Embed Size (px)

Citation preview

The “Blueprint” is Born:

Broadband Policy in the 2009 Economic Stimulus

Legislation

1

“A Blueprint for Big Broadband”An EDUCAUSE White Paper Issued January 2008

Key Recommendation:The U.S. Should allocate $33 Billion to

a new Universal Broadband Fund (UBF) to subsidize the construction

of 100 Mbps local broadband connections to every home and

business.

www.educause.edu/ir/library/pdf/EPO0801.pdf

2

Why Did Congress Include Broadband Funding in the Stimulus Act?1. Broadband demand exploding; broadband

investment dawdling.

2. U.S. falling behind in international rankings of broadband capabilities.

3. Industry (except for Verizon) investing less than what America needs (microeconomics trumping macroeconomics).

4. Need to stimulate the economy and create jobs.

3

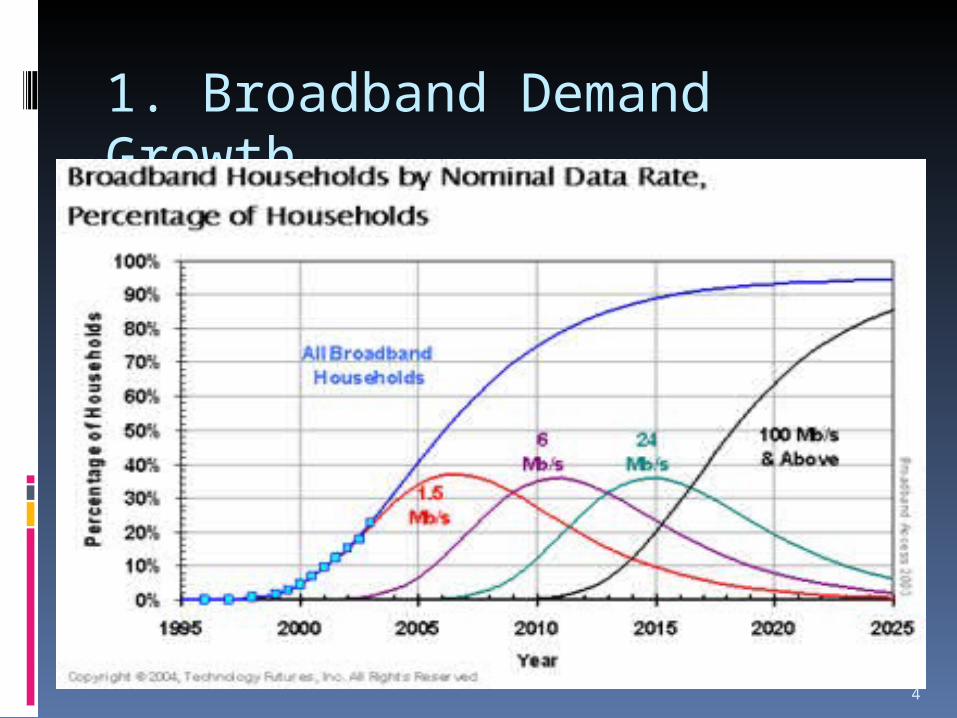

1. Broadband Demand Growth

4

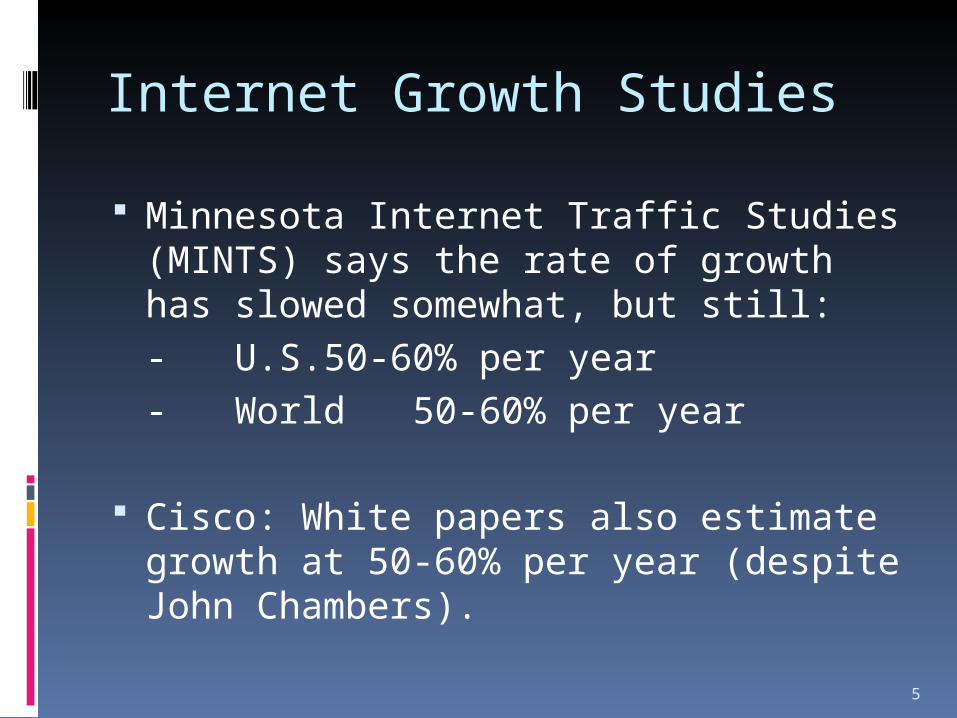

Internet Growth Studies

Minnesota Internet Traffic Studies (MINTS) says the rate of growth has slowed somewhat, but still:

- U.S. 50-60% per year- World 50-60% per year

Cisco: White papers also estimate growth at 50-60% per year (despite John Chambers).

5

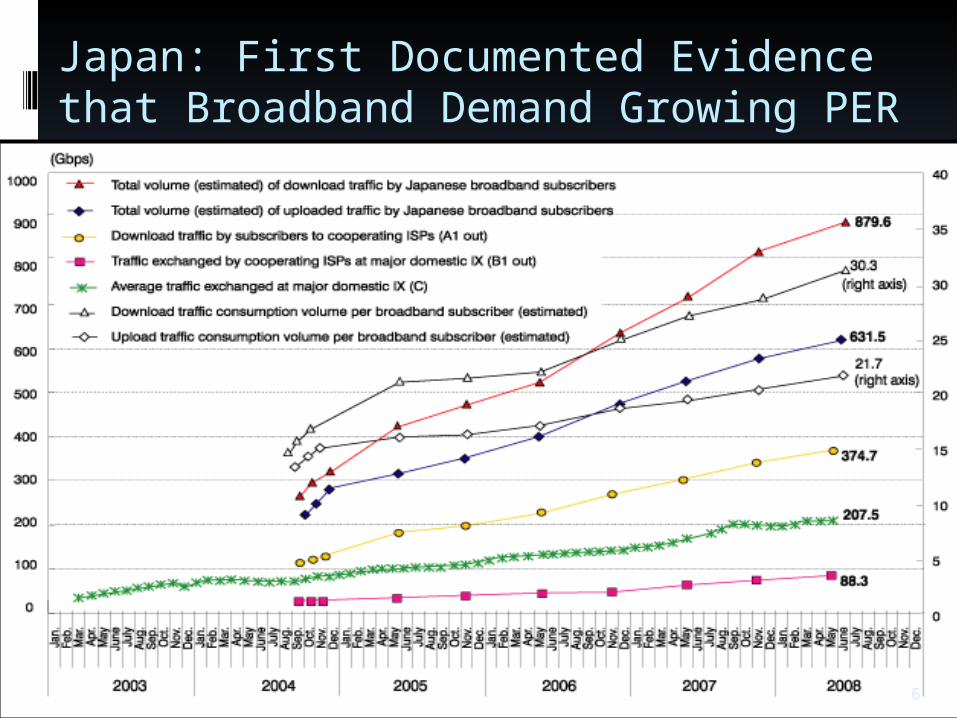

Japan: First Documented Evidence that Broadband Demand Growing PER SUBSCRIBER.

6

United States Broadband Subscribership: 2002-2008

7

2. U.S. Falling Behind in International Broadband Rankings. BB Subscriber Growth: US/Europe

8

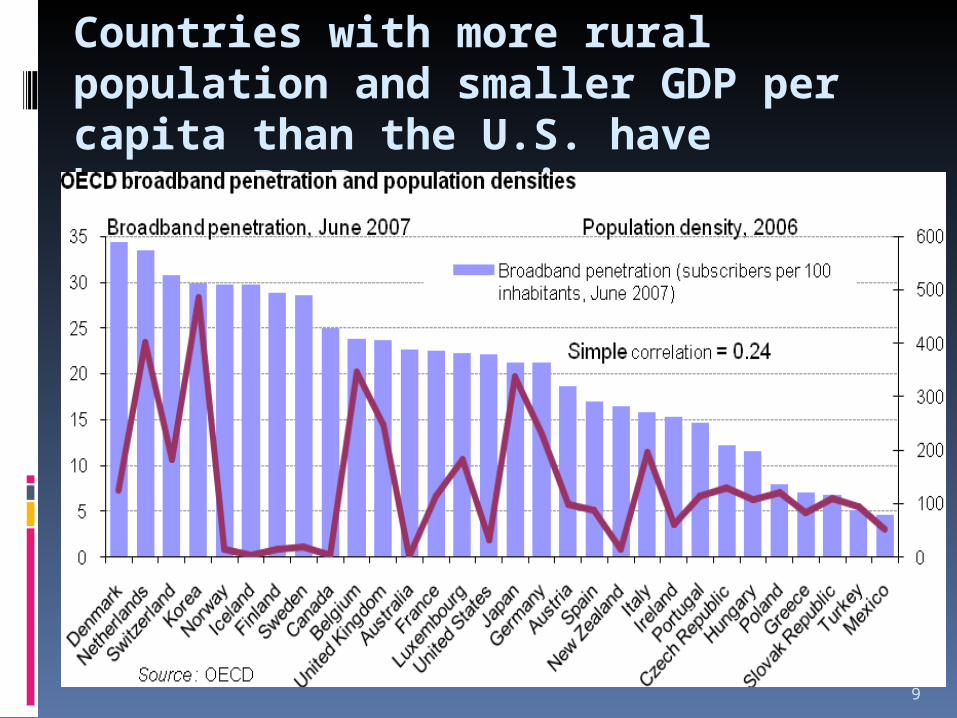

Countries with more rural population and smaller GDP per capita than the U.S. have better BB Penetration.

9

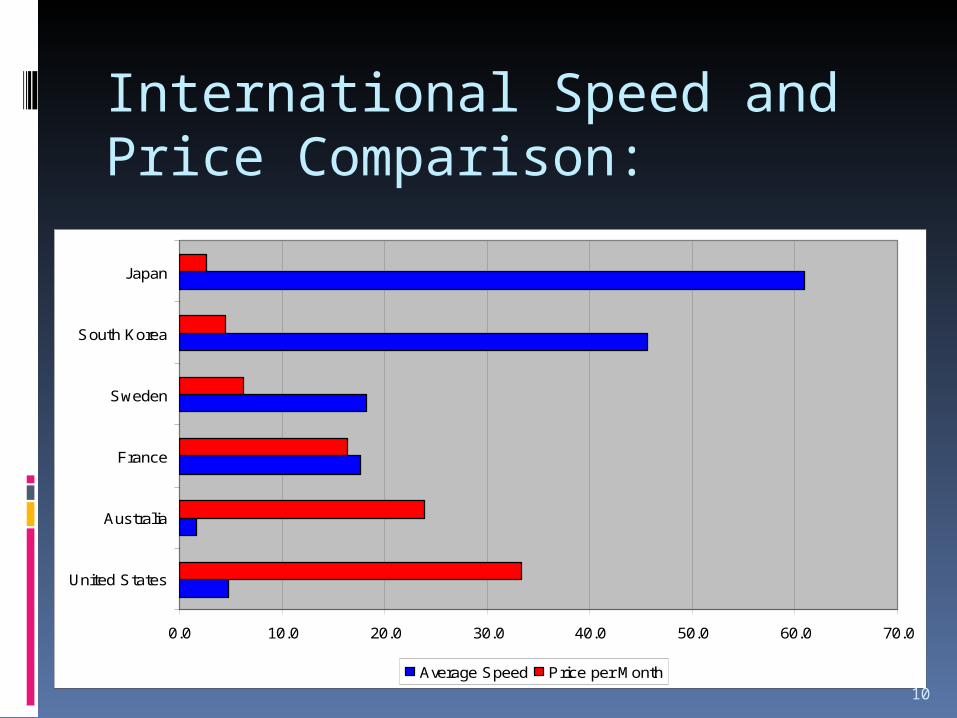

International Speed and Price Comparison:

0.0 10.0 20.0 30.0 40.0 50.0 60.0 70.0

United States

Australia

France

Sweden

South Korea

Japan

Average Speed Price per Month

10

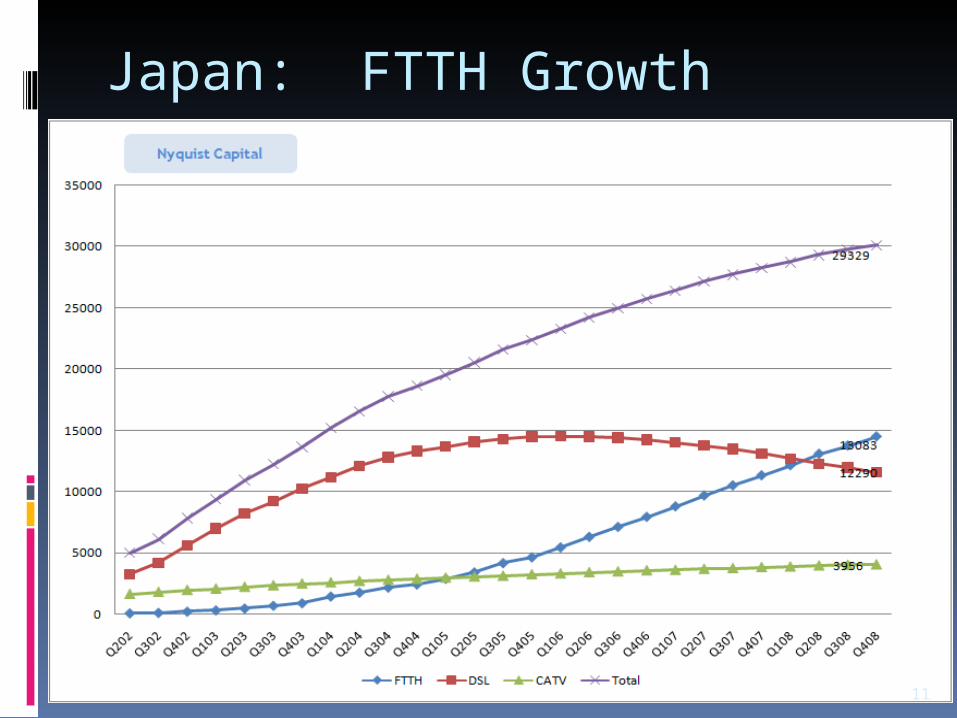

Japan: FTTH Growth

11

3. Industry Reluctant to Invest in Broadband. Is this why??

"Today, fiber serves no purpose," Philippe Capron, chief financial officer

of Vivendi. "There is no new revenue stream and no supplemental service

to offset the considerable investment. All that it does is to encourage the

illegal downloading of films.”

“Expanding broadband to bail out economies,” by Eric Pfanner; February 25, 2009; International Herald Tribute, available at http://www.iht.com/articles/2009/02/25/technology/broadband.php?page=1

12

Cable’s “Long-term” Vision

Rouzbeh Yassini: The "Father of the Cable Modem" praised the cable industry's DOCSIS 3.0 modems:

It's "a great technology... a technology that will go on for five, six, seven, or even eight years.” [!]

http://www.lightreading.com/document.asp?doc_id=172668&site=cdn

13

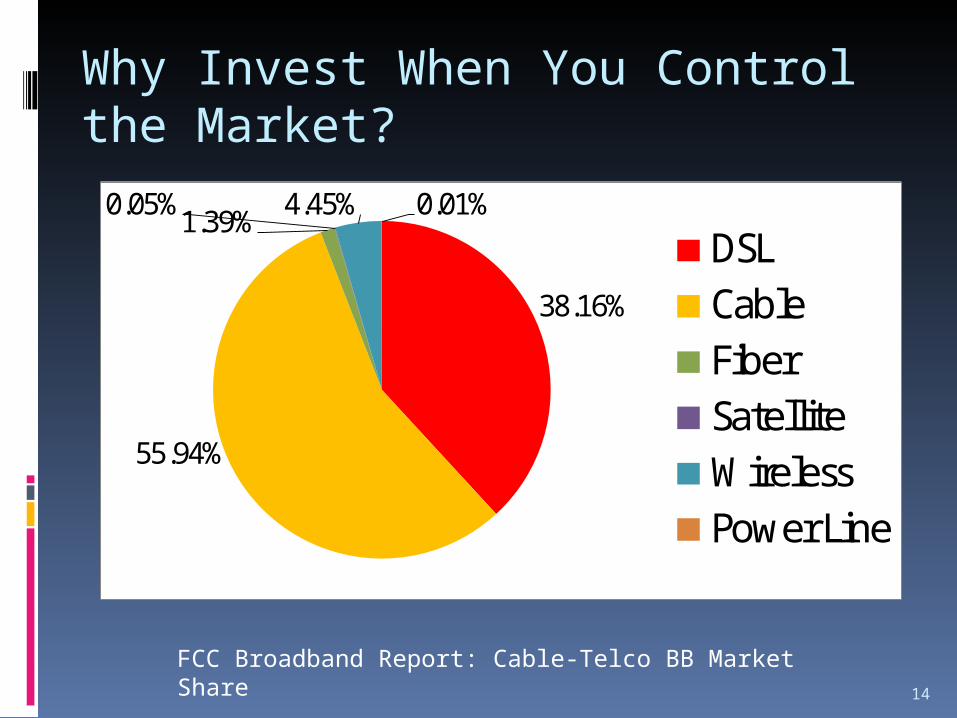

Why Invest When You Control the Market?

38.16%

55.94%

1.39%0.05% 4.45% 0.01%

DSLCableFiberSatelliteWirelessPower Line

FCC Broadband Report: Cable-Telco BB Market Share

14

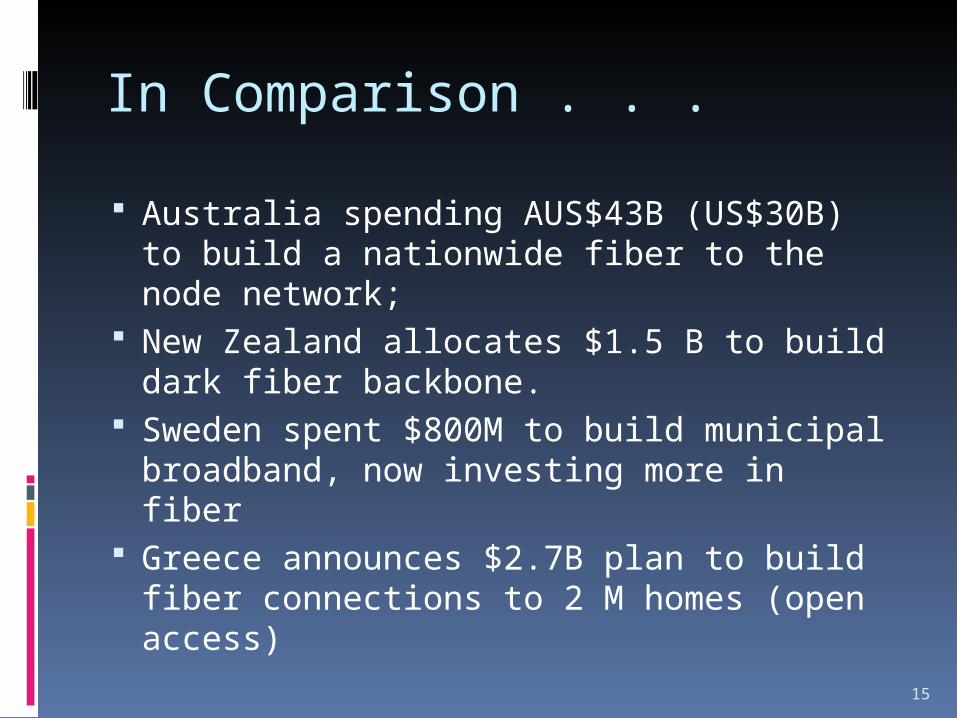

In Comparison . . .

Australia spending AUS$43B (US$30B) to build a nationwide fiber to the node network;

New Zealand allocates $1.5 B to build dark fiber backbone.

Sweden spent $800M to build municipal broadband, now investing more in fiber

Greece announces $2.7B plan to build fiber connections to 2 M homes (open access)

15

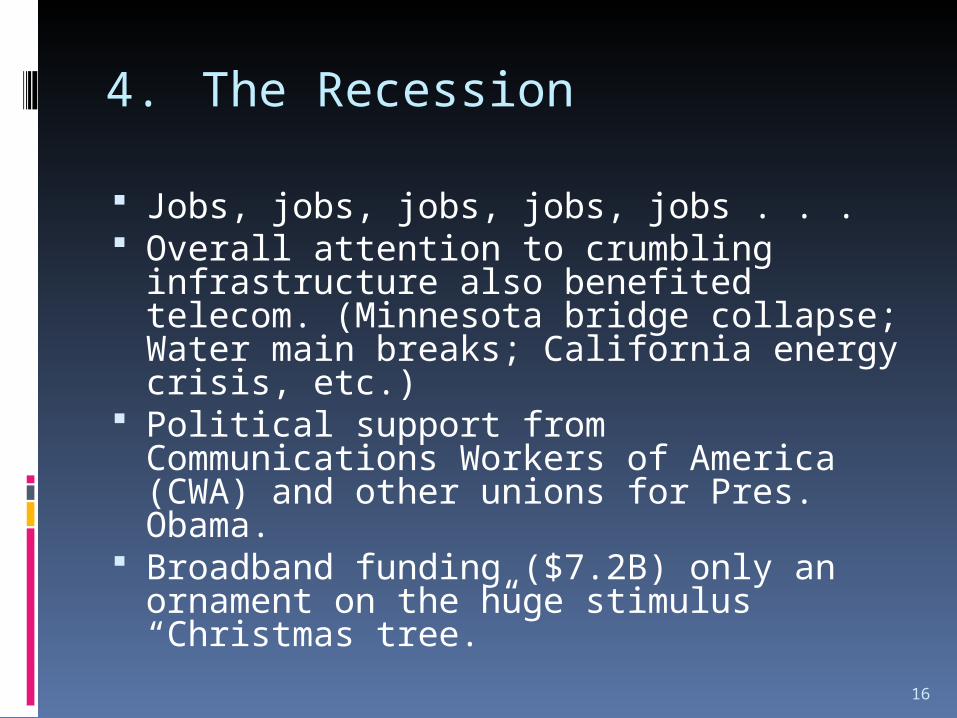

4. The Recession

Jobs, jobs, jobs, jobs, jobs . . . Overall attention to crumbling

infrastructure also benefited telecom. (Minnesota bridge collapse; Water main breaks; California energy crisis, etc.)

Political support from Communications Workers of America (CWA) and other unions for Pres. Obama.

Broadband funding ($7.2B) only an ornament on the huge stimulus “Christmas tree.”

16

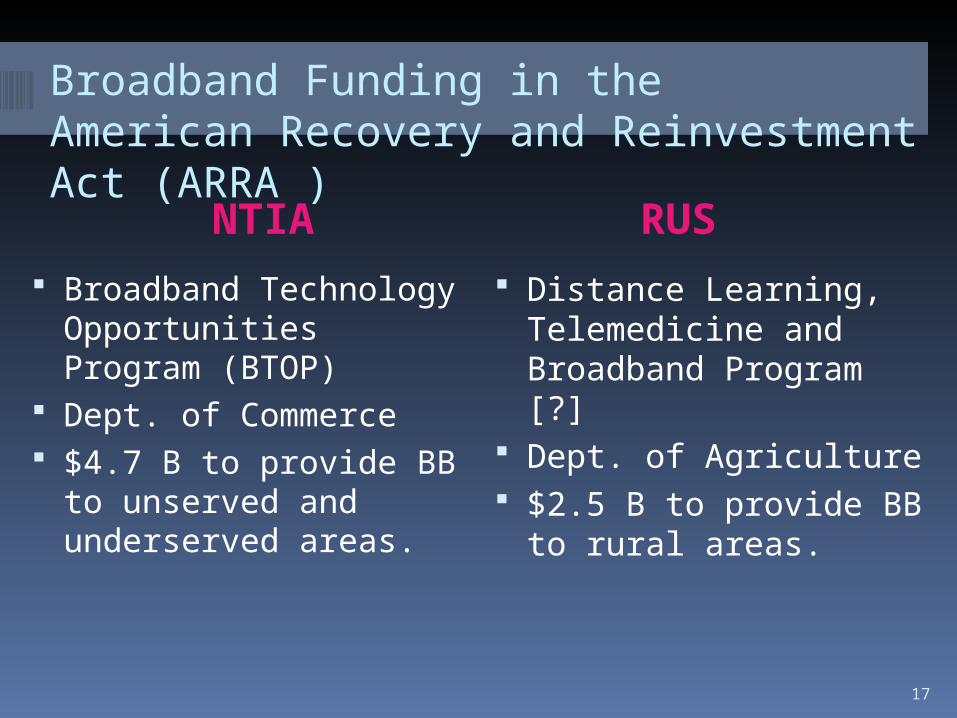

Broadband Funding in theAmerican Recovery and Reinvestment Act (ARRA )

NTIA RUS Broadband Technology

Opportunities Program (BTOP)

Dept. of Commerce $4.7 B to provide BB to

unserved and underserved areas.

Distance Learning, Telemedicine and Broadband Program [?]

Dept. of Agriculture $2.5 B to provide BB

to rural areas.

17

ARRA Summary

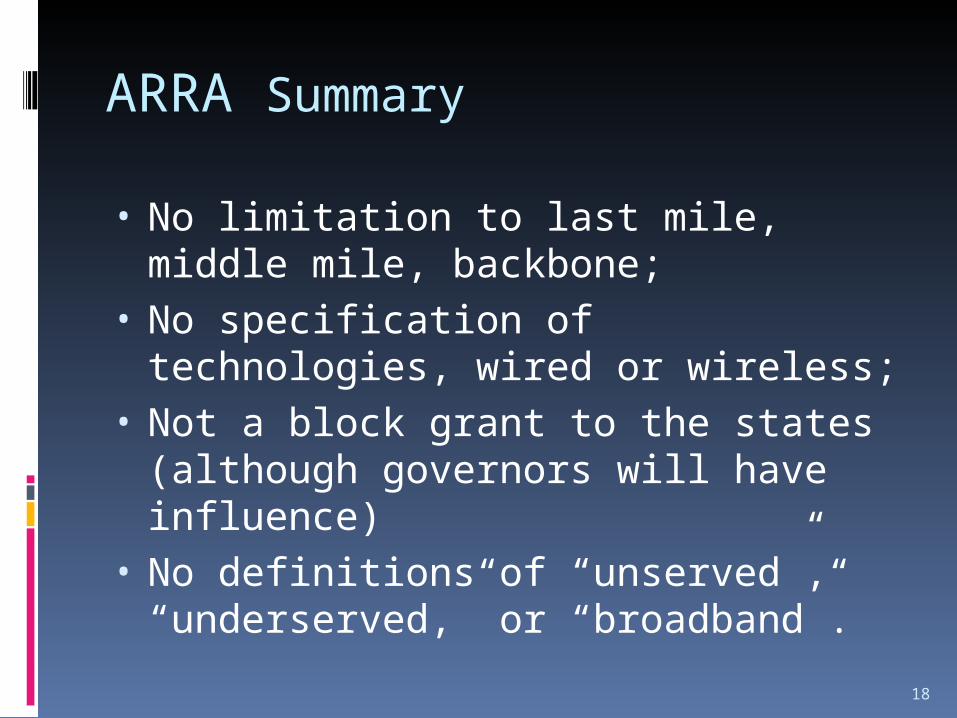

• No limitation to last mile, middle mile, backbone;

• No specification of technologies, wired or wireless;

• Not a block grant to the states (although governors will have influence)

• No definitions of “unserved”, “underserved,” or “broadband”.

18

NTIA Funding Breakdown$ 200 Million

$ 250 Million

$ 350 Million

$ 10 Million

$ 141 Million

$ ~3.75 Billion

Expanding public computer center capacity (“at least”)

Stimulate broadband demand and usage (“at least”)

Broadband Mapping (“up to”)

Inspector General for audits

Administrative Expenses

Broadband Grants

19

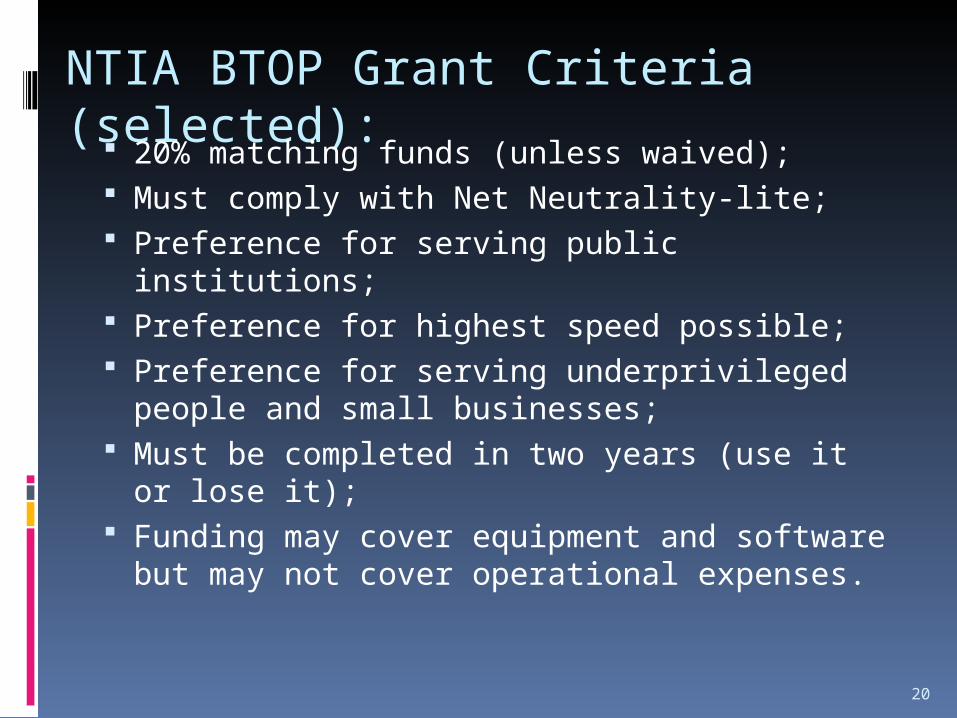

NTIA BTOP Grant Criteria (selected): 20% matching funds (unless waived);

Must comply with Net Neutrality-lite; Preference for serving public institutions; Preference for highest speed possible; Preference for serving underprivileged

people and small businesses; Must be completed in two years (use it or

lose it); Funding may cover equipment and software

but may not cover operational expenses.

20

RUS Broadband Program Criteria (Selected)

Loans, loan guarantees or grants At least 75% of each project’s service

territory must be a rural area w/o sufficient high-speed broadband;

Preference for former RUS borrowers; Preference for applications permitting

multiple service providers.

21

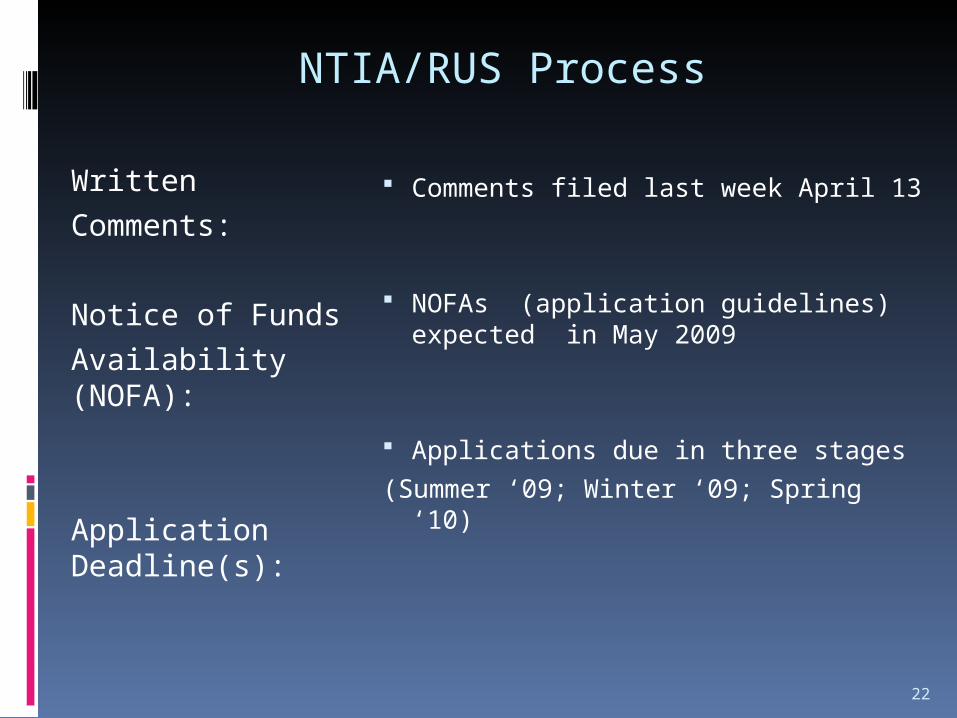

NTIA/RUS Process

Written

Comments:

Notice of Funds

Availability (NOFA):

Application Deadline(s):

Comments filed last week April 13

NOFAs (application guidelines) expected in May 2009

Applications due in three stages

(Summer ‘09; Winter ‘09; Spring ‘10)

22

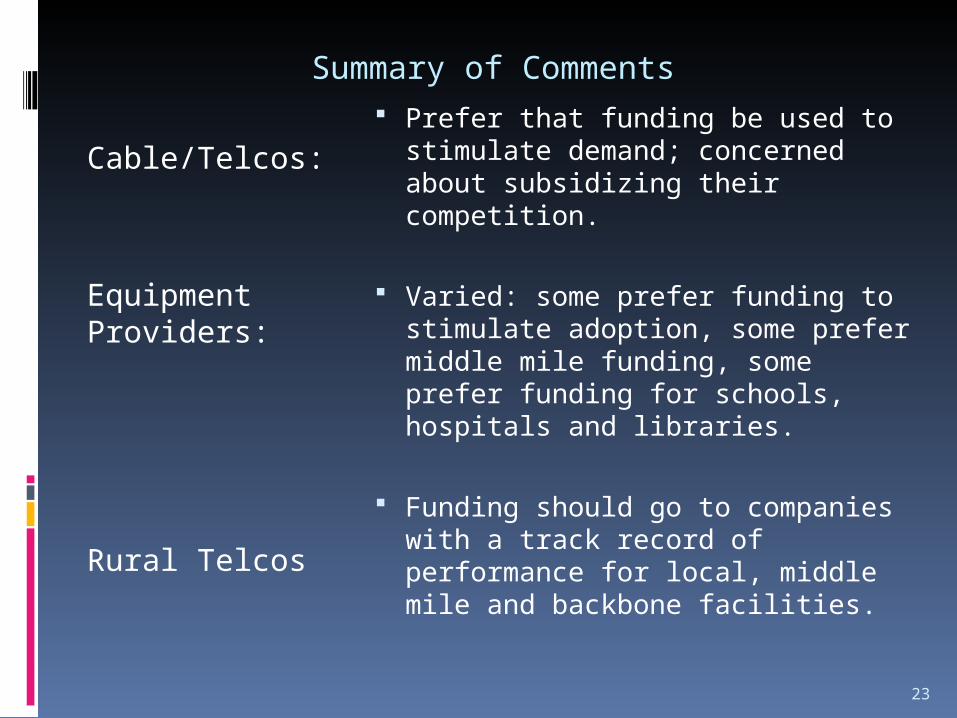

Summary of Comments

Cable/Telcos:

Equipment Providers:

Rural Telcos

Prefer that funding be used to stimulate demand; concerned about subsidizing their competition.

Varied: some prefer funding to stimulate adoption, some prefer middle mile funding, some prefer funding for schools, hospitals and libraries.

Funding should go to companies with a track record of performance for local, middle mile and backbone facilities.

23

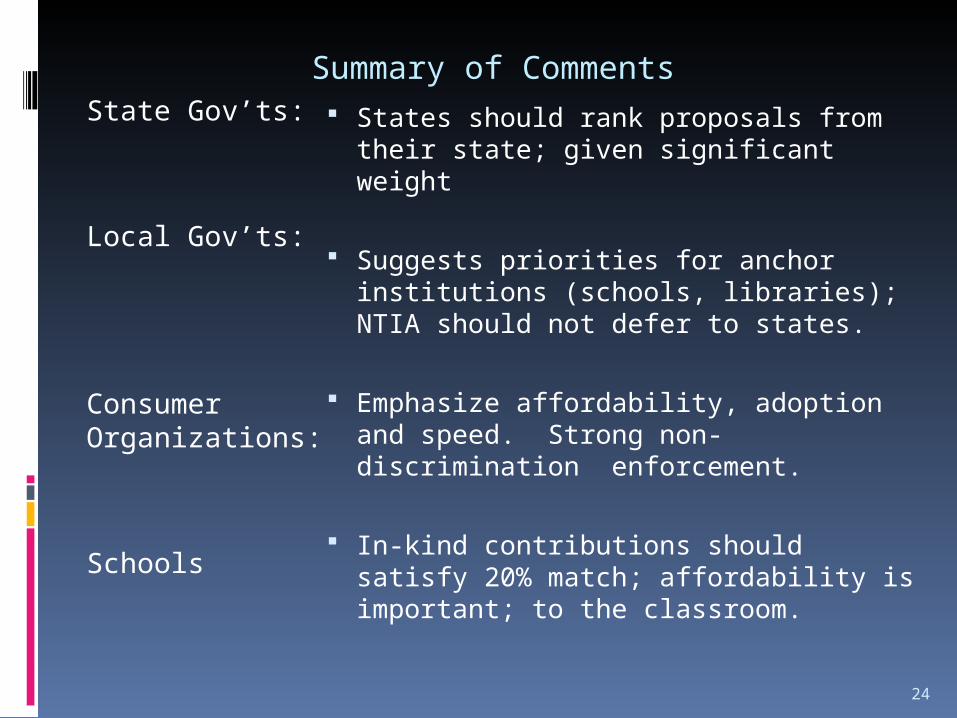

Summary of CommentsState Gov’ts:

Local Gov’ts:

Consumer Organizations:

Schools

States should rank proposals from their state; given significant weight

Suggests priorities for anchor institutions (schools, libraries); NTIA should not defer to states.

Emphasize affordability, adoption and speed. Strong non-discrimination enforcement.

In-kind contributions should satisfy 20% match; affordability is important; to the classroom.

24

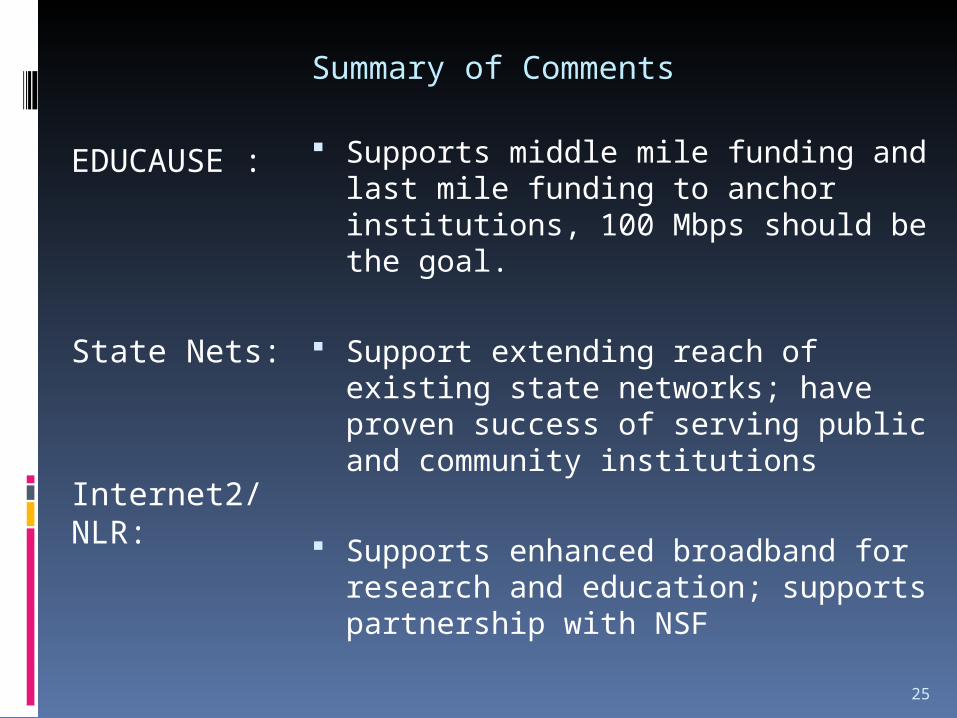

Summary of Comments

EDUCAUSE :

State Nets:

Internet2/NLR:

Supports middle mile funding and last mile funding to anchor institutions, 100 Mbps should be the goal.

Support extending reach of existing state networks; have proven success of serving public and community institutions

Supports enhanced broadband for research and education; supports partnership with NSF

25

Key Issues to Watch

Openness:

Matching Funds:

Middle Mile:

RUS Grants or Loans:

Will NTIA/RUS go beyond the FCC’s Four Principles? Will they apply Openness requirements to private networks (such as research and education networks)?

Will In-kind contributions be permitted?

Will funding for middle mile connections be permitted, or only retail services to consumers?

RUS has traditionally given low-interest loans, but not effectively. Will RUS award some funding in grants?

26

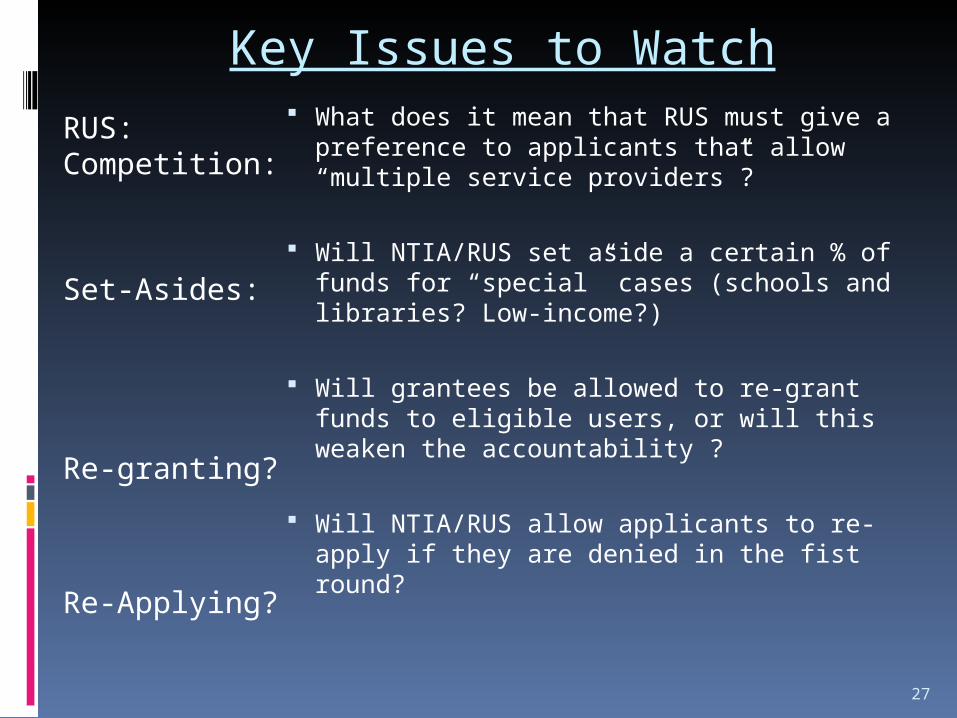

Key Issues to Watch

RUS: Competition:

Set-Asides:

Re-granting?

Re-Applying?

What does it mean that RUS must give a preference to applicants that allow “multiple service providers”?

Will NTIA/RUS set aside a certain % of funds for “special” cases (schools and libraries? Low-income?)

Will grantees be allowed to re-grant funds to eligible users, or will this weaken the accountability ?

Will NTIA/RUS allow applicants to re-apply if they are denied in the fist round?

27

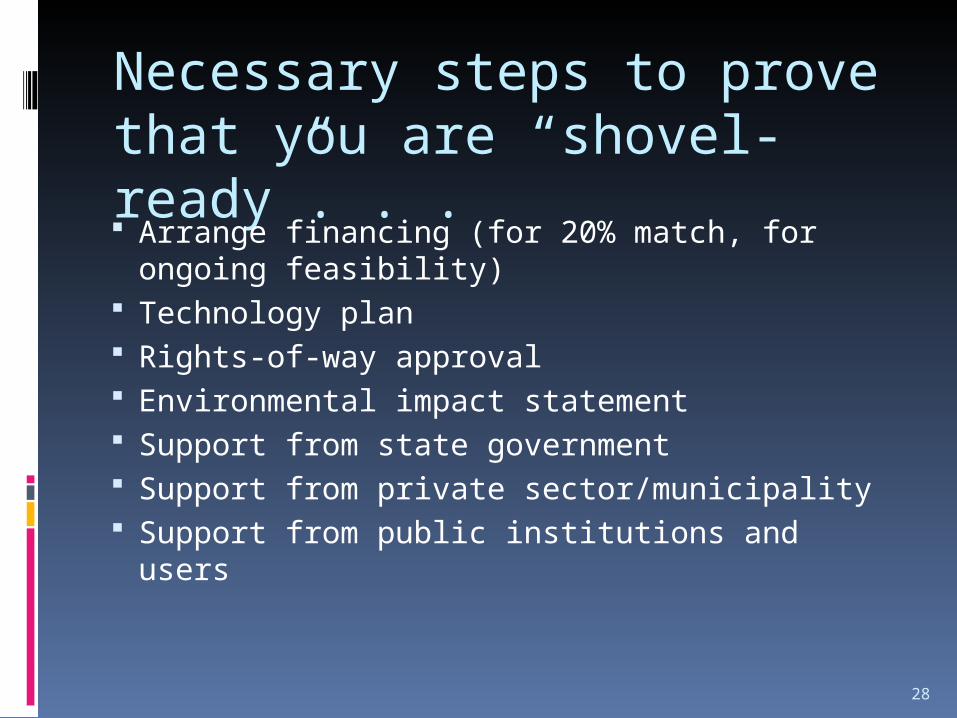

Necessary steps to prove that you are “shovel-ready”. . . Arrange financing (for 20% match, for

ongoing feasibility) Technology plan Rights-of-way approval Environmental impact statement Support from state government Support from private sector/municipality Support from public institutions and users

28