Embed Size (px)

Citation preview

Gcoforum, Vol. 19,1'0. I, pr. 3-28,1988Printed in Great Britain

lX)I6-7185/8853.00+0.ooPergamon Press pic

The Debt Crisis and Development: aComparison of Major Economic Theories

CHRIS EDWARDS,* Norwich, U.K.

Abstract: This article sets out to look at the different economic views about theissues surrounding the debt crisis. Section 2 defines the debt crisis and outlines thegrowth, nature and size of less developed country debt. Section 3 explains theinternational financial context within which the debt crisis developed. Section 4 looksat the crisis of the 1980s, compares it with that of the 1930s, and examines thelikelihood and consequences of widespread default on debt. Sections 5 and 6 look atthe differing views on where the blame for the crisis lies and what arc the appropiatesolutions or outcomes.

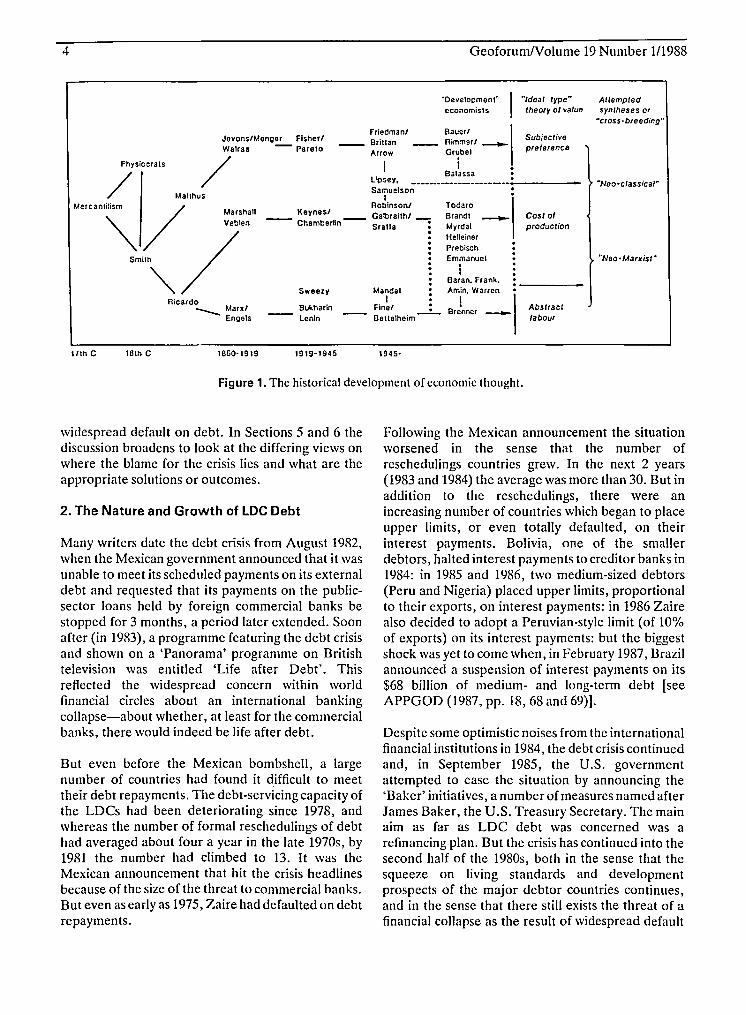

1. Introduction Some of the major economists through whom thesefive perspectives have evolved are listed in Figure 1.

This article is about the debt crisis and some of thedifferences among economists about the issuessurrounding the debt crisis and development. Thescope of the article is deliberately broad in an attemptto provide a framework within which a large numberof books, articles and proposals about the debt crisiscan be put into perspective.

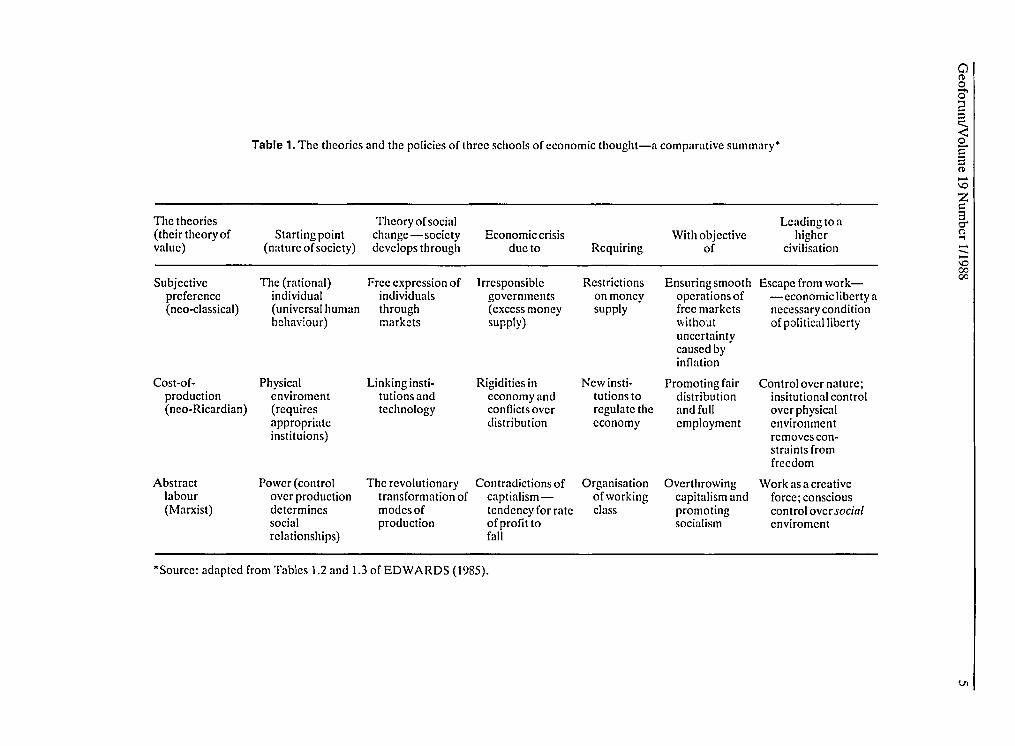

The basic assumption of this article is that it is helpfulto look at economic theories in terms of differentschools of thought. In a book published with twocolleagues in 1983 (COLE et al., 1983) and in a morerecent book on international trade and money(EDWARDS, 1985), it is argued that three distinctbut internally consistent 'theories of value' have beenestablished within economics in this century. Thesethree theories are 'ideal' or pure types and it is notclaimed that every economist fits neatly into one ofthese pigeon holes. For one thing economists havebeen known to be inconsistent-for another therehave been attempts at some cross-breeding betweenthese three groups. The two most important crossbreeds are those of neo-classicism and neo-Marxism.

"School of Development Studies,University of EastAnglin, Norwich NR4 7TJ, U.K.

3

This is not an appropriate place to analyse theemergence of these perspectives nor is there the spaceto explain in detail the different characteristics ofthese schools of thought. Again the interested readeris referred to COLE et al. (1983) and EDWARDS(1985). But Table 1, which attempts to summarisesome of the major characteristics of the three theoriesof value, may be a useful guide.

This article sets out to look at the differing economicviews about the issues surrounding the debt crisis.The view taken is a deliberately broad one embracingviews about the development process. But since thedebt crisis is the pivot for the article, it is appropriateto begin by defining the debt crisis, and in outliningthe growth, nature and size ofless developed country(LDC) debt. This is done in Section 2. The thirdsection then explains the international financialcontext within which the debt crisis developed - thesharp rises in the oil price in the mid-1970s and early1980s, the 1970s growth of international lendingthrough the eurocurrency markets and the recessionof the early 19805,culminating in the debt crisis from1982 onwards. Section 4 then looks at the crisis of the1980s, compares it with that of the 19305 andexamines the likelihood and consequences of

4 GeoforumNolume 19 Number 1/1988

·Dcvclop.menf Ieconomists

"Idee! Iype"Iheory 0/ value

Altempledsynlheses or

·cross·breeding"

"Neo'Marx;SI"

"Nee·c/assical-

Abslracllabour

Cosiolproduclion

Subjecl;vepre/erence

TodaroBrandl __

MyrdalHelleiner .PrebischEmmanuel •

i :Baran. Frank. • _Amin. Warren •

IBrenner ~

BauerlRimmerl _

Grubel.I

Balassa

MandelI

FinelBellelheim

Friedmanl__ Brlttan

Arrow

Bukllarinlenin

Sweezy

lipsey. •• ~---_

SamuelsonI

RobinsonlKeynesl Galbraithl

-- Chamberlin-- Srafla --:

···············

Jevons/Menger FlsherlWalras - Pareto

/Physiocrats

/ Mallhus.,,""'\/ ~;;:::",m;,\/Ricarde__ Marxl

Engels

I1lh C 18th C 1860-1919 1919-'945 1945·

Figure 1. The historicaldevelopment of economic thought.

widespread default on debt. In Sections 5 and 6 thediscussion broadens to look at the differing views onwhere the blame for the crisis lies and what are theappropriate solutions or outcomes.

2. The Nature and Growth of LDC Debt

Many writers date the debt crisis from August 1982,when the Mexican government announced that it wasunable to meet its scheduled payments on its externaldebt and requested that its payments on the publicsector loans held by foreign commercial banks bestopped for 3 months, a period later extended. Soonafter (in 1983), a programme featuring the debt crisisand shown on a 'Panorama' programme on Britishtelevision was entitled 'Life after Debt'. Thisreflected the widespread concern within worldfinancial circles about an international bankingcollapse-about whether, at least for the commercialbanks, there would indeed be life after debt.

But even before the Mexican bombshell, a largenumber of countries had found it difficult to meettheir debt repayments. The debt-servicing capacity ofthe LDCs had been deteriorating since 1978, andwhereas the number of formal reschedulings of debthad averaged about four a year in the late 1970s, by1981 the number had climbed to 13. It was theMexican announcement that hit the crisis headlinesbecause of the size of the threat to commercial banks.But even as early as 1975, Zaire had defaulted on debtrepayments.

Following the Mexican announcement the situationworsened in the sense that the number ofreschedulings countries grew. In the next 2 years(1983 and 1984) the average was more than 30. But inaddition to the reschedulings, there were anincreasing number of countries which began to placeupper limits, or even totally defaulted, on theirinterest payments. Bolivia, one of the smallerdebtors, halted interest payments to creditor banks in1984: in 1985 and 1986, two medium-sized debtors(Peru and Nigeria) placed upper limits, proportionalto their exports, on interest payments: in 1986 Zairealso decided to adopt a Peruvian-style limit (of 10%of exports) on its interest payments: but the biggestshock was yet to come when, in February 1987, Brazilannounced a suspension of interest payments on its$68 billion of medium- and long-term debt [seeAPPGOD (1987, pp. 18,68 and 69)].

Despite some optimistic noises from the internationalfinancial institutions in 1984, the debt crisis continuedand, in September 1985, the U.S. governmentattempted to ease the situation by announcing the'Baker' initiatives, a number of measures named afterJames Baker, the U.S. Treasury Secretary. The mainaim as far as LDC debt was concerned was arefinancing plan. But the crisis has continued into thesecond half of the 1980s, both in the sense that thesqueeze on living standards and developmentprospects of the major debtor countries continues,and in the sense that there still exists the threat of afinancial collapse as the result of widespread default

Table 1. The theories and the policies of three schools of economic thought-a comparative summary"

The theories Theory of social Leading to a(their theory of Starting point change-society Economic crisis With objective highervalue) (nature of society) develops through dueto Requiring of civilisation

Subjective The (rational) Free expression of Irresponsible Restrictions Ensuring smooth Escape from work-preference individual individuals governments on money operations of - economic liberty a(nco-classical) (universal human through (excess money supply free markets necessary condition

behaviour) markets supply) without of political libertyuncertaintycaused byinflation

Cost-of- Physical Linking insti- Rigidities in New insti- Promoting fair Control over nature;production enviroment tutionsand economy and tutions to distribution insitutional control(nco-Ricardian) (requires technology conflicts over regulate the and full over physical

appropriate distribution economy employment environmentinstituions) removes con-

straints fromfreedom

Abstract Power (control The revolutionary Contradictions of Organisation Overthrowing Work as a creativelabour over production transformation of captialism- of working capitalism and force; conscious(Marxist) determines modes of tendency for rate class promoting control oversocial

social production of profit to socialism enviromentrelationships) fall

*Source: adapted from Tables 1.2 and 1.3 of EDWARDS (1985).

C)(b

o0'...,

~C:3(b

......\0

Zc:::3cr'(b...,......-.......\00000

VI

6

by those countries. At the same time, the risk of afinancial collapse has been kept in check to someextent as the major commercial banks have built uptheir 'bad-debt' provisions against LDC loans. Thusin May 1987, the world's largest commercial bank,the U.S.-based Citicorp, increased its bad debtreserves on its LDC loans by $3 bn to a total of $5 bn.Then in June and July 1987, three major British bankssubstantially increased their 'bad-debt' provisions.The NatWest Bank set aside an additional £446million to bring its provisions on loans to heavilyindebted countries up to about 30% of the total: theMidland Bank increased its provisions to more than£1 bn to bring the total to about a quarter of theirLDC loans: and this was soon followed by LIoydsBank bringing its provisions to a total of fl.3 bn orabout 30% of its LDC loans.

However, although the risk of a financial collapse hasbeen reduced by these provisions, it still remains.Additionally the world economy continues to be lopsided in its growth. In 1986, the U.S. economy wasrunning a deficit on its balance of payments currentaccount equivalent to about 3% of its nationalincome, compared to a previous high of 1.5% in the1870s. In the meantime, the debtor countries in LatinAmerica were facing a net capital outflow equivalentto about 4% of their national income or to about aquarter of their domestic savings. By contrast, themuch-maligned reparation payments of WestGermany following the First World War were (only)about 2.5% of national income.

Furthermore recent U.S. attempts to restore somesemblance of balance to the American economy havethreatened to reduce the growth of the worldeconomy. At the time of writing this article (mid1987), there are few signs that the two major worldsurplus countries (Japan and West Germany) wereexpanding fast enough to reduce this threatsignificantly. And there are few signs that the flow ofcapital FROM the major debtor countries the ThirdWorld will be reversed in the near future . The threatof collective default by these major debtors which hasexisted since 1984 remains. And if a collective defaultoccurred, then the spectre of a financial crisis wouldcertainly be resurrected.

I come back to some of these issues in later sections.But before doing so, it is important to set out the size,nature and growth of Third World debt, since thereare some differences between the statistical sourceswhich need to be clarified.

The three main reporting systems on the debt of the

GeoforumNolume 19 Number 1/1988

LDCs are those of the World Bank, the Bank forInternational Settlements (BIS) and the Organisationfor Economic Cooperation and Development(OECD). Broadly speaking, the World Bank is adebtor reporting system while the OECD and the BISreceive their information from creditors. They eachhave their limitations as sources and a manual of theBIS has pointed out that "there are no countries forwhich full information on the outstanding stock ofexternal indebtedness is available" [BIS quoted inSTRANGE (1986, p. 138»).

The World Bank's World Debt Tables give data oninternational debt dating back to the 1960s but itsseries includes only long-term debt and for manycountries only public and publicly-guaranteed debt ispresented [see NUNNENKAMP (1986, p. 27»).Long-term debt is defined as debt repayable overmore than a year. The exclusion of short-term debtfrom the World Bank's series is a serious limitationnot just because short-term debts generally accountfor at least 15% of total external LDC debt [seeKORNER et al. (1986, p. 8) and Table 3] but moreimportantly, because they vary considerably overtime and because many of them are publiclyguaranteed. In particular just before crises andreschedulings, external debt tends to be understatedand much of the unrecorded debt appears to be shortterm (GREEN and GRIFFITH-JONES, 1986, p.26) . A good example is given by Brazil. With its shortterm debt estimated to have risen from less than $5 bnin 1978 to as much as $17 bn in 1982, Brazil's foreigndebt increased at a faster pace than indicated by theWorld Bank's official debt statistics [see BATISTA,World Bank Discussion Paper No.7 (1987, pp. 36 and38)].

The LDC debt is also understated by the Basle-basedBIS, the central bankers' bank, but for differentreasons. While the BIS figures do include short-termdebt, they exclude debt owed to creditors other thanthe commercial banks. Thus the BIS figures, likethose of the World Bank, understate the total debt.

The third reporting system is that of the OECD. TheOECD's figures are not only more comprehensivethan those produced by the BIS and the World Bankbut they are in general more up-to-date. Unlike theWorld Bank's figures, they include debt owed byprivate organisations whether or not it is guaranteedby the government. And unlike the 81S, the OECDincludes debt owed to official creditors with theexception of the International Monetary Fund(IMF). However, unlike the BIS, the OECDexcludes short-term debt. The OECD series also

GeoforumlVolume 19 Number 1/1988

excludes military debt financed by official credits ,which is estimated to be equal to a littl e over 10% oftotal LDC long- and short-term extern al debt [seeKORNER et al. (1986, p. 5) and NUNNENKAMP(1986, p. 27)].

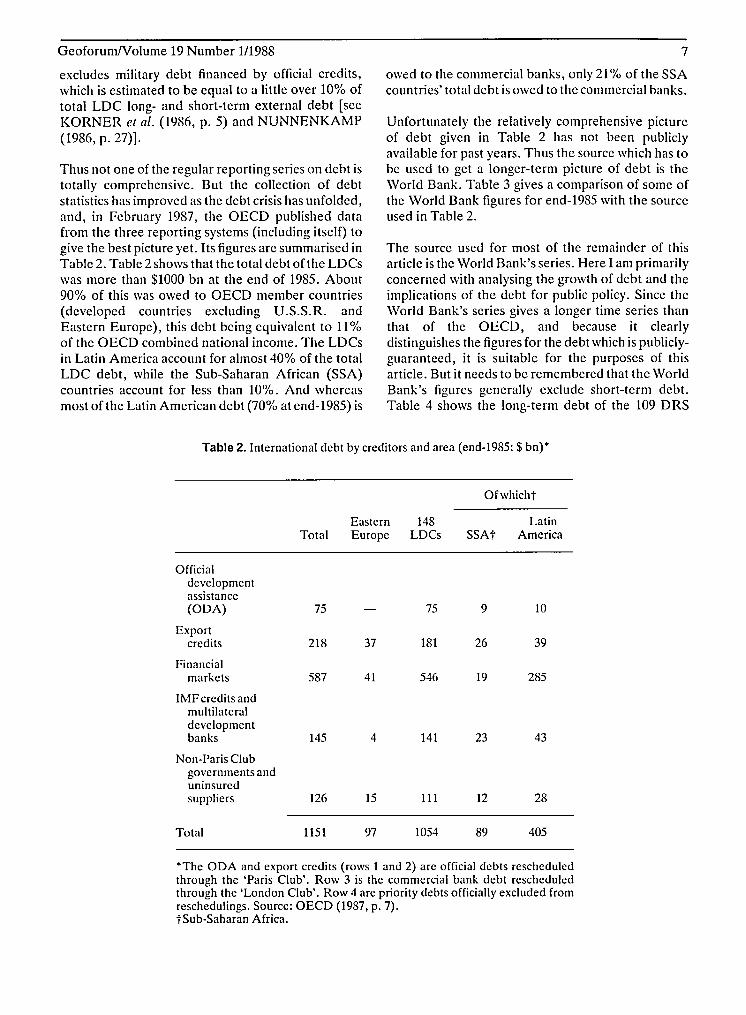

Thus not one of the regular reporting series on debt istotally comprehensive. But the collection of debtstatistics has improved as the debt crisis has unfolded ,and, in February 1987, the OECD published dat afrom the three reporting syste ms (including itself) togive the best picture ye t. Its figures arc summarised inTabl e 2. Table 2 shows that th e total debt of the LDCswas more than $1000 bn at the end of 1985. About90% of this was owed to OECD member countries(developed countries excluding U.S.S.R. andEastern Europe), this debt being equivalent to 11%of the OECD combined national income. The LDCsin Lat in America account for almo st 40% of the totalLDC debt , while the Sub -Saharan African (SSA)countries account for less th an 10%. And whereasmost of the Latin Am eric an debt (70% at end-1985) is

7

owed to the commercial banks , only 21% of the SSAcountries' total debt is owed to the commercial banks.

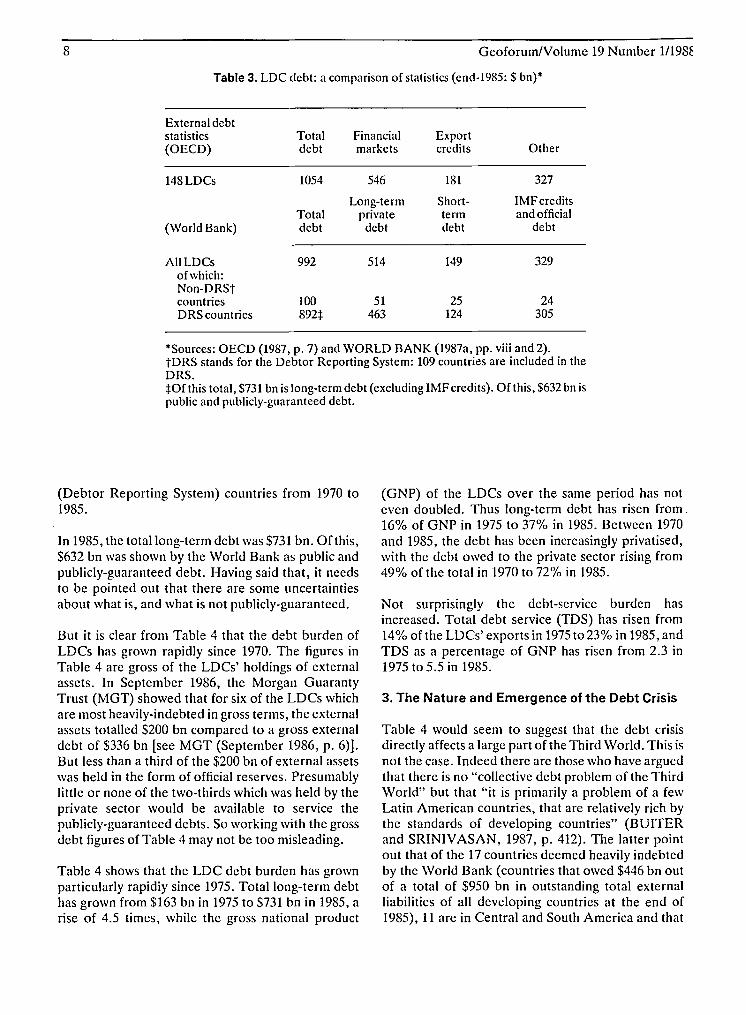

Unfortunatel y the relatively comprehensive pictureof debt given in Table 2 has not been publiclyavailable for past years. Thus the source which has tobe used to get a lon ger-term picture of debt is theWorld Bank . Table 3 gives a comparison of some ofthe World Bank figures for end-1985 with th e sourceused in Table 2.

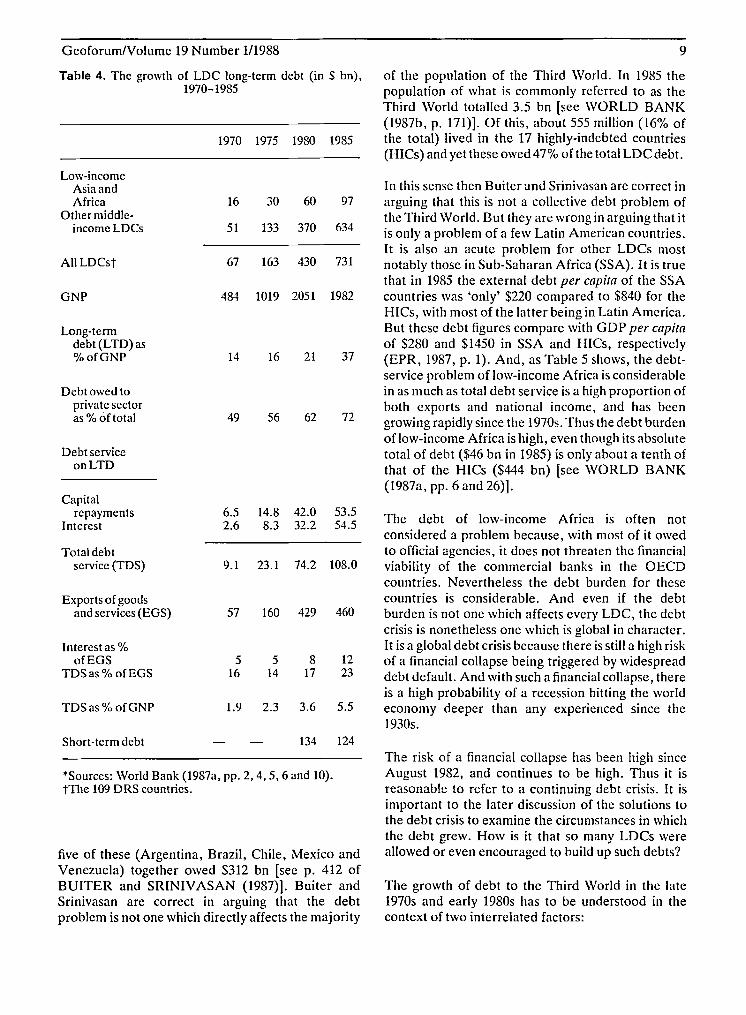

The source used for most of the rem aind er of thisarticle is the World Bank's se ries. Here I am primarilyconce rned with analysing th e gro wth of debt and th eimplications of the debt for publi c policy. Since theWorld Bank's series gives a longer time series thanthat of the OECD, and because it clearlydistinguishes the figures for the debt which is publiclyguaranteed , it is suitable for th e purposes of thisarticle . But it needs to be rem embered that the WorldBank 's figures generally exclude short-te rm debt.Table 4 shows the long-te rm de bt of the 109 DRS

Table 2. Intern ation al debt by cred itors and area (end-1985: S bn)*

Ofwhicht

Eastern 148 LatinTotal Euro pe LDCs SSAt Am erica

Officialdevelopmentassistance(ODA) 75 75 9 10

Exp ortcredits 218 37 181 26 39

Financi almarkets 587 41 546 19 285

IMF cred its andmultilateraldevelopmentbanks 145 4 141 23 43

Non-Paris Clubgovernments anduninsuredsuppliers 126 15 III 12 28

Total 1151 97 1054 89 405

"The ODA and export credits (rows 1 and 2) arc official debts reschedul edthrough the 'Paris Club' . Row 3 is the commercial bank debt rescheduledthrough the 'Londo n Club ' . Row 4 are priority debt s officially excluded fromreschedulings . Source: OECD (1987, p. 7).r Sub-Saharan Afri ca.

8 GeoforumNolume 19 Number 1I198~

Table 3. LDC debt: a comparison of statistics (end-1985: $ bn)*

External debtstatistics Total Financial Export(OECD) debt markets credits Other

148LDCs 1054 546 181 327

Long-term Short- IMFcreditsTotal private term and official

(World Bank) debt debt debt debt

AllLDCs 992 514 149 329of which:Non-DRStcountries 100 51 25 24DRS countries 892:j: 463 124 305

*Sources: OECD (1987, p. 7) and WORLD BANK (1987a, pp. viii and 2).tDRS stands for the Debtor Reporting System: 109 countries are included in theDRS.:j:Ofthis total, $731 bn is long-term debt (excluding IMF credits). Ofthis, $632bn ispublic and publicly-guaranteed debt.

(Debtor Reporting System) countries from 1970 to1985.

In 1985, the total long-term debt was $731 bn. Ofthis,$632 bn was shown by the World Bank as public andpublicly-guaranteed debt. Having said that, it needsto be pointed out that there are some uncertaintiesabout what is, and what is not publicly-guaranteed.

But it is clear from Table 4 that the debt burden ofLDCs has grown rapidly since 1970. The figures inTable 4 are gross of the LDCs' holdings of externalassets. In September 1986, the Morgan GuarantyTrust (MGT) showed that for six of the LDCs whichare most heavily-indebted in gross terms, the externalassets totalled $200 bn compared to a gross externaldebt of $336 bn [see MGT (September 1986, p. 6)].But less than a third of the $200 bn of external assetswas held in the form of official reserves. Presumablylittle or none of the two-thirds which was held by theprivate sector would be available to service thepublicly-guaranteed debts. So working with the grossdebt figures of Table 4 may not be too misleading.

Table 4 shows that the LDC debt burden has grownparticularly rapidiy since 1975. Total long-term debthas grown from $163 bn in 1975 to $731 bn in 1985, arise of 4.5 times, while the gross national product

(GNP) of the LDCs over the same period has noteven doubled. Thus long-term debt has risen from.16% of GNP in 1975 to 37% in 1985. Between 1970and 1985, the debt has been increasingly privatised,with the debt owed to the private sector rising from49% of the total in 1970 to 72% in 1985.

Not surprisingly the debt-service burden hasincreased. Total debt service (TDS) has risen from14% of the LDCs' exports in 1975t023% in 1985, andTDS as a percentage of GNP has risen from 2.3 in1975 to 5.5 in 1985.

3. The Nature and Emergence of the Debt Crisis

Table 4 would seem to suggest that the debt crisisdirectly affects a large part of the Third World. This isnot the case. Indeed there are those who have arguedthat there is no "collective debt problem of the ThirdWorld" but that "it is primarily a problem of a fewLatin American countries, that are relatively rich bythe standards of developing countries" (BUlTERand SRINIVASAN, 1987, p. 412). The latter pointout that of the 17 countries deemed heavily indebtedby the World Bank (countries that owed $446 bn outof a total of $950 bn in outstanding total externalliabilities of all developing countries at the end of1985), 11 are in Central and South America and that

GeoforumNolume 19 Number 1/1988 9

Table 4. The growth of LDC long-term debt (in $ bn), of the population of the Third World. In 1985 the1970-1985 population of what is commonly referred to as the

Third World totalled 3.5 bn [see WORLD BANK(1987b, p. 171)]. Of this, about 555 million (16% of

1970 1975 1980 1985 the total) lived in the 17 highly-indebted countries(HICs) and yet these owed 47% of the total LDC debt.

1.9 2.3 3.6 5.5

57 160 429 460

9.1 23.1 74.2 108.0

5 5 8 1216 14 17 23

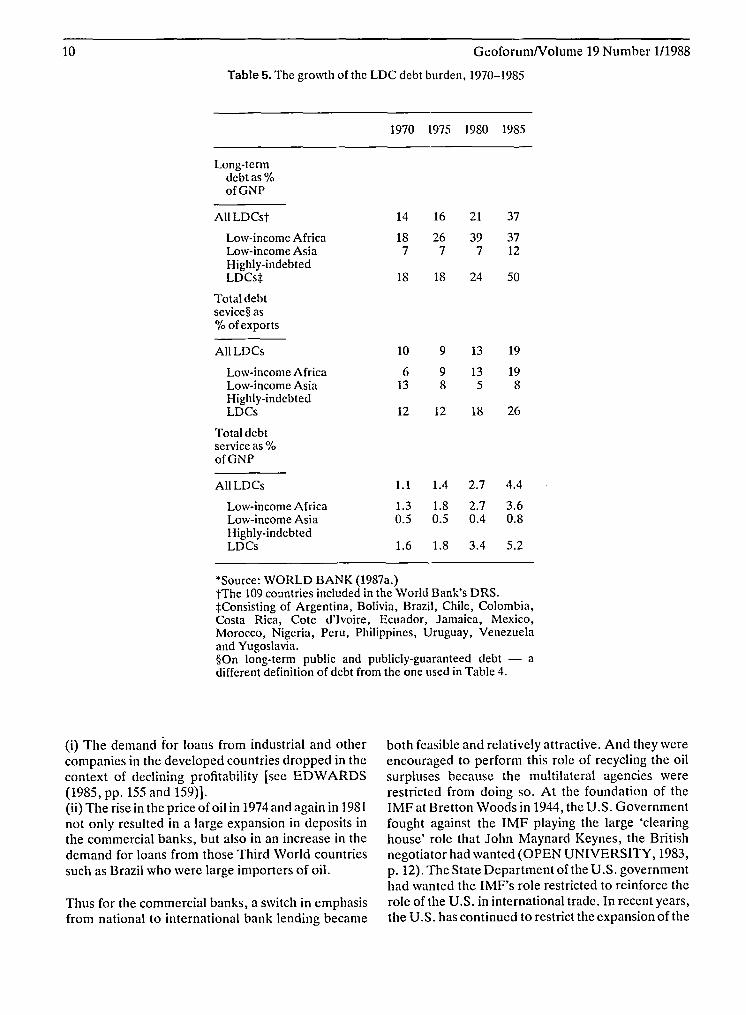

The debt of low-income Africa is often notconsidered a problem because, with most of it owedto official agencies, it does not threaten the financialviability of the commercial banks in the OECDcountries. Nevertheless the debt burden for thesecountries is considerable. And even if the debtburden is not one which affects every LDC, the debtcrisis is nonetheless one which is global in character.It is a global debt crisis because there is still a high riskof a financial collapse being triggered by widespreaddebt default. And with such a financial collapse, thereis a high probability of a recession hitting the worldeconomy deeper than any experienced since the1930s.

In this sense then Buiter and Srinivasan are correct inarguing that this is not a collective debt problem ofthe Third World. But they are wrong in arguing that itis only a problem of a few Latin American countries.It is also an acute problem for other LDCs mostnotably those in Sub-Saharan Africa (SSA). It is truethat in 1985 the external debt per capita of the SSAcountries was 'only' $220 compared to $840 for theHICs, with most of the latter being in Latin America.But these debt figures compare with GOP per capitaof $280 and $1450 in SSA and HICs, respectively(EPR, 1987, p. 1). And, as Table 5 shows, the debtservice problem of low-income Africa is considerablein as much as total debt service is a high proportion ofboth exports and national income, and has beengrowing rapidly since the 1970s. Thus the debt burdenof low-income Africa is high, even though its absolutetotal of debt ($46 bn in 1985) is only about a tenth ofthat of the HICs ($444 bn) [see WORLD BANK(1987a, pp. 6 and 26)].

72

37

97

634

731

1982

16 21

56 62

30 60

133 370

163 430

1019 2051

49

67

14

51

16

6.5 14.8 42.0 53.52.6 8.3 32.2 54.5

484

Exportsof goodsandservices(EGS)

Debtowedtoprivatesectoras%oftotal

TDS as % of GNP

Debt serviceon LTD

Interest as %ofEGS

TDSas % ofEGS

Capitalrepayments

Interest

Long-termdebt (LTD) as% of GNP

Total debtservice(TDS)

AllLDCst

GNP

Low-incomeAsiaandAfrica

Other middleincomeLDCs

Short-term debt 134 124

"Sources: WorldBank (1987a,pp. 2, 4, 5, 6 and 10).tThe 109DRS countries.

five of these (Argentina, Brazil, Chile, Mexico andVenezuela) together owed $312 bn [see p. 412 ofBUITER and SRINIVASAN (1987)]. Buiter andSrinivasan are correct in arguing that the debtproblem is not one which directly affects the majority

The risk of a financial collapse has been high sinceAugust 1982, and continues to be high. Thus it isreasonable to refer to a continuing debt crisis. It isimportant to the later discussion of the solutions tothe debt crisis to examine the circumstances in whichthe debt grew. How is it that so many LDCs wereallowed or even encouraged to build up such debts?

The growth of debt to the Third World in the late1970s and early 1980s has to be understood in thecontext of two interrelated factors:

10 GeoforumNolume 19 Number 1/1988

Table 5. The growth of the LDC debt burden, 1970-1985

1970 1975 1980 1985

Long-termdebt as %of GNP

AIILDCst

Low-income AfricaLow-income AsiaHighly-indebtedLDCst

Total debtsevice§ as% of exports

AIILDCs

Low-income AfricaLow-income AsiaHighly-indebtedLDCs

Total debtservice as %of GNP

14

187

18

10

613

12

16

267

18

9

98

12

21

397

24

13

135

18

37

3712

50

19

198

26

All LDCs

Low-income AfricaLow-income AsiaHighly-indebtedLDCs

1.1 1.4 2.7 4.4

1.3 1.8 2.7 3.60.5 0.5 0.4 0.8

1.6 1.8 3.4 5.2

"Source: WORLD BANK (1987a.)tThe 109 countries included in the World Bank's DRS.tConsisting of Argentina, Bolivia, Brazil, Chile, Colombia,Costa Rica, Cote d'Ivoire, Ecuador, Jamaica, Mexico,Morocco, Nigeria, Peru, Philippines , Uruguay, Venezuelaand Yugoslavia.§On long-term public and publicly-guaranteed debt - adifferent definition of debt from the one used in Table 4.

(i) The demand for loans from industrial and othercompanies in the developed countries dropped in thecontext of declining profitability [see EDWARDS(1985, pp. 155 and 159)].(ii) The rise in the price ofoil in 1974 and again in 1981not only resulted in a large expansion in deposits inthe commercial banks, but also in an increase in thedemand for loans from those Third World countriessuch as Brazil who were large importers of oil.

Thus for the commercial banks, a switch in emphasisfrom national to international bank lending became

both feasible and relatively attractive. And they wereencouraged to perform this role of recycling the oilsurpluses because the multilateral agencies wererestricted from doing so. At the foundation of theIMF at Bretton Woods in 1944, the U .S. Governmentfought against the IMF playing the large 'clearinghouse' role that John Maynard Keynes, the Britishnegotiator had wanted (OPEN UNIVERSITY, 1983,p. 12). The State Department of the U .S . governmenthad wanted the IMF's role restricted to reinforce therole of the U.S. in international trade. In recent years,the U .S. has continued to restrict the expansion of the

Eurocurrencies - claims on

11

Table 6. Growth of the eurocurrency market, 19641986 ($ bn)*

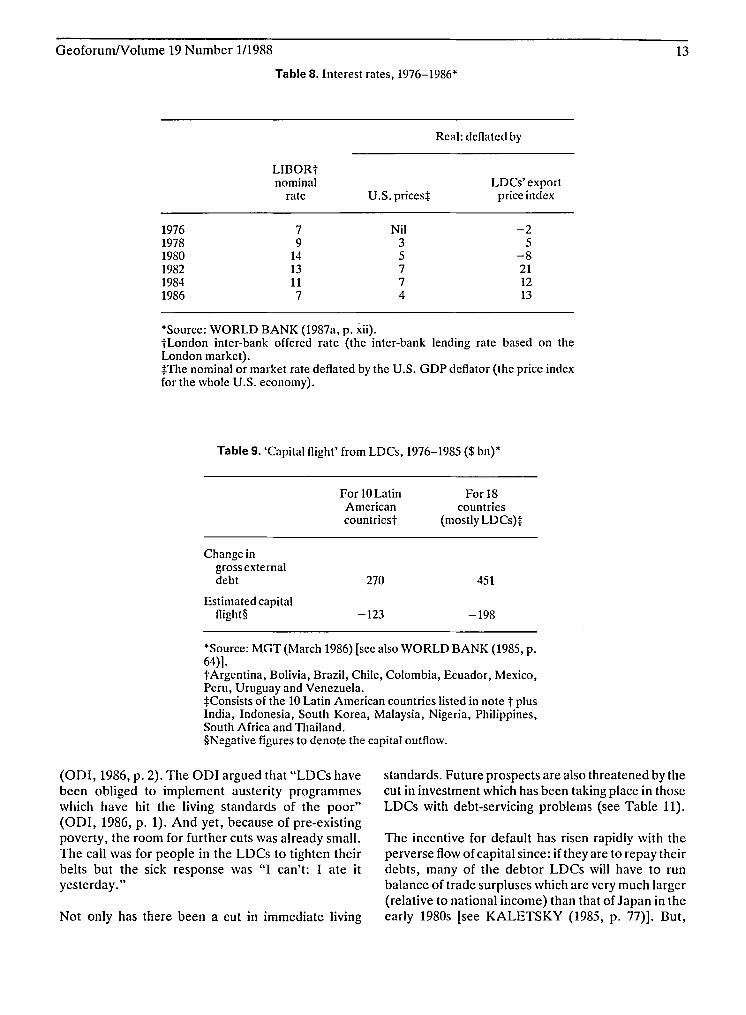

The trouble began as the world economy moved intoa recession from 1979. The Thatcher and Reagangovernments came to power in the U.S. and theU.K. , and identified the major economic problem asinflation. The cure for this illness was identified as aliberal dose of monetarism, and the result was a dropin output and a sharp rise in int erest rates. In 1982output actually fell in the Industrial MarketEconomies (see Table 7) , and interest rates roserapidly. They rose relative to the general level ofinflation in the developed countries, but the rise wasparticularly steep for the LDCs, as the rising nominalinterest rates coincided with a sharp fall in the pricesof LDCs' exports. Thus as Table 8 shows, from beinglow or even negative in 'real terms' (that is, relative tochanges in LDCs' export prices) in the late 1970s,interest rates rose rapidly in the first half of the 1980s.

13722433

Banks

17300557914

Non-banks

1964197619811986(September)

in international banking became more intense .Middle-income LDCs found that there was noshortage of banks wanting to lend to them without'political strings', while the banks were able to reducethe risk to themselves to some extent - firstly bychannelling loans through banking syndicates andsecondly by lending at variable interest rates [seeNUNNENKAMP (1986, p. 106)]. Thus, whereas in1970 only about a half of all loans to LDCs were fromprivate sources, by the mid-1980s this had risen totwo-thirds [see Table 4 and KORNER et al. (1986, p.6)]. International lending was becoming increasinglyprivatised. By the late 1970s, th e commercial bankswere congratulating themselves on the magnificentjob which they had managed of recycling the oilsurpluses. Less than a decade later, the recycling jobhad turned distinctly sour as the most heavilyindebted countries ran into trouble.

The significant aspect of the expansion ininternational bank lending which took place in the1970s was that much of it took place through theeurocurrency market - a sector of the bankingmarket which is conducted outside formal centralbanking regulation. Most eurocurrencies consist ofeurodollars - in March 1986 about three-quarters ofthe total. Eurodollars are deposits in a commercialbank denominated in dollars but held outside thejurisdiction of the Federal Reserve Bank (theAmerican central bank). Since the eurocurrencyoperations are outside the formal jurisdiction of thecentral banks, the commercial banks are not requiredto hold reserves with the central banks in respect ofthese operations. Such operations as a result wereinitially more profitable than 'nationally-based'banking. With other factors such as the cold war andinterest rate controls in the U.S. encouragingdepositors to hold their dollars outside the U.S., it isnot suprising that, through the 1970s, theeurocurrency market grew extremely rapidly (seeTable 6). Between 1964 and 1981, it grew 3 times asfast as world money supply. It grew as, through thelate 1970s and early 1980s, there was increasing'competition in fiscal laxity' . Governments competedin deregulation to prevent financial services movingto what would otherwise be less regulated centres.Thus the growth of the 'offshore ' London market ledto international banking facilities being established inNew York in 1981, and at the end of 1986 a similar'offshore' facility was scheduled to open in Japan.

GeoforumlVolume 19 Number 1/1988

IMF and in particular any increase In thesubscriptions of the surplus countries (Japan andWest Germany) , since these would reduce the votingpower of the U.S . within the IMF.

Thus a pattern emerged in the late 1970s ofcommercial banks expanding their internationallending to middle-income LDCs and of official loansgoing to the low-income LDCs. Much of the lendingby the commercial banks was initially highlyprofitable as it was done on the basis of smallreserves. In general, commercial banks hold aproportion of their assets in a highly liquid form tomeet the likely demands of depositors for cash andthus to maintain confidence. But this is not just amatter of conservatism. They arc also required by thecentral bank to hold a certain proportion of assets inhighly liquid forms earning little or no interest. Theyare required and willing to do so since the centralbank stands behind them ready to act as the lender oflast resort.

As the eurocurrency market grew, so the competition'Sources: EDWARDS (1985. p. 177) and MGT (April1987, p. 15).

12

The rising real interest rates hit the LDCs in threeways:

(i) Through the effects on repayments. Not only didhigher interest rates mean higher interest paymentson the debts, but the higher interest rates in the U.S.pushed up the dollar exchange rate and meant thatthe largely dollar-denominated debt became moreexpensive to service in terms of national currencies.(ii) Through the recessionary effect. Higherinterest rates had a deflationary effect on the worldeconomy which in turn meant smaller markets forexports from the LDCs.(iii) Through the capital-flight effect. Higher U.S.interest rates and a stronger dollar encouraged aflight of capital from the LDCs. Thus, as Table 9shows, between 1976 and 1985 capital flight from 18countries was equivalent to almost half the rise inexternal debt for those countries over the sameperiod. [However some sources point out that 'capitalflight' was not new to the late 1970s- it had occurredbefore -and that the estimating of 'capital flight' wasextremely crude (UN, 1986, p. 75). Some were alsosuspicious that capital flight was being well publicisedin the mid-1980s to excuse the drying-up ofcommercial bank loans at that time.]

As interest rates rose and non-oil commodity pricesfell, the most heavily-indebted and the SSA countriesmoved into a debt crisis in the early 1980s. Debtservice ratios rose and rescheduling of debt becameincreasingly common both for official debt (throughthe Paris Club) and for debts owed to the commercialbanks (through the bank advisory committees,

GeoforumNolume 19 Number 1/1988

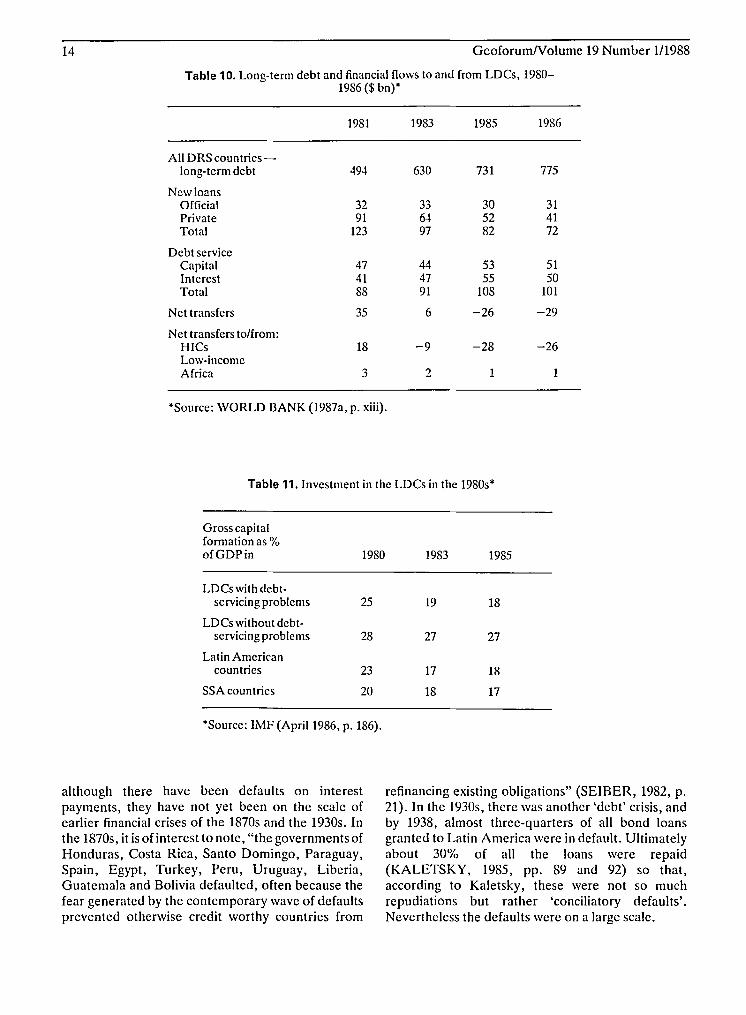

known as the London Club). The capital was rolledover and new syndicated loans were put togetherunder pressure from the IMF and the BIS to enableinterest commitments to be met. But gradually theflow of new loans dried up as the commercial banksran for cover. As each of the major commercial bankstried to protect their own interests, they destroyedthe collective interests of them all. In the 1970s therehad been a considerable flow of capital into the LDCsfrom private sources: from 1983 this changed to areverse transfer ofcapital FROM the LDCs, despite acontinuation of official capital flows into the LDCs(see Table 10). The commercial banks were runningfor cover, but this only led each of them into deepertrouble. The panic had started. The debt crisis hadbroken.

4. Debt, Default and Depression - a Repeat ofthe 1930s7

As the debt burden has risen and the flow of capital tothe LDCs has turned into a reverse (or perverse) flowfrom them to the creditor countries, their economieshave been hit. Living standards have been cutsharply. As Table 7 shows, national output fell in thehighly-indebted and SSA countries in 1982 and 1983,and in a number of Latin American countries averageper capitareal income fell by more than 10% between1980 and 1985 [see SACHS (1986, p. 410) and MGT(February 1986, p. 6)]. The Overseas DevelopmentInstitute (ODI) has argued that, because they havehad little time to restore external balance, LDCs havegenerally been obliged to overemphasise demandrestraint, mainly through fiscal and monetary control

Table 7. Growth rates in GOP, 1965-1986*

Of which

IMEst LOCs HICs SSA:j:

1965-1973 4.7 6.5 6.9 6.41973-1980 2.8 5.4 5.4 3.21982 -0.5 2.1 -0.5 -0.21983 2.2 2.1 -3.2 -1.51984 4.6 5.1 2.0 -1.71985 2.8 4.8 3.1 2.21986§ 2.5 4.2 2.5 0.5

GOPin 1980($bn) 7570 2116 890 187

*Source: WORLD BANK (1987b, p. 172). Average annual growth rate in grossdomestic product (GOP) (% per annum).tIndustrial market economies.:j:Sub-Saharan Africa.§Preliminary.

GeoforumNolume 19 Number 1/1988

Table 8. Interest rates, 1976-1986*

Real: deflated by

LIBORtnominal LDCs' export

rate U.S. pricesj price index

1976 7 Nil -21978 9 3 51980 14 5 -81982 13 7 211984 11 7 121986 7 4 13

*Source: WORLD BANK (1987a, p. xii).[London inter-bank offered rate (the inter-bank lending rate based on theLondon market).:!:The nominal or market rate deflated by the U.S. GDP deflator (the price indexfor the whole U.S. economy).

Table 9. 'Capital flight' from LDCs, 1976-1985 ($ bn)*

13

Change ingross externaldebt

Estimated capitalflight§

For 10LatinAmericancountriest

270

-123

For18countries

(mostly LDCs):j:

451

-198

*Source: MGT (March 1986) [sec also WORLD BANK (1985, p.64)].tArgentina, Bolivia, Brazil, Chile, Colombia, Ecuador, Mexico,Peru, Uruguay and Venezuela.:j:Consistsof the 10 Latin American countries listed in note t plusIndia, Indonesia, South Korea, Malaysia, Nigeria, Philippines,South Africa and Thailand.§Negative figures to denote the capital outflow.

(001, 1986, p. 2). The 001 argued that "LOCs havebeen obliged to implement austerity programmeswhich have hit the living standards of the poor"(001, 1986, p. 1). And yet, because of pre-existingpoverty, the room for further cuts was already small.The call was for people in the LOCs to tighten theirbelts but the sick response was "I can't: I ate ityesterday."

Not only has there been a cut in immediate living

standards. Future prospects are also threatened by thecut in investment which has been taking place in thoseLOCs with debt-servicing problems (see Table 11).

The incentive for default has risen rapidly with theperverse flow of capital since: if they are to repay theirdebts, many of the debtor LOCs will have to runbalance of trade surpluses which are very much larger(relative to national income) than that of Japan in theearly 1980s [see KALETSKY (1985, p. 77)]. But,

14 GeoforumNolume 19 Number 1/1988

Table 10. Long-term debt and financial flows to and from LDCs, 19801986 ($ bn)*

1981 1983 1985 1986

All DRS countries-long-term debt 494 630 731 775

New loansOfficial 32 33 30 31Private 91 64 52 41Total 123 97 82 72

Debt serviceCapital 47 44 53 51Interest 41 47 55 50Total 88 91 108 101

Net transfers 35 6 -26 -29

Net transfers to/from:HICs 18 -9 -28 -26Low-incomeAfrica 3 2 1 1

*Source: WORLD DANK (1987a, p. xiii).

Table 11. Investment in the LDCs in the 1980s*

Gross capitalformation as %ofGDPin 1980 1983 1985

LDCs with debt-servicing problems 25 19 18

LDCs without debt-servicing problems 28 27 27

Latin Americancountries 23 17 18

SSA countries 20 18 17

"Source: IMF (April 1986, p. 186).

although there have been defaults on interestpayments, they have not yet been on the scale ofearlier financial crises of the 1870s and the 1930s. Inthe 1870s, it is of interest to note, "the governments ofHonduras, Costa Rica, Santo Domingo, Paraguay,Spain, Egypt, Turkey, Peru, Uruguay, Liberia,Guatemala and Bolivia defaulted, often because thefear generated by the contemporary wave of defaultsprevented otherwise credit worthy countries from

refinancing existing obligations" (SEIBER, 1982, p.21). In the 1930s, there was another 'debt' crisis, andby 1938, almost three-quarters of all bond loansgranted to Latin America were in default. Ultimatelyabout 30% of all the loans were repaid(KALETSKY, 1985, pp. 89 and 92) so that,according to Kaletsky, these were not so muchrepudiations but rather 'conciliatory defaults'.Nevertheless the defaults were on a large scale.

GeoforumNolume 19 Number 1/1988

Is such a widespread default likely in the late 1980sand early 1990s?Some would say that it is by pointingto the parallels between the situation in the 1980s andthat of the 1930s. Thus there are echoes of today'scrisis in the following quote from the book by Korneret al.: "In the second half of the 1920's, LatinAmerica's debt-service commitments becamealarmingly high. The costs of interest and capitalrepayments reached almost three times the level ofcapital inflow, yet they could at first be covered bybalance of trade surpluses. But from 1928/29onwardsthe catastrophe could no longer be averted. The lastAmerican boom before the world economic crisis,and the US government's high interest policies from1928 onwards, attracted capital to the US market andbrought about a drastic reduction in the supply ofcredit for Latin American countries ... Bolivia in1930 was the first country to stop servicing its debts.By the end of 1933 all the countries of the regionexcept Argentina and Haiti had followed Bolivia'sexample" (KORNER et al., 1986, pp. 17 and 18).

Change the names of one or two Latin Americancountries, change 1928 to 1982, change a few otheryears, and the above quote could well apply to thedebt crisis of the 1980s. In the 1980s debt-servicecommitments seem to be as high for some countries inLatin America as they were in the 1930s. Table 12shows that this certainly seems to apply to Argentinaand Brazil.

There are other obvious parrallels in the above quotefrom Korner et al. - a perverse flow of capital andthen gradually default. The situation in the 1980s is,so far, similar. There are further parallels. In the1930s (as in the 1980s) there was a restructuring of theinternational trading and financial structure. In the1930s (as now) a major reserve currency wasdeclining. Then it was the pound sterling, now it is thedollar which is in slow decline.

Furthermore, it is public knowledge that there havebeen discussions between the large debtor countriesabout collective default since 1982, discussions whichhave been frequent since 1984. The Cartagena groupof 11 Latin American countries (Argentina, Bolivia,Brazil, Colombia, Chile, Dominican Republic,Ecuador, Mexico, Peru, Uruguay and Venezuela)came into being as a political response to theexperience of dealing with creditors ell bloc in theParis and London Club negotiations. As a result, theyhave formulated not only collective demands on debtbut have also discussed collective default [seeAPPGOD (1987, pp. 32 and 62), KORNER et al.

15

(1986, p. 182) and NAVARRETE (1987, pp. 3-6)].Collective default was called for by Fidel Castro inmid-1985, and a number of economists (notablyKaletsky and Lever and Huhne) have pointed to thehigh incentive which exists for the debtor countries todefault. Kaletsky has emphasised the high andgrowing 'vulnerability ratio' of the LDCs(KALETSKY, 1985, p. 102). But so far no collectivedefault has occurred. Why not?

One explanation was offered in 1984in a book by twoAmerican economists, Thomas Enders- and RichardMattione. They argued that there are considerablerestraints on default since, in the event of default, theforeign exchange reserves of the defaulting countriescould and would be seized. Argentina couldwithstand such a seizure because it is self-sufficient inoil and is a net exporter of food. But they claimed thatmost debtor countries would not be able to withstandsuch a seizure.

But in a book published in the following year,Anatole Kaletsky argued that Enders and Mattionewere wrong. Kaletsky argued that the sovereignimmunity of nation states means that privatecreditors could not seize foreign exchange reserves.Furthermore, he said, the veil of incorporation meansthat state corporation assets could not be seizedlawfully by creditors. Finally, he claimed that, in theevent of a default, it is probable that commercialshort-term debt would continue to be provided todebtor countries because of competition betweencapitalists in the creditor countries. Thus, by contrastwith Enders and Mattione, Kaletsky concluded that"Western legal systems would give creditors onlymodest opportunities to disrupt a defaultingcountry's trade or to restrain others from doingbusiness with it" (KALETSKY, 1985, p. 21).

Thus Kaletsky's research seems to establish that thenet incentives for default are high. The debtorcountries 'vulnerability ratios' are high, their assetscould not be seized in the event of a default, and thereseems little immediate prospect of an improvement intheir situation. Why then has default not been morewidespread, matching the scale of the 1930s?

The short answer is that, although there are parallelswith the 1930s, there are also three importantdifferences:

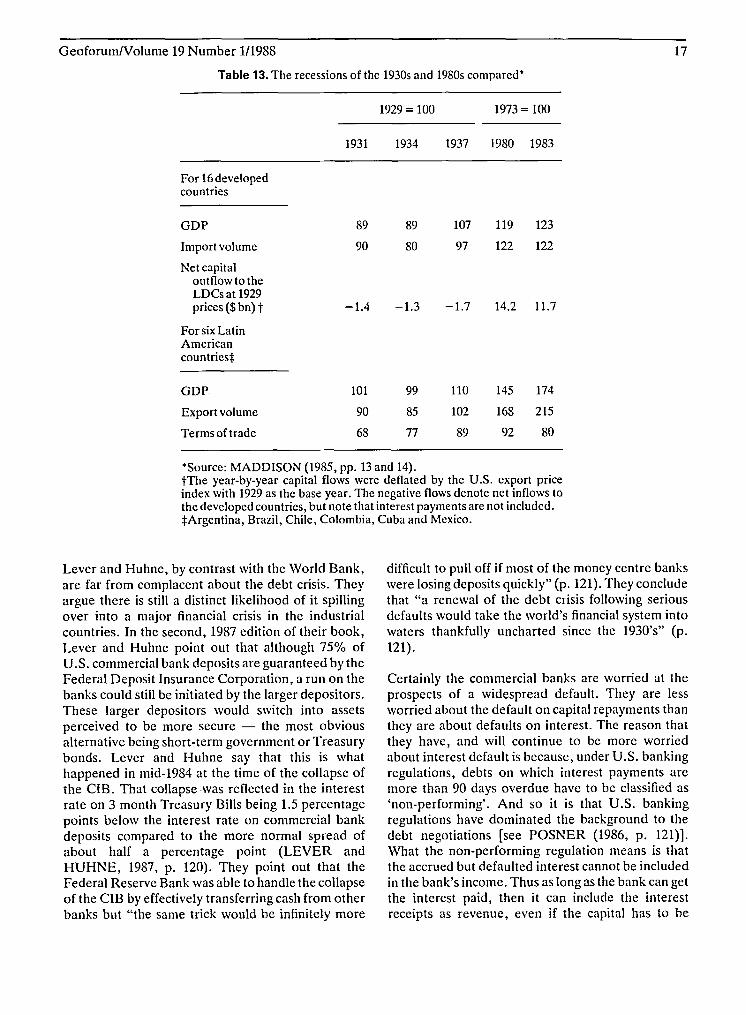

(i) The first difference is that the depression wasworse in the 1930s than it has been in the 1980s. AsTable 13 shows, in the 19305the fall in the output of

16 GeoforumNolume 19 Number 1/1988

Table 12. Debt-service ratios in the 1930s and 1980s: Argentina and Brazil'

Debt serviceasa % ofthevalueofexports 1931 1933 1980 1982

Argentina 23 30 32 103Brazil 28 41 61 87

'Sources: CLINE (1983, pp. 130 and 131) and SEIBER (l982, p. 24).

the developed countries from the peak of the cyclewas much greater: in the 1930s the fall in importvolume by the developed countries was much greater:in the 1930s, the terms of trade deterioration of theLDCs was greater (although it should be noted thatthe terms of trade have continued to fall since 1983,the last year shown in Table 13). Finally the tablesuggests that the flow of capital from the DCs hasbeen positive in the 1980s whereas it was negative inthe 1930s. [But note that the figures shown in Table 13are taken from the book by MADDISON (1985),who does not include the interest payments in thecapital flow calculations. The inclusion of interestoutflows from the LDCs would worsen both the 1930sand 1980sfigures.](ii) A second difference is that in the 1930s, themoney was mostly owed to holders of bonds whofound it more difficult to organise collectively than dothe commercial banks now (STRANGE, 1986, p.48). The latter have been able to co-ordinate theirpressures on the debtor countries, but they have alsobeen able to co-ordinate the rescheduling of theirloans. They have had a considerable incentive to actcollectively for they are highly integratedinternationally. There are laws in the U.S (the 1933Glass-Steagall and McFadden Acts) limiting theintegration of the financial sector in the U.S. bothacross states and by function (STRANGE, 1986, pp.52 and 53). One purpose of these Acts was to preventa domino effect whereby if one bank goes under theyall collapse, but the laws are unlikely to be effective,since the banks are highly interdependent throughmassive inter-bank borrowings. For example, in theeurocurrencies market, the value of inter-bank loansis twice that of the loans from the banking sector tonon-banks (see Table 6), so that, if one major bankgoes under, the viability of others is severlythreatened. Thus, in 1984, the Far Eastern EconomicReview wrote that the collapse of the ContinentalIllinois Bank(CIB) "underlined the fact that the mostdangerous bank runs are started not by the public but

by other banks", (31 May 1984, p. 79). Just before itscollapse, the CIB had been rolling over $8 bn (about20% of its total assets) through the inter-bank marketevery night.(iii) This inter-bank lending is one of the factorsinducing the central banks to co-operate in theirsupervisory and regulatory activities, although as weshall see, they have experienced considerabledifficulties in agreeing on the principles. But close cooperation between the commercial banks andbetween the central banks has been facilitated by theIMF and the 'hegemonic' role of the U.S. (SACHS,1986, p. 410). Thus the Baker plan was aimed atreducing the incentive for the LDCs to default. As the1984/85 annual report of the BIS put it: "it wasnecessary to give the debtor countries hope that it wasworth their while to continue their efforts towards reestablishing their creditworthiness. Failing this, theconsequences for the creditors of a massivedefault ... could again have constituted a threat tothe financial system" [quoted in PAGE (1986, p. 37)].Thus "whereas in the past, repayment 'morale' was, ifnecessary, restored by 'gunboat diplomacy', themethods of disciplining a debtor country today aremore subtle" (KORNER et al., 1986, p. 21). The'more subtle' methods referred to here are those ofIMF conditionality, but they could also include thepressures on the commercial banks and themultilateral agencies.

Thus there are important differences as well asparallels between the crisis of the 1980s and that ofthe 1930s. But this seems hardly to justify thecomplacency of the World Bank which in its 1985World Development Report concluded that "byhistorical standards, debt servicing difficulties in the1960s and 1970s do not seem unduly serious" (p. 4).The obvious counters to this are that the difficultieshave worsened since the 1970sand that in any case thehistorical standards themselves are particularlyunpleasant.

GeoforumIVolume 19 Number 1/1988 17

Table 13. The recessions of the 19305 and 19805 compared'

1929 =100 1973=100

1931 1934 1937 1980 1983

For 16developedcountries

GDP 89 89 107 119 123

Import volume 90 80 97 122 122

Net capitaloutflow to theLDCsat 1929prices ($ bn) t -1.4 -1.3 -1.7 14.2 11.7

For sixLatinAmericancountriest

GDP 101 99 110 145 174

Export volume 90 85 102 168 215

Terms of trade 68 77 89 92 80

'Source: MADDISON (1985, pp. 13and 14).tThe year-by-year capital flows were deflated by the U.S. export priceindex with 1929 as the base year. The negative flows denote net inflows tothe developed countries, but note that interest payments are not included.:j:Argentina, Brazil, Chile, Colombia, Cuba and Mexico.

Lever and Huhne, by contrast with the World Bank,are far from complacent about the debt crisis. Theyargue there is still a distinct likelihood of it spillingover into a major financial crisis in the industrialcountries. In the second, 1987 edition of their book,Lever and Huhne point out that although 75% ofU.S . commercial bank deposits arc guaranteed by theFederal Deposit Insurance Corporation, a run on thebanks could still be initiated by the larger depositors.These larger depositors would switch into assetsperceived to be more secure - the most obviousalternative being short-term government or Treasurybonds . Lever and Huhne say that this is whathappened in mid-1984 at the time of the collapse ofthe CIS. That collapse was reflected in the interestrate on 3 month Treasury Bills being 1.5 percentagepoints below the interest rate on commercial bankdeposits compared to the more normal spread ofabout half a percentage point (LEVER andHUHNE, 1987, p. 120). They point out that theFederal Reserve Bank was able to handle the collapseof the ClB by effectively transferring cash from otherbanks but "the same trick would be infinitely more

difficult to pull off if most of the money centre bankswere losing deposits quickly" (p. 121). They concludethat "a renewal of the debt crisis following seriousdefaults would take the world's financial system intowaters thankfully uncharted since the 1930's" (p.121).

Certainly the commercial banks are worried at theprospects of a widespread default. They are lessworried about the default on capital repayments thanthey are about defaults on interest. The reason thatthey have, and will continue to be more worriedabout interest default is because, under U.S. bankingregulations, debts on which interest payments aremore th an 90 days overdue have to be classified as'non-performing'. And so it is that U.S. bankingregulations have dominated the background to thedebt negotiations [see POSNER (1986, p. 121)].What the non-performing regulation means is thatthe accrued but defaulted interest cannot be includedin the bank's income. Thus as long as the bank can getthe interest paid, then it can include the interestreceipts as revenue, even if the capital has to be

18

rolled-over to pay the interest. A banker's expressionwhich sums this up is " rolling loans gather no loss".

It is the increased probability that interest paymentswill not be met on a large part of the Third World'sdebt that has forced the commercial banks to increasetheir provisions for bad debts . But although theprovisions of the commercial banks have been verylarge relative to their share capital , they still coveronly about a quarter to a third of their total debts tothe LDCs. And the remaining two-thirds is stilIgreater than the total share capital of the commercialbanks [see SACHS (1986 , p. 402)).

The response to this might reasonably be: "but surelythis exposure is not risky because the central bankswould bailout any major commercial banks whichrun into trouble?". After all, one of the statedobjectives of the 1913 Act establishing the FederalReserve Bank was "to furnish an elastic currency"(SMITH, 1982, p. 259), and the Fed has committeditself to bailing out the 11 largest U.S . commercialbanks (KALETSKY, 1985, p. 42) . And surely, theargument might go, the Bank of England and the Fedhave already shown how effectively they can act bytheir multi-billion dollar rescues of the NatWest bankin 1974 and ofthe CtB 10years later [sec EDWARDS(1985, p. 186) and KALETSKY (1985, p. 111)]. Butin the event of a widespread default, two problemsremain: (i) there are some uncertainties about whichcentral bank acts as lender ofIast resort, and (ii) thereare some doubts about the capacity of some centralbanks to rescue their commercial banks.

The responsibilities of the central banks havesupposedly been agreed since they drew up the BasleConcordat in 1975. But which central bank bails outwhich commercial banks is not always crystal clear asthe collapse of Ambrosiano illustrated in 1982. Theresponsibility in that example of the subsidiary of anItalian bank dealing in dollars in Luxemburg was notentirely clear. According to some reports, theallocation of responsibilities is stilI not clear. It seemsthat the U.S. and Swiss central banks emphasise hostcountry responsibility (for banking branches andsubsidiaries) while the Bank of England places moreemphasis on source country responsibility. This maybe partly because there are more branches of foreignbanks in London than there are branches of Britishbanks overseas.

But even if this lender of last resort responsibility isclear (precise details are ofcourse not publicised) , thecapacity of the central banks to bailout the

GeoforumNolume 19 Number 1/1988

commercial banks is in doubt. As Lever and Huhnepoint out , the dollar-denominated deposits in theEuropean and Japanese commercial banks faroutweigh the dollar reserves of their central banks.The !atters' foreign-currency reserves would simplybe inadequate for them to effectively act as lenders oflast resort. For example, "in Brit ain's case , the dollardeposits of the banks total $496 billion against Bankof England reserves worth $14 billion " [LEVER andHUHNE (1987, p. 121) - the figures relate to thefourth quarter of 1984].

In the event of a default, the central banks wouldneed to act rapidly and in close co-ordination tohandle (i) and (ii). But, as a result of theseuncertainties, the precise outcome of a co-ordinateddefault is difficult to predict.

It may be that these uncertainties have deterred thedebtor countries from defaulting more widely, foralmost certainly they fear that such a default wouldtrigger a financial collapse which would rebound onthem through its dislocation to trade. Certainly, asKALETSKY (1986) has pointed out, this is a fearwhich the commercial banks have been quick toexploit.

Another factor deterring a more extensive default hasbeen that the terms of lending have softenedsomewhat over the past 5 years [see DEVLIN (1986,p. 45)) . Indeed the most recent agreement withMexico had apparently to be " foisted upon areluctant IMF ... by the combined pressure of theUS Treasury and Federal Re serve Board and theMexican threat of repudiation" (BUITER andSRINIVASAN, 1987, p. 411) . But the IMF has notbeen the only one to complain. The BritishChancellor of the Exchequer, Nigel Lawson,probably had this agreement in mind when heexpressed his concern in April 1987 at the way inwhich conditions on IMF loans had beenprogressively weakened over the previous year [seeEPR (1987, p. 3)].

Thus one factor deterring default has been thesoftening of the terms of new loans and ofrescheduling of agreements. But another factorstressed by a number of economists has been thecommon interest of the ruling classes or elites in theLDCs with those in the developed countries. PeterKenen has questioned whether the officials of thedebtor countries reflect any rational calculusregarding their countries' interests. Instead he arguesthat "many of these officials acted out of a personal

GeoforumNolume 19 Number 1/1988

sense of partnership with their industrialised-countrycounterparts in a mutual effort to preserve thestability of the world financi al system" (SACHS ,1986, pp. 438 and 439). Similarly, Arthur MacEwanha s argued that "we might better understand theactions of Latin American ruling groups if we viewthem as junior partners in the operation of financialcapitalism" (MacEWAN, 1986, p. 10). Seen in thecontext of the development of national capitalism andof the capitalist state in Latin America and of thehistory of repressive governments in Latin America,MacEwan argues that it is not so difficult to explainboth the reluctance of Latin American governmentsto default, and also the lack of a popular opposition tothe austerity programmes (MacEWAN, 1986, pp.11-13).

Looking from such a viewpoint, it is likely that, formany of the debtor governments, the IMFconditionality programmes provide both an excuseand a scapegoat for the austerity measures whichhave been imposed. Thus , while Kaletsky's analysis isuseful in showing why , in an abstract sense, the LatinAmerican countries have a large incentive to default,he does not explain why such a widespread defaultha s not been initiated. MacEwan's analysis suggeststhat it is the additional dimension of capital and classwhich helps to explain the reluctance.

5. Who is to Blame? (Different Views of theCauses of the Debt Crisis)

There is some general agreement among economiststhat the debt crisis broke in the early 1980s. But thereis very little agreement on where the blame for thecrisis lies. There is also little agreement on what is tobe done. In this section I look at the different views asto the causes of the crisis, while in Section 6 I look atthe variety of solutions which have been proposed.

On the nco-classical right, the blame has tended to beassigned to profligate LDC governments andirresponsible bankers. Governments because , it isalleged, they ran up huge debts to finance overambitious investment schemes and unproductive,recurrent state expenditure. Bankers because, it isalleged, they should have been more prudent andrecognised the risks for what they were.

Thus the emphasis here has been on commercialmisjudgements by the commercial banks and oninternal mismanagement and 'distorted' domesticprice structures within the worst-affected LDCs [seeBUITER and SRINIVASAN (1987, p. 414)]. In

19

1981, the Berg report on Sub-Saharan Africa placed astrong policy emphasis on more open trade policies(WORLD BANK, 1981) and in 1983, Chap. 6 of theWorld Bank's World Development Report pointedout that those of the LDCs which had followed themost open, ' least distorted' policies had grownfastest. In the view of the free market economists, themassive capital flight from the LDCs (summarised inTable 9 earlier) merely served to demonstrate howartificially high were exchange rates and howartificially low were interest rates in many LDCs.

The call was for the LDCs to 'get their act together',and every exogenous shock to the system wasaccompanied by yet more shrill calls to get rid of'market distortions'. In this view, state interventionwas to be opposed whether it was from national orinternational sources. State intervention wasadjudged to be slow, bureaucratic and cumbersome.In this view, governmental or evenintergovernmental bodies such as the United NationsConference for Trade and Development (UNCTAD)could be said to stand for "Under No CircumstancesTake Any Decision".

In general , the structural adjustment orconditionality programmes imposed by the WorldBank and the IMF received support from the freemarket economists. At the same time, some doubtswere expressed about whether the IMF should itselflend more, since this was viewed as bailing out thecommercial banks and might merely serve to increase'moral hazard' - that is to encourage the commercialbanks to make more irresponsible loans in the beliefthat the IMF would act as a sort of internationallender of last resort (BUITER and SRINIVASAN(1987, p. 412) and VAUBEL (1983)].

The views of Keynesian economists in the politicalcentre are quite different. The emphasis here hasbeen on the external shocks which the LDCs havesuffered as a result of rising interest rates, fallingcommodity prices and declining prospects for exportsas a result of the recession . In 1983, William Clineattempted to show that of the $482 bn rise in debt ofthe non-oil LDCs between 1973 and 1982, the vastmajority was due to external factors [see CLINE(1983, p. 25)] .

A similar emphasis to that of Cline has been given byKILLICK (1984a), the second Brandt report in 1983and by LEVER and HUHNE (1987). The argumenthere was that the rising interest rates , declining nonoil commodity prices and the effects of the recession

20

on world trade had imposed shocks on the ThirdWorld which could best be met by additional loans.The problem was not that the LDCs were insolventbut that they were illiquid.

A number of 'centre' economists have questioned thetechnical competence of the IMF. "Devaluation,reduction of the budget deficit, restrictions ondomestic credit and cuts in subsidies for publicgoods - these are as a rule the major features of IMFstabilisation programmes" (KORNER et al., 1986, p.54). SPRAOS (1984) has criticised the IMF fordictating not just these means but any means in itsconditionality programmes. In his view they shouldsimply be concerned with the restoration of theexternal balance not with how it is done. Lever andHuhne have criticised the IMF for its poor diagnosisof the problem as one of internal mismanagementrather than of external shocks (LEVER andHUHNE, 1985, p. 67) and Killick has criticised theIMF for not focussing on the 'real economy' in itsdiagnosis (KILLICK, 1984a, p. 266). Thus, ingeneral, the economists in the political centre haveargued for an increased funding role by the IMF andSidney Dell has decried both the decline in the IMF'sfunding role as well as the increasing severity of itsconditions (DELL, 1981). Some indication of thereduced funding role of the IMF is given by the factthat in 1983-1984 the IMF's quotas amounted to lessthan 5% of world imports compared to more than12% in the mid-1960s [see EDWARDS (1985, p.191)]. The 'centre' economists have welcomed theBaker refinancing initiatives of October 1985,although they have argued that the proposed level ofincreased funding by the IMF and the World Bank isunlikely to be anywhere near enough. In general, the'Keynesian' view is that the IMF stands for 'ImposingMisery and Famine'.

The views of the Marxist and neo-Marxist left aresomewhat different. As is to be expected, they arehighly critical ofwhat are viewed as the simplistic,even vulgar, views of the right, but economists on theleft also acknowledge that not all the blame can beassigned to purely exogenous factors [see KORNERet al. (1986, p. 3)]. Their argument is for a politicaleconomy approach which specifically recognises thepolitical structures within the LDCs and theinteraction of those political structures with nationaland international capital. Many of the problems ofthe LDCs are seen as rooted in the economic andpolitical structures emerging from colonialism andnco-colonialism (KORNER et al., 1986, p. 157).

GeoforumNolume 19 Number 1/1988

From this viewpoint, the focus is on the politicalcontext of the IMF. The emphasis is on the politicaldominance of the IMF by the U.S., with the U.S.being able to block any change in quotas, since theserequire 85% of the total votes while the U.S. has20%. The IMF is accused of not being politicallyneutral and of favouring U.S. geo-political interests(KORNER et al., 1986, pp. 68 and 69). It is pointedout that agreements with the IMF are usually 'lettersof intent' which conveniently avoid democraticdebate and publication (KORNER et al., 1986, p.54). It is also pointed out that the IMF has not beenconsistent in always attacking state intervention. Forexample, Richard Brown has argued on the basis ofhis research on the IMF and the Sudan that IMFpolicy has been 'flexible' in the Sudan but that "thisflexibility was apparently motivated more by the USview of its strategic interest than by a response to amore plausible and coherent alternative strategy forrecovery" (BROWN, 1986, p. 508). Similarly TrevorParfitt has argued that "Zaire was favoured with fivereschedulings of its debt by the Paris club andsuccessive IMF programmes despite repeated failureto live up to the conditions set for aid" (PARFITT,1986, p. 21). The IMF is even accused of not acting inaccordance with its own Articles-especially ArticleI(ii) and Article IV(3b) - and of not acting inaccordance with its own guidelines for standbyarrangements (KORNERetal., 1986,pp. 44and 57).

In addition, it has been argued that the IMF has cooperated with the World Bank to protect the privatefinancial system. GRIFFITH-JONES (1986, p. 14)has argued that " ... financial interests appear tohave been . . . dominant in the way that debt criseshave been managed", and from this viewpoint, theIMF could be said to stand for 'Imposing Monetarismfor Financial Capital' or for the 'Interest ofMetropolitan Finance'.

At the beginning of this section, I referred to theclaim by the World Bank in 1983 that in the 1970sthere had been a strong correlation between opentrade policies and economic growth. The WorldBank's claim was part of a neo-classical bandwagonand there began to grow a conventional wisdom infavour of free trade summed up by Deepak Lal in1983: "the case for.Iiberalising financial and tradecontrol systems and moving back to a nearly-freetrade regime is incontrovertible" (LAL, 1983, p. 32).But the tide has turned. These claims have beenrefuted by careful and detailed research.

The conclusions from research carried out at the

GeoforumNolume 19 Number 1/1988

Institute of Development Studies (IDS) in Sussex,England [some of it summarised in IDS (1984)] is thatthe argument and 'evidence' of Chap. 6 of the 1983World Development Report was far too crude. One ofthe LDCs held up by the World Bank as a primeexample of a country which has experienced rapideconomic growth allegedly as a result of open-tradepolicies has been South Korea. But the IDS's detailedresearch has established that there was, through the1960s and 1970s, considerable intervention by thestate in South Korean trade and industrial policy. In athesis dated November 1983, Richard LueddeNeurath concluded that "The South Korean casesuggests not only that import controls may becompatible with successful export orientation, butalso that - properly applied - they may have aconstructive role to play in such a strategy"(LUEDDE~NEURATH, 1983, abstract) LueddeNeurath argued that the state actively intervenedthrough foreign exchange allocations andquantitative trade controls to direct industrialisationin South Korea, and that "the Korean import regimehas been highly 'managed' throughout the last twodecades" (LUEDDE-NEURATH, 1983, p. 4).

Furthermore his research suggested that "economistseager to use Korea's success to support theirtheoretical preconceptions, were often all too contentwith superficial analyses particularly regarding theextent and significance of state intervention inKorea" (LUEDDE-NEURATH, 1983, p. 10). Yetthe World Bank's stubbornness is considerable for,despite all the evidence to the contrary, the 1987World Development Report classifies South Korea asone of those countries which between 1964 and 1985were strongly outward-oriented (WORLD BANK,1987b, pp. 82 and 83).

Given these differences about the policies conduciveto economic growth, it is not surprising to find thatthere are widely differing views about the causes ofthe debt crisis. And given these differences, it is notsurprising that there are also considerabledisagreements about the most appropriate policiesfor resolving the crisis. These I turn to in the next andfinal section.

6. 'Solutions, Scenarios and Snags'Differences about Approaches to the Debt Crisisand Financial Liberalisation

There have been a vast number of proposals toresolve the debt crisis. This section does not discussall of these in detail, but is limited to discussing the

21

different approaches In terms of comparativeeconomic theory.

But first it is useful to take a look at how the debt crisishas been handled since 1982. The approach hasessentially been an ad hoc mixture of case-by-caserescheduling of the debtor countries' debt, of debtwrite-offs by the commercial banks and of a limitedamount of debt 'securitisation', either through thedebt being marketed at a discount and/or beingconverted (again at a discount usually) into equityinvestments in the debtor countries.

The renegotiation of debt has been on a country-bycountry basis with the official bilateral debt handledthrough the Paris Club and with the commercial debtrescheduled through the London Club. Thus whereasthe debtor countries have negotiated on an individualbasis, the creditors have negotiated in groups with theIMF and the World Bank usually playing prominentco-ordinating roles.

This is not to deny that there have been official callsperiodically for more generalised, systematic actionon the debt front. One example was the planannounced in September 1985 by the U.S. Secretaryto the Treasury, James Baker. The Baker Planproposed $9 billion of new loans from the WorldBank and other multilateral agencies if thecommercial banks committed $20 bn of new loansover the next 3 years. But, as was pointed out earlier,the Baker Plan, which was mostly directed at 15heavily-indebted countries, was put forward to deterthe debtor countries from further defaults on theirinterest payments. Baker's call was made inSeptember 1985-less than 3 months after the call byFidel Castro, the Cuban leader, for the debtorcountries to default. The response from thecommercial banks to the Baker initiative has beenweak, with only $2 bn of 'new money' beingcommitted by them in the first year compared to theBaker 'target' of$7 bn (APPGOD, 1987, p. 37). Thisresponse is particularly weak when it is noted that the$7 bn target is itself small compared to the largecommercial bank lending to the LDCs of the early1980s.

The Baker Plan was soon followed by a more radicalplan which was aimed at the same group of middleincome highly-indebted countries. This was the planput forward by Bill Bradley, a New Jersey senator. Itis a proposed debt relief for these countries, but on acase-by-case basis and conditional on economicpolicy reforms. The debt relief would be financed by a

22

tax on the commercial banks and channel1ed throughthe multilateral agencies. But something like 30% ofthe debt relief would go to Brazil and virtually none toSSA countries [see Williamson in SACHS (1986, pp.434 and 435)], because less than a third of the SSAdebt is owed to the commercial banks.

Thus neither the Baker nor the Bradley plan would beof much assistance to the SSA countries. By contrast,the plan of Nigel Lawson is directed at the SSAcountries. He has called for loans with interest at wel1below market rates to be provided to the indebtedcountries in Sub-Saharan Africa, the debt relief to beprovided "when the debtors are implementingappropriate reform policies" (EPR, 1987, p. 6). Hehas argued that "for some time to come ... thesecountries are un bankable" [quoted in the Guardian(23 July 1987, p. 21)]. Such debt relief would be asmal1 addition (about 4%) to the annual British aidbill. It would of course make little difference to theposition of the commercial banks. Indeed Lawson hasobjected to any direct government help for themiddle-income debtors on the ground that it wouldamount to taxpayers bailing out the commercialbanks for making what were essentially 'commercialmisjudgements' .

Thus there seems, at the very least, to be a differenceof emphasis between the official British andAmerican proposals. As a result the Baker, Bradleyand Lawson plans have not yet been acted on. Giventhis, there seems little prospect of progress on someof the more radical and far-reaching plans.

One such plan was put forward in 1976 by UNCTAD.The latter has commonly acted as the agent of LDCs'interests, and thus it is not surprising that, withinUNCTAD's demands, those for debt relief have beenprominent. UNCTAD's proposal was that the leastdeveloped countries should have their official debtcancelled (UNCTAD, 1976, pp. 22-30). Concerningcommercial debt, the proposal was that there shouldbe a long-term consolidation of the debt over a periodof at least 25 years, with a new multilateral institutionset up that could, if necessary, fund the short-termdebt of LDCs.

In 1980 the UNCTAD proposals found some supportfrom the first Brandt Report (BRANDT, 1980). Inaddition to repeating most of UNCTAD's proposals(including the creation of a new multilateraldevelopment institution and a large increase inofficial development assistance), the Brandt reportrecommended a large expansion in world liquidity in

GeoforumNolume 19 Number 1/1988

the form of a large issue of Special Drawing Rights(SDRs) - essential1y money issued through theIMF - the distribution of these SO Rs to be linked toLDCs' needs. In its second report, in the light of, as itput it, "the acute dangers to the world's financialsystem" (BRANDT, 1983, p. 11), the BrandtCommission repeated its earlier proposals but alsocal1ed for a rediscounting of the LDCs' private bankdebt by an official agency, and the rescheduling of thedebt over a long period at reduced interest rates(BRANDT, 1983, pp. 93 and 94).

The proposals of the second Brandt report werefollowed by many others along the same general linesin as much as they involved a substantial increase inofficial intervention. Thus proposals by ROHATYN(1983) and KENEN (1983) had this element incommon - namely the purchasing at a discount ofthe commercial banks' debt by a multilateral agencyand the rolling-over of the debt to the LDCs overlonger periods and at concessional interest rates.

These proposals are opposed by neo-classicaleconomists. The major objection is that of 'moralhazard' - namely that encouragement will be givento reckless lending and borrowing, if the loans areunderwritten. Clearly, as long as the problem isviewed as essentially a combination of economicmismanagement by the debtor LDCs and recklesslending by the commercial banks, then the objectionof moral hazard logically follows.

The counter-argument is that, by buying the debts ata discount from the commercial banks, the latter arediscouraged from making yet more reckless loans.But the neo-classicists stil1object that the rolling-overof the loans to the debtor LDCs does little todiscourage the latter from profligate spending. AsNunnekamp puts it: "debtors striving for economicadjustment in order to prevent or reduce financialstrains would in effect be punished"(NUNNENKAMP, 1986, p. 174). But since theproposals of UNCTAD, Brandt, Rohatyn and Kenenare based on the assumption that most of the debtorLDCs problems stem from external shocks, it is notsurprising that UNCTAD and the others dismiss thisside of the moral hazard argument.

The neo-classicists favour as both an immediate andlong-term solution a continuation of the presentpattern - structural adjustment programmes by thedebtor LDCs combined with the gradual writing-offof debt by both the official and particularly the privatecreditors. And if the writing-down of the commercial

GeoforumNolume 19 Number 1/1988

banks' debt is facilitated by the marketing of theirdebts at a discount and/or their conversion into localcurrency investments in the debtor LDCs, then somuch the better. Such a pattern reduces the problemof moral hazard (NUNNENKAMP, 1986, p. 184).The neo-classicists recognise that the problem is oneof preventing a liquidity crisis (or financial collapse)while avoiding the socialisation of the banks privatelosses. But they argue that it is important to avoid thesocialisation of losses through the government bailingout the banks. If this were to happen, it would be thebig banks who would be bailed out (or at least therewould be a general expectation of the big ones beingbailed out); deposits would be switched to them andthe small banks would suffer competitively(NUNNENKAMP, 1986, pp. 179 and 180).

But Keynesian economists argue that it is worthrisking the encouragement of further reckless lendingif by so doing the dangers of a liquidity crisis areaverted. In their view, state intervention in thefinancial sector is necessary and desirable not just inthe short term but also in the long term. Theyemphasise that interdependence is intrinsic tomodern banking and that "there is an inevitableconflict between micro-efficiency and macrostability" (HIRSCH, 1977, pp. 242 and 245). Theinterdependence is due to the risk externalities inbanking, whereby, if one bank takes a risk, some ofthe costs will be borne by them all. In a recent book,Kaufman has complained that in the financial sector"we seck the efficiencies of deregulation, but refuseto submit to the 'prosper or perish' rules of themarket-place" (KAUFMAN, 1986, p. 46). But forthe Keynesians this conflict is inherent to banking. Itis reflected in a recent statement by the Bank ofEngland: "while the bank will try to avoid placinglocally-incorporated banks at a competitivedisadvantage, this will not be done by imposing alaxer regime than prudence dictates" (Bank ofEngland Quarterly Bulletin, June 1986, p. 242). In theview of Keynesian economists, the refusal to submitto the dictates of the. market place in banking isinevitable if macro-stability is to be assured. As aresult, Fred Hirsch argues, concentration isinevitable in banking, whether it comes aboutthrough market-determined oligopolies or throughadministratively-sponsored monopolies (HIRSCH,1977, p. 252).

Thus, for Keynesian economists, because of bankingexternalities, there is a grave risk of a financialcollapse if an unrestrained free market is allowed tooperate in banking. And this is the situation at the

23

moment. As Lever and Huhne put it: "the world'sfinancial safety and economic health is balanced on aknife-edge" (LEVER and HUHNE, 1987, p. 12).

Keynesian economists recognise that some of theThird World debt is being traded at a discount butpoint out that the debt discount market is still verythin - that is, it accounts for a small proportion ofthedebt owed by the Third World. Similarly theyrecognise that some of the debt is being convertedinto direct investment in the debtor countries butagain point out that this conversion accounts for asmall proportion of the total - less than 5% of thetotal [see MGT (September 1986)]. They recognisealso that large provisions for bad debt have beenmade by the U.S. and U.K. banks in the past year butthey emphasise that these provisions account for onlyabout a quarter to a third of the LDC debt to thecommercial banks. Furthermore they point out thatthe debt discounting and the writing-off of debts bythe banks are discouraging new private loans to theLDCs. This drying-up of loans increases the flow ofcapital FROM the LDCs which in turn increases theincentive to default.

They also point out that the defaults reluctantlyannounced by some of the LDCs are likely to be acontractionary force in the world economy, and,while they welcome the multi-year reschedulingsstretching over the next decade, they emphasise thatin many cases the reschedulings have merely rolledover the crisis for a few years. Thus despite thewriting off of some of the debt, despite thesecuritisation of the debt and despite the debtreschedulings, economists in the centre point out thatthe debt crisis is still far from over. The risk of afinancial crisis is still, according to them, high.

But the opposition of Keynesian economists to a freemarket in finance is based on arguments which arebroader than those of a financial collapse. A financialcollapse may be averted and yet a free financialmarket may still be unhealthy. In this view, extensivestate intervention in the financial sector is not anecessary evil but is desirable for economic growth.

The Keynesians put forward a more fundamentalargument for state intervention in the financialsector. This more fundamental argument for a stateintervention is not new. It was put forward forward byKeynes over 50 years ago in his General Theory ofEmployment, Interest and Money. In a passagelargely neglected in later presentations of his ideas,Keynes argued for "a somewhat comprehensive

24