason to minimise their contributions in all but the last two years. As a result of the right given to these categories to choose the pensionable salary, they choose the smallest level throughout their life career and they change it to a higher level two years before retirement. There is also a growing trend among workers in the informal sectors not to be covered and even more seriously that some private companies reluctant to cover their workers or to evade contributions. This problem is expected to grow as a result of the shifting from public sector to the private sector. It was easier to collect contributions and taxes from those in formal sector employment than from those in the informal sector.

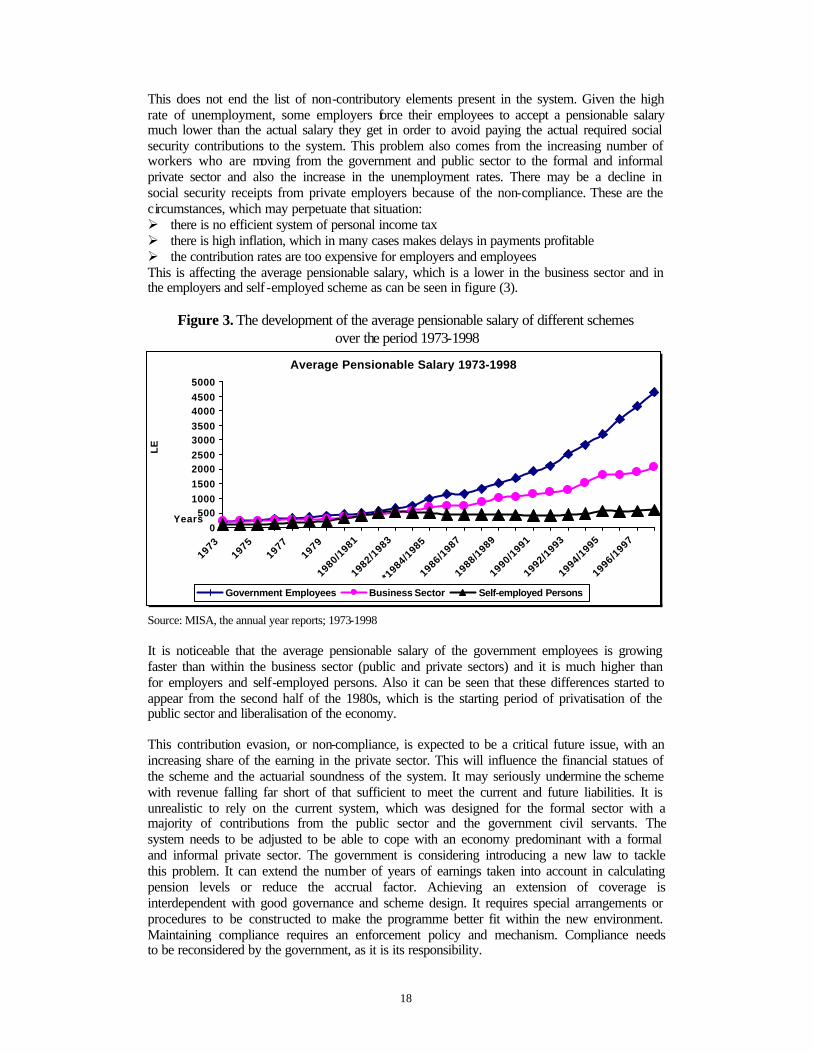

18

This does not end the list of non-contributory elements present in the system. Given the high rate of unemployment, some employers force their employees to accept a pensionable salary much lower than the actual salary they get in order to avoid paying the actual required social security contributions to the system. This problem also comes from the increasing number of workers who are moving from the government and public sector to the formal and informal private sector and also the increase in the unemployment rates. There may be a decline in social security receipts from private employers because of the non-compliance. These are the circumstances, which may perpetuate that situation: Ø there is no efficient system of personal income tax Ø there is high inflation, which in many cases makes delays in payments profitable Ø the contribution rates are too expensive for employers and employees This is affecting the average pensionable salary, which is a lower in the business sector and in the employers and self -employed scheme as can be seen in figure (3).

Figure 3. The development of the average pensionable salary of different schemes over the period 1973-1998

Source: MISA, the annual year reports; 1973-1998 It is noticeable that the average pensionable salary of the government employees is growing faster than within the business sector (public and private sectors) and it is much higher than for employers and self-employed persons. Also it can be seen that these differences started to appear from the second half of the 1980s, which is the starting period of privatisation of the public sector and liberalisation of the economy. This contribution evasion, or non-compliance, is expected to be a critical future issue, with an increasing share of the earning in the private sector. This will influence the financial statues of the scheme and the actuarial soundness of the system. It may seriously undermine the scheme with revenue falling far short of that sufficient to meet the current and future liabilities. It is unrealistic to rely on the current system, which was designed for the formal sector with a majority of contributions from the public sector and the government civil servants. The system needs to be adjusted to be able to cope with an economy predominant with a formal and informal private sector. The government is considering introducing a new law to tackle this problem. It can extend the number of years of earnings taken into account in calculating pension levels or reduce the accrual factor. Achieving an extension of coverage is interdependent with good governance and scheme design. It requires special arrangements or procedures to be constructed to make the programme better fit within the new environment. Maintaining compliance requires an enforcement policy and mechanism. Compliance needs to be reconsidered by the government, as it is its responsibility.

Average Pensionable Salary 1973-1998

0

5001000

1500

20002500

30003500

40004500

5000

19731975

19771979

1980/1981

1982/1983

*1984/1

985

1986/1987

1988/1989

1990/1991

1992/1993

1994/1995

1996/1997

Years

LE

Government Employees Business Sector Self-employed Persons

19

Unemployment and Early Retirement One of the challenges facing the social security system in Egypt is soaring unemployment, a phenomenon that did not exist, at least officially, under the state-owned economy. A lower labour force participation ratio for younger age-groups could be a further burden on the social security system by decreasing the number of contributors and this is linked to the problem of unemployment. Employment reached its peak in 1975 and since then has been decreasing, as a mirror image, unemployment was quite reasonable during the 1980s, but has increased dramatically over the last decade as it can be seen in figure (4). Figure 4. Development of unemployment rates 1949-1997

Source: Central Agency for Public Mobilisation and Statistics (CAPMAS) The official unemployment rate is close to a range of 10-12%. It is expected that the unemployment rate may get higher in the near future as a result of privatising more public companies. Although the sharp increase in unemployment is due to the transition towards a market economy it is also a mix of many other different effects and factors. The system has been complemented by unemployment benefits, but they are of short duration and little is available in terms of no-training and job protection. This forced the Egyptian government to pay compensations to the workers of the privatised companies who became unemployed in order to facilitate the selling of these companies and also give them early retirement income. To alleviate the future burden of the old-age social security provision on the economy and public finances it is crucial to increase labour force participation. Ultimately much depends on the economic growth of the country, the transformation of its labour force into one largely incorporated into the formal sector of the economy, and a greater maturity in its political and corporate governance. This will take time. The government is encouraging and using early retirement option to achieve two goals. Firstly, to reduce the effect of increasing unemployment rates by easing the pressure on the labour market (enabling the long-term employed to retire and alleviating youth unemployment). Secondly: easing the process of privatising the public sector and to ease the consequences of the economic reform. Early retirement is often seen as a “painless way to cut unemployment or to cut the number of redundant employees”. It is thought that this measure would stabilise the labour market and free new vacancies for young entrants; this has not materialised, as labour force participation among the young continued to decrease in the early 1990s. The increasing trend in favour of taking the early retirement option was very noticeable over the last decade. This was reflected in a steadily increasing number of

Unemployment Rates 1949-1997

0

2

4

6

8

10

12

14

194919

5219

5519

5819

6119

6419

6719

7019

7319

7619

7919

8219

8519

8819

9119

94

Years

%

20

pensioners during this period, which has sharply accelerated since 1990. This can be seen from figure (5), which shows the percentage of the number of early retirement pensioners to the total number of pensioners over the period 1991-1998. In 1998 the number of early retirement pensioners represented 12.43% of the total number of pensioners compared with 4.04% in 1979.

Figure 5. The development of the percentage of the number of early retirement pensioners to the total number of pensioners over the period 1991-1998.

Source: MISA, the annual year reports; 1990-1998 It is expected that the number of early retirements may increase over the next few years for the purpose of releasing more jobs for young people to ease the high unemployment. An additional burden is created because early retirement is without cuts to the pension benefits and offers generous payoffs. The early retirement option is a very important measure, as its effect on the actuarial soundness of the pension system needs to be analysed very carefully. The early retirement benefits represented 11.5% of the total benefits paid in 1998 compared with 9.8% in 1992 and 5.8 in 1981. The government actuary indicated in the latest actuarial valuation reports that these increases in the early retirement rates contributed significantly to the deficit of the system (Ibrahim F. etal 1994). These may make the system too expensive to maintain and require an increase in the financing. There are some other risks, which need to be considered later, such as those risks related to economic progress. Also important those demographic risks arising from decreases in birth rates, increasing longevity and their effect on the present value of liabilities borne by the scheme. The effects of these risks on the social security pension system will be discussed in another paper.

% of Early Retirement Cases to the Total Pension Cases Over the Period 1991-1998

9.50

10.00

10.50

11.00

11.50

12.00

12.50

1991 1992 1993 1994 1995 1996 1997 1998

Year

%

21

Conclusion Egypt is making transition from a planned economy to a market economy, but there is strong likelihood that the provision of retirement income will remain largely a public sector responsibility. Currently the main two components of the Egyptian social insurance system are the state scheme and the occupational pension funds. The state still has a monopoly of pension provision and, with low salaries and wages in the still mostly state-run economy, social security applies to everyone, even though it has some universal restrictions on the benefits to achieve the goal of uniformity and redistribution. Currently, the proportion of employees depending on the state for their retirement income is around 98%. This is due to the nature of the scheme, which makes the state the main and only provider of pensions, while the occupational schemes just provide an extra income usually in the form of a lump sum received on retirement. The defined benefit and contribution system offers the public the following advantages: • a stable rate of contributions for both employees and employers; • a defined benefit equal to pre-determined fraction of final pay; • no risk of insolvency, because the government is committed to covering any deficit; • additional benefits (such as pension increases) funded by the government. Although the system generally satisfies many of the criteria for a good pension system, such as, redistribution, fairness, certainty, adequacy, and coverage, a lot of improvement is needed. The system must find a suitable way of tackling the problems, which delay its development. The system has a complicated legislation structure, which needs to be revised. Also the problem of dealing with inflation and the investment strategy of the funds need to be reformed. Political decision is a crucial factor in making any changes, which is a feature of the most of the state social insurance pension systems. The recent developments of the reform process of the Egyptian economy have left major effects on the social insurance pension scheme. The system needs to be reformed to survive the economic reforms of liberalisation and privatisation and to be prepared to face the expected demographic changes. The government is currently considering a new legislation, which may eliminate some of the weaknesses in the current pension environment and improve the investment policy. The improvement of the investment policy is a crucial factor, as it can help with financing the extra costs of funding the early retirements encouraged by the government, increasing the pensions by more than 10% every year and controlling the deficit. The government is using some of the proceeds of privatisation to finance an annual increase of 10-15% of the social security benefits every year to improve the real value of the benefits. Although the government is promising to finance these extra benefits from the general revenues it will depend on the financial status of the state to be able to achieve that. The government recently decided to privatise the management of part of the fund, to allow investment in non-governmental instruments and the capital markets. In the light of these changes, it has been proposed that the current constraints on investment strategy should be eased to allow direct investment in commercial projects, the stock market, real assets, and the other instruments. A special law, whose main aim is to improve investment management and to offer more options to employees, may be needed to regulate this system very soon. Those with incomes above L.E. 1200 would need additional pension provision in order to maintain the lifestyle they enjoyed during their working lifetime and this can be achieved through private pensions. The government is trying to form a new strategy to shift some responsibilities to the private sector by introducing some sort of private pension plans in the near future. Its target is likely to be high-income earners with some sort of tax incentives to encourage participation and widen the population coverage. It is also encouraging the creation of supplementary, privately run occupational pension schemes. It has introduced tax incentives to encourage the growth of occupational schemes but not private pension funds. It has introduced a new system for social assistance which will give additional pension to about

22

665 thousands families and cost about 46.55 million pound a month. This will take place from August 2000. The government has to reconsider introducing system of contracting out in order to reduce the number of people depending on the state for their retirement income. The final averaging period for pensionable salary needs to be increased in order to reduce one sort of contribution evasion. Pensions have to be adjusted annually or to be linked to the RPI in order to maintain the real value of benefits. As so often, there has been a trade-off between actuarial and political considerations, so it remains to be seen how effective these reforms will be. Bibliography 1. “Actuarial Valuation Reports”, (1962-1992). Government Sector Fund, Cairo, Egypt. 2. “Actuarial Valuation Reports”, (1962-1992). Private and Public Business Sector Fund,

Cairo, Egypt. 3. Booth. P. M. & Stroinski K. (1994), “The development of competition and Privatisation

of Insurance Institutions in Poland: lessons for the actuarial Profession and regulators”, Communist Economies & Economic Transformation, Vol. 6, No. 3, 1994.

4. Central Agency for Public Mobilisation and statistics, (1998). “The statistical annual year book”, Cairo, Egypt.

5. Centre for Insurance Studies in Egypt, (1988). “Guide to provisions and procedures for Social Insurance Scheme in Egypt”, Centre for Insurance Studies, Cairo, Egypt.

6. Centre for Insurance Studies in Egypt, (1988). “The main features of Social Insurance Policy in Egypt”, Centre for Insurance Studies, Cairo, Egypt.

7. David E. Philip, (1997). “Public Pensions, Pension Reform and Fiscal Policy”, European Monetary Institute.

8. Egyptian Financial Group, (1996). “Guide to the Egyptian Capital Market”, Cairo, Egypt. 9. Government Actuary’s Department, UK, (1997). “Report on the non-state pension funds

in Egypt”, The government Actuary’s Department, UK. 10. Ibrahim F. & Nagib S., (1994). “Financing and funding the Egyptian pension Scheme”,

The Academy of Technology and scientific Research, Cairo, Egypt. 11. Ministry of Insurance and social Affairs, (1998). “The Achievements and work results

year book”, The Ministry of Insurance and social Affairs, Cairo, Egypt. 12. Mohamed, A.F.S., (1997). “The Egyptian Pension Scheme, Present and Future

Development,” City University, London. 13. Nagib S., (1985). “Actuarial soundness of the Egyptian Social Insurance Scheme

(technical basis and pace of funding)”, Journal of the Faculty of Commerce, Cairo University, Egypt.

14. Sabra, E.A.E., (1998). “Actuarial Modelling of the Egyptian State Pension Scheme”, City University, London.

15. The World Bank, (1993). “ Report on Complementary Pension Funds in Egypt”, The World Bank, Cairo, Egypt.