Embed Size (px)

Citation preview

The changing face of agriculture and food trade: The role of global value chains Jared Greenville

Trade and Agriculture Directorate

Information session for the Committee on

Agriculture, WTO

8 June 2017, Geneva

2

Trade and Agriculture Directorate | Organisation for Economic Co-operation and Development (OECD) | www.oecd.org/tad | [email protected]

Today’s talk

Focus is on trade within GVCs and the policy influences that impact it • Interested in whether changes in the way trade is done

have implications for international agro-food trade policy

But the concept of GVC used may differ from past studies • Not a specific value chain/niche market perspective • Broad global story of how trade is organised

Interested in exploring policies that allow countries to get the most from international markets • Concept of domestic value added

3

Trade and Agriculture Directorate | Organisation for Economic Co-operation and Development (OECD) | www.oecd.org/tad | [email protected]

Agro-food trade is growing

0

500

1000

1500

2000

2500

3000

3500

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

USD bn (real)

US GDP deflator Food price deflator

4

Trade and Agriculture Directorate | Organisation for Economic Co-operation and Development (OECD) | www.oecd.org/tad | [email protected]

Trade in agro-food products is increasingly ‘global’

• Sectors producing food source in inputs internationally • Production processes buy from GVCs

• Agro-food products also get used in the production of

other food products • Exports are sold into ongoing into GVCs

• Interconnections mean policies have wider impacts on

markets • Trade barriers and NTMs

5

Trade and Agriculture Directorate | Organisation for Economic Co-operation and Development (OECD) | www.oecd.org/tad | [email protected]

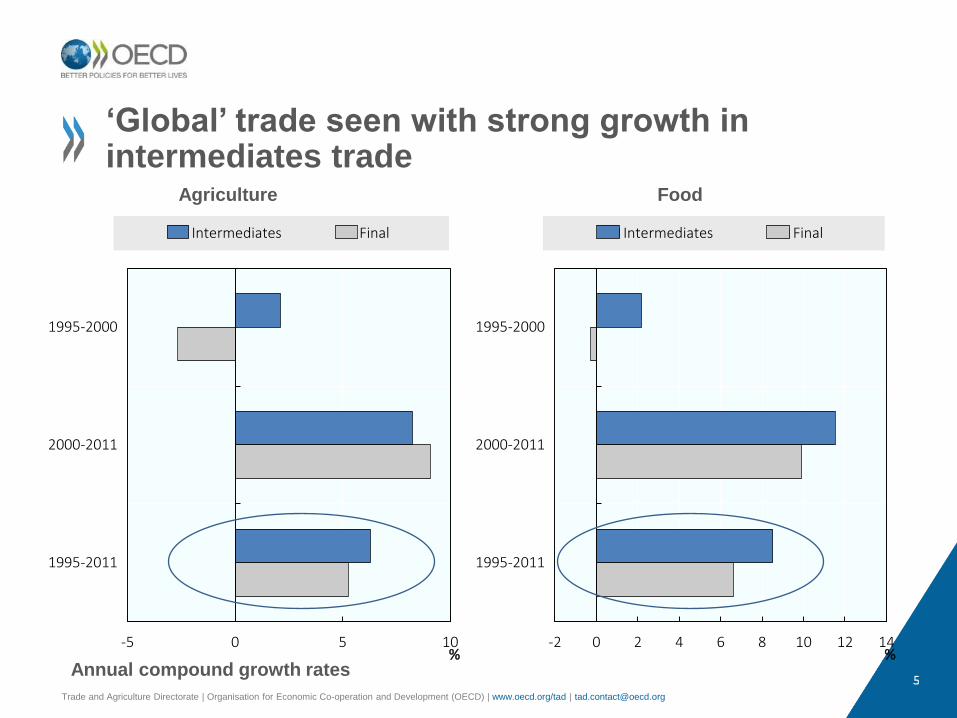

‘Global’ trade seen with strong growth in intermediates trade

-5 0 5 10

1995-2000

2000-2011

1995-2011

%

Intermediates Final

-2 0 2 4 6 8 10 12 14

1995-2000

2000-2011

1995-2011

%

Intermediates Final

Agriculture Food

Annual compound growth rates

6

Trade and Agriculture Directorate | Organisation for Economic Co-operation and Development (OECD) | www.oecd.org/tad | [email protected]

GVCs – what are they?

Value chains: describe a production process for a final

good

• Full range of activities from concept to final good

• Represent all the links between industries

Global value chains focus on the international

linkages relate to trade

• But there are also significant domestic linkages

• And products are often delivered to final demand

7

Trade and Agriculture Directorate | Organisation for Economic Co-operation and Development (OECD) | www.oecd.org/tad | [email protected]

How do we measure GVCs?

Measured from country-industry perspective

• We look first at the links for an industry in a given country

• Look at the breakdown of value added in exports

Track trade in value added flows between countries

• And see where it is used and potentially re-exported

• Computed from Inter-Country Input-Output tables

INSIGHTS INTO VALUE ADDED

8

9

Trade and Agriculture Directorate | Organisation for Economic Co-operation and Development (OECD) | www.oecd.org/tad | [email protected]

Which sectors contribute to agro-food final value? Broad players in the value chain

0

1

2

3

4

5

6

0 10 20 30 40 50 60 70 80 90

% of countries and regions

Share of final agro-food value added

Agriculture Food Industry Services

Shows the distribution of shares in agro-food final value of specific sectors

Service share greater than industrial

Most from ag and food – wider distribution in ag

10

Trade and Agriculture Directorate | Organisation for Economic Co-operation and Development (OECD) | www.oecd.org/tad | [email protected]

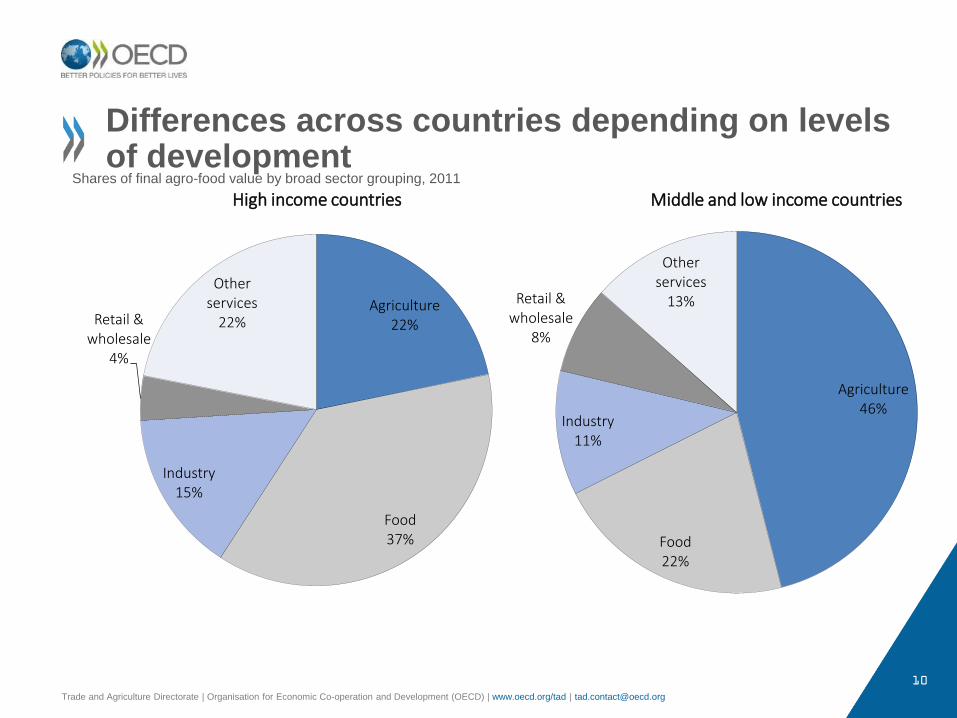

Differences across countries depending on levels of development

Agriculture 22%

Food 37%

Industry 15%

Retail & wholesale

4%

Other services

22%

High income countries

Agriculture 46%

Food 22%

Industry 11%

Retail & wholesale

8%

Other services

13%

Middle and low income countries Shares of final agro-food value by broad sector grouping, 2011

SOME RESULTS ON AGRO-FOOD GVCs

11

12

Trade and Agriculture Directorate | Organisation for Economic Co-operation and Development (OECD) | www.oecd.org/tad | [email protected]

How important are GVCs? Ratio of value added trade in intermediates to final goods

0

2

4

6

8

10

12

14

16

18

20

0

10

20

30

40

50

60

70

(Left hand axis) (Right hand axis)

Ratio less than 1

Ratio of value added trade in intermediates to final goods

13

Trade and Agriculture Directorate | Organisation for Economic Co-operation and Development (OECD) | www.oecd.org/tad | [email protected]

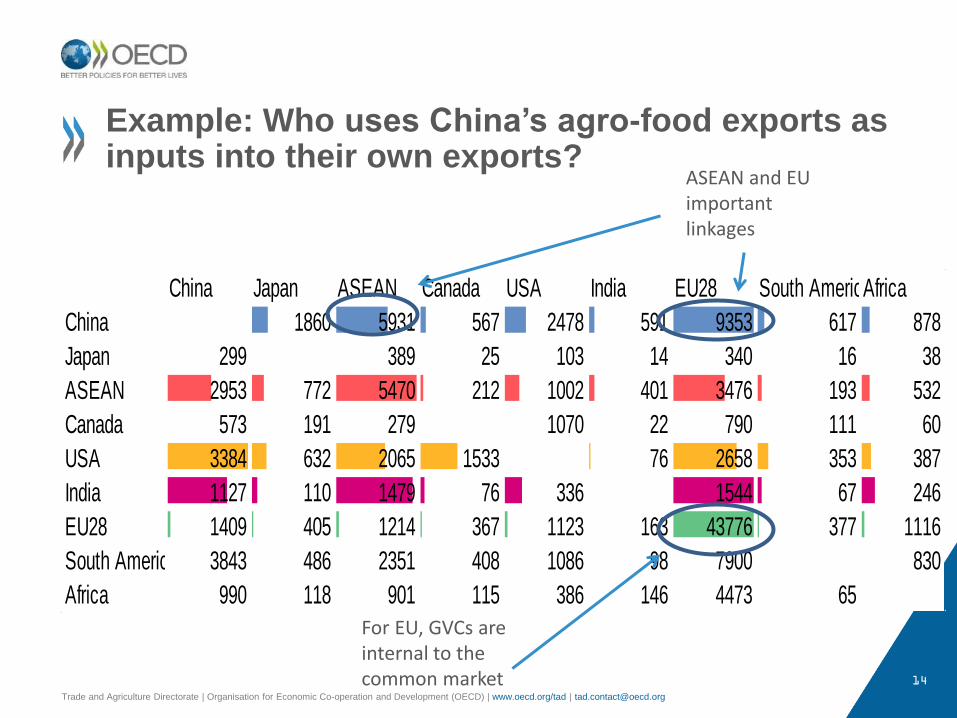

China Japan ASEAN Canada USA India EU28 Sth America Africa

China 1860 5931 567 2478 591 9353 617 878

Japan 299 389 25 103 14 340 16 38

ASEAN 2953 772 212 1002 401 3476 193 532

Canada 573 191 279 1070 22 790 111 60

USA 3384 632 2065 1533 76 2658 353 387

India 1127 110 1479 76 336 1544 67 246

EU28 1409 405 1214 367 1123 163 377 1116

Sth America 3843 486 2351 408 1086 98 7900 830

Africa 990 118 901 115 386 146 4473 65

Agro-food GVC hubs: EU, China followed by ASEAN, USA

Column shows source of foreign value added in own exports: Buying from GVCs

Row shows how exported value added is used in other country exports: Selling to GVCs

What does the agro-food GVC landscape look like?

14

Trade and Agriculture Directorate | Organisation for Economic Co-operation and Development (OECD) | www.oecd.org/tad | [email protected]

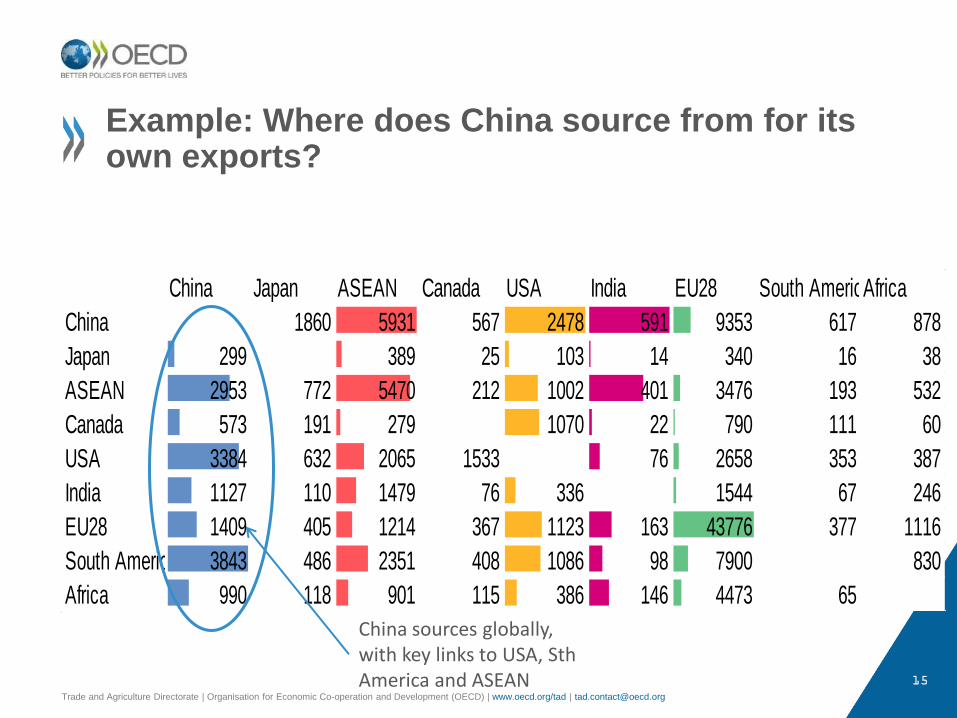

China Japan ASEAN Canada USA India EU28 South AmericaAfrica

China 1860 5931 567 2478 591 9353 617 878

Japan 299 389 25 103 14 340 16 38

ASEAN 2953 772 5470 212 1002 401 3476 193 532

Canada 573 191 279 1070 22 790 111 60

USA 3384 632 2065 1533 76 2658 353 387

India 1127 110 1479 76 336 1544 67 246

EU28 1409 405 1214 367 1123 163 43776 377 1116

South America 3843 486 2351 408 1086 98 7900 830

Africa 990 118 901 115 386 146 4473 65

ASEAN and EU important linkages

For EU, GVCs are internal to the common market

Example: Who uses China’s agro-food exports as inputs into their own exports?

15

Trade and Agriculture Directorate | Organisation for Economic Co-operation and Development (OECD) | www.oecd.org/tad | [email protected]

China Japan ASEAN Canada USA India EU28 South AmericaAfrica

China 1860 5931 567 2478 591 9353 617 878

Japan 299 389 25 103 14 340 16 38

ASEAN 2953 772 5470 212 1002 401 3476 193 532

Canada 573 191 279 1070 22 790 111 60

USA 3384 632 2065 1533 76 2658 353 387

India 1127 110 1479 76 336 1544 67 246

EU28 1409 405 1214 367 1123 163 43776 377 1116

South America 3843 486 2351 408 1086 98 7900 830

Africa 990 118 901 115 386 146 4473 65

China sources globally, with key links to USA, Sth America and ASEAN

Example: Where does China source from for its own exports?

16

Trade and Agriculture Directorate | Organisation for Economic Co-operation and Development (OECD) | www.oecd.org/tad | [email protected]

Looking more closely at backward and forward linkages

Backward linkages: buying from GVCs

• Measures the amount of foreign value added embodied in

exports

• Comes through intermediate input usage

Forward linkages: selling into GVCs

• Measures the amount of domestic value added that forms part

of another country’s exports

• So picks up the ongoing value chain

• Domestic value exported can be either direct (own exports) or

indirect (exports from other domestic industries that make use

of the outputs produced, eg processing sector exports using

agricultural production as inputs)

17

Trade and Agriculture Directorate | Organisation for Economic Co-operation and Development (OECD) | www.oecd.org/tad | [email protected]

0 0.2 0.4 0.6 0.8 1 1.2 1.4 1.6

Oilseeds

Plant-based fibers

Wheat

Other grains

Livestock

Other crops

Bovine meat

Wool & silk

Other animal products

Sugar

Vegetables, fruit & nuts

Beverages & tobacco

Dairy

Vegetable oils & fats

Other meat products

Processed rice

Other food products

Forward Backward

Forward and backward indicators across sectors

Mostly food

products with lower

rates of forward

participation, but

with higher

backward

18

Trade and Agriculture Directorate | Organisation for Economic Co-operation and Development (OECD) | www.oecd.org/tad | [email protected]

Position and total participation across sectors

Position

shows

how

relatively

forward or

backward

a sector is.

Greater

than 0

more

forward,

less than 0

more

backward

Other animal products

Bev & tob

Livestock Bovine meat

products

Other grains

Other crops

Dairy products

Other food

Other meat

Oil seeds

Plant-based fibers

Processed rice

Sugar

Vegetable oils & fats

Vegetables, fruit, nuts

Wheat

Wool & silk

-0.2

-0.1

0

0.1

0.2

0.3

0.4

0.5

0 0.2 0.4 0.6 0.8 1 1.2 1.4 1.6 1.8

Position

Total participation

By sector

19

Trade and Agriculture Directorate | Organisation for Economic Co-operation and Development (OECD) | www.oecd.org/tad | [email protected]

Forward and backward indicators across countries

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

0

0.2

0.4

0.6

0.8

1

1.2

CHN IDN JPN KOR VNM NOR THA NLD LUX KHM BEL CHE EGY PAK UKR … ETH BRA USA ARG LKA

Backward (right hand axis) Forward (right hand axis) Backward (left hand axis) Forward (left hand axis)

Top 15

Bottom 5

GETTING THE MOST FROM GVCs: IMPLICATIONS FOR

MULTILATERAL REFORMS?

20

21

Trade and Agriculture Directorate | Organisation for Economic Co-operation and Development (OECD) | www.oecd.org/tad | [email protected]

Getting the most from GVCs: domestic value added creation

Domestic value added represents the returns from

participation….

• The benefits to an economy from being involved in trade

• It represents the returns to labour and capital, along with

taxes paid to governments (but less subsidies)

• It picks up the benefits to the entire economy from the

activity

• Both within the sector and to all who contribute

• Directly links to jobs and growth

22

Trade and Agriculture Directorate | Organisation for Economic Co-operation and Development (OECD) | www.oecd.org/tad | [email protected]

Getting the most from GVCs : participation spillovers

Past studies have found the potential for splliovers

from GVC participation

• Past engagement through the use of foreign factors

grows DVA over time • Often in developing country context, but results hold for

developed

• Results hold for agri & food along with manufacturing &

services

• Influence on increasing export sophistication

Essentially productivity related upgrading (through

scale or scope)

23

Trade and Agriculture Directorate | Organisation for Economic Co-operation and Development (OECD) | www.oecd.org/tad | [email protected]

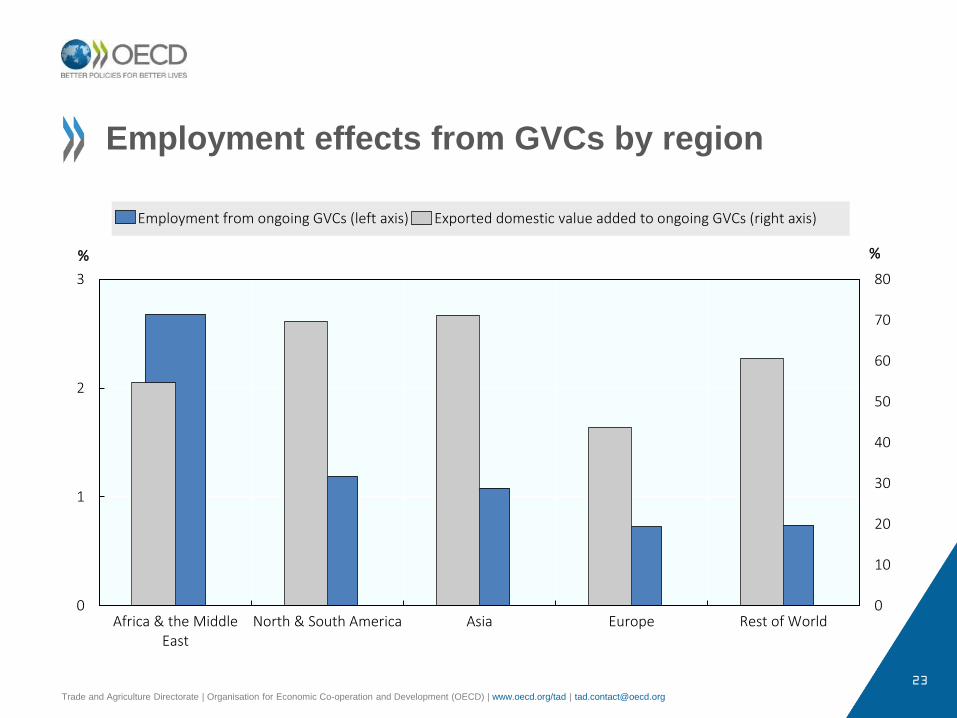

Employment effects from GVCs by region

0

10

20

30

40

50

60

70

80

0

1

2

3

Africa & the MiddleEast

North & South America Asia Europe Rest of World

% %

Employment from ongoing GVCs (left axis) Exported domestic value added to ongoing GVCs (right axis)

24

Trade and Agriculture Directorate | Organisation for Economic Co-operation and Development (OECD) | www.oecd.org/tad | [email protected]

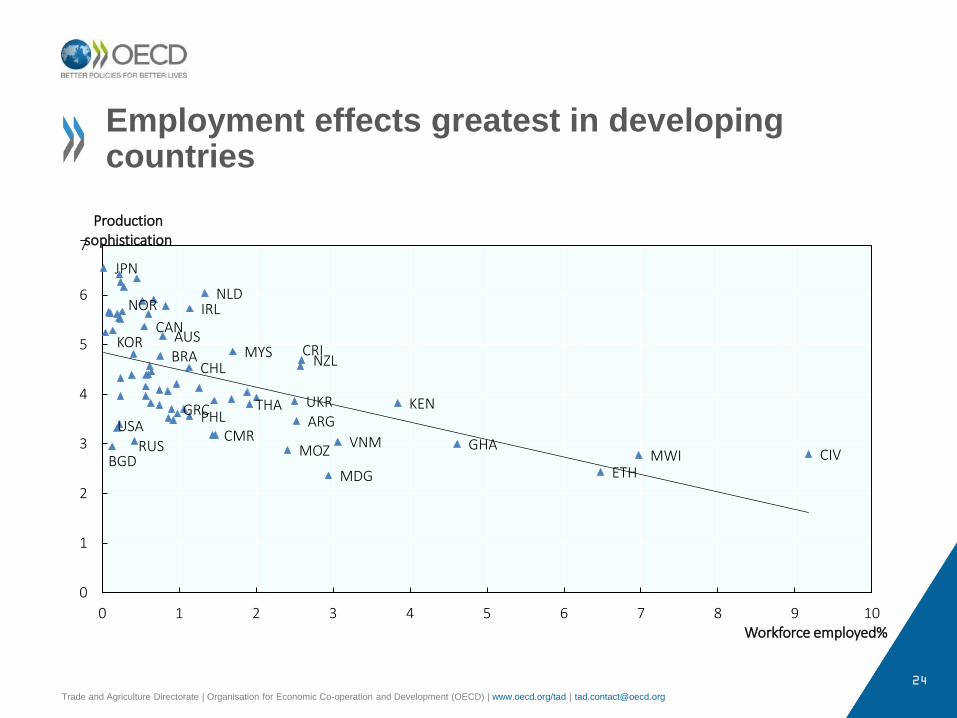

Employment effects greatest in developing countries

CIV MWI ETH

GHA

KEN

VNM

MDG

NZL CRI

ARG UKR

MOZ

THA

MYS

CMR

NLD IRL

PHL

CHL

GRC

AUS BRA

CAN

RUS

NOR

USA

BGD

KOR

JPN

0

1

2

3

4

5

6

7

0 1 2 3 4 5 6 7 8 9 10

Production sophistication

Workforce employed%

25

Trade and Agriculture Directorate | Organisation for Economic Co-operation and Development (OECD) | www.oecd.org/tad | [email protected]

Policy influences on GVC participation

OECD Trade and Agriculture Directorate 25

-0.04 -0.02 0 0.02 0.04

Distance

GDP/capita

Tariffs charged

Ag Land (sq. km)

SPS charged (L1)

TBT charged (L3)

RTA export share

RTA import share

Finance

Primary edu

Transport infrast.

Food safety

Ag R&D intensity

FDI (inflow)

Customs

Backward

-0.5 0 0.5 1

GDP/capita

Ag R&D intensity

Tariffs faced

TBT faced (L2)

SPS faced (L1)

Distance

RTA import share

Finance

Food safety

RTA export share

Transport infrast.

Primary edu

Customs

Ag Land (sq. km)

FDI (outflow)

Forward

Market size increases domestic sourcing and shift to final products

Trade facilitation important

Trade policies important

So too are aspects of the enabling environment

Effect on standardised coefficients: direction of effect is important, not size

26

Trade and Agriculture Directorate | Organisation for Economic Co-operation and Development (OECD) | www.oecd.org/tad | [email protected]

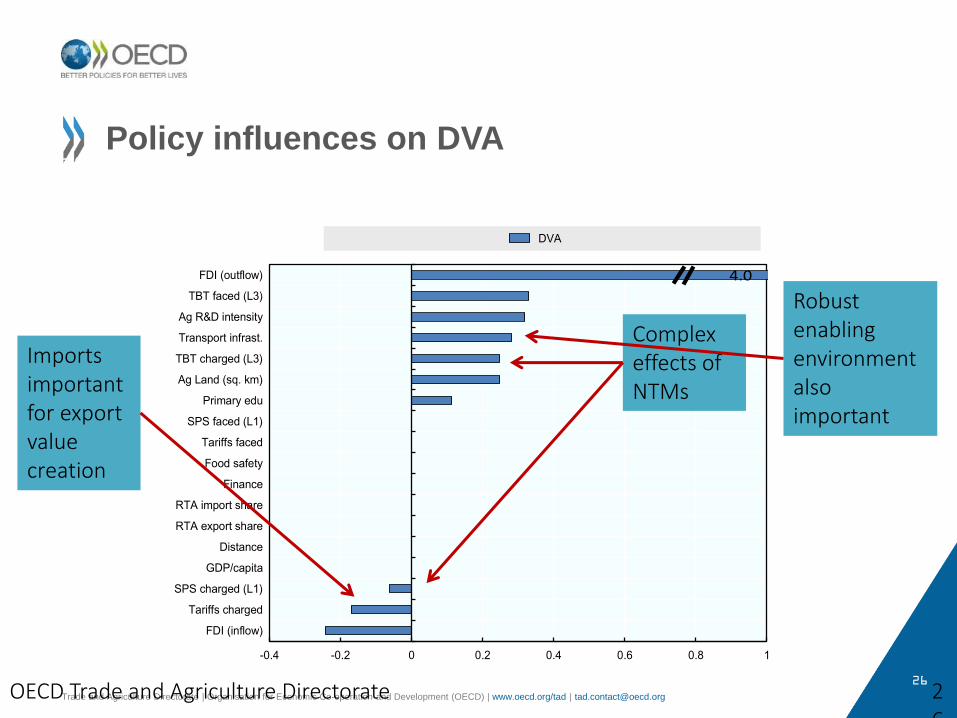

Policy influences on DVA

OECD Trade and Agriculture Directorate 26

Effect on standardised coefficients: direction of effect is important, not size

4.0

-0.4 -0.2 0 0.2 0.4 0.6 0.8 1

FDI (inflow)

Tariffs charged

SPS charged (L1)

GDP/capita

Distance

RTA export share

RTA import share

Finance

Food safety

Tariffs faced

SPS faced (L1)

Primary edu

Ag Land (sq. km)

TBT charged (L3)

Transport infrast.

Ag R&D intensity

TBT faced (L3)

FDI (outflow)

DVA

Imports important for export value creation

Complex effects of NTMs

Robust enabling environment also important

27

Trade and Agriculture Directorate | Organisation for Economic Co-operation and Development (OECD) | www.oecd.org/tad | [email protected]

Which sectors contribute to agro-food exports?

OECD Trade and Agriculture Directorate

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

0.09

0.1

-0.2 0 0.2 0.4 0.6 0.8 1 1.2

Services share Own industry share Industrial share Other agriculture share Other food share

Contribution to value added in exports

Proportion of total country-sectors

Negative value added in ag and food = policy risk

Shows the distribution of shares in agro-food export value of domestic value added created by specific sectors

Most usually generated in the industry itself

Other ag and other food industries next most important

Service share greater than industrial

Share of export DVA

28

Trade and Agriculture Directorate | Organisation for Economic Co-operation and Development (OECD) | www.oecd.org/tad | [email protected]

Key messages

• World agro-food markets have changed and so have the ways that policies impact the domestic effects of these

• Agro-food GVCs important – domestic value added creation is often underpinned by sourcing inputs internationally for exports

• Import tariffs act as taxes on exports • NTMs – need to harness trade creation and minimise cost

• Domestic agricultural support policies need to be carefully

designed to avoid negative effects on DVA (and so jobs) • Enabling environment important

• Policies outside agriculture are important – particularly services

• Plus there will be an allied jobs effect, but issues of ‘where’

29 29 29

Trade and Agriculture Directorate | Organisation for Economic Co-operation and Development (OECD) | www.oecd.org/tad | [email protected]

Access all of the

information from the

Trade & Agriculture

Directorate at:

www.oecd.org/tad

You can reach us via

e-mail by sending your

message to the following

address:

We invite you to connect

with us on Twitter by

following:

@OECDagriculture

We look forward to hearing from you!

Contact us