Embed Size (px)

Citation preview

0

The BuzzCity Report

A QUARTERLY BRIEFING ON THE MOBILE INTERNET

VOL 4, ISSUE 4: SEPTEMBER 2014

Contents

Welcome ...................................................................................................................................................................

Market update ......................................................................................................................................................... 1

Mobile advertising ............................................................................................................................................... 1

Quarterly ranking: Top 50 mobile advertising countries ...................................................................................... 3

Featured markets .................................................................................................................................................... 4

India .................................................................................................................................................................... 5

Indonesia............................................................................................................................................................. 6

South Africa......................................................................................................................................................... 7

Nigeria ................................................................................................................................................................. 8

Pakistan .............................................................................................................................................................. 9

Malaysia ............................................................................................................................................................ 10

United States ..................................................................................................................................................... 11

United Kingdom ................................................................................................................................................. 12

Bangladesh ....................................................................................................................................................... 13

Thailand ............................................................................................................................................................ 14

Feature: Online Videos ......................................................................................................................................... 15

Introduction ....................................................................................................................................................... 15

Overview ........................................................................................................................................................... 16

Audience Highlights .......................................................................................................................................... 17

Other Observations ........................................................................................................................................... 20

Conclusions....................................................................................................................................................... 21

Media Insights: Consumers & Advertising ............................................................................................................ 22

Global Highlights ............................................................................................................................................... 22

Summary / Recommendations .......................................................................................................................... 25

Welcome

Dear Mobile Colleagues

Welcome to the latest edition of The BuzzCity Report.

In this report we cover the third quarter of 2014 during which our network

delivered 83 billion paid ads. Over the course of the year we delivered

244 billion ads, a growth of 24% from last year.

As mobile surfing grows, the public’s insatiable demand for content has

spilled over to video on mobile. In a study on video consumption, we

found 84% watch online videos and a quarter of surfers watch videos on

mobile daily. This will no doubt increase as more 4G services roll out in

the key markets we serve.

In this report we also investigate how surfers view advertising and the

media that influences them. Despite their ambivalence towards ads in

general, more than three quarters of mobile surfers rely on advertising to

make purchasing decisions. Even those who claim they don’t trust

advertising appear to be influenced by ads. Key among the influencing

media is digital and the rapid rise of online videos in the consumers’

perception. But the high expectations consumers have of advertising

suggest the need for advertisers to work harder to secure positive

engagement with the consumer if their brand and message is to stand

out.

We also look at those hotspots that have attracted advertising dollars and

are likely to do so in the coming months.

KF Lai

CEO, BuzzCity

1

Market update

The following commentary provides the headline changes and noteworthy developments in mobile advertising emerging from the global markets that we track each month.

Key indicators: Q2 2014 Ads served % of total

Number of ads served by BuzzCity’s top 20 markets 67.3 bil 81%

Number of ads served by BuzzCity’s top 50 markets 74.6 bil 90%

Network total 83.0 bil 100%

Mobile advertising

1. In the third quarter of 2014, 83 billion ad banners were served across the entire network. This brings the total number of ads served this year to 244 billion, a growth of 24% against the same period of 2013.

2. By the end of September 2014, 62% of the audience was accessing the Internet with smartphones. Android powered phones made up 34% of user devices. Notable among the competing operating systems available, Windows Phone now make up 2.5% of user devices globally compared to Apple iOS at 2.8%.

3. Smartphones are now dominant devices in at least 125 markets, where more than 50% of mobile users are equipped with smartphones.

4. At the end of September 2014, CPCs averaged 1.4 cents across the network.

5. Notable among key markets in the third quarter of 2014:

a. India. Despite a seasonal softening of ad spend; carriers as predicted in the last quarter,

continued with off-portal content promotions and other value added services. Notable among the latter are awareness campaigns for mobile money services and services for personalised data plans.

Mobile content players remained active over the last quarter.

By September 2014, our network serves more than 124 million Indian mobile surfers 51% of who surf with smartphones. Among Indian surfers Nokia (39%), Samsung (26%) and Micromax (8%) are the most popular phones.

32% 31% 33%

46% 46% 51%

59% 59% 63%

71% 72%

62%

Global Smartphone Penetration

2

Mobile is growing

faster than other

media and has

greater influence.

b. Indonesia. The pace of gentle growth continued in Q3 with a modest growth of 3% as mobile

content players picked up the pace of competitive campaigns. By the end of September 2014, nearly three quarters of mobile surfers in Indonesia accessed the Internet with smartphones. Our network now serves an audience of 74.8 million Indonesians.

By the end of September, bids prices rose marginally to USD 1.2 cents. Competitive bids are expected to continue as higher audience activity is expected as 4G services become prevalent.

c. South Africa. Advertising traffic grew by another 20% in Q3 (following a 46% growth in Q2)

despite a softening late in Q2 and early Q3.

Notable among the campaigns are the cautious return of independent mobile content players, particularly those promoting mobile messaging services. We expect this to continue as will off portal campaigns among carriers. Telcos too are active promoting personalised data services and mobile money.

We expect brand campaigns in the FMCG sector to increase in Q4 to coincide with annual holiday sales.

By end of September, bid prices averaged at 3.5 cents per click.

d. Nigeria. Advertiser activity softened by another 15% this

quarter although activity remained high. In the third quarter of 2014 our network delivered 3.3 billion ads to 14 million Nigerians.

e. Thailand. After two consecutive quarters of double-digit

growth, advertising declined by 26% as mobile content players in particular cut back on spends as a result of delays in carrier billing processes. Media in general saw weakened earnings in the last few quarters as a result of an economic slowdown brought on by political unrest.

Our network now delivers more than 1.5 billion ads per quarter to 7.9 million Thais.

By the end of September 2014 Samsung (40%), Apple (21%) and Nokia (10%) were among the most used phones among Thai users.

f. Malaysia. Traffic increased by another 20% as 2.4 billion were served to 19.8 million surfers in

the Malaysia. E-commerce portals and mainstream entertainment maintained their campaigns for traffic although there was a softening in activity among mobile content players.

By October 2014, 42% of Malaysian surfers used Samsung devices and more than three quarters (77%) used Android powered phones, notably Lenovo (15%).

CPC rates remained competitive at 2.8 cents per click by the end of September.

3

Quarterly ranking: Top 50 mobile advertising countries

Rank Country Banners Served

Q3 2014 Quarterly Growth

1 India 20,024,930,999 -13%

2 Indonesia 16,924,448,748 3%

3 South Africa 4,863,657,094 20%

4 Nigeria 3,293,106,709 -15%

5 Pakistan 2,630,588,670 -14%

6 United States 2,399,393,317 -6%

7 Malaysia 2,373,994,548 20%

8 United Kingdom 2,245,805,219 10%

9 Bangladesh 1,933,339,820 -5%

10 Singapore 1,754,800,889 789%

11 Thailand 1,487,351,334 -26%

12 Kenya 1,082,578,303 -26%

13 Canada 1,054,229,761 -60%

14 Vietnam 964,576,986 -20%

15 Mexico 881,465,845 26%

16 China 861,280,087 35%

17 Argentina 753,477,402 37%

18 France 660,149,745 108%

19 Brazil 572,357,179 -53%

20 Spain 567,479,472 267%

21 Turkey 538,660,655 -17%

22 Philippines 532,286,080 -1%

23 Sri Lanka 525,941,658 -10%

24 Venezuela 525,725,408 -4%

25 Saudi Arabia 439,156,666 -54%

26 Russia 429,817,974 47%

27 Ghana 424,270,236 -29%

28 United Arab Emirates 325,976,522 -21%

29 Germany 316,775,975 23%

30 Colombia 306,636,885 17%

31 Australia 293,725,559 104%

32 Oman 241,667,685 -7%

33 Egypt 224,665,573 -6%

34 Tanzania 201,893,881 -30%

35 Morocco 181,019,372 -5%

36 Sudan 159,651,862 -46%

37 Romania 152,018,647 -11%

38 Costa Rica 150,598,717 -57%

39 Iran 143,956,115 -28%

40 Kuwait 131,295,598 -27%

41 Italy 128,997,690 -47%

42 Uganda 120,262,031 -18%

43 Netherlands 113,836,918 -26%

44 Guatemala 112,911,133 -3%

45 Zimbabwe 105,009,915 -18%

46 Qatar 96,110,968 -24%

47 Serbia 95,469,348 -22%

48 Ecuador 94,262,562 -17%

49 Nicaragua 91,293,324 107%

50 Nepal 89,917,069 -13%

4

Featured markets

The pages that follow provide a snapshot of select markets for June 2014, with traffic growth and handset info. (To find out about any country not listed in the top 10, visit our campaign planner at planner.buzzcity.com.)

Mobile hotspots

The ‘Mobile Hotspot’ badge indicates those countries that we predict are likely to generate rapid and exponential growth in coming months, and with it, excellent value for advertisers.

All of these countries display a crucial mix of factors that we look for when we predict rapid growth (these could include falling cost of Internet access, heavy promotion of web services, cheaper handsets with better usability, and the rollout of new technologies – all leading to rapid consumer adoption).

Over the next year, we predict that there will be a lot more competition for advertising in these countries, and it would benefit advertisers greatly to take advantage now, before we start to see the inevitable increases in required bid rates that are likely to follow.

5

India

Summary

More than 6. 6 billion ads per month served to an audience of more than 124 million mobile surfers.

Carriers are active with off portal promotions of mobile content & OTT services (e.g. mobile money).

Top Phones: Nokia 26% , Samsung 23%

Traffic Distribution:

Featurephone : 51%

Smartphone : 44%

Desktop : 5%

Average CPC : 1.4 cent

6,730 6,617

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Jan-14 Mar-14 May-14 Jul-14 Sep-14

Mill

ion

s

39%

26%

22%

8%

1%

1%

Nokia

Samsung

Other Makers

Micromax

MAUI

SonyEricsson

Handset Maker

31%

28%

6%

5%

4%

2%

2%

Android OS

Nokia S40

Symbian OS

Samsung OS

Windows OS

Windows Mobile OS

MAUI OS

Handset OS

Glamour & Dating 50%

General Content

25%

Portals 18%

Entertainment & Lifestyle

6%

Community 1%

Channel

6

Indonesia

Summary

More than 5.7 billion ads a month are delivered to 78.4 million users.

Top Phones: Nokia 32%, Samsung 22% and BlackBerry 4%

Traffic Distribution:

Featurephone : 36%

Smartphone : 57%

Desktop : 6%

Tablet : 2%

Average CPC stabilised at USD 1.2 cents by end of September 2014

5,415 5,722

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14

Mill

ion

s

44%

24%

7%

6%

4%

2%

2%

Android OS

Nokia S40

Symbian OS

Windows OS

Blackberry OS

MTK / Nucleus OS

Sony Ericsson OS

Handset OS

32%

22%

4%

2%

2%

2%

1%

Nokia

Samsung

BlackBerry

MAUI

Lenovo

SonyEricsson

LG

Handset Maker

Glamour & Dating 41%

General Content 30%

Portals 17%

Entertainment & Lifestyle

10%

Community 2%

Channel

7

South Africa

Summary

1.4 billion banners served monthly to 20 million users

Top Phones: Nokia 66%, Samsung 14% and Blackberry 5%.

Traffic Distribution:

Featurephone 62%

Smartphone 34%

Desktop 3%

Tablet 1%

Average CPC stabilised at USD 3.6 cents by end of September.

1,764

1,431

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14

Mill

ion

s

56%

20%

6%

5%

2%

2%

Nokia S40

Android OS

Symbian OS

Blackberry OS

Windows OS

Windows Mobile OS

Handset OS

66%

14%

8%

5%

4%

1%

1%

Nokia

Samsung

Other Makers

BlackBerry

Huawei

Apple

LG

Handset Maker

Glamour & Dating 54%

General Content 26%

Portals 16%

Community 2%

Entertainment & Lifestyle

2%

Channel

8

Nigeria

Summary

1 billion banners served monthly to 14 million users

Top Phones: Nokia 61%, Samsung 3% and Blackberry 4%.

Traffic Distribution

Featurephone 73%

Smartphone 25%

Desktop 1%

Tablet 0.3%

Average CPC stabilised at USD 1.3 cents

1,403

1,028

-

200

400

600

800

1,000

1,200

1,400

1,600

Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14

Mill

ion

s

61%

25%

4%

3%

2%

2%

1%

1%

Nokia

Other Makers

BlackBerry

Samsung

MAUI

LG

HTC

HUAWEI

Handset Maker

52%

12%

7%

4%

2%

2%

1%

1%

Nokia S40

Android OS

Symbian OS

Blackberry OS

MTK / Nucleus OS

MAUI OS

Windows OS

Samsung OS

Handset OS

Glamour & Dating 45%

General Content 29%

Portals 21%

Entertainment & Lifestyle

3% Community

1%

Channel

9

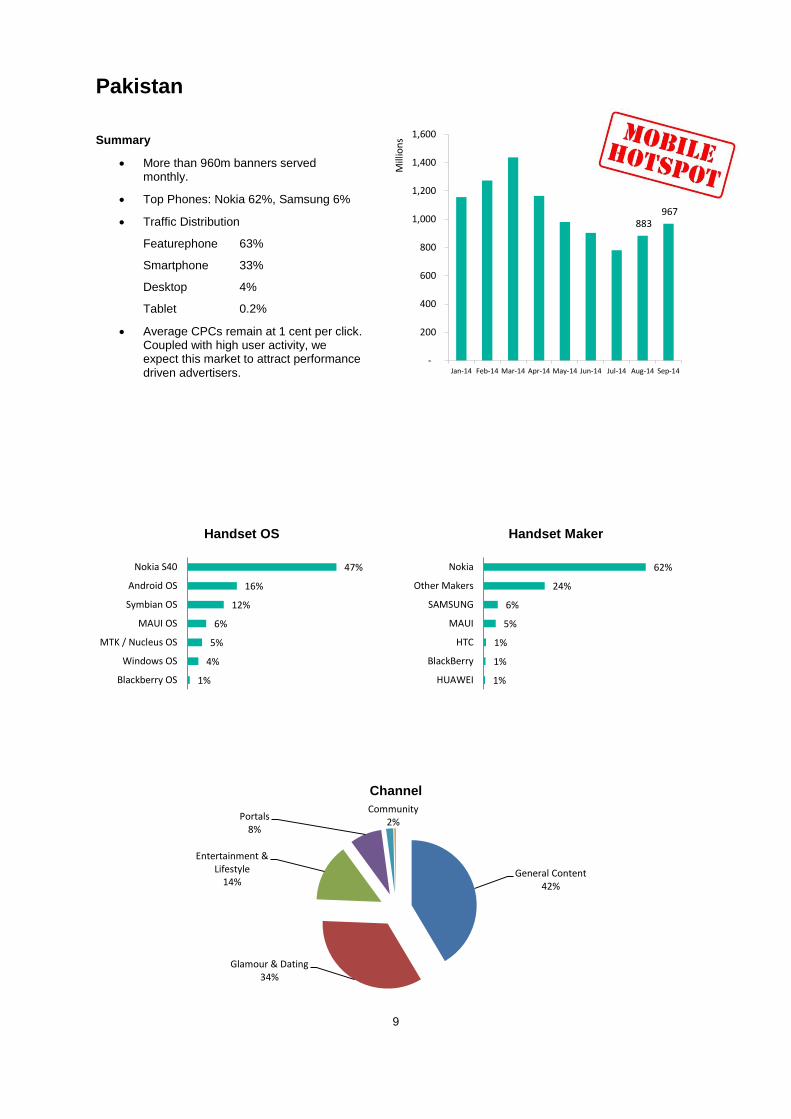

Pakistan

Summary

More than 960m banners served monthly.

Top Phones: Nokia 62%, Samsung 6%

Traffic Distribution

Featurephone 63%

Smartphone 33%

Desktop 4%

Tablet 0.2%

Average CPCs remain at 1 cent per click. Coupled with high user activity, we expect this market to attract performance driven advertisers.

883 967

-

200

400

600

800

1,000

1,200

1,400

1,600

Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14

Mill

ion

s

47%

16%

12%

6%

5%

4%

1%

Nokia S40

Android OS

Symbian OS

MAUI OS

MTK / Nucleus OS

Windows OS

Blackberry OS

Handset OS

62%

24%

6%

5%

1%

1%

1%

Nokia

Other Makers

SAMSUNG

MAUI

HTC

BlackBerry

HUAWEI

Handset Maker

General Content 42%

Glamour & Dating 34%

Entertainment & Lifestyle

14%

Portals 8%

Community 2%

Channel

10

910

813

-

100

200

300

400

500

600

700

800

900

1,000

Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14

Mill

ion

s

Malaysia

Summary

Monthly traffic in excess of 810 million banners served to 19.8 million users.

Top Phones: Samsung 42%, Lenovo 15% and Nokia 11%

Traffic Distribution

Featurephone 10%

Smartphone 81%

Desktop 3%

Tablet 6%

CPCs remain competitive at under 3 cents per click as advertisers take advantage of latent traffic.

42%

21%

15%

11%

4%

2%

1%

Samsung

Other Makers

Lenovo

Nokia

Apple

SonyEricsson

ALCATEL

Handset Maker

77%

7%

4%

3%

2%

1%

1%

1%

Android OS

Nokia S40

iOS

Symbian OS

Windows OS

Sony Ericsson OS

Windows Mobile OS

Blackberry OS

Handset OS

Glamour & Dating 51%

General Content

32%

Entertainment & Lifestyle

12%

Portals 2%

News & Information

2%

Channel

11

United States

Summary

Monthly traffic of 1 billion banners served to 19.3 million users.

Top Phones: Apple 23%, Samsung 19% and Nokia 8%

Traffic Distribution

Featurephone 18%

Smartphone 62%

Desktop 16%

Tablet 5%

CPCs remain competitive at 1.4 cents per click

731 691

-

200

400

600

800

1,000

1,200

Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14

Mill

ion

s

35%

23%

19%

8%

4%

2%

Other Makers

Apple

Samsung

Nokia

LG

Handset Maker

General Content

41%

Glamour & Dating 40%

Entertainment & Lifestyle

8%

Portals 5%

Community 4%

Channel

39%

23%

15%

6%

2%

1%

Android OS

iOS

Windows OS

Nokia S40

Samsung OS

Symbian OS

Handset OS

12

United Kingdom

Summary

Each month the network serves 705 million impressions to 12.5 million unique visitors in the UK

Top Phones: Samsung 27%, BlackBerry 23% and Apple 16%.

Traffic Distribution

Featurephone 2%

Smartphone 96%

Desktop 1%

Tablet 2%

CPCs remain competitive at 1.7 cents per click

811

705

-

200

400

600

800

1,000

1,200

1,400

Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14

Mill

ion

s

27%

23%

16%

16%

7%

4%

3%

1%

Samsung

BlackBerry

Other Makers

Apple

Nokia

LG

HTC

HUAWEI

Handset Maker

45%

23%

16%

4%

3%

2%

1%

Android OS

Blackberry OS

iOS

Nokia S40

Windows OS

Windows Mobile OS

Symbian OS

Handset OS

General Content

44%

Glamour & Dating 27%

Entertainment & Lifestyle

15%

Portals 8%

Community 3%

Channel

13

Bangladesh

Summary

More than 680 million banners served each month to 18 million users.

Top Phones: Nokia 46%, Samsung 8%

Traffic Distribution

Featurephone 57%

Smartphone 40%

Desktop 3%

Tablet 0.2%

CPCs remain at the minimum bid rate of 1 cent with high unmet demand.

652 686

-

100

200

300

400

500

600

700

800

Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14

Mill

ion

s

30%

23%

13%

10%

4%

3%

1%

Nokia S40

Android OS

Symbian OS

MAUI OS

MTK / Nucleus OS

Windows OS

Windows Mobile OS

Handset OS

46%

38%

8%

4%

2%

1%

Nokia

Other Makers

Samsung

MAUI

Micromax

SonyEricsson

Handset Maker

General Content

38%

Glamour & Dating 30%

Portals 26%

Entertainment & Lifestyle

4%

Community 2%

Channel

14

673

402

-

100

200

300

400

500

600

700

800

900

Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14

Mill

ion

s

Thailand

Summary

More than 400 million banners served each month to 7.9 million users.

Top Phones: Samsung 40%, Apple 21% and Nokia 10%

Traffic Distribution

Featurephone 5%

Smartphone 85%

Desktop 1%

Tablet 9%

Bid rates stabilised at 4.1 cents per click by end of September

40%

25%

21%

10%

1%

1%

Samsung

Other Makers

Apple

Nokia

ZTE

Lenovo

Handset Maker

67%

21%

5%

4%

1%

1%

Android OS

iOS

Nokia S40

Windows Mobile OS

Windows OS

Symbian OS

Handset OS

General Content 78%

Entertainment & Lifestyle

13%

Glamour & Dating 8%

Portals 1%

Channel

15

Feature: Online Videos

Introduction

We continue our study of our audience and their use of mobiles, particularly as a device for viewing videos. To investigate the potential of video and mobile across our network, we surveyed more than 5,400 respondents between 24th Aug & 1st Sept 2014.

Methodology

The survey consisted of multiple choice questions to cater to the media channel of choice, the mobile Internet. In many cases, respondents were asked questions offering multiple selections of multiple choices.

The survey was covered countries across The Americas, Asia, Africa and Western Europe. Particular focus was placed on benchmark markets for comparisons, where relevant, against previous studies.

Country September

Traffic

Argentina 288,225,610

Bangladesh 686,087,504

Brazil 195,905,879

Colombia 78,985,973

France 250,305,800

Ghana 116,401,516

Guatemala 30,879,480

India 6,616,767,175

Indonesia 5,722,077,470

Kenya 344,215,498

Malaysia 812,796,149

Mexico 349,289,128

Nigeria 1,027,607,217

Pakistan 967,412,337

Philippines 161,577,266

Saudi Arabia 133,366,607

Singapore 663,263,759

South Africa 1,430,514,862

Spain 292,008,670

Sri Lanka 157,950,254

Thailand 401,544,087

United Kingdom 705,312,526

United States 690,764,897

Venezuela 152,141,816

Vietnam 245,373,430

16

Overview

Many observers believe that mobile video will be a powerful channel for content and consequently, advertisers.

After all, more people are surfing with smartphones, connection speeds are improving and more affordable data

plans are being made available to consumers.

And then there is the public’s insatiable demand for content.

Against this background, we note that our 25 benchmark countries (for the surveys we run) are served by 3G &

4G Networks. Only Kenya and Vietnam do not yet have 4G services. All others are served with at least one

provider; most have at least two 4G providers.

In Indonesia, Internux, were first to market its 4G services, Bolt, in late 2013. Firstmedia is expected to launch its

4G service by end of 2014 and Smartfren Telecom by early of 2015. Kenya expects to launch 4G in 2015 and

Vietnam is expected to issue licences in 2015.

In the first two quarters of 2014, on-going operator campaigns across our network frequently targeted data

hungry users to offer them better surfing packages. During this period we also saw independent video sharing

sites running major membership drives.

By March 2014, reports from Ofcom in the UK suggest “… active 4G mobile subscriptions in the UK has risen

from 318,000 in Q1 2013 to over 6 million Q1 2014.”

The Big question: What do users watch and how will it affect content marketing?

17

Audience Highlights

1. 84% of mobile surfers on our network watch online videos. a. Most, 56%, download the videos they watch and b. 30% watch via online sharing sites. c. 15% also post their own videos.

i. Note: More Video capture apps are emerging - these typically interface with the built-in video recording app, and make it easy to post videos directly to popular social networking sites.

2. When viewing videos, mobiles are the most widely used device (75%) a. ( Our ‘Lifestyle Survey’ of Dec 2013 shows 86% access Internet with their phones) b. Notably, 79% watch on one device only and for 68%, this single device is mobile!

15%

30%

56%

0%

10%

20%

30%

40%

50%

60%

Yes, I also post my own. Yes, I watch online viavideo sharing sites.

Yes, I download videos.

Do you watch or download videos online?

11%

75%

10% 7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

PC / Laptop Mobile Phone Tablet SmartTV / Set-top-box

What do you use to view online videos?

18

3. Surfers prefer to watch. a. Full length movies & TV series 29% b. Clips or short videos 23% c. For free …43%

4. Many are avid viewers - a quarter (27%) watch often (at least once a day). a. 27% watch regularly – a few times a week b. 19% watch once or twice a month.

27%

27% 19%

11%

16%

How often do you watch videos on the Internet?

Often – at least once a day.

Regularly - a few times aweek

Sometimes - once ortwice a month

Rarely - a few times ayear

Never - I don’t watch videos online

28%

10% 9% 7%

25%

44%

13%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Full lengthmovies & TV

series

Live content(sports, news)

Usergenerated

content

Businessrelated videos

Clips / ShortVideos

Free videocontent

I don’t watch videos online

When watching videos online I prefer…

19

5. Online videos offer surfers the ability to consume (more) content on their own terms and forms the basis

of their preference

i. Online videos offer what I want immediately (34%) ii. The Internet offers more variety of videos (31%) iii. Surfers enjoy viewing what friends share online (20%)

6. Notably, the perceived value of variety, immediacy and personalisation outweigh the long held values of TV as a communal viewing experience.

30%

20%

16%

34%

12%

12%

16%

8%

11%

0% 5% 10% 15% 20% 25% 30% 35% 40%

Online videos offer what I want immediately.

I prefer the customised experience of online videos

I enjoy viewing what my friends share online

The Internet offers more variety of videos

TV offers better screen size

I prefer watching TV with friends and family

Watching TV is more relaxing and comfortable

TV is just more reliable

I get better quality with TV

Which of these statements apply to you?

20

Other Observations

1. We also deduce from the survey that,

Surfing Devices 2012 2013 2014

PC / Laptop 26% 10% 11%

Mobile 78% 86% 75%

Tablet 6% 7% 10%

Smart TV - 4% 7%

a. SmartTV ownership appears to have risen to 7% , while

b. PC ownership remains at approximately 11% having dropped from 2012

c. Tablet ownership has increased to at least 10% but does not seem to have grown as fast as PC’s have dropped.

2. Multi Device Surfing – present among 8% of respondents but not yet part of mainstream user behaviour.

21

Conclusions

1. Mobile video has undoubtedly become a mass consumer phenomenon! Among our audience, 84%

watch videos online and three quarters (75%) use their phones for viewing.

a. Multi device consumption is habitual among 8% of the respondents although we are yet to see

marked growth in the last 3 surveys.

2. At least a quarter (27%) of our audience watch online videos at least once a day and another 27%

watch online videos a few times a week.

3. Not surprisingly, free to view content is much sought after (43%) and this would typically be movies &

TV series (29%) or short videos (23%). We can expect, web videos and web series to play a crucial role

in how we experience entertainment in the very near future.

4. Most videos (56%) are downloaded for viewing but 30% is streamed from video sharing sites (including

premium video sharing sites with paid-content).

5. As with e-commerce, key factors driving the popularity of online videos are variety (34%), immediacy

(30%) and customisation (20%) – for consumers, it’s consumption on their own terms!

a. Notably the communal aspect of video sharing (16%) has rivalled if not outpaced the

communal value watching TV with family and friends (12%). (Not to be confused with replacing

TV – it is another experience of entertainment).

6. Comparisons with previous survey data suggests a growth of 3 percentage points in SmartTV ownership

and some three percentage point growth of tablet ownership in almost two years. Notably, the growth of

tablets is not as rapid as many had predicted.

7. The rise of online videos has led some brands to adapt to become producers and sponsors of their own

original content (and not just repurposing TV commercials). In many ways though, these brands follow

traditional ‘branding on TV’ - once that brand awareness and emotional connection have been

established, the brand runs retail marketing campaigns that encourage consumers to take a test drive

or get a promotional discount.

8. Digital video on the other hand promises the same emotional response with the practicality of direct

response. Advertisers can potentially, track spending directly to purchase in a way not possible with TV

and inspire engagement with mobile surfers.

9. Data and analytics will of course be important. But advertisers also need to be mindful that the user

experience of video is subjective – an emotional quality made more personal by the intimate nature of

mobiles. The only way to secure engagement is to actually create content that people care about or are

interested in - this though is not something to be quantified or measured.

22

Media Insights: Consumers & Advertising

The purpose of advertising is to share information. This information isn't always about a product and advertising

serves everything from businesses to social consciousness to get a message across. But in a fragmented

environment where the pubic consume content across numerous media, which has the ability to influence

consumers to act (or react) the most?

To investigate this we surveyed 5,100 mobile surfers across 25 countries between 11th Sept and 2

nd October

2014.

Respondents were asked of their general opinions of advertising; these were not cast against a particular set of

messages or advertising creatives. In this respect, responses reflect preconceived ideas of advertising. The basic

assumption is derived from findings of numerous external studies - the attention people pay to advertising is

influenced by how much they like to look at or notice advertising.

(Newspapers were not included in this study and forms part of another investigation).

Global Highlights

1. Mobile surfers have mixed feelings towards advertising – just as many have positive views of advertising as they do negative. Generally positive attitudes often coexist with unfavourable opinions about advertising.

2. Among the respondents, 60% agree with positive sounding opinions and 59% agree with the negatives.

a. While quarter (25%) feel advertising is informative, another quarter finds most ads are not relevant to them (23%).

b. Similarly, 22% claim to get value for money from advertised products while another 21% find advertising misleading.

c. Not surprisingly, 19% of respondents agree with positive and negative assertions on advertising.

25%

22%

24%

19%

27%

23%

21%

18%

Most advertising is informative.

I get value for money from advertised products.

In general, I feel I can trust advertising.

Products usually live up to advertiser claims

I ignore most of them.

Most are not relevant to me.

Most advertising is misleading.

Most are offensive and insult my intelligence.

How would you describe your attitude towards advertising?

23

3. Similarly, mobile surfers find all media just as invasive as they are actionable and attitudes are consistent across all media.

a. These responses suggest the influence the respective media have over surfers. Particularly influential are digital media and notably online video.

4. More ambivalence: Surprisingly, those who claim to distrust advertising take note of or act on ads as much as those who trust ads. This is also true for those who claim advertising ‘is just annoying’.

23%

13% 11% 11%

29%

23%

18%

23%

15%

26%

0%

5%

10%

15%

20%

25%

30%

35%

Media Influence

Actionable Ads

Invasive Ads

10% 9%

6% 6%

14% 14%

9% 10% 10% 12%

0%

5%

10%

15%

20%

25%

30%

35%

In which media are you most likely to act on or take notice of ads?

Trust Ads

Don’t Trust

They'reAnnoying

24

21%

18%

20%

18%

23%

How often do you use advertising to help make your purchase decisions?

Often - almost daily

Regularly - perhaps weekly

Sometimes - maybe monthly

Rarely - a few times a year

Never.

5. Despite their ambivalence, 77% of mobile surfers claim to use advertising to make purchasing decisions. 21% use advertising for purchasing decisions daily and another 18% weekly.

6. What do you dislike the most about ads?

34%

24%

28%

35%

22%

28%

There are too many

I don’t trust advertising

They are just annoying

I see the same ad too often

They are not relevant to me

They waste my time

25

Summary / Recommendations

1. Despite numerous mixed feelings about advertising, more than three quarters (77%) of mobile surfers

rely on advertising to make purchasing decisions.

2. While negative attitudes to advertising prevail (59%), consumers are generally well disposed to

advertising (60%).

a. Even those who claim they don’t trust advertising appear to be influenced by ads – they do act

or take notice of ads.

3. Digital media has become more influential than traditional media in generating consumer action or at the

very least strong opinions towards advertising.

4. But consumers have high expectations of advertising and the challenges facing marketers will only

increase. Advertisers should take note though, as a sizeable proportion of respondents feel

i. They see the same ad too often (35%)

ii. There are too many ads (34%)

iii. Advertisements are just annoying (28%)

iv. They are a waste of time (28%)

v. That the ads are not relevant (22%), and

vi. They just don’t trust advertising (24%).

5. If the purpose of advertising is to share information, then publishers too have a role in making sure that

information that is relevant is being shared with consumers. Internet advertising systems often allow

publishers to select advertisers and can help minimize the annoyance and irrelevance of any particular

advertisement – publishers must be diligent in their use of these tools to remain profitably ad supported.

6. The consumer may be ambivalent, but they are not passive. Consumers are behaving the same way

they have for ages. They perceive a need, seek information, assess the value of a product or service,

make a purchase, then use and evaluate it. What has changed is where they collect information and

share experiences – on mobile.

7. So if consumers don’t trust advertising, don’t just push promotion campaigns, build brand! Telling the

brand story becomes more important as consumers look for associative messages that are relevant to

them.

8. Consumers see the same ad too often: Advertisers will need to vary the message and also the ad

format – look beyond banner advertising to other rich media and video formats. Marketers need to look

to rich media or video formats to deliver emotion and engagement beyond the direct response of a

banner.

9. Engagement is of course specific to a brand or product. Marketers will want to consider measuring: -

a. Visit Frequency – how often consumers return is a key reflection of the value they get from a

site or application. The goal is to identify the pattern that is most relevant for your service and

monitor consumer usage against that pattern.

b. Primary Usage - If consumers are consistently performing core actions (browsing products,

creating a wish list, creating product alerts) it is a good indication of the value they derive.

c. Active Time - the total time a user spends on primary usage of the site.

10. A combination of these core metrics (at the very least) helps to uncover the level of user engagement for

any application or online service. To get to the combination that is right requires some thought and it

may not be easy, but it’s essential if marketers want to continuously delight users and in turn increase

their lifetime value.

26

BuzzCity Pte Ltd 1 Lorong 2, Toa Payoh

#02-03, Yellow Pages Building Singapore 319637

+65 6395 3700

General enquiries and feedback [email protected]

Partnerships and Business Development [email protected]

Advertising enquiries [email protected]

For a full list of our global offices and local representation, please visit www.buzzcity.com