Embed Size (px)

Citation preview

1

2

Th

e 7 P

rincip

lesThe Seven Cooperative Principles date back to some of the earliest co-ops that formed in England in the 1800s. To this day they form the foundation on which cooperatives around the world operate. Seattle Metropolitan Credit Union has adapted these principles to the financial needs and goals of our members, and they guide us in everything we do.

Membership Should Be Open To All Membership at Seattle Metropolitan Credit Union is open to every resident of the State of Washington, without gender, social, racial, political, or religious discrimination.

Members Should Call The Shots Seattle Metropolitan Credit Union is a democratically run organization, controlled by our members. Our Board of Directors is composed of and democratically elected by our membership.

Member Participation Benefits the Entire Credit Union SMCU returns surpluses to members in the form of fewer fees, more services, lower interest on loans and higher dividends on deposits. The more members participate, the more there is to go around.

Autonomy & Independence Set Us Apart As a financial cooperative, Seattle Metropolitan Credit Union is controlled by our members, not outside shareholders.

Financial Education Should Be Free & Available To All We believe that financial education is a critical benefit of membership. SMCU provides financial information via seminars, workshops, newsletters and our website at no cost to our members.

Cooperation Among Cooperatives Is Vital We serve our members best and contribute to the cooperative movement by working with other cooperatives through local, state, regional, national and international organizations.

Giving Back To The Community Is An Obligation We believe it is a priority to give back to the communities where we do business while focusing on our members and their needs. SMCU seeks to achieve a greater good through responsible corporate citizenship.

3

Check-In and Refreshments ......................................................8:30 a.m.

SMCU’s 81st Annual Meeting ..................................................9:00 a.m.WelcomeIntroduction of the Board of DirectorsCall to OrderAscertain QuorumApproval of 80th Annual Meeting Minutes Supervisory Committee ReportVolunteer Election ResultsUnfinished BusinessNew BusinessCEO Remarks Questions from the Membership

Adjournment .................................................................................. 10:30 a.m.

Agenda

Board of Directors, Supervisory Committee,

and Senior Management .......................................................................... 4

From the Board Chair ..................................................................................... 5

From the CEO .................................................................................................... 6

Minutes of the 80th Annual Meeting ...................................................... 8

Executive Committee Report ...................................................................11

Supervisory Committee Report ..............................................................12

Finance & Budget Committee Report .................................................14

2013 Financial Statements ........................................................................16

Contents

4

Board of DirectorsJim Yearby ........................................................................................... Chair

James A. Fossos ........................................................................ Vice Chair

Camilla Bishop ........................................................................... Secretary

Rodney Eng ....................................................................................Director

Ken Harer .......................................................................................Director

Ray Hill .............................................................................................Director

Robert Leighton ...........................................................................Director

Frank Mathews .............................................................................Director

Jack McGoldrick ..........................................................................Director

Senior Management

Supervisory Committee

Richard Romero ..............................................................President/CEO

Larry Grager ............................................SVP, Chief Financial Officer

Jill Vicente .................................................SVP, Chief Strategy Officer

Tonita Webb .................................................SVP, Chief Admin Officer

Jane Brunton ...............................................................VP, Internal Audit

Caleb Cook ............................................................................... VP, Lending

Chad Meadows ................................................................VP, Retail Sales

Brent Richins ........................................................VP, Member Services

Ben Wakefield ......................................................................................Chair

Gary Skinner ................................................................................Secretary

Robert Leighton ........................................................................... Member

Sandra Philbrook ......................................................................... Member

5

From the Board ChairL ast year I reported that your

credit union was facing tough

economic times but was financially

healthy. Today, tough-enough times

continue, and SMCU remains

financially sound. We do have many

tough challenges ahead but your

board and management team are

working hard, doing everything that

is possible to protect the assets of

your credit union.

As you have seen from your

newsletter and other media and

marketing materials, your credit

union has money to make loans.

Whether you are in the market for a

new automobile, seeking to purchase

the new home of your dreams, or you

simply want to remodel your existing

home, money is available to you at

very competitive rates.

Your board, CEO, and his leadership

team are working hard to make sure

that you get the service that you

deserve as a member of a first-class

financial institution. Our goal is to be

your financial institution of choice,

not just because you are a member,

but because we offer you very

competitive financial rates and more

importantly, great, friendly service.

To serve your needs, we are investing

in new talent, technology, and

other infrastructure to make sure

we remain viable and relevant as

you seek financial services. Our

strategic plan focuses on responsible

growth with investment in new and

innovative tools to meet your financial

service needs. Many channels are

now provided to meet your needs

whether your choice is service at a

branch, on your home computer, or

while on the road through your smart

phone.

As we grow and expand our financial

reach, we will always keep our focus

on credit union risk. Maintaining the

safety and soundness of your assets

is one of the board’s most important

responsibilities. I want you to know

(continued)

6

From the CEO2013 was a good year for

Seattle Metropolitan Credit Union. The Credit Union’s Net Worth, the measurement used to indicate financial strength, finished at 9.09%. Our Return on Assets, the measurement used to calculate how well the Credit Union earns income, finished at .85% (10 basis points over the industry average.) Our assets, the measurement used to gauge the size of our Credit Union, grew by 17 million dollars – under a controlled growth plan.

During 2013 SMCU management and your Board of Directors worked closely to ensure that you continue to have access to the best, most up-to-date financial products and

services available. To that end, we laid the groundwork for enhanced service delivery channels, such as SMCU’s first mobile banking app and a significantly improved online Mortgage Center. Both of these projects will be implemented in 2014 and will provide our members with faster, more convenient service, from wherever they choose to do their banking.

While we are proud of the work we have done and look forward to making these enhanced services available to our members, the job of providing quality member service is never finished. To that end, we have created new feedback channels, such as a quarterly member survey,

that your board is on its job. We will

continue to provide governance and

oversight that will assure that your

assets are protected as you would

expect us to do.

Meeting all of your financial needs

is the board’s highest priority. We

want to exceed your expectations by

making sure that you have the best

experience in all your dealings with

Seattle Metropolitan Credit Union.

You deserve no less, and the board

is committed to making sure your

financial needs are met; that is our

highest priority. It is privilege to serve

you. Thank you for the opportunity.

Jim YearbyBoard ChairSeattle Metropolitan Credit Union

(continued)

From the Board Chair (continued)

7

Richard Romero President/CEOSeattle Metropolitan Credit Union

and have new processes in place to ensure that we can respond to service opportunities and suggestions quickly to continue to meet our members’ needs.

We enter 2014 with a cautiously optimistic outlook. While the financial results in 2013 for SMCU were strong, the Credit Union continues to battle against an economic environment of low investment returns and a tough, competitive market for originating new loans. These challenges continue to push SMCU’s management team to find new ways to earn income and to deliver service at levels that our members have come to expect.

Because we are a credit union, our greatest asset is our membership and the cooperative structure that sets us apart from other financial institutions. You, our member-owners, share in SMCU’s success. As such, it is in your best interest to be aware of issues that can impact the operation of the Credit Union.

We ask that you remain connected to your Credit Union by subscribing to

our email list, following us on social media, and visiting our website. Stay aware of legislative actions that could benefit or harm our organization. From time to time, SMCU will reach out to you in order to keep you informed of when your voice can count. We may ask you to contact a legislator or representative in order to get our voice heard.

We consider ourselves truly fortunate that you have chosen us to be your trusted financial advisor. Our aim every day is to remain worthy of that trust. If you have suggestions about ways we can improve our

service, please let us know.

Thank you for being a member.

From the CEO (continued)

8

Minutes from the 80th Annual MeetingB oard Chair, Mr. Jim Yearby,

welcomed all attendees and

thanked all attendees for their time.

Chief Executive Officer and

President, Richard Romero, reported

that the Credit Union’s current

finances are strong and getting

stronger by the month. Mr. Romero

further stated that he remains

committed to the Credit Union’s 7

Principles and that the upcoming

year will focus on improving the

organization’s infrastructure.

Mr. Yearby introduced the members

of the Board, the members of

the Supervisory Committee,

and the members of the Senior

Management Team.

Board Secretary, Camilla Bishop,

ascertained the quorum and called

the meeting to order at 6:12 PM.

Board members present were Jim

Yearby, Board Chair; Rodney Eng,

Board Vice Chair; Camilla Bishop,

Board Secretary; Jim Fossos; Ken

Harer; Ray Hill; Robert Leighton; and

Frank Mathews.

A member from the floor moved

to accept the minutes of the

2012 79th Annual Meeting as

presented. The motion was

seconded and approved by vote

without opposition or abstention.

Chair of the Supervisory Committee,

Ben Wakefied, introduced the

members of the Supervisory

Committee. Mr. Wakefield

then reviewed the duties of the

Supervisory Committee and thanked

Jane Brunton, Internal Audit, for her

assistance throughout the past year.

Nomination & Election Committee

Chair, Ken Harer, reported the

results of the 2013 Volunteer

Election. Mr. Harer stated that 2,336

valid votes were cast in this election,

approximately 6.7% of the Credit

Union’s membership. Mr. Harer

additionally stated that the majority

of votes were cast by mail. Mr. Harer

reported that Ms. Bishop, Mr. Fossos,

and Mr. Hill were re-elected to the

Board of Directors. Mr. Harer further

reported that Mr. Gary Skinner and

Mr. Robert Leighton were re-elected

to the Supervisory Committee.

Mr. Fossos moved to approve the

Supervisory Committee report as

presented by Mr. Wakefield, the

Nomination & Election Committee

report as presented by Mr.

(continued)

9

Harer, and the Finance & Budget

Committee report as printed in the

meeting material. The motion was

seconded and approved by vote

without opposition or abstention.

Mr. Yearby asked the attendees if

there was any unfinished business to

be addressed at the meeting.

In response, a member stated that

she did not think that the question

she posed at the previous year’s

annual meeting had been addressed.

The online catalog of items that

members may purchase using their

Rewards Points does not list the

price in Rewards Points for each

item. Debbie Robinson, Operations

Manager, replied stating that point

values are assigned by third-party

vendors provided by the Visa. As such,

the point values and the publishing of

these values are unfortunately not

controlled by the staff of the Credit

Union. Ms. Robinson further stated

that she brought the member’s

request to the attention of VISA.

Mr. Yearby asked the attendees if

there was any new business to be

addressed at the meeting.

In response, a member asked why

the meeting is held at the downtown

location as the afternoon commuter

traffic makes it inconvenient for her

to reach the downtown location

at this time on weekday evenings.

Mr. Yearby replied stating that the

meetings were previously held on

Saturdays and the Board would

consider changing the day or the

location of the Credit Union’s Annual

meeting in the future.

A member asked if Mr. Yearby or

Mr. Romero would expand upon

some of the budget priorities for

2013 and explain the new business

model referenced in Mr. Yearby’s

letter to the members. In response,

Mr. Romero stated that the business

model is aimed at improving the

Credit Union’s infrastructure,

such as information technology

and management structure. Mr.

Romero further stated that the

2013 business model will focus on

identifying a clear target market as

well as on market penetration.

A member asked why he is being

charged fees on his accounts when the

total balance of his accounts exceeds

the required minimum balance. In

response, Mr. Harer stated that it is

costly to the Credit Union to support

multiple accounts with low balances.

To address this after the 2008/2009

financial crisis, the Credit Union

implemented fees on low-balance

accounts to encourage members

to consolidate their accounts. The

measures were taken to keep the

2013 Minutes (continued)

(continued)

10

2013 Minutes (continued)

Credit Union financially solvent. The

member clarified that his question

regards his money market accounts.

Branch Manager, Wendi Fracasso,

replied by stating that it is common

to charge a fee for dropping below a

minimum balance for money market

accounts to support the advantages

offered with money market accounts.

The same members also stated that

he currently has limited access to

the Credit Union’s services where

he lives in Kenmore, Washington. In

response, Mr. Romero replied that the

2013 business plan includes a review

of branch profitability and analysis of

where our membership resides. Mr.

Romero further stated that executing

a branching strategy is a difficult and

expensive operation best supported

by thorough research.

The same member also asked

what outreach is being conducted

to generate new membership.

Ms. Vicente replied that the two

most significant efforts currently

underway are the reward offered to

members for referring new members

and the constant work continued

by the Business Development

department.

Mr. Yearby asked the attendees if

there were any further questions

or concerns. No further questions

or concerns were raised. Mr. Yearby

thanked the attendees for coming

and for raising their questions.

Mr. Fossos moved to adjourn the

meeting. The motion was seconded

and approved by vote without

objection or abstention.

11

(continued)

Executive CommitteeT hese are both exciting and

challenging times for your board

and Seattle Metropolitan Credit

Union. First, thank you for your loyal

service over the years. You have done

an outstanding job supporting your

credit union and you deserve much

of the credit for our success.

As Board Chair, one of my duties is to

chair the executive committee. The

executive committee is composed of

the board officers. Let me introduce

them to you at this time. Ken Harer is

our past chair of the board, Jim Fossos

is our vice chair, Camilla Bishop is our

secretary, Richard Romero is our

treasurer and I, Jim Yearby, serve as

the current chair of the board.

I am privileged to work with such

a competent and dedicated group

and, as you may guess, they keep

me out of trouble. The committee’s

primary charge is to help carry out

the business of the credit union and

to act on behalf of the full board

between board meetings, when it is

necessary. Typical duties include:

• Helping set the annual strategic

plan and direction of the credit

union

• Leading the evaluation of the

CEO’s annual performance

• Setting the monthly board

meeting agenda

• Reviewing and approving credit

union lease agreements

• Assessing the economic

market conditions and devising

strategies to keep the credit

union’s assets safe and its

service competitive

• Reviewing and recommending

proposals for expanding credit

union service

• Recommending the sale,

acquisition or restructure of

credit union assets, and

• Performing related duties as

required.

The above duties are not exhaustive

but are intended to give you an idea

of the charge of the committee. The

committee has done an outstanding

job executing its responsibilities the

past year as in previous years. The

committee is especially skilled at

providing oversight and helping with

strategic credit union direction and

decisions.

While the committee is proud of its

accomplishments, we realize there

are many challenges and much work

that remains to be done as we move

forward. We are aware of both our

12

T he Washington State Credit

Union Act defines the corporate

governance requirements for credit

unions, including the requirements

and duties of the Supervisory

Committee. The Bylaws of SMCU

further define the membership,

terms, duties and responsibilities of

the Supervisory Committee.

As of 12/31/13, the SMCU

Supervisory Committee was

composed of three elected

volunteers: Ben Wakefield, Chair;

Gary Skinner, Secretary; and Bob

Leighton; as well as one appointed

member, Sandra Philbrook. Jane

Brunton, VP of Internal Audit,

worked on behalf of the Committee.

The duties and responsibilities of

the Supervisory Committee include

the following:

• Engage a CPA firm to perform

a certified audit and member

account verification annually, as

required by the regulatory and

insuring agencies.

• Ensure that deficiencies

identified through audits are

brought to the attention of the

Board and management; track

and document progress made in

addressing deficiencies.

• Recommend courses of

corrective action to the

Board and management to

Supervisory Committee

challenges and opportunities and

will look to strike a proper balance

between the two that will add the

maximum value to the credit union.

We realize in such a competitive

financial market, we must be nimble

and able to change quickly, if needed,

in ways that enable the credit union

to continue providing excellent

service to our existing and new

members and to remain relevant now

and in the future. You can count on us

to continue executing our duties well.

We appreciate your loyal support.

Jim YearbyExecutive Committee ChairSeattle Metropolitan Credit Union

(continued)

Executive Committee Report (continued)

13

(continued)

Supervisory Committee Report (continued)

better ensure the safety and

soundness of their actions.

• Regularly review the financial

records and the Minutes of the

Board.

• Ensure that effective internal

controls are established and

maintained, and that policies and

procedures are established and

maintained and in compliance

with current regulations.

• Periodically meet with

management to discuss issues of

internal control and compliance.

• Review member complaints

concerning safety and

soundness issues.

• Carry out all duties as required

by law, regulation, and SMCU’s

Bylaws.

• Approve the firm that serves

as Tellers of the Volunteer

Elections for the Board and

Supervisory Committee.

• Report annually to the members

at the Annual Meeting about the

Committee’s activities.

The Committee held regular meetings throughout 2013. Turner, Warren, Hwang & Conrad, AC (TWHC) was engaged by the Committee to perform the annual certified CPA Audit for the calendar and fiscal year ending 12/31/13, and

the Member Account Verification as of 9/30/13.

In addition to the CPA Audit, and the joint risk examination by the Division of Financial Institutions; Department of Credit Unions (DFI/DCU), our state regulator; and the National Credit Union Administration (NCUA), our federal regulator, the Supervisory Committee reviewed all internal and external audit reports. In 2013, the Committee engaged outside experts to work with internal staff to perform audits, including a Member Information Risk Assessment, an Accounts Payable Audit, a Review of Corporate Credit Cards, an Automated Clearing House (ACH) and Wire Audit, an IT Operational Audit and multiple Security Assessments, a Non-Deposit Investment (NDIP) Compliance Review, a Bank Secrecy Act (BSA) Audit, a General Ledger (GL) Reconciliation Review, and a Review of Fiserv (legacy system) User Access Privileges.

At each regular meeting, the Committee reviewed the audit and exam responses and noted the progress. The Committee received the Board packets on a monthly basis and reviewed those for issues related

to safety and soundness.

The Committee remains focused on

the timely resolution of audit and

exam findings and recommendations.

14

In addition to the CPA Audit,

Management Letter and Financial

Statement Report, and the DFI/

DCU/NCUA regulatory report, the

Committee is especially concerned

with the following critical issues:

Asset Liability Management (ALM)

and Interest Rate Risk (IRR), the

safeguarding of member information,

IT security, financial management,

responsibility and accountability,

expense control, credit risk

management, and regulatory

compliance and risk management.

The Committee effectively carried

out its responsibilities during 2013.

As of this writing, there are no

material adjustments to report.

Ben WakefieldSupervisory Committee ChairSeattle Metropolitan Credit Union

Supervisory Committee (continued)

Finance & Budget Committee

T he Finance & Budget Committee

of Seattle Metropolitan Credit

Union is tasked with the following

duties and responsibilities:

• Reviewing SMCU’s financial

statements and supporting

documents;

• Reviewing delinquency statistics

and monthly charge-off reports;

• Reviewing the monthly Asset/

Liability Committee (ALCO)

meeting minutes.

• Reviewing our Credit Union

investment, liquidity, and

balance sheet risk-management

strategies;

• Recommending to the Board

of Directors key financial ratio

benchmarks for the Credit

Union for their approval and

adoption;

• Approving correspondent

financial institutions and

investment brokers;

(continued)

15

Finance & Budget Committee (continued)

• Reviewing monthly budget

variance reports and responses

from Management; and

• Recommending the annual

budget to the Board of Directors

for approval and adoption.

The members of the 2013 Finance &

Budget Committee were:

• Jim Fossos, Board Director,

• Ken Harer, Board Director,

Committee Chair

• Ray Hill, Board Director

• Frank Mathews, Board Director

• Richard Romero, Treasurer,

CEO

Providing support to the Committee

were Larry Grager, Senior Vice

President/Chief Financial Officer;

Caleb Cook, Vice President of

Lending; and Martin Dinn, Executive

Administrative Coordinator.

2013 Highlights

SMCU ended the year with

41,585 members.

SMCU paid just over $1.6 million in

dividends to our members.

Member loan balances ended the

year at $360 million, and member

share deposits increased to $537

million by December 31, 2013. Total

assets are just under $600 million.

In 2009, the National Credit Union

Administration (NCUA) announced

the Corporate [CU] Stabilization

Program, a program designed to add

financial strength to the credit union

industry over a number of years,

and to replenish the federal share

insurance fund (NCUSIF). SMCU’s

required assessment by NCUA was

$0.5 million for 2012 and $0.4 million

for 2013.

Loan losses dropped significantly

as our economy showed continued

improvement. Credit quality of our

loan portfolio improved significantly,

such that we needed no additional

contributions to provisions for loan

losses, making a big, favorable impact

on net earnings this year.

With prudent management, we

were able to increase our net

worth to 9.09%.

Your Finance & Budget Committee

members are proud that Seattle

Metropolitan Credit Union remains a

well capitalized credit union. We thank

our members, staff and volunteers.

Ken HarerFinance & Budget Committee ChairSeattle Metropolitan Credit Union

16

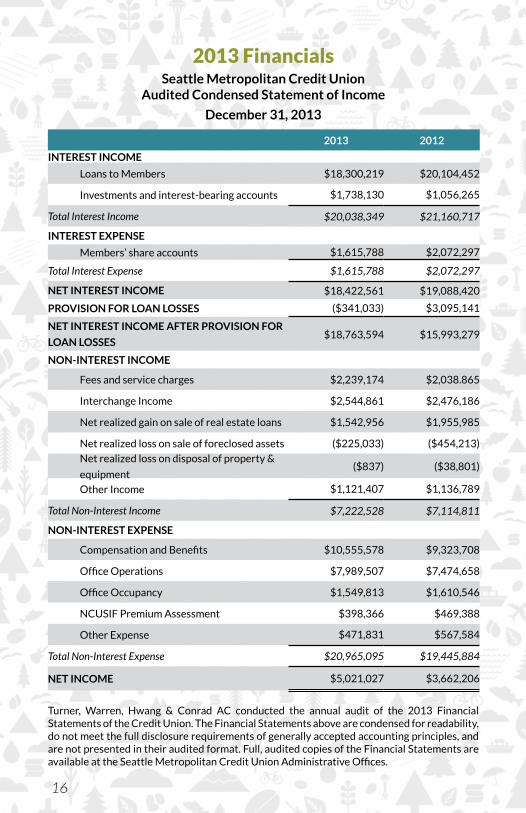

2013 FinancialsSeattle Metropolitan Credit Union

Audited Condensed Statement of Income

December 31, 2013

2013 2012

INTEREST INCOME

Loans to Members $18,300,219 $20,104,452

Investments and interest-bearing accounts $1,738,130 $1,056,265

Total Interest Income $20,038,349 $21,160,717

INTEREST EXPENSE

Members’ share accounts $1,615,788 $2,072,297

Total Interest Expense $1,615,788 $2,072,297

NET INTEREST INCOME $18,422,561 $19,088,420

PROVISION FOR LOAN LOSSES ($341,033) $3,095,141

NET INTEREST INCOME AFTER PROVISION FOR

LOAN LOSSES$18,763,594 $15,993,279

NON-INTEREST INCOME

Fees and service charges $2,239,174 $2,038.865

Interchange Income $2,544,861 $2,476,186

Net realized gain on sale of real estate loans $1,542,956 $1,955,985

Net realized loss on sale of foreclosed assets ($225,033) ($454,213)

Net realized loss on disposal of property &

equipment($837) ($38,801)

Other Income $1,121,407 $1,136,789

Total Non-Interest Income $7,222,528 $7,114,811

NON-INTEREST EXPENSE

Compensation and Benefits $10,555,578 $9,323,708

Office Operations $7,989,507 $7,474,658

Office Occupancy $1,549,813 $1,610,546

NCUSIF Premium Assessment $398,366 $469,388

Other Expense $471,831 $567,584

Total Non-Interest Expense $20,965,095 $19,445,884

NET INCOME $5,021,027 $3,662,206

Turner, Warren, Hwang & Conrad AC conducted the annual audit of the 2013 Financial Statements of the Credit Union. The Financial Statements above are condensed for readability, do not meet the full disclosure requirements of generally accepted accounting principles, and are not presented in their audited format. Full, audited copies of the Financial Statements are available at the Seattle Metropolitan Credit Union Administrative Offices.

17

2013 Financials (cont.)

Seattle Metropolitan Credit UnionAudited Statement of Financial Condition

December 31, 2013

2013 2012

ASSETS

Cash and Cash Equivalents $31,750,981 $80,580,763

Investments

Available for Sale $149,885,569 $77,530,867

Other $32,240,100 $34,776,700

Loans to Members $359,902,692 $365,350,322

Loans Held for Sale - $3,061,000

Accrued Interest Receivable $1,423,965 $1,270,897

Property and Equipment $11,418,861 $10,844,837

NCUSIF Deposit $4,979,577 $4,940,926

Other Assets $3,697,608 $4,097,330

TOTAL ASSETS $595,299,353 $582,453,642

LIABILITIES AND MEMBERS’ EQUITY

Liabilities

Members’ Share Accounts $537,864,885 $526,611,595

Accrued Expenses and Other Liabilities $5,568,339 $6,338,625

Total Liabilities $543,433,224 $532,950,220

Commitments and Contingent Liabilities

Members’ Equity

Retained Earnings, Substantially Restricted $5,201,500 $5,201,500

Undivided Earnings $48,885,321 $43,864,294

Accumulated Other Comprehensive Income ($2,220,692) $437,628

Total members’ equity $51,866,129 $49,503,422

TOTAL LIABILITIES AND MEMBERS’ EQUITY $595,299,353 $582,453,642

Turner, Warren, Hwang & Conrad AC conducted the annual audit of the 2013 Financial Statements of the Credit Union. The Financial Statements above are condensed for readability, do not meet the full disclosure requirements of generally accepted accounting principles, and are not presented in their audited format. Full, audited copies of the Financial Statements are available at the Seattle Metropolitan Credit Union Administrative Offices.

18