Embed Size (px)

Citation preview

Thai Film Industries Plc.Thai Film Industries Plc.

2

TOPICS OF TODAYTOPICS OF TODAY

World BOPP Demand VS. Supply

History of Pricing

TFI Expansion Plan

Q & A

3

BOPP DEMAND VS. SUPPLYBOPP DEMAND VS. SUPPLY

4

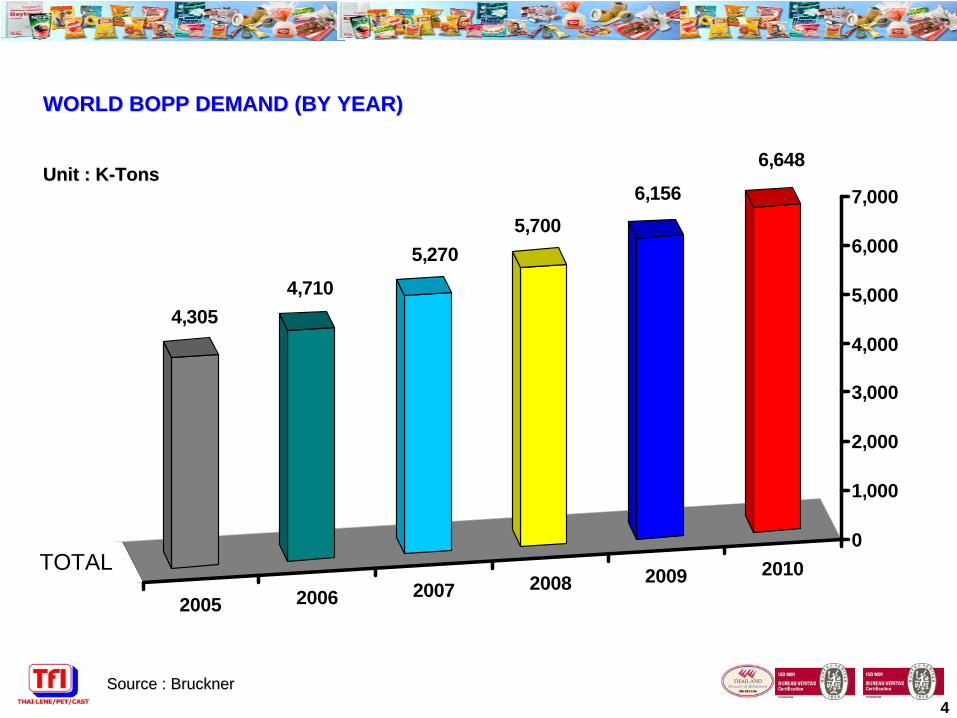

WORLD BOPP DEMAND (BY YEAR)WORLD BOPP DEMAND (BY YEAR)

Source : BrucknerSource : Bruckner

Unit : KUnit : K--TonsTons

2005 2006 2007 2008 2009 2010TOTAL

6,648

6,1565,700

5,270

4,7104,305

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

5

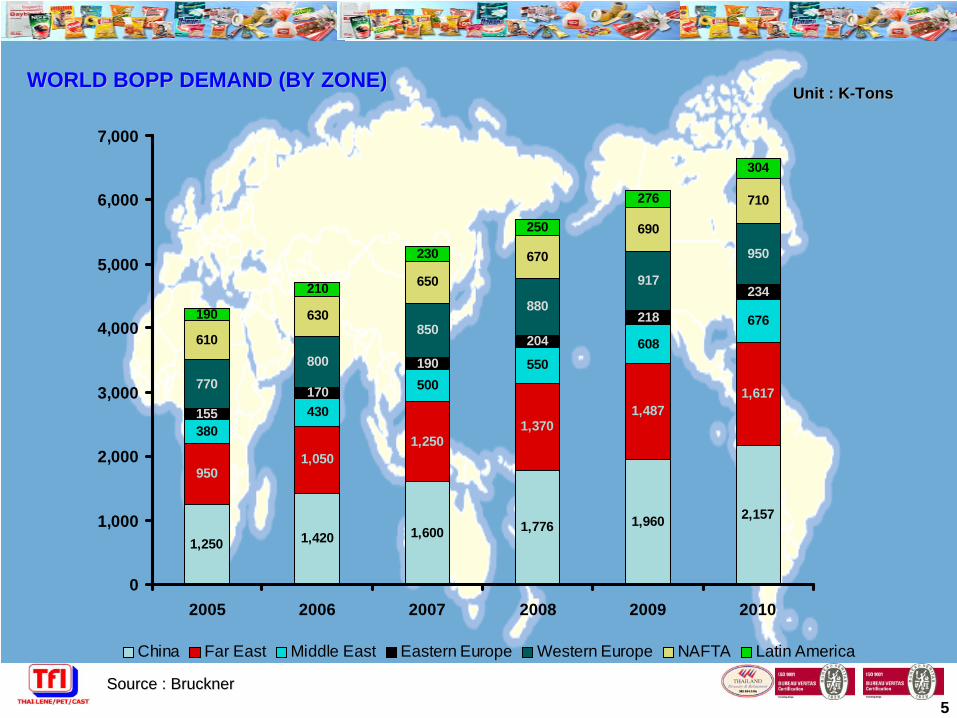

WORLD BOPP DEMAND (BY ZONE)WORLD BOPP DEMAND (BY ZONE)

Source : BrucknerSource : Bruckner

Unit : KUnit : K--TonsTons

1,250 1,420 1,600 1,776 1,960 2,157

9501,050

1,2501,370

1,4871,617

380430

500550

608

676

170

190204

218

234

770800

850

880

917

950

610

630

650

670

690

710

210

230

250

276

304

155

190

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2005 2006 2007 2008 2009 2010

China Far East Middle East Eastern Europe Western Europe NAFTA Latin America

6

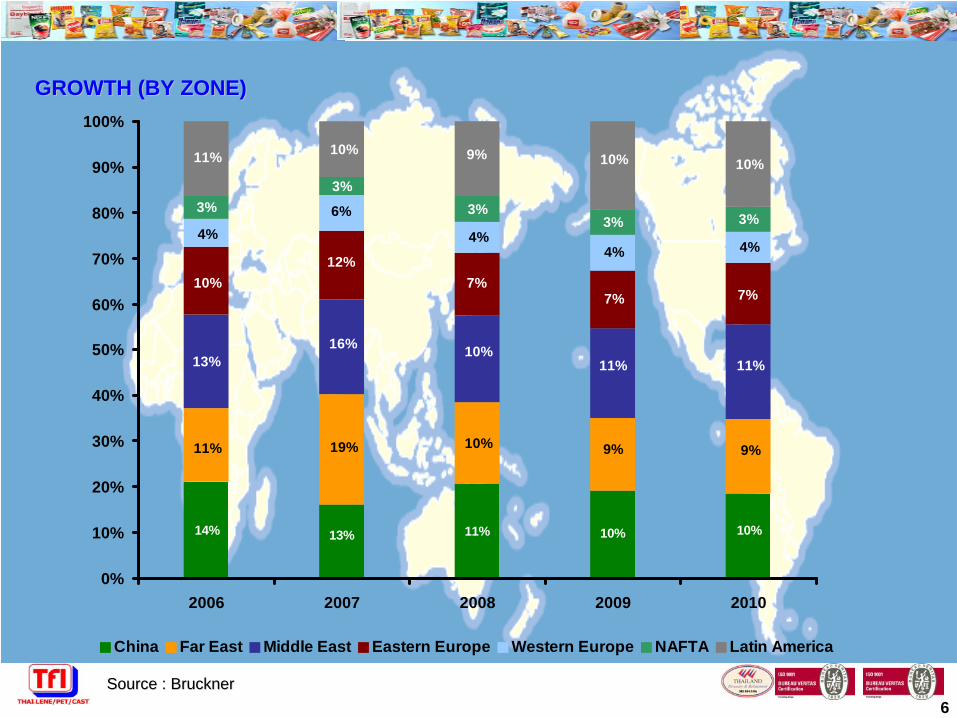

GROWTH (BY ZONE)GROWTH (BY ZONE)

Source : BrucknerSource : Bruckner

3%3%

3% 3%

10%10%11%13%14%

9%9%10%19%11%

11%11%10%16%

13%

7%7%7%

12%10%

4%4%4%

6%4%

3%

11% 10% 9% 10% 10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006 2007 2008 2009 2010

China Far East Middle East Eastern Europe Western Europe NAFTA Latin America

7

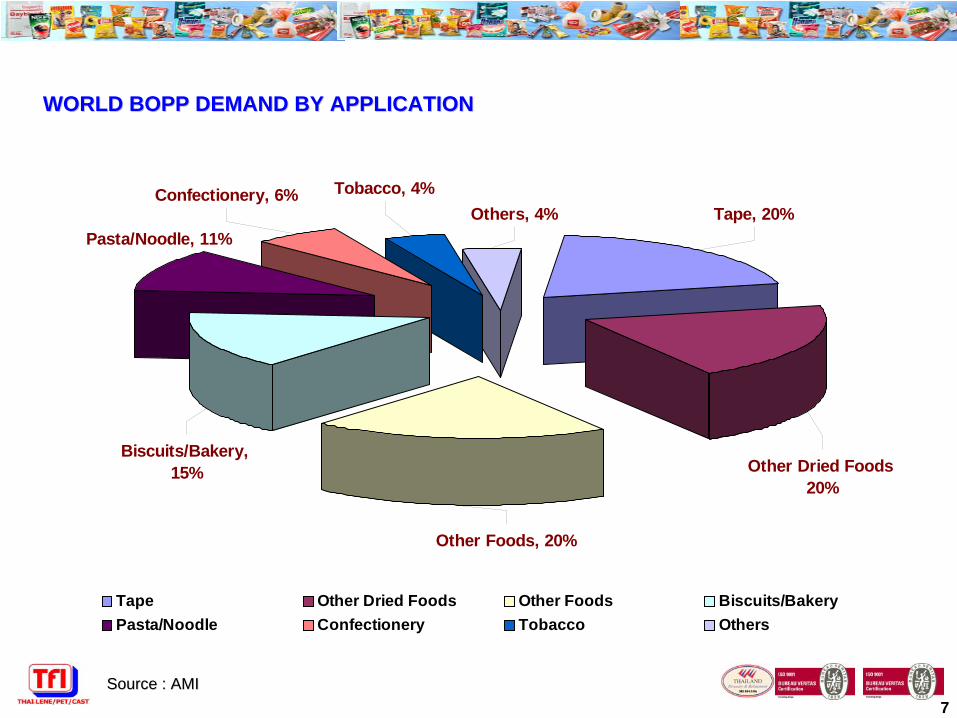

WORLD BOPP DEMAND BY APPLICATIONWORLD BOPP DEMAND BY APPLICATION

Source : AMISource : AMI

Pasta/Noodle, 11%

Other Dried Foods 20%

Other Foods, 20%

Biscuits/Bakery, 15%

Tape, 20%Others, 4%Confectionery, 6% Tobacco, 4%

Tape Other Dried Foods Other Foods Biscuits/BakeryPasta/Noodle Confectionery Tobacco Others

8

WORLD BOPP DEMAND VS. SUPPLYWORLD BOPP DEMAND VS. SUPPLY

* Global capacity used at 85% utilization** Capacity in year 2010, not include new machines which not ordered.- Growth at 8% per years (= 456,000 tons in year 09 and 492,000 tons in 2010)

Unit : KUnit : K--TonsTons

Source : BrucknerSource : Bruckner

5,000

5,722

6,046

5,700

6,156

6,648

(434)

(700)

(602)

-2,000 0 2,000 4,000 6,000 8,000

Yr 08

Yr 09

Yr 10

Global Capacity* Demand Balance

9

Sample of new capacities 2008Sample of new capacities 2008--20102010

ASIA

China : Fujian Fuzhou Jingtai (8.2m. line), Zhejiang Baihui (8.2m.line)

India : Cosmo ( 8.2m. line), Jindal(8.7m. line),Polyplex (8.7m.line)

Thailand : AJ Plast (8.2m.line)

MIDDLE EAST

U.A.E : Flex Middle East (8.7m.line)

Saudi Arabia : Roward National (8.2m.line)

Source : AMI + BrucknerSource : AMI + Bruckner

10

NAFTA

USA : Vifan (8.2m.line)

Mexico : Altopro S.A. (8.2m.line)

EUROPE

Russia :

Biaxplen, Euromet (8.2m.line)

France :

Toray Film ( 8.2m.line)

Turkey :

Turkmenneftegas ( 7.2m.line)

SOUTH AMERICA

Brazil : Polo (8.2m.line), Vitopel (8.2m.line)

Source : AMI + BrucknerSource : AMI + Bruckner

Sample of new capacities 2008Sample of new capacities 2008--20102010

11

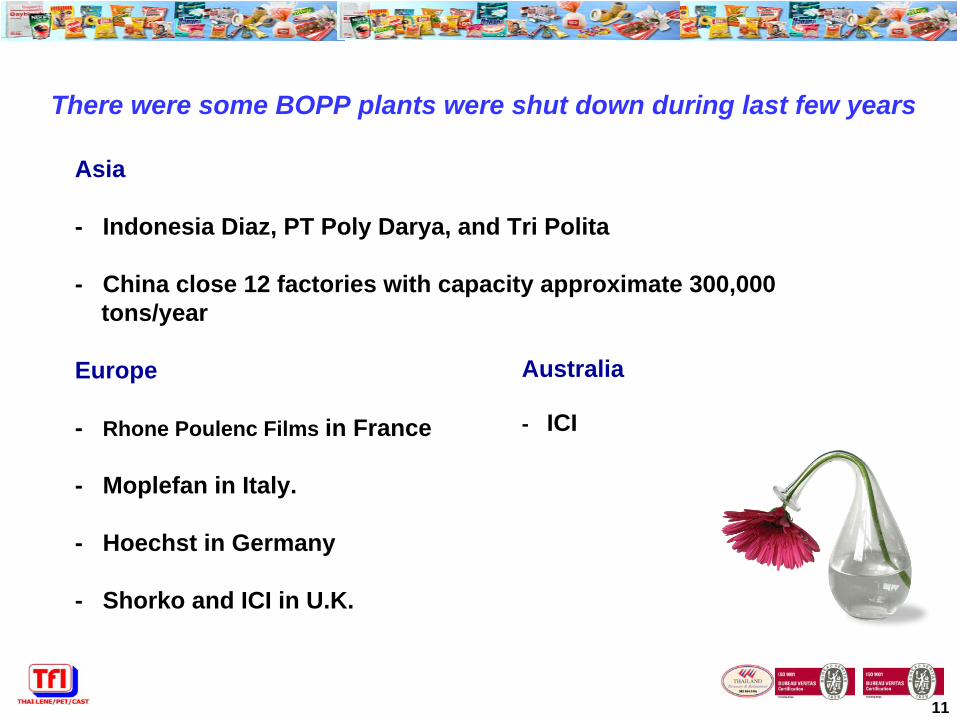

There were some BOPP plants were shut down during last few years

Asia

- Indonesia Diaz, PT Poly Darya, and Tri Polita

- China close 12 factories with capacity approximate 300,000 tons/year

Europe

- Rhone Poulenc Films in France

- Moplefan in Italy.

- Hoechst in Germany

- Shorko and ICI in U.K.

Australia

- ICI

12

Some were merged and acquired…

- Hoechst (Germany) was merged by Treophan.

- Shorko (U.K) and Radici (Italy) were taken over by Taghleef (Dubai film group).

- Manuli (Italy) now inviting new investors.

Bulgaria

- Famtex was merged by Plastchim (supplier of PE films, PP and injection molds)

Source : AMI + Plastic MagazineSource : AMI + Plastic Magazine

13

Growth of BOPP comes from…

1. Increasing of world population

2. Growing of economy in China, India, Russia, Brazil and etc.

3. Substitution to other plastic films i.e. PE film, LDPE film, Cellophane film, PVC film and paper. In term of yield and price per sq.meter, BOPP film is better alternative.

4. Increasing of consumption per capita in developing countries due to higher standard of living required such as in China, Indochina, India, South America and etc.

5. Higher demand of consumer on sanitation and environmentally friendly issues.

Source : AMI + TFISource : AMI + TFI

14

HISTORY OF PRICINGHISTORY OF PRICING

15

1998 1998 -- 2007 Historical Price BOPP Plain Film (Export Market)2007 Historical Price BOPP Plain Film (Export Market)

Unit : US$/TonsUnit : US$/Tons

0200400600800

10001200140016001800200022002400260028003000320034003600

BOPP Film 2000 1400 1200 2000 2500 1800 1300 1000 1100 1150 1200 1250 1250 1300 1500 1650 2200 2450 3000 3200 3400

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007*1ST HALF 2008

**2ND HALF 2008

2009 F

2010 F

Down Trend Up Trend Down Trend Up Trend Down Trend Up Trend

16

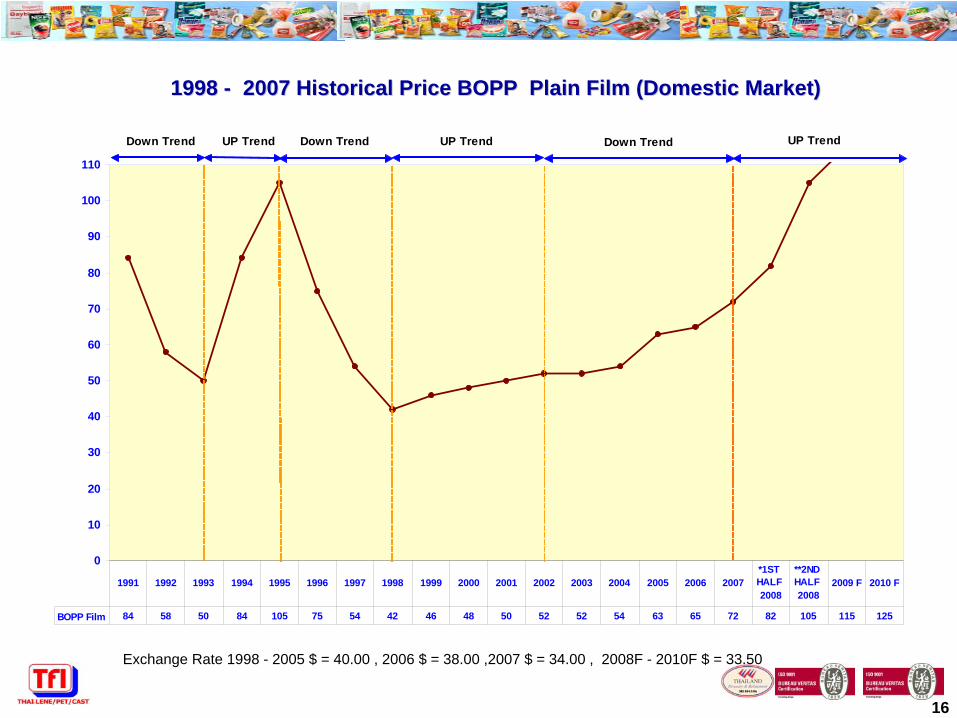

1998 1998 -- 2007 Historical Price BOPP Plain Film (Domestic Market)2007 Historical Price BOPP Plain Film (Domestic Market)

Exchange Rate 1998 - 2005 $ = 40.00 , 2006 $ = 38.00 ,2007 $ = 34.00 , 2008F - 2010F $ = 33.50

0

10

20

30

40

50

60

70

80

90

100

110

BOPP Film 84 58 50 84 105 75 54 42 46 48 50 52 52 54 63 65 72 82 105 115 125

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007*1ST HALF 2008

**2ND HALF 2008

2009 F 2010 F

Down TrendDown Trend Down TrendUP Trend UP Trend UP Trend

17

TFI EXPANSION PLANTFI EXPANSION PLAN

18

TFI Expansion Plan 2008TFI Expansion Plan 2008--20102010Unit : Tons/YearUnit : Tons/Year

115,000115,000 115,000100,000

3,5003,500 3,500

23,50017,000

3,5003,500 3,500

7,000

7,0007,000 7,000

5,000

107,000

160,500

122,000 122,000

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

2007 2008 2009 2010

BOPP PET CPP METALLISED BOPA Total

19

With LoveWith Love Thank you for your attentionThank you for your attention

Wanlop KunanukornkulWanlop Kunanukornkul

Thai Film Industries Public Co,,Ltd.Thai Film Industries Public Co,,Ltd.

![[English.01] KPIC BOPP Film Grade CatalogEnglish.01] KPIC BOPP Film Grade...• Bruckner Line : 25㎛BOPP film. • Above data are typical laboratory averages. They are intended to](https://img.dokumen.tips/doc/110x75/5c70159d09d3f20d2f8b6797/english01-kpic-bopp-film-grade-english01-kpic-bopp-film-grade-bruckner.jpg)