Embed Size (px)

Citation preview

The Credit Cloud: China Will LeapfrogThe U.S. In The Race For $53 TrillionIn Corporate Funding

Corporate & Government Ratings:

Jayan U Dhru, Senior Managing Director, New York 212-438-7276; [email protected]

Primary Credit Analysts:

Terry E Chan, CFA, Melbourne (61) 3-9631-2174; [email protected]

David C Tesher, New York 212-438-2618; [email protected]

Eduardo Uribe-Caraza, Mexico City (52) 55-5081-4408; [email protected]

Paul Watters, CFA, London (44) 20-7176-3542; [email protected]

Table Of Contents

Asia-Pacific--Has China Created A Corporate Credit Bubble?

U.S.--Continuing Economic Recovery Will Fuel Financing Needs

Europe--Trying To Get Back On Track

Latin America--Meeting A Growing Need

Downside Risk For Funding In The Western Economies

Increased Liquidity Among Western Economies Is A Partial Offset

A Fine Balance

Appendix

Related Research

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT MAY 14, 2013 1

1132346 | 300000480

The Credit Cloud: China Will Leapfrog The U.S. InThe Race For $53 Trillion In Corporate Funding(Editor's Note: Stress in the eurozone, global fiscal and budgetary gridlock, uncertainty surrounding central bank monetary

policies, and robust corporate issuance conditions fueled by investors' thirst for yield continue to generate storm clouds over the

global financial landscape. At this critical juncture, will the financial storm be blown to sea or will darker clouds begin to roll in?

Through a series of reports in 2013 titled "The Credit Cloud," Standard & Poor's Ratings Services aims to provide insight on the

competing forces that can influence corporate credit quality and alter the fragile equilibrium that currently exists in the global

corporate credit landscape.)

China is number one. At least it will soon be in terms of nonfinancial corporate debt. Standard & Poor's Ratings

Services forecasts that China's outstanding corporate debt will catch up and surpass the U.S.'s to represent the largest

amount globally within the next two years. We expect the debt needs of China, with its higher nominal GDP growth

rate, to reach $18 trillion over the next five years ending 2017--a significant share of the estimated $53 trillion of global

refinancing and new money requirements over this period. (Watch the related CreditMatters TV segment titled, " $53

Trillion For Global Corporate Debt Funding Needs Over The Next Five Years, Says Standard & Poor’s", dated May 14,

2013.)

Overview

• Globally, nonfinancial corporations will demand up to $53 trillion in refinancing and new debt needs over the

next five years. China will likely surpass the U.S. as the world's largest corporate debt borrower by 2014 or

2015.

• The Asia-Pacific region will seek $27 trillion, pushing its debt to $32 trillion outstanding by 2017, exceeding the

U.S., Canada, the eurozone and the U.K. combined.

• As the U.S. economy recovers, corporates will seek $13 trillion for refinancing and to make up for recent

underinvestment in capital expenditures.

• Eurozone and U.K. corporations will seek $10 trillion, constrained by a low-growth environment marked by

tough loan renewal conditions.

• Latin America's corporations will seek $1.4 trillion, primarily to support growing consumption and proposed

energy and infrastructure projects.

• While downside risks exist, such as credit rationing from Western banks and a potential Chinese economic

correction, our base case assumes that the banks and capital markets will be able to handle these 2013-2017

refinancing and new funding requirements.

Asia-Pacific continues to lead the way among global regions in terms of financing requirements for nonfinancial

corporate borrowers. North America is second, bolstered by a strengthening U.S. economic recovery, as evidenced by

improving housing, employment, and consumer sentiment metrics. Meanwhile, financing needs in the eurozone are

relatively subdued as the continent struggles with only marginal economic growth at best. While there has been a

pickup in Latin America, led by Brazil, the region's share remains comparatively small.

Of the $49 trillion-$53 trillion in financing (which includes both rated and unrated bonds and loans) that we estimate

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT MAY 14, 2013 2

1132346 | 300000480

nonfinancial corporates will need from 2013-2017, outstanding debt to be refinanced accounts for about $34.7 trillion,

and new money that borrowers will seek to fund growth makes up $14.7 trillion-$18.7 trillion (see table 1). The

developed Western economies of the U.S., Canada, the eurozone, and the U.K. account for about $18 trillion, or 53%,

of the refinancing amount. Of the Asia-Pacific region's almost $16 trillion refinancing need over the five-year period,

China's $8 trillion accounts for about half.

Table 1

Nonfinancial Corporate Debt Demands*

--For 2013-2017--

--New debt demand (bil.

US$)--

--Total debt

demand (bil. US$)--

Total debt

(bil. US$)

2012

Refi

demand

(bil. US$)#

Real local

currency GDP

CAGR

assumed¶

Nominal local

currency GDP

CAGR assumed¶

1x nom

GDP

growth§

1.2x nom

GDP

growth† 1x§ 1.2x†

Asia-Pacific20,838 15,628 N/A N/A 9,040 11,628 24,668 27,256

Australia 1,101 826 3.1% 5.1% 223 288 1,049 1,114

China 10,994 8,246 8.4% 11.5% 7,346 9,321 15,592 17,566

Hong Kong 457 343 4.1% 8.1% 218 270 560 612

India 862 647 6.5% 13.4% 529 702 1,176 1,348

Indonesia 141 106 6.4% 12.4% 87 113 193 219

Japan 5,179 3,884 1.3% 2.3% (227) (115) 3,657 3,769

Korea 1,335 1,001 3.7% 6.2% 535 647 1,536 1,648

Malaysia 393 295 5.2% 7.5% 179 220 474 515

Singapore 189 141 3.9% 5.7% 47 60 188 201

Thailand 187 140 4.7% 7.2% 103 123 243 263

North America13,178 9,884 N/A N/A 3,594 4,408 13,477 14,291

U.S. 12,185 9,139 3.0% 5.1% 3,413 4,179 12,552 13,318

Canada 993 745 2.2% 4.2% 181 228 925 973

Europe

(Eurozone and

U.K.)

11,158 8,369 N/A N/A 1,719 2,066 10,088 10,434

Eurozone 9,199 6,899 1.0% 2.5% 1,393 1,654 8,292 8,554

U.K. 1,959 1,469 1.6% 3.8% 326 411 1,795 1,880

Latin America1,083 812 N/A N/A 351 626 1,163 1,439

Brazil 830 623 3.3% 7.2% 221 410 843 1,032

Mexico 253 190 3.3% 9.1% 130 217 320 407

Total 46,257 34,693N/A N/A

14,703 18,728 49,396 53,420

*See appendix for details regarding data calculations. #Assumes that the debt matures roughly pro rata over an average seven-year period. So

for five years, it is 5/7, which is rounded up to 75%. ¶Based on International Monetary Fund April 2013 (current prices) projections--real local

currency GDP growth, nominal local currency GDP growth, and implied foreign exchange rate forecasts against US$; except Latin America

nominal and real GDP, Standard & Poor's. §Assumes debt grows at the same rate as GDP over the next five years. †Assumes debt grows at 1.2x

the rate of GDP over the next five years (except for Latin America: 1.5x). CAGR--Compound average growth rate. N/A--Not applicable.

China is poised to overtake the U.S. as the country with the world's largest corporate debt wall in 2014 (if debt grows

at 1.2x nominal GDP growth) or 2015 (assuming 1.0x nominal GDP growth). In the former scenario, China's

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT MAY 14, 2013 3

1132346 | 300000480

The Credit Cloud: China Will Leapfrog The U.S. In The Race For $53 Trillion In Corporate Funding

nonfinancial corporations would owe $13.8 trillion in 2014, versus U.S. corporations' $13.7 trillion--and, in the latter

scenario, $14.7 trillion in 2015 versus $14.1 trillion (see chart 1).

In a similar vein, but over a longer-term horizon, Asia-Pacific could have more corporate debt than North America, the

eurozone, and the U.K. combined by 2017, regardless of whether debt grows at 1.2x the nominal GDP growth of each

country or 1.0x nominal GDP. In the 1.2x scenario, Asia-Pacific's nonfinancial corporates would owe US$32.5 trillion,

versus the US$30.8 trillion combined total of their peers in North America, the eurozone, and the U.K. In the 1.0x

scenario, the projected figure is US$29.9 trillion for the Asia-Pacific versus US$29.7 trillion for the two other regions

(see chart 2). (Note: The cited $32.5 trillion, $30.8 trillion, $29.9 trillion, and $29.7 trillion figures are the sums of new

funding and refinancing plus the residual debt that did not require refinancing during 2013-2017 (collectively "the

balance outstanding"). Because of the addition of the residual debt, these amounts are higher than the amounts shown

in the "Total debt demand" columns of table 1, which are the sums of new funding and refinancing ("demand flow").)

Funding requirements for Brazil and Mexico, representing Latin America's largest emerging economies, would only

reach US$1.4 trillion by 2017, despite the region's economy growing at a faster rate (1.5x the rate of GDP) than the rest

of the world.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT MAY 14, 2013 4

1132346 | 300000480

The Credit Cloud: China Will Leapfrog The U.S. In The Race For $53 Trillion In Corporate Funding

Asia-Pacific--Has China Created A Corporate Credit Bubble?

Asia-Pacific's nonfinancial corporates, on the backs of Chinese companies, are lining up for $25 trillion-$27 trillion in

refinancing and new financing in the next five years. New financing could stack up Asia-Pacific's debt wall to as much

as $32.5 trillion by 2017--60% higher than at the end of last year. Within the next five years, China's economic

expansion could see its nonfinancial corporates looking for $16 trillion-$18 trillion in financing. As it stands, the

country's credit boom has resulted in outstanding corporate debt of 134% of GDP, the second highest (after the

financial center of Hong Kong) in our sample of economies.

Why has China's corporate credit been growing so fast? Simply put, high levels of investment, primarily in

manufacturing, real estate, and infrastructure, have supported the country's strong economic growth rate, particularly

over the past five years--and credit is fueling this investment. The corporate sector is the primary beneficiary of such

credit, given that the household sector is relatively underdeveloped, with domestic banks being the largest lenders,

though a significant shadow banking sector (credit intermediation outside the regular banking system) does exist.

While China is now on a lower growth trajectory than in the prior decade, the trajectory is still very high by global

standards. The country's banks, like many other Asian banks, have not come under the same stresses that banks in

Europe and U.S. have in recent years. Thus, Chinese banks have the financial capacity to continue lending.

Consequently, absent a more substantial rebalancing of the economy toward consumption, away from investment,

China's corporate debt growth is likely to continue at a fast pace for the foreseeable future.

China has had a remarkable three-decade run without suffering a year of recession. In fact, for the past two decades,

China has never reported an annual real GDP growth number below 7.5% or a nominal GDP number below 6%. While

it is tempting to say that China's economy can grow at such a level for another 20 years, we suggest that the risk of a

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT MAY 14, 2013 5

1132346 | 300000480

The Credit Cloud: China Will Leapfrog The U.S. In The Race For $53 Trillion In Corporate Funding

correction may continue to be building.

One downside risk is the likely lower productivity of investment that has been occurring since 2008. Among a sample

of 32 economies, China has the highest risk of an economic correction because of low investment productivity.

Chinese companies have been borrowing to make capital investments, primarily in manufacturing, real estate, and

infrastructure--fueling economic growth. There had been a growth spike in nominal credit to private sector in 2009,

which runs counter to the fall in nominal and real GDP growth that year (see chart 3).

Chart 3

The situation is compounded by the restricted flow of information and lack of transparency in China. Besides the rapid

credit expansion in 2009-2010 and resulting high private-sector-credit-to-GDP ratio, other risks from a banking

perspective include the significant increase in property prices, relatively weak payment and corporate governance

culture, and market distortions created by state ownership in banks. Further complications include the existence of

local government financing platforms as borrowers and shadow banking's role in lending.

A substantial portion of corporate credit in China resides with state-owned enterprises (SOEs). Our survey last year of

the top 100 corporates in China highlighted that about 80% of such corporates are SOEs. Although some of the SOEs

are publicly listed, there continues to be a high degree of information asymmetry between the SOEs and external

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT MAY 14, 2013 6

1132346 | 300000480

The Credit Cloud: China Will Leapfrog The U.S. In The Race For $53 Trillion In Corporate Funding

stakeholders. Our study also showed that borrowers' financial risk profiles are, on average, relatively weak. We assess

most companies come in at around the "significant" level--the fourth of our six rankings of financial risk (see "Business

Risk/Financial Risk Matrix Expanded," Sept. 18, 2012). Large companies tend to cluster in the "intermediate" and

"highly leveraged" categories. On the other hand, their business risk profiles are mostly stronger.

China has admirably managed through the global financial crisis, especially by their adept handling of stimulus

spending. While this track record provides comfort, unintended consequences of government policy decisions could

possibly trigger an economic correction. For example, in an attempt to rebalance the economy to depend less on

investment and more on consumption, government policy may cause investment to scale down faster than

consumption can compensate for the slack. This could result in a fairly quick rise in the banks' nonperforming loans

above currently manageable levels. Such a scenario is not necessarily disastrous. Rather, it could be cathartic in

reducing economic inefficiencies, allowing China to embark on its next stage of economic development. This is

particularly pertinent considering that China's working population is forecasted to decline in the next few years,

removing the advantage of the demographic dividend that the country has enjoyed in recent decades.

(See the Related Research section at the end of this article for a list of Standard & Poor's recently published reports

regarding China's credit situation.)

U.S.--Continuing Economic Recovery Will Fuel Financing Needs

We estimate that U.S. nonfinancial corporates will need to borrow $12.6 trillion-$13.3 trillion in the five years through

2017 (up from as much as $11.7 trillion for 2012-2016), as the recovery in the world's biggest economy takes hold.

About one-third of the total will likely be new financing. In 2012, U.S. non-financial corporates raised a record $674

billion in bonds. Companies will likely use the bulk of new financing for capital expenditures--and, to a lesser extent,

for shareholder returns and mergers and acquisitions (M&A)--as they make up for underinvestment in the wake of the

recent financial crisis and recession. Many firms have cut costs, but with the economy improving, they need to grow

top-line revenue, as it is difficult to solely cut one's way to prosperity. Funding for capital expenditures and M&A is

one way to accomplish this goal.

U.S. leveraged loan volume reached $465 billion last year--a 24% increase from 2011 and the third-highest year behind

pre-recession 2006 and 2007. In all, outstanding debt among U.S. nonfinancial corporations reached $12.2 trillion--an

increase of 6% from $11.5 trillion in 2011. Based on still current favorable credit market conditions and projected

economic expansion, the wall of U.S. nonfinancial corporate debt could grow to as much as $16.4 trillion by 2017.

We estimate that there was a shortfall in capital investment by the U.S. nonfinancial corporate borrowers we rate of

$175 billion from 2009 until the end of 2011 (see "The Credit Overhang: U.S. Corporations Have Underinvested By

$175 Billion To Bolster Cash," Dec. 12, 2012). Many speculative-grade issuers, in particular, focused on fortifying their

balance sheets, building liquidity, and enhancing profitability by cutting fat from their cost structures, rather than

investing for long-term growth. This period of underinvestment finally reversed course in 2012, fueled by robust

spending in second half of the year.

Meanwhile, U.S. corporates' record cash balances--now earning minimal interest income--as well as signs of strength

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT MAY 14, 2013 7

1132346 | 300000480

The Credit Cloud: China Will Leapfrog The U.S. In The Race For $53 Trillion In Corporate Funding

in the U.S. economy, especially in housing and employment figures, suggest that companies will soon increase stock

buybacks and dividends. We believe debt financing will be an integral part of this. Last year, nonfinancial companies in

the S&P 500 Index increased share repurchases and dividends by about 3%, to $595 billion (consisting of a 5% decline

in repurchases and 15% growth in dividends). Based on higher dividend payments and announced dividend increases

in the first quarter of this year, 2013 will likely top last year's total. Likewise, share buybacks (both completed and

announced) have increased meaningfully since the beginning of the year, with the recent announcement by Apple a

prime example.

In addition, M&A in North America will likely increase this year, as long as the positive momentum in the U.S.

economy continues and the European economic and banking outlook does not deteriorate markedly. Favorable credit

markets, sizable corporate cash reserves, and companies in maturing industries seeking to grow through acquisition all

augur well for an increase in M&A. Despite the record level of cash held by U.S. corporates, large acquisitions will

likely involve debt issuance because of low domestic cash balance and repatriation concerns. We also expect growing

participation by financial buyers and sellers that have very high levels of uninvested funds at their disposal to further

drive new financing needs. (See "Conditions Are Ripe For North American M&A To Surge In 2013," April 8, 2013.)

Europe--Trying To Get Back On Track

In the aftermath of the sovereign debt and financial crises that hit Europe, it seems clear that the combination of

expansionary monetary policy and multiyear fiscal consolidation is not likely to put the region's economy back on a

steady growth track anytime soon. In this environment, we expect nonfinancial companies in the European Economic

and Monetary Union (eurozone) and the U.K. to maximize their financial flexibility. They will likely achieve this by

preserving free cash flow, maintaining high cash balances, and refinancing on a timely basis--including diversifying

their funding sources at a faster pace than has been seen to date.

As a consequence, we have reduced our expectations for the overall corporate funding requirement in the eurozone

and U.K. for 2013-2017. We now estimate a total funding requirement of $10.0 trillion-$10.4 trillion, down from our

previous estimate of $10.5 trillion-$10.9 trillion last year. This puts Europe firmly into the slow lane compared with the

rest of the world. Over the next five years, we estimate that European corporate debt could fall to 20% of the global

total, from 24% at the end of 2012. Notably, we project that China's corporate debt will likely be at least 50% above

that of Europe by the end of 2017, despite being at a similar level today.

We also expect that European corporates have a lot further to go to wean themselves off their reliance on bank debt

for term funding, particularly in the eurozone. While this is happening slowly at present, we expect the pace to pick up

once the economic uncertainties in Europe dissipate and companies develop a greater appetite for additional term

debt. Falling yields in the bond market can only help support this process.

At the end of last year, banks provided almost 86% of outstanding private nonfinancial corporate debt in the

eurozone--just four percentage points lower than in 2008 and significantly higher than the 63% and 51% that the banks

provided in the U.K. and U.S., respectively. This is particularly relevant given our forecast that eurozone corporations

will need about $5.9 trillion to refinance existing corporate bank debt over the next five years. While we expect that

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT MAY 14, 2013 8

1132346 | 300000480

The Credit Cloud: China Will Leapfrog The U.S. In The Race For $53 Trillion In Corporate Funding

local banks will renew the vast majority of existing loans to small and medium-size enterprises (those firms most at

risk), maturities and terms may be more onerous given the capital constraints that banks face.

Of greater concern--though, perhaps, not in the short term, because of lack of demand--is companies' need for new

financing to fund growth. We estimate that the new money requirement for nonfinancial eurozone corporations could

be as high as $1.65 trillion over the next five years.

While total corporate debt has grown modestly in the past year--rising 1.1% in the eurozone and 2.8% in the U.K.--this

has all come from the bond markets. The outstanding volume of bank debt in the eurozone shrank 0.9% last year,

while outstanding bonds increased 15%, according to the European Central Bank. In the U.K., the shift was similar,

with outstanding corporate loans falling 1.8% and bonds growing 11%.

Putting this all together, in the next few years we can envisage eurozone corporate bond issuance picking up to

between €130 billion to €190 billion (US$170 billion-US$250 billion) per year as the proportion of bank to bond activity

moves towards 70/30. On top of this, given funding pressures from overstretched governments, the European

Commission is targeting the continent's private sector to fund a large part of their Europe 2020 long-term investment

program. Potentially sized at around 1.5 trillion-2.0 trillion euros ($2.0 trillion-$2.6 trillion) in total over the period

2013-2020, we estimate that institutional investors will likely be called on to invest between €50 billion and €70 billion

($65 billion-$90 billion) annually in the bond market once the program becomes established. Depending on the final

risk sharing and guarantee arrangements that will be put in place after the current consultation concludes, there is a

real risk that the institutional financing of this infrastructure program ends up competing for investor euros with what

would already be a challenging level of euro-denominated bond issuance on a net basis by eurozone corporations.

Latin America--Meeting A Growing Need

Despite Latin America's relatively small share of nonfinancial corporate debt accounting for less than 5% of the

worldwide total, regional funding requirements are on the rise. The increasing demand of a growing and young middle

class fueling consumer spending, many Latin American countries' large investments in the energy sector and overall

infrastructure to catch up with decades of underinvestment, and the ongoing consolidation in several regional

industries leading to M&A opportunities (see "Economic Growth And Opportunities In Several Markets Will Fuel M&A

Activity In Latin America," April 10, 2013) will be some of the factors contributing to larger funding requirements in the

years to come.

Our forecast calls for Latin American corporate funding requirement needs to grow at a multiple of 2x regional GDP in

the next two to three years, and to gradually decline to 1.2x-1.5x afterward. Our overall five-year forecast is 1.5x

average GDP growth, which would bring the funding requirements to about $1.4 trillion for Brazil and Mexico in 2017.

Funding needs by other Latin American economies would add to this amount. Our base case still assumes that

regional banks and debt capital markets will continue to provide the majority of liquidity for Latin American

companies to refinance their debt maturities and fund their growth. Of course, long-term growth will depend very

much on enduring business-friendly public policies and an improved institutional framework in each of the countries in

the region.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT MAY 14, 2013 9

1132346 | 300000480

The Credit Cloud: China Will Leapfrog The U.S. In The Race For $53 Trillion In Corporate Funding

On the other hand, the refinancing of $1.1 trillion of debt in Brazil and Mexico, the largest debt issuers in the region,

could be an issue if economic conditions in the eurozone or in the world's other large markets were to deteriorate, or if

economic policies in the key regional markets change for the worse.

We believe that banks and institutional investors will continue to provide the liquidity necessary for the refinancing of

Latin American corporate debt, considering the overall regional positive economic prospects ahead (Standard & Poor's

baseline assumption calls for regional growth to pick up to about 3.2% in 2013 and 3.4% in 2014--see "Latin America’s

Economic Growth Should Pick Up in 2013-2014 But Remain South of Prerecession Levels," April 23, 2013). Still, the

interconnection of the global banking system and swings in investor appetite could pose some threat. Also, temporary

industry disruptions in a few regional sectors (e.g., Mexican low income housing) and the downward pressure on

commodity prices stemming from weaker Asian demand could negatively affect the financial performance of regional

producers--and ultimately have an impact on their funding needs and refinancing alternatives. Still, under our

base-case scenario, we expect the regional demand for funds to increase in coming years.

About $100 billion of bonds that Standard & Poor's rates in Latin America will mature in the next five years and nearly

75% of them are rated at an investment-grade level, which should make for low refinancing risk. Lower-rated

borrowers' refinancing will likely continue to depend on benign economic conditions and investor appetite for high

yields, given the aversion of some of the larger banks and institutional investors to take on that type of risk. So the

likelihood of a few of these bonds defaulting is still present. However, the good news is that more regional companies

rated in the 'BB' category (and of course above) are finding funding in the debt capital markets as they take advantage

of low interest rates and a burgeoning investor class. Nonfinancial corporate bonds already represent close to 25% of

the total funding needs in Brazil and Mexico. Meanwhile, given growth prospects in the region, some of the larger

financial institutions expect to continue growing their loan portfolios (accounting for the lion's share of credit to the

private sector) by 10-20% in the next couple of years, with a focus on medium-size enterprises.

Downside Risk For Funding In The Western Economies

We have premised our debt projections on a recovery following historical patterns. Yet that is not at all certain given

the myriad of uncertainties that prevail. Not least, Western banks may continue to ration credit as they seek to repair

their balance sheets, and reassess their risk thresholds. Moreover, the largest U.S. banks could curtail their lending as

they stash away more capital to meet what could soon be much stricter requirements (see "Brown-Vitter Bill:

Game-Changing Regulation For U.S. Banks," April 25, 2013). Lack of confidence in the strength of recovery and tight

credit conditions could certainly weigh on growth prospects.

In the unlikely downside scenario of the U.S., eurozone, and U.K. experiencing similar nominal GDP cumulative

average growth rates as they did for the past four years (2.4%, 0.7%, and 1.7% per annum respectively) over the next

five years, their collective refinancing and new funding needs for 2013-2017 would decline to $19 trillion-$20 trillion, or

18%-20% down from our base case $24 trillion to $25 trillion. In turn, the global corporate need would fall to $45

trillion-$48 trillion.

Still, while downside risks remain, our base-case assumption is that banks and capital markets will largely be able to

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT MAY 14, 2013 10

1132346 | 300000480

The Credit Cloud: China Will Leapfrog The U.S. In The Race For $53 Trillion In Corporate Funding

meet borrowers' financing needs--in part because of the still very accommodative monetary policy of U.S. and

European authorities. But the balance is tenuous. Governments and banking regulators are not as well positioned as

they were last year to counter adverse conditions, having already exhausted much of their fiscal and monetary

arsenals. Furthermore, some countries are struggling to implement austerity measures to deal with their own sovereign

debt and deficit problems. This may impede their ability to respond to additional economic turbulence. Depending on

the severity of a flare-up, a wider set of borrowers than just those that are highly leveraged could find their financing

and refinancing needs in jeopardy.

While most of the economic and regulatory challenges that banks face are similar in the U.S. and Europe, we believe

there could be more severe effects on lending in the eurozone, where banks have been slow to trim their corporate

exposures, which is likely to put further pressure to curtail lending in unfamiliar regions or sectors. Beyond having to

adapt to a sovereign debt crisis and economic slump, European banks continue to work toward meeting

capital-adequacy and stress-testing standards as part of the Basel III accord. This will likely have more profound

consequences for corporate borrowers in Europe because they rely more on banks than the bond market for funding

than their U.S. counterparts. The effects may be exacerbated for borrowers with comparatively weak credit quality or

those sectors where banks have a high concentration of risk.

We do not expect U.S. lenders to incorporate Basel III standards for several years, as firm rules have not been

established by the Federal Reserve. At the same time, U.S. banks may limit their loan growth because of the higher

regulatory cost of capital that domestic rules may require. This could mean that traditional relationship lending--such

as general-purpose credit facilities--may become more expensive or less available.

The corporate bond market in the U.S. has demonstrated its ability to make up any shortfall, providing more than $550

billion in corporate funding in each of the past three years. The less-developed bond market in Europe presents greater

challenges for corporates. By our calculations, if eurozone corporations were to raise 25%-30% of their new funding

requirements in the bond markets (up from about 15% historically), this would amount to between $170 billion and

$250 billion each year. According to Eurostat, prior to 2012 (which was a record-breaking year for corporate

euro-denominated bond issuance, when net issuance reached a $134 billion equivalent), there were only two years

since 2000 when net issuance even came close to $100 billion. As such, the liquid U.S. bond market can and does

provide a partial offset to capacity constraints in Europe.

Meanwhile, Asian banks are, in our view, likely to continue lending, although at a rate in line with decelerating

economic growth. In some Asian countries, such as China, a large portion of bank lending may be state-directed so

that financing capacity isn't subject to the same limitations as in Western markets.

Increased Liquidity Among Western Economies Is A Partial Offset

A partial offset to the funding risk is the ever-growing pile of liquid assets sitting on the sidelines in the U.S. and

eurozone corporate balance sheets, totaling $4.85 trillion at the end of 2012 (see appendix note). These balances have

built up as companies have focused on managing overheads, maximizing free cash flow, and minimizing discretionary

expenditures in response to the recessionary concerns in U.S. and eurozone. While each region's corporate balance

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT MAY 14, 2013 11

1132346 | 300000480

The Credit Cloud: China Will Leapfrog The U.S. In The Race For $53 Trillion In Corporate Funding

sheet cash is substantial relative to each region's GDP (14.6% of U.S. GDP and 21.0% of eurozone GDP), the additional

financial flexibility this cash provides can be gauged by calculating the excess liquid assets relative to the years before

the financial crisis. On this basis, the corporate cash buffer is significantly higher in the eurozone than in the U.S. This

may reflect the U.S.'s better progress in taking policy actions to turn its economy around, translating into higher

business confidence levels, as well as greater confidence in the depth of liquidity available in the U.S. debt capital

markets. By our calculations, liquid assets have increased by about 4.8% of GDP in the eurozone over the past six

years, compared with the average level over the period 1999-2006, equivalent to €460 billion euros. On the same basis,

excess liquid assets in the U.S., while still meaningful, are substantially less, at 1.8% GDP, equivalent to $280 billion.

Further, the cash is not evenly distributed. In the U.S., certain rating categories--mainly investment grade (i.e., those

companies rated 'BBB-' or higher) and industries (e.g., technology and health care) hold a larger share of the cash pile.

The top 25 largest cash holders, which make up less than 2% of Standard & Poor's total rated issuers, account for

about 45% of total cash and short-term investments. In contrast, issuers in the speculative-grade category (rated 'BB+'

or lower), specifically in the 'B' and 'CCC/C' rating categories, have not benefited as much from the overall

strengthening of liquidity.

Accessibility of the cash is also a concern. In the U.S., for example, companies with global operations hold significant

portion of their cash overseas, which is subject to taxes as high as 35% upon repatriation. Cash flow generated

domestically is mostly earmarked for dividends and share repurchases, while cash flow generated overseas generally

sits idle. The cash imbalance continues to grow as a result. Standard & Poor's estimates that of the top 10 largest cash

holders in U.S., 80% of their cash was held overseas as of year-end 2012 versus 77% in 2011 (based on six out of 10

companies that disclosed this information). As seen with Apple Inc.'s record $17 billion bond issuance in April

earmarked for shareholder returns, these issuers continue to access the debt market as a form of balance sheet

arbitrage.

Overall, Standard & Poor's believes that while there is some scope for these liquid assets to be deployed to support and

supplement companies' growth needs, the excess over and above the average levels that prevailed prior to the

financial crisis is quite limited relative to the amount of financing required over the next five years. For the U.S., the

$260 billion excess is only equivalent to just over 2% of the overall financing requirement, while in Europe, the €460

billion would provide a more meaningful 7% of the projected financing requirement over the next five years.

A Fine Balance

All told, the growing demand for financing by nonfinancial corporate entities around the world could squeeze some

borrowers, especially those at the speculative-grade level, through the higher cost or shifting availability of capital--if

only at the margins. With the U.S. crawling to an economic recovery, Europe mired in recession, and the financing

requirements in Asia-Pacific taking center stage with China likely to soon become the world's largest debtor nation,

banks around the world are shoring up their balance sheets and rethinking their appetite for risk. Having spent much of

their fiscal and monetary capacity in recent years, governments and regulators do not have the same headroom to

battle adverse conditions as they once did. And for those who believe in the old adage "what goes up must come

down," it must seem that China's incredible three-decade-long economic growth trajectory will soon have to come to

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT MAY 14, 2013 12

1132346 | 300000480

The Credit Cloud: China Will Leapfrog The U.S. In The Race For $53 Trillion In Corporate Funding

an end. Still, despite the remaining downside risks, we believe that the banks and capital markets will have the capacity

to meet borrowers' needs over the next five years.

Appendix

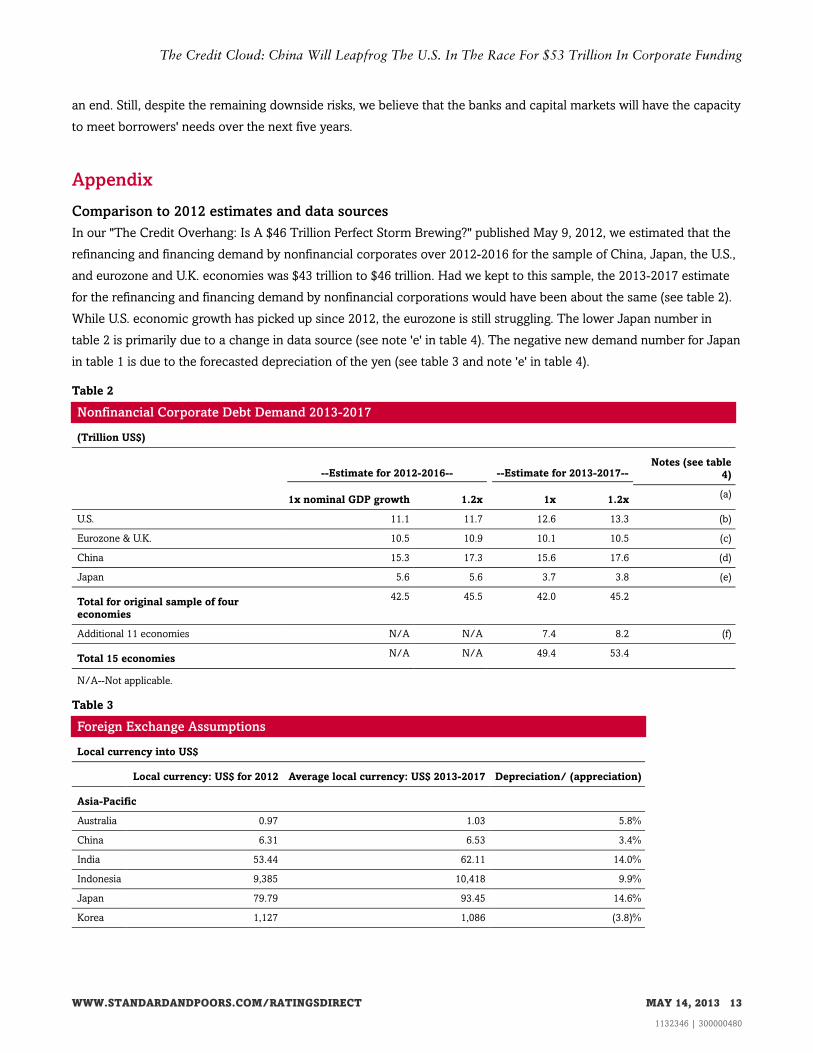

Comparison to 2012 estimates and data sources

In our "The Credit Overhang: Is A $46 Trillion Perfect Storm Brewing?" published May 9, 2012, we estimated that the

refinancing and financing demand by nonfinancial corporates over 2012-2016 for the sample of China, Japan, the U.S.,

and eurozone and U.K. economies was $43 trillion to $46 trillion. Had we kept to this sample, the 2013-2017 estimate

for the refinancing and financing demand by nonfinancial corporations would have been about the same (see table 2).

While U.S. economic growth has picked up since 2012, the eurozone is still struggling. The lower Japan number in

table 2 is primarily due to a change in data source (see note 'e' in table 4). The negative new demand number for Japan

in table 1 is due to the forecasted depreciation of the yen (see table 3 and note 'e' in table 4).

Table 2

Nonfinancial Corporate Debt Demand 2013-2017

(Trillion US$)

--Estimate for 2012-2016-- --Estimate for 2013-2017--Notes (see table

4)

1x nominal GDP growth 1.2x 1x 1.2x(a)

U.S. 11.1 11.7 12.6 13.3 (b)

Eurozone & U.K. 10.5 10.9 10.1 10.5 (c)

China 15.3 17.3 15.6 17.6 (d)

Japan 5.6 5.6 3.7 3.8 (e)

Total for original sample of four

economies

42.5 45.5 42.0 45.2

Additional 11 economies N/A N/A 7.4 8.2 (f)

Total 15 economiesN/A N/A 49.4 53.4

N/A--Not applicable.

Table 3

Foreign Exchange Assumptions

Local currency into US$

Local currency: US$ for 2012 Average local currency: US$ 2013-2017 Depreciation/ (appreciation)

Asia-Pacific

Australia 0.97 1.03 5.8%

China 6.31 6.53 3.4%

India 53.44 62.11 14.0%

Indonesia 9,385 10,418 9.9%

Japan 79.79 93.45 14.6%

Korea 1,127 1,086 (3.8)%

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT MAY 14, 2013 13

1132346 | 300000480

The Credit Cloud: China Will Leapfrog The U.S. In The Race For $53 Trillion In Corporate Funding

Table 3

Foreign Exchange Assumptions (cont.)

US & Canada

US N/A N/A N/A

Canada 1.00 1.04 3.8%

Eurozone & U.K.

Eurozone 0.78 0.76 (2.6)%

U.K. 0.63 0.65 3.1%

Latin America

Brazil 1.99 2.05 2.9%

Mexico 13.36 13.48 0.9%

N/A--Not applicable.

Source: International Monetary Fund

Table 4

Notes For Table 2

“The Credit Overhang: Is A $46 Trillion

Perfect Storm Brewing?” article published

May 9, 2012

"The Credit Cloud: China Will Leapfrog The U.S. In The Race For $53 Trillion

In Corporate Funding"

(a)Refinancing and new financing demand

We assume that for the five-year period

2012-2016:

We assume that for the five-year period 2013-2017:

(i) refinancing demand is equal to three-quarters

of outstanding debt at end-2011;

(i) refinancing demand is equal to three-quarters of outstanding debt at end-2012;

(ii) new financing demand equals either 1x times

or 1.2x the cumulative average growth rate of

nominal U.S. dollar-equivalent GDP multiplied by

outstanding debt at end-2011.

(ii) new financing demand equals either 1x or 1.2x the cumulative average growth rate of

nominal local currency GDP multiplied by outstanding debt at year-end 2012. The new

financing demand is translated to U.S. dollar based on forecast average exchange rate

for the five-year period.

Nominal GDP growth rates rather than real rates

because money supply is nominal. For example,

in an economy with zero real GDP growth and

5% inflation, corporates are likely to seek 5%

more in nominal terms when rolling over their

financing.

The modified approach in (ii) is taken to address possible fluctuations in local

currency-U.S. dollar exchange rates, which may mask or exaggerate debt growth. For

example, using U.S. dollar-equivalent GDP growth for Japan would have shown

negative GDP and debt growth, if a yen depreciation against the U.S. dollar is assumed.

For GDP, Standard & Poor's estimates. GDP: Based on International Monetary Fund’s World Economic Outlook database April

2013's GDP and foreign exchange rates (see table 3), except Latin America’s, which are

based on Standard & Poor’s estimates.

(b)U.S.

Data source

Debt securities and loans: from Federal Reserve's

Flow of Funds Accounts of the U.S. (Z.1 release),

March 7, 2013. Table L.101--sum of nonfinancial

corporate businesses' commercial paper (line 19)

and corporate bonds (line 21).

Same as in prior year’s article.

GDP growth assumption

-- Higher because of economic recovery.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT MAY 14, 2013 14

1132346 | 300000480

The Credit Cloud: China Will Leapfrog The U.S. In The Race For $53 Trillion In Corporate Funding

Table 4

Notes For Table 2 (cont.)

(c)Eurozone

Data source

Debt securities and loans: from European Central

Bank Statistics

Same as in prior year’s article.

GDP growth assumption

-- Marginally lower because of still-difficult economic conditions.

U.K.

Data source

Debt securities and loans: from Office for

National Statistics.

Same as in prior year’s article.

GDP growth assumption

-- Marginally lower because of still-difficult economic conditions.

(d)China

Data source

-- For debt securities: Asianbondsonline -- For debt securities: Bank for International Settlements (BIS) Quarterly Review

December 2012

-- For loans: IMF. -- For loans: BIS’s "Long series on total credit and domestic bank credit to the private

nonfinancial sector" (http://www.bis.org/statistics/credtopriv.htm) credit data less

above debt securities data.

We changed the data source because the BIS series separates loans to nonfinancial

corporations and loans to households, which allows us to exclude the latter.

GDP growth assumption

-- Marginally lower because of lower growth trajectory.

(e)Japan

Data source

-- For debt securities: Asianbondsonline -- For debt securities: Bank for International Settlements (BIS) Quarterly Review,

December 2012

-- For loans: IMF. -- For loans: BIS’s "Long series on total credit and domestic bank credit to the private

nonfinancial sector" (http://www.bis.org/statistics/credtopriv.htm) credit data less

above debt securities data.

We changed the data source because the BIS series separates loans to nonfinancial

corporations and loans to households, which allows us to exclude the latter. For Japan,

this has resulted in a lower starting figure for outstanding debt. Consequently,

refinancing and new financing demand estimates are lower.

GDP growth assumption

-- Marginally higher because of monetary easing (we are using nominal GDP).

Foreign exchange assumption

-- We are assuming a significant depreciation of the yen against the U.S. dollar in this

article (see table 3). This, in turn, results in a lower projected U.S. dollar-equivalent debt

number than if the yen-U.S. dollar rate was held constant.

(f)Additional economies

-- Australia, Brazil, Canada, Hong Kong, India, Indonesia, Korea, Malaysia, Mexico,

Singapore, and Thailand.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT MAY 14, 2013 15

1132346 | 300000480

The Credit Cloud: China Will Leapfrog The U.S. In The Race For $53 Trillion In Corporate Funding

Table 4

Notes For Table 2 (cont.)

Data sources

-- For Asia-Pacific countries: Bank for International Settlements statistics.

For Brazil, Banco Central do Brasil; ANBIMA

For Canada, Statistics Canada

For Mexico, Banco de Mexico; Banamex.

Multiplier assumption

-- For Latin America, we adopted multiples of 1x and 1.5x in anticipation that the stage of

economic development of these countries may lead to faster growth in financing

demand.

Related Research

China

• Why Shadow Banking Has Yet To Destabilize China's Financial System, March 27, 2013

• China Banking Outlook 2013: The Credit Downcycle Persists, Feb. 25, 2013

• No Major Default So Far; So Are Chinese Local Government Debts Now Safer?, Feb. 4, 2013

• The Investment Overhang: High For China; Intermediate for Australia, Canada, France And Most BRICS, Jan. 30,

2013

• Banking Industry Country Risk Assessment: China, Jan. 4, 2013

• China (People’s Republic Of)," Dec. 21, 2012)

• China Credit Spotlight: Significant Financial Risks Fan The Flames For China's Top Corporates, Sept. 10, 2012

North America/U.S.

• Conditions Are Ripe For North American M&A To Surge In 2013, April 8, 2013

• The Credit Overhang: U.S. Corporations Have Underinvested By $175 Billion To Bolster Cash," Dec. 12, 2012

Europe

• Underwriting The Recovery: Europe's Mid-Market Seeks New Ways To Fund Growth, April 22, 2013

• Slack Growth In Europe Will Drag On Corporate Credit Prospects In 2013, Dec. 6, 2012

Latin America

• Latin America’s Economic Growth Should Pick Up in 2013-2014 But Remain South of Prerecession Levels," April

23, 2013)

• Economic Growth And Opportunities In Several Markets Will Fuel M&A Activity In Latin America," April 10, 2013

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT MAY 14, 2013 16

1132346 | 300000480

The Credit Cloud: China Will Leapfrog The U.S. In The Race For $53 Trillion In Corporate Funding

S&P may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors. S&P

reserves the right to disseminate its opinions and analyses. S&P's public ratings and analyses are made available on its Web sites,

www.standardandpoors.com (free of charge), and www.ratingsdirect.com and www.globalcreditportal.com (subscription) and www.spcapitaliq.com

(subscription) and may be distributed through other means, including via S&P publications and third-party redistributors. Additional information

about our ratings fees is available at www.standardandpoors.com/usratingsfees.

S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective

activities. As a result, certain business units of S&P may have information that is not available to other S&P business units. S&P has established

policies and procedures to maintain the confidentiality of certain nonpublic information received in connection with each analytical process.

To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certain

regulatory purposes, S&P reserves the right to assign, withdraw, or suspend such acknowledgement at any time and in its sole discretion. S&P

Parties disclaim any duty whatsoever arising out of the assignment, withdrawal, or suspension of an acknowledgment as well as any liability for any

damage alleged to have been suffered on account thereof.

Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and

not statements of fact. S&P's opinions, analyses, and rating acknowledgment decisions (described below) are not recommendations to purchase,

hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P assumes no obligation to

update the Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment

and experience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P does

not act as a fiduciary or an investment advisor except where registered as such. While S&P has obtained information from sources it believes to be

reliable, S&P does not perform an audit and undertakes no duty of due diligence or independent verification of any information it receives.

No content (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any part

thereof (Content) may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval

system, without the prior written permission of Standard & Poor's Financial Services LLC or its affiliates (collectively, S&P). The Content shall not be

used for any unlawful or unauthorized purposes. S&P and any third-party providers, as well as their directors, officers, shareholders, employees or

agents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are not

responsible for any errors or omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or for

the security or maintenance of any data input by the user. The Content is provided on an "as is" basis. S&P PARTIES DISCLAIM ANY AND ALL

EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR

A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT'S FUNCTIONING

WILL BE UNINTERRUPTED, OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no

event shall S&P Parties be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential

damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs or losses caused by

negligence) in connection with any use of the Content even if advised of the possibility of such damages.

Copyright © 2016 Standard & Poor's Financial Services LLC, a part of McGraw Hill Financial. All rights reserved.

WWW.STANDARDANDPOORS.COM/RATINGSDIRECT MAY 14, 2013 17

1132346 | 300000480