Embed Size (px)

Citation preview

THE CHAMBER OF TAX CONSULTANTS

TAX AUDIT - CLAUSES ISSUES & DOCUMENTATION

– CA Ketan L. Vajani

27th August, 2014

Let’s Warm Up ….

Purpose of Tax Audit

Relevance of Accounting Standards andPrinciples of commercial accounting

Materiality

Prudence

Substance Vs. Form

Concept of Test Check

True & Fair Vs. True & Correct

Guidance Note issued by ICAI

Section 44ABDifferent

Tax PayersA Person

Carrying on Profession

If his Gross Receipts

exceed 25 Lakhs Rupees in any Previous

Year.

A Person Carrying on Business

If his total SalesTurnover or

GrossReceipts, as the case may be in

business exceed or exceeds 1 Crore rupees

in any Previous Year

A Person covered U/sec. 44AD,44AE,44

AF,44BB or 44BBB

If such person claims that the profits and

gains from the business is lower than as computed

under above sections irrespective

of his turnover.

Revised Form 3CD Clauses 26 to 41

Clause 26

26. In respect of any sum referred to in clause (a),(b), (c), (d), (e) or (f) of section 43B, the liabilityfor which:

A. Pre-existed on the first day of the previous yearbut was not allowed in the assessment of anypreceding previous year and was:

(a) paid during the previous year;(b) not paid during the previous year.

B. Was incurred in the previous year and was:(a) paid on or before the due date for furnishing

the return of income of the previous year undersection 139(1);

(b) not paid on or before the aforesaid date.

Section 43B - Provisions

Deduction allowed only if actually paid Any tax, duty, cess or fee Contribution to PF, super annuation fund,

gratuity fund etc. Bonus or commission to employees Interest on loan from Financial Institution,

State Financial Corpn etc. Interest on loan from any scheduled bank Payment in lieu of Leave Salary

No disallowance if paid within due dateof filing Return of Income

Section 43B – Documents

Copies of paid challans / vouchers

Computation and Return copy forearlier years – confirm disallowancein earlier years for non payment

Earlier Years’ TAR - givingdisallowance

Section 43B

Exclusive Method of accounting – Service Tax shown as liability– Not paid whether disallowance is to be made u/s. 43B CIT Vs. Noble & Hewitt (India) Pvt. Ltd. 305 ITR 324 (Del.) Shri Kalu Karman Budhelia Vs. ACIT TS-749-ITAT-2012(Mum)

Whether Service Tax collected is Income Chowringhee Sales Bureau P. Ltd. Vs. CIT 87 ITR 542 (SC) – Sales tax

collected is Income ACIT Vs. Real Image Media Technologies P. Ltd. 114 ITD 573 (Chennai)

– Service provider is agent of government and analogy of Sales Tax /Excise does not apply to Service Tax

Effect of Section 145A – Applies to Purchase, Sales andInventories

Taxes paid after the completion of audit but before filing of report- Effect in Audit Report and computation

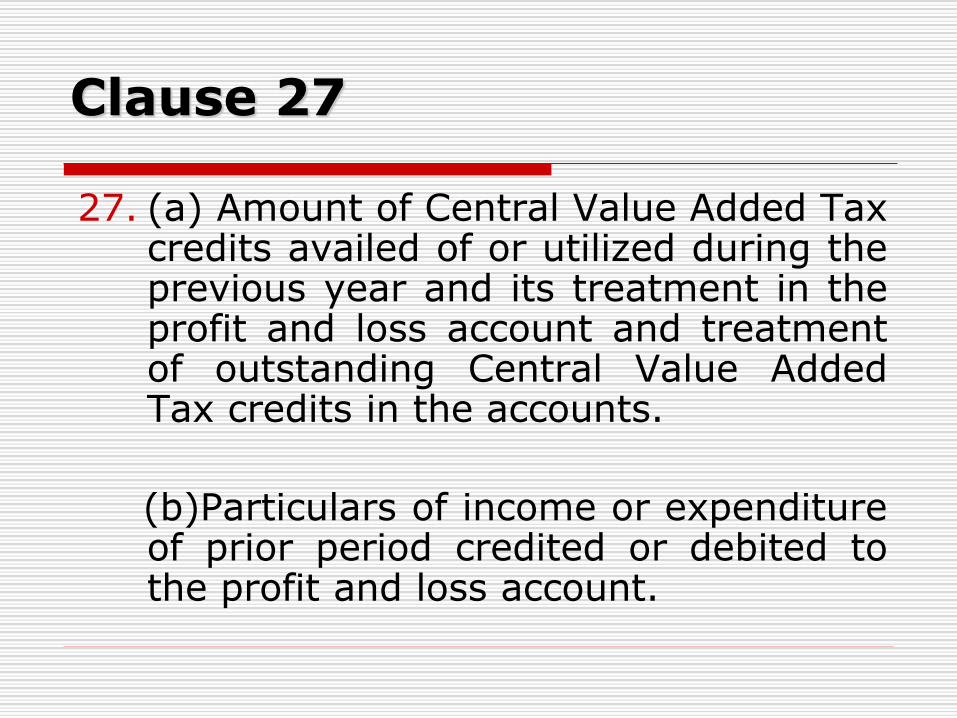

Clause 27

27. (a) Amount of Central Value Added Taxcredits availed of or utilized during theprevious year and its treatment in theprofit and loss account and treatmentof outstanding Central Value AddedTax credits in the accounts.

(b)Particulars of income or expenditureof prior period credited or debited tothe profit and loss account.

Clause – 27(a)

Earlier MODVAT – Now CENVAT

Give details about Cenvat Creditavailed and also utilised for paymentof Service Tax / Excise

Refer Service Tax / Excise Returns

Also refer to RG23 registersmaintained for excise

Take required copies as supportingdocuments

Prior Period Items

Short Provision for expenses made in earlieryear – what about differential payment made inthe current year on receipt of the bill.

Expenses of earlier year for which bills were alsoreceived in the earlier year but left out to bebooked due to error or omission

Liability under dispute in earlier year – Now paid Section 43B items – Sales tax paid of earlier

year during the current year Due to order passed in the current year Order passed earlier but not paid then and paid

now

Documentation

Clause 28

28.Whether during the previousyear the assessee has receivedany property, being share ofa company not being acompany in which public are

substantially interested, withoutconsideration or for inadequateconsideration as referred to insection 56(2)(viia),if yes, pleasefurnish the details of thesame.

Section 56(2)(viia)

Applies to firms or closely heldcompanies

Applies when company / firmsreceives shares of a closely heldcompany Without consideration – FMV exceeds

50000 – FMV taxable

Inadequate consideration – If FMV minusConsideration is > 50000 then –difference is taxable

Section 56(2)(viia)

FMV to be computed as per Rule11UA

Documentation

Valuation of shares received as per Rule11UA

Transfer document specifyingConsideration

Clause 29

29.Whether during theprevious year the assesseereceived any considerationfor issue of shares whichexceeds the fair marketvalue of the shares asreferred to in section56(2)(viib), if yes, pleasefurnish the details of thesame

Section 56(2)(viib)

Applies to closely held companies who hasissued shares to a resident at premium

Consideration received for issue of sharesin excess of FMV is taxable

Benefit of Rs. 50,000/- not available –contra to 56(2)(viia)

FMV is to be determined under Rule 11UA

Company can justify higher FMV before AOon the basis of value of intangible assets inits possession at the time of issue of shares

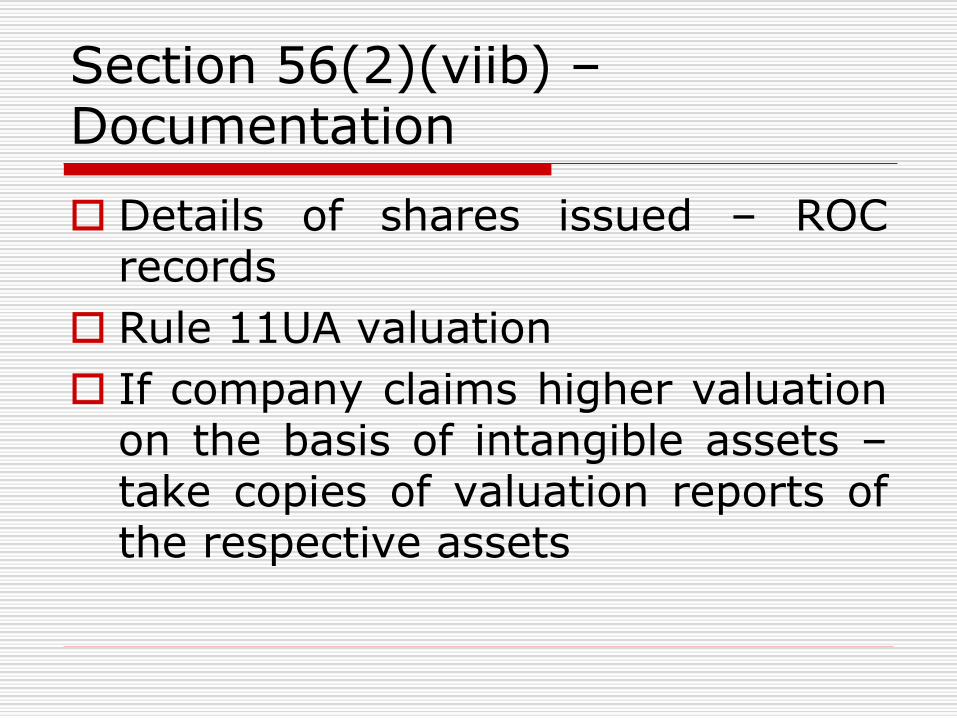

Section 56(2)(viib) –Documentation

Details of shares issued – ROCrecords

Rule 11UA valuation

If company claims higher valuationon the basis of intangible assets –take copies of valuation reports ofthe respective assets

Clause 30

30.Details of any amount borrowed onhundi or any amount duethereon(including interest on theamount borrowed) repaid, otherwisethan through an account payeecheque [Section 69D].

Section 69D

What is Hundi – Promissory Note drawn ina vernacular language

Amount borrowed on Hundi or Repaymentof the same has to be made by accountpayee cheque – Even Interest

If not through account payee cheque, theamount borrowed or repaid will beconsidered as Income in the year ofborrowing or repayment

If borrowing is taxed then repayment willnot be taxed again in the year ofrepayment

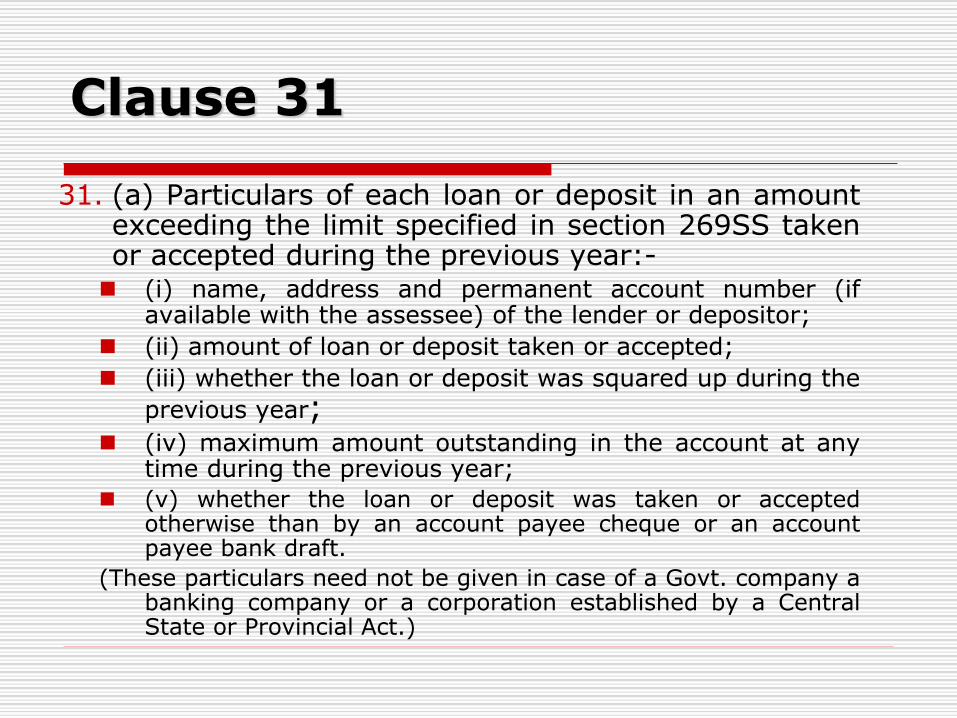

Clause 31

31. (a) Particulars of each loan or deposit in an amountexceeding the limit specified in section 269SS takenor accepted during the previous year:- (i) name, address and permanent account number (if

available with the assessee) of the lender or depositor;

(ii) amount of loan or deposit taken or accepted;

(iii) whether the loan or deposit was squared up during the

previous year; (iv) maximum amount outstanding in the account at any

time during the previous year;

(v) whether the loan or deposit was taken or acceptedotherwise than by an account payee cheque or an accountpayee bank draft.

(These particulars need not be given in case of a Govt. company abanking company or a corporation established by a CentralState or Provincial Act.)

(b) Particulars of each repayment of loan ordeposit in an amount exceeding the limitspecified in section 269T made during theprevious year:(i) name, address and permanent accountnumber (if available with the assessee) of thepayee;(ii) amount of the repayment;(iii) maximum amount outstanding in theaccount at any time during the previous year;(iv) whether the repayment was madeotherwise than by account payee cheque oraccount payee bank draft.

Clause 31 Cont….

Loans Accepted or Repaid

Certificate from assessee about compliance is not tobe obtained – Whether increases the scope of TaxAudit - Whether still certificate can be obtained ?

Amount received from customers against Sale ofGoods

No Transaction in Loan Account – Whether to bereported

Running current account – Loans taken and repaidfrom time to time – How to report

Op. Balance in Loan account is 15000/- - Currentyear Loan taken in cash Rs. 15,000/- - Whethervioldation of section 269SS

Op. Balance – 1 Lakh – Rs. 15,000/- received in cashin the year – Whether violation of section 269SS

Transactions by Journal Entries

Transactions by Journal entry whether covered :

CIT Vs. Triumph International Finance (I) Ltd. 345 ITR 270(Bom)

CIT Vs. Noida Toll Bridge Co. Ltd. 262 ITR 260 (Del.) / CIT Vs.Worldwide Township Projects Ltd. – Del HC – itatonline.org

CIT Vs. Bombay Conductors & Electricals Ltd. 301 ITR 328(Guj)

CIT Vs. Saurabh Enterprises – All HC. – itatonline.org

Lodha Builders Vs. ACIT – Mum Trib – itatonline.org

CBDT Circular No. 387 Dated 6-7-1984

Clause 32

32.(a) Details of brought forward loss or depreciation

allowance, in the following manner, to the extent

available:

SI.No

AssessmentYear

Nature ofloss/allowance(in rupees)

Amount asreturned(in rupees)

Amount asassessed (givereference torelevant order))

Remarks

(b) Whether a change in shareholding of the company has

taken place in the previous year due to which the losses

incurred prior to the previous year cannot be allowed to be

carried forward in terms of Sec 79

Clause 32 Cont…

(c) Whether the assessee has incurred anyspeculation loss referred to in section 73 duringthe previous year, If yes, please furnish thedetails of the same.

(d) Whether the assessee has incurred any lossreferred to in section 73A in respect of anyspecified business during the previous year, Ifyes, please furnish the details of the same.

(e) In case of a company, please state that whetherthe company is deemed to be carrying on aspeculation business referred in explanation tosection 73,If yes, please furnish the details ofspeculation loss if any incurred during theprevious year.

Clause – 32(b) – Section 79

Applies to a company in which public arenot substantially interested

No Loss will be allowed to be set off orcarry forward unless 51% of shares havingvoting power as at the end of the year areheld by persons holding 51% of shareshaving voting power at the end of the yearin which loss was incurred

Exception : Transfer of shares due to deathor gift to a relative

Clause – 32(b) – Section 79

Exception : Does not apply to Indiancompany which is subsidiary of a foreigncompany on Amalgamation or Demergeretc.

Does not apply to Unabsorbed Depreciation

Documentation : List of shareholders andholding as on last date of year and also lastdate of year where loss was first computed.

Brought Forward Losses

When the matter is subject to Litigation at various levels– How to report the figures of losses

How to confirm the figures of brought forward losses /depreciation

Section 79 - Loss of A.Y. 2011-12

Share holding as on 31-3-11

Share holding as on 31-3-14(Option A)

Share holding as on 31-3-14(Option B)

A 25 20 25

B 25 20 25

C 25 20

D 25 20

E 20 50

Section 73 / Section 73A

Section 73 - Speculation Loss can be setoff against only speculation profit –carry forward for 4 years

Section73A – Loss of specified businessu/s. 35AD can be set off against profitsof specified business only – If not set offthen Carry forward to subsequent years– No restriction about No. of years.

Explanation to Section 73

Business of a company consisting ofpurchase and sale of shares of othercompanies is deemed to be speculationbusiness

Exceptions Company whose GTI is mainly consisting of

Incomes other than Business Income

Company whose principal business is (a)banking or (b) granting of loans andadvances or (c) trading in shares

Clause 33

33. Section-wise details of deductions, ifany, admissible under Chapter VI-A orChapter – III (Section 10A, Section10AA)

Section underwhich deductionis claimed

Amounts admissible as per the provision ofthe Income-tax Act, 1961 and fulfills theconditions, if any, specified under therelevant provisions of Income Tax Act,1961 or Income-tax Rules, 1962 or anyother guidelines, circulars etc., issued inthis behalf.

Deductions

Certificates issued under the relevantsections by other CAs. – Whether reliable?

Deduction u/s. 80-I / 80-IA etc. computedin earlier year and accepted in the earlieryear’s assessments – Whether Auditorneeds to verify the claim again every year?

LIC / Mediclaim etc. Payments made fromIncomes other than Business Income -whether needs to be mentioned here ?

Clause 34

34.(a) Whether the assessee is required to deduct or collect tax as per the provisions of Chapter XVII-B or Chapter XVII-BB,if yes please furnish:

1. TAN No.2. Section3. Nature of Payment4. Total amount of payment or receipt of

the nature specified in 35. Total amount on which tax was required

to be deducted or collected out of 4

Clause 34

6. Total amount on which tax was required to be deducted or collected at specified rate out of 5

7. Amount of Tax deducted or collected out of the 6

8. Total amount on which tax was deducted or collected at less than the specified rate out of 7

9. Amount of tax deducted or collected on 8

10. Amount of tax deducted or collected not deposited to the credit of the Central Government out of 6 and 8

Clause 34 Cont…

(b) Whether the assessee has furnished the statementof tax deducted or collected within the prescribedtime. If not, please furnish the details:

(i) TAN No.(ii) Type of Form(iii) Due date for furnishing(iv) Date of furnishing, if furnished(v) Whether the statement of tax deducted or

collected contains the information about all thetransactions which are required to be reported

If returns filed in time – whether the aboveinformation is not required ?

Clause 34 Cont…

(c) Whether the assessee is liable to paythe interest under section 201(1A) orsection 206C (7),if yes, pleasefurnish:

• TAN No

• Amount of Interest under section201(1A)/206C(7) is payable

• Amount paid out of above alongwith date of payment.

Clause – 34 – TDS Compliance

Complete details need to be given for payments liableto TDS including the cases where deduction is madeat lesser rate

Also details of tax deducted but not deposited needsto be given

In case of Multiple TAN – Details are to be givenseparately for each TAN

Dates of filing the TDS Statements are to be reported

Auditor needs to certify that the TDS Statementfiled by assessee contains information about allthe transactions

Interest Working is required to be given – Section201(1A) – Interest Calculation

Clause 35

35.(a) In the case of a trading concern,give quantitative details of principalitems of goods traded:

i. Opening stock;

ii. Purchases during the previous year;

iii. Sales during the previous year;

iv.Closing Stock;

v. Shortage/excess, if any.

Clause – 35 Contd.

b) In the case of a manufacturing concern, givequantitative details of the principal items ofraw material, finished products and byproducts;

A. Raw Materials;(i) Opening Stock;(ii)Purchases during the previous year;(iii)Consumption during the previous year;(iv)Sales during the previous year;(v)Closing stock;(vi)Yield of finished products;(vii)Percentage of yield;(viii)Shortage/ excess, if any.

Clause 35 – Contd.

B. Finished Products/ By- products:

(i) Opening Stock;

(ii) Purchases during the previous year;

(iii)Quantity manufactured during the previousyear;

(iv)Sales during the previous year;

(v) Closing stock;

(vi)Shortage/ excess, if any.

(Information may be given to the extentavailable.)

Quantitative Details

Retail Traders dealing in many items– Stock details not maintained – Howto Report

Whether MR Letter shall be sufficientcompliance for Auditor

Other possible Documentation

Difference in units – Items purchasedin Kilos but sold in Pieces or Dozens

Clause 36

36.In the case of a domestic company, details oftax on distributed profits under section 115-0in the following form:

(a) total amount of distributed profits;(b)Amount of reduction as referred to in section

115-O(1A)(i); - Dividend received fromsubsidiary

(c) Amount of reduction as referred to in section115-O(1A)(ii); - Dividend received from NewPension System Trust

(d)Total tax paid thereon;(e) dates of payment with amounts.

Clause 37 & 38

37.Whether any cost audit was carried out? if yes,give the details, if any, of disqualification ordisagreement on any matter/item/value/quantity as may be reported/identified by thecost auditor. – Whether report to be attached ?

38.Whether any audit was conducted under theCentral Excise Act, 1944, if yes, give thedetails, if any, of disqualification ordisagreement on anymatter/item/value/quantity as may bereported/identified by the auditor.

Clause 39

39.Whether any audit was conductedunder section 72A of the FinanceAct,1994 in relation to valuation oftaxable services, if yes, give thedetails, if any, of disqualificationor disagreement on anymatter/item/value/quantity as maybe reported/identified by the auditor.

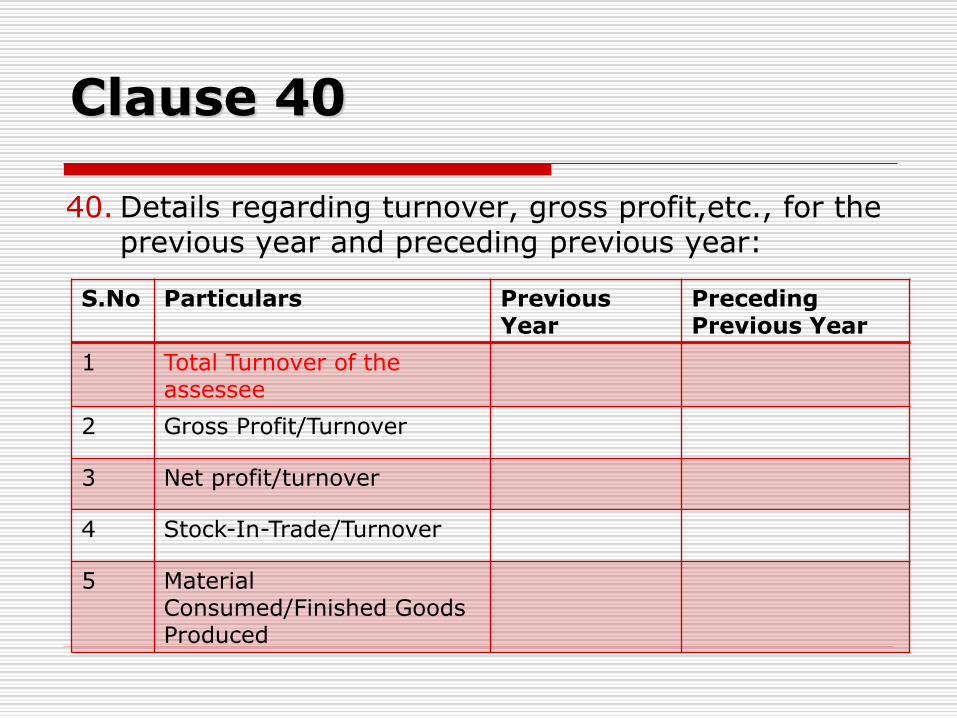

Clause 40

40. Details regarding turnover, gross profit,etc., for the previous year and preceding previous year:

S.No Particulars Previous Year

Preceding Previous Year

1 Total Turnover of the assessee

2 Gross Profit/Turnover

3 Net profit/turnover

4 Stock-In-Trade/Turnover

5 Material Consumed/Finished Goods Produced

Accounting Ratios

Total Turnover needs to be given

With Taxes or without Taxes ?

Whether the Turnover for the businesscovered by Presumptive Tax Scheme isto be excluded here

Figures of the earlier financial yearare to be given

When earlier year was not under Audit,How to confirm the figures

Clause 41

41.Please furnish the details of demandraised or refund issued during theprevious year under any tax lawsother than the Income Tax Act,1981and Wealth Tax Act 1957 along withdetails of relevant proceedings.

Demand Raised / Refund Issued

Details are to be given about demandraised or refund issued under anytax law other than Income Tax andWealth Tax

How to confirm that all details areprovided by the assessee

Auditor’s Responsibility wheninformation withheld by the assessee

What details are required to be given

E-filing of Audit Reports

Extension of Date, But which ???

Due Date extended for Tax Audit Report

Due Date for Section 44AB is the one specified in section 139(1)

Both are interlinked

Whether both extended or only date for Audit Report is extended

Filing of Return without Audit Report – Possible ? Desirable ?

Chalte Chalte …….

CA – Consistent Achiever

CTC – Capitalising The Challenges

Do Remember : When the going gets tough…. the Tough gets going

Vajani & Vajani

Chartered Accountants

Phone : 2375 9876 / 2374 0792

Handphone : 09820525972

Email:[email protected]

![BURNING ISSUES - The Chamber Of Tax Consultants...Consultants v. Union of India [2018] 400 ITR 178, observed that “To elaborate, if the power to notify standards has to be exercised](https://img.dokumen.tips/doc/110x75/5f2b22657194081597293ad1/burning-issues-the-chamber-of-tax-consultants-consultants-v-union-of-india.jpg)