Embed Size (px)

Citation preview

The Economic Impacts of Eminent Domain

Daniel L. Chen and Susan Yeh⇤

January 2012

Abstract

We model government takings of private property, embedding prominent theories

of their economic consequences. Random assignment of U.S. judges and the fact that

judges make takings precedent in a manner correlated with their race, political party,

and prior government advocacy facilitate causal estimates of allowing government

takings. Novel data on judicial biographies and takings decisions since 1975 indicate

that decisions favoring physical takings increase growth by 0.2% points but reduce

minority home ownership and employment by 0.5% and 0.3% points respectively,

while those favoring regulatory takings initially depress property prices but spur

economic growth in the medium-run by 0.7% points.

Keywords: Eminent Domain, Property Rights, Takings, Regulation, Growth, Inequality

JEL codes: R32, K11, R42, R52

⇤Daniel L. Chen, Assistant Professor of Law, Economics and Public Policy, Duke Law School,[email protected]; Susan Yeh, Sharswood Fellow in Law and Economics and Lecturer, Universityof Pennsylvania Law School, [email protected]. We thank Andres Sawicki for sharing data. Workon this project was conducted while Daniel Chen received financial support from the Ewing MarionKauffman Foundation. We acknowledge joint financial support from the John M. Olin Center for Law,Economics, and Business at Harvard Law School.

1

1 Introduction

The ability for governments to take land from individuals is hotly debated around the

world. In India and China, fatal riots have followed government acquisitions of private land

on behalf of commercial developers, while in the former Soviet bloc, legislation allowing

governments to take land for the establishment of privately-owned industrial parks is

pending.1 Referred to as eminent domain, compulsory purchase, compulsory acquisition,

or expropriation by different legal systems,2 a common question arises: is state taking

of private property justified? Proponents in the United States argue that government

exercise of eminent domain spurs economic growth through public goods provision, blight

removal, and commercial development (Kelo v. City of New London, 545 U.S. 469 (2005)).

Skeptics, however, believe that public choice incentives lead revenue-seeking governments

to collude with private developers (Byrne 2005) at the expense of disadvantaged groups

(see Justices O’Connor’s and Thomas’s dissents in Kelo) and believe that governments

compensate landowners too little for land acquisition (Chang 2010; Munch 1976). In the

U.S., contention surrounding government takings has risen to a new level: if governments

simply regulate and restricts certain property rights, such as the ability to use the land

productively, the regulation would be considered a taking.3 Liberty issues aside, little is

empirically known about the consequences of government takings, despite a plethora of

economic and legal theories regarding their potential consequences (Epstein (1985, 2008);

Kaplow 1986; Blume, Rubinfeld and Shapiro 1984).4

1See http://www.nytimes.com/2011/02/05/nyregion/05metjournal.html,

http://www.nytimes.com/2011/02/23/world/asia/23india.html, http://www.cga.ct.gov/2005/rpt/2005-r-0321.htm, and http://www.nytimes.com/2011/12/26/world/asia/in-china-the-wukan-revolt-could-be-a-harbinger.html?hp. In China alone, the government has taken land from an estimated 40million households, many of whom have been under-compensated and as a result remain landless andunemployed (Cao et al. 2008).

2Eminent domain (United States), compulsory purchase (United Kingdom, New Zealand, Ireland), re-sumption/compulsory acquisition (Australia), expropriation (South Africa and Canada).

3Pennsylvania Coal Co. v. Mahon (1922) established the doctrine of regulatory takings (see AppendixA). Examples of regulatory takings include zoning restrictions for the location of hotels (Dexter 345 Inc.

v. Cuomo, 2011 WL 6015780) and regulations shortening the fishing year (Vandevere v. Lloyd, 644 F.3d957).

4A growing literature in economic development links secure property rights (but not eminent domain) tohousing renovations (Field 2005), agricultural investments (Besley 1995), and agricultural productivity(Banerjee, Gertler and Ghatak 2002; Hornbeck 2010). An extensive theoretical literature in macroeco-nomics links economic growth to the ability by governments to expropriate capital (but not land) expost (Aguiar and Amador 2011).

2

Empirical studies to date have primarily focused on descriptive statistics. Data

limitations have made it practically impossible to study the causal effects of eminent

domain. Few centralized sources of data document the condemnation of property across

jurisdictions exist since various levels of government, local, state, and federal, are able to

invoke the power of eminent domain. We sidestep this issue by focusing on court-made

laws that make it harder or easier for subsequent government actors to take. We study

the U.S. because its common law system, random assignment of judges, and system of

appellate courts with regional jurisdiction setting legal precedent for millions of people,

allows us to isolate causal effects.

In particular, we derive a natural experiment from the random assignment of U.S.

appellate judges to three-judge panels exercising judicial discretion in interpreting the

facts and the law differently and in a manner correlated with their demographic char-

acteristics. Between 1979 and 2004, 220 federal appellate cases addressed regulatory

takings, and between 1975 and 2008, 134 appellate cases addressed physical takings. Our

empirical strategy exploits the fact that appellate decisions are binding precedent only

for future cases within the same circuit. Because judicial composition of eminent domain

panels is unlikely to be correlated with subsequent economic outcomes other than through

eminent domain decisions, the random assignment of judges creates exogenous variation

in appellate precedent making it harder or easier to exercise eminent domain. This ex-

ogenous variation can be used to estimate the causal impact of allowing eminent domain

on economic outcomes, since takings law can otherwise be endogenous to economic out-

comes. Among other channels, endogeneity arises because the Fifth Amendment of the

U.S. Constitution allows governments to take land only for “public use” and if there is

“just compensation.” For example, if property prices are expected to increase, then courts

may be less likely to rule that a condemnation or regulation meets the criteria for public

use such as blight removal or that the compensation is just. Thus appellate decisions fa-

voring private property rights would be endogenous to anticipated price trends, leading to

a spurious estimate were we to only examine the correlation between appellate decisions

and future property prices.

The sign of any effect of eminent domain on subsequent economic outcomes is

theoretically ambiguous. Section 2 embeds prominent theories of eminent domain in a

3

general model of both regulatory and physical takings, emphasizing how increased risk

of takings can distort incentives to develop land efficiently (Riddiough 1997) and, when

landowners receive full compensation for takings, overinvestment can occur because full

compensation provides full-coverage insurance to the private investor against the risk of

taking with no premium paid (Blume, Rubinfeld and Shapiro 1984; Miceli and Segerson

1994; Innes 1997; Turnbull 2002). After documenting that our model is consistent with

the predictions of models in the literature, we show how estimating the empirical impact

of eminent domain permits inference as to the predominant underlying mechanism, i.e.,

whether under- or over- investment or public use.

We present an analysis of zip-code level property prices, state GDP, home owner-

ship, and individual labor market outcomes as well as data on eminent domain appellate

decisions collected by ourselves as well as by other authors. Section 3 establishes that the

composition of judicial panels is indeed related to eminent domain appellate decisions.

After verifying that judges are effectively randomly assigned, we show that panels with

judges who are Republican appointees and prior U.S. Attorneys are more likely to uphold a

physical taking on behalf of the government while panels with judges who are Democratic

appointees and minority are more likely to rule against a physical taking. Republican ap-

pointees, who might generally favor commercial development as well as individual liberty

rights, might not have any particular stance on eminent domain on average, but those

who are prior U.S. Attorneys, a highly political and legal position, would have served on

behalf of the government and could view takings cases more favorably for the government.

A large literature, moreover, documents that black and white judges decide differently on

a range of issues (Chew and Kelley (2008); Scherer (2004); Kastellec (2011)), and minority

Democratic appointees are likely to have prior experiences serving people whose proper-

ties are physically taken, who tend to be poor and minority (Carpenter and Ross 2009;

Frieden and Sagalyn 1989). We show, in contrast, that panels with black (or minority)

judges are more likely to vote to uphold a regulatory taking against a plaintiff’s challenge,

as regulatory takings challenges tend to be brought forward by wealthier, non-minority

parties, especially business entities (Stein 1995).

A variety of evidence in Section 3 establishes that the random assignment of judges

differentially impacts appellate decisions creating legal precedent in eminent domain. In

4

Section 4, we consider the subsequent impact on property values, growth, and economic

inequality. Two-stage least squares estimates using this variation suggest that making

it easier to regulate without having to compensate landowners spur economic growth.

Property prices initially decline, but then increase in response to pro-takings regulatory

precedent. Making it easier to acquire private property increases growth in state GDP

and property prices, but decrease minority labor market outcomes. Our baseline estimates

indicate that rulings in favor of the government in regulatory takings cases spurs growth

in property prices by 0.2% points and growth in GDP by 0.7% points and ruling in

favor of the government in physical takings cases spurs growth in property prices by 0.12-

0.23% points and economic growth by 0.2% points. Significantly, however, pro-government

physical takings precedent reduces minority home ownership and employment by 0.5% and

0.3% points respectively. We verify our estimation strategy is robust to using alternative

judicial characteristics by implementing LASSO, a sparse model, to optimally extract

information from different combinations of judges on three-judge panels (Belloni et al.

2011). Our results provide evidence that the law of eminent domain has real economic

consequences.

In our analyses, we explore how closely our empirical design tracks a randomized

control trial by varying our controls and data in a variety of specifications. Previous

studies have not used randomization to address the issue of endogeneity of takings, where

property characteristics themselves, linked to the surrounding economy, can drive govern-

ment decisions that would in turn affect property values.5 The closest study preceding

ours is Guidry and Do (1998), which finds that property transferred under eminent do-

main correspond to higher property prices in a cross-sectional analysis of a small sample

of properties, and Quigley and Rosenthal (2005) conclude that as much as 54% of land

value can be linked to land use regulations.6 Methodologically motivated by Deaton

(2010) and Lee (2008), we show how the empirical framework developed here provides

causal estimates of court precedent holding all else equal including unobserved factors. It

overcomes the basic issues of omitted variables and reverse causality. Furthermore, it has5Cities are less likely to condemn occupied homes for economic redevelopment projects and are morelikely to take underutilized property (Mihaly (2006); Chang (2010)) in urban areas (Byrne 2005) andfrom minority and poor residents (Carpenter and Ross (2009)).

6Other studies have found increases in property values (Jaeger (2006); Katz and Rosen (1987); Beaton(1991)) though some find decreases (Nickerson and Lynch (2001)).

5

the advantages that the exclusion restriction is likely to hold, that the LATE interpreta-

tion of the IV estimates is policy relevant, that the general equilibrium effects are those

that we would want to include, and that the impulse response function is well-identified.

Our method should prove fruitful for policy-makers and judges interested in assessing the

impact of court-made law.

2 Background

This section outlines a theoretical model of government takings to guide our empirical

work. Appendix A develops the model formally. Physical takings and regulations are

decisions of the local, state, or federal government. Let ⇡p be the exogenous probability

that the court allows a physical taking to occur and the government must provide com-

pensation C > 0 and ⇡r be the probability that the court allows a regulation with zero

compensation C = 0.

Through stare decisis, the legal doctrine by which judges must respect the prece-

dents established by prior decisions, appellate court precedent increases or decreases these

probabilities, ceteris paribus, i.e., with the same fact patterns as found in previous takings

cases. Appendix B describes key elements of the U.S. legal context necessary for model

estimation and highlights major doctrinal developments. A pro-government decision in a

physical takings case lowers the threshold for what constitutes public use, so increases ⇡p.

A pro-government decision in a regulatory takings case raises the likelihood of subsequent

regulatory activity so increases ⇡r. With probability 1�⇡p�⇡r, the court rules in favor of

the plaintiff, and the government action is overturned. Compensation C depends only on

government policy and the property’s current condition. The landowner invests I in his

property to maximize expected returns, taking into account ⇡p and ⇡r, the government’s

probability of initiating a taking ⇡, compensation C, the government’s compensation

policy G (e.g., just or partial), and uncompensated losses L due to regulation:

max

IER = max

I{(1� ⇡)(V (I)� I) + ⇡[(1� ⇡p)V (I) + ⇡pC(G, I)� ⇡rL� I]} (1)

6

Our model shows that compensation is key to efficient investment in a world with takings.

The law requires the government to compensate the landowner in a taking, accounting

for a number of factors including the book value (appraisal price of the property). Under-

investment can arise if the government does not compensate property owners sufficiently.

Over-investment, however, can arise with just compensation because it removes the risk

that an investment could lose all value to the landowner when property is taken by the

government instead of sold at market value. Property owners are over-insured, or to put

it another way, do not pay the insurance premium on the insurance they receive in the

event of a taking (Blume, Rubinfeld and Shapiro (1984); Kaplow (1986)). Over-investment

results because the marginal increase in value to society is less than the marginal increase

in value to the individual. Our derivation in Appendix A provides a theory-based test for

the presence of under- or over-compensation. Translating to our empirical context:

• If there is under-compensation, then a higher probability of taking would lead to

lower investment and therefore lower property values, lower growth, and lower em-

ployment. This might occur particularly for minority landowners in physical takings

since their land is disproportionately condemned and under-compensated.

• If there is over-compensation, then a higher probability of taking would lead to

higher investment and therefore higher property values and higher employment but

lower growth in the medium or long-run (Green (2003)).

• If compensation is optimal, then the probabilities of taking should have no significant

impact on property values, growth, and unemployment.

We summarize:

Investment Level Growth/GDP vs.⇡p, ⇡r, ⇡

Employment vs.⇡p, ⇡r, ⇡

Property Valuevs. ⇡p, ⇡r, ⇡

Below first-best(Under-investment) - - -

At first-best(Optimalinvestment)

0 0 0

Above first-best(Over-investment) - + +

7

Social benefits from the public use project would be capitalized and directly impact

prices, growth, and employment, each of which we predict to be positively related to Br

and Bp. Making it easier for the government to take private property would stimulate

growth only if the social benefits, which may differ for regulatory and physical takings,

exceed the distortions from increased probability of taking when compensation is not

optimal.

3 Design of Study

3.1 Data

Our empirical analysis draws on several sources of data on eminent domain cases—established

datasets as well as our own data collection. Sunstein et al. (2006) collect data on all appel-

late regulatory takings published decisions from 1979-2004. We apply a similar method-

ology to collect appellate physical takings decisions from 1975-2008. We also collect all

district court cases involving regulatory and physical takings. Our outcome variables are

property values (house price indices) at the zip code level from the Fiserv Case-Shiller

Weiss data, state gross domestic product (GDP) from the Bureau of Economic Analy-

sis, and housing and employment outcomes from the Current Population Survey (CPS).

These and other data collection efforts are described further in Appendix C.

3.2 Specification

Our basic specification models the changes in eminent domain precedent at the circuit-

year level and its relationship to unit outcomes in those circuits over time:

Yict = �0 + �1Lawct + "ict (1)

The dependent variable, Yict, is a measure of outcomes of unit i in circuit c and time t. Our

main outcomes are change in log property prices at the zip code level measured at quarterly

frequency, change in log local GDP at the state level measured at yearly frequency, and

8

housing and employment status of individual i in circuit c at yearly frequency.7 The

key coefficient of interest is �1 on Lawct, where Lawct is the measure of eminent domain

precedent issued in circuit c and year t (or quarter t for property prices). Lawct is the

proportion of cases with a pro-government (pro-taking) outcome. In robustness checks,

we use the number of cases as weights.8

If eminent domain decisions and economic outcomes are systematically correlated

with omitted variables, then �1 is biased. For example, social trends may drive judi-

cial decisions, so ascertaining a causal effect from judicial decisions to social trends is

difficult. A particular form of endogeneity arises because the Fifth Amendment of the

U.S. Constitution allows governments to take land only for “public use” and if there is

“just compensation.” If property prices are expected to increase, then courts may be less

likely to rule that a condemnation or regulation meets the criteria for public use such as

blight removal or that the compensation is just. Thus appellate decisions favoring private

property rights would be endogenous to anticipated price trends, leading to a spurious

estimate were we to only examine the correlation between appellate decisions and future

property prices. An additional concern with judge-made law is that there is so much

cross-fertilization across different areas of legal doctrine (e.g. between tort and property

law). If different, but related, doctrinal areas have independent effects on economic out-

comes, social changes may be misattributed to one legal rule when many legal rules are

changing simultaneously.

The common approach of controlling for potential confounders can accentuate the

problem of omitted variable bias if the included terms are themselves correlated with

other omitted variables (Clarke (2005)):

Yict = �0 + �1Lawct + �2Cc + �3Tt + �4Cc ⇤ Time + �5Wct + �6Xict + "ict (2)7We also examine hours worked and log real weekly earnings. Earnings are normalized to account forinflation. We use CPS weights when examining labor market outcomes. Logs real weekly earnings aretaken of 1+earnings and earnings are set to 0 if an individual is not employed or not in the labor force.We do this because actual wages, not reservation wages, are of normative interest by legal scholars. Inrobustness checks, we also drop individuals not employed or not in the labor force.

8With less than one eminent domain decision per circuit per year, we did not consider quadratic ornon-monotonic functions of the number of pro-plaintiff decisions.

9

With a research design involving random treatment assignment, however, adding controls

can add precision to the estimates if the controls are strong predictors of the outcomes. We

show that our main estimates are invariant to the inclusion or exclusion of: circuit fixed

effects, Cc, and time fixed effects, Tt, to address whether fixed unobservable differences

within circuits and within time periods are correlated with pro-plaintiff precedent and

economic outcomes; circuit-specific time trends, Cc ⇤ Time, to allow different circuits to

be on different trajectories with respect to outcomes; state fixed effects to address the

possible influence of state-specific takings statutes or state interpretation of federal laws;

a vector of observable unit characteristics, Xict, depending on the unit being observed (for

example, at the individual level: age, gender, educational attainment, and race, which

each enter as dummies with the exception of age); and time-varying circuit-level controls,

Wct, such as the characteristics of the pool of judges available to be assigned.

Since economic outcomes are serially correlated, "ict is not i.i.d. Hence, all spec-

ifications cluster standard errors at the circuit level. Bester, Conley and Hansen (2011

forthcoming) suggest scaling up the cluster t-statistic with relatively few clusters (e.g.,

12 circuits), but the scaling is very close to one with large N. Barrios et al. (2010) in-

dicates that the use of clustered standard errors, along with the random assignment of

treatment, address possible spatial correlation in the errors as well. In robustness checks,

we also execute a wild bootstrap suggested by Cameron, Miller and Gelbach (2008) for

small number of clusters and a Monte Carlo simulation, where we randomly assign the

legal variation to another circuit to test for spurious correlations.

Since Lawct and "ict may be correlated due to uncontrolled-for social trends or other

legal developments that correlate both with Lawct and outcomes Yict, �1 may be biased.

To overcome this, we need an instrumental variable for Lawct that is uncorrelated with

"ict. Figure 3 roughly depicts the intuition for our 2SLS identification strategy, in which

we exploit the random variation that arises from using the random deviation in the actual

number of black judges per seat in eminent domain cases.9 These numbers are depicted in

jagged red lines in Figure 3 for each of the 12 Circuits. The smoother blue lines indicate

the expected number of judges with particular biographic characteristics per seat for each9Without loss of generality, we only write black judges and regulatory takings cases until we discuss thefirst stage analyses.

10

Circuit. Circuit-years receiving an unexpectedly high proportion of black judges on their

regulatory takings panels receive an unexpectedly higher proportion of pro-government

eminent domain decisions. Each spike in the actual number of black judges per seat above

the expected number of black judges per seat corresponds to the circuit-year randomly

receiving a “treatment” of more pro-government regulatory takings precedent. Thus,

changes in outcomes can be attributed to the “treatment” of pro-government eminent

domain precedent and not to other unobserved social trends or legal developments.

Figure 3 suggests the first stage equation:

Lawct = �0 + �1Treatmentct + �2Cc + �3Tt + �4Cc ⇤ Y ear + �5Xict + �6Wct + "ict (3)

where Lawct is defined as the percentage of decisions that are pro-government (pro-taking),

conditional on there being any decision in that circuit and time period. The “Treat-

ment” group (Treatmentct = 1) comprises people who experience an unexpectedly higher

percentage of pro-government decisions due to an unexpectedly higher actual number

of black judges being assigned to the regulatory takings panels. The “Control” group

(Treatmentct = 0) comprises people who experience an unexpectedly lower percentage

of pro-government decisions. Formally, Treatmentct = 1[(Nct/Mct > E(Nct/Mct)], where

Nct is the number of black judges assigned to all regulatory takings cases in that circuit-

quarter divided by 3 and Mct is the number of eminent domain cases in that circuit quarter.

The actual number of black judges per seat is given by Nct/Mct, while E(Nct/Mct) is the

expected number of black judges per seat. The moment condition for causal inference is

E(Treatmentct"ict) = E[1[(Nct/Mct�E(Nct/Mct))]"ict] = 0, which holds since being above

or below the threshold is uncorrelated with social trends or legal developments that might

otherwise be correlated with outcomes through ict. The effect of law on outcomes is the

difference in Outcomeict for Treatmentct = 1 or 0, divided by the difference in Lawct for

Treatmentct = 1 or 0. That is, we could simply look at the Wald estimator for outcomes

in any given year during or after the treatment to estimate the treatment effect.10 An10Note that economic outcomes are unlikely to zigzag in the manner suggested by the Figure 3. Rather,

we look for deviations from an underlying trend. Estimates of the treatment effect would be obtainedfrom differencing the average of these deviations for treated circuit-years with the average of thesedeviations for non-treated circuit-years.

11

illustration of such a calculation is displayed in Appendix Table A17.11

Before moving on to extensions of the basic model, we make two remarks. First,

the exclusion restriction is likely to hold, and we will thus be able to interpret the 2SLS

estimates as the causal impact of eminent domain precedent. Here, the identity of judges

sitting on eminent domain panels is not likely directly to affect economy-wide outcomes

that are of interest except through the appellate precedent alone.12 Second, the LATE

interpretation of the instrumental variables estimate is restricted in terms of external

validity. Here, only cases where there is enough controversy to allow judicial biographical

characteristics to matter are going to be the subject of the study. These cases may very

well be the difficult decisions that set new precedent, and the sorts of cases in which

judges interested in empirical consequences of decisions, like Judge Richard Posner or

Justice Stephen Breyer seek guidance (Posner (1998); Breyer (2004)).

For more statistical power, we employ the entire excess proportion of black judges

per seat as a continuous instrumental variable. That is, we write:

Lawct = �0 + �1Zct + �2Cc + �3Tt + �4Cc ⇤ Time + �5Wct + �6Xict + "ict (4)

where Zct is the difference between the actual number of black judges per seat and the

expected number of black judges per seat. The moment condition for causal inference

is E[(Nct/Mct � E(Nct/Mct))"ict] = 0. In words, the greater the excess proportion of

black judges per case, the more pro-takings is the regulatory takings precedent in that

circuit-year. We attribute the degree to which outcomes change to this excess proportion.

Laws are not likely to have an immediate impact. Firms may need time to adjust

to judicial decisions; alternatively, the effects of a law change may fade as expectations or

statutory regimes adjust. We build on our basic model with a distributed lag specification11The ratio of the differences is comparable to the point estimates displayed in Table 5 Panel A and

Appendix Table A10.12Causation from demographic characteristics to decision-making is not necessary for the methodology.

Rather, only correlation is needed. The exact mechanism for why demographic characteristics affectdecision-making is also irrelevant. For example, decisions could be different because litigants tailortheir oral arguments to the judge. We use demographic characteristics instead of judicial attitudesbecause demographic characteristics provide a multivariate characterization of judges that can be usedacross judges. These characteristics provide additional power relative to attitudinal scores, which areunidimensional, or to individual judge fixed effects, which would be imprecisely estimated if each judgehears only a handful of eminent domain cases.

12

that includes four years (16 quarters) of lags of the law and a one year (4 quarters) lead.

The use of leads helps assess whether trends in property prices precipitate eminent domain

precedent.13 We therefore estimate a distributed lag specification to study the dynamic

effects of law over time:

Outcomeict = �0 + �1y

XLawc(t�y) + �2Cc + �3Tt + �4Cc ⇤ Time (5)

+�5y

XWc(t�y) + �6Xict + "ict

A problem with this dynamic treatment effect specification is that circuit-years

with no cases greatly reduce sample size. If no appellate cases appear in any of the last,

say, 16 quarters, the observation would drop from the estimation. To address this missing

data problem, consider the moment condition for causal inference:

E[(Nct/Mct � E(Nct/Mct))"ict] = 0 (6)

We seek to construct an instrumental variable whose moment conditions will imply the

original moment condition. Consider an instrument, pct �E(pct). The moment condition

for this instrumental variable is:

E[(pct � E(pct))"ict] (7)

where pct is the number of black judges per seat in regulatory takings cases in circuit c

and time t and pct is defined as 0 when there are no cases. Specifically, let:

pct =

8><

>:

Nct/Mct if 1[Mct > 0]= 1

0 if 1[Mct > 0]= 0

(8)

and define Lawct also as 0 when there are no cases. When 1[Mct > 0] = 1, pct = Nct/Mct

returns the original moment condition E[(Nct/Mct�E(Nct/Mct))"ict] = 0. When 1[Mct >

13This test subsumes the standard check for a reduced form relationship between the instrument and theleads. Such a relationship would be included in the second-stage estimates of the lead coefficient sincethe first stage for the lead law includes all the instruments, leads and lags.

13

0] = 0, then pct = 0 and E(pct) = 0, so E[(pct � E(pct))"ict] = 0. However, these two

conditional moment conditions do not imply E[(pct � E(pct))"ict] = 0 unconditionally.

The presence of appellate cases, 1[Mct > 0], may be a function of "ict, so it needs to be

controlled. After controlling for it, then E[(pct � E(pct))"ict] = 0 unconditionally.

In addition, since E[(pct � E(pct))"ict] = E(pct"ict) � E[E(pct)"ict] = E(pct"ict) �

E(pct)E("ict) = E[pct"ict], we can ignore E(pct), the expected number of black judges per

seat. We have now constructed our instrumental variable, pct. This allows a distributed lag

specification since there is no dividing by 0, but one needs to include a binary indicator

1[Mct > 0] representing whether there are cases. This binary indicator ensures that

circuit-years with no black judges assigned to cases are treated differently if there are no

appealed cases in that circuit-year.

The inclusion of 1[Mct > 0], however, threatens the moment condition in a dis-

tributed lag specification. Whether there are any cases in a given year may respond to

previous years’ realization of the instrument. That is, having many black judges being as-

signed to regulatory takings cases in prior years may affect litigants’ willingness to appeal

in the current year. If this is the case, then treatment affects both the left and right-hand

side and leads to downward bias in the estimates of interest with the greatest downward

bias in the most lagged treatment and the least downward bias in the least lagged treat-

ment (such as lead coefficients). This form of downward bias makes the distributed lag

specification difficult to interpret.

To address this potential downward bias, we instrument for 1[Mct > 0] with the

random assignment of district court judges to their cases. One district court judge is ran-

domly assigned per case (Bird (1975)).14 Figure 1 displays the boundaries of each district

court with dashed lines. Whether the district court cases were disproportionately assigned

to certain types of judges will be uncorrelated with treatment (the random assignment

of appellate judges) but may affect the likelihood of subsequent appeal. Theoretically,

district judges could affect the likelihood of appeal, for example, if some district judges

are less likely to be reversed and this lower reversal rate discourages litigating parties from

pursuing an appeal. Indeed, the correlation between district judge demographic character-14We use only cases decided by district court judges and exclude recommendations by magistrate judges

because litigants cannot directly appeal a magistrate judge’s recommendation (28 U.S.C. § 636(c)(1)).

14

istics and their reversal rates has been documented (Steinbuch (2009), Barondes (2011),

Haire, Songer and Lindquist (2003), Sen (2011)). Once we identify both 1[Mct > 0] and

Lawct , then the number of lags and leads in our model will not matter since additional

lags and leads of our fitted 1[Mct > 0] and Lawct would be orthgonal to other years’ fitted

1[Mct > 0] and Lawct.15

Eminent domain appellate decisions affirm or overturn a local regulation or con-

demnation that potentially affects a large portion of the circuit since some regulations

are at the state level. To distinguish between the geographically local direct effects and

the precedential effects of an appellate decision, we coded the corresponding zip codes

for the regulation or condemnation addressed in each case in our database (see Appendix

Figures A1). In robustness checks, we estimate the specification Yict = �0 + �1Lawct +

�2LocalLawict + "ict, where we separately instrument for Lawct and LocalLawict using

the random assignment of judges in cases that occur in the zip code locally and in cases

that occur in the circuit. We apply this specification to property price data only since

our other datasets are not available at the zip code level and conduct our analysis at the

circuit-quarter level using the calendar month of each decision. In principle, analysis at

the circuit-quarter level would increase the number of experiments by fourfold relative to

analysis at the circuit-year level.

3.3 Interpretation

It is important to note the difference between the conditional and unconditional effect of

Lawct. The conditional effect is the one of policy-interest to a judge making a decision on

a case already in front of him or her. The counterfactual for a pro-government decision

is a pro-plaintiff decision. The unconditional effect is the one of policy-interest to an

advocate or historian interested in the social change that is due to court-made law. The

counterfactual for a pro-government decision is no decision. For example, to calculate

the effect of 1 pro-government decision when there is only 1 decision in that circuit-year,

we would need to add the effect of 1[Mct > 0] with the effect of Lawct to obtain the15The results could, of course, vary depending on the observations that need to be dropped to allow for

additional years of lags or leads, the need to fit additional parameters, and the coarsening of the firststage because all lags and leads of all instruments are used for any given endogenous variable.

15

unconditional estimates of going from 0 to 1 pro-government decision.16 We show the

distributed lag coefficients for conditional effects of Lawct. We also show the average lag

coefficients of Lawct and of 1[Mct > 0], their respective joint tests of significance, and

joint tests of significance for the distributed lags of Lawct+1[Mct > 0].

In interpreting the magnitudes, we discuss the “typical ” conditional (unconditional)

effects, which refers to the causal effect of the typical number of pro-government takings

appellate decisions in a circuit-year. For example, to get the typical conditional effect,

we multiply the conditional effect of Lawct by E[Lawct|1[Mct > 0]], the typical propor-

tion of decisions that are pro-government when there are appellate takings cases, and by

E[1[Mct > 0]], the proportion of circuit-years with an appellate takings case.17 For uncon-

ditional effects, we calculate the typical effect of pro-government decisions, pro-plaintiff

decisions, and all decisions. These are, in turn: 1[Mct > 0]*E[1[Progovernmentct >

0]]+Lawct*E[Lawct|1[Mct > 0]]*E[1[Mct > 0]], 1[Mct > 0]*E[1[Proplaintiffct > 0]], and

1[Mct > 0]*E[1[Mct > 0]]+Lawct*E[Lawct|1[Mct > 0]]*E[1[Mct > 0]].18 All of these

calculations could be multipled by four to obtain cumulative effects.

3.4 First Stage

We begin our analysis by examining whether different outcomes result from eminent

domain cases being assigned to judges with different background characteristics. The

only prior study of this question documents that political affiliation alone does not predict

decisions in eminent domain cases Sunstein et al. (2006). This lack of correlation with

political affilation, which we confirm, may be due to Republican appointees being both

pro-growth and pro-individual property rights relative to Democratic appointees. Instead,

we find that Republican appointees who are prior U.S. Attorneys are more likely to vote

pro-government, but minority Democratic appointees are more likely to vote pro-plaintiff

in physical takings cases, and black (and minority) judges are more likely to vote pro-16To calculate the effect of n pro-government decisions when there are m decisions, we would need to add

1[Mct > 0]+n/m*Lawct.17Both E[Lawct|1[Mct > 0]] and E[1[Mct > 0]] are displayed in Table 1.18The effect of 1 pro-government decision in a typical circuit-year is 1[Mct > 0]+Lawct/E[Mct|1[Mct >

0]]. E[Mct|1[Mct > 0]] is obtained from dividing E[Mct], the typical number of appellate takingspanels, by E[1[Mct > 0]], the proportion of circuit-years with an appellate takings case. Both E[Mct]and E[1[Mct > 0]] are displayed in Table 1.

16

government in regulatory takings cases.

These voting patterns are intuitive, given the highly political nature of U.S. At-

torney positions. U.S. Attorneys, who are appointed by the President, hold discretion

in prosecuting particular types of crimes, and their political orientation can wield a sub-

stantial influence (Lochner (2002); Perry (1998)). Partisan bias, for example, has been

documented in the prosecution of federal public corruption cases (Gordon (2009)). Re-

publican appointees who are prior U.S. Attorneys would have advocated on behalf of

the government and may be less likely to support the pro-individual property rights di-

mension of the Republican platform while retaining the pro-economic growth aspect of

the party priorities. Republican-prior U.S. Attorneys also vote in favor of the govern-

ment in regulatory takings cases, though less significantly so, perhaps because business

entities constitute the largest share of regulatory takings plaintiffs and Republicans have

traditionally been pro-business.

In contrast, that minority Democratic appointees tend to favor the plaintiffin

physical takings cases may relate to the phenomena that people whose properties are

physically condemned tend to be poor and minority (Carpenter and Ross (2009); Frieden

and Sagalyn (1989)). Minority Democratic appointees may have prior experience serving

on behalf this demographic, or they may consciously or unconsciously sympathize based

on their backgrounds. Minority Republican appointees, however, vote in favor of the

government in physical takings cases. Notably, many of these judges previously served

in U.S. Attorneys General offices. Indeed, prior research has documented that prior

experiences may make judges more susceptible to priming of group identity (Berdejo

and Chen (2010)).19 Along these lines, black judges may be more likely to favor the

government in regulatory takings challenges, because such regulatory takings challenges

tend to be brought forth by relatively wealthy, non-black individuals, with business entities

constituting the largest share of regulatory takings plaintiffs (Stein (1995)). Most notably,

black judges have been found to vote differently than white judges on affirmative action,

race harassment, unions, and search and seizure cases in a manner consistent with the

interests of their group identity (Chew and Kelley (2008); Kastellec (2011); Scherer (2004);19Asmussen 2011 and other scholarship also suggest that Presidents who appoint minority candidates

take the opportunity to appoint more ideologically extreme individuals than they would otherwise.

17

Brudney et al. (1999)).

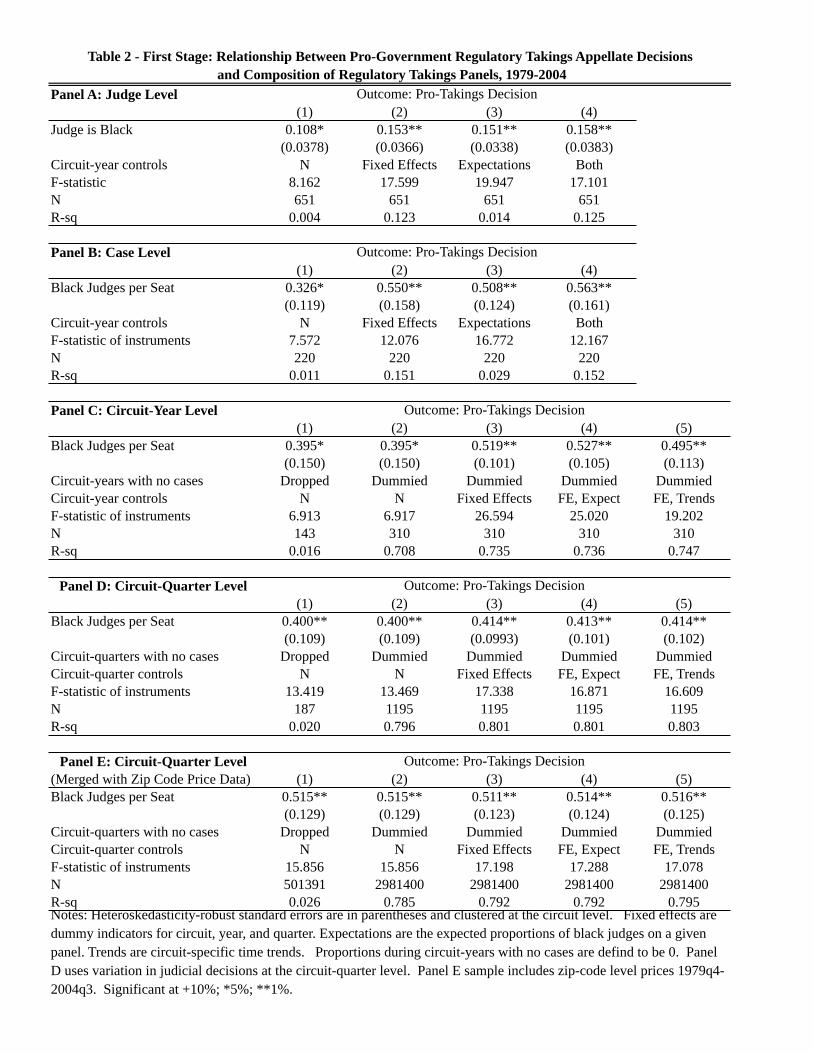

Table 2 shows that black judges are 11% more likely to vote in favor of the govern-

ment (pro-takings) in regulatory takings cases (Panel A).20 At the case level, an additional

actual black judge per seat on a three-judge panel increases the chances of a pro-takings

decision by 33% (Panel B). At both the judge level and case level, point estimates and

statistical significance increase with controls for circuit and year fixed effects and the ex-

pected judge type per seat. At the circuit-year level, an additional actual21 black judge

per seat increases the proportion of pro-government regulatory takings decisions by 40%

(Panel C). These estimates are slightly different from the case level since cases are not

evenly distributed across circuit-years.22 The estimates and statistical significance are

robust regardless of whether the circuit-years with no cases are dropped or are dummied

and the proportion of pro-takings decisions and judge type per seat are set to 0 for those

circuit-years with no cases.23 The F-statistic is 6.9 and increases with the inclusion of

controls up to 26.6. The R-square does not change much with the inclusion of these

controls. The first stage analysis is similar for the circuit-quarter level (Panel D).

At the level of our analysis, merged with price data, the estimates are slighly

different because of the differing numbers of zip codes per circuit (Panel E). The joint

F statistic on the two instruments is well past the conventional threshold for weak in-

struments at 15.9 (Stock and Yogo (2005)), and the F statistics again increase with the

inclusion of fixed effects and additional circuit-year controls up to 17. A falsification of

the instrumental variables shows that this kind of legal variation is not related to the

instrument in the one or two years before and after the true instrument (Appendix Table

A2).

To check whether our (linear) specifications miss important aspects of the data,20All analyses in this section cluster standard errors at the circuit level.21In what follows, when the term is omitted, we always mean actual as opposed to expected.22Not every circuit-year has a case and cases can bunch up unevenly across circuit-years. For an example

of how a coefficient can differ between circuit-year and case level, suppose there are 4 cases, one caseeach with 0, 1, 2, or 3 judges who are black, and suppose that the panel makes a pro-governmentdecision when there are 3 black judges. If 1 circuit-year has the case with 0 black judges and the othercircuit-year has the remaining 3 cases, the coefficient at the circuit-year level is 0.5 (= difference inpercent pro-takings/difference in black judges assigned per seat) but when the 1 circuit-year with thecase has the case with 1 black judge, the coefficient at the circuit-level is 1.5. This example also showshow an increase in the probability of a pro-government decision due to an additional judge of a typeper seat can be greater than 1.

23The R-square increases significantly.

18

Figure 4A presents nonparametric local polynomial estimates of the effect of number of

black judges per seat on the proportion of pro-government decisions.24 The relationship

is monotonically increasing and not driven by outliers. In other words, having randomly

more black judges assigned corresponds to unexpectedly more pro-government takings

decisions. Similar results obtain with minority judges.

We conduct an identical analysis for physical takings in Table 3. Minority Demo-

cratic appointees are 20% less likely to vote in favor of the government in physical takings

cases while Republican appointees who are prior U.S. Attorneys are 18% more likely to

vote in favor of the government (Panel A). Similar patterns hold at the case level (Panel

B). At the circuit-year level, an additional minority Democratic appointee reduces the

proportion of pro-takings decisions by 62%, while an additional Republican-prior U.S.

Attorney judge per seat increases the proportion of pro-takings decisions by 93% (Panel

C).25 The joint F-statistic is 9 and increases with the inclusion of controls up to 19. The

first stage analysis is similar for the circuit-quarter level and the F-statistic ranges from

12 to 13. At the level of our analysis, merged with price data, the joint F statistic on

the two instruments exceeds the conventional threshold for weak instruments at 43 (Panel

E). Nonparametric local polynomial estimates show that the relationship is monotonically

increasing between Republican-U.S. Attorney judges and pro-government decisions while

it is decreasing, though less sharply so, for minority Democratic appointee judges and

pro-government decisions (Figure 4B). Neither relationship is driven by outliers.

3.5 LASSO Instruments

Some econometricians recommend larger first stage F-statistics to ensure that the first

stage is sufficiently strong, such as F stat=25 or 50 to allow for heteroskedasticity and

serial autocorrelation (Olea and Pflueger (2010)) The number of possible combinations of

judges or demographic characteristics on a judicial panel is very large, because judicial24Estimation proceeds in two steps. In the first step, we regress the proportion pro-government on circuit

and year fixed effects and we regress the number of black judges per seat on the same. Next, we takethe residuals from these two regressions and use the nonparametric local polynomial estimator to char-acterize the relationship between black judges and pro-government decisions. We use an Epanechnikovkernel with the default bandwidths selected by Stata.

25Such large point estimates are possible if having 1 Republican-prior U.S. Attorney tips the decision andthere are few cases with 2 Republican-prior U.S. Attorneys.

19

demographics are heterogeneous within each circuit and a circuit may have as many as

forty judges in the pool of judges available to be assigned. With this very large number of

possible panel compositions, our strategy benefits from a surfeit of experimental variation.

Choosing among a large number of instruments, however, is a challenging statistical issue

involving a trade-off between increasing the power of the first stage regression (Angrist and

Imbens (1995)) and avoiding the weak instruments problem with additional instruments

(Stock and Yogo (2005).

We use a LASSO technique to address this issue of instrument selection (Belloni et

al. (2011)) and to verify the robustness of our main IV results to alternative instruments.

Using LASSO (least absolute shrinkage and selection operator) in the first stage presents

several advantages relative to using OLS. While OLS has low bias, it also has two disad-

vantages. First, OLS lacks sparseness: large subsets of covariates are deemed important,

resulting in too many instruments, which makes 2SLS susceptible to a weak instruments

problem. Second, OLS lacks continuity: changing the data a bit results in different sub-

sets of covariates deemed important. LASSO is a sparse model, which solves both of these

problems. Formally, LASSO modifies OLS by minimizing the sum of squares subject to

the sum of the absolute value of the coefficients being less than a constant. The nature

of this constraint tends to set some coefficients to exactly 0 and hence reduces model

complexity. Intuitively, LASSO gives interpretable models by imposing a data penalty

for having too many covariates. In addition, LASSO ensures stability in instrument selec-

tion, making it an effective tool in selecting optimal instrumentals from a large number of

valid instruments. Belloni et al. (2011) show that LASSO is theoretically optimal under

certain conditions including sparsity.26 Because it selects optimal instruments, LASSO

enhances statistical precision when using the random assignment of judges.27 Intuitively,

optimal instruments are the strongest predictors of the endogenous variable where the

cross-correlation of the predictors are such that the two-stage least squares maximizes the

amount of information that can be obtained from exogenous predictors of the endogenous

variable. On a separate note, the use of the LASSO instruments provides a check of over-26Even if sparsity were not satisfied, LASSO can still be effective for finding relevant instrumental vari-

ables.27Belloni et al. (2011) show that the increased uncertainty due to selecting among many instruments

does not show up to first order.

20

identification since the two-stage least squares estimates derived from different judicial

characteristics should be similar assuming homogenous treatment effects.28

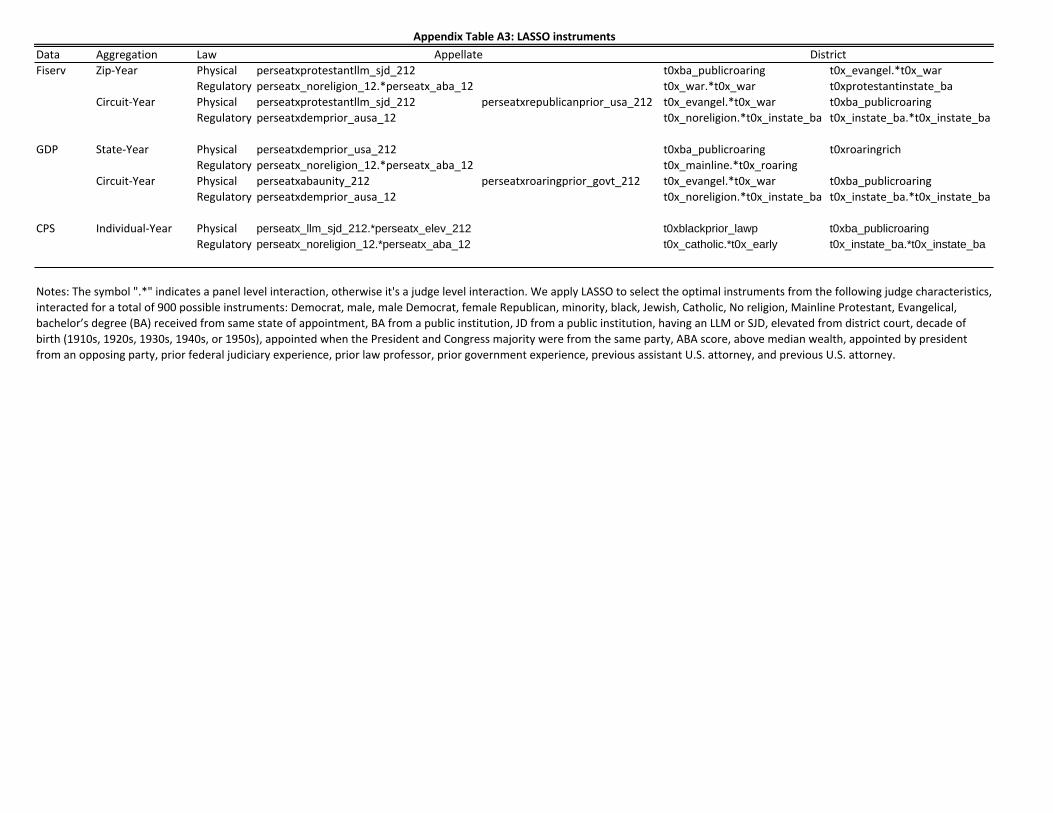

To construct our potential LASSO instruments, we use 30 biographical character-

istics29 and their interactions at the judge level and panel level,30 yielding a total of 900

possible instruments. The instruments chosen by the LASSO procedure are listed in Ap-

pendix Table A3. For example, at the circuit-year level, the LASSO procedure selected

Democrat prior assistant U.S. Attorneys for regulatory takings. The F statistic is 38,

representing a 100% improvement over the non-LASSO first stage F-statistics displayed

in Column 5 of Panel C in Tables 2 and 3. We consider a similar set of biographical

characteristics and instrumental variables for the district judges to identify an exogenous

component of the existence of an appeal. The random assignment at the district level is

not correlated with the random assignment at the appellate level. In our main tables, we

show the two-stage least squares results using the district LASSO instruments.

4 The Impact of Eminent Domain

4.1 Governmental and Market Response to Appellate Decisions

We should expect to see an effect if the following three assumptions are met: judges follow

precedent; on the margin, pro-takings decisions in appellate courts make it easier for

subsequent government actors to take; and market actors respond to appellate decisions.

While the first assumption is less contested, we examine the second two assumptions.

In separate analyses (Chen and Yeh 2011), we document that land appropriations for

transportation projects shift in response to eminent domain decisions. We use a dataset28By homogenous treatment effects, we mean the assumption that close cases whose decisions could be

affected by the judicial panel composition affect economic outcomes in the same manner regardless ofthe type of judicial panel.

29Democrat, male, male Democrat, female Republican, minority, black, Jewish, Catholic, No religion,Mainline Protestant, Evangelical, bachelor’s degree (BA) received from same state of appointment, BAfrom a public institution, JD from a public institution, having an LLM or SJD, elevated from districtcourt, decade of birth (1910s, 1920s, 1930s, 1940s, or 1950s), appointed when the President and Congressmajority were from the same party, ABA score, above median wealth, appointed by president from anopposing party, prior federal judiciary experience, prior law professor, prior government experience,previous assistant U.S. attorney, and previous U.S. attorney.

30For example, for the combination of “black and Democrat,” we examine the number of black Democraticappointees per seat for the judge level interactions and examine the number of Democrat appointeesper seat multiplied with the number of black judges per seat for panel level interactions.

21

provided by the Uniform Relocation Assistance and Real Property Acquisition Policies

Act of 1970, which requires states to report basic statistics about property transfers for

transportation projects. In response to pro-takings physical (but not regulatory) takings

cases, local governments become more likely to displace commercial landowners, who

are more expensive to relocate, even as compensation remains the same or falls. We

further document that the number of ordinances and exactions that become codified

also increases after pro-takings decisions. In other work, we show that markets, firms,

and media respond to appellate decisions. For example, media stock prices respond to

appellate decisions on FCC actions affecting media firms but not non-media firms (Chen,

Yeh and Araiza (2011)), the number of newspaper reports about the appellate topic

increase in response to appellate decisions in the circuits where the decisions occur (Chen

and Yeh (2011); Chen, Yeh and Araiza (2011)), and firms adopt sexual harassment human

resources policies subsequent to pro-plaintiff appellate sexual harassment decisions (Chen

and Sethi (2011)). We now turn to the effects of eminent domain decisions on property

prices.

4.2 Property Prices

4.2.1 Regulatory Takings

Pro-government decisions in appellate regulatory takings cases, which make it easier to

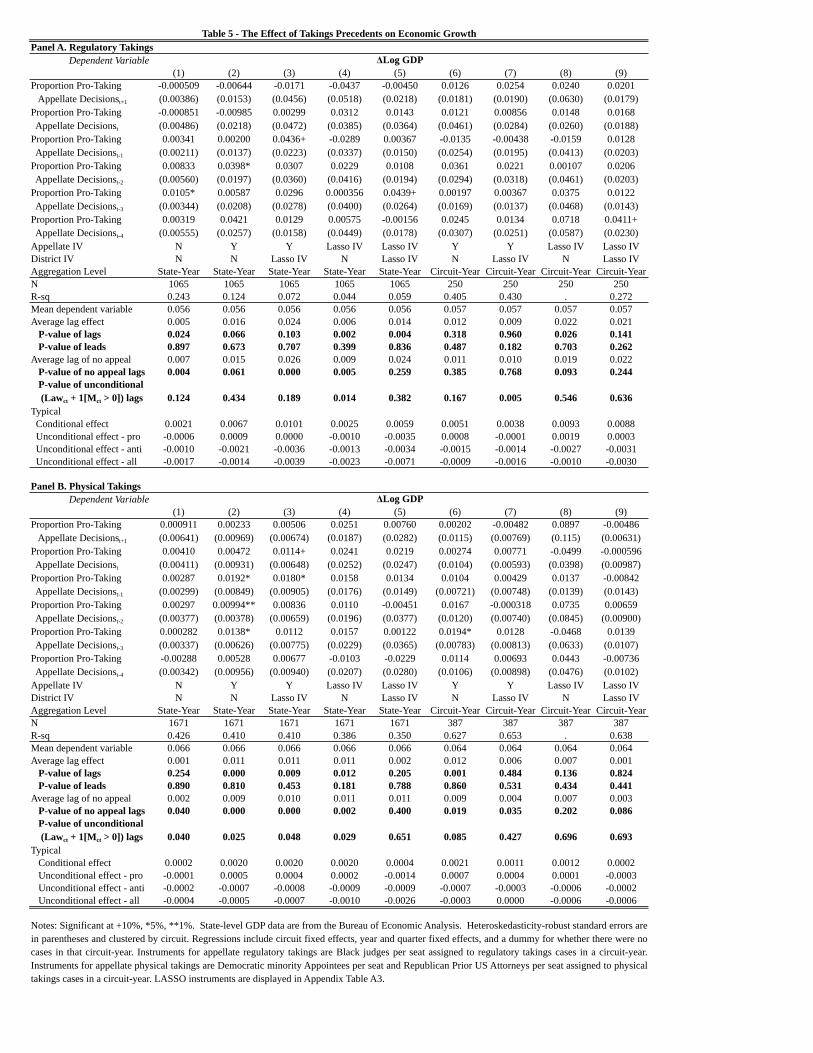

regulate without having to compensate landowners, spur growth in property prices. Table

4 Panel A shows the main results for the distributed lag specification of first-differenced

log house prices. Column 1 displays the naïve OLS estimates. The OLS lead coefficient

is the largest and statistically significant at the 1% level, indicating the importance of an

instrumental variables strategy to address trends that may drive both prices and judicial

decisions (Column 1). Indeed, in the IV estimates, the lead coefficient is not statistically

significant and its magnitude is a fraction of the magnitude of the lag coefficients (columns

2-9).

Column 2 displays the estimates using appellate-level IV, Column 3 displays the

estimates using both appellate and district-level IVs, Column 4 displays the estimates

using LASSO to select the appellate IV, and Column 5 uses LASSO for both appellate

22

and district IV. Columns 6-9 display the corresponding IV estimates when the data is

collapsed to the circuit-year level using population-weighted averages. Because change

in prices may be autocorrelated, it is customary to rely on joint tests of significance

to determine whether the effects are statistically significant. The main IV estimates in

Column 2 are not individually statistically significant, but they are jointly significant

at the 1% level. The average lag effect is 0.005, which indicates that a pro-government

regulatory takings decision (more precisely, when 100% of regulatory takings decisions

are pro-government instead of pro-plaintiff) increases property price growth by 0.5 log

points (percentage points) on average in each year for the next four years.31 When using

IV for both the appellate decisions and the presence of an appeal from the district court,

the average lag effect is similar in magnitude and the individual coefficients are similar

in magnitude and more statistically significant, though their joint significance weakens

(Column 3).32 Using LASSO instruments at the appellate level gives jointly significant

effects whose average is similar in magnitude to the previous estimates (Columns 4 and 5).

At the circuit-year level, the estimates are not significantly different from 0 when using

the non-LASSO instrument of black judges (Columns 6-7) but becomes more precisely

estimated and statistically significant when using the LASSO instrument (Columns 8-9).

The average effect is similar to the average effects found at the zip-year level in Columns

2-5.33 In unreported regressions, when we weight by the number of cases in the current

and previous 4 years to take into account the number,34 instead of percentage, of pro-

takings cases, the estimates become more statistically significant and precisely estimated

across the specifications.35

31The outcome is quarterly change in log prices. If the mean dependent variable of 1.1% is annualized,the average yearly change is about 5%, which is close to average local GDP growth displayed in Table5 and to annualized growth in other studies using the same data (Mian and Sufi (2009)).

32Estimates using the district IV may be less precise than the estimates without district IV becausethe LASSO-selected district IV have, at worse, F-statistics of around 8, just below the conventionalthreshold for strong instruments. Estimates may be further weakened because we greatly increase thenumber of endogenous variables to 12 and the number of instrumental variables to 36. While theoff-year (e.g. contemporaneous appellate instrument on lag pro-takings precedent) and off-level (e.g.district instrument on pro-takings precedent) instruments are statistically insignificant, the cumulationof off-year/off-level coefficients as illustrated in Appendix Table A2 may be an issue.

33The R-square is of less value in the IV context and is not reported in some of the IV regressions.34Both treating Lawct as an average of Mct number of decisions or as appearing with Mct frequency show

improvements.35In additional unreported results, the results change little when we control for lagged dependant vari-

ables, whether in levels or changes.

23

Appendix Table A4 presents a number of robustness checks using the main IV

specification in Table 4, Column 2 as the baseline. Columns 1-3 show the average of

the yearly lags, joint F test of the lags, and joint F test of the leads, respectively. The

robustness checks include: adding circuit-specific time trends (row A), removing circuit

and year fixed effects (row B), clustering standard errors at the state level, which exceeds

the conventional threshold for the number of clusters (row C), controlling for the expected

number of black judges per seat (row D), using zip code level population weights (row

E), and adding 2-year leads (row F). As randomization would predict, for each check, the

point estimates hardly change36 and the statistical significance generally increases with

the inclusion of controls, especially fixed effects. When we drop 1 circuit at a time, the

average lag estimates change little (row G), though the joint significance varies. Using

legal variation at the circuit-quarter (row I) reveals slightly larger point estimates and

statistical significance. The lead coefficients are typically insignificant.

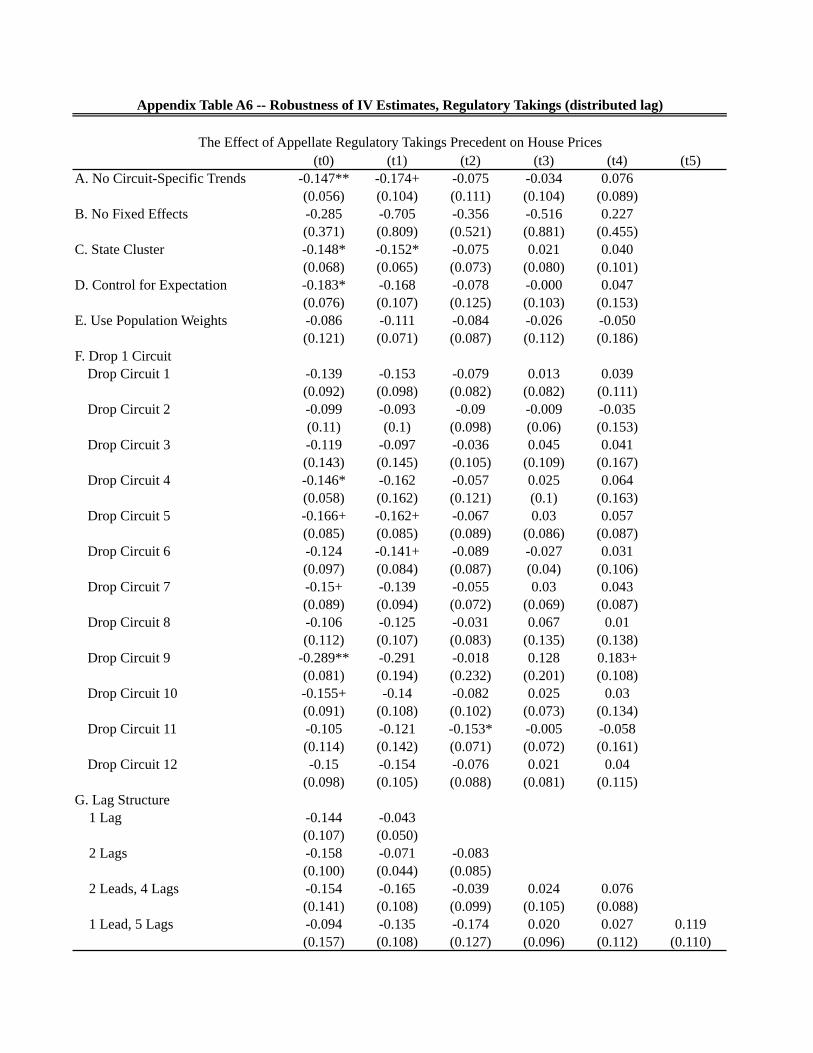

Appendix Table A5 further verifies the robustness of our distributed lag specifi-

cation by showing the point estimates for each lag and by varying the number of lags

and leads. Consistent with the baseline IV results in Column 2 of Table 4, the point

estimates of the individual lags are insignificant. However, each row suggests a negative

initial impulse that is eventually overcome by a net positive response, as revealed by the

point estimates on the more distant lags (rows A-F) and by the robustness of this pattern

to varying the number of lags and leads (row G). Notably, in the specification with 4 leads

and 1 lag, none of the lead coefficients are individually or jointly statistically significant

and the magnitudes of the leads are an order of magnitude smaller than the estimated

lags. When controlling for the local direct effect of the taking, the precedential effects

become slightly larger (rows H-I). The local direct effects are opposite in sign. The lead

coefficients of the precedential effects are negligible while the lead coefficients of the local

direct effects are larger in absolute value than the lag coefficients of the local direct effects;

this pattern is consistent with the local taking having occurred quite a few years before

the appellate decision.37

36The point estimate becomes negative when using population weights, but Column 6 in Table 4 showsthat the impact on population-weighted mean outcomes is, in any event, not distinguishable from 0 andColumn 7 in Table 4 also shows an imprecisely negative impact. Moreover, when we use the LASSOinstrument in order to correspond to Column 8 in Table 4, the point estimate is positive and significant.

37The mean local direct takings effect on growth is still negative even accounting for the lead coefficients.

24

We also observe the pattern of having a negative impulse followed by net posi-

tive growth by years 3 and 4 when we use log price index as the outcome and include

circuit-specific time trends as the default specification in the same set of robustness checks

(Appendix Table A6).38 According to our model, negative price effects may be due to un-

derinvestment as with regulations, governments typically do not compensate landowners.

However, as we discuss later, the impact on economic growth is positive, suggesting that

the public use benefits eventually outweigh underinvestment.

Having established that our empirical framework approximates a randomized con-

trol trial, we next interpret the magnitude of our estimates. Conditional on the presence

of an appeal, the average effect of pro-takings precedent on property price growth is 0.5%

points (Column 2 of Table 4), which implies property price growth is 0.2% points higher

on average due to the typical proportion of regulatory takings appellate precedent in a

circuit-year. To put our magnitudes in perspective, we compare our estimated effects with

those in other studies with exogenous variation: houses along unpaved paths that were

randomly assigned to be paved experienced a 16% increase in appraised property values

(Gonzalez-Navarro and Quintana-Domeque (2011)), whereas we find a 4% increase in

property prices after four years (Appendix Table A6). We conduct a back-of-the-envelope

calculation using estimates from Shoag (2011), which exploits idiosyncratic variation in re-

turns to state government pension plans to estimate an additional $1 of state spending per

capita leads to 0.01 percent change in housing prices. This implies that pro-government

regulatory takings precedent in a typical circuit-year is equivalent to $20 increase in state

spending per capita. This number may be somewhat smaller, however, if Shoag’s impacts

are underestimated due to an attenuated channel from state government pension plans to

house prices. Applying the formulas in Section 3.3 to estimates using district IV (Column

5), we find that the typical unconditional effect of pro-takings precedent in a circuit-year

accounting for the effect of the presence of an appeal is 0.05% points, or $5 in per capita38For a positive effect by the last year, price growth must be on average positive during the period of the

lag distribution, which our price growth analyses confirm. Quantitatively, the levels and growth line uponly approximately. For example, in the check that drops Circuit 12 (Washington, D.C.) in AppendixTable A6, a 4% increase in property price levels occurs in the 4th year. The cumulative effect of pricegrowth in the corresponding row in Appendix Table A5 implies a 2.5% increase in price levels. Thedifference may be due to the level analysis being a poorer fit of the data. It assumes that prices returnto the same level as the control group after the fourth year whereas the growth regression assumes thatprice growth returns to the control group growth rate after four years.

25

state spending.39 The typical unconditional effect of pro-plaintiff precedent is a reduction

of 0.03% points in property price growth. The typical unconditional effect of all decisions

is 0.02% points in property price growth. In sum, we find economically significant posi-

tive impacts on growth in property prices when it is easier for the government to regulate

without having to compensate landowners for restrictions on property development.

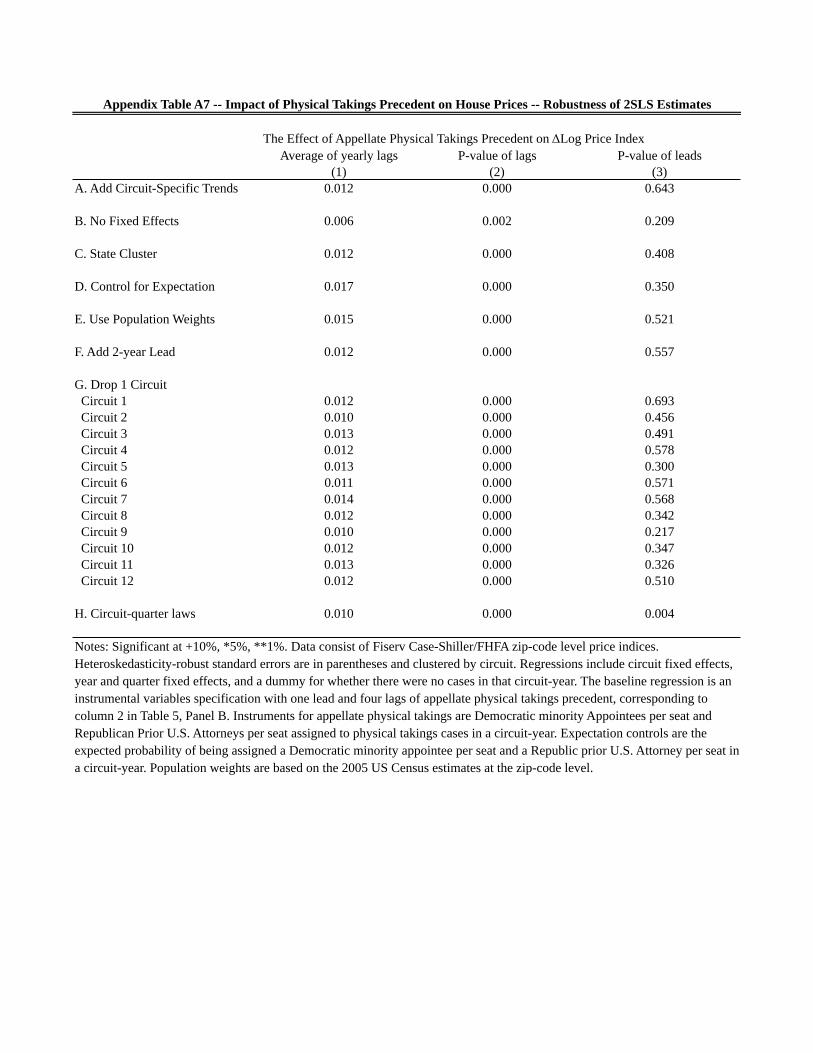

4.2.2 Physical Takings

Ruling in favor of the government in physical takings cases, making it easier to condemn

property, also spurs growth in property prices. Table 4 Panel B presents the same speci-

fications as in Panel A.40 The point estimates of the lags are similar across secifications,

in general jointly significant, and often individually significant, while the lead coefficients

are not statistically significant. Conditional on having an appeal, the average lag effect

of a pro-takings decision ranges from 0.007 to 0.013 (referring only to the statistically

significant estimates in the bottom portion of Panel B). In all robustness checks, the av-

erage conditional lag effect ranges from 0.006 to 0.017 (Appendix Table A7); the lags are

always jointly significant at the 1% level and the leads are not jointly significant except

in one robustness check, which we observe at the circuit-quarter level.41 Consistent with

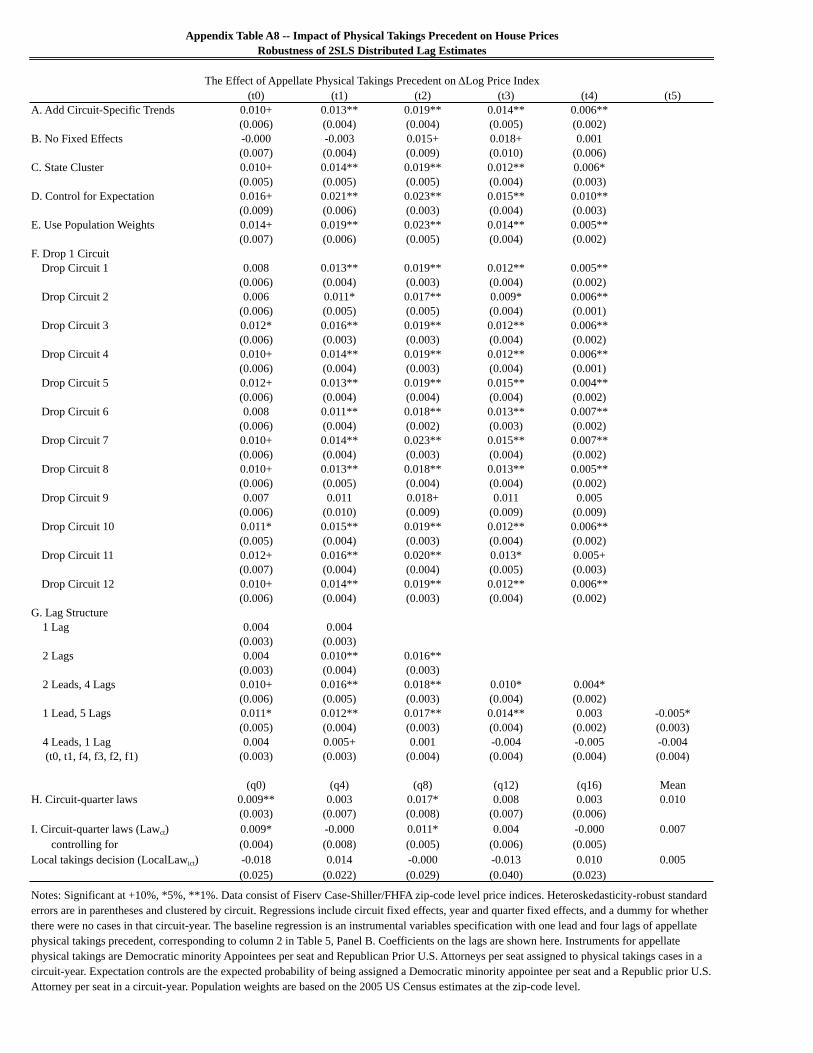

Table 4’s results, the robustness checks in Appendix Table A8 show that the individual

point estimates are positive and significant though there is also some decay over time in

the magnitude. Because of the small number of clusters in our main specification due to

only 12 circuits, we use a wild bootstrap (Cameron et al. (2008)) and find that the point

estimates within a year of the pro-takings precedent and 3-4 years later each differ from

the null of 0 at the 10% level. As in Appendix Table A5, we again observe that the prece-

dential effect is robust to conrolling for the local direct effects (Appendix Table A8 Rows39The effect of presence of an appeal is jointly significant and consistent across specifications. The

joint significance of the lagged sum of the coefficients on 1[Mct > 0] and on Lawct are also generallystatistically significant.

40The sample size is larger because we have additional years of data for physical takings.41Some physical takings cases take very long to resolve. The media frequently discusses the cases before

the actual decision is published, and the time between oral argument, which is public, and publicationcan be many years (in the extreme). Since the oral argument date is not reliably observable for mostcases, we substitute the publication date of the district court decision as the date of appellate decisionto verify that economic outcomes do not move in advance of appellate decisions.

26

H and I), which are again occasionally sizeably negative though imprecisely measured.42

Having established the robustness of the estimates, we again turn to their interpre-

tation. The conditional effect of 0.7 to 1.3% points in property price growth per year on

average over 4 years translates to a effect of 0.12-0.23% points due to the typical number

of physical takings appellate precedents in a circuit-year. When effects of pro-takings

decisions and presence of an appeal are significantly estimated (Columns 2, 6, 7), the

typical unconditional effect of pro-government takings decisions is 0.04-0.07% points, the

typical unconditional effect of pro-plaintiff takings decisions is negative 0.04-0.08% points,

the typical effect of all decisions is negative 0.01-0.06% points in property price growth.

4.2.3 Discussion

Our results thus far indicate that compared to conditional effects, the unconditional effects

of takings decisions are far smaller. The net unconditional effect of all decisions is even

negative for physical takings. One interpretation of the negative effect is that some district

judges write strong opinions that are more likely to be appealed but are also more likely

to influence precedent in a manner that threatens local developers.43 A complementary

interpretation is that the presence of an appeal captures selection: physical takings cases

that reach the appeals court could involve exceptionally large or wasteful government

projects that have a delayed positive effect, whereas regulatory takings cases that reach the

appeals court could involve regulations that make environmental or business sense earlier

on (Appendix Table A5 and A8 Row I). This potential selection effect is consistent with the

smaller and possibly negative local direct effects of the taking. The smaller unconditional

effect relative to the conditional effect could also reflect reluctance of local business owners

to invest in the surrounding area given the uncertainty surrounding the pending appellate

decision. These mechanisms could help explain popular unrest in response to high profile42In unreported results, the lead coefficients of the precedential effects are again negligible while the lead

coefficients of the local direct effects are sizeable and larger in magnitude than the lag coefficients of thelocal direct effects, which is consistent with the local taking having occurred quite a few years beforethe appellate decision.

43Local developers appear more likely to appeal eminent domain decisions. In the Auburn Courts ofAppeals database, which records a random sample of over 18,000 decisions from 1925 to 2002, of the164 appellate court decisions since 1975 involving property, a government actor is appealing the decision20% of the time, and of the 855 appellate decisions since 1975 involving regulation, a government isappealing the decision 22% of the time.

27

takings, which may have negative local direct effects, but the vast majority of unlitigated

takings may actually have a positive impact on growth.

4.3 Economic Growth

4.3.1 Regulatory Takings

In the previous sub-section, we find that making it easier for the government to take leads

to an increase in property price growth, but as our theory suggests, this could be due to

over-investment by landowners who are receiving full insurance against the risk of taking

with no premium paid. To distinguish between over-investment and public use benefits,

we turn to the effects on economic growth. We find that decisions making it easier for the

government to take have positive effects on economic growth. Table 5 shows specifications

similar to those in Table 4. The average lag effect is 0.016 in Column 2. With LASSO, the

average estimate is 0.006, but becomes more jointly significant (Column 4). Collapsed to

the circuit-year level, the estimates increase to 0.022 (Column 8). In robustness checks,

the lag estimates have mean effects ranging from 0.010 to 0.024 except when population

weights are used (Appendix Table A9). Leads are not significant in any specification. The

impulse response function is also robust and show an initial negative effect on economic

growth if any, followed by a more robust positive growth effect in the second through

fourth years (Appendix Table A10).44 The average lag effect of the presence of a case is

robustly positive, ranging from 0.009 to 0.026 (Table 5).

To interpret the magnitudes, economic growth is 0.7% points faster due to the

typical regulatory takings appellate precedent in a circuit-year (Table 5 Column 2). To

interpret the unconditional effect, we focus a specification that uses district IV and has

relatively precise estimates of both the average lag effect of a decision and the average lag

effect of the presence of an appeal (Column 3). The typical unconditional effect of pro-

government takings decisions is negative 0.003% points, the typical unconditional effect

of pro-plaintiff takings decisions is negative 0.04% points, the typical effect of all decisions

is negative 0.04% points in economic growth.44There are no significant leads in the specification with 4 leads and 1 lag and the point estimates of the

leads are very small, while similarly precisely estimated as in other specifications.

28

4.3.2 Physical Takings

As with the property prices analyses, the estimates of the impact of physical takings prece-

dent on economic growth is precise and robust. The average lag effect of pro-government

physical takings decisions of 1.1% points is jointly significant in many specifications (Table

5 Panel B). The lead effects are not statistically significant. The point estimates are cen-

tered around 1.1% points with the inclusion and exclusion of controls, dropping circuits,

and population weighting (Appendix Table A11). The positive growth effect appears par-

ticularly sharp in the first and second year after the decision and never appears in the

leads (Appendix Tables A11 and A12).

To interpret the magnitudes, economic growth is 0.2% points faster due to the

typical physical takings appellate precedent in a circuit-year (Table 5 Column 2). To

interpret the unconditional effect, we focus a specification that uses district IV and has

relatively precise estimates of both the average lag effect of a decision and the average

lag effect of the presence of an appeal (Column 3). The typical unconditional effect of

pro-government takings decisions is 0.04% points, the typical unconditional effect of pro-

plaintiff takings decisions is negative 0.08% points, the typical effect of all decisions is

negative 0.07% points in economic growth.

4.4 Economic Inequality

Our model suggests that those landowners who are disproportionately affected by takings

and who are undercompensated would be adversely affected by decisions making it easier

for the government to take. As the dissent in Kelo articulated, “extending the concept

of public purpose to encompass any economically beneficial goal guarantees that these

losses will fall disproportionately on poor communities. Those communities are not only

systematically less likely to put their lands to the highest and best social use, but are

also the least politically powerful.” Even if developers create jobs, it is not clear how the

jobs would be distributed. We now investigate whether eminent domain has a disparate

impact on minority groups, as feared by many legal observers and as suggested by the

voting patterns correlated with a judge’s demographic background. Recall that in physical

takings cases, minority Democratic appointees are more likely to vote for the plaintiff, who

29

is often a minority. In regulatory takings cases, black judges are less likely to vote for the

plaintiff, who is typically relatively wealthy and non-black.

4.4.1 Housing Outcomes

We begin our analysis by observing that 51% of minorities (71% of whites) own a home,

8% of minorities (2% of whites) live in public housing, 27% of minorities (12% of whites)

live below the poverty line (Appendix Table A13). Focusing on specifications with both

appellate and district LASSO IV (Columns 4, 8, and 12), we find pro-government de-

cisions in regulatory takings cases reduce minority home ownership by 2.9% points and

increase the probability minorities live in public housing by 0.8% points. Whites are