Embed Size (px)

Citation preview

Registrar of Cane Cooperative Societies, Uttar Pradesh

TERMS OF REFERENCE for selection of Valuer(s) for 25 Cooperative Sugar Mills (including 4 with distilleries) of U.P.Cooperative Sugar Factories Federation Limited

(UPCSFFL) 1. Purpose i. The Registrar Cane Cooperative Societies, Uttar Pradesh (Registrar) intends to transfer assets or assets and liabilities of at least 25 nos. of Cooperative Sugar Mills of UPCSFFL(hereinafter referred as Cooperative Sugar Mills).. For this purpose the Registrar wants to engage services of a panel of Valuer(s) to value assets or assets and liabilities of the Cooperative Sugar Mills as per U.P. Cooperative Societies Act, 1965 and U.P. Cooperative Sugar Mills (Special Provision) Rules, 2007 and other existing laws. UPCSFFL are engaged in the production and sale of sugar and alcohol with mills situated at different locations in the State of Uttar Pradesh. A brief profile of Cooperative Sugar Mills is enclosed at Annexure-I for ready reference. Further information in respect of the same can be accessed on websites � HYPERLINK "http://www.upcane.org" �www.upcane.org� or � HYPERLINK "http://www.upsugarfed.org" �www.upsugarfed.org� or can be obtained at the office of the undersigned. Registrar, Cane Cooperative Societies ,Uttar Pradesh, 17, New Beri Road, Lucknow- 226001 Uttar Pradesh Ph: 0522 – 2204295

0522 – 2204163 (Fax) RFQ cum RFP Documents may be taken by paying Rs.1000/-(Rs one thousand only) non refundable from the office of the Registrar, Cane Cooperative Societies, Uttar Pradesh. RFQ cum RFP document down loaded from the website should be submitted with non refundable draft of Rs. 1000/-/-(Rs one thousand only) in favour of Registrar, Cane Cooperative Societies, Uttar Pradesh payable at Lucknow. For the purpose of valuation exercise, 25 mills have been grouped into five bundles (or ‘packets’). The bidders may bid for one or more bundles. Two independent valuers will be appointed for independent valuation of each bundle. The details of Cooperative Sugar Mills in each bundles are as below:

Packet Unit Name District Remarks Morna Muzaffarnagar Sugar mill Gajraula Jyotibafule Nagar Sugar mill

1.

Snehroad Bijonre Sugar mill

Bagpat Bagpat Sugar mill Sarsawa Saharanpur Sugar mill Ramala Bagpat Sugar mill Anoopshahr Bulandshahr Sugar mill Satha Aligarh Sugar mill Bilaspur Rampur Sugar mill

2.

Kaimganj Farrukhabad Sugar mill with distillery Semikhera Bareilly Sugar mill Budaun Badaun Sugar mill Bisalpur Pilibhit Sugar mill Powayan Shahjahanpur Sugar mill

3.

Pooranpur Pilibhit Sugar mill Tilhar Shahjahanpur Sugar mill Belrayan Lakhimpur Kheri Sugar mill Sampurannagar Lakhimpur Kheri Sugar mill with distillery Mahmudabad Sitapur Sugar mill

4.

Nanpara Bahraich Sugar mill with distillery Sultanpur Sultanpur Sugar mill Sathiaon Azamgarh Sugar mill Aurai Sant Ravidas Nagar Sugar mill Ghosi Mau Sugar mill with distillery

5.

Rasra Ballia Sugar mill 2. Eligibility criteria i. The bidder should be a Government Approved Valuer/ Practising Chartered

Accountant. ii. Bidder who has completed valuation assignments of at least 10 industrial units, of

which at least 2 assignments involve valuation of sugar mill/distillery will be qualified for opening of their financial bids.

iii. Preference will be given to valuers with prior experience of valuation of Industrial Units/PSUs for disinvestment purposes for Government of India or State/UT using all four methods of valuation.

iv. The bidder should satisfy itself that it has capacity and manpower and undertake that it can complete valuation of the awarded bundles within the stipulated timeframe (4 weeks from the date of appointment).

v. The bidder will need to submit a Bid Security of Rs. 50,000 (Rupees fifty Thousand Only) per bundle which shall be refunded to the unsuccessful bidders within one week from the date of opening of the bids. For successful bidders, the same shall be converted into Performance Security and will be refunded after completion of the valuation assignment to the satisfaction of Registrar.

3. Proposed schedule for completing the assignment The Valuer shall be expected to have the entire valuation process completed and submit its report within 4 weeks from the date of appointment. The site visit to Cooperative Sugar Mills and distilleries shall be completed within two weeks of appointment. The appointed valuer may contact the REGISTRAR for any assistance/ escort at the site of sugar mill. If the valuer feels that he will not be able to complete the assignment in the stipulated time frame due to non- availability of data it should give a notice stating the information gaps and the expected time delays on such account so as to reach the office of REGISTRAR, at least 7 days before the completion date stating the information gaps. 4. Last date for submission of bid

The interested bidders may submit their bids within a sealed cover subscribing on the top of envelope “Bid for appointment of Valuer” positively by 13.00 hrs. on January 30, 2009 or before, on any working day between 11.00 hrs. and 16.00 hours (IST) to the office of the Registrar,Cane Cooperative Societies ,Uttar Pradesh,17, New Beri Road, Lucknow- 226001 Uttar Pradesh Ph: 0522 – 2204295,0522 – 2204163 (Fax). 5. Bidding Format The sealed cover (as mentioned in para 4 above) should contain: • Application Covering letter as per Annexure II • 2 separate sealed envelops marked as:

- Envelop-A: Technical Bids (as per Annexure III) & - Envelop-B: Financial Bids (as per Annexure IV)

Envelop – A i.e. Technical Bid, should contain the supporting documents (as per details below and Annexure III) and Bid Performance Security amount whereas, Envelop -- B should contain unconditional Financial Bid. Documents to be submitted with Technical Bids

i. Valid and duly authenticated registration certification issued by the State or Central

Government certifying the Valuer as a “Government Certified Valuer”/certificate of practicing chartered accountant.

ii. Proof for each completed valuation assignment for which credit is claimed iii. Full particulars of the constitution, ownership and main business activities of the

prospective Valuer(s) (bidder). iv. Undertaking stating that the bidder has not been barred from undertaking similar

assignments from any of the State Governments or the Union Government of India. v. Details of the pending litigation and contingent liabilities, if any, that could affect the

performance of the bidder under the mandate, as also details of any past conviction and pending litigation against sponsors/partners and any areas of possible conflicts of interest.

Documents to be submitted with Financial Bids The Valuer(s) are required to submit the sealed Financial Bids incorporating the Lump-sum Fee chargeable (including valuation fee, expected out of pocket expenses and gross of all applicable taxes). The Bid should be unconditional. The valuer may bid for one or more bundles for valuation. The bid should indicate the fee chargeable on per Bundle for the following:

a. Fee for Valuation of Bundle 1 b. Fee for Valuation of Bundle 2 c. Fee for Valuation of Bundle 3 d. Fee for Valuation of Bundle 4 e. Fee for Valuation of Bundle 5

6. Opening of Bids & Bid Evaluation Criteria The opening of bids shall take place at the office of the Registrar,Cane Cooperative Societies ,Uttar Pradesh,17, New Beri Road, Lucknow- 226001 Uttar Pradesh at 15.00 hours IST in the presence of bidders on January 30th 2009. The bids shall be scrutinized on the basis of details provided in Envelop A (Technical Bid) following the under mentioned qualifying criteria: Technical

• Past experience of the bidder • Past experience of Valuation in disinvestment/sale for GOI

• Past experience of valuation in disinvestment for Central/ State Government PSUs

• Past experience valuation of industrial units • Past experience valuation of Cooperative Sugar Mills • No. of years experience of key personnel associated with the engagement • Number of certified valuers with the firm

Financial Lump sum Fee quoted for valuation For each Bundle, the two independent valuers

with with the lowest demanded will be appointed as valuers. 7. Letter of Appointment The selected Valuer(s) shall be issued a Letter of Appointment after completion of the bid evaluation and selection process. 8. Payment of fee to the appointed Valuers i. After 15 days On submission of Valuation Report:- 50% of payable fee. ii.The remaining 50% fees will be paid on satisfactory completion of the stated deliverables (As stated in Para 10). 9. Scope of work The responsibilities of the Valuer(s) would, inter-alia, be to undertake a valuation of Cooperative Sugar Mills. The methodology used for valuation should include but is not limited to:

1. Discounted cash flow (DCF) 2. Balance Sheet Method 3. Market multiples method/Comparable companies method 4. Market valuation of assets/Asset Valuation Method

The above methods have been explained in detail in Annexure V If the valuer in his professional opinion believes that any one or more methods of valuation may be inappropriate, he may exclude these methods. However, the valuer will have to provide a justification for not using the method. The above valuations have to be supported with well laid out assumptions, which will need to be fully justified and explained in the report and in the presentation as specified under the “Deliverables” section of these Terms of Reference. In case of market multiples method, the use of a comparable should be explained in the valuation report. If the valuer in his professional opinion believes that other methods of valuation may be appropriate, he may also include these methods in addition to those required. However, the valuer will have to provide a justification for using the method. In case of Market valuation of assets/Asset Valuation Method, valuation may be done for:

a. Plant and Machinery b. Land and Building c. Intangibles, if required d. Other assets & Liabilities.

Presentation to Registrar, As a part of terms of ToR, the valuers will be required to make a presentation to Registrar,Cane Cooperative Societies ,Uttar Pradesh,17, New Beri Road, Lucknow- 226001 Uttar Pradesh and justify the valuation and the underlying assumptions. 10. Deliverables

The deliverables for valuers includes:

The last date for submission of valuation report is four weeks from the issue of letter of appointment.

A sealed valuation report containing valuation Report of each of the Cooperative Sugar Mills /distillery in the bundle awarded to the Valuer in Letter of Appointment.

A presentation to justify the recommended valuation, if called for. Penalty for Late submission For each day of delay in submission of the valuation report a penalty of 1% of the valuation fee shall be deducted from fees payable to the valuer for each bundle. 11. Other terms and conditions

All the information/details to be supported by authentic documents duly certified by the authorized signatory.

Registrar reserves the right to negotiate the Lump-sum Fee and with the selected bidder.

Registrar reserves the right to reject any or all Bids without assigning any reason thereof as well as the right to add/delete/modify any one or more of the terms and conditions.

Registrar reserves the right to discontinue the services of the appointed Valuer(s) at any point of time on account of force-majeure or non-satisfactory performance by the Valuer(s).

The Valuer is required to comply with the guidelines issued by the Registrar. * The validity of the offer will be 90 days from the last date of submission of the bid.

*All disputes will be at Lucknow courts of law. Registrar, Cane Cooperative Societies ,Uttar Pradesh, 17, New Beri Road, Lucknow- 226001 Uttar Pradesh Ph: 0522 – 2204295 0522 – 2204163 (Fax)

ANNEXURE-1

The kisan sahkari chini mills limited,Aurai The kisan sahkari chini mills limited,Aurai has been established under U.P.Cooperative Societies Act,1965 and its first crushing season was 1971-72.The present crushing capacity of The kisan sahkari chini mills limited,Aurai is 1250 tcd.the factory has been established in Gyanpur Tehsil of Sant Ravidas Nagar District.The technical as well as financial performance of last 5 years of The kisan sahkari chini mills limited,Aurai is as under :- Sl.no

Particulars 2002-03 2003-04 2004-05 2005-06 2006-07

2007-08

Technical Performance 1. Cane Crushed

(lac qtls.) 5.37 1.73 .95 .44 .57 ---

2. Sugar Recovery(%) 7.7 7.2 6.62 7.9 7.2 --- 3. Capacity utilization

(%) 52 42 32 20 30 ---

4. Sugar Production (lac qtls)

.41 .12 .06 .03 .04 ---

Financial Performance 1. Net profit/loss

(Rs. In lacs) -927.51 -804.00 -775.17 -865.89 -899.32 -824.08

2. Cost of production ( Rs. Per Bag )

3285.87 8231.71 14468.56 25229.88 21860.24 ---

3. Accumulated Profit/loss (Rs. In lacs)

-7665.51

-8469.51

-9241.09 -10114.98

-11014.30

-11838.38

4. Networth (Rs. In lacs)

-6081.74

-6885.73

-7665.31 -8531.20 -9381.20

-10254.59

5. 8. 9.

CAPITAL EMPLOYED SALE Share Capital & Outstanding loans (Rs. In lacs)

-536.14 297.75

-424.44 258.59

-724.60 491.54

-909.21 78.27

-1129.57 53.13

-1207.54 ---

(i) Share Capital State Govt. Capital 1524.56 1524.56 1524.56 1524.56 1524.56 1524.57 Others Share Capital 45.51 45.52 45.52 45.53 45.53 45.52 Total Share Capital 1570.07 1570.08 1570.08 1570.09 1570.09 1570.09 (ii Outstanding loans a. State Govt. 2812.92 3136.27 3600.36 4429.52 5071.00 5511.71 b. Shakkar Vishesh Nidhi 1011.73 1075.12 1138.50 1201.88 1265.26 1328.64 c. Sugar Development Fund as

on 31.03.2006 27.88 29.63 31.39 37.13 39.21 27.89

10 Number of Persons Employed

a. Permanent 187 b. Seasonal 354 c. Total 541

11 Land Area(acres) 89.638

The kisan sahkari chini mills limited,Rasra The kisan sahkari chini mills limited,Rasra has been established under U.P.Cooperative Societies Act,1965 and its first crushing season was 1975-76.The present crushing capacity of The kisan sahkari chini mills limited,Rasra is 1250 tcd.The factory has been established in Ballia District.The technical as well as financial performance of last 5 years of The kisan sahkari chini mills limited,Rasra is as under :- Sl.No. Particulars 2002-03 2003-04 2004-05 2005-06 2006-07

2007-08

Technical Performance

1. Cane Crushed (lac qtls.)

9.63 7.10 6.60 9.72 11.04 9.97

2. Sugar Recovery(%)

8.5 8.01 9.02 8.19 7.43 7.78

3. Capacity utilization (%)

87 81 82 78 79 76

4. Sugar Production (lac qtls)

.82 .57 .60 .79 .82 .82

Financial Performance

1. Net profit/loss (Rs. In lacs)

-983.27 -773.24 -649.21 -813.02 -1620.00 -1631.36

2. Cost of production ( Rs. Per Bag )

2294.69 2851.62 3094.93 2951.69 3426.72 3226.72

3. Accumulated Profit/loss (Rs. In lacs)

-6512.62

-7285.87

-7935.08

-8748.10

-10368.10

-11999.46

4. Networth (Rs. In lacs)

-4946.05

-5718.85

-6320.80

-7121.11

-8739.50 -10370.20

5. 7. 8. 9.

CAPITAL EMPLOYED SALE Share Capital & Outstanding loans (Rs. In lacs)

753.66 1538.93

791.61 1539.14

1498.441586.59

1179.171598.51

1422.86 1599.63

-1077.55

1124.30

(i) Share Capital State Govt.

Capital 1458.35 1458.35 1458.35 1458.35 1458.35 1458.35

Others Share Capital

79.85 80.79 128.24 140.16 141.28 141.29

Total Share Capital

1538.93 1539.14 1586.59 1598.51 1599.63 1599.64

(ii) Outstanding loans

a. State Govt. 2380.89 3369.71 3764.04 4130.02 5185.80 5276.40 b. Shakkar Vishesh

Nidhi 1190.41 1268.85 1347.30 1426.84 1505.81 1944.17

c. Sugar Development Fund as on 31.05.2007

328.90 379.54 402.36 425.17 447.99 ---

10. Number of Persons Employed

a. Permanent 173 b. Seasonal 265 c. Total 438 11. Land Area(acres) 81.3

The kisan sahkari chini mills limited, Anoopshahar The kisan sahkari chini mills limited,Anoopshahr has been established under U.P.Cooperative Societies Act,1965 and its first crushing season was 1977-78.The present crushing capacity of The kisan sahkari chini mills limited,Anoopshahr is 2500 tcd.The factory has been established in Jahangirabad Tehsil of Bulandshahr District.The technical as well as financial performance of last 5 years of The kisan sahkari chini mills limited,Anoopshahr is as under :- Sl.No.

Particulars 2002-03

2003-04

2004-05

2005-06 2006-07

2007-08

Technical Performance

1. Cane Crushed (lac qtls.)

41.14 33.50 31.14 27.21 45.03 31.42

2. Sugar Recovery(%) 8.97 9.16 9.40 8.50 8.10 8.74 3. Capacity utilization

(%) 96.08 101.09 98.65 100.20 91.29 93

4. Sugar Production (lac qtls)

3.69 3.09 2.93 2.31 3.65 2.90

Financial Performance

1. Net profit/loss (Rs. In lacs)

-1934.0

8

-638.59 372.92 -817.99 -1802.97 -2331.01

2. Cost of production ( Rs. Per Bag )

1487.57

1600.99

1640.37

2092.85 2014.01 2076.49

3. Accumulated Profit/loss (Rs. In lacs)

-4619.4

9

-5258.0

8

4886.59

-5704.58

-7507.55 -9838.56

4. Networth (Rs. In lacs)

-3015.9

4

-3651.3

2

-3275.4

7

-4092.30

-5899.12 -8214.58

5. 7. 8. 9.

CAPITAL EMPLOYED SALE Share Capital & Outstanding loans (Rs. In lacs)

3310.65 3599.66

5117.35

3750.99

5373.23

8580.35

3289.24

4330.08

2209.73

3599.66

2644.95

5086.70

(i) Share Capital State Govt. Capital 775.02 775.02 775.02 775.02 775.02 775.02 Others Share Capital 145.66 148.80 152.93 154.02 155.04 165.04 Total Share Capital 920.68 923.82 927.95 929.04 930.06 940.06 (ii Outstanding loans a. State Govt. 810.21 2665.0

2 3090.6

2 3525.08 3959.53 5659.22

b. Shakkar Vishesh Nidhi 564.78 596.93 629.08 661.24 693.38 725.54 c. Sugar Development

Fund as on 28.02.2007 467.96 551.57 581.48 611.39 545.35 515.44

10.

Number of Persons Employed

a. Permanent 272 b. Seasonal 520 c. Total 792 11 Land Area(acres) 97.6

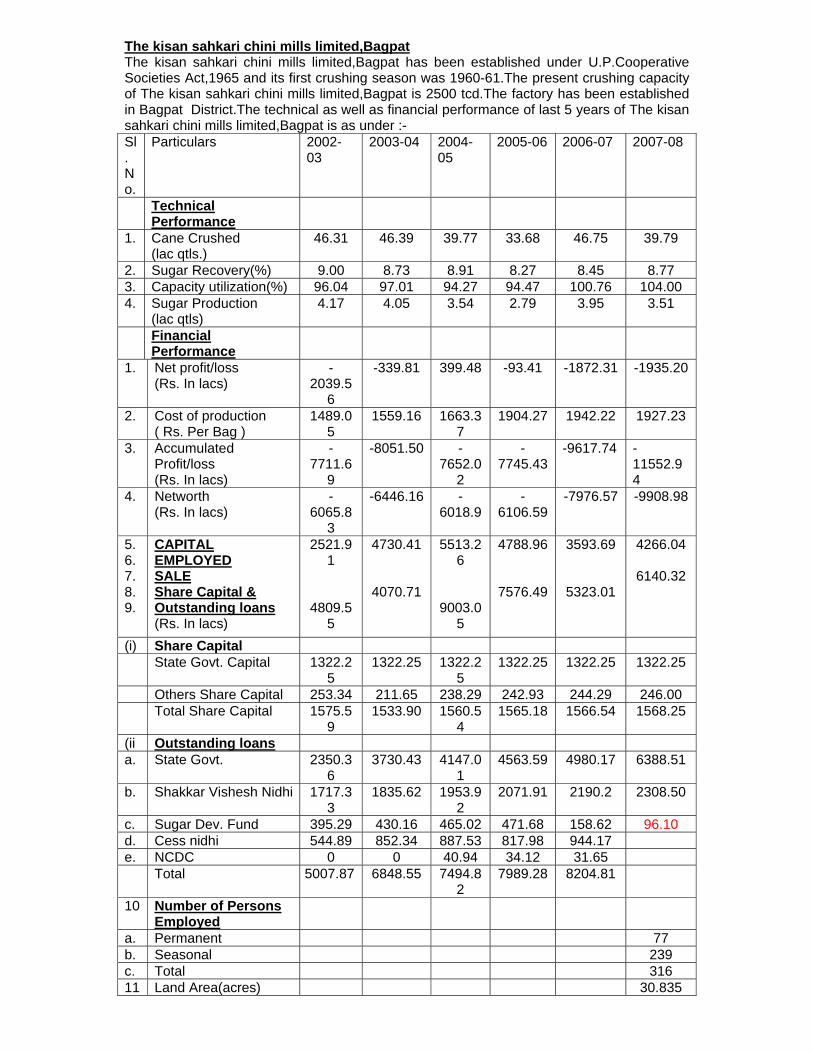

The kisan sahkari chini mills limited,Bagpat The kisan sahkari chini mills limited,Bagpat has been established under U.P.Cooperative Societies Act,1965 and its first crushing season was 1960-61.The present crushing capacity of The kisan sahkari chini mills limited,Bagpat is 2500 tcd.The factory has been established in Bagpat District.The technical as well as financial performance of last 5 years of The kisan sahkari chini mills limited,Bagpat is as under :- Sl.No.

Particulars 2002-03

2003-04 2004-05

2005-06 2006-07

2007-08

Technical Performance

1. Cane Crushed (lac qtls.)

46.31 46.39 39.77 33.68 46.75 39.79

2. Sugar Recovery(%) 9.00 8.73 8.91 8.27 8.45 8.77 3. Capacity utilization(%) 96.04 97.01 94.27 94.47 100.76 104.00 4. Sugar Production

(lac qtls) 4.17 4.05 3.54 2.79 3.95 3.51

Financial Performance

1. Net profit/loss (Rs. In lacs)

-2039.5

6

-339.81 399.48 -93.41 -1872.31 -1935.20

2. Cost of production ( Rs. Per Bag )

1489.05

1559.16 1663.37

1904.27 1942.22 1927.23

3. Accumulated Profit/loss (Rs. In lacs)

-7711.6

9

-8051.50 -7652.0

2

-7745.43

-9617.74 -11552.94

4. Networth (Rs. In lacs)

-6065.8

3

-6446.16 -6018.9

-6106.59

-7976.57 -9908.98

5. 6. 7. 8. 9.

CAPITAL EMPLOYED SALE Share Capital & Outstanding loans (Rs. In lacs)

2521.91

4809.55

4730.41

4070.71

5513.26

9003.05

4788.96

7576.49

3593.69

5323.01

4266.04

6140.32

(i) Share Capital State Govt. Capital 1322.2

5 1322.25 1322.2

5 1322.25 1322.25 1322.25

Others Share Capital 253.34 211.65 238.29 242.93 244.29 246.00 Total Share Capital 1575.5

9 1533.90 1560.5

4 1565.18 1566.54 1568.25

(ii Outstanding loans a. State Govt. 2350.3

6 3730.43 4147.0

1 4563.59 4980.17 6388.51

b. Shakkar Vishesh Nidhi 1717.33

1835.62 1953.92

2071.91 2190.2 2308.50

c. Sugar Dev. Fund 395.29 430.16 465.02 471.68 158.62 96.10 d. Cess nidhi 544.89 852.34 887.53 817.98 944.17 e. NCDC 0 0 40.94 34.12 31.65 Total 5007.87 6848.55 7494.8

2 7989.28 8204.81

10 Number of Persons Employed

a. Permanent 77 b. Seasonal 239 c. Total 316 11 Land Area(acres) 30.835

The kisan sahkari chini mills limited,Morna The kisan sahkari chini mills limited,Morna has been established under U.P.Cooperative Societies Act,1965 and its first crushing season was 1984-85.The present crushing capacity of The kisan sahkari chini mills limited,Morna is 2500 tcd.The factory has been established in Muzaffar nagar District.The technical as well as financial performance of last 5 years of The kisan sahkari chini mills limited,Morna is as under :- Sl.No.

Particulars 2002-03 2003-04

2004-05 2005-06

2006-07

2007-08

Technical Performance

1. Cane Crushed (lac qtls.)

44.93 37.86 39.05 23.70 48.27 40.19

2. Sugar Recovery(%) 9.36 10.06 9.90 8.68 9.10 9.30 3. Capacity utilization

(%) 99 98 100 87 97 100

4. Sugar Production (lac qtls)

4.18 3.81 3.88 2.06 4.39 3.77

Financial Performance

1. Net profit/loss (Rs. In lacs)

-2151.2

7

332.48 1210.42

-67.16 -576.18 -785.77

2. Cost of production ( Rs. Per Bag )

1414.46

1356.97 1499.98

1824.94 1626.91 1648.82

3. Accumulated Profit/loss (Rs. In lacs)

-3713.7

9

-3381.31 -2170.8

8

-2238.04

-2814.22 -3599.99

4. Networth (Rs. In lacs)

-1405.4

5

-991.99 240.28 173.17 -401.18 -1186.56

5. 6. 7. 8. 9.

CAPITAL EMPLOYED SALE Share Capital & Outstanding loans (Rs. In lacs)

5295.65

4141.00

6834.87 4415.30

6565.44

9923.60

3188.338859.11

3983.83 3896.19

6293.55 6570.66

(i) Share Capital State Govt. Capital 1283.1

8 1283.18 1283.1

8 1283.18 1283.18 1283.18

Others Share Capital 61.79 62.42 62.42 62.47 64.20 64.57 Total Share Capital 1344.9

7 1345.60 1345.6

0 1345.65 1347.38 1347.75

(ii Outstanding loans a. State Govt. 64.97 797.68 833.84 1167.60 271.05 2458.52 b. Shakkar Vishesh Nidhi 279.32 293.14 306.97 318.96 332.77 346.59 c. Sugar Development

Fund as on 28.02.2007 264.41 320.32 431.90 373.65 289.17 289.93

10 Number of Persons Employed

a. Permanent 258 b. Seasonal 405 c. Total 663 11 Land Area(acres) 97.48

The kisan sahkari chini mills limited,Ramala The kisan sahkari chini mills limited,Ramala has been established under U.P.Cooperative Societies Act,1965 and its first crushing season was 1978-79.The present crushing capacity of The kisan sahkari chini mills limited,Ramala is 2750 tcd.The factory has been established in Bagpat District.The technical as well as financial performance of last 5 years of The kisan sahkari chini mills limited,Ramala is as under :- Sl.No.

Particulars 2002-03

2003-04 2004-05

2005-06

2006-07

2007-08

Technical Performance

1. Cane Crushed (lac qtls.)

52.05 50.93 49.56 29.65 52.55 52.44

2. Sugar Recovery(%) 9.32 9.46 9.96 8.93 9.38 8.91 3. Capacity utilization

(%) 90.91 92.14 96.63 79.57 96.46 91.00

4. Sugar Production (lac qtls)

4.85 4.82 4.97 2.65 4.93 4.72

Financial Performance

1. Net profit/loss (Rs. In lacs)

-869.22

-199.52 1307.99

850.50 294.70 -498.92

2. Cost of production (Rs.per Bag)

1439.45

1429.06 1542.07

1886.93

1756.61 1533.65

3. Accumulated Profit/loss (Rs. In lacs)

-1549.2

1

-1722.00

-432.90

278.12 520.89 21.97

4. Networth (Rs. In lacs)

935.56 765.72 2056.46

2771.50

3016.68 2523.53

5. 6. 7. 8. 9.

CAPITAL EMPLOYED SALE Share Capital & Outstanding loans (Rs. In lacs)

5676.82

4521.73

7383.39 5111.28

8544.63

10601.47

4705.34

11782.45

6459.08 4954.10

8575.99

7295.94

(i) Share Capital State Govt. Capital 862.25 862.25 862.25 862.25 862.25 862.25 Others Share Capital 163.97 166.69 168.27 172.09 174.38 179.89 Total Share Capital 1026.2

2 1028.94 1030.5

2 1034.3

4 1036.63 1042.14

(ii Outstanding loans a. State Govt. ---- 175.00 175.00 175.00 - 55.79 b. Shakkar Vishesh

Nidhi 332.40 367.64 385.80 378.13 393.37 408.61

c. Sugar Development Fund as on 31.05.2007

---- ---- ---- ---- ---- 90.53

10 Number of Persons Employed

a. Permanent 212 b. Seasonal 421 c. Total 633 11 Land Area(acres) 81.64

The kisan sahkari chini mills limited,Sarsawa kisan sahkari chini mills limited,Sarsawa has been established under U.P.Cooperative Societies Act,1965 and its first crushing season was 1961-62.The present crushing capacity of The kisan sahkari chini mills limited,Sarsawa is 2750 tcd.the factory has been established in Saharanpur District.The technical as well as financial performance of last 5 years of The kisan sahkari chini mills limited,Sarsawa is as under :- Sl.No

Particulars 2002-03

2003-04 2004-05

2005-06

2006-07

2007-08

Technical Performance

1. Cane Crushed (lac qtls.)

45.19 41.52 38.34 41.84 49.48 37.87

2. Sugar Recovery(%) 9.50 9.84 9.95 9.42 9.70 9.32 3. Capacity utilization

(%) 97.54 96.30 95.52 96.86 92.72 98

4. Sugar Production (lac qtls)

4.29 4.08 3.81 3.94 4.79 3.55

Financial Performance

1. Net profit/loss (Rs. In lacs)

-1324.4

8

-113.70 944.72 539.37 -25.34 -558.88

2. Cost of production ( Rs. Per Bag )

1412.98

1379.29 1509.85

1755.66

1654.87 1583.89

3. Accumulated Profit/loss (Rs. In lacs)

-1650.0

3

-1763.73

-819.01

-279.64 -304.98 -863.86

4. Networth (Rs. In lacs)

-434.27

-547.14 421.17 940.58 916.12 358.20

5. 6. 7. 8. 9.

CAPITAL EMPLOYED SALE Share Capital & Outstanding loans (Rs. In lacs)

5509.18

4498.07

6467.70 4993.84

7007.42

9727.78

6069.76

8567.49

5561.62 7486.50

7237.95

7287.96

(i) Share Capital State Govt. Capital 397.24 397.24 397.24 397.24 397.24 397.24 Others Share

Capital 206.08 206.20 206.45 208.00 208.00 208.02

Total Share Capital 603.32 603.44 603.69 605.24 605.24 605.26 (ii) Outstanding loans

a. State Govt. 0.0 785.00 926.30 1067.60

1208.90 1663.17

b. Shakkar Vishesh Nidhi

---- ---- ---- ---- ---- 0.00

c. Sugar Development Fund as on 31.05.2007

---- ---- ---- ---- ---- ---

10 Number of Persons Employed

a. Permanent 115 b. Seasonal 354 c. Total 469 11 Land Area(acres) 22.476

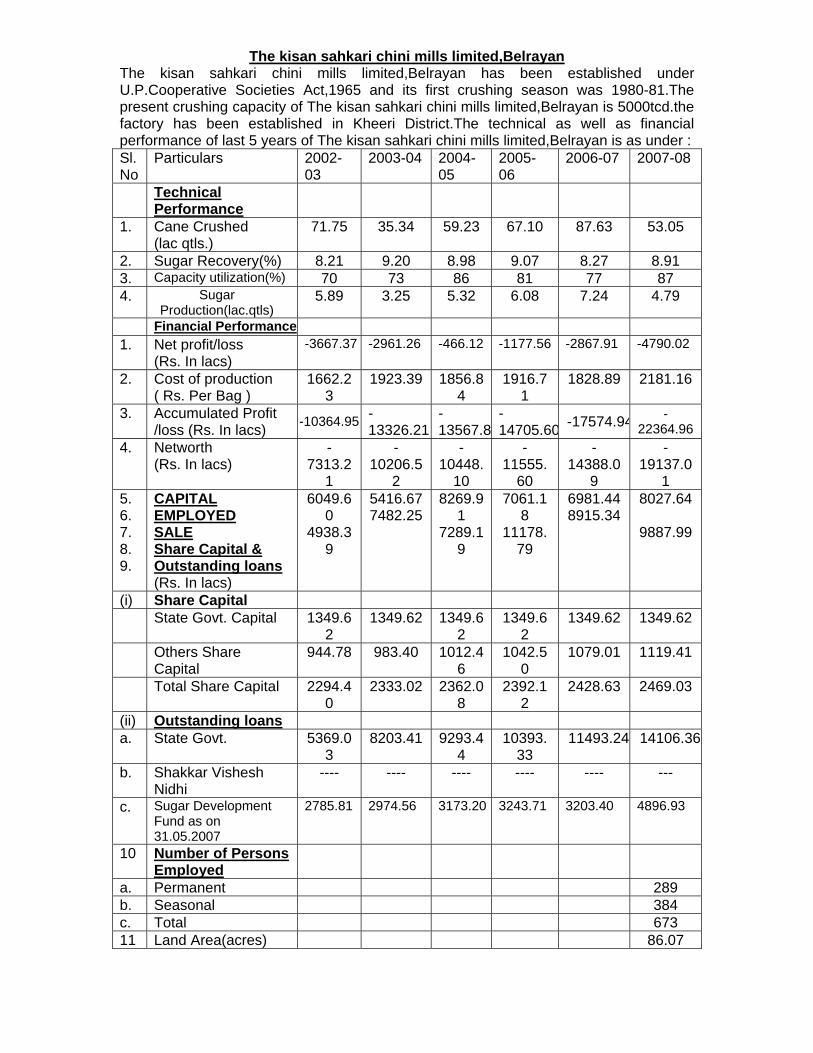

The kisan sahkari chini mills limited,Belrayan The kisan sahkari chini mills limited,Belrayan has been established under U.P.Cooperative Societies Act,1965 and its first crushing season was 1980-81.The present crushing capacity of The kisan sahkari chini mills limited,Belrayan is 5000tcd.the factory has been established in Kheeri District.The technical as well as financial performance of last 5 years of The kisan sahkari chini mills limited,Belrayan is as under : Sl.No

Particulars 2002-03

2003-04 2004-05

2005-06

2006-07

2007-08

Technical Performance

1. Cane Crushed (lac qtls.)

71.75 35.34 59.23 67.10 87.63 53.05

2. Sugar Recovery(%) 8.21 9.20 8.98 9.07 8.27 8.91 3. Capacity utilization(%) 70 73 86 81 77 87 4. Sugar

Production(lac.qtls) 5.89 3.25 5.32 6.08 7.24 4.79

Financial Performance 1. Net profit/loss

(Rs. In lacs) -3667.37 -2961.26 -466.12 -1177.56 -2867.91 -4790.02

2. Cost of production ( Rs. Per Bag )

1662.23

1923.39 1856.84

1916.71

1828.89 2181.16

3. Accumulated Profit /loss (Rs. In lacs) -10364.95 -

13326.21-13567.8

-14705.60 -17574.94 -

22364.96 4. Networth

(Rs. In lacs) -

7313.21

-10206.5

2

-10448.

10

-11555.

60

-14388.0

9

-19137.0

1 5. 6. 7. 8. 9.

CAPITAL EMPLOYED SALE Share Capital & Outstanding loans (Rs. In lacs)

6049.60

4938.39

5416.67 7482.25

8269.91

7289.19

7061.18

11178.79

6981.44 8915.34

8027.64

9887.99

(i) Share Capital State Govt. Capital 1349.6

2 1349.62 1349.6

2 1349.6

2 1349.62 1349.62

Others Share Capital

944.78 983.40 1012.46

1042.50

1079.01 1119.41

Total Share Capital 2294.40

2333.02 2362.08

2392.12

2428.63 2469.03

(ii) Outstanding loans a. State Govt. 5369.0

3 8203.41 9293.4

4 10393.

33 11493.24 14106.36

b. Shakkar Vishesh Nidhi

---- ---- ---- ---- ---- ---

c. Sugar Development Fund as on 31.05.2007

2785.81 2974.56 3173.20 3243.71 3203.40 4896.93

10 Number of Persons Employed

a. Permanent 289 b. Seasonal 384 c. Total 673 11 Land Area(acres) 86.07

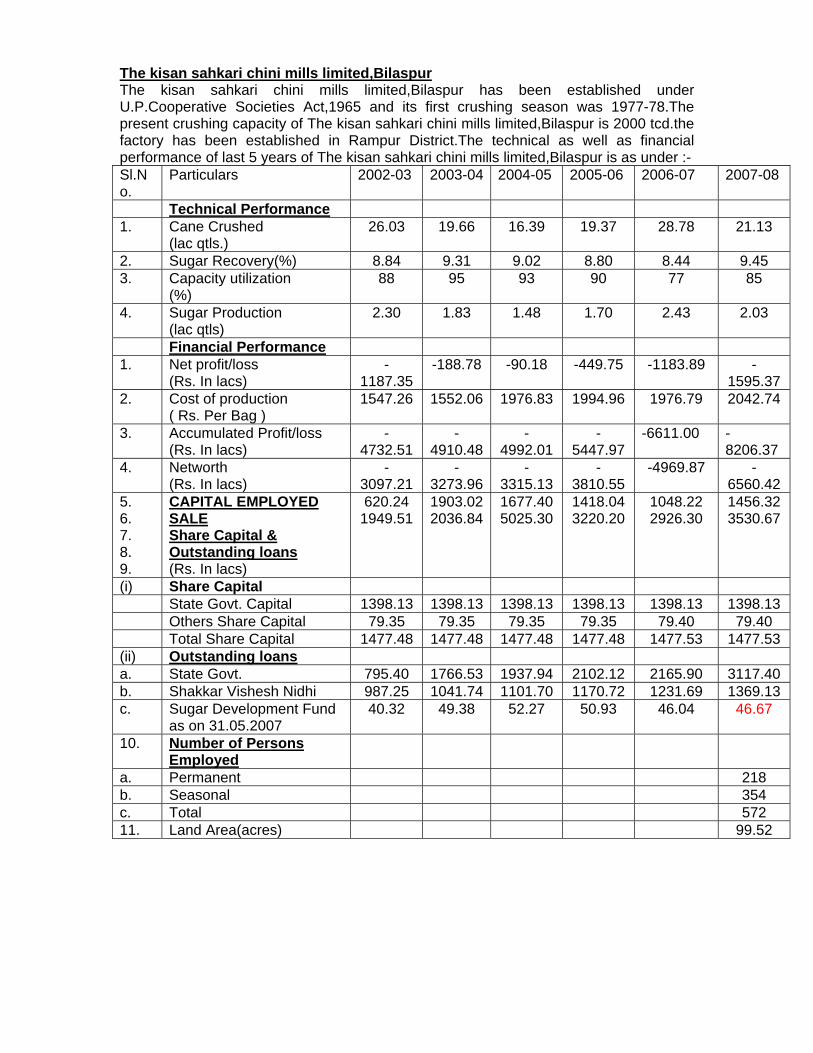

The kisan sahkari chini mills limited,Bilaspur The kisan sahkari chini mills limited,Bilaspur has been established under U.P.Cooperative Societies Act,1965 and its first crushing season was 1977-78.The present crushing capacity of The kisan sahkari chini mills limited,Bilaspur is 2000 tcd.the factory has been established in Rampur District.The technical as well as financial performance of last 5 years of The kisan sahkari chini mills limited,Bilaspur is as under :- Sl.No.

Particulars 2002-03 2003-04 2004-05 2005-06 2006-07

2007-08

Technical Performance 1. Cane Crushed

(lac qtls.) 26.03 19.66 16.39 19.37 28.78 21.13

2. Sugar Recovery(%) 8.84 9.31 9.02 8.80 8.44 9.45 3. Capacity utilization

(%) 88 95 93 90 77 85

4. Sugar Production (lac qtls)

2.30 1.83 1.48 1.70 2.43 2.03

Financial Performance 1. Net profit/loss

(Rs. In lacs) -

1187.35 -188.78 -90.18 -449.75 -1183.89 -

1595.37 2. Cost of production

( Rs. Per Bag ) 1547.26 1552.06 1976.83 1994.96 1976.79 2042.74

3. Accumulated Profit/loss (Rs. In lacs)

-4732.51

-4910.48

-4992.01

-5447.97

-6611.00 -8206.37

4. Networth (Rs. In lacs)

-3097.21

-3273.96

-3315.13

-3810.55

-4969.87 -6560.42

5. 6. 7. 8. 9.

CAPITAL EMPLOYED SALE Share Capital & Outstanding loans (Rs. In lacs)

620.24 1949.51

1903.022036.84

1677.40 5025.30

1418.04 3220.20

1048.22 2926.30

1456.32 3530.67

(i) Share Capital State Govt. Capital 1398.13 1398.13 1398.13 1398.13 1398.13 1398.13 Others Share Capital 79.35 79.35 79.35 79.35 79.40 79.40 Total Share Capital 1477.48 1477.48 1477.48 1477.48 1477.53 1477.53 (ii) Outstanding loans a. State Govt. 795.40 1766.53 1937.94 2102.12 2165.90 3117.40 b. Shakkar Vishesh Nidhi 987.25 1041.74 1101.70 1170.72 1231.69 1369.13 c. Sugar Development Fund

as on 31.05.2007 40.32 49.38 52.27 50.93 46.04 46.67

10. Number of Persons Employed

a. Permanent 218 b. Seasonal 354 c. Total 572 11. Land Area(acres) 99.52

The kisan sahkari chini mills limited,Bisalpur The kisan sahkari chini mills limited,Bisalpur has been established under U.P.Cooperative Societies Act,1965 and its first crushing season was 1977-78.The present crushing capacity of The kisan sahkari chini mills limited,Bisalpur is 2750 tcd.the factory has been established in Pilibhit District.The technical as well as financial performance of last 5 years of The kisan sahkari chini mills limited,Bisalpur is as under :- Sl.No.

Particulars 2002-03 2003-04 2004-05 2005-06 2006-07

2007-08

Technical Performance 1. Cane Crushed

(lac qtls.) 38.28 22.95 26.10 29.40 39.78 25.37

2. Sugar Recovery(%) 8.51 8.77 8.82 8.46 8.37 8.91 3. Capacity utilization

(%) 78.51 79.71 78.57 80.61

74.77 80

4. Sugar Production (lac qtls)

3.26 2.01 2.30 2.49 3.33 2.31

Financial Performance 1. Net profit/loss

(Rs. In lacs) -

1774.02 -672.78 246.98 -756.33 -1813.78 -1760.27

2. Cost of production ( Rs. Per Bag )

1592.59 1602.17 1808.82 2019.12 1968.53 2016.72

3. Accumulated Profit/loss (Rs. In lacs)

-6006.89

-6679.67 -6432.70

-7189.03 -9002.82 -10763.09

4. Networth (Rs. In lacs)

-4736.40

-5409.18 -5139.70

-5918.03 -7730.96 -9465.54

5. 6. 7. 8. 9.

CAPITAL EMPLOYED SALE Share Capital & Outstanding loans (Rs. In lacs)

2535.34 3084.22

3543.14 3461.52

4918.704902.70

4289.51 5251.36

3448.73 4481.88

3801.16 4587.64

(i) Share Capital State Govt. Capital 731.07 731.07 731.07 731.07 731.07 731.07 Others Share Capital 175.25 175.25 175.26 175.77 175.77 198.49 Total Share Capital 906.32 906.32 906.33 906.84 906.84 929.56 (ii) Outstanding loans a. State Govt. 1794.93 3115.81 3555.73 3995.65 4435.57 4905.49 b. Shakkar Vishesh Nidhi 1421.86 1518.12 1615.39 1712.07 1808.75 1905.43 c. Sugar Development

Fund 535.89 564.07 592.25 599.89 582.66 556.12

10. Number of Persons Employed

a. Permanent 206 b. Seasonal 357 c. Total 563 11. Land Area(acres) 92.02

The kisan sahkari chini mills limited,Badaun The kisan sahkari chini mills limited,Badaun has been established under U.P.Cooperative Societies Act,1965 and its first crushing season was 1977-78.The present crushing capacity of The kisan sahkari chini mills limited,Badaun is 1250 tcd.the factory has been established in Badaun District.The technical as well as financial performance of last 5 years of The kisan sahkari chini mills limited,Badaun is as under :- Sl.No.

Particulars 2002-03

2003-04 2004-05

2005-06

2006-07

2007-08

Technical Performance

1. Cane Crushed (lac qtls.)

14.30 15.44 11.63 15.15 16.37 12.50

2. Sugar Recovery(%) 8.59 8.69 8.58 8.34 8.65 8.64 3. Capacity utilization

(%) 93.41 91.54 98.36 93.96 93.04 94

4. Sugar Production (lac qtls)

1.27 1.40 1.03 1.27 1.43 1.11

Financial Performance

1. Net profit/loss (Rs. In lacs)

-1270.31 -840.21 -494.82 -1221.04 -1473.49 -2037.15

3. Cost of production ( Rs. Per Bag )

1968.58

2035.97 2518.34

2413.32

2495.45 2762.07

3. Accumulated Profit/loss (Rs. In lacs)

-5893.1

0

-6734.31

-7242.5

1

-8463.5

5

-9937.04

-11974.19

4. Networth (Rs. In lacs)

-4290.9

2

-5132.13

-5640.3

3

-6861.3

5

-8334.83

-10371.9

8 5. 6. 7. 8. 9.

Capital Employed SALE Share Capital & Outstanding loans (Rs. In lacs)

467.33 1295.3

9

1254.59 1264.69

688.833173.5

0

513.23 2426.6

1

-16.26 2310.39

-44.64 2316.11

(i) Share Capital State Govt. Capital 1465.2

8 1465.28 1465.2

8 1465.2

8 1465.28 1465.28

Others Share Capital 83.44 83.44 83.44 83.46 83.46 83.47 Total Share Capital 1548.7

2 1548.72 1548.7

2 1548.7

4 1548.74 1548.75

(ii) Outstanding loans a. State Govt. 1997.93 3198.23 3516.5

4 4347.47 4801.54 5902.46

b. Shakkar Vishesh Nidhi 700.92 727.28 759.55 818.23 852.47 954.61 c. Sugar Development

Fund as on 31.05.2007

---- ---- ---- ---- ---

10 Number of Persons Employed

a. Permanent 274 b. Seasonal 447 c. Total 721 11 Land Area(acres) 99.51

The kisan sahkari chini mills limited,Gajraula The kisan sahkari chini mills limited,Gajraula has been established under U.P.Cooperative Societies Act,1965 and its first crushing season was 1971-72.The present crushing capacity of The kisan sahkari chini mills limited,Gajraula is 2500 tcd.the factory has been established in hasanpur Tehsil of Jyotibaphuley Nagar District.The technical as well as financial performance of last 5 years of The kisan sahkari chini mills limited,Gajraula is as under :- Sl.No.

Particulars 2002-03 2003-04 2004-05 2005-06

2006-07

2007-08

Technical Performance 1. Cane Crushed

(lac qtls.) 29.21 29.16 30.75 27.62 42.97 30.07

2. Sugar Recovery(%) 9.22 9.34 9.13 8.76 8.80 9.15 3. Capacity utilization

(%) 83 94 94 93 95 92

4. Sugar Production (lac qtls)

2.69 2.72 2.81 2.42 3.78 2.81

Financial Performance 1. Net profit/loss

(Rs. In lacs) -

1478.46 -111.74 364.67 -

176.09 -

1190.29 -1680.89

2. Cost of production ( Rs. Per Bag )

1417.31 1398.50 1560.08 1781.97

1738.81 1884.98

3. Accumulated Profit/loss (Rs. In lacs)

-5970.29

-6082.03 -5717.35

-5893.4

4

-7083.73

-8764.62

4. Networth (Rs. In lacs)

-3994.41

-4103.71 -3736.29

-3896.6

9

-5072.74

-6747.42

5. 6. 7. 8. 9.

CAPITAL EMPLOYED SALE Share Capital & Outstanding loans (Rs. In lacs)

2271.48 2592.85

3487.04 2934.58

4999.646796.60

4348.32

6003.22

3572.23 5248.83

4063.81 5294.60

(i) Share Capital State Govt. Capital 1544.29 1544.29 1544.29 1544.2

9 1544.29 1544.29

Others Share Capital 144.64 146.82 149.28 164.05 177.48 182.98 Total Share Capital 1688.93 1691.11 1693.57 1708.3

4 1721.77 1727.27

(ii) Outstanding loans a. State Govt. 1716.61 2580.60 2956.45 3201.8

6 3231.35 4214.79

b. Shakkar Vishesh Nidhi 688.66 731.29 772.83 814.40 855.95 897.49 c. Sugar Development Fund 586.31 714.35 894.58 971.07 1022.90 1050.02 10 Number of Persons

Employed

a. Permanent 262 b. Seasonal 525 c. Total 787 11 Land Area(acres) 136.8

The kisan sahkari chini mills limited,Kaimganj The kisan sahkari chini mills limited,Kaimganj has been established under U.P.Cooperative Societies Act,1965 and its first crushing season was 1975-76.The present crushing capacity of The kisan sahkari chini mills limited,Kaimganj is 1250 tcd.the factory has been established in Farrukhabad District.The technical as well as financial performance of last 5 years of The kisan sahkari chini mills limited,Kaimganj is as under :- Sl.No.

Particulars 2002-03 2003-04 2004-05 2005-06 2006-07

2007-08

Technical Performance

1. Cane Crushed (lac qtls.)

13.66 11.58 12.61 17.34 24.77 15.54

2. Sugar Recovery(%) 8.93 8.40 9.22 8.71 8.57 9.02 3. Capacity utilization

(%) 90.65 90.05 98.25 100.01 101.50 102.00

4. Sugar Production (lac qtls)

1.22 0.97 1.16 1.51 2.12 1.42

Financial Performance

1. Net profit/loss (Rs. In lacs)

-976.89

-688.37 -11.97 -712.28 -1296.00

-1083.73

2. Cost of production ( Rs. Per Bag )

1709.00

2238.97 2063.39

2062.26

2102.77 2037.32

3. Accumulated Profit/loss (Rs. In lacs)

-6317.3

4

-7005.71

-7017.1

7

-7729.9

6

-9025.96

--10109.69

4. Networth (Rs. In lacs)

-4597.7

8

-5268.89

-5258.8

0

-5952.9

0

-7232.31

-8315.56

5. 6. 7. 8. 9.

CAPITAL EMPLOYED SALE Share Capital & Outstanding loans (Rs. In lacs)

879.36 1467.87

1644.50 1598.03

2344.282940.79

2297.462944.79

1977.68 3255.13

1779.77

3107.08

(i) Share Capital State Govt. Capital 1376.3

9 1376.39 1376.3

9 1376.3

9 1376.39 1376.39

Others Share Capital

190.00 207.14 229.02 246.76 262.83 262.83

Total Share Capital 1566.39

1583.53 1605.41

1623.15

1639.22 1639.22

(ii) Outstanding loans a. State Govt. 1773.24 2986.74 3165.48 3898.39 4281.28 4681.69 b. Shakkar Vishesh Nidhi 1019.88 1088.24 1156.60 1224.96 1293.32 1361.68

c. Sugar Development Fund as on 28.02.2007

33.79

24.15 20.71 17.02 9.55 ---

10 Number of Persons Employed

a. Permanent 183 b. Seasonal 197 c. Total 580 11 Land Area(acres) 83.36

The kisan sahkari chini mills limited,Powayan The kisan sahkari chini mills limited,Powayan has been established under U.P.Cooperative Societies Act,1965 and its first crushing season was 1987-88.The present crushing capacity of The kisan sahkari chini mills limited,Powayan is 2125 tcd.the factory has been established in Shahjahanpur District.The technical as well as financial performance of last 5 years of The kisan sahkari chini mills limited,Powayan is as under :- Sl.No

Particulars 2002-03

2003-04 2004-05

2005-06

2006-07

2007-08

Technical Performance

1. Cane Crushed (lac qtls.)

10.53 .19 9.18 12.26 21.66 10.39

2. Sugar Recovery(%) 7.50 7.55 7.90 7.80 7.50 8.84 3. Capacity utilization(%) 60 34 61 74 64 72 4. Sugar Production

(lac qtls) .79 .01 .73 .96 1.62 .96

Financial Performance

1. Net profit/loss (Rs. In lacs)

-1571.4

7

-1011.07

-718.87

-1229.9

5

-1815.01

-2196.03

2. Cost of production ( Rs. Per Bag )

2679.19

71020.91

3090.89

2931.57

2718.11 3259.58

3. Accumulated Profit/loss (Rs. In lacs)

-7732.5

4

-8754.95

-9480.1

8

-10595.

66

-12144.71

-14340.74

4. Networth (Rs. In lacs)

-4974.09

-5985.79 -6699.88

-7815.12

-9660.68 -11856.71

5. 6. 7. 8. 9.

CAPITAL EMPLOYED SALE Share Capital & Outstanding loans (Rs. In lacs)

2017.05

1041.43

1731.66 662.43

2260.78

927.73

2598.95

1294.71

2126.38 1932.19

2200.64

1493.28

(i) Share Capital State Govt. Capital 1801.0

2 1801.02 1801.0

2 1801.0

2 1504.51 1504.51

Others Share Capital

217.28 234.44 245.59 245.82 245.82 245.82

Total Share Capital 2018.30

2035.46 2046.61

2046.84

1750.33 1750.33

(ii) Outstanding loans a. State Govt. 2125.4

8 4505.27 5462.7

1 5861.3

8 7443.24 7648.03

b. Shakkar Vishesh Nidhi

375.23 417.13 452.59 490.38 526.54 653.02

c. Sugar Development Fund as on 31.05.2007

718.07 779.19 912.43 945.16 968.17 985.40

10 Number of Persons Employed

a. Permanent 142 b. Seasonal 418 c. Total 560 11 Land Area(acres) 106

The kisan sahkari chini mills limited,Puranpur

The kisan sahkari chini mills limited,Puranpur has been established under U.P.Cooperative Societies Act,1965 and its first crushing season was 1971-72.The present crushing capacity of The kisan sahkari chini mills limited, Puranpur is 2500 tcd.the factory has been established in Pilibhit District.The technical as well as financial performance of last 5 years of The kisan sahkari chini mills limited, Puranpur is as under

Sl.No Particulars 2002-03 2003-04 2004-05 2005-06 2006-07

2007-08

Technical Performance 1. Cane Crushed

(lac qtls.) 34.29 16.98 26.06 28.64 35.54 19.69

2. Sugar Recovery(%) 9.11 9.73 9.56 9.20 8.62 8.74 3. Capacity utilization

(%) 78.05 81.23 83.03 86.27 71.23 77.00

4. Sugar Production (lac qtls)

3.12 1.65 2.49 2.64 3.06 1.75

Financial Performance 1. Net profit/loss

(Rs. In lacs) -

1591.78 -871.71 521.17 -745.88 -1916.46 -2039.99

2. Cost of production ( Rs. Per Bag )

1445.43 1591.65 1689.38 1939.95 2007.90 2378.99

3. Accumulated Profit/loss (Rs. In lacs)

-7081.48

-7955.56 -7438.74

-8186.02 -10104.62 -12144.61

4. Networth (Rs. In lacs)

5416.24 -6290.32 -5763.72

-6510.99 -8429.59

-10469.57

5. 6. 7. 8. 9.

CAPITAL EMPLOYED SALE Share Capital & Outstanding loans (Rs. In lacs)

2547.28 2569.96

3715.67 2871.39

4763.725183.04

3630.27 5582.01

3374.82 4036.29

3307.24 3357.76

(i) Share Capital State Govt. Capital 851.08 851.08 851.08 851.08 851.08 851.08 Others Share Capital 115.56 115.56

115.56 115.57 115.57 115.58

Total Share Capital 966.64 966.64 966.64 966.65 966.65 966.66 (ii) Outstanding loans a. State Govt. 2732.50 4095.85 4453.73 5043.00 6194.95 6787.78 b. Shakkar Vishesh Nidhi 527.06 566.45 610.31 654.80 699.28 748.80 c. Sugar Development

Fund ---- ---- ---- ---- 630.53 621.60

10 Number of Persons Employed

a. Permanent 197 b. Seasonal 381 c. Total 578 11 Land Area(acres) 91.68

The kisan sahkari chini mills limited Sampurnanagar The kisan sahkari chini mills limited,Sampurnanagar has been established under U.P.Cooperative Societies Act,1965 and its first crushing season was 1985*86.The present crushing capacity of The kisan sahkari chini mills limited, Sampurnanagar is 5000 tcd.the factory has been established in Kheeri District.The technical as well as financial performance of last 5 years of The kisan sahkari chini mills limited, Sampurnanagar is as under :- Sl.No.

Particulars 2002-03

2003-04 2004-05

2005-06

2006-07

2007-08

Technical Performance

1. Cane Crushed (lac qtls.)

61.52 38.70 49.68 57.61 81.88 48.33

2. Sugar Recovery(%) 8.00 9.15 8.70 8.04 8.22 8.54 3. Capacity utilization

(%) 73 82 84 81 81 79

4. Sugar Production (lac qtls)

4.92 3.54 4.32 4.62 6.73 4.19

Financial Performance

1. Net profit/loss (Rs. In lacs)

-3357.7

3

-1908.97

-498.11

-1551.0

0

-3023.71

-4743.92

2. Cost of production ( Rs. Per Bag )

1588.61

1615.56 1570.36

1772.11

1636.00 2209.03

3. Accumulated Profit/loss (Rs. In lacs)

-7783.9

1

-9692.88

-10190.

99

-11741.

99

-14765.70

-19509.62

4. Networth (Rs. In lacs)

-4920.5

4

-6824.72

-7318.9

7

-8864.7

9

-11883.1

1

-16620.4

6 5. 6. 7. 8. 9.

CAPITAL EMPLOYED SALE Share Capital & Outstanding loans (Rs. In lacs)

6210.83 -

5038.77

6685.07 -

6412.49

9571.58

7987.38

8743.11

10304.62

7202.31 9262.59

5017.44

7888.70

(i) Share Capital State Govt. Capital 760.00 760.00 760.00 760.00 760.00 760.00 Others Share

Capital 100.02 100.02 100.03 100.46 100.46 100.46

Total Share Capital 860.02 860.02 860.03 860.46 860.46 860.46 (ii) Outstanding loans a. State Govt. 860.00 3342.10 3917.70 4493.30 5068.90 6484.50 b. Shakkar Vishesh Nidhi ---- ---- ---- ---- 0.00 c. Sugar Development

Fund as on 31.05.2007

2064.91

2077.51 2092.73

2102.67

2230.06 4972.98

10 Number of Persons Employed

a. Permanent 198 b. Seasonal 328 c. Total 526 11 Land Area(acres) 95.14

The kisan sahkari chini mills limited,Satha

The kisan sahkari chini mills limited,Satha has been established under U.P.Cooperative Societies Act,1965 and its first crushing season was 1976-77.The present crushing capacity of The kisan sahkari chini mills limited, Satha is 1250 tcd.the factory has been established in Aligarh District.The technical as well as financial performance of last 5 years of The kisan sahkari chini mills limited, Satha is as under :- Sl.No

Particulars 2002-03 2003-04 2004-05 2005-06 2006-07

2007-08

Technical Performance

1. Cane Crushed (lac qtls.)

18.67 15.07 11.54 9.36 17.89 13.23

2. Sugar Recovery(%) 8.84 9.18 8.78 8.20 8.60 9.15 3. Capacity utilization

(%) 88 94 91 93 87 92

4. Sugar Production (lac qtls)

1.67 1.39 1.03 .79 1.56 1.23

Financial Performance

1. Net profit/loss (Rs. In lacs)

-1400.4

3 -837.85

-543.18

-1252.9

9

-1459.97

-1376.47

2. Cost of production ( Rs. Per Bag )

1858.18

1968.54 2465.62

3178.56

2520.78 2415.57

3. Accumulated Profit/loss (Rs. In lacs)

-8129.0

2

-8966.87

-9510.0

5

-10763.

04

-12223.01

-13599.48

4. Networth (Rs. In lacs)

-5924.4

2

-6761.80

-7302.6

3

-8555.2

3

-10013.1

3

-11386.6

6 5. 6. 7. 8. 9.

CAPITAL EMPLOYED SALE Share Capital & Outstanding loans (Rs. In lacs)

1243.34

1727.86

2369.21 1641.79

1840.12

3854.48

676.00 2189.5

4

127.40 1468.48

815.95

2251.36

(i) Share Capital State Govt. Capital 2044.3

0 2044.30 2044.3

0 2044.3

0 2044.30 2044.30

Others Share Capital

105.22 105.65 107.92 108.29 110.23 113.05

Total Share Capital 2149.52 2149.95 2152.22 2152.59 2154.53 2157.35 (ii) Outstanding loans a. State Govt. 3165.2

8 4897.15 5472.8

2 6048.4

9 6691.40 7756.83

b. Shakkar Vishesh Nidhi 1721.62 1810.82 1900.60 1979.80 2079.00 2243.43 c. Sugar Development

Fund as on 31.05.2007

25.61 25.61 25.61 25.61 25.61 ---

10 Number of Persons Employed

a. Permanent 221 b. Seasonal 369 c. Total 590

11 Land Area(acres) 70

The kisan sahkari chini mills limited,Semikhera

The kisan sahkari chini mills limited,Semikhera has been established under U.P.Cooperative Societies Act,1965 and its first crushing season was 1984-85.The present crushing capacity of The kisan sahkari chini mills limited, Semikhera is 2750 tcd.the factory has been established in Bareilly District.The technical as well as financial performance of last 5 years of The kisan sahkari chini mills limited, Semikhera is as under :- Sl.No Particulars 2002-03 2003-04 2004-05 2005-06 2006-07

2007-08

Technical Performance

1. Cane Crushed (lac qtls.)

37.24 23.49 26.91 29.79 45.20 34.62

2. Sugar Recovery(%) 9.15 9.35 9.12 8.78 8.69 9.07 3. Capacity utilization

(%) 83 83 85 84 80 83

4. Sugar Production (lac qtls)

3.41 2.21 2.45 2.61 3.95 3.16

Financial Performance

1. Net profit/loss (Rs. In lacs)

-1480.29 32.22 512.74 -291.41 -

1178.90 -

1064.522. Cost of Production

( Rs. Per Bag ) 1402.92 1439.18 1523.84 1911.2 1789.19 1708.75

3. Accumulated Profit/loss (Rs. In lacs)

-3245.62

-3213.39

-2700.65

-2992.06

-4170.97

-5235.49

4. Networth (Rs. In lacs)

-1306.69

-1274.46

-761.64 -1051.33

-2230.24

-3294.68

5. 6. 7. 8. 9.

CAPITAL EMPLOYED SALE Share Capital & Outstanding loans (Rs. In lacs)

2432.153458.91

4664.682773.18

4604.146050.24

3454.59 6205.50

1757.75 5352.58

2292.44

6135.39

(i) Share Capital State Govt. Capital 642.81 642.81 642.81 642.81 642.81 642.81 Others Share

Capital 33.84 33.68 33.76 35.46 35.46 35.46

Total Share Capital

676.65 676.49 676.57 678.27 678.27 678.27

(ii) Outstanding loans

a. State Govt. 257.78 1873.61 2063.53 2355.80 2465.12 1460.00b. Shakkar Vishesh Nidh ---- ---- ---- ---- ---- 0.00 c. Sugar Development

Fund as on 30.04.2007

142.40 142.40 289.95 325.15 280.37 161.65

10 1 Persons Employed

a. Permanent 198

b. Seasonal 307 c. Total 505 11 Land Area(acres) 119

The kisan sahkari chini mills limited,Snehroad The kisan sahkari chini mills limited,Snehroad has been established under U.P.Cooperative Societies Act,1965 and its first crushing season was 1989-90.The present crushing capacity of The kisan sahkari chini mills limited, Snehroad is 3000 tcd.the factory has been established in Najibabad Tehsil of Bijnor District.The technical as well as financial performance of last 5 years of The kisan sahkari chini mills limited, Snehroad is as under :- Sl.No

Particulars 2002-03

2003-04 2004-05

2005-06

2006-07

2007-08

Technical Performance

1. Cane Crushed (lac qtls.)

53.00 46.90 45.59 34.40 50.51 43.33

2. Sugar Recovery(%) 9.42 10.02 10.08 9.67 9.91 10.00 3. Capacity utilization

(%) 87 100 94 89 92 93

4. Sugar Production (lac qtls)

4.99 4.70 4.59 3.33 5.00 4.38

Financial Performance

1. Net profit/loss (Rs. In lacs)

-534.28

-321.18 2192.63

1754.61

501.50 -328.54

2. Cost of production ( Rs. Per Bag )

1277.02

1274.08 1197.40

1317.16

1419.94 1384.32

3. Accumulated Profit/loss (Rs. In lacs)

-956.66

-1277.84

207.03 1961.64

2463.14 2134.60

4. Networth (Rs. In lacs)

3306.49

2989.54 4975.03

7317.26

7989.39 7666.50

5. 6. 7. 8. 9.

CAPITAL EMPLOYED SALE Share Capital & Outstanding loans (Rs. In lacs)

8667.26

4245.17

10095.57

5578.48

8233.21

13185.0

8734.69

9253.39

8668.81 7396.70

10502.09

7371.93

(i) Share Capital State Govt. Capital 1182.5

0 1182.50 1182.5

0 1182.5

0 1182.50 1182.50

Others Share Capital

120.35 122.86 125.58 126.56 127.25 131.61

Total Share Capital 1302.85

1305.36 1308.08

1309.06

1309.75 1314.11

(ii) Outstanding loans .a. State Govt. ---- 12.39 213.33 289.95 325.95 361.95 b. Shakkar Vishesh

Nidhi ---- ---- ---- ---- ---- 0.00

c. Sugar Development Fund as on 31.05.2007

---- ---- ---- ---- ---- ---

10 Number of Persons Employed

a. Permanent 268

b. Seasonal 505 c. Total 773 11 Land Area(acres) 175

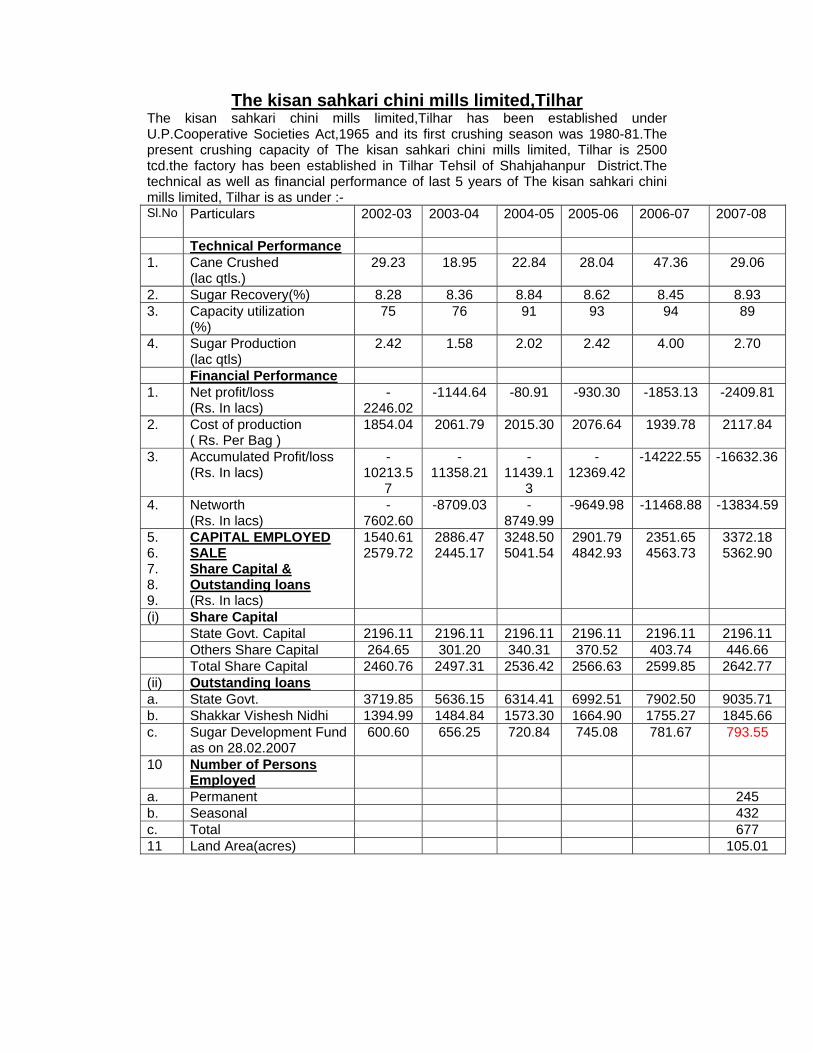

The kisan sahkari chini mills limited,Tilhar The kisan sahkari chini mills limited,Tilhar has been established under U.P.Cooperative Societies Act,1965 and its first crushing season was 1980-81.The present crushing capacity of The kisan sahkari chini mills limited, Tilhar is 2500 tcd.the factory has been established in Tilhar Tehsil of Shahjahanpur District.The technical as well as financial performance of last 5 years of The kisan sahkari chini mills limited, Tilhar is as under :- Sl.No Particulars 2002-03 2003-04 2004-05 2005-06 2006-07

2007-08

Technical Performance 1. Cane Crushed

(lac qtls.) 29.23 18.95 22.84 28.04 47.36 29.06

2. Sugar Recovery(%) 8.28 8.36 8.84 8.62 8.45 8.93 3. Capacity utilization

(%) 75 76 91 93 94 89

4. Sugar Production (lac qtls)

2.42 1.58 2.02 2.42 4.00 2.70

Financial Performance 1. Net profit/loss

(Rs. In lacs) -

2246.02 -1144.64 -80.91 -930.30 -1853.13 -2409.81

2. Cost of production ( Rs. Per Bag )

1854.04 2061.79 2015.30 2076.64 1939.78 2117.84

3. Accumulated Profit/loss (Rs. In lacs)

-10213.5

7

-11358.21

-11439.1

3

-12369.42

-14222.55 -16632.36

4. Networth (Rs. In lacs)

-7602.60

-8709.03 -8749.99

-9649.98 -11468.88 -13834.59

5. 6. 7. 8. 9.

CAPITAL EMPLOYED SALE Share Capital & Outstanding loans (Rs. In lacs)

1540.61 2579.72

2886.47 2445.17

3248.505041.54

2901.79 4842.93

2351.65 4563.73

3372.185362.90

(i) Share Capital State Govt. Capital 2196.11 2196.11 2196.11 2196.11 2196.11 2196.11 Others Share Capital 264.65 301.20 340.31 370.52 403.74 446.66 Total Share Capital 2460.76 2497.31 2536.42 2566.63 2599.85 2642.77(ii) Outstanding loans a. State Govt. 3719.85 5636.15 6314.41 6992.51 7902.50 9035.71b. Shakkar Vishesh Nidhi 1394.99 1484.84 1573.30 1664.90 1755.27 1845.66c. Sugar Development Fund

as on 28.02.2007 600.60 656.25 720.84 745.08 781.67 793.55

10 Number of Persons Employed

a. Permanent 245 b. Seasonal 432 c. Total 677 11 Land Area(acres) 105.01

The kisan sahkari chini mills limited,Ghosi The kisan sahkari chini mills limited,Ghosi has been established under U.P.Cooperative Societies Act,1965 and its first crushing season was 1984-85.The present crushing capacity of The kisan sahkari chini mills limited, Ghosi is 2500 tcd.the factory has been established Mau District.The technical as well as financial performance of last 5 years of The kisan sahkari chini mills limited, Ghosi is as under :- Sl.No

Particulars 2002-03 2003-04 2004-05 2005-06 2006-07

2007-08

Technical Performance 1. Cane Crushed

(lac qtls.) 22.53 19.06 20.21 25.45 28.21 23.02

2. Sugar Recovery(%) 8.35 8.55 8.65 8.40 8.02 8.35 3. Capacity utilization

(%) 76 79 86 79 77 88

4. Sugar Production (lac qtls)

1.88 1.63 1.75 2.14 2.26 2.00

Financial Performance 1. Net profit/loss

(Rs. In lacs) -

1739.34 -1224.22 -466.16 -1539.04 -2141.31 -2010.93

2. Cost of production ( Rs. Per Bag )

1921.50 2109.23 2085.77 2288.87 2438.15 2365.99

3. Accumulated Profit/loss (Rs. In lacs)

-11623.6

7

-12847.89

-13314.0

5

-14853.09

-16994.40 -19005.33

4. Networth (Rs. In lacs)

-9393.00

-10617.21

-11083.3

1

-12620.22

-14761.21 -16772.09

5. 6. 7. 8. 9.

CAPITAL EMPLOYED SALE Share Capital & Outstanding loans (Rs. In lacs)

1001.39 1497.96

1850.26 2044.01

3697.553082.30

3534.97 4021.39

2387.03 3216.89

2044.933514.86

(i) Share Capital State Govt. Capital 2174.70 2174.70 2174.70 2174.70 2174.70 2174.70 Others Share Capital 53.52 53.53 53.59 55.72 56.04 56.09 Total Share Capital 2228.22 2228.23 2228.29 2230.42 2230.74 2230.79(ii) Outstanding loans a. State Govt. 5993.06 7433.76 8271.69 8920.12 9578.54 10569.06b. Shakkar Vishesh Nidhi 997.29 1082.90 1163.69 1251.65 1341.36 1429.31c. Sugar Development

Fund as on 31.05.2007 45.32 49.32 53.32 59.41 1453.65 47.07

10 Number of Persons Employed

a. Permanent 205 b. Seasonal 250 c. Total 455 11 Land Area(acres) 100.177

The kisan sahkari chini mills limited Mahmoodabad The kisan sahkari chini mills limited,Mahmoodabad has been established under U.P.Cooperative Societies Act,1965 and its first crushing season was 1982-83.The present crushing capacity of The kisan sahkari chini mills limited, Mahmoodabad is 2750 tcd.the factory has been established in Mahmoodabad Tehsil of Sitapur District.The technical as well as financial performance of last 5 years of The kisan sahkari chini mills limited, Mahmoodabad is as under :- Sl.No

Particulars 2002-03

2003-04 2004-05

2005-06

2006-07

2007-08

Technical Performance

1. Cane Crushed (lac qtls.)

34.16 15.69 21.11 30.21 31.94 21.34

2. Sugar Recovery(%) 9.04 9.17 8.67 8.78 9.05 8.78 3. Capacity utilization

(%) 75.06 76.72 75.71 82.38 82.38 73.00

4. Sugar Production (lac qtls)

3.09 1.44 1.83 2.65 2.89 1.92

Financial Performance

1. Net profit/loss (Rs. In lacs)

-1918.7

0

-857.57 44.65 -899.03 -1683.21

-2470.98

2. Cost of production ( Rs. Per Bag )

1641.30

1987.59 2338.99

2126.42

2144.70 2335.12

3. Accumulated Profit/loss (Rs. In lacs)

-5891.8

9

-6749.46

-6704.8

1

-7603.8

4

-9287.05

-11758.03

4. Networth (Rs. In lacs)

-4181.56

-4995.52 -4924.58

-5791.44

-7447.85 -9895.57

5. 6. 7. 8. 9.

CAPITAL EMPLOYED SALE Share Capital & Outstanding loans (Rs. In lacs)

2783.14

2988.93

4111.94 3338.52

4395.41

4300.05

4518.83

4290.32

3443.33 5295.50

2602.58

3659.96

(i) Share Capital State Govt. Capital 662.95 662.95 662.95 662.95 662.95 662.95 Others Share

Capital 181.42 191.46 198.16 207.62 215.48 222.99

Total Share Capital 844.37 854.41 861.11 870.57 878.43 885.94 (ii) Outstanding loans a. State Govt. 1574.24 3375.40 3852.27 4329.13 5012.405 5487.37 b. Shakkar Vishesh Nidhi 828.76 877.71 942.06 990.93 1039.874 1451.40 c. Sugar Development

Fund as on 31.05.2007

398.87 560.03 605.43 641.09 660.4 689.66

10 Number of Persons Employed

a. Permanent 282 b. Seasonal 494 c. Total 776 11 Land Area(acres) 66.71

The kisan sahkari chini mills limited,Nanpara

The kisan sahkari chini mills limited,Nanpara has been established under U.P.Cooperative Societies Act,1965 and its first crushing season was 1984-85.The present crushing capacity of The kisan sahkari chini mills limited, Nanpara is 2500 tcd.the factory has been established in Nanpara Tehsil of Bahraich District.The technical as well as financial performance of last 5 years of The kisan sahkari chini mills limited, Nanpara is as under :- Sl.No

Particulars 2002-03

2003-04 2004-05

2005-06

2006-07

2007-08

Technical Performance

1. Cane Crushed (lac qtls.)

39.40 24.39 29.52 33.38 46.25 31.17

2. Sugar Recovery(%) 8.50 8.83 8.75 8.60 8.47 8.76 3. Capacity utilization

(%) 78 83 88 89 86 96

4. Sugar Production (lac qtls)

3.35 2.15 2.58 2.87 3.92 2.82

Financial Performance

1. Net profit/loss (Rs. In lacs)

-1906.3

6

-959-11 -73.55 -820.66 -2063.89

-2311.13

2. Cost of production ( Rs. Per Bag )

1660.82 1768.53 1927.30 2129.50 1965.15 2082.95

3. Accumulated Profit/loss (Rs. In lacs)

-9335.96

-10294.87

-10366.

55

-1199.90

-13142.81

-15449.49

4. Networth (Rs. In lacs)

-5898.82

-6824.53 -6831.36

-7606.25

-9501.85 -11742.32

5. 6. 7. 8. 9.

CAPITAL EMPLOYED SALE Share Capital & Outstanding loans (Rs. In lacs)

3437.10

3217.16

3470.30 3010.91

3535.15

4739.65

3593.61

6530.35

3640.92 5658.84

3854.88

5561.07

(i) Share Capital State Govt. Capital 2590.21 2590.21 2590.21 2590.21 2590.21 2590.21 Others Share

Capital 324.79 357.98 400.16 458.41 505.18 536.03

Total Share Capital 2915.00 2948.19 2990.37 3048.62 3095.39 3126.24 (ii) Outstanding loans a. State Govt. 3513.5

2 5093.78 5686.0

1 6278.1

7 6870.33 7462.50

b. Shakkar Vishesh Nidhi 888.43 960.10 1031.75 1101.03 1172.69 1244.34 c. Sugar Development

Fund as on 30.04.2007

650.84 808.95 942.92 1028.08

998.36 3285.64

10 Number of Persons Employed

a. Permanent 291 b. Seasonal 451 c. Total 742 11 Land Area(acres) 95.92

The kisan sahkari chini mills limited,Sathiaon

The kisan sahkari chini mills limited,Sathiaon has been established under U.P.Cooperative Societies Act,1965 and its first crushing season was 1975-76.The present crushing capacity of The kisan sahkari chini mills limited, Sathiaon is 1250 tcd.the factory has been established in Azamgarh District.The technical as well as financial performance of last 5 years of The kisan sahkari chini mills limited, Sathiaon is as under :- Sl.No

Particulars 2002-03

2003-04 2004-05

2005-06

2006-07

2007-08

Technical Performance

1. Cane Crushed (lac qtls.)

9.69 2.23 2.86 5.25 4.77 ----

2. Sugar Recovery(%) 7.57 7.60 7.10 7.00 6.57 ---- 3. Capacity utilization(%) 66 57 51 62 50 ---- 4. Sugar Production

(lac qtls) .73 .18 .20 .36 .31 ----

Financial Performance

1. Net profit/loss (Rs. In lacs)

-1278.81

-1019.09 -1110.93

-1347.94

-1694.61 -1326.36

2. Cost of production ( Rs. Per Bag )

2912.13

6209.32 8138.45

5373.13

6430.35 ---

3. Accumulated Profit/loss (Rs. In lacs)

-8794.1

5

-9813.24

-10927.

44

-12275.

38

-13969.99

-15296.34

4. Networth (Rs. In lacs)

-6929.1

7

-7940.37

-9053.4

0

-10400.

93

-12095.1

3

-13420.9

3 5. 6. 7. 8. 9.

CAPITAL EMPLOYED SALE Share Capital & Outstanding loans (Rs. In lacs)

62.09 662.38

298.78 648.84

-200.84 895.83

6.81 625.87

-788.71 520.80

-483.28

---

(i) Share Capital State Govt. Capital 1762.02 1762.02 1762.02 1762.02 1762.02 1762.02 Others Share Capital 83.36 90.99 92.11 92.47 92.70 93.22 Total Share Capital 1845.3

8 1853.01 1854.1

3 1854.4

9 1854.72 1855.24

(ii) Outstanding loans a. State Govt. 3319.4

4 4432.91 5088.8

9 5624.5

4 7083.77 6095.85

b. Shakkar Vishesh Nidhi 1380.99 1471.88 1568.09 1651.86 1742.74 2420.75 c. Sugar Development

Fund as on 31.05.2007

---- ---- ---- ---- ---- ---

10 Number of Persons Employed

a. Permanent 246 b. Seasonal 364 c. Total 610 11 Land Area(acres) 86.382

The kisan sahkari chini mills limited,Sultanpur

The kisan sahkari chini mills limited,Sultanpur has been established under U.P.Cooperative Societies Act,1965 and its first crushing season was 1983-84.The present crushing capacity of The kisan sahkari chini mills limited, Sultanpur is 1250 tcd.the factory has been established in Sultanpur District.The technical as well as financial performance of last 5 years of The kisan sahkari chini mills limited, Sultanpur is as under :- Sl.No

Particulars 2002-03

2003-04 2004-05

2005-06

2006-07

2007-08

Technical Performance

1. Cane Crushed (lac qtls.)

16.44 8.70 8.20 13.78 21.19 13.94

2. Sugar Recovery(%) 8.19 8.76 8.73 8.68 8.74 9.11 3. Capacity utilization(%) 85 89 89 92 87 88 4. Sugar Production

(lac qtls) 1.35 0.77 0.72 1.20 1.85 1.31

Financial Performance

1. Net profit/loss (Rs. In lacs)

-1252.36

-791.18 -578.78

-898.45 -1257.23

-1195.86

2. Cost of production ( Rs. Per Bag )

2255.03

2264.15 3145.89

2224.18

2165.80 2273.22

3. Accumulated Profit/loss (Rs. In lacs)

-6578.4

2

-7369.60

7974.07

-8872.5

2

-10131.25

-11327.11

4. Networth (Rs. In lacs)

-5154.81

-5935.67 -6533.94

-7424.75

-8673.00 -9859.85

5. 6. 7. 8. 9.

CAPITAL EMPLOYED SALE Share Capital & Outstanding loans (Rs. In lacs)

314.38 1423.6

2

1209.06 1327.56

1373.69

1838.02

1525.47

1807.25

927.64 2821.27

584.23

2539.05

(i) Share Capital State Govt. Capital 894.92 894.92 901.57 901.57 901.57 901.57 Others Share

Capital 416.55 426.81 426.35 433.95 444.19 452.87

Total Share Capital 1311.47

1321.73 1327.92

1335.52

1345.76 1354.44

(ii) Outstanding loans a. State Govt. 2969.0

5 4432.53 5089.2

9 5615.6

8 6142.07 6459.94

b. Shakkar Vishesh Nidhi 726.60 783.90 842.22 894.34 946.46 992.59 c. Sugar Development

Fund as on 31.01.2007

11.19 12.85 14.37 16.08 1.11 14.61

10 Number of Persons Employed

a. Permanent 235 b. Seasonal 361 c. Total 596 11 Land Area(acres) 96

ANNEXURE II

APPLICATION LETTER (On the letter head of the Bidder) Date: To, Registrar, Cane Cooperative Societies ,Uttar Pradesh, 17, New Beri Road, Lucknow- 226001 Uttar Pradesh Ref: Your advertisement in ---------- dated___________ Sub: Valuation services for Cooperative Sugar Mills in Uttar Pradesh Sir,

Being duly authorised to represent and act on behalf of .................................................... (hereinafter referred to as "the Bidder"), and having reviewed and fully understood all of the requirements of the RFQ cum RFP (BID) and information provided, the undersigned hereby apply for the project referred above. We are enclosing the following documents in one original plus one copy, with the details as per the requirements of the Bid invitation, for your evaluation.

i) A valid and duly authenticated registration document issued by the state or central government certifying our firm as a “Government approved valuer”/certificate of practice of chartered accountant.

ii) Credentials for assignments undertaken in the last two years along with proof thereof (Letter of Appointment etc).

iii) Undertaking that, we will be able to submit the valuation reports for________ bundles, as specified in para 1 of RFQ cum RFP document, if awarded to us, within 4 weeks of appointment.

iv) Technical Bid (Envelope A) as per Annexure III of RFQ cum RFP document

v) Financial Bid (Envelope B) as per Annexure IV of RFQ cum RFP document.

vi) Bid Security in the form of a demand draft of Rs. 50,000 (Rupees fifty thousand only) in favour of “Registrar,Cooperative Cane Socieities , Uttar Pradesh” Payable at Lucknow for each bundle.

Yours sincerely. Signature Name (Authorised Signatory)

ANNEXURE III

FORMAT FOR TECHNICAL BID NAME OF THE BIDDER : REGISTERED OFFICE : DETAILS OF CONTACT PERSONS (along with their telephone numbers, fax numbers, e-mail Ids) : A] SHORTLISTING PARAMETERS Sr. No Criteria 1 Past experience of the company

• Number of years of experience: • Past experience in valuation of industrial units • Past experience in valuation of sugar mills • Past experience in valuation of assets being disinvested by

state/central/UT government 2 Key personnel

• Years of experience • No. of certified valuers

Note: Please provide details of each reference project for which your firm was contracted by the client in the details below: Name of the client: Start date of assignment: End date of assignment: Detailed narrative description of project: Detailed description of actual services provided by your firm:

ANNEXURE IV

FORMAT FOR FINANCIAL BID

FINANCIAL BID (On the letter head of the Bidder) To , Registrar, Cane Cooperative Societies ,Uttar Pradesh, 17, New Beri Road, Lucknow- 226001 Uttar Pradesh Sub: Appointment of Valuer for Sugar Mills in Uttar Pradesh Sir, I/We have perused the proposal document for subject assignment contracting Scope of Work at Para 9 and other details and am/are willing to undertake and complete the assignments as per terms and conditions stipulated in the proposal document. Our offer is inclusive of all taxes including service tax, incidentals, overheads, travelling expenses, printing and binding of reports, all sundries, all other expenditure for execution of this service/assignment covering all 'Scope of Work’ as mentioned in the bid document of Registrar is as follows:

a. For Valuation of bundle1: Rs. ........................... (i.e., in words Rupees.....................................................).

b. For Valuation of bundle 2: Rs. ........................... (i.e., in words Rupees.....................................................).

c. For Valuation of bundle 3: Rs. ........................... (i.e., in words Rupees.....................................................).

d. For Valuation of bundle 4: Rs. ........................... (i.e., in words Rupees.....................................................).

e. For Valuation of bundle 5: Rs. ........................... (i.e., in words Rupees.....................................................).

This offer is valid for a period of 3 months from the date of opening of the bid (bid due date). Witnesses Signature Signature of Authorised Person Name : Name : Address : Address :

ANNEXURE V

Valuation Methodologies being followed

Making a valuation requires an examination of several aspects of a company's activities, such as analysing its historical performance, analysing its competitive positioning in the industry, analysing inherent strengths/weaknesses of the business and the opportunities/threats presented by the environment, forecasting operating performance, estimating the cost of capital, estimating the continuing value, calculating and interpreting results, analysing the impact of prevailing regulatory frame work, the global industry outlook, impact of technology and several other environmental factors.

Keeping with the best market practices the following four methodologies are being used for valuations: -

a) Discounted Cash Flow (DCF) Method.

b) Balance Sheet Method.

c) Transaction Multiple Method.

d) Asset Valuation Method.

While the first three are business valuation methodologies generally used for valuation of a going concern, the last methodology would be relevant only for valuation of assets in case of liquidation of a company. In addition, in case of listed companies, the market value of shares during the last six months is also used as an indicator. However, many sugar company’s stocks suffer from low liquidity and the price determination may not be always efficient. Moreover, there could be increased trading activity after announcement of the valuation, which could be on account of high market expectation of the bid price and even based on malafide intent. This could lead to the price being traded up to unsustainable levels, which is not desirable.

Discounted Cash Flow (DCF) method

The Discounted Cash Flow (DCF) methodology expresses the present value of a business as a function of its future cash earnings capacity. This methodology works on the premise that the value of a business is measured in terms of future cash flow streams, discounted to the present time at an appropriate discount rate.

This method is used to determine the present value of a business on a going concern assumption. It recognises that money has a time value by discounting future cash flows at an appropriate discount factor. The DCF methodology depends on the projection of the future cash flows and the selection of an appropriate discount factor.

When valuing a business on a DCF basis, the objective is to determine a net present value of the free cash flows ("FCF") arising from the business over a future period of time (say 5 years), which period is called the explicit forecast period. Free cash flows are defined to include all inflows and outflows associated with the project prior to debt service, such as taxes, amount invested in working capital and capital expenditure. Under the DCF methodology, value must be placed both on the explicit cash flows as stated above, and the ongoing cash flows a company will generate after the explicit forecast period. The latter value, also known as terminal value, is also to be estimated.

The further the cash flows can be projected, the less sensitive the valuation is to inaccuracies in the assumed terminal value. Therefore, the longer the period covered by the projection, the less reliable the projections are likely to be. For this reason, the approach is used to value businesses, where the future cash flows can be projected with a reasonable degree of reliability. For example, in a fast changing market like telecom or even automobile, the explicit period typically cannot be more than at least 5 years. Any projection beyond that would be mostly speculation.

The discount rate applied to estimate the present value of explicit forecast period free cash flows as also continuing value, is taken at the "Weighted Average Cost of Capital" (WACC). One of the advantages of the DCF approach is that it permits the various elements that make up the discount factor to be considered separately, and thus, the effect of the variations in the assumptions can be modelled more easily. The principal elements of WACC are cost of equity (which is the desired rate of return for an equity investor given the risk profile of the company and associated cash flows), the post-tax cost of debt and the target capital structure of the company (a function of debt to equity ratio). In turn, cost of equity is derived, on the basis of capital asset pricing model (CAPM), as a function of risk-free rate, Beta (an estimate of risk profile of the company relative to equity market) and equity risk premium assigned to the subject equity market.

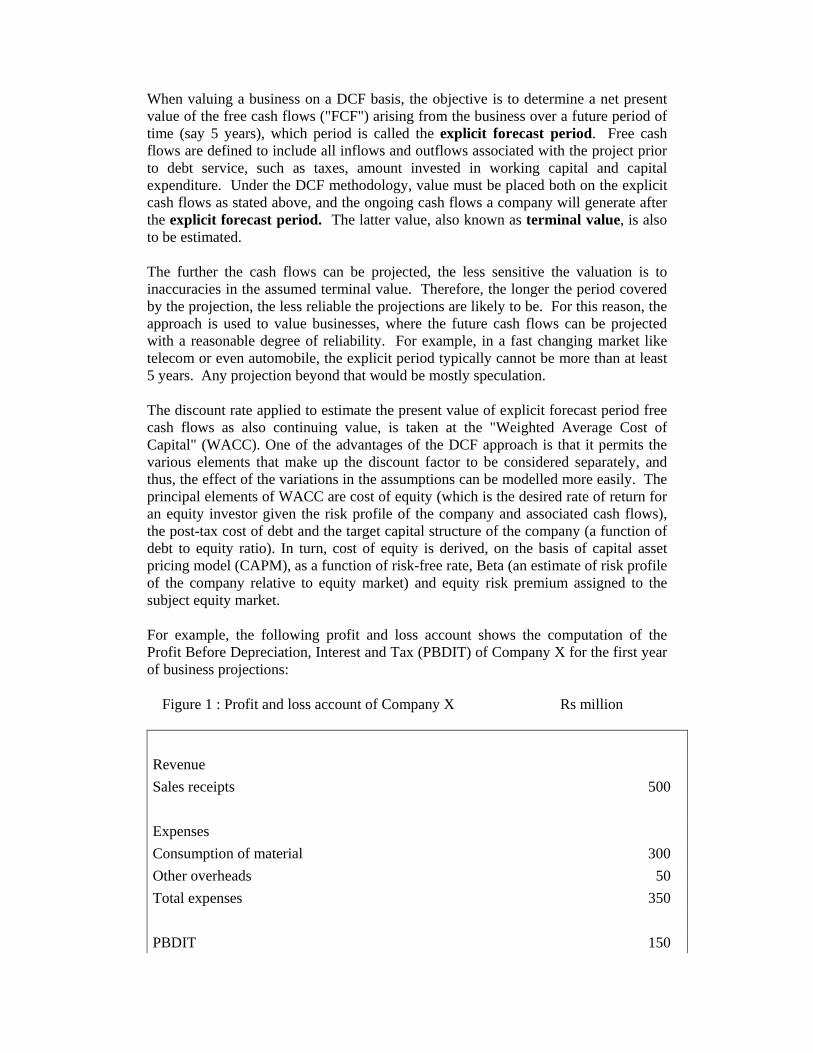

For example, the following profit and loss account shows the computation of the Profit Before Depreciation, Interest and Tax (PBDIT) of Company X for the first year of business projections:

Figure 1 : Profit and loss account of Company X Rs million

Revenue Sales receipts 500 Expenses Consumption of material 300 Other overheads 50 Total expenses 350 PBDIT 150

Computation of Free Cash Flow to Firm (‘FCF’): Free cash flow (FCF) for a year is derived by deducting the total of annual tax outflow inclusive of tax shield enjoyed on account of debt service, incremental amount invested in working capital and capital expenditure from the respective year’s profit before depreciation interest and tax (“PBDIT”) for the explicit period.

Therefore, for Company X, the computation of FCFwould look like the following:

Figure 2: FCF computation for Company X Rs million

Year 1 Year 2 Year 3 Year 4 Year 5 PBDIT of Company X * 150 200 300 400 500 Less: Income tax (assumed)

-20 -40 -60 -80 -100

Less: Capital expenditure (assumed)

-50 -50 -50 -50 -50

Less: Incremental working capital (assumed)

-25 -50 -75 -100 -125

FCF 55 60 115 170 225

* Notice that a growth has been assumed in the PBDIT

Weighted Average Cost of Capital (‘WACC’)

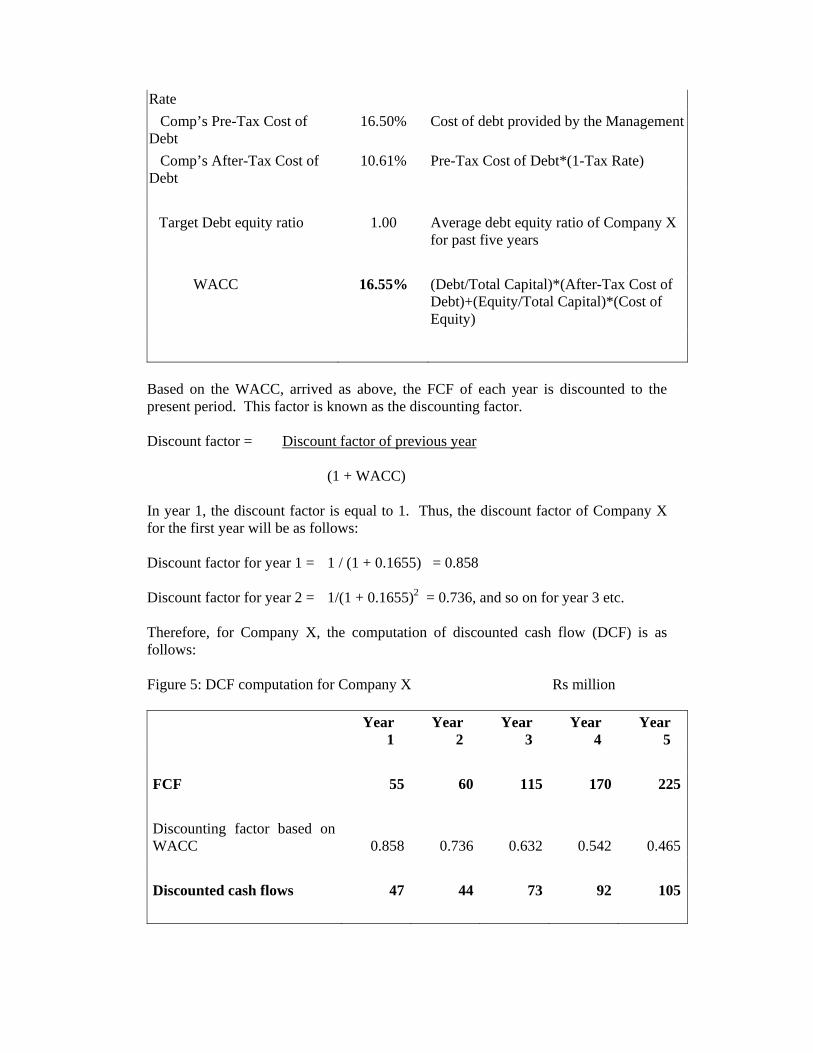

The FCF is then discounted at a discount rate, which represents the WACC. The computation of the WACC is set out below:

Figure 3: WACC parameters

Cost of equity Assumption Risk Free Rate Yield to maturity on Government of India Securities

based on current traded value (preferably these should be of a long-term tenor beyond the forecast period i.e. minimum 10 years)

Beta For the purpose of analysis, average unlevered beta of listed industry comparables is computed, which is then levered to the Company’s own target debt equity ratio The levered (equity) Beta of a scrip is a measure of relative risk to market, arithmetically computed as covariance of equity and market return divided by variance of market return (over a long historical data run) followed with certain adjustments

Equity Risk Premium = Beta * (Market Risk Premium) Market Risk Premium is equal to the difference of average market return and risk free rate #

Cost of Equity =Risk Free Rate + (Equity Risk Premium*Beta) Cost of debt Estimated Corporate Tax Rate Current corporate tax rate in India Comp’s Pre-Tax Cost of Debt Cost of debt provided by the Management Comp’s After-Tax Cost of Debt

Pre-Tax Cost of Debt*(1-Tax Rate) @

Target Debt equity ratio Average debt equity ratio of the Company WACC (Debt/Total Capital)*(After-Tax Cost of

Debt)+(Equity/Total Capital)*(Cost of Equity)

@ This is the tax shield referred to earlier.