Embed Size (px)

Citation preview

Review of Quantitative Finance and Accounting, 12 (1999): 341±350

# 1999 Kluwer Academic Publishers, Boston. Manufactured in The Netherlands.

The Determinants of Debt Maturity:The Case of Bank Financing in Singapore

SHENG-SYAN CHEN

Department of Finance, College of Management, Yuan-Ze University, Taoyuan, TaiwanE-mail: [email protected]

KIM WAI HO

Division of Banking and Finance, Nanyang Business School, Nanyang Technological University,Singapore 639798

GILLIAN H.H. YEO

Division of Banking and Finance, Nanyang Business School, Nanyang Technological University,Singapore 639798

Abstract. This study presents important international evidence by examining the determinants of debt maturity

of listed ®rms in Singapore, a major ®nancial center in Asia. We focus on bank debt because it is the principal

source of ®nancing for most Singapore ®rms. We ®nd that consistent with the contracting-cost hypothesis, ®rms

with greater growth opportunities rely more heavily on short-term bank debt whereas larger ®rms are more likely

to use long-term bank debt. In contrast, we ®nd no strong support for either the tax or signaling hypotheses.

Key words: maturity, bank debt, contract-cost hypothesis, tax hypothesis, signaling hypothesis

JEL Classi®cation: G32, D82, E43

1. Introduction

The determinants of corporate debt maturity have recently been empirically examined in

Barclay and Smith (1995a), Guedes and Opler (1996), and Stohs and Mauer (1996).

Barclay and Smith ®nd that consistent with contracting cost hypothesis, ®rms with more

growth opportunities have less long-term debt while large ®rms and regulated ®rms have

more long-term debt. They ®nd little support for tax and signaling hypotheses. Guedes and

Opler report largely similar results when they examine the determinants of the maturity of

new issues of corporate debt. Stohs and Mauer examine the determinants of corporate debt

maturity using a maturity measure that incorporates detailed information about all of a

®rm's liabilities. They ®nd that proxies for signaling, tax, and maturity-matching

hypotheses are generally signi®cant determinants of debt maturity. However, their

empirical analysis is less supportive of agency cost hypothesis.

This study extends the above literature by using a unique data set collected from

®nancial statements of Singapore listed ®rms. Singapore is an important ®nancial center in

Asia, with many multinational banks operating there. Since results from existing studies

on corporate debt maturity may re¯ect the corporate environment in the U.S., our study

provides important international evidence. Further, since the number of listed ®rms in

Singapore is not large, manual collection of data is not prohibitively costly. Finally,

Singapore ®rms rely principally on bank borrowing, partly because of the relatively

underdeveloped bond market. This provides a unique setting to test the maturity of bank

debt.1 Since bank debt is a form of inside debt (see Fama (1985), James (1987) and others),

it would be interesting to know whether the determinants of its maturity are similar to

those of the maturity structure of all corporate liabilities.

Firms in Singapore are required to disclose separately in their ®nancial statements the

amount of bank debt that is repayable within twelve months from the balance sheet date

(as current liabilities) and the amount that is repayable after twelve months from the

balance sheet date (as long-term liabilities). We use the percentage of total bank borrowing

that is repayable within twelve months from the balance sheet date as our measure of

maturity.2 Our results are consistent with the contracting cost hypothesis: ®rms with higher

growth options tend to use more short-term bank borrowing while large ®rms tend to use

less short-term bank borrowing. We ®nd no strong support for the tax and signaling

hypotheses.

The remainder of the paper is organized as follows. Section 2 provides a brief discussion

of the determinants of the maturity of bank borrowing. Section 3 describes the data.

Empirical results are presented in Section 4. The ®nal section provides some concluding

remarks.

2. Determinants of the maturity of bank borrowing

The determinants of the maturity of bank borrowing may be examined in the context of

contracting cost, tax and signaling hypotheses. These theories and the independent

variables used in our study are brie¯y described in this section. These discussions are

dominated by demand-side considerations as information on supply-side behavior by

banks are not available due to the fact that banks in Singapore have to observe secrecy

codes.

2.1. Growth opportunities

Using shorter-term bank borrowing may mitigate the underinvestment problems (Myers

(1977)) and the Jensen and Meckling's (1976) asset substitution problem (Barnea, Haugen

and Senbet (1980)). The agency problems of underinvestment and asset substitution are

expected to be more severe for ®rms with more growth options in their investment

opportunity sets since they have more ¯exibility in their choice of future investments

(Titman and Wessels (1988) and Barclay and Smith (1995a, 1995b)). Hence, ®rms with

more growth options in their investment opportunity sets should use shorter-term bank

borrowing.

Stulz (1990) and Hart and Moore (1990) provide another explanation for the

relationship between growth opportunities and the maturity of bank borrowing. They

suggest that long-term borrowing is more effective in limiting managerial discretion in

342 CHEN, HO AND YEO

making bad investments. Hence, ®rms with few growth options should use more long-term

bank borrowing.

Following Barclay and Smith (1995a, 1995b) and others, we employ the ratio of the

market value of the ®rm's assets to their book value as a proxy for growth options in the

®rm's investment opportunity set. We expect that the higher the ®rm's market-to-book

ratio, the higher will be the proportion of short-term versus long-term bank borrowing. We

also use depreciation as a percentage of ®rm value and earnings-price ratio as alternative

proxies for growth opportunities. We expect ®rms with more depreciation expenses and

higher earnings-price ratio to have more tangible assets and fewer growth options in their

investment opportunity sets, and hence to use less short-term bank borrowing.3

2.2. Firm size

On average, small ®rms tend to have more growth options than large ®rms (Denis (1994)

and others). If ®rm size is positively correlated with the measurement error in the proxy

variable used to measure the ®rm's investment opportunity set, then the contracting-cost

hypothesis suggests that smaller ®rms will use more short-term bank borrowing (Barclay

and Smith (1993)).

Long-term bank borrowing has higher monitoring costs than short-term bank borrowing

because the bank's bargaining position is weakened with the longer maturity (Fama

(1985)). Larger ®rms are more able to take advantage of the scale economies by reducing

the per unit monitoring costs because they tend to borrow larger loans (Reed and Gill

(1989)). Hence, this contracting-cost argument suggests that larger ®rms will use more

long-term bank borrowing.

2.3. Firm quality

The signaling hypothesis suggests that high quality (undervalued) ®rms will want to use

more short-term borrowing while low quality (overvalued) ®rms will want to use more

long-term borrowing (Flannery (1986) and Kale and Noe (1990)). As in Barclay and Smith

(1995a, 1995b), we use the ®rm's abnormal future earnings to measure ®rm quality. High

quality ®rms are likely to have positive future abnormal earnings while low quality ®rms

are likely to have negative future abnormal earnings. We expect ®rms with higher

abnormal future earnings to use more short-term bank borrowing.

2.4. Term structure

Brick and Ravid (1985) suggest that if the term structure of interest rates is upward

sloping, the use of long-term debt reduces the ®rm's expected tax liability and hence

enhances the ®rm's value because long-term debt pays more interest in initial periods and

less interest in later periods than short-term debt.4 On the other hand, if the term structure

of interest rates is downward sloping, the use of short-term debt increases ®rm value. Brick

THE DETERMINANTS OF DEBT MATURITY 343

and Ravid's analysis suggests that ®rms use less short-term bank borrowing when the term

structure of interest rates is upward sloping and vice-versa.5

3. Data and summary statistics

Data on short- and long-term bank borrowing are collected from available ®nancial

statements of ®rms listed on the Stock Exchange of Singapore between 1983 and 1991.

Firms from the ®nance industry (i.e. banks, ®nancial service and insurance companies) are

excluded. To ensure no survivorship bias, ®rms which have merged or delisted during the

sample period as well as ®rms which were newly listed during the same period are also

included. The ®nal sample of ®rms is 128, representing approximately 70% of the number

of Singapore listed ®rms on the main trading section of the Stock Exchange of Singapore

at the end of 1991.6

The summary statistics are shown in Table 1. The amounts of short-term bank

borrowing for a ®rm are the average book values of short-term bank borrowing (i.e. bank

borrowing due within one year) as classi®ed under current liabilities in the balance sheet

Table 1. Summary statistics for short- and long-term bank borrowing for Singapore ®rms during the period 1983

to 1991

Variable

Number of

Observations Mean Median

Standard

Deviation

Interquartile

Range

Amount of short-term

bank borrowing

Singapore thousands 128 29,944 12,556 58,183 28,218

US thousands 14,781 6,198 28,720 13,929

Amount of long-term

bank borrowing

Singapore thousands 128 24,610 1,519 77,653 14,669

US thousands 12,148 750 38,330 7,241

Total amount of bank

borrowing

Singapore thousands 128 54,554 19,237 127,941 47,841

US thousands 26,928 9,496 3,153 23,615

Percentage of total bank

borrowing that is

short-term 128 80% 88% 22% 33%

Notes: The amounts of short- and long-term bank borrowing for a ®rm are respectively the average book

values of short-term bank borrowing under current liabilities and long-term bank borrowing under long-term

liabilities as disclosed in the ®nancial statements of the ®rm over the 1983 through 1991 time period. The

total amount of bank borrowing is the sum of average book values of short- and long-term bank borrowing.

The percentage of total bank borrowing that is short-term for a ®rm is measured by the mean ratio of the

amount of short-term bank borrowing to the total amount of bank borrowing over the same time period.

344 CHEN, HO AND YEO

over the years 1983 through 1991. The amounts of long-term bank borrowing are the

average book values of long-term bank borrowing (i.e. bank borrowing due in more than

one year) as classi®ed under long-term liabilities in the ®nancial statements over the same

period. The total amount of bank borrowing is the sum of the average book values of short-

and long-term bank borrowing. The percentage of total bank borrowing that is short-term

for a ®rm is the mean ratio of the amount of short-term bank borrowing to the total amount

of bank borrowing over the same time period. The mean (median) percentage of total bank

borrowing that is short-term is 80% (88%). The relatively high average percentage of bank

borrowing that is short-term is consistent with the observation in Fama (1985) that on

average bank borrowing is of shorter term maturity. However, there is also considerable

cross-sectional variation in the maturity of bank borrowing in our sample. The standard

deviation is 22% while the interquartile range is 33%.

Data on explanatory variables are collected from ®nancial statements of the sample

®rms and the Stock Exchange of Singapore. Market-to-book ratio is measured as the mean

ratio of the market value of the ®rm's assets to the book value of its assets, where the

market value of assets is estimated as the book value of assets minus the book value of

common equity plus the market value of common equity (as in Barclay and Smith

(1995a)). Firm size is measured as the mean natural logarithm of the estimated market

value of the ®rm.7 Abnormal future earnings is measured as the mean level of annual

abnormal earnings where abnormal earnings in year t� 1 is de®ned as earnings per share

in year t� 1 (excluding extraordinary items and adjusted for any change in shares

outstanding) minus earnings per share in year t, scaled by share price in year t. Term

structure is measured as the difference between the 5-year Singapore government bond

yield and the 3-month Singapore government bond yield at the ®rms' ®scal year-end. Data

on government bond yields are obtained from the Monthly Statistical Bulletin of the

Monetary Authority of Singapore and the Singapore Stock Exchange Journal.8

4. Empirical results

4.1. Cross-sectional regressions

Results of our base-case cross-sectional OLS regressions are reported in Table 2.9 Models

(1) to (4) are univariate regressions involving each of the four variables: market-to-book

ratio, log of ®rm value, abnormal earnings and term structure. Model (5) combines all four

variables in one regression.10 The t-values are computed with heteroskedasticity-consistent

standard errors if tests reject homoskedasticity at the 10% signi®cance level (White

(1980)). The number of observations varies across regressions because of data availability.

Consistent with the contracting-cost hypothesis, the coef®cient on the market-to-book

variable is positive and signi®cant at the 5% level using a one-tailed test. This evidence

suggests that ®rms with higher market-to-book ratio (i.e. ®rms with more growth options)

use more short-term bank borrowing.

The coef®cient on the log of ®rm value is negative and signi®cant at the 1% level using

a one-tailed test, suggesting that larger ®rms tend to use longer-term bank borrowing. This

evidence is consistent with the contracting-cost hypothesis.

THE DETERMINANTS OF DEBT MATURITY 345

The results on the abnormal earnings provide little support for the hypothesis that ®rms

use the maturity of bank borrowing to signal their ®rm quality. The term structure variable

is also not signi®cant, suggesting that taxes may have no material effect on the maturity of

bank borrowing in our sample.11

Model (6) in Table 2 includes industry dummies in the base-case regression. The

industry dummies (excluding the properties industry) are based on the industry

classi®cation by the Singapore Stock Exchange. The F-statistic for the joint signi®cance

of the industry dummies is insigni®cant at the 5% level. Results on other regression

Table 2. Cross-sectional regressions of the percentage of total bank borrowing that is short-term for Singapore

®rms from 1983 to 1991

Independent PredictedModel Speci®cation

Variable Sign (1) (2) (3) (4) (5) (6)

Intercept 0.725 1.463 0.798 0.777 1.358 1.189

(17.81)a (9.05)a (33.85)a (9.67)a (5.00)a (4.15)a

Market-to-book ratio � 0.054 0.057 0.049

(2.24)b (2.32)b (1.99)b

Log of ®rm value ÿ ÿ 0.055 ÿ 0.060 ÿ 0.052

(ÿ 4.02)a (ÿ 3.39)a (ÿ 2.86)a

Abnormal earnings � ÿ 0.257 0.192 0.033

(ÿ 0.39) (0.30) (0.05)

Term structure ÿ 1.106 3.640 3.124

(0.33) (0.64) (0.55)

F-Statistic for

industry dummies

[1.85]

Adjusted R2 0.04 0.08 ÿ 0.01 ÿ 0.01 0.12 0.13

F-Statistic 6.186 12.204 0.149 0.073 4.431 3.620

P-Value 0.014 0.001 0.700 0.787 0.002 0.003

Number of observations 123 124 106 128 105 105

a,b represent 1% and 5% signi®cance levels using a one-tailed test, respectively.

Notes: The dependent variable is the percentage of total bank borrowing that is short-term for a ®rm,

measured by the mean ratio of the amount of short-term bank borrowing to the total amount of bank

borrowing from 1983 to 1991. The market-to-book ratio is the mean ratio of the market value of the ®rm's

assets to their book value, where the market value of assets is estimated as the book value of assets minus

the book value of common equity plus the market value of common equity. Log of ®rm value is the mean

natural logarithm of the estimated market value of the ®rm (in Singapore thousands). Abnormal earnings is

the mean level of annual abnormal earnings, where abnormal earnings in year t� 1 is de®ned as earnings

per share in year t� 1 (excluding extraordinary items and adjusted for any changes in shares outstanding)

minus earnings per share in year t, divided by the share price in year t. The term structure of interest rates is

the mean difference between the ®ve-year Singapore government bond yield and the 3-month Singapore

government bond yield at the ®rms' ®scal year-end. The industry dummy variables (excluding the properties

industry) are based on the industry classi®cation by Singapore Stock Exchange. The t-values in parentheses

are computed with heteroskedasticity-consistent standard errors if tests reject homoskedasticity at the 10%

signi®cance level (White (1980)). The F-statistic for the industry dummies (in brackets) test whether the

industry dummies are jointly different from zero. The number of observations varies across regressions

because of data availability.

346 CHEN, HO AND YEO

coef®cients are qualitatively unchanged. Thus, ®rm-speci®c characteristics (such as size

and market-to-book ratio) are more important than industry-speci®c effects.

4.2. Additional tests

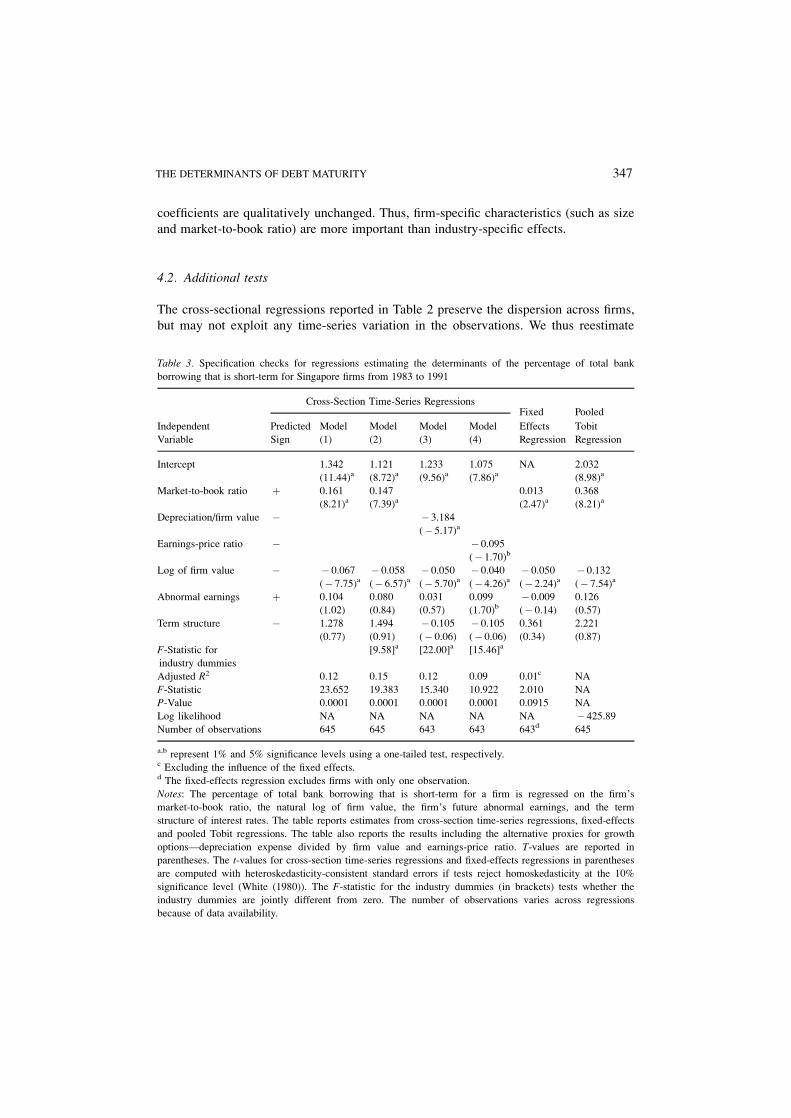

The cross-sectional regressions reported in Table 2 preserve the dispersion across ®rms,

but may not exploit any time-series variation in the observations. We thus reestimate

Table 3. Speci®cation checks for regressions estimating the determinants of the percentage of total bank

borrowing that is short-term for Singapore ®rms from 1983 to 1991

Cross-Section Time-Series RegressionsFixed Pooled

Independent Predicted Model Model Model Model Effects Tobit

Variable Sign (1) (2) (3) (4) Regression Regression

Intercept 1.342 1.121 1.233 1.075 NA 2.032

(11.44)a (8.72)a (9.56)a (7.86)a (8.98)a

Market-to-book ratio � 0.161 0.147 0.013 0.368

(8.21)a (7.39)a (2.47)a (8.21)a

Depreciation/®rm value ÿ ÿ 3.184

(ÿ 5.17)a

Earnings-price ratio ÿ ÿ 0.095

(ÿ 1.70)b

Log of ®rm value ÿ ÿ 0.067 ÿ 0.058 ÿ 0.050 ÿ 0.040 ÿ 0.050 ÿ 0.132

(ÿ 7.75)a (ÿ 6.57)a (ÿ 5.70)a (ÿ 4.26)a (ÿ 2.24)a (ÿ 7.54)a

Abnormal earnings � 0.104 0.080 0.031 0.099 ÿ 0.009 0.126

(1.02) (0.84) (0.57) (1.70)b (ÿ 0.14) (0.57)

Term structure ÿ 1.278 1.494 ÿ 0.105 ÿ 0.105 0.361 2.221

(0.77) (0.91) (ÿ 0.06) (ÿ 0.06) (0.34) (0.87)

F-Statistic for

industry dummies

[9.58]a [22.00]a [15.46]a

Adjusted R2 0.12 0.15 0.12 0.09 0.01c NA

F-Statistic 23.652 19.383 15.340 10.922 2.010 NA

P-Value 0.0001 0.0001 0.0001 0.0001 0.0915 NA

Log likelihood NA NA NA NA NA ÿ 425.89

Number of observations 645 645 643 643 643d 645

a,b represent 1% and 5% signi®cance levels using a one-tailed test, respectively.c Excluding the in¯uence of the ®xed effects.d The ®xed-effects regression excludes ®rms with only one observation.

Notes: The percentage of total bank borrowing that is short-term for a ®rm is regressed on the ®rm's

market-to-book ratio, the natural log of ®rm value, the ®rm's future abnormal earnings, and the term

structure of interest rates. The table reports estimates from cross-section time-series regressions, ®xed-effects

and pooled Tobit regressions. The table also reports the results including the alternative proxies for growth

optionsÐdepreciation expense divided by ®rm value and earnings-price ratio. T-values are reported in

parentheses. The t-values for cross-section time-series regressions and ®xed-effects regressions in parentheses

are computed with heteroskedasticity-consistent standard errors if tests reject homoskedasticity at the 10%

signi®cance level (White (1980)). The F-statistic for the industry dummies (in brackets) tests whether the

industry dummies are jointly different from zero. The number of observations varies across regressions

because of data availability.

THE DETERMINANTS OF DEBT MATURITY 347

Models (5) and (6) in Table 2 using cross-section time-series regressions, in which ®rm-

year observations for each variable are used. The results are reported in Models (1) and (2)

in Table 3. Generally, the results are similar to those reported earlier.12 The evidence again

supports the contracting-cost hypothesis but does not support the tax and signaling

hypotheses.

Although the F-statistic for industry dummies in Model (2) in Table 3 indicates that they

are jointly different from zero, the adjusted R2 increases marginally. Hence, industry-

speci®c effects are not as important as ®rm-speci®c characteristics.

We also reestimate Model (1) using (1) ®xed-effects regressions where the ®rm-speci®c

time-series mean for each variable is subtracted from each observation, and ®rms with

only one observation are excluded; and (2) appropriate censored (Tobit) estimator. As

shown in Table 3, there is no basic change in the results when these techniques are used.

To check the robustness of our results to alternative proxies for growth options, we

reestimate Model (2) in Table 3 by using depreciation as a percentage of ®rm value and

earnings-price ratio, and the results are reported in Models (3) and (4) respectively in the

same table. The coef®cients on the depreciation as a percentage of ®rm value and

earnings-price ratio are signi®cant at the 1% and 5% level respectively using a one-tailed

test, and their signs are as predicted by the contracting-cost hypothesis. With the exception

in Model (4) that the abnormal earnings variable becomes signi®cantly positive when

earnings-price ratio is used, all other coef®cients are qualitatively similar. The exception

noted in Model (4) suggests potential multicollinearity between abnormal earnings and

earnings-price ratio.13,14

5. Conclusions

This paper provides important international evidence by examining the determinants of

debt maturity of listed ®rms in Singapore, a major ®nancial center in Asia. Since

Singapore ®rms use mainly bank ®nancing, this study focuses on the maturity structure of

bank debt. We ®nd that consistent with the contracting-cost hypothesis, ®rms with higher

growth options in their investment opportunity sets use more short-term bank borrowing

whereas large ®rms tend to use more long-term bank borrowing. We do not ®nd strong

support for tax and signaling hypotheses in our sample ®rms.

Acknowledgments

The authors wish to thank Cheng-few Lee (the Editor), Karlyn Mitchell, two anonymous

referees, and seminar participants at the 1996 FMA meetings for helpful comments and

suggestions. All remaining errors are ours.

Notes

1. COMPUSTAT does not provide details on the maturity structure of bank debt.

2. Barclay and Smith (1995a) use the percentage of the ®rm's total debt that has a maturity of more than three

years as a measure of the maturity structure of a ®rm's debt. Their results are similar using the percentage of

348 CHEN, HO AND YEO

debt maturing in more than one, two, four, or ®ve years. Stohs and Mauer (1996) measure the debt maturity of

the entire liability structure of the ®rm. Due to data limitation, we cannot explore alternative measures of debt

maturity.

3. In Singapore, accounting practices follow closely those recommended by the International Accounting

Standards Committee. For example, intangibles such as internally-generated goodwill and brands are

generally not capitalized as assets.

4. Interest expense is also deductible in Singapore as an expense for the computation of corporate tax liability.

5. Boyce and Kalotay's (1979) tax model also shows that an upward sloping term structure of interest rates

implies that long-term debt is optimal. However, Lewis (1990) argues that taxes have no effect on optimal

debt maturity if optimal leverage and debt maturity structure are determined simultaneously. Further, Brick

and Ravid (1991) demonstrate that in the presence of stochastic interest rates, even if the term structure of

interest rates is decreasing, long-term debt may still be optimal.

6. The number of Singapore listed ®rms at the end of 1991 is the highest in the sample period. Of the full

sample, 11 ®rms have issued public debt during the sample period. Our results are similar when the 11 ®rms

are excluded from our analysis.

7. Sales and number of employees are possible alternative measures of size. However, sales may be in¯uenced

by different accounting policies on revenue recognition by sample ®rms, especially between ®rms in different

industries. For example, sales (or revenue) of property ®rms depend very much on whether the percentage-of-

completion method or the completed contract method is used. Number of employees is not publicly available

for most listed ®rms as there is no compulsory disclosure of such information.

8. The longest term government bond yield published in the of®cial Monthly Statistical Bulletin of the Monetary

Authority of Singapore is the ®ve-year yield. Data from this source is only available from May 1987 when the

Singapore government securities market was restructured to model after the United States Treasury bond

market. Prior to May 1987, the month-end yields for government securities are published in the SingaporeStock Exchange Journal. As there is no exact ®ve-year yield in this data source, we adopt a simple linear

interpolation using the yields of the two bonds with maturity just before and after ®ve years.

9. To prevent extreme observations from having an undue in¯uence on the regression results, we eliminate

outliers that fall beyond 5 standard deviations from the mean of each variable used in the regressions. We also

reestimate these regressions using the appropriate censored (Tobit) estimator. The results are similar.

10. Log of ®rm value may interact with market-to-book ratio in this model. However, results are similar whether

these variables are tested jointly or separately.

11. The lack of support for the tax hypothesis may be due to the fact that the dependent variable measures the

®rm's average bank debt maturity for the entire sample period and thus may not capture any change in the

debt maturity structure of the ®rm if there is a sudden yield curve shift. Hence, in Section 4.2 we re-estimate

our models by cross-section time series regressions.

12. The differences in coef®cients and R2s between Tables 2 and 3 may suggest that some nonstationarities or

multilinearities are submerged in averaging.

13. Using a regulation dummy variable which equals to 1 for regulated ®rms and 0 otherwise, we have also tested

the hypothesis that ®rms in regulated industries use longer-term bank borrowing than unergulated ®rms

(Smith (1986)). Though not reported, our results are consistent with the hypothesis. However, we are careful

in drawing any conclusion as there are only 5 ®rms in industries considered as regulated (transportation,

publishing and printing).

14. Though results are not reported, Diamond's (1991, 1993) liquidity hypothesis is also tested using a quadratic

form for the credit risk proxy. As comprehensive credit rating information is not available in Singapore, we

use three alternative proxies: (i) (mean interest expenses minus mean earnings before interests and tax)

divided by standard deviation of earnings (Marsh (1982)); (ii) standard deviation of the percentage change in

operating income (Titman and Wessels (1988)); and (iii) the ®rm's stock return standard deviation times its

equity-to-value ratio (Barclay and Smith (1995a)). We ®nd little support for the hypothesis, possibly because

of the inadequacy of our proxy variables.

THE DETERMINANTS OF DEBT MATURITY 349

References

Barclay, M.J. and C.W. Smith, Jr., ``The Maturity Structure of Corporate Debt.'' Working paper, University of

Rochester, (1993).

Barclay, M.J. and C.W. Smith, Jr., ``The Maturity Structure of Corporate Debt.'' Journal of Finance 50, 609±631,

(1995a).

Barclay, M.J. and C.W. Smith, Jr., ``The Priority Structure of Corporate Debt.'' Journal of Finance 50, 899±917,

(1995b).

Barnea, A., R.A. Haugen, and L.W. Senbet, ``A Rationale for Debt Maturity Structure and Call Provisions in the

Agency Theoretic Framework.'' Journal of Finance 35, 1223±1234, (1980).

Boyce, W.M. and A.J. Kalotay, ``Tax Differentials and Callable Bonds.'' Journal of Finance 34, 825±838, (1979).

Brick, I.E. and S.A. Ravid, ``On the Relevance of Debt Maturity Structure.'' Journal of Finance 40, 1423±1437,

(1985).

Brick, I.E. and S.A. Ravid, ``Interest Rate Uncertainly and the Optimal Debt Maturity Structure.'' Journal ofFinancial and Quantitative Analysis 26, 63±81, (1991).

Denis, D.J., ``Investment Opportunities and the Market Reaction to Equity Offerings.'' Journal of Financial andQuantitative Analysis 29, 159±177, (1994).

Diamond, D.W., ``Debt Maturity Structure and Liquidity Risk.'' Quarterly Journal of Economics 106, 709±737,

(1991).

Diamond, D.W., ``Seniority and Maturity of Debt Contracts.'' Journal of Financial Economics 33, 341±368,

(1993).

Fama, E.F., ``What's Different about Banks?'' Journal of Monetary Economics 15, 29±36, (1985).

Flannery, M.J., ``Asymmetric Information and Risky Debt Maturity Choice.'' Journal of Finance 41, 19±37,

(1986).

Guedes, J. and T. Opler, ``The Determinants of the Maturity of New Corporate Debt Issues.'' Journal of Finance51, 1809±1834, (1996).

Hart, O. and J. Moore, ``Default and Renegotiation: A Dynamic Model of Debt.'' Working paper, MIT, (1990).

James, C., ``Some Evidence on the Uniqueness of Bank Loans.'' Journal of Financial Economics 19, 217±235,

(1987).

Jensen, M.C. and W. H. Meckling, ``Theory of the Firm: Managerial Behavior, Agency Costs and Ownership

Structure.'' Journal of Financial Economics 3, 305±360, (1976).

Kale, J.R. and T. H. Noe, ``Risky Debt Maturity Choice in a Sequential Equilibrium.'' Journal of FinancialResearch 13, 155±165, (1990).

Lewis, C.M., ``A Multiperiod Theory of Corporate Financial Policy under Taxation.'' Journal of Financial andQuantitative Analysis 25, 25±43, (1990).

Marsh, P., ``The Choice between Equity and Debt: An Empirical Study.'' Journal of Finance 37, 121±144,

(1982).

Myers, S.C., ``Determinants of Corporate Borrowing.'' Journal of Financial Economics 5, 147±175, (1977).

Reed, E.W. and E. K. Gill, Commercial Banking, Englewood Cliffs, New Jersey: Prentice Hall, 1989.

Smith, C.W., ``Investment Banking and the Capital Acquisition Process.'' Journal of Financial Economics 15, 3±

29, (1986).

Stohs, M. H. and D. C. Mauer, ``The Determinants of Corporate Debt Maturity Structure.'' Journal of Business69, 279±312, (1996).

Stulz, R.M., ``Managerial Discretion and Optimal Financing Policies.'' Journal of Financial Economics 26, 3±28,

(1990).

Titman, S. and R. Wessels, ``The Determinants of Capital Structure Choice.'' Journal of Finance 43, 1±20,

(1988).

White, H., ``A Heteroskedasticity-Consistent Covariance Matrix Estimator and a Direct Test for

Heteroskedasticity.'' Econometrica 48, 817±838, (1980).

350 CHEN, HO AND YEO

![Government Debt Maturity Structure, Fiscal Policy, and Default · Government Debt Maturity Structure, Fiscal Policy, and Default∗ SergiiKiiashko† November22,2017 [Linktolatestdraft]](https://img.dokumen.tips/doc/110x75/6050d317a7955115112203b2/government-debt-maturity-structure-fiscal-policy-and-default-government-debt-maturity.jpg)