Embed Size (px)

Citation preview

1

The Board’s Fiduciary Role: Moving Beyond Oversight

Susan S. Meier, Senior Governance Consultant September 13, 2016

© 2016. Not to be distributed or reproduced without the express permission of BoardSource.

2

BoardSource

• Inspires and supports excellence in nonprofit governance and board and staff leadership

• Is the premier source of cutting-edge thinking and resources related to nonprofit boards

• Engages and develops the next generation of board leaders

3

Susan Meier • Senior Governance

Consultant at BoardSource • Principal, Meier and

Associates • Former Vice President of

Consulting & Training at BoardSource

• 28+ years in the nonprofit sector

• Board member experience 4

Objectives

To increase our understanding of:

the fiduciary role of a nonprofit board of directors the range of systems, policies, committees, and documents that nonprofits should have in place to help ensure appropriate financial oversight the distinction between program monitoring and evaluation and the board’s role in each the basics of good legal and ethical oversight

5

Agenda Fiduciary Oversight, Transparency and Confidentiality

Financial Oversight

Program Monitoring and Evaluation

Legal & Ethical Oversight

6

Poll Question 1: What does “fiduciary” even mean?

A. A person who holds something in trust for another

B. A trustee

C. A person or institution given the power to act on behalf of another in situations that require great trust, honesty and loyalty

D. All of the above

7

I. Fiduciary Oversight, Transparency and Confidentiality

Transparency & IRS Form 990

Part VI: Governance, Management, and Disclosure Part VII: Compensation of Officers, Directors, Trustees, Key Employees, Highest Compensated Employees, and Independent Contractors

on of Officers,oyees, Highest Compendependent Contractors

9

Form 990 - Governance 1. Number of voting board members 2. Family or business relationships between officers, directors, trustees,

key employees 3. Significant changes to organizational documents 4. Contemporaneous minutes of board and committee meetings 5. Process to review 990 6. Conflict of Interest Policy 7. Whistleblower Policy 8. Document Retention and Destruction Policy 9. Process for determining compensation for CEO, officers, key

employees 10. Public availability of 1023 or 1024

10

Form 990 - Compensation • Salary and wages, bonuses • Severance payments, deferred payments, retirement

benefits, fringe benefits • Other financial arrangements or transactions such as

personal vehicles, meals, housing, personal and family educational benefits, below-market loans, payment of personal or family travel, entertainment, and personal use of the organization’s property

11

Executive Compensation Safe Harbor

• Review and approval by governing body or compensation committee (without conflict of interest with respect to a compensation arrangement)

• Use of comparable data • Contemporaneous documentation and

recordkeeping of deliberations and decisions

12

Poll Question 2

Does your full board review your IRS 990 before it is filed?

a) Yes b) No c) Not sure

d?

13

Beyond the Form 990: Transparency

The Basics • Open communication • All board members have access to the same

information

External Transparency

• Annual reports, board and staff lists, and 990 on Web site

• Proactive sharing of good and bad news

Being Proactive

• Hard questions are asked • Hard truths are spoken

14

Transparency vs. Confidentiality

• Board confidentiality

• Dealing with a breach

• Electronic communications

14 14

15

II. Financial Oversight

16

Can you repeat that, please?

16

• “sell the forward spread

and buy protection on the tightening move,”

• “use indices and add to existing position,”

• “go long risk on some belly tranches especially where defaults may realize” and

• “buy protection in rallies and turn the position over to monetize volatility.”

Investment Strategy Quotes New York Times, 1/26/2012

17

Poll Question 3

Which financial statements does your full board of directors review regularly? (Check all that apply.)

Annual budget Budget-to-actual statements Cashflow statements Balance sheets Other

18

Basic Questions Every Board Member Should Be Asking

• Is our financial plan consistent with our strategic plan? • Have we run a gain or a loss? • Is our projected cash flow adequate? • Do we have sufficient reserves? • Are any specific expense areas rising faster than their

sources of income? • Are our key expenses, especially salaries and benefits,

under control? • Are we meeting guidelines and requirements set by our

funders?

19

Assess Financial Performance

Learn about overall financial health.

• Liquidity • Revenue and expense activity • Status of significant investments • Reserves • Compliance with donor

restrictions where applicable

s

20

Assess Financial Performance (cont’d)

Board “Must Haves”

Reserve policy

Diversified revenues

Investment policy and strategy to guide decision making

Access to investment expertise, not just on the board but in a third party

21

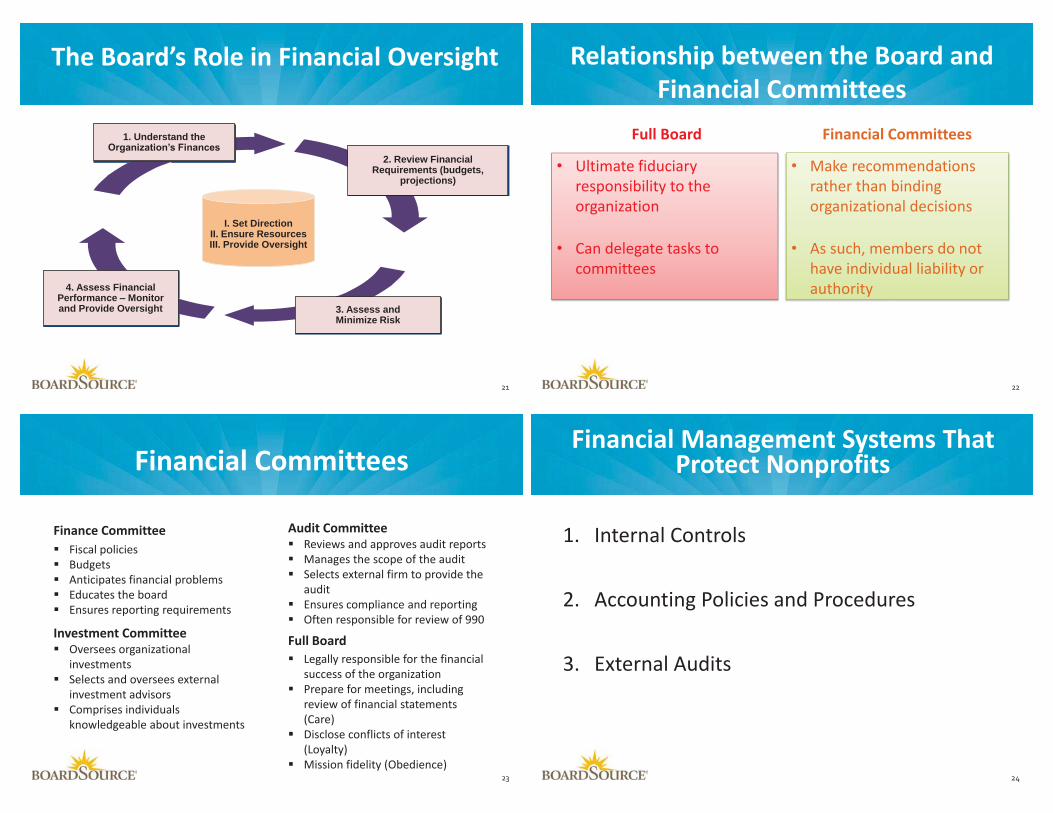

1. Understand the Organization’s Finances

4. Assess Financial Performance – Monitor and Provide Oversight 3. Assess and

Minimize Risk

2. Review Financial Requirements (budgets,

projections)

I. Set Direction II. Ensure Resources III. Provide Oversight

The Board’s Role in Financial Oversight

22

Relationship between the Board and Financial Committees

Full Board

• Ultimate fiduciary responsibility to the organization

• Can delegate tasks to committees

Financial Committees

• Make recommendations rather than binding organizational decisions

• As such, members do not have individual liability or authority

23

Fiscal policies Budgets Anticipates financial problems Educates the board Ensures reporting requirements

Financial Committees

Finance Committee Audit Committee

Full Board

Reviews and approves audit reports Manages the scope of the audit Selects external firm to provide the audit Ensures compliance and reporting Often responsible for review of 990

Oversees organizational investments Selects and oversees external investment advisors Comprises individuals knowledgeable about investments

Legally responsible for the financial success of the organization Prepare for meetings, including review of financial statements (Care) Disclose conflicts of interest (Loyalty) Mission fidelity (Obedience)

Investment Committee

24

Financial Management Systems That Protect Nonprofits

1. Internal Controls

2. Accounting Policies and Procedures

3. External Audits

25

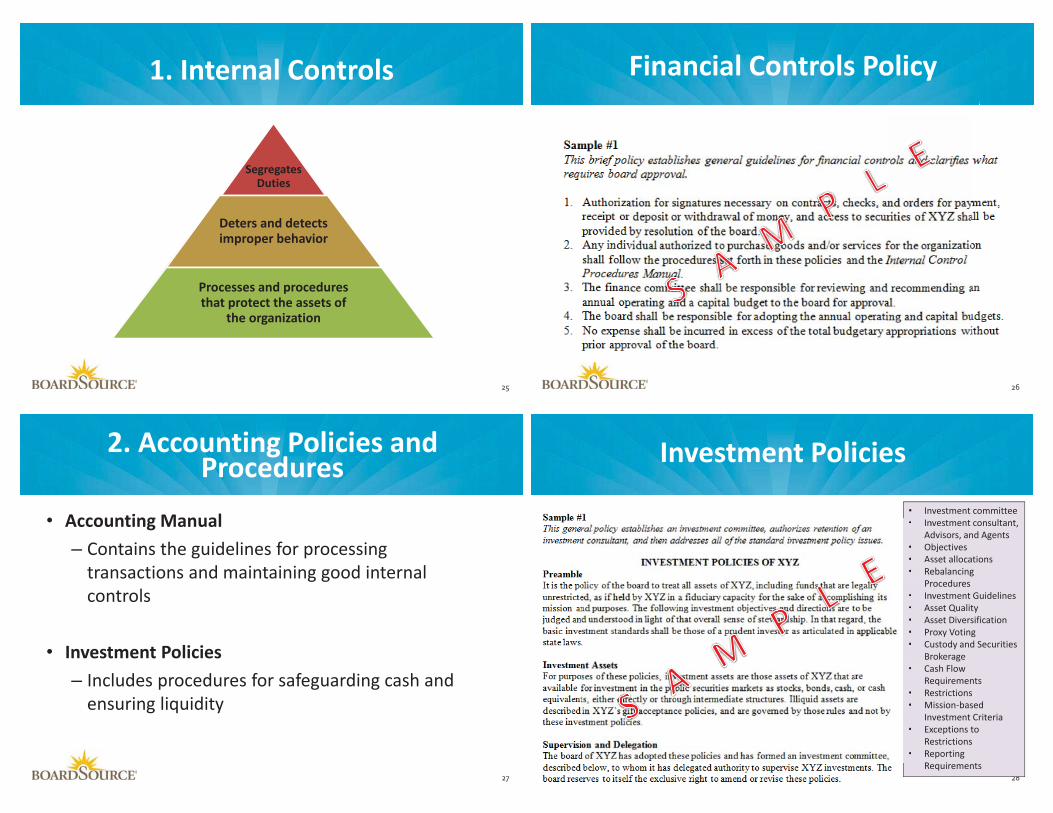

1. Internal Controls

Segregates Duties

Deters and detects improper behavior

Processes and procedures that protect the assets of

the organization

26

Financial Controls Policy

27

2. Accounting Policies and Procedures

• Accounting Manual

– Contains the guidelines for processing transactions and maintaining good internal controls

• Investment Policies

– Includes procedures for safeguarding cash and ensuring liquidity

28

Investment Policies

• Investment committee • Investment consultant,

Advisors, and Agents • Objectives • Asset allocations • Rebalancing

Procedures • Investment Guidelines • Asset Quality • Asset Diversification • Proxy Voting • Custody and Securities

Brokerage • Cash Flow

Requirements • Restrictions • Mission-based

Investment Criteria • Exceptions to

Restrictions • Reporting

Requirements

•••

•

••

•

•

• InAdObAsRePrInAsAs

•

•••

•••

29

3. External Audit

• Process to ensure that financial statements accurately reflect financial position

• Adds a level of oversight and scrutiny to ensure the organization is on solid footing

30

III. Program Monitoring and Evaluation

31

Monitoring versus Evaluation

• Monitoring – Are we doing what we said we would do?

• Evaluation – Are we doing the right thing?

•

•

32

Basic Questions

• Is this program or service making enough of a difference for the people served?

• Is it cost-effective? • To what extent is it still needed or wanted? • Is there a more effective and efficient way

to meet the need? • What is another way to address the issue

we are trying to respond to?

33

Use of Dashboards: Why and How?

Source: Lawrence M. Butler, author of The Nonprofit Dashboard: Using Metrics to Drive Mission Success, Second Edition (BoardSource, 2012).

What is the value of using a dashboard?

Saves time Tracks progress Sheds light on system dynamics Points up potential problems Reveals patterns Expands board members’ comfort zones Develops a shared knowledge base Focuses information from a governance perspective Reinforces board oversight

What approaches can be used to define dashboard metrics?

Outcomes Mission as spine Strategic initiatives or drivers of success Risk factors Services and resources

34

Graphic Dashboard

Source: Lawrence M. Butler author of The Nonprofit Dashboard: A Tool for Tracking Progress (BoardSource, 2007).

35

IV. Legal and Ethical Oversight

Legal Duties of the Board and Board Members

Duty of Care Duty of Loyalty Duty of Obedience

37

• Duty of Care – Using your best judgment – Actively participating, paying attention – Asking pertinent questions

• Duty of Loyalty – Avoiding conflicts of interest – Putting aside personal and professional interests

• Duty of Obedience – Staying true to the organization’s mission – Obeying the law, both public and organizational

Exists when a board member, officer, or management employee has a personal interest that is in conflict with the interests of the organization, such that he or she may be influenced by this personal interest when making a decision for the organization.

Conflict of Interest

39

Conflict-of-Interest Policy Full disclosure Persons in decision-making roles make known their connection with groups or individuals doing business with a nonprofit. Information provided annually.

Abstention Abstain from voting on any actual or potential conflict- of-interest transaction. Record Recusal is noted in the minutes.

40

Other Areas to Beware

• Whistleblower • Document Retention & Destruction • Employment Taxes • Self-dealing & excessive benefit e benefit

Minimizing Risk

1. Timely submission of IRS 990 2. Transparency 3. Basic Financial literacy for all board members 4. Conflict of Interest Policy 5. Approval of compensation for CEO and senior staff 6. Regular review of bylaws, policies, and insurance 7. Dashboards 8. Assessments 9. Informed Board Members 10. Engaged governance and decision-making

42

Thoughts, Questions…

43

Resources www.boardsource.org

44

Mark Your Calendars: Upcoming Webinars • The Board Building Cycle

– Tuesday, March 24, 2015: 1:00 – 2:00pm Eastern • Pivotal Points: The Board’s Role in Leadership

Transitions – Friday, May 8, 2015: 1:00 – 2:00pm Eastern

• The Board’s Role in Fundraising – Monday, June 2, 2015: 12:00 – 1:00 Eastern

45

Mark Your Calendars: One More 2016 Webinar

• The Board’s Role in Advocacy – Thursday, October 20, 2016: 1:00 – 2:00pm Eastern

46

BoardSource 750 9th St NW, Ste 650 Washington, DC 20001

Phone (202) 349-2500

Web site: www.boardsource.org