Embed Size (px)

Citation preview

The Bad Assets

Company Overview

Ticker: QCOMRecent Price: $53.30 Incorporated: 1985Headquarters: San Diego, CAMarket Cap: 95.4 B

Enterprise Value: 85 BReturn on Equity: 18.4%Return on Capital: 14.2%Return on Assets: 11.7%P/E (TTM): 14

History of Multiple Access

Wire

1800s: Morse Telegraph

History of Multiple Access

Wire

1860s: Bell Multiple Telegraph

History of Multiple Access

Frequency

1G - Frequency Division Multiple Access (FDMA)

Time

Time

Hertz

Hertz120 Hz60 Hz

History of Multiple Access2G - 1982: Time Division Multiple Access (TDMA)

FDMA

Freq

uenc

y

Time

TDMA

Freq

uenc

y

Time

History of Multiple Access2G/3G/4G – 1987: Code Division Multiple Access (CDMA)

Freq

uenc

y

Time

History of Multiple Access2G/3G/4G – 1987: Code Division Multiple Access (CDMA)

Freq

uenc

y

Time

History of Multiple Access

Time

Freq

uenc

y

2G/3G/4G – 1987: Code Division Multiple Access (CDMA)

History of Multiple Access

Time

Freq

uenc

y

A

B

C

D

Orthogonal-Frequency Division Multiple Access

2G/3G/4G – 1987: Code Division Multiple Access (CDMA)

History

1985 – “Quality Communications” (Qualcomm) is founded 1989 – CDMA is proven during San Diego convention1991 – Qualcomm goes public1993 – CDMA is made an industry standard1998 – Qualcomm unveils world’s first CDMA smartphone 1999 – Qualcomm joins the S&P 500 and the Fortune 500

History

2000 – Qualcomm releases first multimedia CDMA chipset2003 – Qualcomm spearheads the evolution of wireless broadband2007 – Qualcomm named the world’s leading mobile chipset provider2010 – 3G connections surpass 1 billion users2011 – Qualcomm acquires Atheros 2013 – Qualcomm powers the world’s first LTE Smartphone

Business Overview

Leader in development and commercialization of CDMA– Coded Division Multiple Access

Owner of several substantial intellectual property rights– Coded Division Multiple Access (CDMA)– Time Division Multiple Access (TDMA)– Orthogonal Frequency - Division Multiple Access (OFDMA)

Manufacturer and developer of industry standards

Manufactures chips and system software

Business Segments

Qualcomm CDMA Technologies (QCT)– Voice and Data Communications– Networking– Application Processing– Multimedia – Global Positioning Systems

Qualcomm Technology Licensing (QTL)– Grants licenses and rights to use portfolio of intellectual property – Licensees pay QCOM fees and royalties for use of intellectual property

How Qualcomm Makes Money

QCT is responsible for manufacturing and developing software

QTL collects royalties and fees on intellectual rights

9 Key Business Applications of QCT

AutomotiveHealthcareEducation Mobile ComputingNetworkingSmart CitiesSmart HomesWearables Internet of Everything

How Qualcomm Collects Money

Smartphones cannot use modern networks without paying QTLQualcomm is essentially a “highway system” with tolls

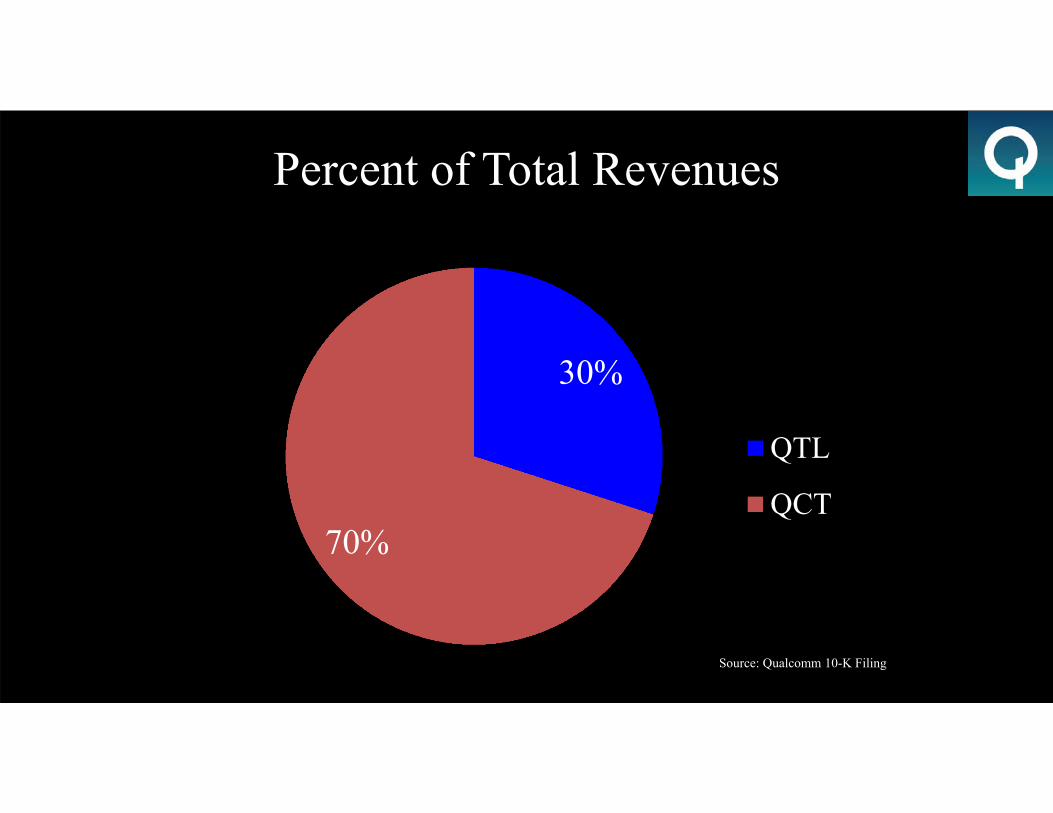

Percent of Total Revenues

30%

70%

QTL

QCT

Source: Qualcomm 10-K Filing

Revenue by Segment

$12,141

$16,715

$18,665

$6,327 $7,554 $7,569

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

$20,000

2012 2013 2014

Rev

enue

(in

Mill

ions

)

QCT QTL

Source: Qualcomm 10-K Filing

9 Month Revenues by Segment

$9,012

$12,258

$13,816 $13,529

$4,775 $5,680 $5,774 $6,162

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

Q1-Q3 2012 Q1-Q3 2013 Q1-Q3 2014 Q1-Q3 2015

Rev

enue

(in

Mill

ions

)

QCT QTL

Sources: Qualcomm Q3 2015, 2014, 2013, 2012 Reports

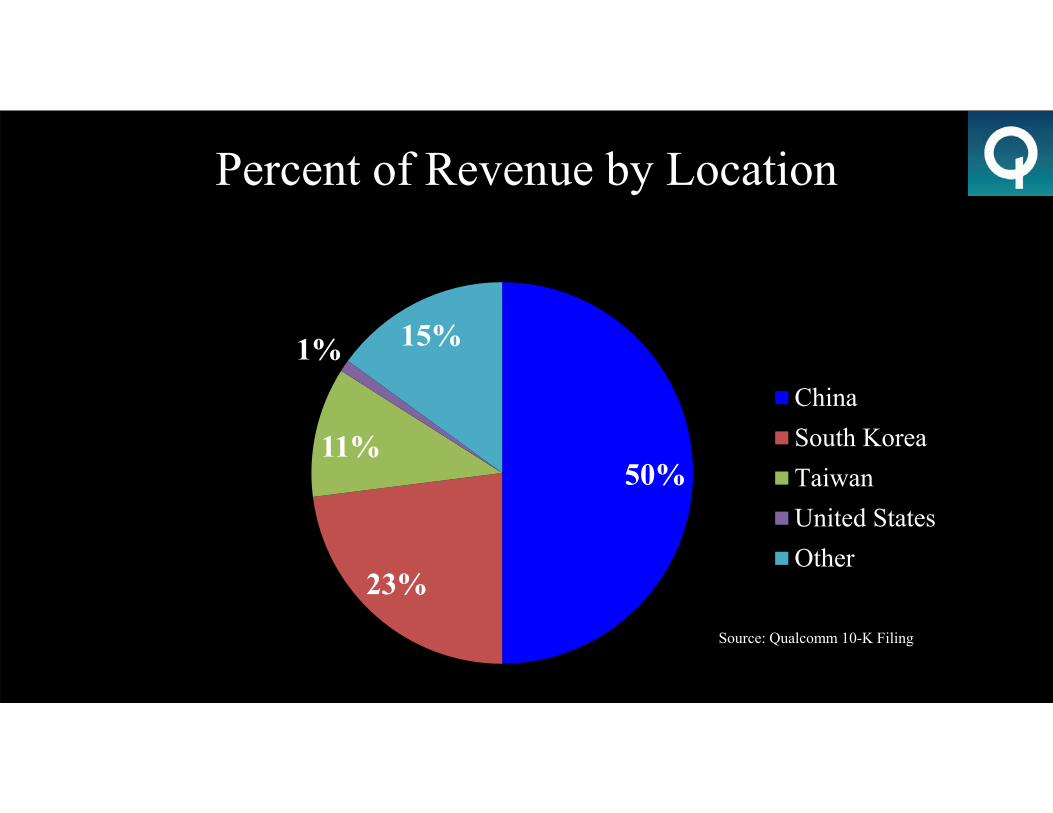

Percent of Revenue by Location

50%

23%

11%

1% 15%

ChinaSouth KoreaTaiwanUnited StatesOther

Source: Qualcomm 10-K Filing

Employees

31,300 Employees 40 Countries

120 Different NationalitiesHighly Educated & Skilled

New Board Members

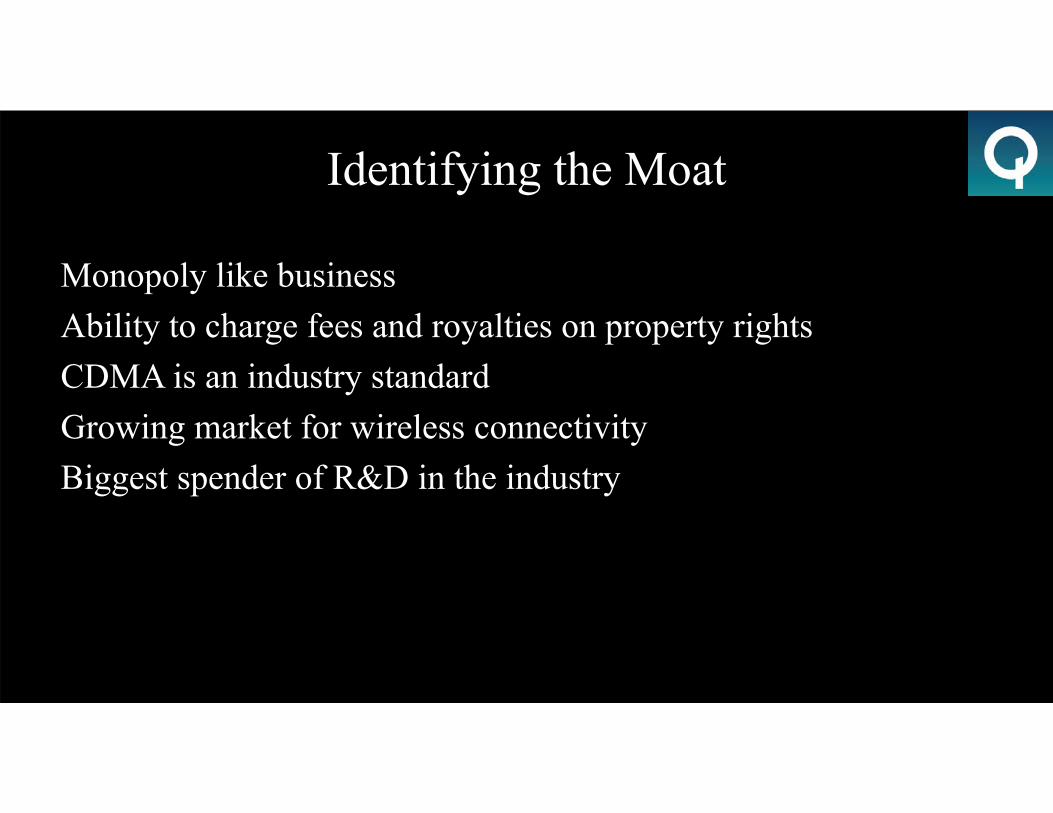

Identifying the Moat

Monopoly like business Ability to charge fees and royalties on property rights CDMA is an industry standard Growing market for wireless connectivityBiggest spender of R&D in the industry

Is There Opportunity Today?

Samsung and Q4 earnings outlookChinese InvestigationTrading at multi-year lowsStrong financial track recordGrowing wireless markets Strategic realignment planNew board membersSeparation of QCOM Segments??

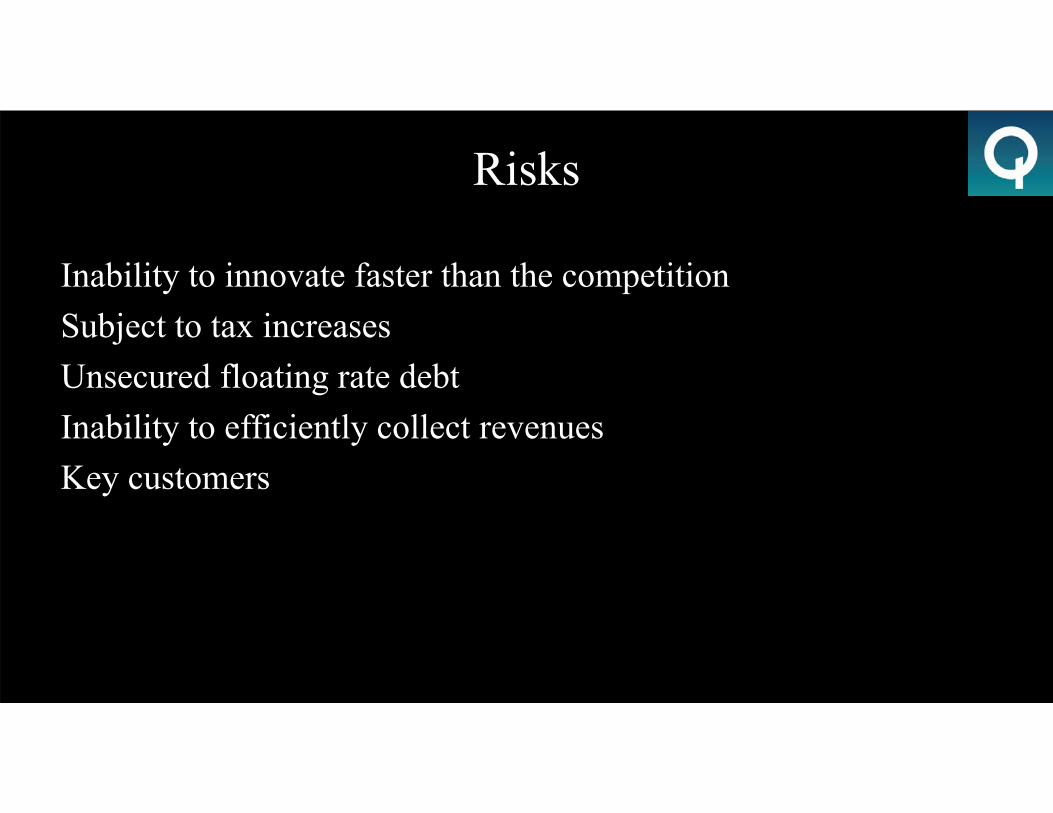

Risks

Inability to innovate faster than the competitionSubject to tax increasesUnsecured floating rate debtInability to efficiently collect revenuesKey customers

Qualitative ReviewQualitative Question

What type of business is this: commodity or sustained competitive advantage?

Competitive Advantage

Can you easily explain what the business does? Yes *sweats*Is it heavily unionized? NoDoes it require heavy capital infusion? NoDoes it require lots of research and development? YesCan inventory become obsolete? NoAre there chronic "one time" write offs? NoIs the company able to raise its prices to offset inflation? YesWill the company be able to sell more in the future? YesIf I gave you $1 billion could you develop a competitor? If the answer is "no" your business has a sustained competitive advantage. No

In the News

Q4 EarningsFDA Approval Jana Partners Steve Mollenkopf takes over as CEODr. Paul E. Jacobs is named CFO

Recent Acquisitions

Cambridge Silicon Radio (CSR)IkanosCapsule Technolgie

Strategic Realignment Plan

Designed to:-Improve execution-Enhance financial performance-Drive profitable growth-Create sustainable long-term value for stockholders

Implementation of a cost realignment plan -Targeted reductions that will not threaten growth-Reduction of annual share-based compensation grants

Total restructuring costs are expected be $350 to $450 million

China’s National Development and Reform Commission (NDRC)

Qualcomm was found guilty of violating Anti-Monopoly Law (AML)The abuse:

– Licensing of patents• Non adjusting royalty rates with changing patents• Non disclosed list of patents in licenses sold• Creating cross-license agreements without offsetting the royalties charged

– Baseband chipsets• Requirement of licensees to sign a contract that violates the AML• Requirement of licensees to promise not to challenge Qualcomm’s patents

China’s National Development and Reform Commission (NDRC)

Qualcomm must now:– List the patents to be licensed in the portfolios and stop licensing expired patents– Stop bundling Standard Essential Patents (SEPs) with non-SEPS– Change cross-licensing methods– Stop including no-challenge clauses in supply contracts– Pay a penalty of $975 million

Qualcomm committed to a voluntary rectification plan

Quantitative Analysis

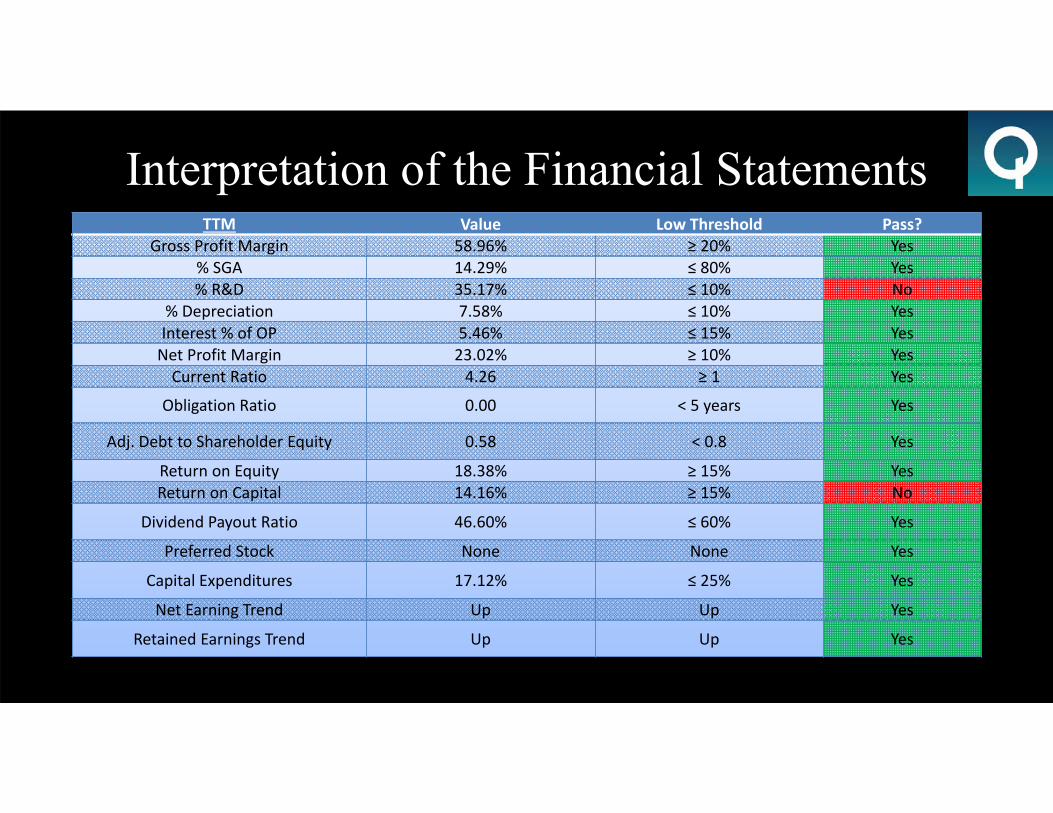

Interpretation of the Financial StatementsTTM Value Low Threshold Pass?

Gross Profit Margin 58.96% ≥ 20% Yes% SGA 14.29% ≤ 80% Yes% R&D 35.17% ≤ 10% No

% Depreciation 7.58% ≤ 10% YesInterest % of OP 5.46% ≤ 15% YesNet Profit Margin 23.02% ≥ 10% YesCurrent Ratio 4.26 ≥ 1 Yes

Obligation Ratio 0.00 < 5 years Yes

Adj. Debt to Shareholder Equity 0.58 < 0.8 Yes

Return on Equity 18.38% ≥ 15% YesReturn on Capital 14.16% ≥ 15% No

Dividend Payout Ratio 46.60% ≤ 60% Yes

Preferred Stock None None Yes

Capital Expenditures 17.12% ≤ 25% Yes

Net Earning Trend Up Up Yes

Retained Earnings Trend Up Up Yes

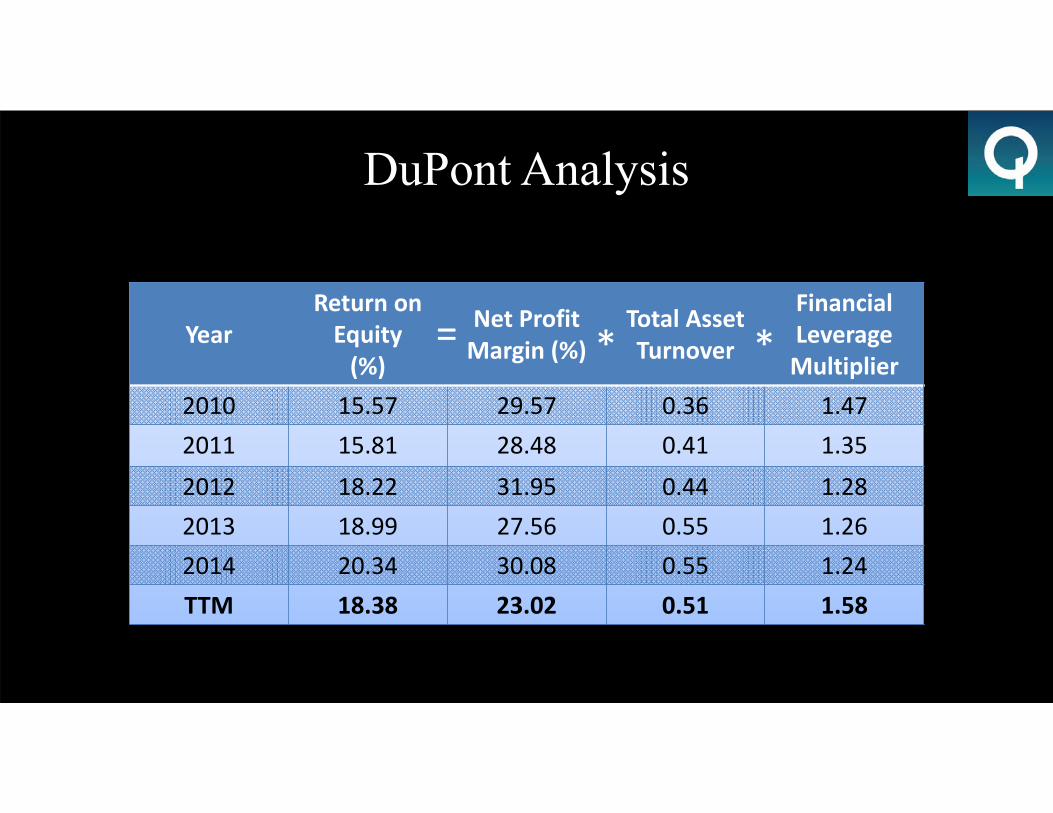

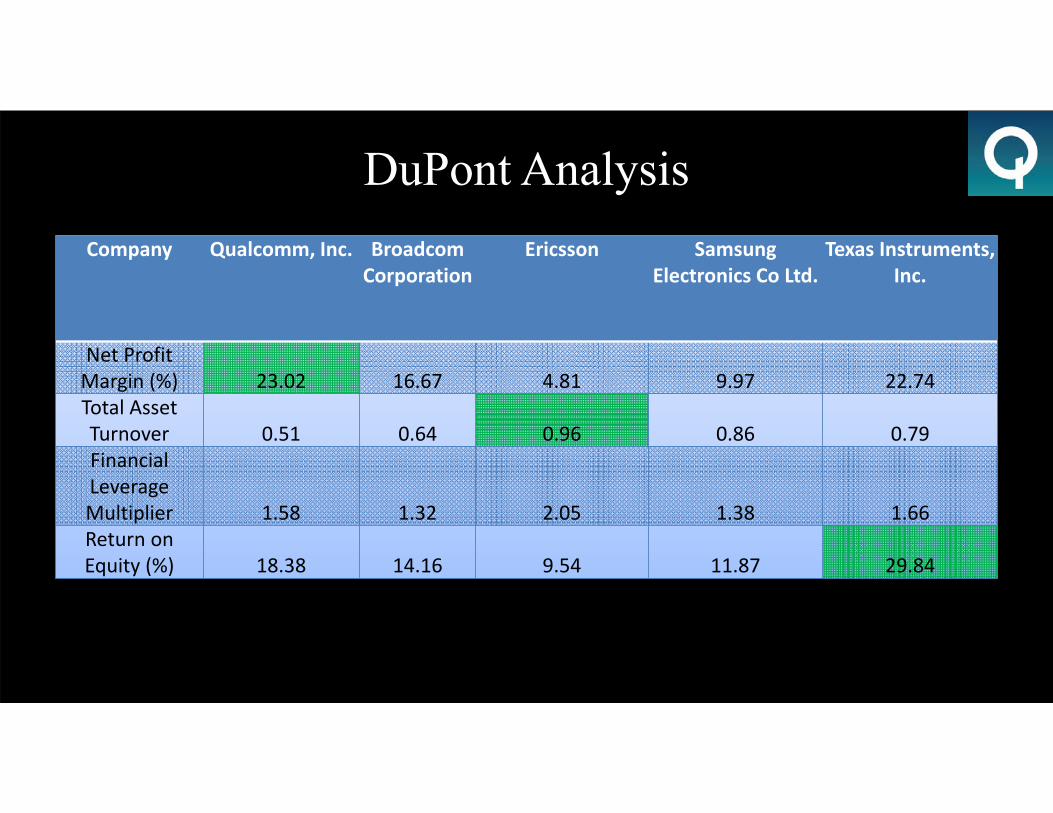

DuPont Analysis

YearReturn on Equity(%)

Net Profit Margin (%)

Total Asset Turnover

Financial Leverage Multiplier

2010 15.57 29.57 0.36 1.472011 15.81 28.48 0.41 1.35

2012 18.22 31.95 0.44 1.282013 18.99 27.56 0.55 1.262014 20.34 30.08 0.55 1.24TTM 18.38 23.02 0.51 1.58

= * *

Net Profit Margin

37.78%

32.82%37.23%

28.36%

15.28%

29.57% 28.48%

31.95%

27.56%30.08%

23.02%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 TTM

Net

Pro

fit M

argi

n (%

)

Year

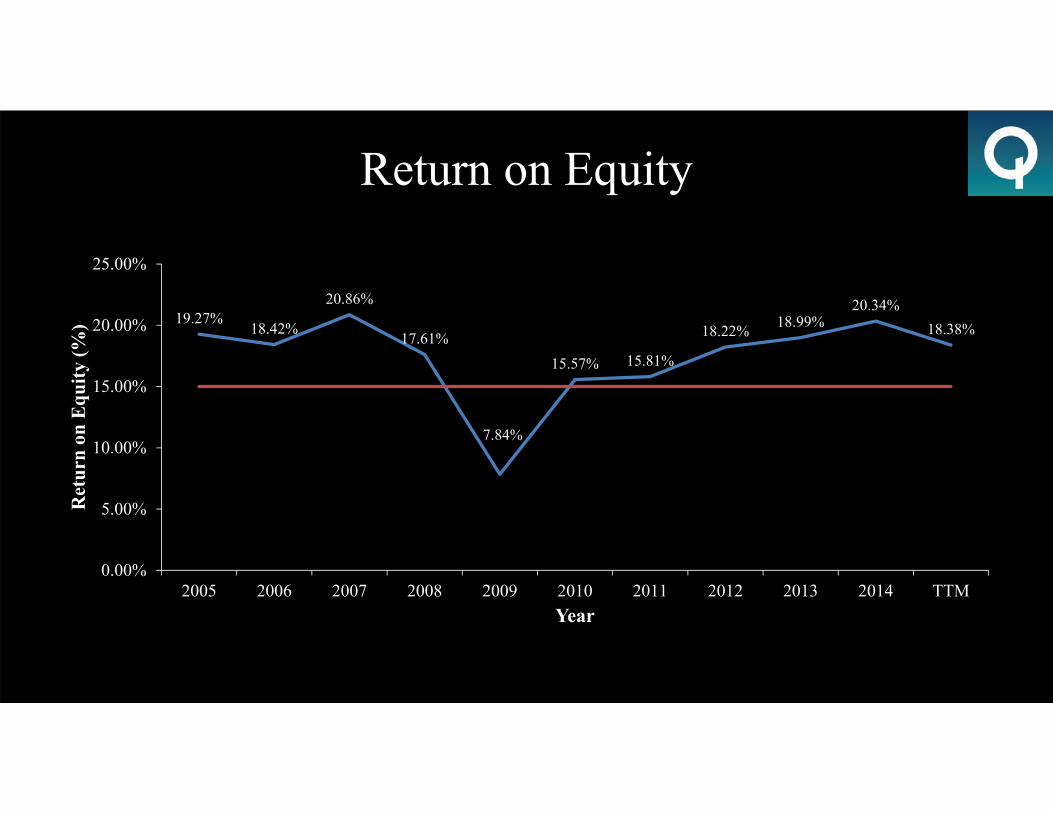

Return on Equity

19.27%18.42%

20.86%

17.61%

7.84%

15.57% 15.81%

18.22% 18.99%20.34%

18.38%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 TTM

Ret

urn

on E

quity

(%)

Year

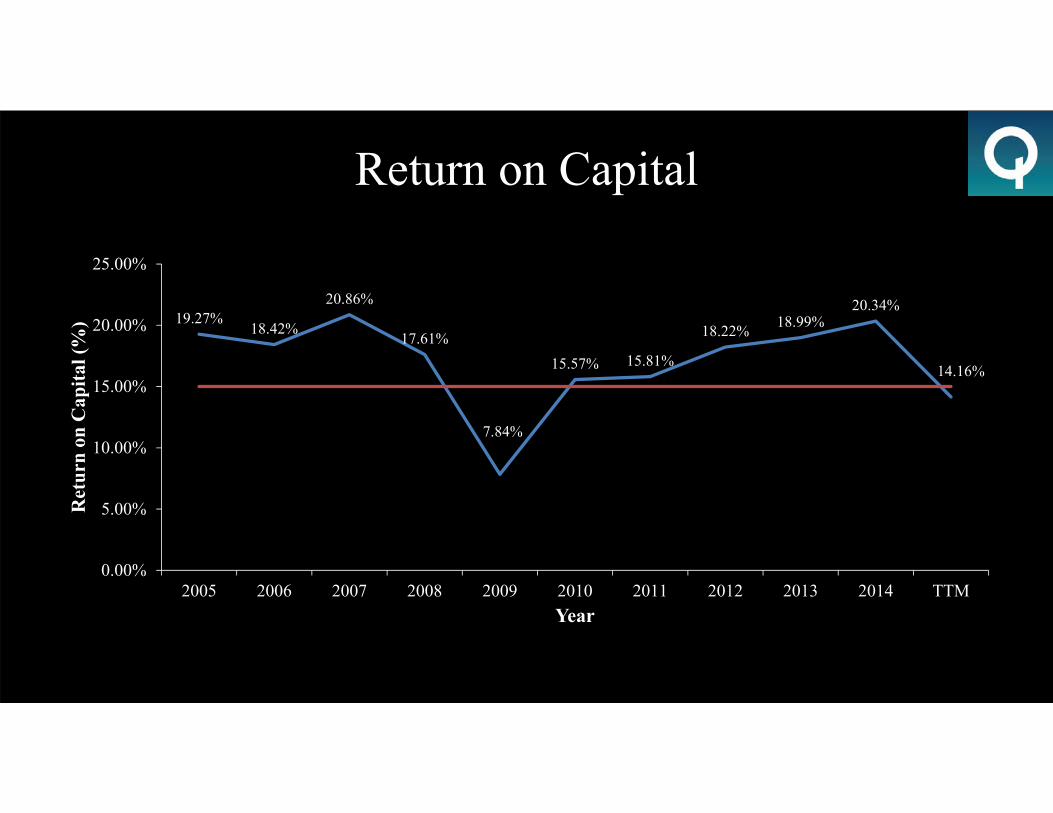

Return on Capital

19.27%18.42%

20.86%

17.61%

7.84%

15.57% 15.81%

18.22% 18.99%20.34%

14.16%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 TTM

Ret

urn

on C

apita

l (%

)

Year

Retained Earnings

4,328

8,54111,235

16,204

25,461

32,699

$0.00

$5,000.00

$10,000.00

$15,000.00

$20,000.00

$25,000.00

$30,000.00

$35,000.00

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 TTM

Ret

aine

d E

arni

ngs (

$ in

mill

ions

)

Year

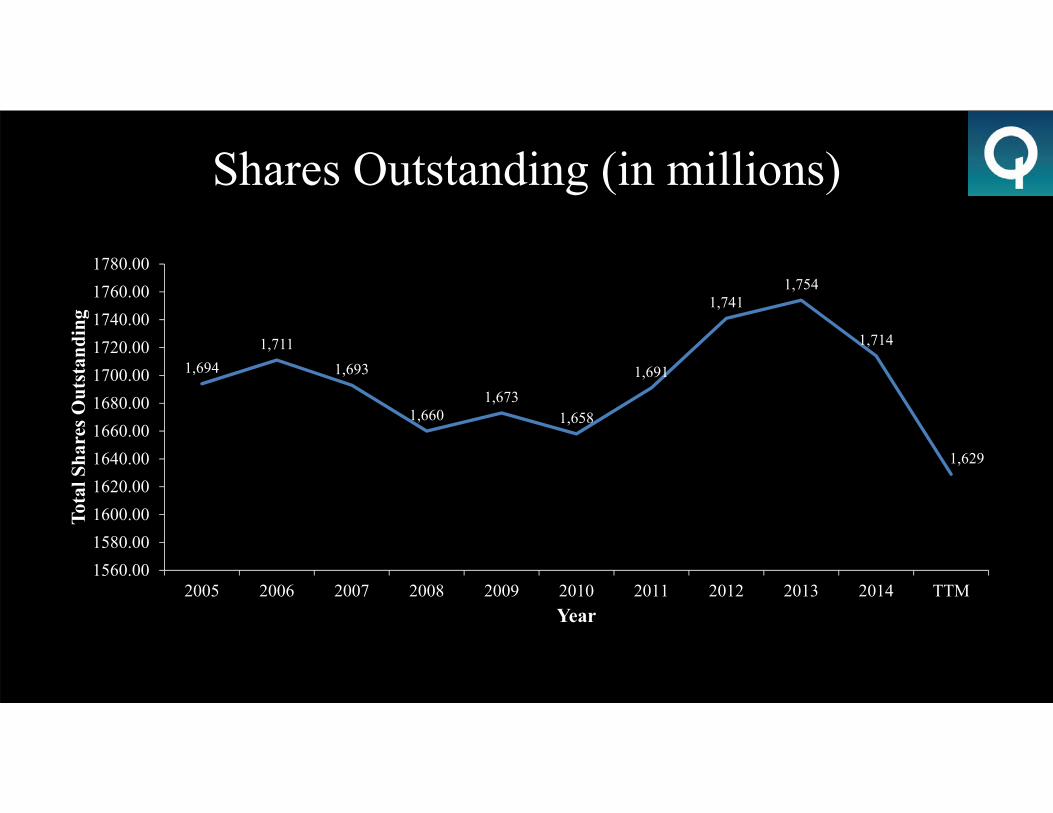

Shares Outstanding (in millions)

1,6941,711

1,693

1,6601,673

1,658

1,691

1,7411,754

1,714

1,629

1560.001580.001600.001620.001640.001660.001680.001700.001720.001740.001760.001780.00

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 TTM

Tota

l Sha

res O

utst

andi

ng

Year

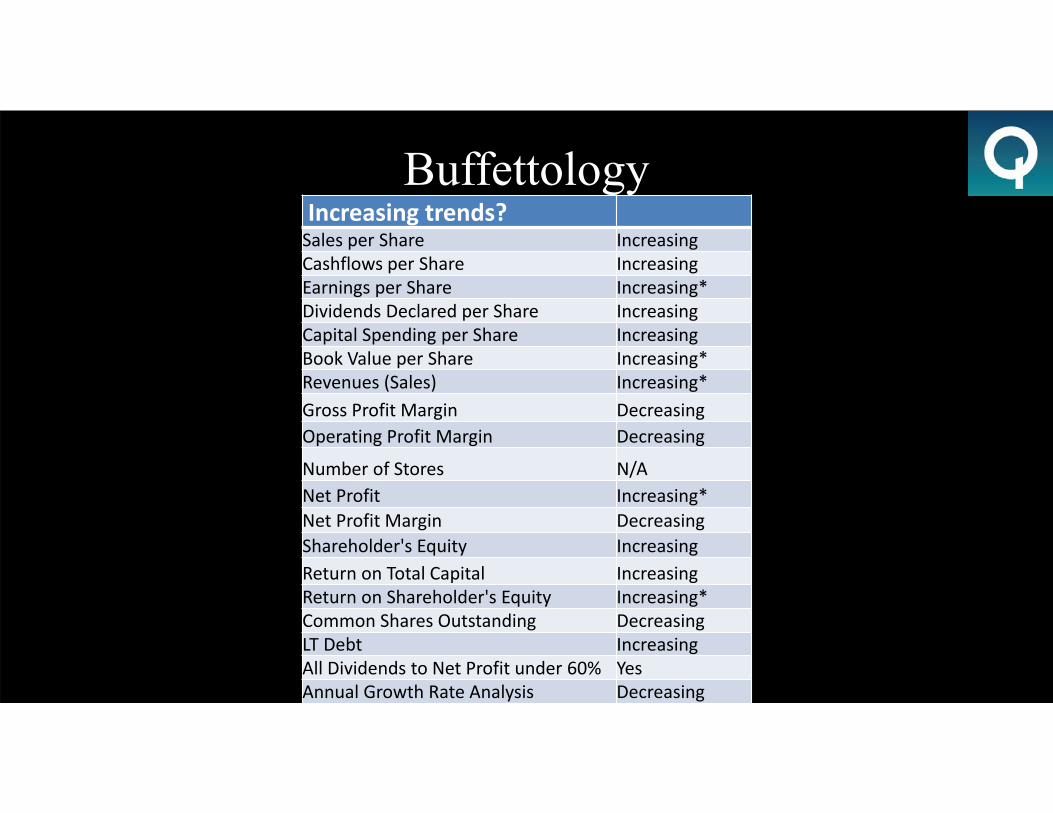

BuffettologyIncreasing trends?Sales per Share IncreasingCashflows per Share IncreasingEarnings per Share Increasing*Dividends Declared per Share IncreasingCapital Spending per Share IncreasingBook Value per Share Increasing*Revenues (Sales) Increasing*Gross Profit Margin DecreasingOperating Profit Margin Decreasing

Number of Stores N/ANet Profit Increasing*Net Profit Margin DecreasingShareholder's Equity IncreasingReturn on Total Capital IncreasingReturn on Shareholder's Equity Increasing*Common Shares Outstanding DecreasingLT Debt IncreasingAll Dividends to Net Profit under 60% YesAnnual Growth Rate Analysis Decreasing

Value Bands

Price/Earnings

10.0

15.0

20.0

25.0

30.0

35.0

40.0

Price/Normalized Earnings (Less Cash)

0

5

10

15

20

25

30

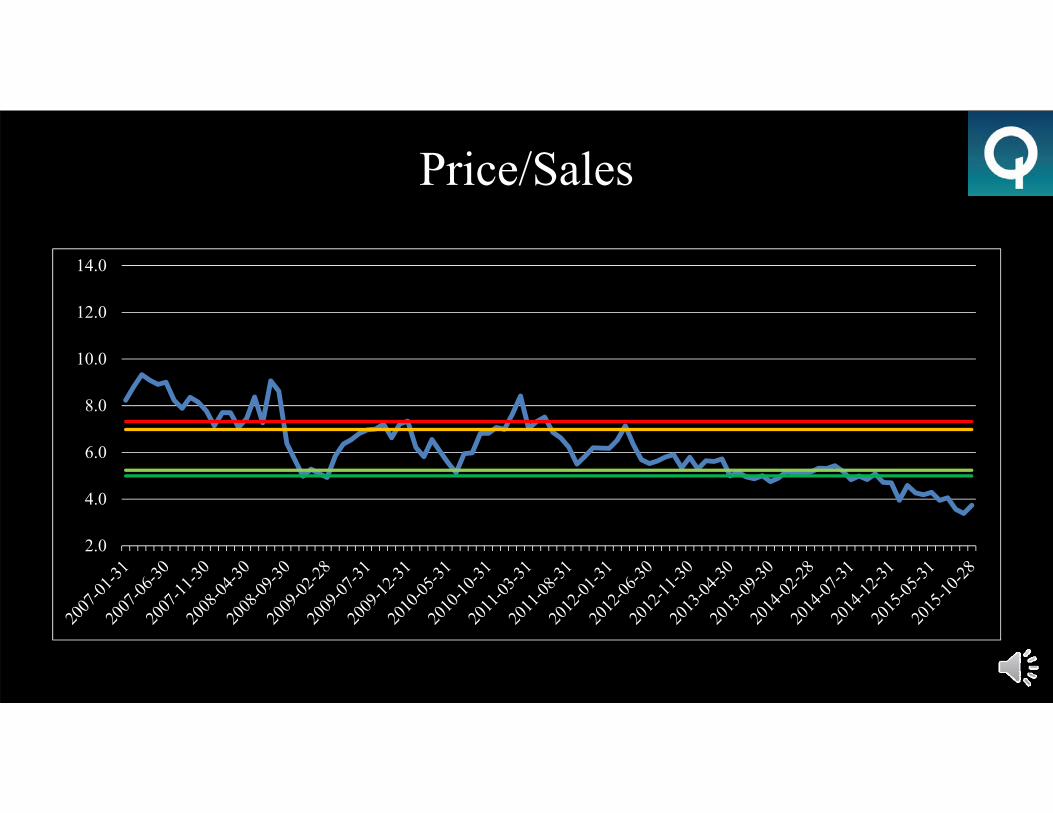

Price/Sales

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Price/Book

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

Price/Cash Flow

0.0

5.0

10.0

15.0

20.0

25.0

30.0

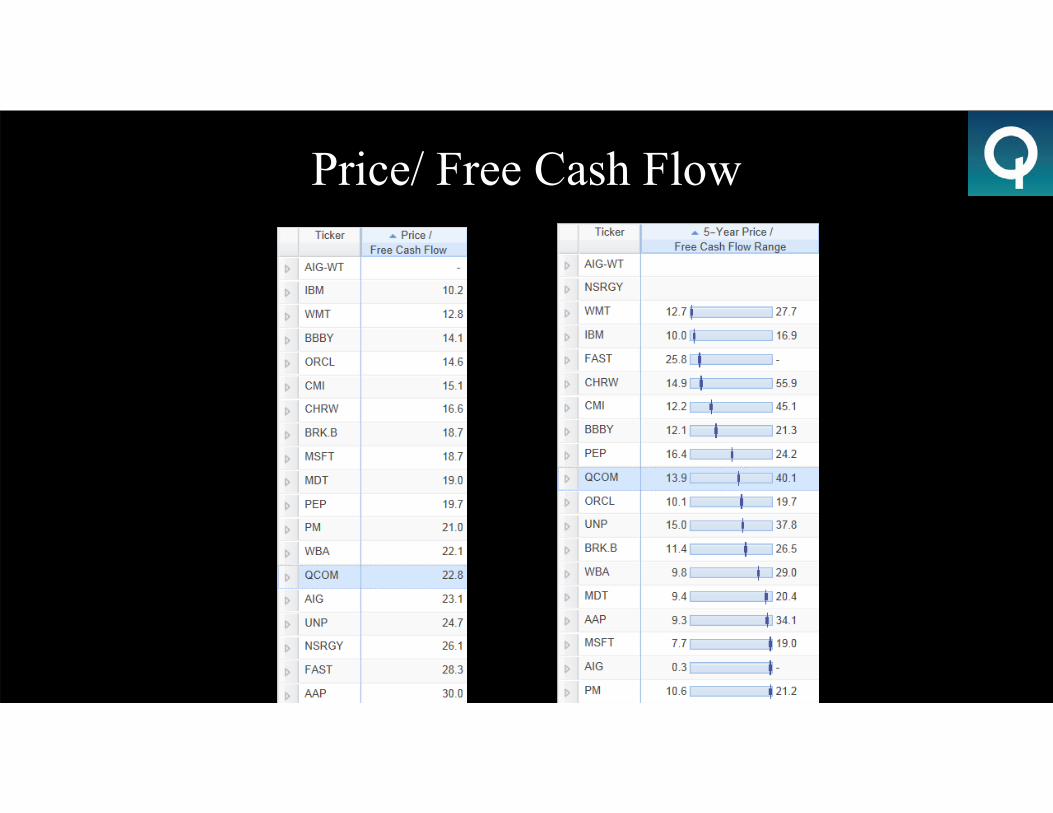

Price/Free Cash Flow

10.0

15.0

20.0

25.0

30.0

35.0

Enterprise Value/ Revenue

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

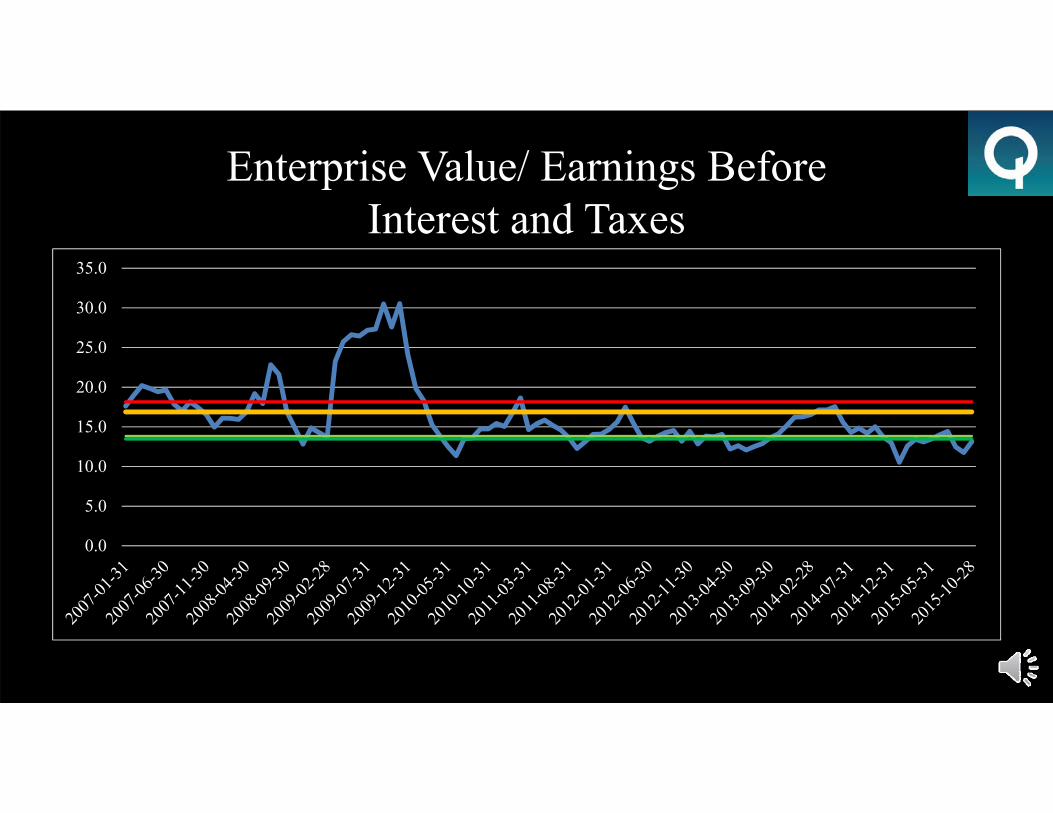

Enterprise Value/ Earnings Before Interest and Taxes

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Enterprise Value/ Earnings Before Interest, Taxes, Depreciation, and Amortization

5.0

7.0

9.0

11.0

13.0

15.0

17.0

19.0

21.0

Discounted Cash Flow Model

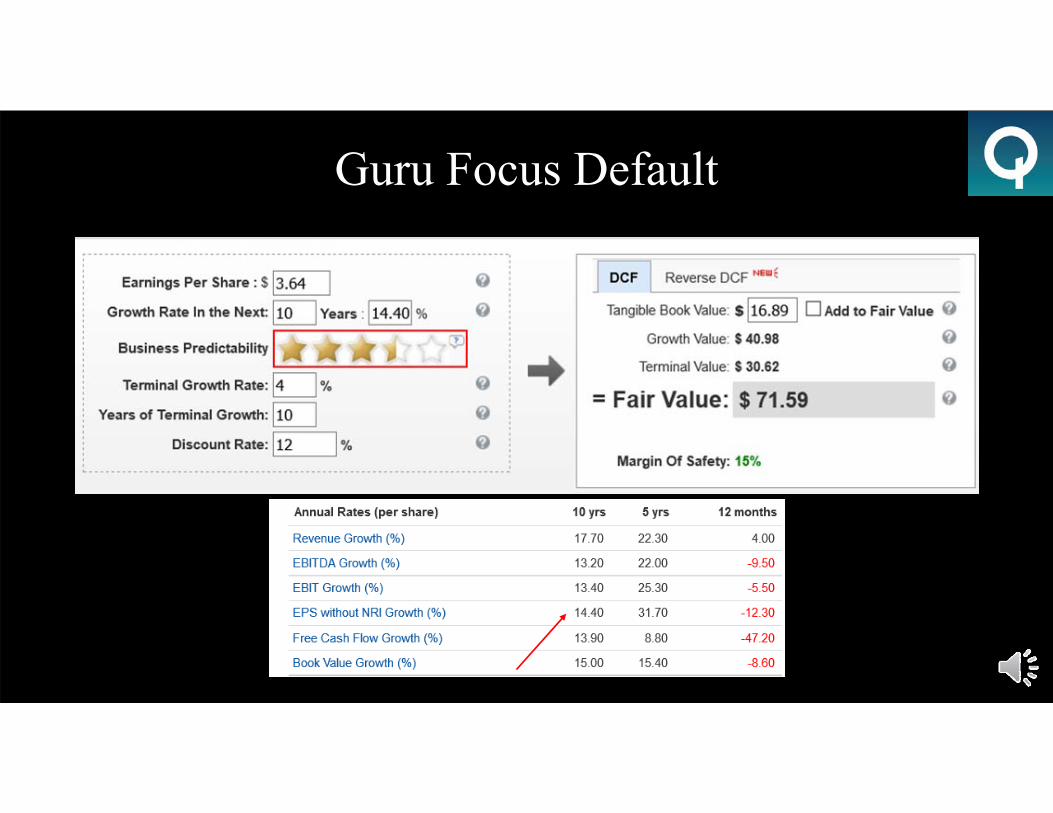

Valueline’s Growth Rate

Guru Focus Default

Kill It

Cut 10 Year Growth Rate by 16.6%

Conscious Investor

5 Years

5 Year Safety

Cut Earnings Growth by 41.42% Cut P/E by 17.91%

10 Years

10 Year Safety

Cut P/E by 18.89%Cut Earnings Growth by 33.27%

Kill It

Cut P/E by 3.9%Cut Earnings Growth by 66.93%

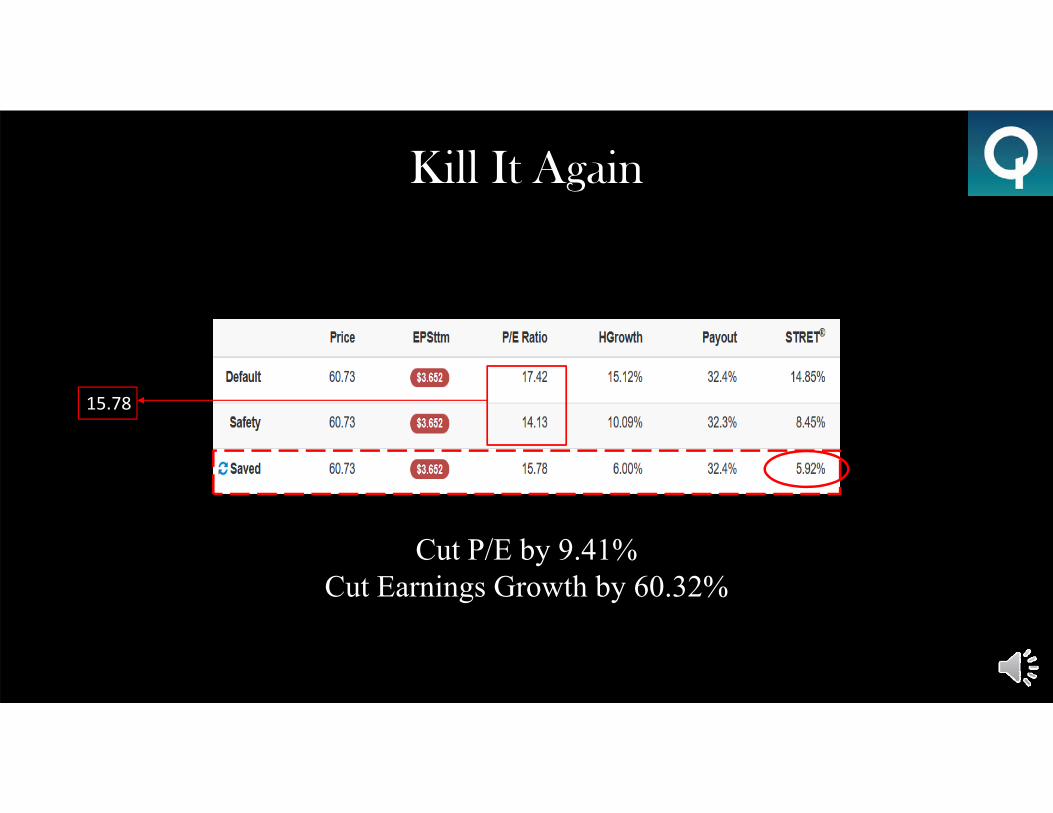

Kill It Again

15.78

Cut P/E by 9.41%Cut Earnings Growth by 60.32%

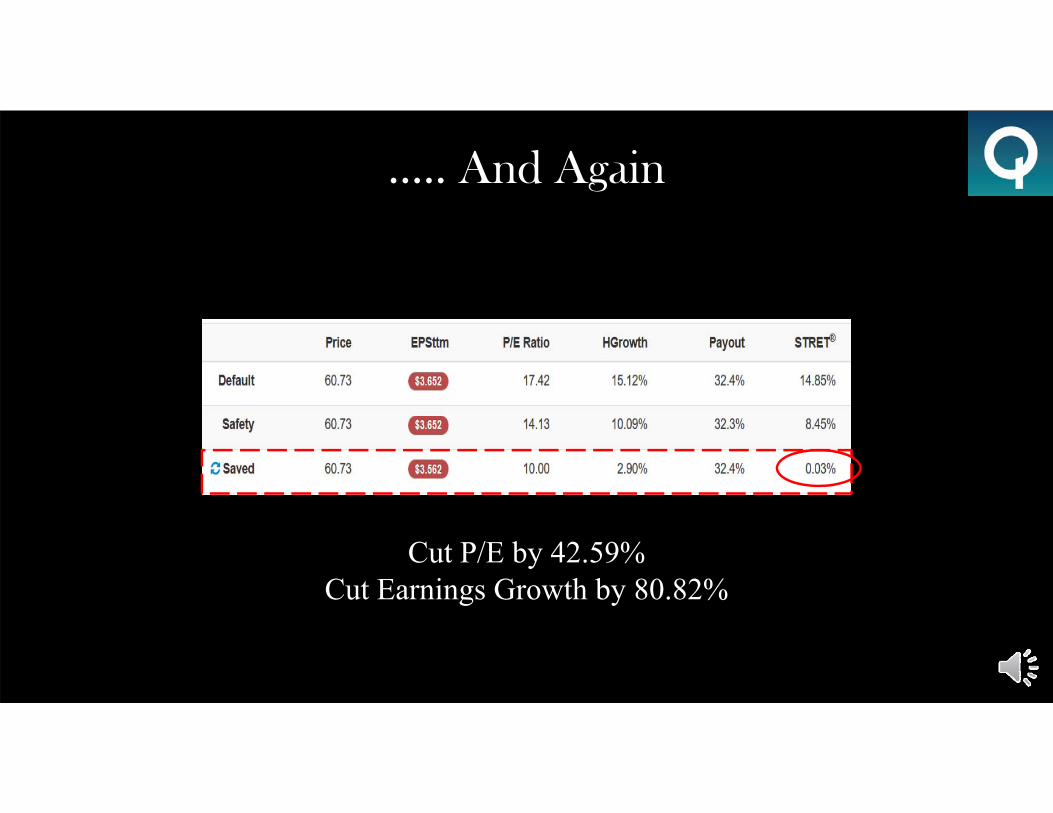

….. And Again

Cut P/E by 42.59%Cut Earnings Growth by 80.82%

Industry BreakdownCompany Qualcomm, Inc. Broadcom

CorporationEricsson Samsung Electronics

Co Ltd.Texas Instruments,

Inc.Market Cap (in billions) 93.9 32.06 31.63 135.78 60.22

Yield (%) 3.05 1.05 4.09 1.78 2.31

P/E (ttm) 16.32 29.73 11.88 9.90 20.97

P/B 2.79 2.87 0.80 0.99 6.10

P/FCF 22.56 20.26 8.85 36.83 17.31

P/S 3.74 3.81 1.21 0.79 4.74

EV/EBIT 13.10 26.77 4.71 4.84 14.51

ROE (%) 18.38 14.16 9.54 11.87 29.84ROA (%) 12.46 8.78 4.07 8.40 17.09

Operating Margin (%) 25.26 13.26 7.37 11.30 32.35

Net Margin (%) 23.02 12.66 4.81 9.97 22.74

Number of Guru Holdings 1,567 656 240 ‐ 896

DuPont AnalysisCompany Qualcomm, Inc. Broadcom

CorporationEricsson Samsung

Electronics Co Ltd.Texas Instruments,

Inc.

Net ProfitMargin (%) 23.02 16.67 4.81 9.97 22.74Total Asset Turnover 0.51 0.64 0.96 0.86 0.79FinancialLeverage Multiplier 1.58 1.32 2.05 1.38 1.66Return on Equity (%) 18.38 14.16 9.54 11.87 29.84

Intra-Portfolio Valuations

Price/Earnings

Price/Book

Price/Sales

Price/ Free Cash Flow

Enterprise Value to Earnings Before Interest,Taxes, Depreciation, and Amortization

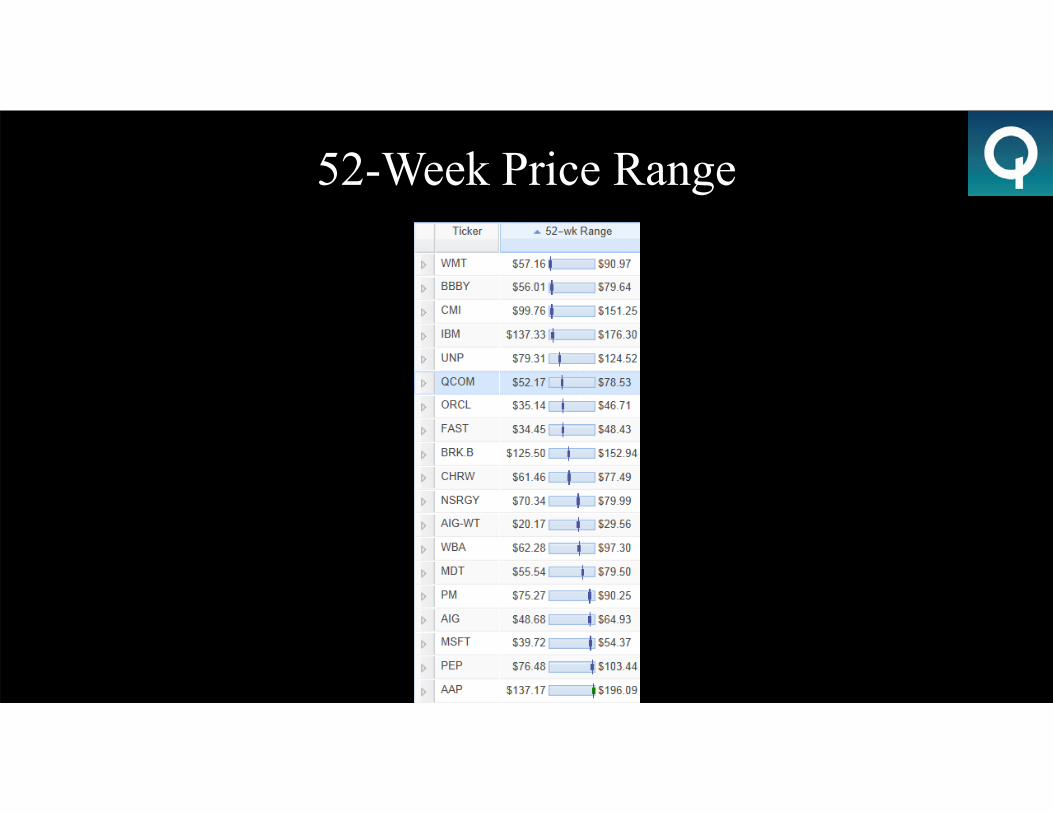

52-Week Price Range

Conclusion

Historically undervaluedStrong operating and profit marginsDeveloper of industry standardEffective use of licenses

Recommendation

Limit Order at $53.14"I try to buy stock in businesses that are so wonderful that an idiot can run them. Because sooner or later, one will.”-Warren Buffett