Embed Size (px)

Citation preview

The Allowance for

Loan Losses:

Critical Issues for

Credit Union Leaders

Michael J. Sacher, CPASacher Consulting

Foreword by Dr. Harold M. SollenbergerProfessor Emeritus of Accounting and Information Systems

Michigan State University

ideas grow here

PO Box 2998

Madison, WI 53701-2998

Phone (608) 231-8550

www.filene.org PUBLICATION #243 (7/11)

The Allowance for

Loan Losses:

Critical Issues for

Credit Union Leaders

Michael J. Sacher, CPASacher Consulting

Foreword by Dr. Harold M. SollenbergerProfessor Emeritus of Accounting and Information Systems

Michigan State University

Copyright © 2011 by Filene Research Institute. All rights reserved.Printed in U.S.A.

Deeply embedded in the credit union tradition is an ongoing

search for better ways to understand and serve credit union

members. Open inquiry, the free flow of ideas, and debate are

essential parts of the true democratic process.

The Filene Research Institute is a 501(c)(3) not-for-profit

research organization dedicated to scientific and thoughtful

analysis about issues affecting the future of consumer finance.

Through independent research and innovation programs the

Institute examines issues vital to the future of credit unions.

Ideas grow through thoughtful and scientific analysis of top-

priority consumer, public policy, and credit union competitive

issues. Researchers are given considerable latitude in their

exploration and studies of these high-priority issues.

The Institute is governed by an Administrative Board made

up of the credit union industry’s top leaders. Research topics

and priorities are set by the Research Council, a select group

of credit union CEOs, and the Filene Research Fellows, a blue

ribbon panel of academic experts. Innovation programs are

developed in part by Filene i3, an assembly of credit union

executives screened for entrepreneurial competencies.

The name of the Institute honors Edward A. Filene, the “father

of the U.S. credit union movement.” Filene was an innova-

tive leader who relied on insightful research and analysis when

encouraging credit union development.

Since its founding in 1989, the Institute has worked with over

one hundred academic institutions and published hundreds of

research studies. The entire research library is available online

at www.filene.org.

Progress is the constant replacing of the best there

is with something still better!

— Edward A. Filene

iii

Filene Research Institute

iv

The author would like to thank Bill Eckhardt, Daniel McCue, and

Norm West of Alaska USA Federal Credit Union for their encour-

agement and incisive feedback in the preparing of this report. In

addition to his generous foreword, Professor Harold Sollenberger

provided initial guidance and a welcome final review.

Filene would also like to acknowledge members of the Filene

Research Council and their staffs for their timely and helpful advice.

These members include:

• Gerry Agnes—Elevations Credit Union, Boulder, Colorado.

• Patricia Campbell—Christian Financial Credit Union, Roseville,

Michigan.

• Teresa Freeborn—Xceed Financial Federal Credit Union,

El Segundo, California.

• Laida Garcia—Florida Central Credit Union, Tampa.

• Steve Post—VSECU, Montpelier, Vermont.

Acknowledgments

v

Foreword vi

Executive Summary and Commentary vii

About the Author ix

Chapter 1 Introduction 2

Chapter 2 Relevant ALL Accounting Standards

and Principles 7

Chapter 3 A Sound ALL Approach for Credit Unions 17

Chapter 4 Q&E and TDR Factors 24

Chapter 5 Common ALL Mistakes: A Great Recession

Post-Mortem 29

Chapter 6 Final ALL Considerations 33

Endnotes 39

Table of Contents

vi

The seriousness of valuating loan portfolios cannot be overstated at

any time, much less during the recent past, present, and coming time

periods. Probably no other element in credit union financial report-

ing has as great an impact on a credit union’s reported earnings and

financial position. Equity levels that were once very strong have been

significantly impacted by loan losses and allowance account balances.

These losses have come from loans charged off as uncollectible, debt

restructurings, and foreclosures and from numerous other causes that

have reached levels unheard of over the lifetimes of every current

credit union manager.

Accounting for expected and even unexpected losses during this

unusual period has required careful application of both old account-

ing practices and newly instituted accounting rules and regulations.

Historic methods have had difficulties handling current loss volumes

while trying to fairly reflect a credit union’s true financial position.

Also, new directives from accounting authorities have, at times,

become moving targets. There is mounting uncertainty regarding the

adequacy of allowance for loan loss accounts and methodologies used

for calculating loan loss provisions, determining loan portfolio fair

values, and ensuring that the matching principle is actually working

properly.

This research report addresses a broad set of issues related to loan loss

accounting and reporting. The most troublesome issues surround

estimates of loan loss—how to make estimates, how to apply man-

agement judgment as to the probability of losses, how to determine

the adequacy of allowances, and how to account for these estimates.

With examples, actual experiences of the author, references to appro-

priate accounting regulations and standards, and a straightforward

attack on loan loss accounting and management, this report is an

excellent primer for credit union managers.

The author, Michael J. Sacher, is highly qualified to discuss these

critical financial and accounting issues. His prior experience includes

many years as an auditor of credit unions and a partner in a major

CPA firm. As a consultant, he has focused much of his work on

credit unions and on loan valuation problems. His knowledge

of accounting theory, the history and current status of financial

accounting reporting standards, credit union regulators’ needs,

and the CPA profession’s best practices for auditing and reporting

combine in a unique way to give insight into actual problems arising

from the financial crises of the past four years. Here, he combines the

theory, reporting requirements, financial market information needs,

and common sense into a clear picture of how credit union loan

valuation reporting should be handled.

Foreword

by Dr. Harold M. Sollenberger,

Professor Emeritus of Accounting and Information Systems

Michigan State University

vii

by Ben Rogers,

Research DirectorThe Washington Mutual (WaMu) collapse of 2009 stands as the

nation’s largest- ever bank failure. Economic, strategic, and market

challenges all coalesced against the thrift at the end, but the more

immediate cause of its failure was an insurmountable mismatch on

its balance sheet: bad loans overwhelmed the bank’s ability to stay

solvent. WaMu’s allowance for loan losses (ALL) was not big enough.

Today’s financial landscape is littered with the bones of banks and

credit unions alike done in by bad loans. But credit losses are a story

as old as banking itself: Financial institutions suffer, and some col-

lapse, when borrowers cannot (or will not) repay their loans. Regula-

tions and accounting standards are enacted with the best intent to

control and measure credit losses. But marketplace volatility exhib-

ited by devaluation of collateral and negative earnings has focused

increased scrutiny of the ALL. Add to the mix complex accounting

requirements heretofore not applicable to most credit unions and

the result has been confusion, disagreement, and contention over

the ALL.

What Is the Research About?The Allowance for Loan Losses: Critical Issues for Credit Union Lead-

ers illuminates the ground on which credit unions calculate their

particular allowance. Respected CPA and industry veteran Michael

Sacher unpacks the various accounting standards at play and matches

them with the expectations of CFOs and credit union examiners

alike. The result is a useful document that can be used as both a tem-

plate and a reference for finance managers, supervisory committee

members, and boards of directors walking the fine line between “too

much” and “not enough” ALL. In some cases the fate of the credit

union depends on that line.

The report breaks down into four parts:

• An introduction to the current ALL trends among US credit

unions.

• An examination of the relevant accounting standards and inter-

pretations, including credit union–specific guidance around

FASB and NCUA requirements.

• A model ALL approach for credit unions, with specific guidance

and suggestions for qualitative and environmental (Q&E) factors.

• Common ALL mistakes, a Great Recession post- mortem that

identifies specific areas for review for those involved in day-to- day

management or long- term supervision of the allowance.

Executive Summary and Commentary

viii

What Are the Credit Union Implications?This analysis of credit unions’ ALL deals directly with a pressing cur-

rent problem: What is the right way to reserve for credit losses? The

issue is made more challenging because it is not just a management

issue but a regulatory issue in which reasonable people with differing

perspectives often disagree. And for CFOs to disagree with examin-

ers, even respectfully, requires a firm basis in the relevant accounting

principles.

Several points in the report are particularly salient for credit unions

today:

• What goes up must come down. Loan loss and allowance trends

are at least stable and, in many cases, declining for a majority of

credit unions. This calls for a measured reanalysis of the ALL, and

credit unions should consider carefully the author’s suggestions

on how to formulate sound Q&E positions.

• Learn how to properly account for troubled- debt restructure

(TDR) loans and properly consider impairment for all loans that

do not meet the homogenous definition.

• History can be misleading. An overreliance on historical trends

and ratios accounted for some of credit unions’ ALL confusion at

the beginning of the crisis. Conversely, credit unions should not

dwell too much on midcrisis trends in building today’s allowance.

The turmoil of the last three years calls for a thorough review of

every credit union’s ALL policy.

• Track with the right tools. Included is a helpful list of analytical

tools and the factors boards of directors and supervisory commit-

tees should consider based on the metrics presented by financial

managers. It also provides a useful list of available ratios for

improved supervisory tracking.

The ALL is just one of many accounting variables that a credit union

should manage well. But its importance has been reinforced during

the Great Recession. This timely, tactical report will help your credit

union manage it better.

ix

Michael J. Sacher

Mike Sacher is a CPA with over 30 years’ experience providing ser-

vices to credit unions. Mike has earned a national reputation for his

expertise in areas such as accounting and finance, internal control,

asset liability management, and governance issues of importance to

credit unions. In 2008, Mike launched his own consulting prac-

tice, Sacher Consulting, with the goal of assisting credit unions as a

trusted business advisor and partner.

From 2001 to 2008, Mike was the partner in charge of the Los

Angeles office of McGladrey & Pullen’s National Credit Union Divi-

sion, where he oversaw the delivery of audit and consulting services

to over 150 credit unions annually ranging in size from $5 million

to $7 billion in assets. Mike was also the assurance leader of the

division, where he helped to resolve complex accounting and audit-

ing matters, and he led the firm’s efforts to customize the approach

to credit union audits. Prior to joining McGladrey & Pullen, Mike

was a senior partner in the O’Rourke Sacher & Moulton CPA firm,

which was acquired by McGladrey & Pullen in 2001.

In 2008, Mike became a member of the board of directors of Kaiser

Federal Bank, and he also serves as chairman of the Audit Com-

mittee. Mike is a member of the American Institute of Certified

Public Accountants and the California Society of Certified Public

Accountants.

Mike has a bachelor’s in Business Administration (Accounting Con-

centration) from California State University, San Francisco. He has

been a certified public accountant since 1978.

About the Author

CHAPTER 1Introduction

The objectives of this report are to clarify the accounting theory surrounding the allowance for loan losses, to discuss specific areas where errors have been common in credit unions, to provide best practices for consideration of management, and to discuss internal controls that are critical to the allowance for loan losses process.

3

The allowance for loan losses (ALL) is arguably the most important

accounting estimate in a credit union’s financial reporting structure.

Unlike many accounting applications that are precise and highly

objective by their very nature, determining the appropriate balance

of the ALL requires significant judgment by management. The severe

recession over the past few years, with its record levels of unemploy-

ment, housing value declines, skyrocketing delinquencies and charge-

offs, restructuring of troubled loans, and high level of foreclosures in

many areas of the United States, has significantly impacted manage-

ment of the ALL.

Many credit unions have struggled with the accounting principles

that define an appropriate ALL balance as well as practical meth-

ods for determining the balance on an ongoing basis. Accounting

standard setters and regulators—the Financial Accounting Standards

Board (FASB), the Securities and Exchange Commission (SEC),

the American Institute of Certified Public Accountants (AICPA),

the National Credit Union Administration (NCUA), and state

regulators—have been concerned about the ability of financial

institution management to manage earnings vis-à-vis building ALL

balances during periods of strong earnings and high credit quality

and depleting the ALL (and bypassing expense recognition) during

periods of declining earnings and weakened credit quality. Auditors

and regulators have challenged many credit unions on their approach

and have demanded significant upward adjustments to the ALL,

resulting in significant operating losses and reduced capital levels.

The objectives of this report are to clarify the accounting theory sur-

rounding the ALL, to discuss specific areas where errors have been

common in credit unions, to provide best practices for consideration

by management, and to discuss internal controls that are critical to

the ALL process.

4

Current ALL Trends Tell a StoryIn order to understand the impact of the deteriorating economy on

credit unions over the past few years, consider the following statistics

as portrayed in the accompanying figures.

The delinquency ratio (loans over 60 days delinquent divided by

total loans) has increased substantially over the past few years, with

credit unions in the “sand states” (California, Nevada, Arizona, and

Florida) significantly exceeding the national peer group averages (see

Figure 1). However, it appears that delinquencies have reached a

plateau, and hopefully a downward trend is developing.

In response to rising delinquency, the ALL as a percentage of loans

outstanding has significantly increased over the past few years, espe-

cially in the sand states (see Figure 2).

With rapidly increasing charge-offs, the ALL became inadequate to

absorb one year’s worth of net charge-offs for many credit unions,

a tell-tale signal of ALL understatement (see Figure 3). However, it

appears that as credit unions stepped up ALL funding in 2009–2010,

the current ALL balances were much more adequate.

The Great Recession led to a remarkable increase in provision for

loan loss (PLL) expense, which has significantly eroded earnings over

the past few years (see Figure 4). Note that PLL averaged less than

0.5% of average assets prior to the current economic cycle.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Q1 Q2

20062005

Delin

quen

cy ra

tio (p

erce

nt)

Q4 Q3 Q4 Q1 Q2 Q3 Q1Q4 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2007 2008 2009 2010

Sand statesUS overall

Figure 1: Delinquent Loans as a Percentage of Total Credit Union Loans

Source: NCUA, Callahan & Associates.

5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Q1 Q2

20062005

Q4 Q3 Q4 Q1 Q2 Q3 Q1Q4 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2007 2008 2009 2010

ALL

(per

cent

age

of to

tal l

oans

)

Sand statesUS overall

Figure 2: ALL as a Percentage of Total Loans

Source: NCUA, Callahan & Associates.

Sand statesUS overall

0

50

100

150

200

250

Q1 Q2

20062005

Q4 Q3 Q4 Q1 Q2 Q3 Q1Q4 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2007 2008 2009 2010

Net c

harg

e-of

fs (p

erce

ntag

e of

prio

r-ye

ar A

LL)

Figure 3: Net Charge-Offs as a Percentage of Prior-Year ALL

Source: NCUA, Callahan & Associates.

6

The level of PLL quadrupled to 2% for the sand states and doubled

to over 1% for all credit unions in the United States. Consider that

total net income during the “best of years” for the industry was in

the range of 1% of average assets (1% return on assets).

0.0

0.5

1.0

1.5

2.0

2.5

Q1 Q2

20062005

PLL

(per

cent

age

of a

vera

ge a

sset

s)

Q4 Q3 Q4 Q1 Q2 Q3 Q1Q4 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2007 2008 2009 2010

Sand statesUS overall

Figure 4: PLL as a Percentage of Average Assets

Source: NCUA, Callahan & Associates.

Credit unions are required to adhere to gener-ally accepted accounting principles (GAAP). This chapter reviews and clarifies those that are most relevant and most likely to affect a credit union’s allowance practices.

CHAPTER 2Relevant ALL Accounting Standards and Principles

8

About Accounting Standards ReferencesAt the end of 2009, the FASB implemented the Accounting Stan-

dards Codification (ASC), which supersedes the prior accounting

standards set by FASB and other accounting standard setters (SEC,

AICPA, etc.). Those previous standards that were still effective upon

adoption of the ASC were combined into the new ASC and were

given new topical references. This report makes references to the new

ASC, and in some cases also references the original FASB opinion

number to facilitate a reference that might be known to the reader by

the original FASB reference.

What Is the ALL?The ALL represents an estimate of losses that have been incurred on

loans in the portfolio that are considered to be “impaired” as of the

balance sheet date, based in part on review of individual loans and

in part on high- level analytics of groups of loans sharing common

risk characteristics. Credit unions are also familiar with the allowance

for loan and lease losses (ALLL) designation, but because leases are

usually a minimal slice of credit union portfolios, we use the simpler

terminology throughout this report. It should be noted that the ALL

is also referred to as the allowance for credit losses, since the same

accounting requirements apply to other receivables in addition to

loans to borrowers made by financial institutions.

The following overview of the ALL is given in the ASC:

The allowance for credit losses shall be established at a level that is

adequate but not excessive to cover probable credit losses related to

specifically identified loans as well as probable credit losses inherent

in the remainder of the loan portfolio that have been incurred as of

the balance- sheet date. Impairment shall not be recognized before

9

it is probable that impairment has occurred, even though it may be

probable that impairment will occur in the future. The measurement

of credit losses in a portfolio of loans and receivables consists of two

parts: reviewing specifically identified loans and estimating credit

losses in the remaining portfolio.1 [Underlining added for emphasis.]

There are several critical points (underlined by the author in the

above paragraph) that are worthy of further comment.

Adequate but Not ExcessiveAn inadequate ALL results in overstated assets, overstated earnings,

and overstated capital. An excessive ALL results in understated assets,

understated earnings, and understated capital. In either case, the

financial statements are misstated. The goal is to get a reasonable

ALL properly supported by appropriate analytics. Due to the great

degree of subjectivity in many of the factors used in the determina-

tion of the ALL, management must exercise due care not to manage

earnings by either understating or overstating the ALL. Earnings

management is not acceptable and can result in harsh criticism of

those charged with corporate governance.

Probable Credit LossesThe term “probable” is not defined by mathematical percentages.

However, the accounting standards define a range of outcomes,

including remote, reasonably possible, and probable. This range of

probability was originally defined in SFAS Statement 5, “Accounting

for Contingencies” (March 1975). The ALL is not meant to measure

loans that have less than a probable chance of not paying interest and

principal according to their contractual terms. Great care must be

taken by preparers of financial statements to ensure that ALL calcula-

tion methods properly meet the “probable” threshold.

Incurred As of the Balance-Sheet DateNot only must the loss rise to a level of probable, but the underly-

ing event that gave rise to the loss must have occurred prior to the

balance- sheet date. This is a critical concept misunderstood by many.

Currently, GAAP in the United States operate under what is referred

to as an incurred loss model. Before an ALL is recognized, the cir-

cumstances giving rise to a loss must have already occurred (and be

estimable). Consideration is being given to adopting an expected loss

model, wherein losses would be recognized based on expectations of

probable future events that will have a direct impact on the collect-

ibility of principal and interest amounts contractually due. There is

10

strong opposition in the financial services industry to the expected

loss model, which is being considered due to the convergence of US

GAAP with international standards. However, regulators may in fact

prefer the expected loss model, as it is believed to be more forward-

looking and may eliminate some volatility created by the current

accounting guidance.

Reviewing Specifically Identifiable LoansIt is critical to recognize that retail financial institutions such as

credit unions have hundreds or perhaps many thousands of loans to

individual consumers. It would be virtually impossible to evaluate

each loan for impairment on a regular basis. However, certain loans

must be individually evaluated once they no longer fit within other

homogenous loan categories. The following types of loans are typi-

cally evaluated on an individual basis:

• Individually significant loans, including member business loans

that do not have homogeneous risk characteristics.

• Loans that have already been identified as having credit problems,

such as TDRs, loans delinquent over a predetermined period such

as 60 days, bankruptcies and other collection accounts, loans in

process of foreclosure, and loans where borrowers have requested

short sales.

• Other loans that are no longer accruing interest.

This ALL component is commonly referred to as the specific valua-

tion reserve (SVR).

Estimating Credit Losses in the Remaining PortfolioOnce those loans that are individually evaluated for impairment are

identified, the remaining portfolio is typically evaluated based on

both analytical and qualitative considerations of each major loan cat-

egory. Consideration is given to levels of past charge-offs by category,

current economic trends, quality of and changes in underwriting,

value of underlying collateral, and other related factors.

This ALL component is commonly referred to as the general valua-

tion reserve (GVR). It is critical to understand that the GVR is still a

measure of probable losses as of the balance- sheet date. However, the

manner of estimating those losses is much less precise than the SVR

estimation, since various categories of loans are being pooled and

impairment assessed using high- level analytical techniques.

11

The Evolution of an Impaired LoanTo set the stage for the technical matters, let’s consider the various

phases of a “bad” consumer loan from origination to charge-off.

Upon origination of a consumer loan (auto, mortgage, unsecured,

etc.), the credit union’s underwriting process considers the borrower’s

ability and willingness to repay by evaluating income levels, employ-

ment status, credit score, collateral value, and other appropriate

underwriting metrics. As evidenced by historical industry charge-off

rates, underwriting processes usually result in loans to borrowers

who make principal and interest payments throughout the term of

the loan according to the contractual provisions, and no credit losses

are sustained.2 Occasionally, however, despite the best underwriting

efforts, a loan loss is incurred and a charge-off is recorded.

Typically, there is a loss event3 leading to a loan loss that can be iden-

tified with 20/20 hindsight. The borrower may have lost their job,

the borrower or a close family member may have had a serious illness

or died, or a natural disaster such as an earthquake, fire, or flood may

have occurred. Once the loss event occurs, the potential credit prob-

lems typically become known to management because a payment is

missed and the loan becomes delinquent (a loss event indicator). Or,

in today’s environment, a borrower who is not even delinquent may

contact the credit union and advise of their inability (or unwilling-

ness) to continue making payments on their loan. Ultimately, a loss

is confirmed once the delinquency exceeds a set period of time or

other conditions (such as a short sale or foreclosure) are initiated.

This is referred to as loss confirmation.

To illustrate the impact on the ALL, consider a hypothetical situa-

tion in which we have one loan in our entire loan portfolio. Every

month, we review this loan for the purpose of identifying whether a

loss event has occurred. Six months after the origination of the loan,

we identify that the borrower lost their job. Even though the loan is

not yet delinquent at the end of month six, we are in a position to

assess the likelihood of this event impairing the borrower’s intent or

ability to repay principal and interest according to the contractual

terms of the loan. We can certainly conclude that the risk of loss is

higher upon the loss of employment than it was prior to this event

having occurred. Depending on other factors, such as the borrower’s

willingness and ability to continue making loan payments, we might

conclude that the risk of loss is still remote, or reasonably possible,

or probable. If our conclusion is that a loss is probable, we establish

12

an ALL in month six, even though the loan is not yet delinquent. If

we conclude that the risk of loss is less than probable, we continue to

monitor the loan, and if the risk of loss rises to a level of probable, at

that time an ALL for that loan is established. Importantly, the loss of

employment in this example prompts a greater need to evaluate the

risk of loss and to document the rationale for conclusions regarding

impairment.

This hypothetical example is illustrative of the complexity involved

in ALL theory. First, we need to determine whether a loss event

has occurred. Then, we must assess whether the impact of the loss

event will result in the inability of the borrower to repay principal

and interest according to the contractual terms of the loan. Lastly,

once the likelihood rises to a level of probable, we must estimate the

amount of the inherent loss arising from the loss event. Now imag-

ine the additional complexity of extrapolating this thought process

to various loan segments within the credit union, where each loan

segment might contain thousands of individual loans originated over

the course of several years.

The critical points illustrated by this example are:

• The ALL is a measure of expected losses incurred for loans that

have experienced a loan loss event, the event rendering it prob-

able that principal and interest will not be collected based on the

contractual terms of the loan.

• Although delinquency is an early indicator that a loan loss event

has occurred, delinquency alone is not a loss event and cannot be

solely relied upon to drive the ALL calculation.

• The likelihood scenario required before a loan loss provision is

recorded must be probable as compared to remote or reason-

ably possible as these outcomes are defined in the accounting

standards.

Is the ALL a Fair Value Adjustment?The ALL is not a fair value adjustment. Imagine having a seasoned

portfolio of consumer auto loans totaling $100 million (M). Some

loans in the portfolio were originated very recently. Other loans

have various origination dates, and the average remaining life of the

portfolio is approximately two years. The credit union has histori-

cally incurred losses of approximately 1% per year. For discussion

purposes, let’s assume the economy has been stable over the past few

years (we wish!). For ALL purposes, the credit union has an ALL bal-

ance approximating the one-year loss ratio ($1M), and therefore the

portfolio’s net book value is $99M.

13

Now, imagine the variables that would enter into estimating the fair

value of this portfolio. Said differently, how much would a willing

buyer pay to acquire the portfolio? Would the buyer offer book value

($99M)? Not likely. The buyer would most likely consider the fol-

lowing factors:

• How much in cumulative credit losses will be incurred over the

life of the portfolio and what will the timing of such losses be? The

fair value assessment would extend way beyond the parameters

embedded in the ALL calculation. The buyer is not concerned

with whether the losses meet the “probable” accounting defini-

tion or whether the loss events have already occurred. These are

concepts invented by accountants, and they have little bearing on

the determination of fair value in a free market.

• What is the average life of the portfolio, and what is the rate of

prepayments that should be assumed in order to discount future

cash flows? A portfolio with an average weighted life of 2 years

has much different fair value characteristics than a portfolio of

loans with an average weighted life of 10 years.

• What is the average interest rate in the portfolio, and how does

that rate compare to current market rates of debt instruments

with similar risk and duration?

The above points clearly differentiate the factors that would be

considered for fair value treatment as compared to the ALL model

currently required by US GAAP.

Directional Consistency: An Important ConceptAccountants often use the term “directional consistency” when

describing one of the objectives of the ALL. The term was made

well known in a proposed Statement of Position (SOP) issued by the

AICPA in 2003. Although this SOP was never finalized, the concept

of directional consistency clearly articulates an important ALL con-

cept. The following paragraph from the SOP explains the concept.

The measurement of a component of collective loan impairment

should be based on the relevant observable data relating to existing

conditions and should not project changes in the observable data that

may occur in the future. The measurement will rarely be a math-

ematical function of the observable data; rather, significant judgment

will usually be needed to develop an estimate. However, a credi-

tor should consider the directional consistency of the measurement

with changes in the related observable data from period to period.

For example, if the change in the observable data indicates a dete-

rioration in the credit quality of a pool of loans, an increase in the

14

component of collective loan impairment related to that pool of loans

(as a percentage of the pool of loans under assessment) would be direc-

tionally consistent with the change in the observable data. Conversely,

if the change in the observable data indicates an improvement in the

credit quality of a pool of loans, a decrease in the component of collec-

tive loan impairment related to that pool of loans (as a percentage of

the pool of loans under assessment) would be directionally consistent

with the change in the observable data. In applying this principle,

creditors should take into account the interaction of components of

collective loan impairment over time. For example, in applying this

principle to a component established in a previous period to adjust

the creditor’s historical charge-off experience component for conditions

not reflected in the historical experience, the creditor should take into

account the extent to which those conditions are currently reflected in

the creditor’s historical charge-off experience component. Further, the

extent to which such directional changes should affect the amount of

the allowance for credit losses is a matter of significant judgment and

expertise.4

In other words, during periods of strong economic trends and strong

loan quality, there is an expectation of relatively smaller ALL bal-

ances and lower provision for loan loss expense. During periods of

worsening economic conditions, there is the opposite expectation.

This concept is in strong opposition to a practice followed by many

financial institutions in past years of building reserves during the

good times to avoid the impact of negative earnings during the chal-

lenging times.

A Walk Through the Accounting StandardsMany important aspects of the relevant accounting standards have

been discussed above and are elaborated upon further in the remain-

der of this report. However, it is often necessary to refer back to the

specific accounting standards for purposes of responding to auditor/

examiner concerns and addressing practical issues by those charged

with governance in credit unions. And because of the newly imple-

mented ASC, it is sometimes difficult, especially for those who are

familiar with the original FASB standards, to identify the most cur-

rent accounting reference materials.

There are two primary topics under the ASC that address the ALL.

Key concepts extracted from Topics 450 and 310 of the ASC are

summarized below. In the opinion of the author, it is critical for

15

credit unions to understand these in order to properly comply with

GAAP.

• Topic 450, Subtopic 20, “Loss Contingencies,” addresses account-

ing for loss contingencies. Much of this topic is derived from

Statement of Financial Accounting Standards (SFAS) State-

ment 5, “Accounting for Contingencies,” which was issued

in 1975 and to this day represents one of the foundations of

accounting theory. Topic 450 specifically references Topic 310,

noting that the ALL is a subset of loss contingencies.

• Topic 310, “Receivables,” addresses various issues related to

accounting issues subsequent to the origination or acquisition of

receivables, such as impairment. Former accounting standards

SFAS 5, SFAS 15, and SFAS 114 provide much of the content for

this section, which addresses the following:

■ The general concept that impairment of receivables is rec-

ognized when, based on all available information, it is prob-

able that a loss has been incurred based on past events and

conditions existing at the date of the financial statements.

This general concept applies to large groups of smaller-

balance homogenous loans and to loans that are individu-

ally considered to be impaired, including TDRs.

■ A loss arises when the creditor will not be able to collect

principal and interest according to the contractual terms of

the loan.

■ Losses must be probable before loss accrual.

■ Probable means the future event is likely to occur (that is,

it is likely that principal and interest will not be collected

according to the contractual terms of the loan).

■ Appropriate analytics must support the ALL.

■ An insignificant delay in collection of principal and interest

does not require ALL recognition.

■ If a loan is individually impaired, the amount of the loss

provided in the ALL should be based on the present value

of the expected future cash flows discounted at the loan’s

contractual interest rate that existed prior to any restruc-

tured terms.

■ As a practical expedient, impairment for a collateral-

dependent loan can be measured based on the fair value of

the collateral (less costs to sell).

16

■ Collateral-dependent is defined as a loan for which the

repayment is expected to be provided solely by the underly-

ing collateral. Based on this definition, it is unlikely that

most TDR loans would be defined as collateral-dependent.

■ If a loan is specifically identified as impaired and is mea-

sured for impairment, care should be taken to not double-

count the loan in the general valuation component.

■ It is possible for an impaired loan to have no ALL require-

ment. For example, if the underlying collateral value of an

impaired real estate loan exceeded the loan balance, no ALL

would be needed.

Because every portfolio is different, some of a credit union’s ALL decision making must be subjective. But most credit unions are similar enough that the template in this chapter forms a stable foundation on which to build an ALL approach.

CHAPTER 3A Sound ALL Approach

for Credit Unions

18

There are many methods a credit union can utilize to determine its

ALL balance in accordance with GAAP. The approach used should

be based on the facts and circumstances encountered at that particu-

lar credit union, it should be documented in policy, and it should be

consistently applied and tested for reasonableness based on com-

monsense expectations. The internal controls surrounding the ALL

should be tested for appropriateness of design and operating effec-

tiveness. Appropriate qualitative and environmental (Q&E) factors

should be considered, and accounting for TDRs should be addressed

for propriety.

The “Sample ALL Calculation” section below contains an example

of an ALL calculation with explanations of each reserve component.

The major categories include:

• Specific identification and ALL reserves for all loans that have

already been identified as being specifically impaired, which

include, but are not limited to, TDRs, loans over a set period of

delinquency, bankruptcies, and foreclosures in process.

• A GVR component for all loans that have not been specifically

identified as already impaired.

• Appropriate consideration of Q&E factors.

• Proper accounting for TDR loans.

• Proper consideration of impairment for all loans that do not

meet the homogenous definition, which in credit unions consist

primarily of member business loans.

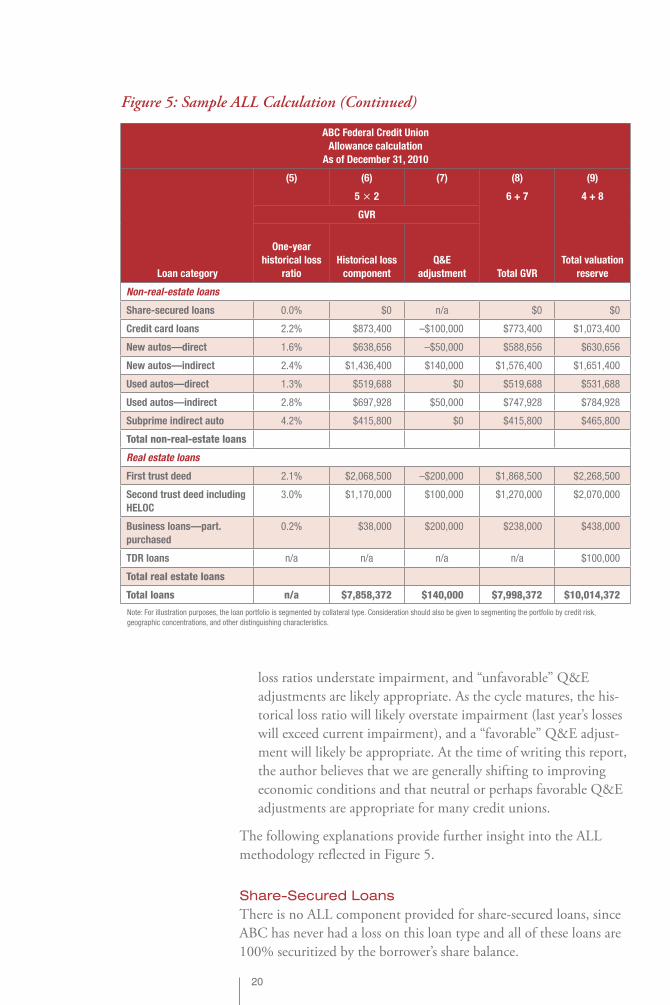

Sample ALL CalculationFigure 5 summarizes a sample ALL calculation for a credit union

with a diversified loan portfolio totaling $400M. The methodology

presented is consistent with the vast majority of credit unions the

author has seen over the years.

19

The ALL calculation reflects the following components with further

explanations provided below:

• Loans that have been identified as requiring an SVR total

$5,232,000 with a related ALL of $2,016,000. The SVR com-

ponent includes TDR loans (see the previous section) as well as

other loans that no longer fit the homogenous definition due to

delinquency status or other loss events having been identified.

• The remaining portion of the loan portfolio totals $394,768,000

and has a GVR totaling $7,998,372. It is important to note the

GVR is a result of utilization of both historical loss ratios and

appropriate Q&E factors.

• Careful consideration must be given to determining the need for

and approach taken to determine the Q&E component of the

ALL. At the beginning stages of an economic downturn, historical

Figure 5: Sample ALL Calculation

ABC Federal Credit Union

Allowance calculation

As of December 31, 2010

Loan category

(1) (2) (3) (4)

Balance of

specifically

identified

impaired loans

Remaining

(unimpaired)

loan balance

Total loan

balance SVR

Non-real-estate loans

Share-secured loans $0 $10,000,000 $10,000,000 $0

Credit card loans $300,000 $39,700,000 $40,000,000 $300,000

New autos—direct $84,000 $39,916,000 $40,000,000 $42,000

New autos—indirect $150,000 $59,850,000 $60,000,000 $75,000

Used autos—direct $24,000 $39,976,000 $40,000,000 $12,000

Used autos—indirect $74,000 $24,926,000 $25,000,000 $37,000

Subprime indirect auto $100,000 $9,900,000 $10,000,000 $50,000

Total non-real-estate loans

Real estate loans

First trust deed $1,500,000 $98,500,000 $100,000,000 $400,000

Second trust deed including

HELOC

$1,000,000 $39,000,000 $40,000,000 $800,000

Business loans—

participation purchased

$1,000,000 $19,000,000 $20,000,000 $200,000

TDR loans $1,000,000 $14,000,000 $15,000,000 $100,000

Total real estate loans

Total loans $5,232,000 $394,768,000 $400,000,000 $2,016,000

(continued on next page)

20

loss ratios understate impairment, and “unfavorable” Q&E

adjustments are likely appropriate. As the cycle matures, the his-

torical loss ratio will likely overstate impairment (last year’s losses

will exceed current impairment), and a “favorable” Q&E adjust-

ment will likely be appropriate. At the time of writing this report,

the author believes that we are generally shifting to improving

economic conditions and that neutral or perhaps favorable Q&E

adjustments are appropriate for many credit unions.

The following explanations provide further insight into the ALL

methodology reflected in Figure 5.

Share-Secured LoansThere is no ALL component provided for share- secured loans, since

ABC has never had a loss on this loan type and all of these loans are

100% securitized by the borrower’s share balance.

Figure 5: Sample ALL Calculation (Continued)

ABC Federal Credit Union

Allowance calculation

As of December 31, 2010

Loan category

(5) (6) (7) (8) (9)

5 × 2 6 + 7 4 + 8

GVR

One-year

historical loss

ratio

Historical loss

component

Q&E

adjustment Total GVR

Total valuation

reserve

Non-real-estate loans

Share-secured loans 0.0% $0 n/a $0 $0

Credit card loans 2.2% $873,400 –$100,000 $773,400 $1,073,400

New autos—direct 1.6% $638,656 –$50,000 $588,656 $630,656

New autos—indirect 2.4% $1,436,400 $140,000 $1,576,400 $1,651,400

Used autos—direct 1.3% $519,688 $0 $519,688 $531,688

Used autos—indirect 2.8% $697,928 $50,000 $747,928 $784,928

Subprime indirect auto 4.2% $415,800 $0 $415,800 $465,800

Total non-real-estate loans

Real estate loans

First trust deed 2.1% $2,068,500 –$200,000 $1,868,500 $2,268,500

Second trust deed including

HELOC

3.0% $1,170,000 $100,000 $1,270,000 $2,070,000

Business loans—part.

purchased

0.2% $38,000 $200,000 $238,000 $438,000

TDR loans n/a n/a n/a n/a $100,000

Total real estate loans

Total loans n/a $7,858,372 $140,000 $7,998,372 $10,014,372

Note: For illustration purposes, the loan portfolio is segmented by collateral type. Consideration should also be given to segmenting the portfolio by credit risk,

geographic concentrations, and other distinguishing characteristics.

21

Credit Card LoansAs of December 31, 2010, ABC had specifically identified loans

totaling $300,000 that were pending charge-off in January 2011.

Therefore, an SVR has been established for the losses on these loans,

which represent 100% of the loan balances.

Additionally, the one-year loss ratio results in a GVR of approxi-

mately $873,000. However, in recognition of an improving economy

over the past 18 months, including more aggressive collections and

stronger underwriting, a favorable Q&E adjustment of $100,000

is established. It should be noted that based on the best data and

most up-to-date analysis, ABC expects unsecured loan charge-offs to

approximate $50,000 per month, which provides further support for

the favorable Q&E adjustment.

Auto Loans (All Categories)Each of these categories reflects the amounts of pending charge-offs

that will occur in January 2011 for the SVR. Q&E factors reflect

differing results for each component based on current conditions.

Consideration is given to declining early- stage delinquency trends,

improving economic conditions, and other relevant factors. In all

cases, the resulting GVR exceeds the expected charge-offs for the

next 12 months by a margin of approximately 20%.

First and Second Trust Deed Loans (Including HELOC)As of December 31, 2010, loans totaling $1.5M have come to

management’s attention that represent probable loss. Loans in this

category are primarily comprised of loans over 60 days delinquent

for which collection efforts are approaching exhaustion and foreclo-

sure proceedings will begin shortly. There is also a loan in this group

where the borrower has approached the credit union for a short sale

due to significant collateral value slippage. Estimated losses for these

specifically identifiable loans total $400,000.

In addition to the amounts resulting from the historical loss ratio,

management has obtained updated combined loan-to-value (CLTV)

data for all real estate loans through the use of third- party automated

valuation models and combined the CLTV data with updated credit

score metrics. Management has made estimates for impairment for

all real estate loans based on bandwidth of CLTV and credit scores,

with emphasis on loans with CLTV ratios above 125%.

Business LoansBusiness loans typically do not meet the definition of a homogenous

loan pool and must be evaluated on an individual basis for impair-

ment characteristics. This process often involves an annual (or more

frequent, as appropriate) review of each loan, using a grading system

22

that quantifies impairment and results in specific loss estimates

after consideration of current collateral value. When these member

business loans consist of participations purchased from other credit

unions, great care should be taken by the investor credit union to

ensure that the servicing credit union is taking appropriate steps to

monitor deteriorating credit characteristics and to maximize collec-

tion efforts. Many credit unions have relied on the servicing credit

union to identify and quantify impairment on participation loans

without the commensurate level of due diligence taken by the inves-

tor credit union.

Sample Calculation of SVR on a TDR LoanIn order to illustrate how to calculate the SVR on a TDR loan, assume

the loan in Figure 6 was modified and is considered to be a TDR.

Net investment in the loan at the date of restructure (including

loan balance, accrued interest, deferred origination costs, etc.) as

compared to the present value of the future expected cash flows

discounted at the loan’s original contractual rate. Therefore, we need

to determine the future expected cash flows on this loan and then

discount those cash flows to their present value at the original 6%

interest rate.

There are many tools available for determining the present value.

As noted in Figure 6, the present value is $172,560 as compared to

the loan balance of $186,376. Therefore, an initial SVR of $13,816

(assuming no re-default) is required at the onset of this modification.

Figure 6: Sample TDR Loan

Original loan balance $200,000

Original term 30 years (360 months)

Original rate 6%

Net investment in loan at date of

restructure

$186,376

Remaining term 300 months

Revisions to original contractual terms Rate changed from 6% to 3% for 3 years (36

months), reverts to 6% fully-amortizing loan

for remaining 264-month (22-year) term

Re-default assumption For illustration purposes, assume no re-default

risk

Original loan payment (P&I) $1,199

Revised loan payment for next 36 months $884

Revised loan payment for months 37 to 300 $1,166

Present value of next 300 payments

discounted at 6% interest rate

$172,560

23

What about re-default? One way of understanding why this is an

important question is to consider the impact on expected cash flows

if a re-default occurs that results in the need to foreclose on the

property securing this loan. If a foreclosure occurred, only one pay-

ment would be received subsequent to the re-default, which would

approximate the collateral value net of selling expenses.

There is no precise way of predicting re-default. However, empirical

evidence clearly indicates that the greater the gap between property

value and loan balances (first and second loan balances combined),

the greater the risk of re-default. In the example given in Figure 6,

if the property were located in the sand states and its value had

declined 50%, there would be a greater risk of re-default than if the

property value were closer to the current loan balance.

One final issue needs to be addressed that often raises questions.

What if the revised rate offered to the borrower (3% in the example)

approximates a market rate for a new loan? If the borrower could

refinance their loan at the same rate as other borrowers in an arms-

length transaction, this modification probably would not be consid-

ered a TDR. However, the borrower would have to be able to execute

such a transaction given their current credit status (credit score,

employment status, debt coverage, etc.) and also given the property’s

current market value. These considerations result in the vast majority

of loan modifications being considered TDRs.

There are several critical takeaways from the example in Figure 6:

• The credit union’s loan- tracking system needs to flag this credit

as a TDR and apply special impairment testing and regulatory

reporting on a go- forward basis.

• The present value of the future cash flows will change through-

out the remaining term of the loan subsequent to the modifica-

tion. Therefore, all TDR loans will need to have the present

value recalculated over their remaining term; at a minimum, this

should be performed quarterly for call reporting purposes.

• Re-default risk is directly related to the loan-to- value ratio (LTV).

Therefore, the credit union needs to obtain updated LTV infor-

mation and carefully document the assumptions used for estimat-

ing re-default risk.

• The absence of delinquency status does not alleviate the need for

the present value calculations and for classification as a TDR loan

over the remaining loan life.

Sometimes historical loss ratios are not enough. This chapter illuminates timely Q&E fac-tors that may apply to your credit union. It also examines the increasingly common TDR arrangements and how to properly account for them.

CHAPTER 4Q&E and TDR Factors

25

What Are Q&E Factors?As noted earlier, historical loss ratios alone are not adequate to

measure impairment on pools of loans, especially during periods of

economic volatility. Said differently, the fact that losses last year were

x% does not necessarily mean this year’s losses will also be x%. The

historical loss ratio is a starting point used to measure impairment;

it needs to be adjusted up or down depending on other appropriate

factors, such as the following, to properly measure impairment in

the GVR:

• A significant downturn in the general economy exhibited by

increasing inflation, rising unemployment, or a declining housing

market.

• A significant deterioration in the quality of the underwriting pro-

cess, exhibited by increasing delinquency and charge-off trends.

• The occurrence of a natural disaster, such as an earthquake or

flood.

• Economic turmoil in the field of membership, such as a major

strike, layoffs, or a merger.

• Experience, ability, and depth of lending management.

• Changes in lending policies and procedures, including changes in

underwriting standards and collection, charge-off, and recovery

practices not considered elsewhere in estimating credit losses.

• Changes in international, national, regional, and local economic

and business conditions and developments that affect the col-

lectibility of the portfolio, including the condition of various

segments.

• Changes in the nature and volume of the portfolio and in the

terms of the loans.

• Changes in the volume and severity of past-due loans, the volume

of non- accrual loans, and the volume and severity of adversely

classified or graded loans.

26

• Most recent charge-off trends (e.g., three-month and six-month

annual charge-off trends are higher/lower than amounts reflected

in one-year historical loss ratio).

• Changes in the quality of the credit union’s loan review system.

• The existence and the effect of any concentrations of credit, or

changes in the level of such concentrations.

• The effect of other external factors, such as competition and legal

and regulatory requirements, on the level of estimated credit

losses in the credit union’s existing portfolio.

Q&E Factors for Residential Real Estate Loans Can’t Be IgnoredFor credit unions facing significant deterioration of collateral value

on real estate loans, unique issues arise that impact the ALL. A real

estate loan with significant collateral devaluation may be impaired

even if it is not yet delinquent. Conversely, real estate loans with sig-

nificant collateral devaluation may not be impaired. The ALL process

must appropriately assess the impact of declining real estate value,

and this process needs to be carefully documented and updated

regularly.

LessonIn order to develop appropriate ALL analytics for real estate loans

in geographic areas facing declining values, credit unions need to

obtain updated fair value analytics on the collateral, often done by

utilization of automated valuation models (AVMs) provided by third

parties. The updated AVM data, combined with updated credit score

data on the borrowers, will identify the real estate loans with the

highest LTV ratios are those with the highest risk and therefore the

greatest likelihood of impairment.

Finally, consider that just as historical loss ratios alone may have

resulted in ALL understatement at the beginning of the declining

economic cycle, historical loss ratios alone will likely result in ALL

overstatement as the economy recovers.

Q&E Ideas for Your ConsiderationAs the term implies, there is a lot of subjectivity that enters into the

methodology and quantification of Q&E factors. Following are six

methods that the author has seen successfully employed by credit

unions.

• For residential real estate loans, create a matrix of each major

portfolio by CLTV and credit score. Those loans with high CLTV

27

and low credit score are at greatest risk of impairment and might

not be properly quantified by loss ratios alone. Estimate the

amount of such impairment by regression analysis, sampling of

loan files, use of industry standards, or other appropriate analyti-

cal methods.

• Consideration should be given to segmenting the portfolio by

year of origination, especially when timing of origination is reflec-

tive of loss exposure.

• Evaluate trends in early-stage delinquency, which are obviously an

indicator of future impairment trends. As early-stage delinquency

trends begin to decline, favorable adjustment of historical loss

ratios should be considered (and vice versa).

• Compare the calculated ALL balance to the amount of expected

charge-offs for the next 12 months. As the ALL balance begins to

represent an amount exceeding 150% of expected charge-offs, a

favorable Q&E adjustment should be evaluated.

• Determine the historical correlation between local area unem-

ployment and increased levels of charge-offs. As unemploy-

ment rises or falls, impound an appropriate factor into the ALL

analysis.

• Compute an annualized loss ratio based on the past three months

and the past six months. If there is a significant difference

between these look-back periods compared to the one-year loss

ratio, determine which look-back period is most reflective of cur-

rent conditions.

• Calculate a loss ratio based on net charge-offs as compared to

delinquent loan balances by loan category. If delinquency is fall-

ing rapidly, this loss ratio might provide a good perspective for a

reduction in the ALL as compared to the conventional approach.

Remember, as the economy stabilizes, unemployment rates fall,

and real estate values firm up, the historical loss ratios of the past

few years could result in an overstated ALL balance. Therefore, the

appropriate Q&E factors should be identified and quantified to

supplement these loss ratios.

What Is a TDR and How Is a TDR Accounted For?A TDR occurs when a creditor, for economic or legal reasons related

to the debtor’s financial difficulties, grants a concession to the

debtor that it would not otherwise consider. That concession either

stems from an agreement between the creditor and the debtor or is

imposed by law or a court. If a loan is restructured in a manner that

would make it difficult or impossible to receive equally favorable

28

terms from another financial institution, there is a good chance the

loan meets the definition of a TDR, and further analysis would be

required. It should be noted that a rate concession to an equivalent

market rate may likely be considered a TDR if the borrower would

not otherwise qualify for the market rate due to impaired collateral

value or inadequate credit standing.

Each real estate TDR must be separately evaluated to determine

the amount of impairment that is derived based on discounting

expected future cash flows at the loan’s original interest rate. There-

fore, assumptions must be made as to the amount of the future cash

flows, which will take into consideration not only the borrower’s

willingness and ability to make the payments during a short-term

rate reduction period, but also their willingness and ability to return

to full payments at the end of the rate reduction period. This is com-

monly referred to as re-default risk. Depending on the amount and

number of restructured consumer loans, similar treatment m ay need

to be considered for such loans. An example of how to calculate the

SVR on a TDR loan is provided in Chapter 3.

My clients often ask why they have to take an accounting loss on

a TDR loan simply because the interest rate has been reduced to

enable the borrower to make payments and avoid default. Said dif-

ferently, why not just recognize prospective interest income at the

reduced rate reflected in the loan modification? One way to answer

this question is to consider what the impact would be if the entire

loan portfolio interest rate were reduced, say from a 6% contrac-

tual rate to a 3% temporary rate for the next three years. The result

would be to impound a significant reduction of earnings into the

future, without any recognition of this economic event in the current

period’s income statement or allowance valuation reserve. When

this impact is considered at the entire portfolio level, it is clear that

some kind of loss recognition is appropriate. The discounted present

value approach enacted by FASB is, in the opinion of the author, a

reasonable way to measure the financial loss resulting from the loan

modification.

LessonRe-default risk is difficult to assess. However, there is an expecta-

tion that the risk of re-default increases as the LTV ratio rises. Since

re-default risk impacts future cash flows in a significant manner,

credit unions must employ appropriate analytical techniques to

measure LTV metrics within the TDR portfolio and make reasonable

assumptions about the re-default risk of such loans.

With the benefit of 20/20 hindsight, it is clear to this author that mistakes have been made by many charged with governance over the ALL. This chapter outlines some of the most common mistakes seen during the Great Recession and offers lessons on how they can be prevented from happening again.

CHAPTER 5Common ALL Mistakes: A Great

Recession Post-Mortem

30

The incredible economic cycle of 2007–2010 provides the perfect

laboratory for assessing how credit unions have accounted for the

ALL. During the period of 2007–2009, annual charge-offs for credit

unions significantly exceeded the prior year-end balance of the ALL,

an indicator of ALL understatement. This was especially evident in

the sand states of Arizona, California, Florida, and Nevada.

Based on a combination of publicly available financial data, as well as

empirical data observed in my consulting practice, the following les-

sons help to explain this condition and are critical for those charged

with governance in credit unions to understand.

Overreliance on Historical Loss Ratios, Failure to Consider Q&E FactorsMany credit unions relied too heavily on historical loss ratios for

the GVR component of the ALL. Since loss ratios by definition

are retrospective, the quickly changing environmental conditions

that gave rise to impairment (rising unemployment combined with

rapidly declining real estate values) were not reflected in the loan loss

analytics.

LessonHistorical loss ratios alone are a poor indicator of impairment during

periods of economic volatility and can lead to ALL understatement

during deteriorating cycles, as well as overstatement during improved

cycles. Credit unions must consider appropriate Q&E factors (see fur-

ther discussion below) to supplement the historical loss ratios. Credit

unions with large residential real estate portfolios, especially in the

sand states, must understand the relationship between current loan

balance and underlying collateral value in order to properly assess

portfolio impairment. Also, it is critical to select a look-back period

(one year, three years, etc.) that is reflective of current economic

conditions. Generally, a one-year look-back period supplemented

by appropriate Q&E factors is common (and appropriate) for credit

unions.

31

Failure to Properly Account for TDRsWhen a borrower is unable to make their contractual loan payments,

lenders often reduce the interest rate or forgive some portion of the

loan in order to lower the amount of the monthly payment. When

this occurs, the loan is classified as a TDR and requires specialized

accounting. This is one of the more complex areas of credit union

accounting, and it requires an understanding of estimating and

discounting future cash flows on an ongoing basis (see further discus-

sion below).

LessonMany credit unions didn’t have adequate controls in place to prop-

erly identify TDR loans, and they also didn’t understand the proper

accounting for such loans. This breakdown of internal controls in

many cases led to an overstatement of earnings and net worth. Also,

many credit unions lack automated systems to properly identify and

prospectively account for TDR loans.

Failure to Properly Account for Business Loans on an Individual Loan BasisMany credit unions originate and hold member business loans,

which typically have large balances and do not meet the homogenous

portfolio definition. Such loans need to be evaluated for impairment

on a loan-by-loan basis, with consideration given to impairment

characteristics such as current collateral value, current borrower

financial condition, and underlying business cash flow assessments.

Often, member business loans have deteriorating characteristics that

would require an ALL reserve component well in advance of such

loans becoming reportably delinquent.

LessonMany credit unions have not implemented adequate monitoring and

assessment methods to properly evaluate impairment on member

business loans. Further, these loans are often serviced by third par-

ties, and credit unions often fail to determine the reliability of the

servicers and the timely receipt of impairment data.

Outdated ALL PoliciesAlthough GAAP for recognition of loan losses have not really

changed, many credit unions didn’t understand how a severe eco-

nomic downturn could impact the ALL, and their allowance policies

and procedures were reflective of ongoing strong economic cycles.

32

Members of the board and supervisory committee often lacked the

technical insights required to monitor the reasonableness of the ALL,

and therefore auditors and examiners were often the first to question

the resulting understated balances.

LessonOngoing efforts should be made to update all critical accounting

policies. The board of directors should ensure not only that these

policies are updated regularly, but also that there is an ongoing edu-

cational process in place to ensure compliance with accounting and

regulatory reporting standards.

No report can address every facet of ALL regu-lation and management. This final chapter offers guidance on some of the most com-mon challenges in today’s confounding ALL environment.

CHAPTER 6Final ALL Considerations

34

A Word About Timing of Charge-OffsCare should be taken to ensure that loans are charged off when

routine collections efforts have been exhausted and the loan is

deemed to be uncollectible, and when the credit union has properly

acquired title to the collateral, if any, securing the loan balance. It

would be improper to delay a charge-off until the last possible dollar

of expected payments had been received. A loan should be charged

off if the asset (or portion thereof ) is considered uncollectible and of

such little value that its continuance on the books is not warranted.

Failure to charge off loans in a timely manner often results in signifi-

cant understatement of the ALL balance, since historical loss ratios

will be understated, and often the loans in question are not properly

identified in the SVR calculation.

One of the outcomes of the Great Recession is the significant delay

experienced by many credit unions throughout the country in being

able to execute a foreclosure on residential properties. The delays are

often the result of backed-up judicial processes, as well as the large

volume of real estate loans pending foreclosure, especially in the sand

states. During this period of delay, delinquent real estate loans con-

tinue to escalate, even though the loss exposure on these loans should

be fully reserved in the SVR component of the ALL.

A question often arises as to when the loan can be charged off,

thereby reducing the delinquency ratio. If the credit union is in phys-

ical possession of the property, the credit union should charge off the

estimated loss portion of the loan and transfer the remaining balance

(fair value less costs to sell) to “other real estate owned” (OREO). It

should be noted that if a residential property has been abandoned by

the borrower, the credit union is likely considered to have physical

possession. However, if the property has not been abandoned, the

balance of the loan should not be transferred to OREO.

35

What Do NCUA Regulations Say About the ALL?NCUA Rules and Regulations Part 702.402(b) states in part, “The

financial statements of a federally- insured credit union shall pro-

vide for full and fair disclosure of all assets, liabilities, and members’

equity, including such valuation (allowance) accounts as may be

necessary to present fairly the financial condition.” Part 702.402(d)(2)

further clarifies this requirement by stating, “The allowance for loan

and lease losses established for loans must fairly present the probable

losses for all categories of loans and the proper valuation of loans.

The valuation allowance must encompass specifically identified

loans, as well as estimated losses inherent in the loan portfolio, such

as loans and pools of loans for which losses have been incurred but

are not identifiable on a specific loan-by- loan basis.”

The NCUA’s position on the ALL is summarized in Interpretive

Ruling and Policy Statement 02-3, issued in May 2002 (www.ncua.

gov/Resources/RegulationsOpinionsLaws/IRPS/2002/IRPS02-3.

html), and Accounting Bulletin 06-1, issued in 2006 (www.ncua.

gov/GenInfo/GuidesManuals/accounting_bulletins/2006/06-01ALLL.

pdf). This regulatory guidance addresses key issues of importance

to credit union management and officials, and should be reviewed

regularly for compliance.

One last regulatory point of confusion regarding TDR accounting:

For call reporting purposes, a restructured loan must continue to

be reported as delinquent (based on the original contractual terms)

until six months of timely contractual payments under the restruc-

tured terms have been received by the credit union. Thereafter, the

TDR loan is no longer reported as delinquent unless another pay-

ment is missed, in which case the delinquency reporting would be

based on the restructured terms. Many credit unions have confused

the delinquency reporting requirements with the TDR accounting

requirements, which, as noted earlier, are based on the present value

of future cash flows.

LessonThe absence of TDR delinquency status does not alleviate the need

for the discounting of future cash flows over the remaining term of

the restructured loan and for classification of the loan as a TDR.

36

Why Do Internal Controls Impact the Determination of the ALL?An appropriate system of internal controls is critical to properly

evaluating the reasonableness of the ALL. The accuracy of the aging

of delinquent loans, the timely foreclosure and repossession of col-

lateral, and the timeliness of charge-offs are but a few examples of

critical internal controls that management must be able to place reli-

ance upon. Management must be able to demonstrate and represent

to the board of directors that such controls are operating effectively,

or the board may face harsh criticism over potential and material

misstatement of financial statement accuracy.

The following is a partial listing of key internal controls that are

appropriate for most credit unions. The supervisory/audit committee

of every credit union should satisfy themselves that the credit union

has identified the appropriate controls surrounding the ALL and that

such controls are operating effectively.

• Delinquency reports are generated from each major loan system

at month’s end and are considered in the determination of the

ALL balance.

• There is an effective loan review system in place to ensure that

loans originated are in compliance with underwriting policies.

• Controls are in place to identify problem loans in a timely

manner.

• The CFO performs a formal review of ALL analytics on at least

a quarterly basis. This review is documented and signed-off on

by others with oversight responsibility, including the CEO, chief

lending officer, and COO.

• A review of the ALL methodology and its application is per-

formed by a party that is independent from the ALL estimation

process on at least an annual basis.

• There is a process to ensure the timely charge-off of uncollectible

loans.

• The board of directors and supervisory committee meet with

management on at least an annual basis to review ALL methodol-

ogy and key analytical trends.

• For commercial loans, if any, there is an appropriate loan grading

system that is updated at least annually, and loans whose credit

quality has deteriorated are individually reviewed for impairment

on at least a quarterly basis.

• Loans recommended for charge-off are approved by the board of

directors.

37

• Actual charge-offs are reconciled to authorized charge-offs.

• The credit union’s internal audit staff reviews the effectiveness

of the above controls on at least an annual basis and reports the

results of this review to management and the board of directors

and supervisory committee.

ALL Analytical ExpectationsThose charged with governance in credit unions should develop

expectations of reasonable ALL analytics and should regularly com-

pare those expectations with actual ALL metrics. The following chart

provides an example of expectations that should be considered by

all credit unions; this example should be customized and updated as

appropriate.

Figure 7: Analytical Expectations

Analytic tool Expectations/Concerns

1. A comparison of current-year charge-offs

to the prior year-end ALL balance. This is

sometimes referred to as a look-back test.

Generally, current-year charge-offs are less than the prior year-end balance of the ALL. When

current-year charge-offs exceed the prior year-end balance, this indicates a possibility that the