Embed Size (px)

Citation preview

FTC Capital GmbH

Praterstrasse 31/11

1020 Vienna | Austria

www.ftc.at | [email protected]

+43-1-585 61 69-0 Nicht zur Weitergabe – not for distribution

The 10 Biggest Myth in Asset Management

Morningstar Conference, Vienna, March 2012

Dr. Bernd Scherer

Professor of Finance, EDHEC Business School

Chief Investment Officer, FTC CAPITAL, Vienna

Myth 1:

Diversification Did Not Work During the Credit Crisis –

It Did

2

Revisit Diversification

Diversification eliminates unsystematic risk and all that investors areleft with is systematic risk. Diversification does not reduce risks. Risksare reduced with cash, i.e. deleverage. (SHARPE, 1972)

Investors have should not complain that they got exactly what theyasked for which is systematic risks.

However, investors fooled themselves by investing into products thathad mainly the equity factor running through them (equity, privateequity, high yield, corporate bonds, etc.)

The 10 Biggest Myth in Asset Management

3

Myth 2:

Young People Should Invest Into Stocks –

Only Some

The 10 Biggest Myth in Asset Management

4

The Role of Shadow Assets

Time does not diversify risks (SAMUELSON, 1968)! Withoutpredictability there are no horizon effects (CAMPBELL/VICEIRA,2002)!

Individual investors have both financial assets and shadow assets(human capital)

–The characteristic of human capital determines horizon effects

–Civil Servants and Investment Bankers

Shadow Assets are Everywhere; It is Shadow Assets That Make Investors Differ

Given that YOUR shadow assets are all equity like you should ALL rethink your portfolio

The 10 Biggest Myth in Asset Management

5

Myth 3:

Risk Parity is About Diversification –

Definitely Not

6

Risk Parity is About Return Expectations Only

The 10 Biggest Myth in Asset Management

7

S&P + 2Y Futures

S&P + 5Y Futures

S&P + 10Y Futures

S&P + 30Y Futures

Excess Return 1.77% 3.48% 5.26% 6.20%

Volatility 1.74% 4.14% 6.77% 9.42%

Sharpe 1.02 0.84 0.78 0.66

t-value 4.57 4.02 4.18 3.56

Turnover 24.74% 87.07% 138.83% 193.74%

Cum. Loss 3.94% 8.03% 15.63% 22.02%

Cum. Loss / Volatility 0.65 0.56 0.67 0.67

Average equity weight 1.7% 8.3% 16.5% 29.9%

Exhibit 1: Performance summary for risk parity portfolios. All strategy characteristics are calculated from monthly data and annualized where applicable. The data set is described in Appendix A. Returns are measured as log returns. Turnover is measured as the average of absolute monthly portfolio differences

multiplied by twelve. The t-value for SHARPE ratios is calculated from ( )212

1 /SR T+ , where SR

denotes the SHARPE ratio measured at monthly frequency over T months.

Risk Parity is About Return Expectations Only

The 10 Biggest Myth in Asset Management

8

Risk parity investing is a heuristic portfolio construction rule that is only

accidentally compatible with portfolio theory.

It neither attempts to arrive at explicit return forecasts nor does it require the

specification of an objective function.

Risk parity relies on the historical performance of low risk bond futures and

that the back-casted performance of risk parity portfolios depends entirely on

the choice of assets rather than on the concept itself.

While leverage aversion might provide theoretical support to risk parity

investing, the concept of risk parity is at odds with consumption based asset

pricing. In any case risk parity seem like an implicit bet on the continuation of

a bull market in bonds (e.g. via quantitative easing). Investors believing in

this can find better ways to take advantage of central bankers with a god

complex.

Myth 4:

Fully Funded Pension Systems Invested into Equities

Can Mitigate a Pension Crisis –

Definitely Not

9

We Could All Be Rich Fallacy

„ An investor that would have invested 200 years

ago one Euro into Equities would (assuming a 10%

return per annum) sit on 189 million Euros today

With 5% return (bonds) tbis would accumulate to

17.000 Euro instead. This shows the advantage of

equities and the advantage of a investing pensions

into equities. The whole society should do this.

Why is this statement wrong?

Survivor bias

Economic leverage changes and so change the

returns on equity

The real side and the financial side of the economy

are tightly linked.

The 10 Biggest Myth in Asset Management

10

Factories

Human

Capital, etc.

Bond

Market

Stock

Market

Financial

Assets

Real

Assets

Myth 5:

Larger Beta Outperforms Lower Beta –

No

11

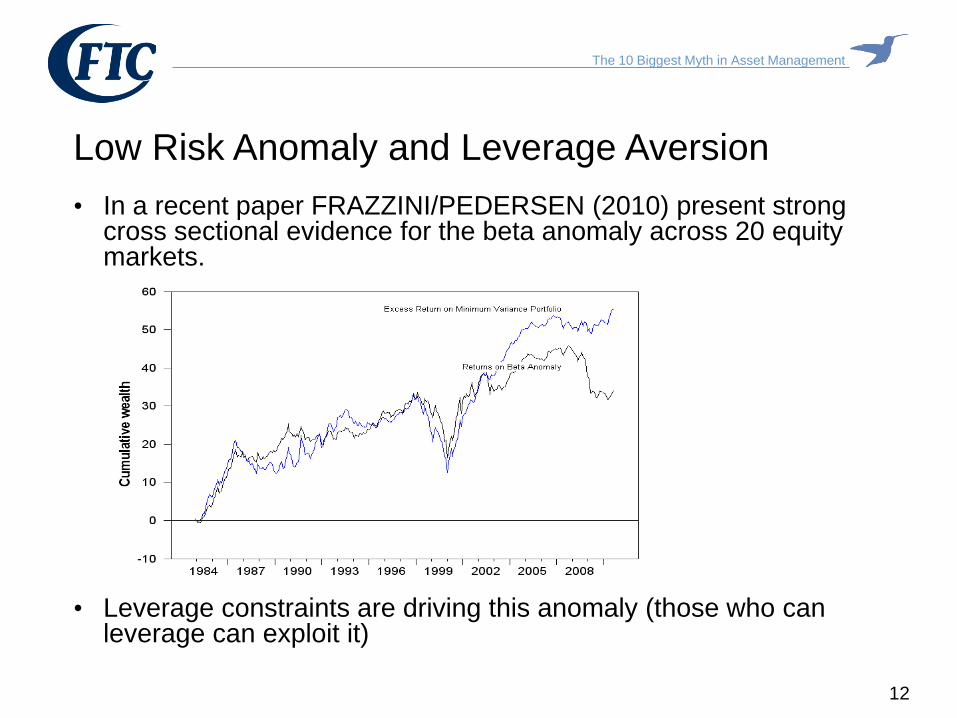

Low Risk Anomaly and Leverage Aversion

• In a recent paper FRAZZINI/PEDERSEN (2010) present strong cross sectional evidence for the beta anomaly across 20 equity markets.

• Leverage constraints are driving this anomaly (those who can leverage can exploit it)

The 10 Biggest Myth in Asset Management

12

Myth 6:

The Credit Crisis Shows that Efficient Markets Are

Dead –

To The Contrary

13

Where are the Yachts?

Very much as the efficient market hypothesis suggests few madeprofits from the credit crisis. Hedge fund performance has been bad inparticular.

Market events reminded us that past anomalies have either beenstatistical flukes or rewards for taking on (tail) risks

– January effect

– Carry strategies

– Short Volatility

– Value Effect

The 10 Biggest Myth in Asset Management

14

Myth 7:

The Last 50 Years Showed Great Improvements in

Defining New Risk Measures –

Not at All

15

A Vicious Research Cycle

The 10 Biggest Myth in Asset Management

16

Utility Optimization

NEUMANN/MORGENSTERN,

1944

Mean Variance Optimizationas an approximation to

Utility Optimization(MARKOWITZ, 1955)

Lower partial Moments

(FISHBURN/SORTINO 1990)

VaR and CvaRoptimization

(ROCKEFELLER/URYASEV,

2000)

Spectral Risk Measures

ACERBI, 2004

Myth 8:

Asset Management is an Annuity Business –

We can Rule This Out

17

From Managing Client Risk to Revenue Risks

Asset based fees (for benchmark long only managers) contain in-build market risks

These risks are incidental to the managers production process and need to be hedged

Asset managers need to start managing their own risks

The 10 Biggest Myth in Asset Management

18

0

0.5

1

1.5

2

2.5

3

3.5

2001 2002 2003 2004 2005 2006 2007 2008

Beta(rela

veto

localind

ex)

Year

Schroders

Invesco

BAER

NorthTrust

State

Price

Myth 9:

Corporate Pension Funds Should Invest Into Equities

– This is In (Almost) All Cases Wrong

19

Portfolio Theory versus Theory of the Firm

How do firms create value?– Invest into projects with positive net present value (positive EVA)

What is the net present value of capital market investments?– NPV equals 0 (capital markets are likely to be many times more efficient than investments

into real capital)

Shareholder value: (FISHER/HIRSHLEIFER)– Investments into max NPV projects maximize shareholder value(separation theorem)

All arguments that are in favor of corporate hedging also point to

pension liability hedging!

The 10 Biggest Myth in Asset Management

20

Myth 10:

There Are Many Asset Classes –

There are Fewer than you Think

21

The Definition of an Asset Class

Are returns (from unconditional buy and hold futures positions) positive and

statistically significant?

Index level returns often represent back-testing bias (if you don’t like back-tests you

don’t like commodity indices…) with respect to their weighting schemes (e.g. GSCI).

Are returns spanned by existing asset classes?

A statistically significant positive risk premium is not enough! The correct question to

pose is: is the risk premium already explained by existing asset classes?

Is this excess return enough to compensate for non-normality in return

exposure?

The 10 Biggest Myth in Asset Management

22