Embed Size (px)

Citation preview

Annals of the „Cons tantin Brâncuşi” Univers i ty of Târgu J iu, Economy S eries , Is s ue 2 /2015

„ACADEMICA BRÂNCUŞI” PUBLISHER, ISSN 2344 – 3685/ISSN-L 1844 - 7007

THE ANALYSIS OF FINANCIAL AND PRUDENTIAL BANKING INDICATORS

IN THE ROMANIAN BANKING SECTOR DURING THE CRISIS AND POST-

CRISIS

ANISOARA NICULINA APETRI,

ŞTEFAN CEL MARE UNIVERSITY OF SUCEAVA, [email protected]

CAMELIA CĂTĂLINA MIHALCIUC

ŞTEFAN CEL MARE UNIVERSITY OF SUCEAVA,

VERONICA GROSU

ŞTEFAN CEL MARE UNIVERSITY OF SUCEAVA,

Abstract

The current dynamics of the worldwide banking system and the changes that have taken place

generally in the banking systems around the world and particularly in the banking system in Romania,

became the main reason we chose to make the research in this field. The Romanian banking system has gone

through several steps in order to achieve the convergence to international provisions. The financial and

prudential banking indicators are important signals of health of the banking sector as a whole, and their

study has been a constant concern for various national and international financial institutions such as

National Bank of Romania, IMF, ECB, World Bank but also for the researchers in the field, and their

analysis in the Romanian banking system represents a research of great topical interest.

Key words: financial system, banking system, solvency indicators, profitability indicators

INTRODUCTION

The banking system has been defined by Costin K. and Dobresu E. (1998) as a complex of

operations and transactions of assets and liabilities. The same authors define the bank machine as 'all the

various categories of banks with domestic and private capital and their mixed combinations, which operates

within a country'. Thus, it emerges the conclusion (Berea, A., 2003) that the banking unit is the organization

of banks and the banking system refers to the operations of these banks. According to the literature in the

field (Corrigan E.G., 1982, David, 2013, p.363), the role of banks is , if not unique, at least particular in

comparison with other companies in the real sector or the financial sector, banking development ensuring

thus ultimately the necessary structure for a good running of the market economy. Based on these aspects , we

used in the first part of the study a brief presentation of the defining stages in the evolution of the banking

system in Romania. In the second part of the study it was highlighted its role in the current financial system,

so that in the third part to be analyzed carefully the prudential and performance indicators that characterize

the banking system in Romania during the crisis and post crisis.

Taking into account the classic positioning indicators of components within its financial system and

the information provided by the National Bank of Romania, available in the official publications of the

national bank's website, in the second part of the study we conducted an empirical analysis on the structure of

the financial system in Romania during 2007-2012. The analysis’ results show that the financial system in

Romania is a financial bank-based system, and its structure is unqual. Dominance of the banking sector in the

financial system in Romania can be explained by the insufficient development of the capital markets and the

existence of a local financial literacy mainly oriented towards the banking sector.

The reports published by the National Bank of Romania: stability reports, annual reports, monthly

newsletters, but also the studies in the field and articles published in scientific sessions, essays, thesis, were

taken into account in the conducted research. For the present study we used a range of research methods such

as: the comparison method, the observation method, the statistical method, the graphical method and the case

study method. The methodological process followed the classification of the existing data, the collection and

updating of new data. The technique used was based mainly on Excel.

The research ends with presenting the conclusions and bibliographic sources to support the scientific

approach.

108

Annals of the „Cons tantin Brâncuşi” Univers i ty of Târgu J iu, Economy S eries , Is s ue 2 /2015

„ACADEMICA BRÂNCUŞI” PUBLISHER, ISSN 2344 – 3685/ISSN-L 1844 - 7007

1. The highlights of the history and the evolution of banking system in

Romania

The banking system in Romania has gone through several steps to achieve convergence to the

international provisions. First evidence of running a banking activity in Romania were discovered between

1786-1855, representing 55 stone plates found in a gold mining area, plates dating from Roman Dacia period

containing details of the agreement on the establishment of a banking institution. The setting up of the

banking system in our country has made with the contribution of the state by transforming the usurers into

bankers and with the participation of representatives of foreign capital (Turliuc, Cocriş, 1997, p.142). After

the setting up and running of the first banks in Romania (Bank of Moldova (1856), National Bank of

Romania (1880)), the Romanian banking system has experienced a period of flourishing development

especially in the period occurring between wars . "As a curiosity, it is worth mentioning that the National

Bank of Romania is one of the oldest in the world (in fact, the sixteenth central bank), surpassing prestigious

institutions as the Bank of Japan (1882), Bank of Italy (1883), Federal Reserve - Central Bank of the United

States of America (1913) and the Swiss National Bank. "(Isărescu M, 2001, p.174). In 1946, the banking

system was reorganized according to the Soviet model of monobank. The Romanian financial system from

1946 until 1989 appears in the banking sphere with a strong centralized nature in the sense that the National

Bank of Romania fulfills most of the banking functions, with the main tasks: regulation of money circulation,

credit economy and the organization of clearing operations and payments (Berea, AA: p., 2003, p. 57). This

model corresponded to the Soviet model of monobank, having in its center the National Bank, in order to

implement the centralized plan and control the administrative funds into the economy, the bank that exercise

functions as issuing bank and some commercial bank functions. With the fall and collapse of communism in

1989, the implementation of reforms in all fields to enable thus the transition from a centrally planned

economy to a market economy became a necessity.

Because the banking system is considered the financial backbone of the market economy, the reform

in this sector has become a priority. The reshaping of the banking system aimed on the one hand, the creation

of a specific banking market economy, on the other hand the harmonization of the Romanian legislation with

that of the European Union countries. In the author's opinion , Maricica Stoica, remodeling the Romanian

banking system mainly focused on the following issues (Stoica, 1999, p.11):

Restructuring the banking system;

Regulation, licensing and banking supervision.

Banking reform has come in terms of creating the legal framework and the type of measures

undertaken several steps, respectively (Apetri, 2013, p.35):

period 1990-1997, in which the "two-tier" banking system was founded, particular to the

market economy, and were developed the major legislation (Romanian Law no. 33/1991 on banking,

Romanian Law no. 34/1991 the Statute of the National Bank of Romania, Romanian Law no. 83/1997 on the

privatization of banks in which the state is a shareholder);

period 1998-2000, marked by efforts to align the national regulations with the European

requirements, the central bank acted to improve banking legislation by developing and approving a new set

of laws (Romanian Law no. 58/1998, Romanian Law no. 83/1998; Romanian Law no. 101/1998), by

initiating a process of rehabilitation and strengthening of the banking system;

during 2001-2004 the continued remediation of the banking system and the negotiations

were conducted between Romania and the European Union regarding the taking over of the relevant

European acquis, which was taken completely by the end of this stage. It also aimed to anchor domestic

regulations with international regulations (eg the implementation of the requirements of the Basel

Committee).

pre-accession period (2005-2006) marked by a series of new elements (adopting the

strategy of targeting inflation, the full liberalization of the capital account, the domestic currency

denominated implementation, commissioning of the electronic payment system SEPA) and post - accession

(2007-currently) EU structures aimed at entry into the Economic and Monetary Union and adopt the euro as

its currency. These periods can be grouped in two major phases, namely: the first phase (1991-2000) which

coincided with the first decade of transition of the Romanian economy, this is the stage of institution building

process inspired by international standards; the second phase (2001 to present) that focuses bank reforms for

integration in the EU requirements.

2. The place of the Romanian banking system within the financial system

The financial system represents a defining element for a modern economy. The analysis of the

financial system is thus a complex process (Hartmann, 2007, Bear, SG, 2013, p.1123), suggesting that a

simple conceptual framework includes three distinct levels, highlighting various aspects such as financial

109

Annals of the „Cons tantin Brâncuşi” Univers i ty of Târgu J iu, Economy S eries , Is s ue 2 /2015

„ACADEMICA BRÂNCUŞI” PUBLISHER, ISSN 2344 – 3685/ISSN-L 1844 - 7007

structure, financial development and performance of both the financial system and the economy as a whole

(Figure 1.1).

The basic elements of a financial system are monetary financial institutions or financial markets

infrastructure, along with the regulatory framework, micro and macro-prudential regulation, or the

competition policy and corporate governance. In this regard, the financial system can be defined as "a

collection of markets, institutions, laws, regulations and techniques that serve to trading bonds, shares and

other financial instruments, setting interest rates and the production and distribution of financial services"

(Rose and Marquis, 2010, Bear, SG, 2013, p.1123).

Although there are a large number of financial intermediaries in the financial system, the banks are

considered prime "actors" in the brokerage process, these acting on the money market but also on the

financial market. Throughout this thesis, the phrases like "banking company", "bank" and "credit institution"

will be interchangeably used. In Romania, the financial system can be seen dominating the banking system

structure of other countries in Central and Eastern Europe (CEE). The banking system as a component of the

financial system of a country can be defined as a group of institutions , financial and banking relationships,

rules, infrastructures and techniques that interact constantly in order to raise money held in savings in the

form of deposits and to distribute them as loan funds, as well as to offer other facilities (various payment

systems) and non-financial entities, legal entities or individuals . The importance of banks for national

economies determines the separation that is frequently performed in the literature between the two types of

financial systems, as the financial systems of the economy (Allen and Gale, 2000; Demirguc-Kunt and

Levine, 2001 Bear, SG, 2013 p.1130).

• bank-oriented system and

• market-oriented system.

Taking into consideration the organization of banking activity and the degree of specialization, we

thus can distinguish two types of banking systems (Dardac, Barbu, 2005, p.101):

The continental model specific to banking systems of continental Europe, less specialized which

functions like the universal bank model.

The American model, applied also in Japan, based on the principle of a strict specialization of

banking institutions.

Romanian banking system is a classical one, based on deposits and granting loans and holds a

dominant position in the financial system. Today, the financial system is made up of the following categories

of entities (Table no.1):

Table no. 1. The structure of the financial system

2008 2009 2010 2011 2012

Credit institutions 43 42 41 41 40

Insurance companies 44 45 43 43 39

Insurance brokers 459 510 567 584 584

Private pension funds 23 25 22 20 20

Investment funds 54 67 76 83 87

Financial investment companies 5 5 6 6 6

Companies of financial investment services 66 64 55 52 46

Nonbanking financial institutions (General Register) 238 228 210 203 187

Nonbanking financial institutions (Inventory Register) 4513 4802 5043 5286 5420

Source: www.bnr.ro, RSF, 2011, RSF 2013

As can be seen in Table no. 1 and Figure no. 1, the banking sector in Romania continues to be the

most important component of the financial market. The Romanian financial system relies on bank loans

("bank-oriented").

110

Annals of the „Cons tantin Brâncuşi” Univers i ty of Târgu J iu, Economy S eries , Is s ue 2 /2015

„ACADEMICA BRÂNCUŞI” PUBLISHER, ISSN 2344 – 3685/ISSN-L 1844 - 7007

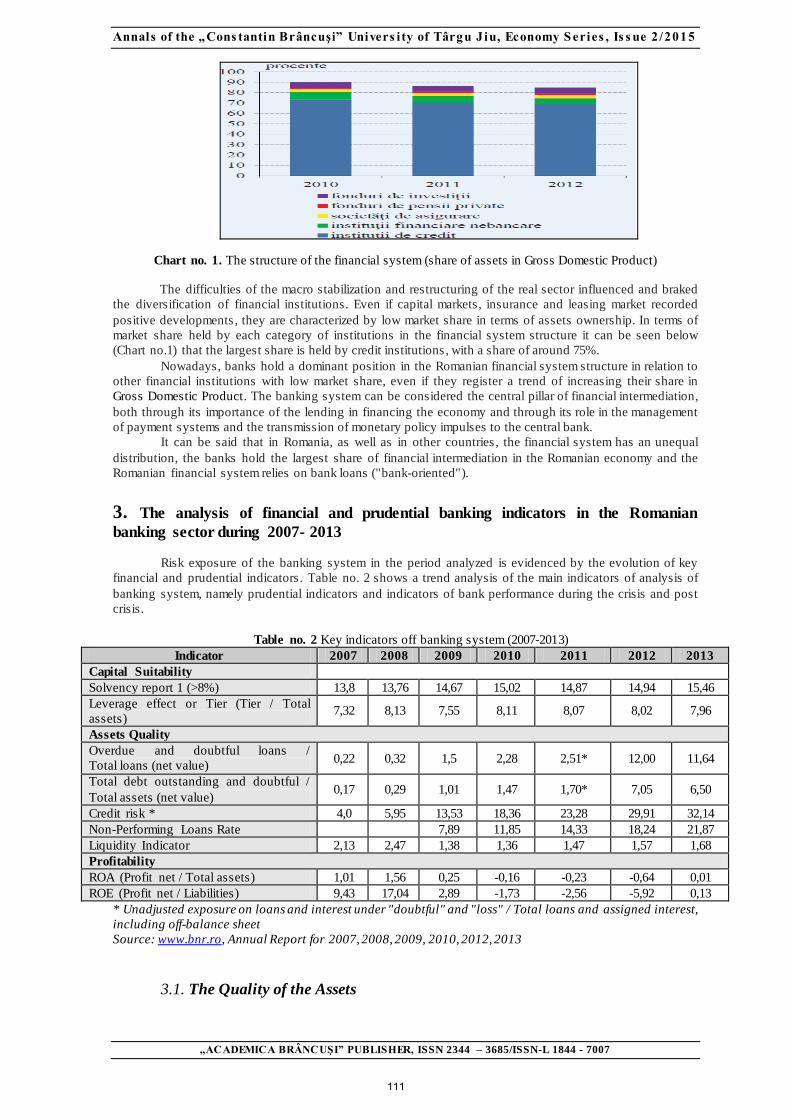

Chart no. 1. The structure of the financial system (share of assets in Gross Domestic Product)

The difficulties of the macro stabilization and restructuring of the real sector influenced and braked

the diversification of financial institutions. Even if capital markets, insurance and leasing market recorded

positive developments , they are characterized by low market share in terms of assets ownership. In terms of

market share held by each category of institutions in the financial system structure it can be seen below

(Chart no.1) that the largest share is held by credit institutions, with a share of around 75%.

Nowadays, banks hold a dominant position in the Romanian financial system structure in relation to

other financial institutions with low market share, even if they register a trend of increasing their share in

Gross Domestic Product. The banking system can be considered the central pillar of financial intermediation,

both through its importance of the lending in financing the economy and through its role in the management

of payment systems and the transmission of monetary policy impulses to the central bank.

It can be said that in Romania, as well as in other countries, the financial system has an unequal

distribution, the banks hold the largest share of financial intermediation in the Romanian economy and the

Romanian financial system relies on bank loans ("bank-oriented").

3. The analysis of financial and prudential banking indicators in the Romanian

banking sector during 2007- 2013

Risk exposure of the banking system in the period analyzed is evidenced by the evolution of key

financial and prudential indicators. Table no. 2 shows a trend analysis of the main indicators of analysis of

banking system, namely prudential indicators and indicators of bank performance during the crisis and post

crisis.

Table no. 2 Key indicators off banking system (2007-2013)

Indicator 2007 2008 2009 2010 2011 2012 2013

Capital Suitability

Solvency report 1 (>8%) 13,8 13,76 14,67 15,02 14,87 14,94 15,46

Leverage effect or Tier (Tier / Total

assets) 7,32 8,13 7,55 8,11 8,07 8,02 7,96

Assets Quality

Overdue and doubtful loans /

Total loans (net value) 0,22 0,32 1,5 2,28 2,51* 12,00 11,64

Total debt outstanding and doubtful /

Total assets (net value) 0,17 0,29 1,01 1,47 1,70* 7,05 6,50

Credit risk * 4,0 5,95 13,53 18,36 23,28 29,91 32,14

Non-Performing Loans Rate 7,89 11,85 14,33 18,24 21,87

Liquidity Indicator 2,13 2,47 1,38 1,36 1,47 1,57 1,68

Profitability

ROA (Profit net / Total assets) 1,01 1,56 0,25 -0,16 -0,23 -0,64 0,01

ROE (Profit net / Liabilities) 9,43 17,04 2,89 -1,73 -2,56 -5,92 0,13

* Unadjusted exposure on loans and interest under "doubtful" and "loss" / Total loans and assigned interest,

including off-balance sheet

Source: www.bnr.ro, Annual Report for 2007, 2008, 2009, 2010, 2012, 2013

3.1. The Quality of the Assets

111

Annals of the „Cons tantin Brâncuşi” Univers i ty of Târgu J iu, Economy S eries , Is s ue 2 /2015

„ACADEMICA BRÂNCUŞI” PUBLISHER, ISSN 2344 – 3685/ISSN-L 1844 - 7007

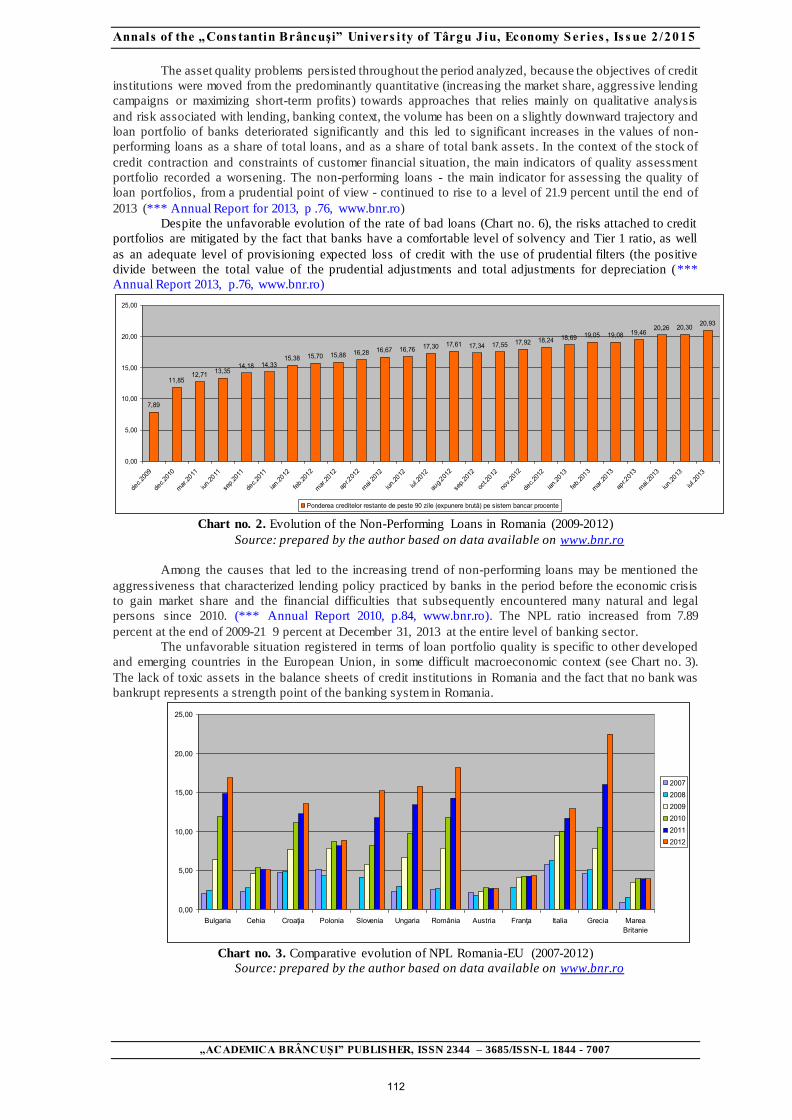

The asset quality problems persisted throughout the period analyzed, because the objectives of credit

institutions were moved from the predominantly quantitative (increasing the market share, aggressive lending

campaigns or maximizing short-term profits) towards approaches that relies mainly on qualitative analysis

and risk associated with lending, banking context, the volume has been on a slightly downward trajectory and

loan portfolio of banks deteriorated significantly and this led to significant increases in the values of non-

performing loans as a share of total loans, and as a share of total bank assets. In the context of the stock of

credit contraction and constraints of customer financial situation, the main indicators of quality assessment

portfolio recorded a worsening. The non-performing loans - the main indicator for assessing the quality of

loan portfolios, from a prudential point of view - continued to rise to a level of 21.9 percent until the end of

2013 (*** Annual Report for 2013, p .76, www.bnr.ro)

Despite the unfavorable evolution of the rate of bad loans (Chart no. 6), the risks attached to credit

portfolios are mitigated by the fact that banks have a comfortable level of solvency and Tier 1 ratio, as well

as an adequate level of provisioning expected loss of credit with the use of prudential filters (the positive

divide between the total value of the prudential adjustments and total adjustments for depreciation (***

Annual Report 2013, p.76, www.bnr.ro)

7,89

11,8512,71 13,35

14,18 14,3315,38 15,70 15,88 16,28 16,67 16,76 17,30 17,61 17,34 17,55 17,92 18,24 18,69 19,05 19,08 19,46

20,26 20,30 20,93

0,00

5,00

10,00

15,00

20,00

25,00

dec.2

009

dec.2

010

mar.20

11

iun.20

11

sep.2

011

dec.2

011

ian.20

12

feb.20

12

mar.20

12

apr.2

012

mai 20

12

iun.20

12

iul.20

12

aug.2

012

sep.2

012

oct.2

012

nov.2

012

dec.2

012

ian.20

13

feb.20

13

mar.20

13

apr.2

013

mai.20

13

iun.20

13

iul.20

13

Ponderea creditelor restante de peste 90 zile (expunere brută) pe sistem bancar procente

Chart no. 2. Evolution of the Non-Performing Loans in Romania (2009-2012)

Source: prepared by the author based on data available on www.bnr.ro

Among the causes that led to the increasing trend of non-performing loans may be mentioned the

aggressiveness that characterized lending policy practiced by banks in the period before the economic crisis

to gain market share and the financial difficulties that subsequently encountered many natural and legal

persons since 2010. (*** Annual Report 2010, p.84, www.bnr.ro). The NPL ratio increased from 7.89

percent at the end of 2009-21 9 percent at December 31, 2013 at the entire level of banking sector.

The unfavorable situation registered in terms of loan portfolio quality is specific to other developed

and emerging countries in the European Union, in some difficult macroeconomic context (see Chart no. 3).

The lack of toxic assets in the balance sheets of credit institutions in Romania and the fact that no bank was

bankrupt represents a strength point of the banking system in Romania.

0,00

5,00

10,00

15,00

20,00

25,00

Bulgaria Cehia Croaţia Polonia Slovenia Ungaria România Austria Franţa Italia Grecia MareaBritanie

200720082009201020112012

Chart no. 3. Comparative evolution of NPL Romania-EU (2007-2012)

Source: prepared by the author based on data available on www.bnr.ro

112

Annals of the „Cons tantin Brâncuşi” Univers i ty of Târgu J iu, Economy S eries , Is s ue 2 /2015

„ACADEMICA BRÂNCUŞI” PUBLISHER, ISSN 2344 – 3685/ISSN-L 1844 - 7007

Regarding the dynamics of prudential indicators we can notice the fact that during the same period it

was influenced by the slowdown in lending, and the manifestation of the international financial crisis, and the

growth of equity, maintaining a high level of solvency. In a competitive economy governed by the principle

of profitability, credit institutions in the local banking landscape have demonstrated the skills acquired

effective financial risk management.

3.2.Capital Suitability The solvency is an important indicator of prudence that characterizes the suitability of bank capital

at risk. The development of the indicators like capital suitability is favorable, solvency of the banking system

hovering above the minimum required, which is the result of constant monitoring exercised by the central

bank to credit institutions and intensified in the context of significant deterioration of operating conditions.

Since 2010 we saw a slowing growth trend of the solvency ratio compared to previous years. A significant

contribution to the capital suitability registration parameter values had the disposal of the supervisory

authority, since the second half of 2008, measures to improve banks' capital suitability. Some of the most

important measures are: the establishment in the case of some banks of a reporting system different from the

regulated one, consisting of monthly reporting of the solvency ratio; raising and maintaining a certain level of

solvency, higher than minimum requirement, in accordance with the risk profile of the bank; maintaining its

funds in order to provide a solvency ratio of at least 10 percent (www.bnr.ro, *** Annual Report 2009, p.

65).

Also, a significant contribution has been provided by the financial assistance program agreed with

the EU-IMF-IFI at the beginning of 2009, together with an intensifying global financial crisis, registered by

the fiscal and personnel policy in the previous year.

In parallel, at the initiative of the International Monetary Fund, the central banks of the nine largest

foreign banks (Erste Group Bank, Raiffeisen Group, Eurobank EFG, National Bank of Greece, UniCredit

Group, Société Générale, Alpha Bank, Volksbank International and Piraeus Bank.), which operate on the

Romanian market, have signed letters of commitment to maintain the exposure towards Romania during the

stand-by operation and proactively increase in capitalization in accordance with the requirements of National

Bank of Romania. At the meeting of the European Initiative on banking coordination in March 2011, nine

central banks of major subsidiaries in Romania reaffirmed their long-term commitment to Romania,

including the maintenance of capitalization well above the 11 percent recorded by all credit institutions in

Romania at the time, without formally committed to maintain a certain level of exposure.

Under these circumstances, the indicator of capital suitability in the banking system is relatively

robust and exceeds the regulatory minimum level (Chart no. 4) with an average of 6%, a level that ensures

banks in Romania the minimum conditions for additional capital requirements related to Basel III framework

(which provide among others, the introduction of two additional segments of capital represented by a fixed

damper of conservation the capital and a damper of countercyclical capital).

13,8 13,7614,67 15,02 14,87 14,94

15,46

7,328,13

7,558,11 8,07 8,02 7,96

0

2

4

6

8

10

12

14

16

18

2007 2008 2009 2010 2011 2012 2013

Raport de solvabilitate 1 (>8%)

Efectul de pârghie sau Rata fondurilor proprii

de nivel I (Fonduri proprii de nivel I / Totalactive)

Chart no. 4. Evolution of the capital suitability indicators

Source: prepared by the author based on data available on www.bnr.ro

Across the period under review, all credit institutions recorded levels above the minimum required

solvency requirements which means that they are adequately capitalized. (*** The European Central Bank -

Financial Stability Review, www.ecb.eu (December 2009). Appropriate level of capitalization was supported

by regulatory and supervisory measures taken by the central bank.

The high share of Tier 1 (91.1 percent), the capital items of good and very good quality, but also the

high levels of solvency indicators outlines an important advantage for the Romanian banking system,

creating thus the proper prerequisites for a proper implementation of the additional capital requirements

imposed by Basel III.

113

Annals of the „Cons tantin Brâncuşi” Univers i ty of Târgu J iu, Economy S eries , Is s ue 2 /2015

„ACADEMICA BRÂNCUŞI” PUBLISHER, ISSN 2344 – 3685/ISSN-L 1844 - 7007

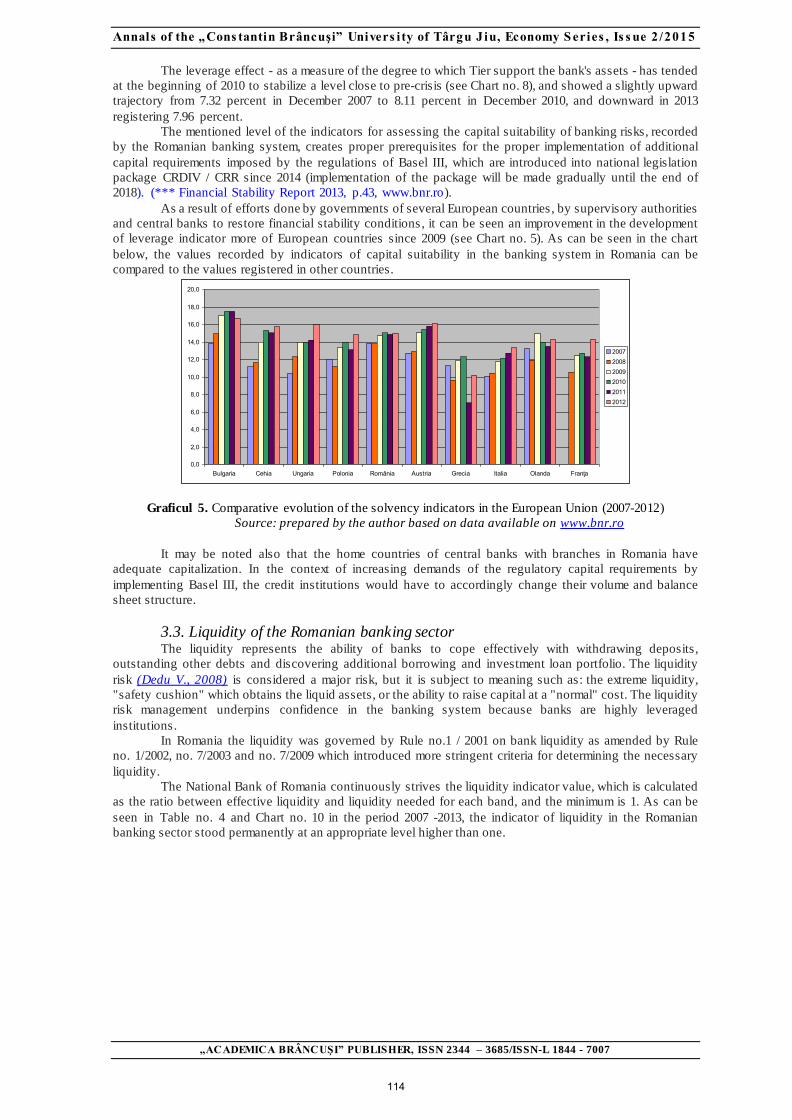

The leverage effect - as a measure of the degree to which Tier support the bank's assets - has tended

at the beginning of 2010 to stabilize a level close to pre-crisis (see Chart no. 8), and showed a slightly upward

trajectory from 7.32 percent in December 2007 to 8.11 percent in December 2010, and downward in 2013

registering 7.96 percent.

The mentioned level of the indicators for assessing the capital suitability of banking risks, recorded

by the Romanian banking system, creates proper prerequisites for the proper implementation of additional

capital requirements imposed by the regulations of Basel III, which are introduced into national legislation

package CRDIV / CRR since 2014 (implementation of the package will be made gradually until the end of

2018). (*** Financial Stability Report 2013, p.43, www.bnr.ro).

As a result of efforts done by governments of several European countries , by supervisory authorities

and central banks to restore financial stability conditions, it can be seen an improvement in the development

of leverage indicator more of European countries since 2009 (see Chart no. 5). As can be seen in the chart

below, the values recorded by indicators of capital suitability in the banking system in Romania can be

compared to the values registered in other countries.

0,0

2,0

4,0

6,0

8,0

10,0

12,0

14,0

16,0

18,0

20,0

Bulgaria Cehia Ungaria Polonia România Austria Grecia Italia Olanda Franţa

200720082009201020112012

Graficul 5. Comparative evolution of the solvency indicators in the European Union (2007-2012)

Source: prepared by the author based on data available on www.bnr.ro

It may be noted also that the home countries of central banks with branches in Romania have

adequate capitalization. In the context of increasing demands of the regulatory capital requirements by

implementing Basel III, the credit institutions would have to accordingly change their volume and balance

sheet structure.

3.3. Liquidity of the Romanian banking sector The liquidity represents the ability of banks to cope effectively with withdrawing deposits,

outstanding other debts and discovering additional borrowing and investment loan portfolio. The liquidity

risk (Dedu V., 2008) is considered a major risk, but it is subject to meaning such as: the extreme liquidity,

"safety cushion" which obtains the liquid assets, or the ability to raise capital at a "normal" cost. The liquidity

risk management underpins confidence in the banking system because banks are highly leveraged

institutions.

In Romania the liquidity was governed by Rule no.1 / 2001 on bank liquidity as amended by Rule

no. 1/2002, no. 7/2003 and no. 7/2009 which introduced more stringent criteria for determining the necessary

liquidity.

The National Bank of Romania continuously strives the liquidity indicator value, which is calculated

as the ratio between effective liquidity and liquidity needed for each band, and the minimum is 1. As can be

seen in Table no. 4 and Chart no. 10 in the period 2007 -2013, the indicator of liquidity in the Romanian

banking sector stood permanently at an appropriate level higher than one.

114

Annals of the „Cons tantin Brâncuşi” Univers i ty of Târgu J iu, Economy S eries , Is s ue 2 /2015

„ACADEMICA BRÂNCUŞI” PUBLISHER, ISSN 2344 – 3685/ISSN-L 1844 - 7007

2,13

2,47

1,38 1,361,47

1,571,68

0

0,5

1

1,5

2

2,5

3

2007 2008 2009 2010 2011 2012 2013

Indicatorul de lichiditate

Chart no. 6 Evolution of the liquidity indicator in 2007-2013

Source: prepared by the author based on data available on www.bnr.ro

The values registered by the indicator of liquidity in the Romanian banking system indicates the

existence of reserves ready to cover any imbalances that may arise as a result of early withdrawal of

resources. Liquidity established according to regulations issued by the National Bank of Romania calculated

for all operations with Romanian currency (RON), maturity ladder was placed at a comfortable level, higher

than the regulated one (1) on each maturity band. The level registered by the liquidity indicators is due to

maintaining depositor’s confidence in the Romanian banking system and the confidence of foreign investors

and domestic depositors in banks and therefore their willingness to extend maturing deposits. This led to a

gradual reduction of the dependence on external financing banks.

3.4. Profitability of the Romanian banking sector The negative values registered by the profitability indicators are due to some extent to the fact that

Romanian banks focused during the crisis, but also the post crisis, on management solutions of non-

performing exposures and less on continuation of the lending in sustainable conditions.

At the end of 2008 (Chart no. 7) the key indicators of profitability had a significant higher level

(1.56 percent and 17.04 percent) than in December 2007 (1.01 percent and 9.43 percent). This was due on

one hand, to the sale of the share stake held by four banks in the capital of an insurance company and, on the

other hand, to the growth of income in net interest.

The year 2009 was characterized by restriction of both supply and demand for loans, which brought

the interruption of the upward trend of lending activity. Faced with the stagnating process of the lending

activity, with the increasing process of provisioning and with the increasing process of financing costs, banks

have tried to mitigate the diminishing profit by resizing networks expanded aggressively in recent years, by

closing their units and restructuring their personnel. Although faced with these difficulties, the banking

system managed to end the year 2009 with a profit of 680 million, and the aggregate profits fell more than 5

times over the previous year, mainly due to unprecedented increase in provisioning costs (from 7,593. 9

million Lei to 14,972.7 million Lei), due to the high level of non-performing loans (*** annual Report 2009,

p. 79-84 www.bnr.ro).

1,01 1,560,25

-0,16 -0,23 -0,64

0,01

9,43

17,04

2,89

-1,73-2,56

-5,92

0,13

-10

-5

0

5

10

15

20

2007 2008 2009 2010 2011 2012 2013

ROA (Profit net / Total activ)ROE (Profit net / Capitaluri proprii)

Chart no. 7. Evolution of the banking profitability indicators (2007-2013)

Source: prepared by the author based on data available on www.bnr.ro

115

Annals of the „Cons tantin Brâncuşi” Univers i ty of Târgu J iu, Economy S eries , Is s ue 2 /2015

„ACADEMICA BRÂNCUŞI” PUBLISHER, ISSN 2344 – 3685/ISSN-L 1844 - 7007

In this context, the profitability indicators registered modest values in 2009, but although positive:

0.25 percent for ROA (1.56 percent the previous year) and 2.89 percent for ROE (17.04 percent in 2008) (see

table no. 2). In the chart no. 7 it is noted that 2010 marked the profitability in a negative way, a trend that

continued in subsequent years of the period under review, with the exception of 2013 when an improvement

encountered in banking activity. The positive values of financial profitability placed slightly above zero the

key indicators of profitability at aggregate level (rate of financial profitability - ROE and rate of economic

profitability - ROA). Although banks have resorted to exercise a tighter control on cost / income indicator

and to a careful risk management, the Romanian banking system registered important losses in the period

under review except 2013, due to the depreciation of financial assets and the effect induced by revaluation of

collateral for loans. After three years of financial losses, the Romanian banking system has managed to

improve its profitability during 2013, achieving positive financial results. The unfavorable economic climate,

the trends of decreasing of the industrial production and construction investment, due to a constant decline in

demand, the budget deficit and accelerated decline in the number of employees are just some of the factors

that led to the decline of financial health indicators in the banking sector in Romania. Although, the financial

and prudential banking indicators indicates a stable banking system, well-capitalized, with sufficient liquidity

indicator, able to withstand shocks. Suitable values recorded by prudence and financial performance

indicators are due to the fact that the National Bank of Romania in the period analyzed had an intense activity

in the field of prudential regulation, bank supervision and appropriate risk management system.

We think that the banking system was characterized by consolidation of solvency and liquidity

indicators, performances that were registered by the credit institutions with foreign capital from countries

strongly affected by the sovereign debt crisis such as Greece, Italy.

4. CONCLUSIONS

An impediment to the development process of the banking sector was, apart the difficult

macroeconomic environment, the low level of economic and financial-banking culture of the population. In

this study were analyzed indicators of the banking system, the analysis is presented in the form of charts and

figures to highlight the differences between the values registered by them in the period under review.

The analysis of the financial health indicators in the Romanian banking sector indicate their

deterioration over the period analyzed, but nevertheless the Romanian banking system remains robust and

shock resistant even during the financial crisis. This can be explained by the low level of debt (leverage) and

the dominant character of traditional banking, based on lending, against securitization transactions, the off-

balance sheet transactions and investment banking activities.

We can say that the appropriate level of key prudential indicators will allow the banking sector to

face in the future, without major difficulties, the volatility of foreign capital flows, the increasing non-

performing loans and loan portfolios, and also the need to optimize credit portfolios, in order to prepare the

implementation of Basel III. In conclusion the study, noted that it is difficult to quantify certain trends in the

evolution of banking systems worldwide and national default.

5. BIBLIOGRAPHY

1. Allen, F. & Gale, D., (2000). Comparing Financial Systems. Cambridge: The MIT Press.

2. Apetri, A., (2013), The banking system in Romania - Developments and Prospects , Publishing

House „Didactică şi Pedagogică”, R.A., Bucharest

3. Basno, C., Dardac, N. (2002), Banking Management, Editura Economică , Bucharest, Romania.

4. Bogza, M., (2002), The banking system in Romani– 12 years of transition, in the first decade of

banking reform in Romania, Symposium banking history and civilization "Cristian Popişteanu" ,

Buccharest, vol.1

5. Berea, A. A. P ,(2003), Modernization of the Banking System, Editura Expert, Bucureşti

6. Beju, D., (2005), Monetary mechanisms and banking institutions , Ed. Casa Cărţii de Ştiinţă, Cluj-

Napoca

7. Cocriş, V. ,(1992), Techniques and banking operations , Editura Universităţii Al. I. Cuza., Iaşi

8. Corrigan E. G., (1982) . Are Banks Special, Federal Reserve Bank, Annual Report

9. Dănilă, N ,(2000,) The privatization of banks , Editura Economică, Bucureşti

10. Dardac, N, Barbu, T. ,(2005) , Monedă, bănci şi politici monetare, Editura Didicatică şi Pedagocică,

R.A.,Bucureşti

11. David., D., (2013), Trends in the evolution of the banking sector in Romania, study published in the

book “Post-doctoral studies in economics”. Post-doctoral dissertation, Publishing House.

Academiei Române

12. Dardac, N., Privatization and banking restructuring lecture notes, www.ase.ro

116

Annals of the „Cons tantin Brâncuşi” Univers i ty of Târgu J iu, Economy S eries , Is s ue 2 /2015

„ACADEMICA BRÂNCUŞI” PUBLISHER, ISSN 2344 – 3685/ISSN-L 1844 - 7007

13. Demirguç-Kunt, A. & Levine, R., eds. (2001), Financial Structure and Economic Growth. A Cross -

Country Comparison of Banks, Markets, and Development. Cambridge: The MIT Press.

14. Dedu V., (2008), Management and banking audit, Editura Economică

15. Fîrţesu, B.N., (2013), Reform of the financial-banking system of post-communist Romania,

published in the book “Post-doctoral studies in economics”. Post-doctoral dissertation, Ed.

Academiei Române

16. Heteş. I., (2008) Operations of credit institutions , Ed. Universităţii de Vest, Rimişoara

17. Hlaciuc, E., (2000), Banking Accounting, Editura Universității Stefan cel Mare, Suceava

18. Hartmann, P., Heider, F., Papaioannou, E. & Lo Duca, M., (2007), The role of financial markets

and innovation in productivity and growth in Europe. European Central Bank Occasional Paper

No. 72.

19. Isărescu, M., (2002), Banking reform in Romania: 1990-2002, the first decade of banking reform in

Romania, The symposium on banking history and civilization "Cristian Popişteanu" , Bucureşti,

vol.1

20. Isărescu M., (2001). Economic reflections. Markets. Money. Banks . Editura Expert Bucureşti

21. Isăresu M., (2006). Economic reflections - Policies of the National Bank of Romania, Editura Expert

Romania

22. Isărescu M., (2009), Theoretical and practical contribution to monetary and banking policies ,

Editura Academiei Române, Bucureşti

23. Kiriţescu C. ,(1997), The cash system of the Romanian currency “Leu” and its precursors , vol. I,

Editura Enciclopedică, Bucureşti

24. Mihai, I., (2003),Technique and management of the banking operations, Editura Expert, Bucureşti

25. Rose, Martin and Milton Marquis, (2010). Money and Capital Markets. McGraw-Hill

26. Stoica, M., (1999), Banking management, Editura Economică, Bucureşti

27. Turliuc, V., Cocriş, V. ,(1997), Currency and Credit, Editura Ankarom, Iaşi

28. Trenca I., (2008), Banking methods and techniques – regulatory principles, experiences , Ed. Casa

Cărţii de Ştinţă, Cluj-Napoca

29. Trenca, I., (2007), Basis of the Financial Management, Casa Cărtii de Ştiinţa Cluj-Napoca

30. Turliuc, V., Basno, C., (1978), Monetary circulation and credit, Editura Universităţii Al. I. Cuza,

Iaşi

31. Turliuc, V. Cocriş, V., (1997), Currency and Credit, Editura AnkaRom, Iaşi

32. Ursu, S.G., (2013), Restructuring financial - banking system under the impact of the financial and

economic crisis started in August 2007, a study published in the book “Post -doctoral studies in

economics”. Post-doctoral dissertation, Ed. Academiei Române

33. *** Annual report for 2001, www.bnr.ro

34. *** Report on the financial stability for 2006, www.bnr.ro

35. *** Report of financial stability for 2013, www.bnr.ro

36. *** Annual report for 2009, www.bnr.ro

37. *** Annual report for 2010, www.bnr.ro

38. *** Annual report for 2013, www.bnr,ro

39. *** European Central Bank - Financial Stability Review, (December 2009), www.ecb.eu

117