Embed Size (px)

Citation preview

THE EFFECT OF REGULATION BY SASRA ON PERFORMANCE OF SMALL

SACCOS IN KENYA

BIWOTT KEVIN

A PROJECT SUBMITTED TO SCHOOL OF BUSINESS IN PARTIAL FULFILMENT

…OF THE REQUIREMENT FOR THE AWARD OF A MASTER OF BUSINESS

..ADMINISTRATION (STRATEGIC MANAGEMENT) DEGREE, OF KABARAK

UNIVERSITY.

2014

ii

DECLARATION

This research report is my original work; I hereby state that it has not been presented in the same

form to any other Institution or Kabarak University for an academic credit.

Signature……………………….. Date…………………..

Biwott Kevin

GMB/NBE/1213/09/12

This project has been submitted for Examination with our approval as university supervisor.

Signature………………………. Date…………………..

Dr. Irene Asienga

Signature……………………… Date……………………

Mr. Firtz Mulumia Gerald Oketch

iii

DEDICATION

This project is dedicated to my family and more so to my wife and my son and those who

inspired and supported me during my course work and the final completion of this research

work. You are the pillars of my life.

iv

ACKNOWLEDGEMENT

I wish to sincerely recognize the efforts of my supervisors Dr Irene Asienga and Mr. Gerald

Oketch for their patience, guidance, resilience, support and time committed throughout the

period of this research proposal.

v

LIST OF ABBREVIATIONS

ACCOSCA -African Confederation of Cooperative Savings and credit Association.

BOSA - Back Office System Administration.

CAMEL - Capital Adequacy, Asset Quality, Management, Earnings & Liquidity.

CIF’s - Cooperatives Financial Institutions.

DTS - Deposit Tanking Sacos

FOSA - Front Office System Administration.

FSA - Financial Services Authority.

GDP - Gross Domestic Product.

KUSCCO - Kenya Union of Savings and Credit Cooperatives

SACCOs - Savings and Credit Cooperatives.

SASRA - Sacco Society Regulation Authority.

MUSCCO - Malawi Union of Savings & Credit Cooperatives

NCUA - National Credit Union Administration.

WOCCU - World organization of Credit Cooperative Union.

vi

ABSTRACT

A Sacco society is defined as a user-owed, user-controlled business that distributes benefits

based on patronage. Direct government regulation of Saccos came about through legislation

enacted by the Kenyan parliament, the Sacco Act of 2008. The regulations were necessitated by

the need to give proper structures and prudential standards to Saccos especially those involved in

deposit taking activities referred to as FOSAs and after the pyramid scheme saga. The FOSAs

carry out banking business with members of the public most of whom are not their members.

Since the Saccos were not regulated by central bank or the Banking Act, the government forged

direct regulation through Sacco Society Regulation Authority. This study hence sought to find

out the effect of statutory deposit, management qualification and quality and membership

regulations requirements on the performance of small Saccos. The study was based in Kenya and

targeted small. Survey research design was used. Data was collected by use of structured

questionnaires. Respondent comprised of Small deposit taking Sacco staff. The data collected

was analyzed through descriptive and inferential statistical techniques. The findings were that

Sacco performance will improve with implementation of the Sasra regulation. Statutory deposit

regulation will highly affect Sacco liquidity, members also showed confidence in qualified

managers based on performance but felt that membership regulation is punitive. In conclusion

the regulation has positive effects on Saccos and hence we recommend compliance by Saccos to

the regulations.

Key words: Sacco regulation, Small Saccos performance, Sacco regulation Authority (Sasra)

vii

LIST OF TABLES

Table 1.1 Performance Measure…………………………………….………………………………………….……..6

Table 1.2 Sacco Performance………………………………………………………………………..…………..……..8

Table 2.1 Conceptual Framework……………………………………………………………………………..…..…21

Table 3.1 Sacco Details…………………………………………………………..….......................................24

Table 4.0.1 Baseline Characteristic of Data……………………………………..………………….….......….27

Table 4.0.2 Tests of normality………………………………………………………...……………………..….…...28

Table 4.0.3 Support for direct regulation by government……………………….……………..….….29

Table 4.1.1 Does statutory deposit requirement affect Sacco performance……...…..………29

Table 4.1.2 Effects of Statutory deposit factors……………………………………………………..………..30

Table 4.1.3 Chi-Square Tests Effect of Statutory regulation on the amount of deposit……31

4.1.4 Spearman rank correlation on the relationship between statutory deposit factors.31

Table 4.2.1 management quality and qualification requirement……………………...……………32

Table 4.2.2 Management quality and qualification requirement factors…………………….…34

Table 4.2.3 Spearman rank correlation on the relationship of factors……………….…………..35

Table4.3.1Support for the introduction of membership requirement……………….………....36

Table 4.3.3 membership requirement factors……………………………………………………………....37

Table 4.3.7 Regression analysis model summary………………………………….......................….38

viii

Content TABLE OF CONTENTS

Contents

COVER PAGE............................................................................................... Error! Bookmark not defined.

DECLARATION ......................................................................................................................................... ii

DEDICATION ........................................................................................................................................... iii

ACKNOWLEDGEMENT ............................................................................................................................ iv

LIST OF ABBREVIATIONS .......................................................................................................................... v

ABSTRACT .............................................................................................................................................. vi

CHAPTER ONE. ........................................................................................................................................ 1

INTRODUCTION. .................................................................................................................................. 1

1.1 Background of the Study. ............................................................................................................... 1

1.2 Global Perspective of Saccos. ......................................................................................................... 4

1.2.1 African Perspective ..................................................................................................................... 4

1.2.3 Kenyan Perspective ..................................................................................................................... 5

1.3 Problem Statement. ..................................................................................................................... 10

1.4 Objectives of the Study ................................................................................................................ 11

1.4.2 Specific Objectives .................................................................................................................... 11

1.5 Research Hypothesis .................................................................................................................... 11

1.6 Justification of the Study .............................................................................................................. 11

1.7 Significance of the Study .............................................................................................................. 12

CHAPTER TWO....................................................................................................................................... 13

2.0 INTRODUCTION............................................................................................................................ 13

2.1 Theoretical Review. ..................................................................................................................... 13

2.2 Empirical Review .......................................................................................................................... 16

2.2 Statutory deposit fund requirement on savings ............................................................................ 16

ix

2.3 Management qualification and quality ......................................................................................... 18

2.4 Membership regulation requirements ......................................................................................... 20

2.5 Conceptual Framework ................................................................................................................ 22

2.6 Summary and Knowledge Gap ..................................................................................................... 23

CHAPTER THREE .................................................................................................................................... 24

RESEARCH METHODOLOGY ................................................................................................................... 24

3.1 Introduction ................................................................................................................................. 24

3.2 Research Design........................................................................................................................... 24

3.3 Target Population of Study ........................................................................................................... 24

3.4 Sampling ...................................................................................................................................... 24

3.5 Data Collection Methods.............................................................................................................. 26

3.6 Reliability and Validity of Data Collection Instrument ................................................................... 26

3.7 Data Analysis Techniques ............................................................................................................. 26

3.8 Ethical Considerations .................................................................................................................. 27

CHAPTER FOUR ..................................................................................................................................... 28

ANALYSIS, PRESENTATION AND DISCUSSION ......................................................................................... 28

Introduction ...................................................................................................................................... 28

4.0.1 Baseline Characteristic of Data .................................................................................................. 28

4.0.4 Support for direct regulation by government in SACCOS ........................................................... 30

4.1 Effect of statutory deposit fund requirement on performance of small Saccos in Kenya ............... 31

4.1.4 Spearman rank correlation on the relationship between statutory deposit factors .................... 34

Table 4.2.2 Management quality and qualification requirement factors ............................................. 36

4.3.1 Support for the introduction of membership requirement by SASRA ......................................... 38

4.3.1Membership requirement factors .............................................................................................. 40

4.3.8 Hypothesis Testing .................................................................................................................... 41

CHAPTER FIVE........................................................................................................................................ 42

SUMMARY, CONCLUSION AND RECOMMENDATION.............................................................................. 42

x

5.1 Introduction ................................................................................................................................. 42

5.2 Summary of the findings .............................................................................................................. 42

5.4 Conclusion ................................................................................................................................... 43

5.4 Recommendations ....................................................................................................................... 43

5.5 Further Research ......................................................................................................................... 44

REFERENCE ............................................................................................................................................ 45

QUESTIONNAIRE.................................................................................................................................... 50

1

CHAPTER ONE.

INTRODUCTION.

This chapter presents the study background and general insight on the topic researched on,

problem definition, objectives of the research, research questions, research purpose and also

justification of the topic studied. The scope of the study was also given at this stage.

1.1 Background of the Study.

The cooperative idea was started in Rhine province of Germany in 1847 as a result of great

famine that affected the production of wheat and potatoes, the staple food for the locals. Few rich

people from the province under the leadership of Friedrich R. Wilhelm decided to collectively

store their produce and then sell it cheaply among its members in case of low production. This is

among the first forms of cooperatives (Prinz, 2002).

Herman Frank also was a pioneer in cooperatives; he consolidated two pilot projects in to credit

unions in 1852 to finance poor rural communities. The rural communities were considered

unbankable because of very small, seasonal cash flow and limited human resource (WOCCU,

2008). The project was very successful and hence increased the people living standard.

The standard definition of a corporative in US is a user-owed, user-controlled business that

distributes benefits based on patronage rather than investment (Zeuli and Croop, 2004). The coop

user is a person that supplies produces for purchase or process and hence benefits on service

base. Its hence important to note that in Saccos the members have mutual and equal ownership

on the business despite their contribution.

International Cooperative Alliance (ICA) is a non-governmental organization that was

established in 1895 as an umbrella organization to promote friendly and economic relations

between cooperative organizations throughout the world. The ICA aims to promote exchange of

information such as news and statistics between cooperatives through research and reports,

directories, conference and publications (Onuoha, 2002).

2

International Cooperative Alliance regards Saccos as an autonomous association of persons

united voluntary to meet their common economic, social and cultural needs and aspirations

through jointly owned and democratically controlled enterprise.’ This is the most accepted

definition as ICA is the biggest global cooperative body with over 230 nations of the world

subscribing to its membership (ICA 2008).

The co-operative principles are guidelines by which co-operatives exist and they include:

Voluntary open membership, open to all persons able to use the services and are willing to

accept the responsibilities of membership without discrimination; Democratic member control,

members participate actively in setting their policies and making decisions - one man one vote;

Member economic participation, members contribute equitably; Autonomy and Independence,

the legal personality is separated from its members; Educate, train and Information, empower

members; Co-operation among cooperatives, work together on all levels to achieve synergy; And

Concern for community, always work for sustainable development (ICA, 2013).

Traditionally, the organization of the co-operative movement is in tiers, which form a pyramid

shaped structure. At the bottom of the structure are primary co-operative societies whose

membership consists of individuals. The primary societies serve their members directly,

(Mugambwa, 2006). The next block in the pyramid is secondary societies consisting of

association of the primary Saccos. They come together to enjoy economies of scale in dealing

with bulk sourcing. At the top of the pyramid is apex unions consisting of association of

secondary Saccos. They come together to strengthen the movement and lobby for favorable

legislation from governments of the day.

There are several types of cooperatives from around the world, the major type Credit unions,

they are cooperative financial institutions that are owned and controlled by their members to

provide the same financial services as banks but adhere to cooperative principles (Schram 2010).

Housing cooperatives forms a legal mechanism for ownership of housing where residents own

shares reflecting their equity in the cooperative's real estate or have membership and occupancy

rights in the cooperative and they underwrite their housing through paying subscriptions or rent

(Ridley-Duff, 2009).

3

Agricultural or farmers' cooperatives help farmers pool their resources for mutual economic

benefit. Agricultural cooperatives are divided into agricultural service cooperatives, which

provide various services to their individual farming members, and agricultural production

cooperatives, where production resources such as land or machinery are pooled and members

farm jointly. Vieta (2010).

Women cooperative or the famous merry-go-round play a particularly strong role in empowering

women especially in developing countries. They allow women who might have been isolated and

working individually to band together and create economies of scale as well as increase their

own bargaining power in the market. During International Women's Day in 2013, Dame Pauline

Green said, "Cooperative businesses have done so much to help women onto the ladder of

economic activity. With that comes community respect, political legitimacy and influence

Grimes and Milgram (2000).

The UN declared that the 2012 was the International Year of the Cooperatives (IYC). In

launching the year, the UN secretary general Ban Ki Moon said “Cooperatives are a reminder to

the international community that it is possible to pursue both economic viability and social

responsibility.” It is also a fact that the cooperative movement has been an important vehicle of

empowerment and liberation from economic misery to many poor people across the world. The

world cooperative movement has approximately one billion people making it one of the largest

constituencies in the world. On the other hand, 3 billion people do benefit from the cooperative

movement” (ICA, 2013).

Regulation is a rule or law designed to govern conduct. It functions by creating limits, constrains,

duty or responsibility. It can take many forms; legal restrictions promulgated by a government

authority, contractual obligations that bind many parties, self-regulation by an industry such as

through a association, social regulation, co-regulation, third-party regulation, certification,

accreditation or market regulation (Cunningham 2007). In its legal sense regulation can be

distinguished from primary legislation on the one hand and judge-made law on the other.

4

1.2 Global Perspective of Saccos.

The regulations of Saccos were introduced in many places around the world. India adopted a

regulation that gave cooperatives a hybrid business alliance system that has enabled the

cooperative owned business to grow to big empire of companies and own vast properties around

and outside India (Fischer and Cuevas, 2006). UNISAP Federation is responsible for Sacco

control in Mexico and has seen Saccos grow to have lower risk than banks. The Saccos have

hence grown and patronizes more than 60% of the total Mexican rural population (Be’roff,

2008).

Brazil was an early adopter of cooperative model and as early as 1874 they had Teresa Christina

cooperative in Parana formed by Jean Maurice a medical doctor from France. The regulation of

cooperatives here was marked by legislation in 1890 to address involvement of military

personnel in cooperatives. Canada adopted a DEA (data envelopment analysis) system that

checks; asset to equity ratio and a modified Z-score of all credit unions and compares them

weekly to a fixed score. This has made Saccos to operate prudently hence fewer cases of

cooperative failure (Pille and Puradi, 2002).

In U.S credit unions were regulated by non banking financial institution laws SEC (securities and

exchange) Act. The system consists of complex rules that guide the operations of credit unions in

the country. The system was introduced on the aftermath of great depression of 1929 and was

meant to improve the public confidence on financial institution; it has been in force to date.

(Kumar et al, 1997).

1.2.1 African Perspective

In Egypt, regulation of credit union controlled strictly as the government sets the ceiling interest

rate for issuing loans. Credit unions are also registered and managed directly by ministry of

economy hence few cases of mismanagement of the unions. The regulations are however too

stringent hence lead to the rise of an underground lending market by unregistered individuals

come together and loan money amongst themselves (Mahmoud and Wright, 2000).

5

Cooperative societies are very popular in Nigeria. Onuoha (2002) in his study of cooperative

history in Nigeria state that modern cooperative societies came as a result of the Nigerian

cooperative society law enacted in 1935 following the report submitted by C. F. Strickland in

1934 to the then British colonial administration on the possibility of introducing cooperatives

into Nigeria. Through cooperatives, farmers could pool their limited resources together to

improve agricultural output and this will enhance socio-economic activities in the rural areas

(Ebonyi and Jimoh, 2002).

The Sacco regulation 2005 of Tanzania restricted Sacco with stringent rules on composition and

operations of Saccos. This has caused a steady drop in the number of Saccos and other

microfinance institutions have taken over. In this case of stringent regulation, deregulation was

direly needed to revive the sector (Rubambey, 2005).

1.2.3 Kenyan Perspective

The co-operative nature of the Kenyan people can be traced to the pre-colonial traditional

societies where people cooperated in several activities such as hunting, farming, building houses,

taking care of animals and in many other important chores. The Kikuyu had Ngwataniro (work

group) that members assisted each other in constructing houses (KUSCCO Magazine, 2012). The

Kalenjin also had organized groups (Kokwet) that were working on member’s farms in rotation

especially during planting and harvesting seasons, this practice has been preserved to date in

many areas. The Luo people had organized vibrant groups notably the youth’s Nyolwaro that

was responsible for thatching new member’s huts, farming or fishing together to enable synergy

and provision for the young families.

The first formal Savings and Credit Co-operative Society (SACCO) in Kenya was at Lumbwa,

Rift Valley in 1908. The Lumbwa Sacco was formed by white settlers to enable its members

bargain for better fertilizer and seeds prizes Chebor (2008) ‘Understanding cooperative

movement and its values’. The Sacco was also to provide services to members and enable them

seek competitive markets but the members did not collectively sell their products. The Sacco was

however restricted to the white settlers only and no person of African or Asian persuasion could

join.

6

The formation of department of co-operative development (later Commission of Co-operatives

Development) in 1946 advocated for agriculture based Saccos and by 1954 there were over 500

Saccos in central province patronizing over 170,000 members with a turnover of two hundred

and eighty thousand shillings; the most successful being Makueni Settlement Sacco which paid a

dividend of 7% on member’s savings (Cooperative Bank, 2010). The cooperatives also played a

major role in liberalization of Kenya through political mobilization against colonialism. In 1954

co-operators moved and join Mau-Mau to help end the white man’s rule in Kenya (Odido, 2008).

The context of cooperatives sector in Kenya consists of primary Saccos consisting marketing

societies, farming societies, housing societies, consumer societies, producer society and credit

societies as per Odido (2008); secondary Saccos are small Saccos that have grown to offer their

members with various services and lastly apex cooperative bodies firms that offer support

service to Saccos the likes of CIC Insurance, Kuscco Limited, Co-operative Bank, Co-operative

College and ALCO and ICA Kenya.

Kenya is regarded as the leading country in Africa in co-operative movement by African

confederation of cooperative savings and credit associations (ACCOSCA, 2013). There are

10,800 registered co-operatives Societies with a membership of 6 million. Co-operatives have

created about 250,000 direct employments and 5.9 million people benefit indirectly. The sector

holds 31% of total national savings and contributes 46% of the national GDP. It has 70% of the

coffee market, 76% dairy, 90% pyrethrum, and 95% of cotton (Ochanda, 2013).

Sacco size determinants are measured on the basis below by Daves Grace (Vice president Woccu

in analysis of the Sacco balance sheet and pearl. Protection effective financial structure, asset

quality, rates of return and cost, liquidity and sings of growth. Camel structure is acronym of

capital adequacy, asset quality, Management and liquidity.

Sasra uses a standard template in determining the size of Saccos and how to regulate and cluster

them. They focus on the loans, deposits and asset base Njuguna (2012). Small Saccos are

considered to be those with asset base of below 1 Billion while Saccos with savings between one

and three billon are considered medium while Saccos with over four billion are large Saccos.

7

Table 1.1 Performance Measure

SACCOS

NO.

ASSETS DEPOSIT LOANS

Asset

Size 2012 2011 2012 2011 2012 2011 2012 2011

CATEGORY

kshs

kshs kshs kshs kshs kshs kshs kshs

LARGE

Above

4B

10

9

94,439

80,198 71,631

53,928

78,164

58,996

MEDIUM 1B-4B

41

38

79,982

70,003 55,720

41,526

57,978

51,632

SMALL

Below

1B

73

77

27,485

27,403 18,734

31,981

18,275

24,915

TOTAL

124

124

201,906

177,604 146,085

127,435

154,417

135,543

Source: Research data 2014

The movement has however faced myriad problems of corruption; embezzlement of funds; HIV

Aids pandemic crippling the members; negative political influence and the latest is formation of

pyramid schemes under Ministry of Co-operatives that robed many Kenyans their savings.

(Kuscco, 2010) The government undertook reforms on the Saccos industry that passed new

Saccos bill 2008 (Republic of Kenya 2007; International Monetary Fund 2007; The Kenya High

Commission in the United Kingdom, 2007).

Co-operative Societies ordinance Act of 1931 by the colonial government marked the first

intervention for cooperatives by government. The Act was replaced in 1932 and 1945 but all the

legislation were based on segregation and disenfranchising the native communities (ICA, 2002).

In 1944 the colonial government sent W.K Campbell to investigate the possibilities of Africans

participating in Co-operative Societies and he affirmed that it would help in improving living

standard. By 1946 the colonial government changed their tact to support the idea of co-

operatives as a tool to empower natives due to rising opposition on their apartheid approach to

matters. The legislation of cooperatives in Kenya has been strong and metamorphose from the

cooperative ordinance act of 1931 which was repealed in 1932 and later in 1945. The colonial

government in 1946 established Department of cooperatives to register Saccos. The first law

8

governing Saccos was Cap 490 of Kenya formulated in 1966 based on International Labour

Organization, this was later replaced by Co-operative Societies Act, 12 of 1997.

According to Kenya law reports, the Sacco Act No. 14 of 2008 will affect operation and

reporting of Saccos. Saccos are required to hire qualified staff for their book keeping and a

C.E.O of a Sacco is required to have a minimum of a masters degree in business field. The

Saccos must also deposit 10% of their total member deposits or a minimum of ten million Kenya

shillings to a statutory deposit fund in Sasra that is meant to act as insurance for the deposits. The

Act requires that all members of a Sacco be homogeneous. This implies that Saccos should be

composed of members with the same background and also composed of Kenyans only. Kioko

(2012)

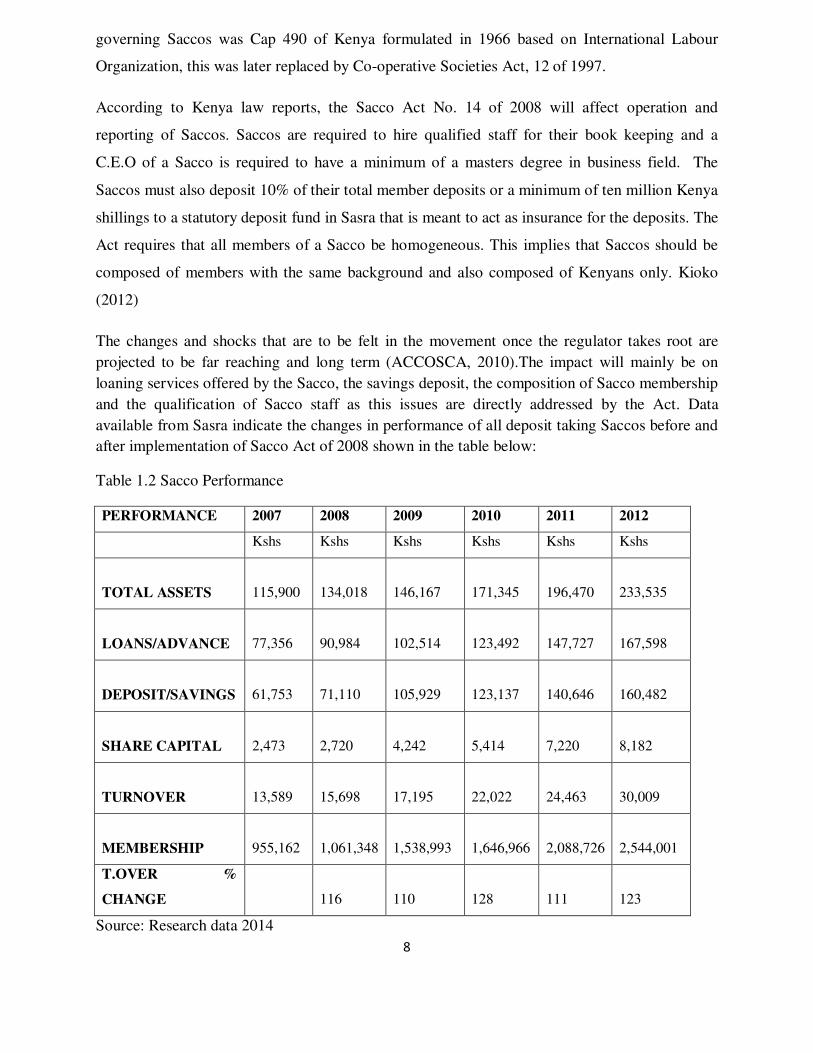

The changes and shocks that are to be felt in the movement once the regulator takes root are

projected to be far reaching and long term (ACCOSCA, 2010).The impact will mainly be on

loaning services offered by the Sacco, the savings deposit, the composition of Sacco membership

and the qualification of Sacco staff as this issues are directly addressed by the Act. Data

available from Sasra indicate the changes in performance of all deposit taking Saccos before and

after implementation of Sacco Act of 2008 shown in the table below:

Table 1.2 Sacco Performance

PERFORMANCE 2007 2008 2009 2010 2011 2012

Kshs Kshs Kshs Kshs Kshs Kshs

TOTAL ASSETS

115,900

134,018

146,167

171,345

196,470

233,535

LOANS/ADVANCE

77,356

90,984

102,514

123,492

147,727

167,598

DEPOSIT/SAVINGS

61,753

71,110

105,929

123,137

140,646

160,482

SHARE CAPITAL

2,473

2,720

4,242

5,414

7,220

8,182

TURNOVER

13,589

15,698

17,195

22,022

24,463

30,009

MEMBERSHIP

955,162

1,061,348

1,538,993

1,646,966

2,088,726

2,544,001

T.OVER %

CHANGE

116

110

128

111

123

Source: Research data 2014

9

The table above shows the performance of Saccos in various fronts. The total number of

members in registered Saccos sharply rose by 45% immediately after enactment of the

regulation. The turnover marginally increased by 9% over the same period. This hence show that

that the regulation directly affect the performance of Saccos.

The regulations being introduced are important as they are meant to provide minimum

operational and prudential standards in Sacco societies (Wanyoike, 2013). It is safe to regulate

Saccos as they take deposit from its public and any mismanagement or embezzlement may cause

financial problems to millions of people or even cause panic in the Sacco movement. The

regulation will also help in customizing Saccos to give uniform products hence avoiding cases of

exploitatively interest rates. The regulator will also help in realizing that members who serve as

staff in Saccos are qualified to hold their current positions. This goes a long way into realizing

proper and quality services to Sacco members hence it is important to introduce the new

regulations.

10

1.3 Problem Statement.

The Sacco reforms affected mainly deposit taking Saccos that operate Front Offices (FOSA)

while the ones operating back offices (BOSA) only will not be subjected to the new requirements

immediately. A FOSA means that a Sacco operates a deposit taking account just as a typical

current account in banks. BOSA means back office services i.e. the loaning activities and

advocacy for members. According to KUSCCO (2010) by the month of May 2010 over 8,500

Saccos representing more than 80% operated a FOSA and hence required to comply with the

new regulations (Sacco Act No. 14 of 2008).

Previous researchers (Zeuli and Cropp 2013, Gordon and McClathey 1999, Grossman and olive

2002, Huppi and Fedder 2010) Kioko (2012), and Wanyoike (2013) focused mainly on Sacco

performance either financially or non financial. However the impact of direct control by

government through regulators like Sasra on the performance and sustainability of small Saccos

had not been fully addressed. This study therefore sought to explore the effect of regulations by

Sasra on performance of small Saccos in Kenya to fill existing knowledge gap.

11

1.4 Objectives of the Study

1.4.1 General Objectives

To determine the effect of Sasra regulation on performance of small Saccos in Kenya

1.4.2 Specific Objectives

i) To determine the effect of statutory deposit fund requirement on performance of

small Saccos in Kenya.

ii) To determine the effect of management qualification on the performance of small

Saccos in Kenya.

iii) To determine the effect of membership regulation requirements on performance of

small Sacco in Kenya.

1.5 Research Hypothesis

In an attempt to achieve the above objectives, this study developed the following null hypotheses

i) Ho1: Statutory deposit fund requirement has no significant effect on performance of

small Saccos in Kenya.

ii) Ho2: Management qualification and quality has no significant effect on the

performance of small Saccos in Kenya.

iii) Ho3: Membership regulation requirements has no significant effect on performance

of small Saccos in Kenya.

1.6 Justification of the Study

The cooperative movement in Kenya had grown tremendously since inception in 1931 when the

first ordinance to regulate their operations was enforced. Saccos had moved from their traditional

saving and lending activities to Investments, banking services through front office and back

office services according KUSCCO LTD (2010). The SACCOs held huge deposits amounting to

Kshs.250 billion in form of member’s savings and accumulated funds from previous business

activities over the years. To be able to grow and compete in the financial market, regulation was

necessary hence the justification of the above study.

12

1.7 Significance of the Study

It will help Sacco members understand the new regulations Requirements and how it will impact

on their membership. Those in affected field like international traders will know how best to act

to cushions themselves against the stringent regulation. The non members utilizing the Sacco

products will also be advised on steps to take to comply with the new regulation.

The employees in Saccos will benefit from the research as they will understand in depth what the

regulator requires them to do and the professional and ethical requirements introduced. They will

also get to understand the various job requirements, description and qualification expectation of

their current positions.

The management team includes the board of directors and the line managers, they will benefit in

understanding the regulators effect on their Sacco and the ways they can avoid or restructure

their Saccos to be in line with the new regulation rules. It will also help the board of directors to

change their Sacco strategic plans to conform to regulations and hence gain assurance of

continuity.

13

CHAPTER TWO.

LITERATURE REVIEW

2.0 INTRODUCTION.

The purpose of literature review is to provide background of the information taken in the area of

study. Overview of literature in respect to the impact of Sacco regulation on Small Saccos was

discussed here.

2.1 Theoretical Review.

According to Zeuli and Cropp (2004) cooperative principles and practice in 21st Century, People

who cooperate organize and belong to cooperatives do so for economic, social and even political

reason. Cooperating is a satisfactory way of achieving one’s own objective while at the same

time assisting others in achieving theirs.

An economic theory of credit union moves from the basic theory of a firm of profit maximization

to a complex because the output of any cooperative business is used up or consumed by its

members hence one cannot assume that members seek profit maximization irrespective of the

price or quality of service or goods, this theory cannot relate directly to Saccos. Smith and

Woodburg (2008). Also members of a Sacco provide the demand and supply for funds and

loans. The Saccos the intermediates between member-saver and member-borrower. This

heterogeneity maximizes its dividends rate for saver and minimizes loan rate for borrower. This

theory assumes homogenous member objective which is generally accepted in cooperatives.

A dynamic theory of cooperatives was proposed by Gutherie et al (2002) in ‘pure cooperatives’.

Past researches in the US had created a model that was built in the assumptions that Saccos are

static in their operational environment and that they experienced lower risk. Hence a

mathematical a mathematical model of operation that was created has filed to be operational in

the modern day as cooperatives have more flexible structure. Numbers of issues have to be

considered in creating new models that will keep dynamically changing depending on equity

retention, inter-temporal deposits and loan rate if equilibrium state has to be reached.

14

The agency theory is a theory of relationship between principal and agents in a business. The

conflicts or dilemma occurs due to divergent interest. The agents look to maximize their earnings

from the share holder and the principal looks to maximize his profits Kioko (2012). In the Sacco

movement, the elected board of directors can conflict with the members over dividend payout

rate and policies as the management may look to retain more dividends or want to award

themselves with more honorarium and hence reducing members’ earnings.

The theory of cooperative federalism comes from the school of thought that favors consumer

cooperatives. Vanek (2012)all argued that consumers should form co-ops which all members are

consumers for unity with purpose in advocating against punitive actions of wholesalers or

maximizing goods quality and reducing supply chain for lower prices. They sampled

Cooperative wholesalers in UK that undertake purchasing of farms and factories to sell to

members and profit is distributed to members as dividends.

The individualism school of thought favors worker’s cooperatives or unions that advocates for

persons own rights. Britain’s Christian Socialists and in works of Joseph Reeves ‘putting this

forth as path to state socialism’ they proposed that in joining workers union the labourer

becomes more powerful and can bargain for better pay for services and even better working

conditions Lewis (2009).

The Michael Porters Five Force Theory states bargaining power of consumers as one of the

major determinants of competitiveness and hence in individualism school, Balkanizing people to

increase their bargaining power is key to holding membership of Saccos through convergence of

interest Porter et al (2008).

In a high transparent financial environment, Demirguc and Levine (2007), financial institutions

that engages in excessive risk taking by demanding higher deposit interests rates or moving

balances to a safer institutions shifts responsibility for assuring transparency and controlling risk

taking to regulatory system, of course, even if country’s net covered all SACCO balances,

depositors would remain at risk for the opportunity costs of claiming and restructuring the

amounts they are due and for costs occasioned by delays in recovering deposits fund

disbursements.

15

Co-operative values and principles

The bases of co-operatives are the co-operative values and co-operative principles, at the 1995

Manchester Congress of the International Co-operative Alliance, the Congress adopted an

Identity Statement on Co-operatives, which authoritatively elucidates the co-operative values and

co-operative principles. There are seven co-operative principles:

The principle of voluntary and open membership, that membership of a co-operative society

must be voluntary and available, without artificial restrictions or any social, religious or political

discrimination, to all persons who wish to benefit from co-operative (ICA, 2013)

The principle of democratic control that control of the organization is based on one member one

vote irrespective of the number of shares held by a member. This is in recognition of the fact

that people working together to achieve a common objective should have equal say in the joint

enterprise (Mugabwa, 2012).

The principle of member economic participation that imposes a limit on return paid on share

capital. Its basis is that co-operatives acknowledge capital as an important factor of production

that should be rewarded (Kioko, 2012).

The fourth principle is autonomy and independence this means that co-operative societies should

enjoy a certain degree of autonomy and a right to run their business to the best of their capacity

and also legal separation of personality of the cooperative (Mugabwa, 2012).

Finally principle of social responsibility on the part of co-operatives and their members, This

entails, working towards improvement of the community in the area they operate, showing

concern and social responsibility (ICA, 2013).

16

2.2 Empirical Review

2.2 Statutory deposit fund requirement on savings

Gordon and McClatchey (1999) researched on the behavioral change after introduction of

reserve deposit by credit unions. They observed that the introduction of insurance deposit did not

increase risk taking behavior by the credit unions as it was expected by their objectives; “A time

series tests employing industry average financial ratios for federal and state credit unions did not

support the increased risk-taking hypothesis.” This implies that the credit unions did not switch

to a frenzy of loans issuing or saving increasing procedures although they were already insured

and would be compensated in case of insolvency.

Individual countries adopt statutory deposit fund for different reasons, like in developing

countries, a common goal is to expand the reach of financial management system and to increase

the flow of credit by minimizing depositor’s doubts about the financial institutions ability to

redeem depositor’s claims when funds are needed Fischer and Cuevas (2006). Hence the scheme

bolsters depositor’s faith in the stability of the SACCOs financial sector.

The quality of a nation contracting environment limits the contribution that variations in

regulatory structures can improve both sustainable economic and microeconomic growth. Recent

adaptors of statutory deposit fund include Africa and Latin America countries with low levels of

financial development and government accountability. Using time series data for fifty eight

credit unions, Cull et al (2005), found that explicit statutory deposits favorably impact the levels

and volatility of financial activity only in the presence of a strong Institutional development.

Statutory Deposit Fund can be explicit or merely implicit. Explicit deposits are contractual

obligations while implicit deposits coverage is only conjectural. Implicit deposits funds exists to

the extent of political incentives that influence a government reaction to a large or widespread

financial institutions problems that makes the public bailouts of insolvent institutions seems

inevitable, Folkerts & Lindren(1998) stated that during financial crisis, the pressure on

government officials to rescue some financial institution stakeholders becomes difficult to resist.

17

The SACCOs have hence diversified and others have reduced their trading grounds or downsized

their investment portfolios. In research paper by Gordon and McClatchey (1999) titled “Deposit

Insurance and risk taking behavior in the credit Union Industry”, they set to find out the

behavioral change after introduction of reserve deposit by credit unions. They observed that the

introduction of reserve deposit did not increase risk taking behavior of credit unions as was

expected.

Grossman and Olive (2002) analyzed the usefulness of one share one vote systems on the control

of co-operatives for maximum utilization. They found that the system provided an important

front for selection of efficient management team since everyone had an equal chance to air his or

her views hence decisions made are for the best company. “We assumed two types of control

benefits — benefits to security holders and private benefits to the controlling party. One share-

one vote maximized the benefits to security holder relative to benefits of the controlling party

hence encouraged the efficient management team.” This document gave a thumb up for the

cooperative systems of running organizations as it produced better results and ensured that the

shareholder’s agents act in the best interest of share holders.

Crisis management entails a number of difficult policy trades off between recovery speed,

economic efficiency and distribution fairness, Honohan and Klingebiel (2003). Due to

deficiencies in prior disaster planning, it has become a common practice to issue blanket

guarantees to arrest financial institutions management crisis including SACCOs.Advocate of

using blanket guarantees to halt a systematic financial crisis argue that sweeping guarantees

creates an expectation of their future financial safety and can immediately be helpful in stopping

spread flight to quality. However, because blanket guarantees create these future expectations,

they undermine business discipline and may prove greatly destabilizing in the long run. Honohan

and Klingebiel (2003) analyzed the impact of blanket guarantees and other crisis management

strategies on the full fiscal costs of resolving financial system distress. Their analysis of forty

credit union that experienced financial crisis between1980 to 1997 indicated that unlimited

deposit guarantees with open ended liquidity support and capital forbearance significantly

increased the ultimate fiscal cost of revolving financial crisis

18

Government guarantees never completely extinguish market discipline and still stability can still

be undermined if SACCOs deposit insurance managers do not exert more discipline that is

required. Using SACCO level data covering forty three SACCOs for a period of between1990-

1997, Demirgus and Huizinga (2004) studied deposit discipline by modeling deposit interest

rates. They found out that explicit Insurance does lower Sacco’s financial risk and does make

interest payment less sensitive to individuals Sacco risk and liquidity.

2.3 Management qualification and quality

Both Boards of directors and senior management are accountable for the internal governance of

the SACCOs Drake (2002). The general assembly is the supreme authority and the highest

decision making in the SACCOs. While it has a duty to the general assembly, Senior

management must be accountable for the implementation of policies, preparation of the budgets,

strategic plans and achievement of predetermined targets specified in the strategic plans.

In an article written by Andrew (2008) said that due to the effect of poor management of these

institutions. The purpose of this paper was to assess the impact of the new regulatory framework

and the continued poor perception of credit unions amongst users of financial service products.

Also an assessment was made of what future may hold for the direction of the UK credit union

sector. The study found out that the membership of the credit unions was growing, as well as

member’s deposits and loans, but the numbers of credit unions were falling. The result ultimately

lead to a strong, secure and professionally managed credit union sector, capable of meeting the

credit needs of a wide range of persons.

A key underlying factor behind merger activities is the beneficial side effect of economy of scale

for which Mckillop et al (2002) noted was a considerable scope which in turn allowed credit

unions to diversify into a range of product and services. The management of these ranges of

highly sophisticated portfolio of investments needed highly qualified managers to run efficiently.

Increasing members of credit unions, particularly to those that have merged to form larger

entities, employed professional personnel in key roles such as Managers as regulatory

requirement became a reality. There is a downside to merger, consolidation drive in that it is

19

arguable that such a move will ultimately threaten the viability of smaller SACCOs, forcing them

into merger and possibly affecting new start up rates of borrowing of their credit facilities.

The credit union ethos has always been as self help financial cooperatives and the push to

merger, led to larger financial organizations professionally managed which competed effectively

with other financial institutions.

Although policies are not a requirement in the provision of the Act, all SACCOs are required to

have by laws that define at the minimum the field and requirement for membership scope of

activities, duties and responsibilities of the Board members, committees and operational staff. In

the absence operational policies, some activities like setting interest rates on loans and saving

products have been institutionalized in the bylaws, Ademba (2011). Because of these, SACCOs

are forced to refer to the AGM for operational decisions that can be easily made by senior

management and hence SACCOs have kept their interest rates below market rates despite higher

borrowing costs, stiff competition, fluctuating inflation rates and changing cost structures

SACCOs are required to comply with the standards set by the regulatory body. In Kenya, the

ministry of cooperative development and marketing oversees Sacco’s activities but this will

move to Sacco regulatory Authority (SASRA) established by law. Currently, SACCOs are

monitored poorly as there is no annual or frequent examination of SACCOs by the regulatory

body. Moreover, there is no comprehensive set of standards by which SACCOs should comply,

(Woccu, 2008). It is hence hoped that the new SACCO regulation will establish prudent

standards that will govern the SACCO sector. These standards will establish benchmarks and

also enforce safety and sound principle to safeguard SACCOs from losses. As financial

institutions, SACCOs should be accountable to their members and to the public by enhancing

excellence through professionalism, (Ademba, 2011).

Wanyoike, (2013) studied Effect of compliance to Sasra Regulation on financial performance of

Saccos and found out that qualifications should be upgraded for managers to have more

qualifications. Since this qualification was needed for more performance. The board of directors

were also to be trained or elected on professional grounds.

Maintaining competitiveness with much larger rivals demanded that credit unions focus on both

efficiency and member/customers satisfaction. While mergers can potentially increase efficiency,

they can also reduce member’s satisfaction through rationalization of staff and/ or branches and

20

from the problems in the integration of systems, procedures and technologies, (Ralston et al

,2001). Overall, it is submitted that with supervision and regulations passed to FSA, the outlook

for credit unions in the UK was better than at any in history. The results of the new regime

ultimately led to a strong, secure and professionally run credit union sector, capable of meeting

the credit needs of a wide range of persons.

However, it must be noted this did not happen overnight as the move away from wholly

volunteer run organizations was not universally popular. The enforced professionalism put a lot

of administrative load that led a reduction in number of credit unions, further increasing pressure

on consolidation. This however, in the long run, led to a move from long held ethos self help

community credit union, to much larger financial service providers, as evidenced by the

movement in the USA, ACCOSCA (2008).Credit unions can help social and financial exclusion,

however, state bodies must also recognize that they will only be able to help if they prove

successful at attracting more members, highly qualified staff. The legislation and regulation must

reflect the need to allow credit unions to attract all members of the society, by allowing them to

provide competitive, effective, efficient and reliable services preferred by customers.

The governance structure of SACCOs assumes its legitimacy via the votes of its members who

surrender their wealth or administration to board of management, (Muchemi, 2005). The board

can therefore make or break the wealth acquisition aspirations of the SACCO membership. One

way through which SACCOs can improve management financial decisions is through provision

of financial education to its members. Broadly defined, financial education encompasses all

aspects of our lives and it revolves around the ability and courage to enable us acquires logical

wealth acquisition and management skills. If correctly applied, the knowledge can positively

impact on the running of these SACCOs. It is therefore important to understand the life cycle of

wealth creation and management and its relevance to various stages of Sacco’s growth prospects.

2.4 Membership regulation requirements

Amongst the papers presented by Gordon (2002) on cooperatives and wealth accumulation in his

preliminary analysis shows cooperatives are the means of quick and sure wealth creation. The

concept where by people saves in small amounts to source for an enormous capital to invest

hence high returns. Successful cooperatives create wealth and help their members as they join

with common goal to a better financial or social welfare. In his study, Gordon found out that in

15 mutual benefit sector cooperatives in California shows that these cooperatives provided

21

higher wages to their employees than the natural minimum wage. The cooperatives help in

wealth creation especially for those who do not have much capital to start up business.

This study concluded that the cooperatives movement curbs poverty amongst the poor as savings

helps in drawing a large pool of capital available for investing and issuing loans to members.

Emma and Sam (2009) researched on the topic “Africa Cooperatives and the financial crisis

concluded that the volatility occurring in global financial markets noted from mid 2007 onwards

brought with it serious long-term consequences for the proper functioning of economy. These

effects include escalating foreclosures, downsizing of enterprises, and increase in unemployment

and volatility in commodity markets. SACCOs were hence directly affected by the crisis since

they fight for house hold money markets. As a financial institution, the SACCOs compete with

banks, mortgage companies and many other financial service providers.

Kioko (2012) in the studied impact of regulation on performance and he found out that there is

need for homogeneous Sacco members to be in line with the trust basis which Saccos relied, his

findings were that since Saccos give loans that are guaranteed by members, then there is need for

members to have a bond before they can belong to the same union.

The Act requires that all members of a Sacco be homogeneous. This implies that Saccos should

be composed of members with the same background and also composed of Kenyans only. A

complementary body of research explored the risk shifting incentive that one can infer from the

behavior of estimate of safety net subsidies imbedded in individual SACCO stock prices,

(Havakimian and Laevan, 2003). These studies show that countries with poor private and public

contracting environments are less apt to design their statutory deposit fund scheme systems well.

This implies countries with weak contracting environments are apt suffer adverse consequences

from installing effective membership in deposit fund schemes.

Financial intermediation among non-members may cause a pyramid effect and hence failure of

the corporation. Huppi and Fedder (2010) concluded that the co-operatives served members only

and took deposits to ensure loaned members don’t default. “Successful group lending scheme

work well with groups that are homogeneous and jointly liable for defaults. The practice of

denying credit to group members in case of default by one of them is the most effective and least

costly way of enforcing joint liability. Another way to encourage members to repay was viewed

22

requiring mandatory deposit that is reimbursed only when all borrowers have repaid their loans.”

Saccos are hence known to be a source of wellbeing to the rural members as they have a limited

access to financial services from banks or other financial institutions hence checks should be put

to ensure its continuity.

2.5 Conceptual Framework

The conceptual framework interlinks the dependent and independent variables.

The independent variables demonstrates activities that remain unchanged in the study and would

include the statutory deposit requirement as a regulation to Saccos that each Sacco submit to the

government 10% of the total deposit by members with a minimum of Ksh 10 Million to act as

insurance deposit: management qualification and quality requirement that Sacco board of

directors must have an understanding of business operations and that the C.E.O’s minimum

qualification be a masters degree and good conduct. Finally the membership requirement

regulation that dictates that all the members that join a Sacco must be people with the same

interest and Sacco can only carry out business with its members.

The dependent variable changes when subjected to independent variables in this case the

performance of Saccos financially subjected to the independent variables above.

Table 2.1 Conceptual Framework

Independent Variable Dependent Variable

Source: Author (2014)

Statutory deposit fund

requirement

Management quality and

qualification Requirement

Membership regulation

requirement

Performance of small Saccos

Profitability

23

2.6 Summary and Knowledge Gap

In brief the research will focus on wealth creation by Saccos, you mobilize savings and invest

together, you have a larger returns (Kioko 2012) reviewed on risk behavior of credit union when

a capital is insured (Gordon and McClathey 1999) realized that the credit union became more

cautious instead of increasing lending margins. (Huppi and Feder 2010) also analyzed the role of

Saccos in rural lending and concluded that they are core source of finance for the unbanked rural

majority. (Wanyoike 2013) researched on effect of Sasra regulation on performance deposit

taking saccos. Baker (2008) studied on behavior and mortality of credit unions and concluded

that the young and small Saccos were growing at a quick rate while the large Saccos were dying

off due to pyramid effect. Lastly (Kushik and Lopez 2006) who studied deregulation of credit

union in US concluded that deregulation caused Saccos to be more aggressive and hence

conformed to the changes in environmental factors.

24

CHAPTER THREE

RESEARCH METHODOLOGY

3.1 Introduction

This chapter covered research design, the population of the study, sample frame, sampling

procedure and data analysis techniques.

3.2 Research Design

The research problem was studied through survey research design. The research design analyses

data and explores the possibility of obtaining as many relationships as possible between different

variables without knowing end applications (Panneerselvam and Senthilkumar, (2009). This

research design was relevant to this study because it gives insight into the process of obtaining

responses from or about all of the members of the population in order to establish as many

relationships as possible between the variable of the study as a basis for general findings

(Kothari, 2012). The study was therefore able to generalize the findings to a larger population.

Survey research clarifies problems, gathers data and creates initial hypothesis and theories about

subjects.

3.3 Target Population of Study

According to Ngechu (2004), a population is a well-defined set of people, services, elements,

events, group of things or households being investigated. This investigation ensures that

population of interest is homogenous. The population of this project comprised of all 11 small

licensed deposit taking Saccos Staff in Nairobi County.

3.4 Sampling

According to Mugenda (2003), a sample is a smaller group obtained from the accessible

population. The target population for this study will be staff of small Saccos in Nairobi County.

Kotler (2001) argues that if well chosen, samples of about 10% of the population can often give

good reliability. We will however apply the formula below.

25

Table 3.1 Sacco Details

SMALL DEPOSIT TAKING SACCOS IN NAIROBI 2014

NO NAME

MEMBERSHIP

STAFF ASSETS

1 NASSEFU 3,327 9 980,966,412

2 WANAANGA 2,477

12 911,362,906

3 NATION STAFF 1,853

6 739,225,893

4 MWITO 5,244 8 726,611,777

5 COMOCO 2,878 4 526,354,722

6 FUNDILIMA 1,712

10 514,418,862

7 KENVERSITY 2,409

7 454,657,971

8 AIRPORTS 1,432 5 352,286,343

9 KINGDOM 5,856

19 293,820,393

10 NAFAKA 1,151

6 281,793,770

11 ORTHODOX 2,730 7 62,840,379

TOTALS 31,069 93

Source: Author (2014)

n = N/ 1+N(e)2

Hence sample size will be n=93/1+93(e) 2

= 75.46

The study will use 75 as the sample size in the study.

26

3.5 Data Collection Methods

The main data collection method chosen for this project was a questionnaire. According to

Pannererselvam and Senthilkumar, (2005), a questionnaire consists of a set of well formulated

questions to probe and obtain responses from respondents. The questionnaire for this project was

designed to gather information relevant to the research questions and to be administered to the

population under study. The study used secondary data of Sacco on performance available from

Sasra.

3.6 Reliability and Validity of Data Collection Instrument

According to Shanghverzy (2003), reliability refers to the consistency of measurement and was

assessed using the test-retest reliability method. Reliability is increased by including many

similar items on a measure, by testing a diverse sample of individuals and by using uniform

procedures. According to Sekaran (2003), validity is the degree by which the sample test item

represents the content the test is designed to measure. Content validity which was employed by

this study measured the degree to which data collected using particular instrument represents a

specific domain or content of a particular concept.

3.7 Data Analysis Techniques

The data analysis techniques for the study involved editing of raw data to detect errors and

omissions, coding of responses, classification of data with common characteristics and

tabulation. Tabulation was the process of summarizing raw data and displaying the same in

compact form for further analysis (Saunders, 2009). The summarized data was analyzed using

descriptive and inferential statistics. Descriptive statistics include mean, median, standard

deviation and frequency distribution while inferential statistics will involve use of regression

analysis and correlations Z-score and Chi-square test for goodness of fit of an observed

distribution was also used. In addition, computer application of SPSS software was used to

analyze data.

27

3.8 Ethical Considerations

Throughout the study, the researcher maintained confidentiality in the information and data

collected. A full disclosure on the purpose and usage of data was given on the use of institutional

data.

28

CHAPTER FOUR

ANALYSIS, PRESENTATION AND DISCUSSION

Introduction

In this section, findings of the study were presented, analyzed and discussed in line with other

researchers work.

4.0.1 Baseline Characteristic of Data

Table 4.0.1 Baseline Characteristic of Data

Variables Classification Frequency Percent Valid

Percent

Cumulative

Percent

Position Held Manager 4 11.1 11.1 11.1

Staff 32 88.9 38.9 88.9

Total 36 100 100 100

Duration of

association

with the Sacco

Below 1 year 10 27.8 27.8 27.8

1-5 years 15 41.7 41.7 69.4

5-10 years 8 22.2 22.2 91.7

>10 years 3 8.3 8.3 100

Total 36 100 100

Source: Research data 2014

The modal number of the period that the respondents have worked in Sacco sector was below

one year with a mean of 2.11 and the middle age being 6 years of work experience. The ordinary

staff accounted for 89% of the total responses with 11% being managers.

29

Table 4.0.2 Tests of normality

Position

Held in

Sacco

Number of

Years in

Sacco

Movement

Do you think Sasra

regulation will

affect Sacco

performance

N Valid 36 36 36

Missing 0 0 0

Mean 2.3889 2.1111 1.7500

Skewness -.691 .472 .533

Std. Error of Skewness .393 .393 .393

Kurtosis -.590 -.496 -1.606

Std. Error of Kurtosis .768 .768 .768

Source: Research data 2014

4.0.2 Test of Data Reliability: Cronbach alpha

Table 4.0.2 Test of Data Reliability: Cronbach alpha

N %

Cases

Valid 9 25.0

Excluded 27 75.0

Total 36 100.0

a. Listwise deletion based on all

variables in the procedure.

30

Reliability Statistics

Cronbach's Alpha N of Items

.618 40

Source: Research data 2014

Preliminary data was gathered by administering a pilot questionnaire to 10 respondents. The

questionnaire was then re-administered to them after 2 weeks to test for reproducibility.

Cronbach’s alpha was used to test the reliability, the values for the components evaluated under

the disparate variables ranged from 0.82 to 0.89 with an overall Cronbach’s alpha of 0.8 showing

good reliability.

4.0.4 Support for direct regulation by government in SACCOS

Table 4.0.3 Support for direct regulation by government

0

10

20

30

40

50

60

70

80

Yes No Not Sure

3-D Column 1

Source: Research data 2014

Table 4.0.3 above shows that of those interviewed, 75% support the introduction of Sacco

regulation 17% do not support it and 8% are not sure. This shows that the regulation has high

support in the Sacco fraternity and that hence the regulation proves to be good for Sacco

management.

31

4.1 Effect of statutory deposit fund requirement on performance of small Saccos in Kenya

Table 4.1.1 statutory deposit requirement affect on small Sacco performance

0

10

20

30

40

50

60

Yes No Not Sure

3-D Column 1

Source: Research data 2014

Of those who responded 55% of them agreed that the regulation affects Sacco performance while

13.95 Disagreed. 30.6% were however unsure.

Table 4.1.2 Effects of Statutory deposit factors

Strongly

Agree

Agree Neutral Disagree Strongly

Disagree

Totals

Effect of Statutory

deposit requirement on

Sacco liquidity

44.40% 33.30% 19.40% 2.80% 0.00% 100.00%

Statutory Deposit

regulation increase the

amount of deposit

23.50% 36.50% 7.60% 23.50% 8.80% 100.00%

Statutory deposit fee is

not affordable to small

Saccos

29.40% 20.60% 14.70% 20.60% 14.70% 100.00%

Source: Research data 2014

32

Chi-Square Tests

Value df Asymp. Sig.

(2-sided)

Pearson Chi-Square 6.431a 6 .377

Likelihood Ratio 7.067 6 .315

Linear-by-Linear

Association .006 1 .936

N of Valid Cases 36

a. 9 cells (75.0%) have expected count less than 5. The

minimum expected count is .11.

Table 4.1.2 above shows that 77% of those interviewed agree that the statutory deposit

requirement affects liquidity while 20% were neutral the remaining percentage said that it had no

effect.

Table 4.1.2 above shows that of the interviewed 23% of them strongly agree that the regulation

increased members deposit and 36% others also agree while23% of them also disagree that and

8% strongly disagree. However 7% were neutral.

Half of those interviewed agree that the statutory deposit is not affordable to small Saccos 20%

of them disagree while 14% strongly disagree and 14% were neutral.

The findings above are in agreement with (Fischer & Cueveas, 2006) who found out that

insurance funds introduction does affect growth in credit unions and that it bolsters depositor’s

faith in stability of Saccos. Our findings that deposits in the Saccos increased after introduction

of statutory deposit requirement (with 56% being in agreement) is in line with this study that was

done in Europe.

33

Table 4.1.3 Chi-Square Tests Effect of Statutory regulation on the amount of deposit

Value df Asymp. Sig.

(2-sided)

Pearson Chi-Square 15.712a 8 .047

Likelihood Ratio 17.839 8 .022

Linear-by-Linear

Association 5.340 1 .021

N of Valid Cases 34

a. 15 cells (100.0%) have expected count less than 5. The

minimum expected count is .35.

Half of the managers interviewed agree that the statutory deposit is not affordable to small

Saccos as shown above; the significance level was about 4.7% showing that there is not much

difference between expected and observed findings

34

4.1.4 Spearman rank correlation on the relationship between statutory deposit factors

Liquidity Deposit Cost

Increase

Affordability Profit

Statutory

deposit

requirement

effect on

liquidity

C.

Coefficient

1 .540**

.372* .511

** 0.229

Sig. (1-

tailed)

. 0 0.015 0.001 0.097

N 36 34 34 34 34

The

regulation

has lead to

increase in

the amount

of deposits

C.

Coefficient

.372* 1 0.162 .341

* 0.263

Sig. (1-

tailed)

0.015 0.18 . 0.024 0.067

N 34 34 34 34 34

Statutory

deposit has

increase

cost of

operations

C.

Coefficient

.511**

.407**

1 .341* .438

**

Sig. (1-

tailed)

0.001 0.008 0.024 . 0.005

N 34 34 34 34 34

Statutory

deposit fee

amount is

not

affordable

to small

Saccos

C.

Coefficient

0.229 .410**

0.263 1 .438**

Sig. (1-

tailed)

0.097 0.008 0.067 0.005 .

N 34 34 34 34 34

Profitability

of the

Sacco

C.

Coefficient

-0.151 -0.206 0.073 -.433**

1

Sig. (1-

tailed)

0.2 0.129 0.345 0.007 0.038

N 33 32 32 32 32

Source: Research data 2014

35

Table above, there exist high correlation among the various statutory deposit and their effects on

Sacco performance. This correlation among various factors demonstrates that statutory deposit

was significant correlated to factors evaluated. Strong correlation of 97% confidence level were

noted.

Statutory deposit fund requirement is a sum deposited for security to a regulator. In this study,

the introduction of this regulation has had an effect on Sacco performance. The increase in

deposits increased liquidity and hence an increase in loaning activity. This is contrary to (Gordon

&McClatchy, 1999) research on behavior change after introduction of reserve deposit on credit

unions. Their findings were that the unions did not increase risk taking behavior as they had

hypothesized. This implies that credit unions did not switch to a frenzy of issuing loans even

though the savings were insured and would be compensated in any eventuality.

The effect caused by transfer of money to the government has increased confidence in Saccos

and hence improved liquidity. This is in agreement with (Folkerts &Lindsen, 1998) who found

out that in case of financial problems of financial institutions with public insurance (fund) pushes

government to bailout and hence security is high and difficult for government to resist helping

out as stakeholders are of public in nature.

4.2.1 Effect of management qualification on the performance of small Saccos in Kenya

Table 4.2.1 management quality and qualification requirement

0

10

20

30

40

50

60

70

Yes No Not Sure

3-D Column 1

70% of those interviewed did support the introduction of management quality requirement 18%

were however against the regulation and 12% were not sure. A chi-square test is presented.

The management qualification and quality requirement was supported by most of those

interviewed. It was their opinion that such management would improve performance. This is in

36

agreement with (Andrew, 2008) who found out that ultimately the credit unions became strong,

secure and professionally managed. A policy framework on new management was introduced In

Europe which led to growth in the sector and emergence of strong credit unions capable of

meeting credit of a wide range of persons.

Table 4.2.2 Management quality and qualification requirement factors

Strongly

Agree

Agree Neutral Disagree Strongly

Disagree

Totals

Managers give quality

service to Saccos

31.40% 37.10% 17.10% 5.70% 8.60% 100.00%

Managers qualification

is important for Saccos

performance

52.90% 11.80% 0.00% 5.90% 29.40% 100.00%

Management quality

and requirement is of

more benefit compared

to cost

11.80% 29.40% 11.80% 29.40% 17.60% 100.00%

Qualified managers are

expensive for small

Saccos

32.40% 17.60% 17.60% 14.70% 17.60% 100.00%

Table 4.2.2 above shows that 68% of those interviewed agree that qualified managers give

quality service to Saccos. 17% were however neutral with 15% being in disagreement.

Management qualification has also been rated highly on performance with 63% of those

interviewed agreeing and no one was neutral. 29% however disagree and further 17% strongly

feel that qualification does not necessarily cause improved performance.

Of the respondents interviewed 40% agree that management quality is of more benefit compared