Embed Size (px)

Citation preview

•Thank you for the invitation to present to youThank you for the invitation to present to you today.

1

• The focus on my presentation will be on the y pcurrent state of the infrastructure market in Queensland, both in terms of project opportunities and project delivery.

• I will give a short overview of the current state of the PPP market and our experiences in alliancing and more traditional contracts

• I’ll then discuss some of the opportunities and challenges in the resources and property markets.

• Finally I will take a look to the future outlook for Q l d i f t t d h t thQueensland infrastructure and how we meet the challenges of sustaining the momentum built up over the past few years and retaining and building the skills base to meet the future infrastructure challenges.

2

• As the map shows, the Leighton Group has aAs the map shows, the Leighton Group has a significant presence in Queensland across resources, infrastructure, property and services

• This year, Thiess celebrates 75 years from its humble beginnings as a road contractor on the Darling Downs

• Our companies employ over 9,000 people directly in Queensland

• The bulk of our contract mining activities in Qld is coal in the Bowen basin undertaken by Thiess and Leighton Contractors.

• We are also delivering a number of major projects as part of the South East Queensland Infrastructure plan including the GatewayInfrastructure plan, including the Gateway Upgrade, CLEM 7 and Airport Link tunnels.

• I think its an exciting time to be involved in theI think its an exciting time to be involved in the infrastructure market in Queensland

• There are always doomsayers when things get a bit tougher, but if you looked at the market anytime in the past you would traditionally always see an expected drop off in projects twoalways see an expected drop off in projects two-three years out

• This is a function of the political cycle and the short term planning horizon of some Governments

• To their credit, the Queensland Government has put forward a 20 year South East Queensland Infrastructure Plan and have largely stuck to it. This is a model other States could follow.Th h ll i t k th t• The challenge now is to keep the momentum going in the context of tighter budgets at both the State and Federal level

4

• The Australian economic and socialThe Australian economic and social infrastructure market is forecast to stay at near record high levels, supported by government spending

• The infrastructure market is expected to decline in 2010 from its peak in 2009, and then resume steady growth, largely due to the large government infrastructure programs

• The Federal Government is delivering its $22bn Nation Building stimulus focussing onNation Building stimulus, focussing on economic and social infrastructure, with $8.5bn allocated to new transport investment

• Priority projects in Queensland include– Ipswich Motorway and Bruce Highway upgradesIpswich Motorway and Bruce Highway upgrades– Gold Coast Light Rail– Feasibility study into Brisbane inner city rail

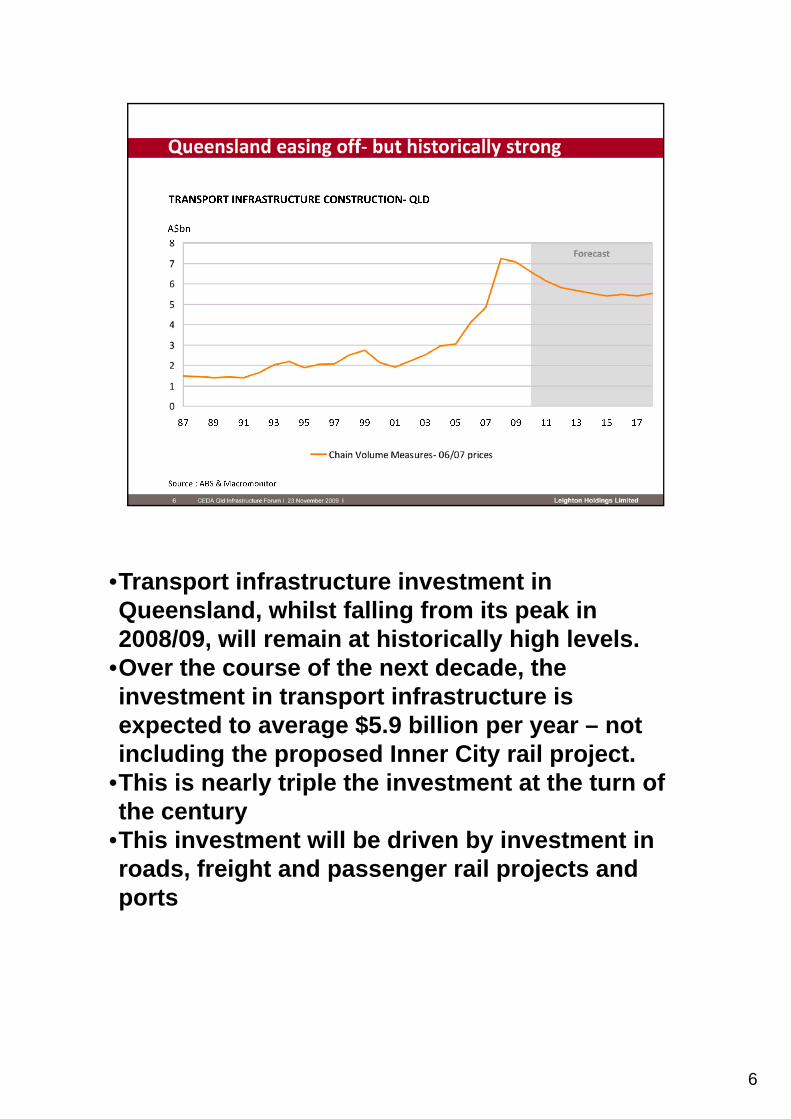

•Transport infrastructure investment in Queensland, whilst falling from its peak in 2008/09, will remain at historically high levels.

•Over the course of the next decade, the investment in transport infrastructure isinvestment in transport infrastructure is expected to average $5.9 billion per year – not including the proposed Inner City rail project.

•This is nearly triple the investment at the turn of the century

•This investment will be driven by investment in roads, freight and passenger rail projects and ports

6

• The downturn from the 2008/09 peak is mainlyThe downturn from the 2008/09 peak is mainly due to the completion of the major privately funded road projects, as shown in the chart above.

• These are all excellent projects and will have a significant impact on travel times and amenity insignificant impact on travel times and amenity in and around Brisbane, particularly for journeys to and from the airport.

• The $1.7 billion Northern Link project is now proposed to be council funded, and although there are a number of other potential PPP motorways in Queensland, it is unlikely that they will come to the market in the near future, for reasons I shall discuss shortly.

• The PPP model had to change- it would beThe PPP model had to change it would be difficult to finance the traditional traffic model in today’s market.

• However as the Qld Schools package currently being delivered by Leighton Contractors and the Victorian Desalination plant has shown it is stillVictorian Desalination plant has shown, it is still possible to finance quality social infrastructure PPP’s.

• In my view, the model needs to continue to mature so that there is a true partnership p papproach - the often forgotten ‘third P’- with a more even handed approach from all parties

8

• The contractor to date has taken all of theThe contractor to date has taken all of the design and construction risk, as well as participating as an equity financier, but often on an unequal footing with the finance sector in terms of provisions such as escrow conditions on equity holdings.on equity holdings.

• The contractor also faces exposure to increasingly onerous conditions regarding ‘material adverse change’ provisions and has been expected to step up beyond the call of duty t l i th t l fi l t dto resolve issues that are purely finance related, without reward

• It is not reasonable to ask the contractor to step in, and to put on the table part of the D+C margin, which reflects the construction risk, to g , ,resolve a financing dispute.

Another element of the ‘partnership’ that is out p pof kilter is bidding costsThe cost of bidding PPPs has become excessive in Australia- much of this tied up in increasingly prescriptive contractual requirements both for the sponsors and for the D+C contractorsD+C contractors.A key factor behind this is lawyers encouraging clients to shift greater risk to the contractor-ignoring the key principle that risk should lie with the party best able to manage it.Bonding and guarantee requirements are alsoBonding and guarantee requirements are also increasingly onerous, and as projects get bigger, fewer contractors have the balance sheet to be able to provide the bonding required.

Government’s talk about increasingGovernment s talk about increasing international competition in this marketThis won’t happen when bid costs remain high and international players can get better returns for lower risk elsewhereIt’s frustrating that Governments don’t recognise that Australian contractors are fiercely competitive and an export success story, providing the infrastructure that Australia needs to be internationally competitiveneeds to be internationally competitiveIf Governments want to improve international competition, they should look at aligning risk allocations with global practices.They will find that D+C contractors in AustraliaThey will find that D+C contractors in Australia manage risks that would give many overseas companies second thoughts.

• Challenges remain to the PPP market,Challenges remain to the PPP market, particularly for economic infrastructure

• It would be difficult to finance a project that involved the full pass through of traffic risk in the current climate

• Credit remains tight, compounded by the withdrawal of some overseas players, although it has improved somewhat in the last six months

• However, debt financing that is available is characterised by:

– Shorter tenors and increased refinancing risk– Increased financing margins– Bank unwillingness to take syndication risk– Capped take and hold appetite meaning that the domestic market may not have the depth to finance larger ($1 b+) projects

• I’ve outlined some of the issues with the PPPI ve outlined some of the issues with the PPP model in the current market, but there are of course a range of alternative procurement options depending on the project.

• We have strong experience in Alliancingdelivering quality infrastructure in Queenslanddelivering quality infrastructure in Queensland across a number of sectors, including

– Water– Rail– RoadsRoads

• Program alliancing has also been delivering great results

13

• For example, the Thiess United Group JointFor example, the Thiess United Group Joint Venture, as part of the Trackstar Alliance, are delivering for Queensland Rail four major rail infrastructure projects in south east Queensland as part of the South East Queensland Infrastructure Plan (SEQIP) Rail AllianceInfrastructure Plan (SEQIP) Rail Alliance.

• Under the SEQIP Rail Alliance, the joint venture partners plan, design, construct and commission all civil earthworks and structures, stations, signalling, overhead and trackstations, signalling, overhead and track installations for the four railway infrastructure projects. These include:

– Caboolture to Beerburrum duplication – Robina to Reedy Creek extension – Beerburrum to Landsborough duplication, and – Corinda to Darra third track.

• We are also continuing to deliver traditional gdesign and construct contracts, such as the Northern Access Road for Brisbane Airports.

• There is no ‘perfect’ or ‘one size fits all procurement method. There are a range of contract types that will be best suited depending on the conditions around the projecton the conditions around the project.

• What I would caution against is the shift in some recent PPP’s to split the project into a D+C and separate PPP component whilst still trying to apply a PPP risk profile to the D+C contractor. This will lead to tensions and interface issues

• Again we need a reasonable risk sharing model where risks and rewards are aligned and manageable

• I’d like now to turn to the opportunities in theI d like now to turn to the opportunities in the resources and property sector, looking in the context of where the capital investment, skills and jobs momentum in Queensland might be maintained as State Government infrastructure investment eases off.investment eases off.

16

• Demand for Queensland’s coal will continue toDemand for Queensland s coal will continue to remain strong, fuelled by China’s appetite for steel production to meet its own infrastructure needs

• Queensland is well placed as a low cost, reliable supplier of coal to Asia and the rest of the world.

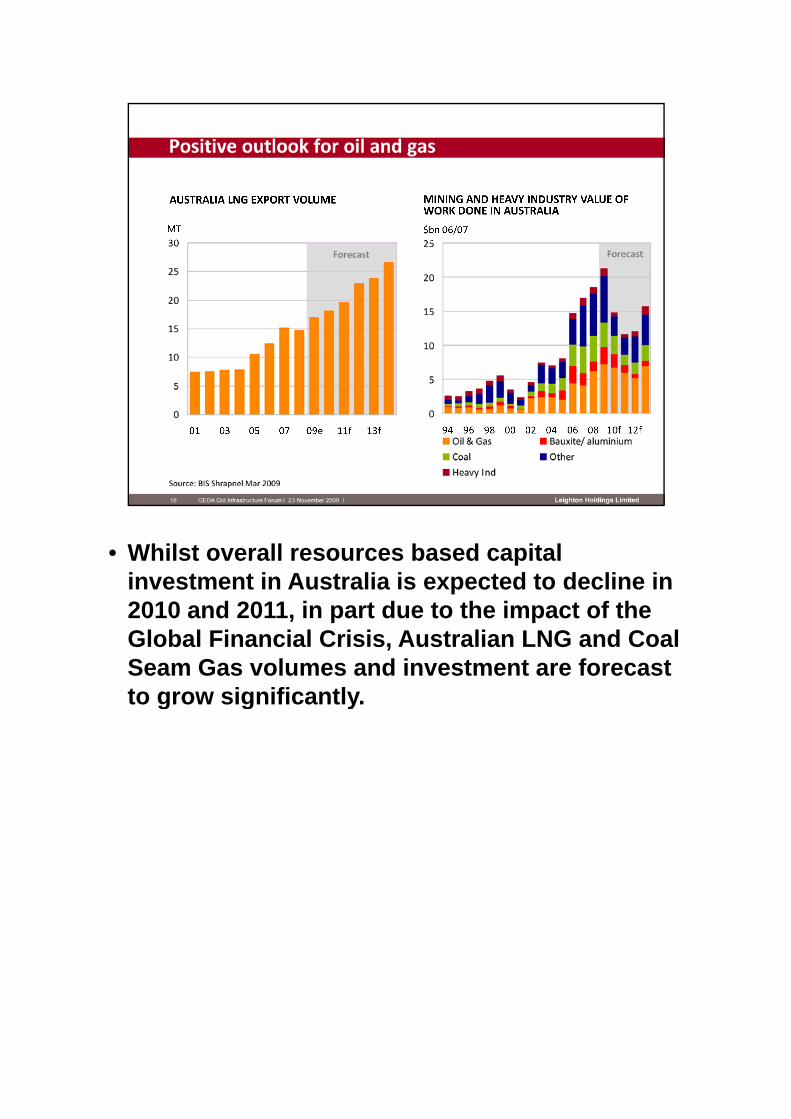

• Whilst overall resources based capitalWhilst overall resources based capital investment in Australia is expected to decline in 2010 and 2011, in part due to the impact of the Global Financial Crisis, Australian LNG and Coal Seam Gas volumes and investment are forecast to grow significantlyto grow significantly.

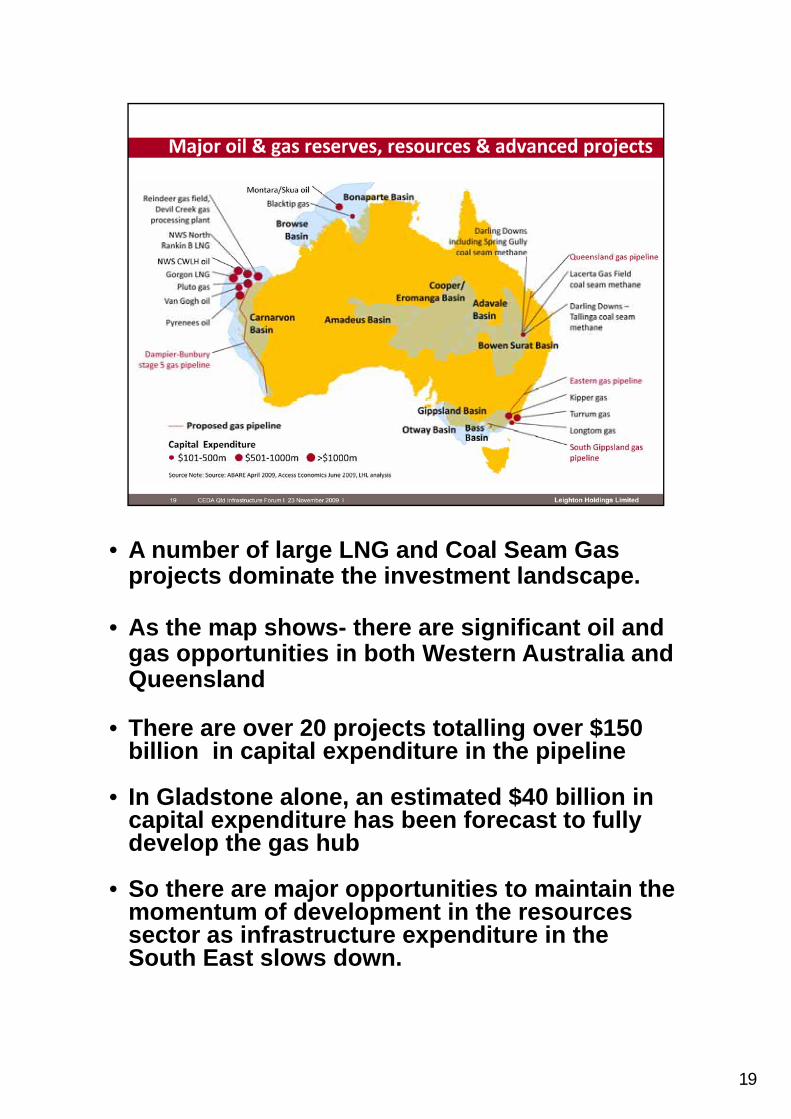

• A number of large LNG and Coal Seam Gas gprojects dominate the investment landscape.

• As the map shows- there are significant oil and gas opportunities in both Western Australia and Queensland

• There are over 20 projects totalling over $150 billion in capital expenditure in the pipeline

• In Gladstone alone, an estimated $40 billion in capital expenditure has been forecast to fullycapital expenditure has been forecast to fully develop the gas hub

• So there are major opportunities to maintain the momentum of development in the resources sector as infrastructure expenditure in the South East slows downSouth East slows down.

19

• The continued strong resources sector hasThe continued strong resources sector has provided some support to the property market, with companies such as Santos significantly expanding their presence in Queensland.

• However, the property market internationally has undoubtedly been hit by the global financial crisisundoubtedly been hit by the global financial crisis, and Queensland is no exception

• The restricted availability of both equity and debt continue to constrain institutional investment in commercial property in Brisbane, and the supply pipeline has slowed to a trickle.

• CB Richard Ellis is forecasting the Brisbane CBD vacancy rate to peak at 13.7% in 2010

• The commercial property investment market is expected to remain soft for sometimeexpected to remain soft for sometime.

• But it’s not all doom and gloom for property in Queensland

• Access Economics predict Queensland to again lead the nation with economic growth of 3.8%lead the nation with economic growth of 3.8% per annum between 2009 and 2013

• We should see a slow recovery for the industrial sector after 2011

• The residential sector is also expected to pexperience an upswing from 2010, driven by underlying demand growth, supply shortages, continuing relatively low interest rates and improving affordability

• Turning now to the future. We could ask the geconomists who have predicted 8 out of the last 3 depressions. Or we could use a bit of common sense.

• A recent report for the Business Council of Australia on building Australia’s future infrastructure needs stated that “given theinfrastructure needs stated that given the constraints faced by Governments, Australia may struggle to invest in the infrastructure we need for future growth”.

• It also said that “it will be important to avoid the stop/start investment in infrastructure in the ppast, and ensure that we do not only invest in infrastructure in response to a crisis”

• I agree with those comments• If Australia stops investing in the infrastructure

to make our cities work and to get our resources gto market we will fall behind our international competitors and lose market share, even as our major customers in Asia pick up growth.

22

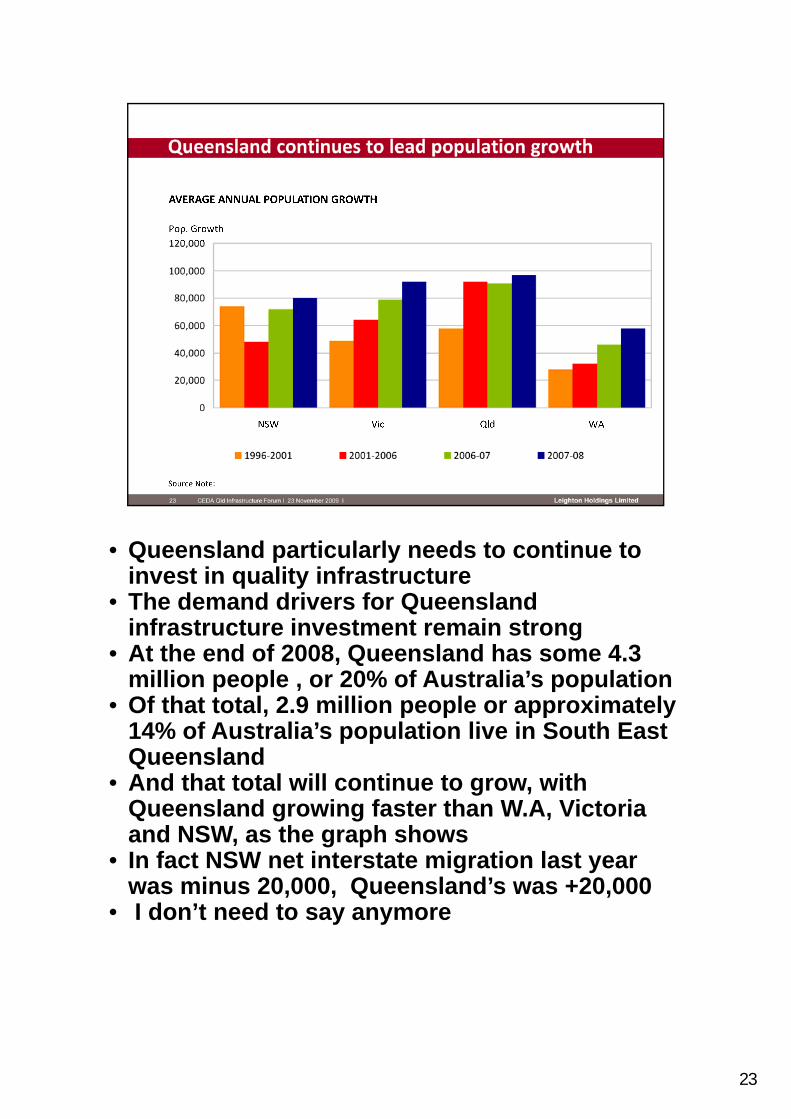

• Queensland particularly needs to continue to Q p yinvest in quality infrastructure

• The demand drivers for Queensland infrastructure investment remain strong

• At the end of 2008, Queensland has some 4.3 million people , or 20% of Australia’s population

• Of that total, 2.9 million people or approximately 14% of Australia’s population live in South East Queensland

• And that total will continue to grow, with Queensland growing faster than W.A, Victoria

d NSW th h hand NSW, as the graph shows• In fact NSW net interstate migration last year

was minus 20,000, Queensland’s was +20,000• I don’t need to say anymore

23

• As I pointed out earlier, demand for QueenslandAs I pointed out earlier, demand for Queensland coal, particularly from China, remains strong.

• As well as demand for contract mining, that means we will need to continue to invest in infrastructure to get the coal to market, including;

– the Northern and Southern missing links in the freight rail network– coal terminals at places like Wiggins Island

th f th d l t f H P i t d– the further development of Hay Point and Dalrymple Bay

• In conclusion, I believe the prospects for theIn conclusion, I believe the prospects for the infrastructure market in Queensland remains strong.

• Investment in transport infrastructure in the South East will ease off, but from all time highs.

• However, investment in infrastructure for the freight supply chain for our resources sector will need to pick up if we are to retain our international competitiveness.

• As long as Government’s keep their nerve andAs long as Government s keep their nerve and continue to have a long term focus on the infrastructure needed to grow the State, Queensland will stay a strong market and remain a great place to live, work and invest.Thank you for again for the invitation to speak• Thank you for again for the invitation to speak.

25