Embed Size (px)

Citation preview

1

Tennessee Gas Pipeline

2015 Customer Meeting Business Session

Thursday August 13,2015

2

Agenda

Thursday, August 13th, 2015

8:30 a.m. Welcome Sital Mody

8:45 a.m. Pipeline Operations Update Ray Miller

9:05 a.m. Macro Overview and TGP flow changes Ernesto Ochoa

9:25 a.m. Break

9:45 a.m. Business Development Projects Paul Smith

10:05 a.m. Northeast Energy Direct Update Curtis Cole

10:25 a.m. Pipeline Expansion in New England Suedeen Kelly

11:20 a.m. Closing Remarks and Q&A TGP Team

11:45 a.m. Lunch Salt

11:50 to 5:30 p.m. Afternoon Activities (As Selected)

6:30 p.m. Social Solarium

7:45 p.m. Dinner Wentworth Ballroom

3

This presentation contains forward-looking statements. These forward-looking statements are identified as any statement that does not relate strictly

to historical or current facts. In particular, statements, express or implied, concerning future actions, conditions or events, future operating results or

the ability to generate revenues, income or cash flow or to pay dividends are forward-looking statements. Forward-looking statements are not

guarantees of performance. They involve risks, uncertainties and assumptions. Future actions, conditions or events and future results of operations of

Kinder Morgan, Inc. may differ materially from those expressed in these forward-looking statements. Many of the factors that will determine these

results are beyond Kinder Morgan's ability to control or predict. These statements are necessarily based upon various assumptions involving

judgments with respect to the future, including, among others, the ability to achieve synergies and revenue growth; national, international, regional

and local economic, competitive and regulatory conditions and developments; technological developments; capital and credit markets conditions;

inflation rates; interest rates; the political and economic stability of oil producing nations; energy markets; weather conditions; environmental

conditions; business and regulatory or legal decisions; the pace of deregulation of retail natural gas and electricity and certain agricultural products;

the timing and success of business development efforts; terrorism; and other uncertainties. There is no assurance that any of the actions, events or

results of the forward-looking statements will occur, or if any of them do, what impact they will have on our results of operations or financial

condition. Because of these uncertainties, you are cautioned not to put undue reliance on any forward-looking statement. Please read "Risk Factors"

and "Information Regarding Forward-Looking Statements" in our most recent Annual Report on Form 10-K and our subsequently filed Exchange Act

reports, which are available through the SEC’s EDGAR system at www.sec.gov and on our website at www.kindermorgan.com.

We use non-generally accepted accounting principles (“non-GAAP”) financial measures in this presentation. Our reconciliation of non-

GAAP financial measures to comparable GAAP measures can be found in the Appendix to our Analyst Day presentation, dated

1/28/2015, on our website at www.kindermorgan.com. These non-GAAP measures should not be considered an alternative to GAAP

financial measures.

Forward-Looking Statements / Non-GAAP Financial Measures

5

Marcellus/Utica

SCOOP/Stack

5

6

Agenda

• Past Winter

• This Summer

• Storage

• Pipeline Integrity

• Operational Expectations

• Pictures

• Scheduling NOPR

7

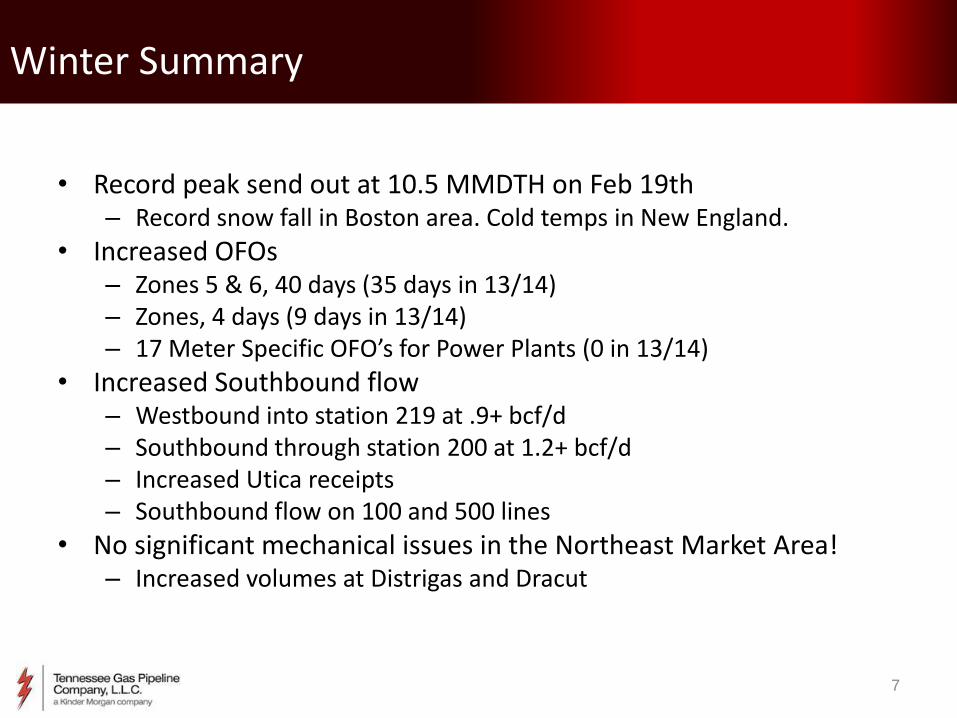

Winter Summary

• Record peak send out at 10.5 MMDTH on Feb 19th – Record snow fall in Boston area. Cold temps in New England.

• Increased OFOs – Zones 5 & 6, 40 days (35 days in 13/14) – Zones, 4 days (9 days in 13/14) – 17 Meter Specific OFO’s for Power Plants (0 in 13/14)

• Increased Southbound flow – Westbound into station 219 at .9+ bcf/d – Southbound through station 200 at 1.2+ bcf/d – Increased Utica receipts – Southbound flow on 100 and 500 lines

• No significant mechanical issues in the Northeast Market Area! – Increased volumes at Distrigas and Dracut

8

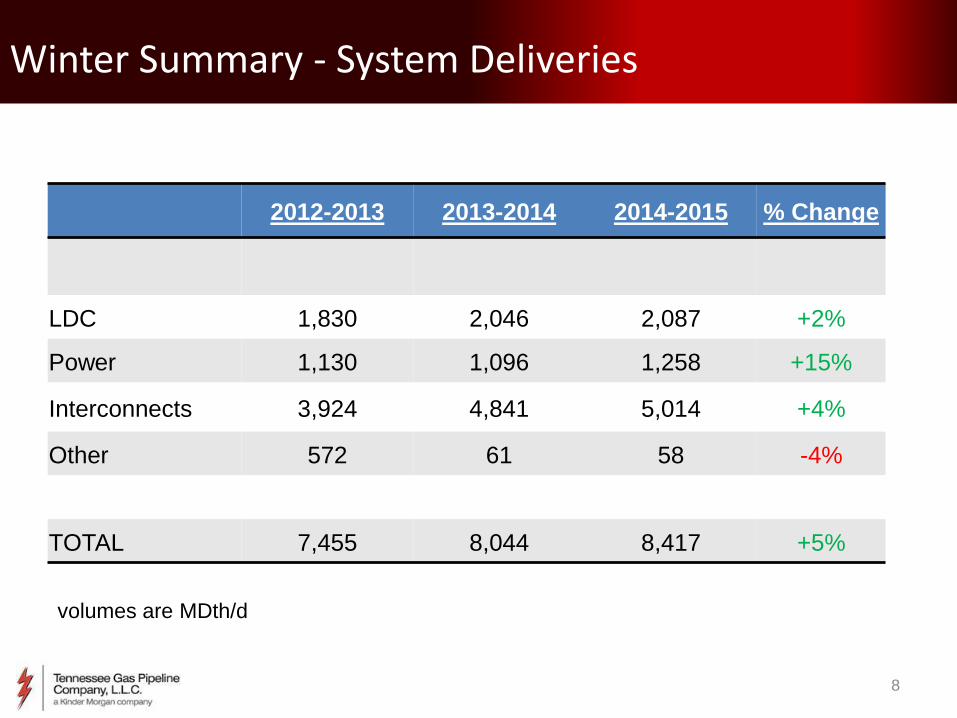

Winter Summary - System Deliveries

2012-2013 2013-2014 2014-2015 % Change

LDC 1,830 2,046 2,087 +2%

Power 1,130 1,096 1,258 +15%

Interconnects 3,924 4,841 5,014 +4%

Other 572 61 58 -4%

TOTAL 7,455 8,044 8,417 +5%

volumes are MDth/d

9

-

200

400

600

800

1,000

1,200

1,400

1,600

2009-2010 2010-2011 2011-2012 2012-2013 2013-2014 2014-2015

Zone 6

Zone 5

Zone 4

Zone 2

Zone 1

Zone 0

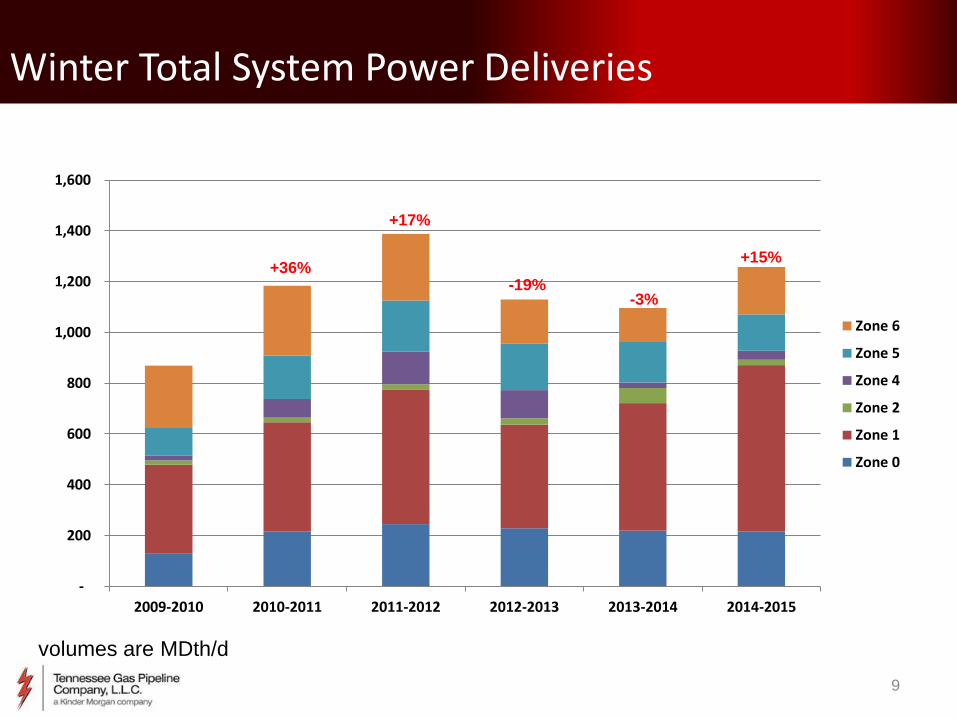

Winter Total System Power Deliveries

volumes are MDth/d

+36%

+17%

-19% -3%

+15%

10

Cold New England Weather

200

400

600

800

1000

1200

1400

Nov Dec Jan Feb Mar

HD

Ds

Winter 2014/15

Winter 2013/14

Winter 2012/13

30 Year Average

11

Winter New England Deliveries

2012-2013 2013-2014 2014-2015 % Change

LDC 1,324 1,467 1,511 +3%

Power 346 274 315 +15%

Interconnects 468 1,316 1362 +3%

TOTAL 2,137 3,057 3,187 +4%

volumes are MDth/d

12

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2012 2013 2014 2015 YTD

• All volumes are MDth/d

Winter New England LDC Deliveries

13

Winter North Supply Analysis

Winter Period (Nov-Mar) Average MDth/d

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

09-10 10-11 11-12 12-13 13-14 14-15

Dracut

Distrigas

Shelton

Wright

Niagara

Marcellus

Utica

Rex

+70%

+15% +5%

+38%

+17%

Total Marcellus supply was

over 19 bcf/d this winter!

14

0

100

200

300

400

500

600

700

800

900

1,000

11-12 12-13 13-14 14-15

Canada

Mexico

Winter System Exports

-1% -2%

volumes are MDth/d

+155%

15

Summer Summary

• Demand is up (vs previous summer) – Overall system - 7% higher – Power Generation - 15% higher

• Market Area Supply continues to increase – Increase in both Utica and Marcellus Supply

• Increased Southbound Flows – Station 200 (Ohio) – 1.5 to 1.6 Bcf/d – Station 860 (Tennessee) - 0.8 – 0.9 Bcf/d – South Texas market remains strong

• Main drivers – Heat and Storage fill – High level of system maintenance, repair, rebuild activity

• GETTING READY FOR WINTER

16

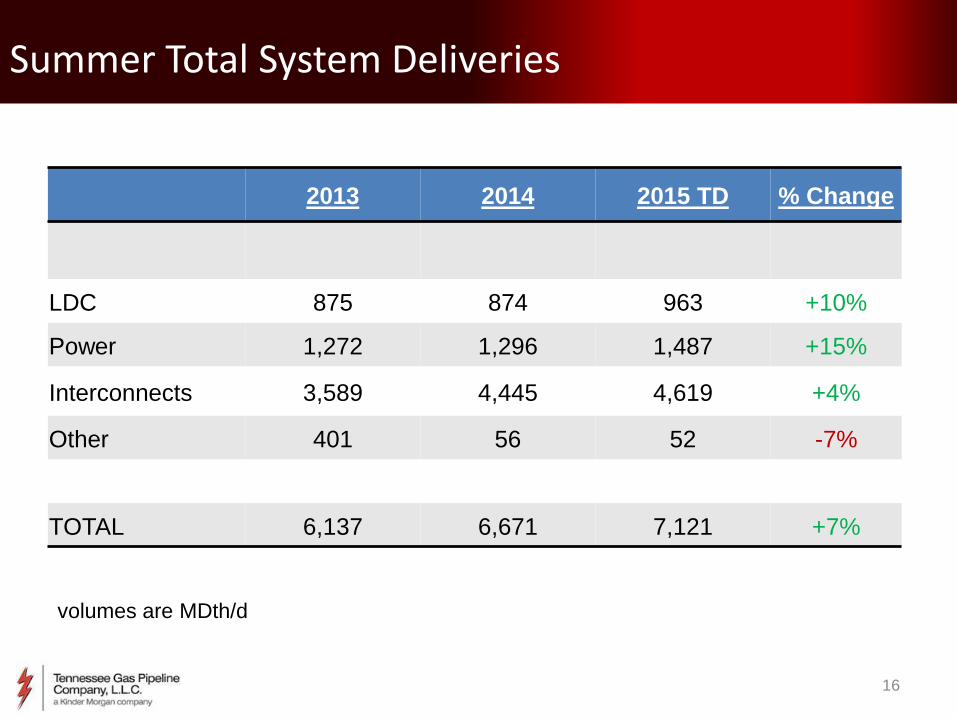

Summer Total System Deliveries

2013 2014 2015 TD % Change

LDC 875 874 963 +10%

Power 1,272 1,296 1,487 +15%

Interconnects 3,589 4,445 4,619 +4%

Other 401 56 52 -7%

TOTAL 6,137 6,671 7,121 +7%

volumes are MDth/d

17

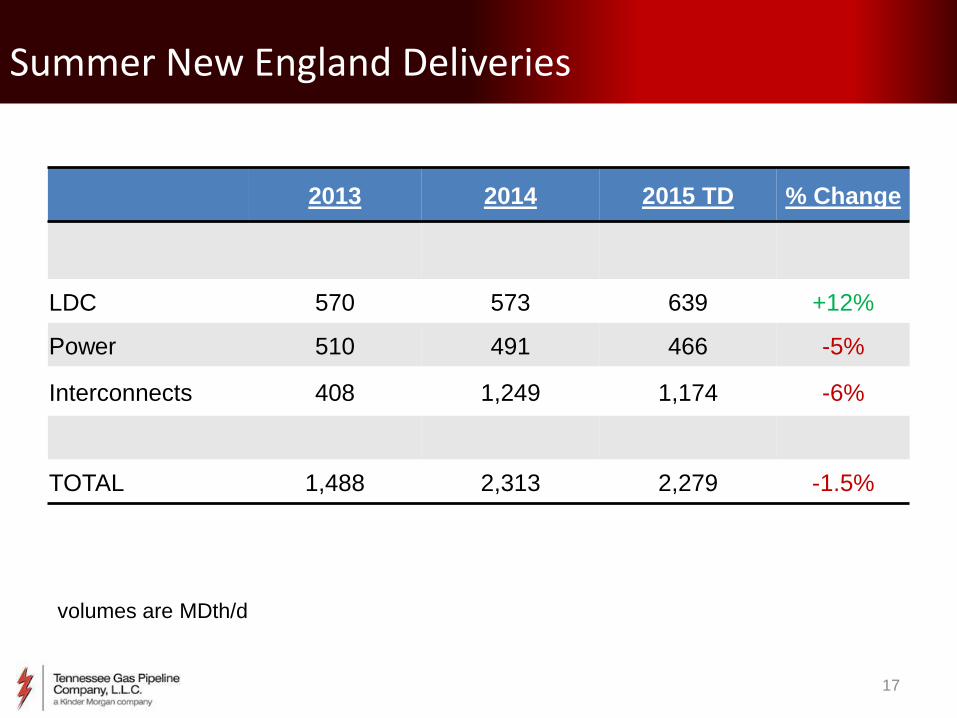

Summer New England Deliveries

2013 2014 2015 TD % Change

LDC 570 573 639 +12%

Power 510 491 466 -5%

Interconnects 408 1,249 1,174 -6%

TOTAL 1,488 2,313 2,279 -1.5%

volumes are MDth/d

18

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2009 2010 2011 2012 2013 2014 2015 TD

Zone 6

Zone 5

Zone 4

Zone 2

Zone 1

Zone 0

Summer Total System Power Deliveries

volumes are MDth/d

+22%

+9%

+16%

-22% +2%

+15%

19

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2010 2011 2012 2013 2014 2015 TD

Dracut

Distrigas

Shelton

Wright

Niagara

Marcellus

Utica

Rex

Summer North Supply Analysis

volumes are MDth/d

+52%

+13% +8%

+36%

+15%

Total Marcellus supply near

20 bcf/d this summer!

20

National EIA Storage Statistics Through 07-31-2015

0

500

1000

1500

2000

2500

3000

3500

4000

Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct

BC

F

5 Year Range

2002-2003

2013-2014

2014-2015

5 Year Average 2009-2014

535 Bcf > 2014; 64 Bcf > 5 Yr. Avg. 32 Bcf Inj

2.912 Tcf Current Inventory

21

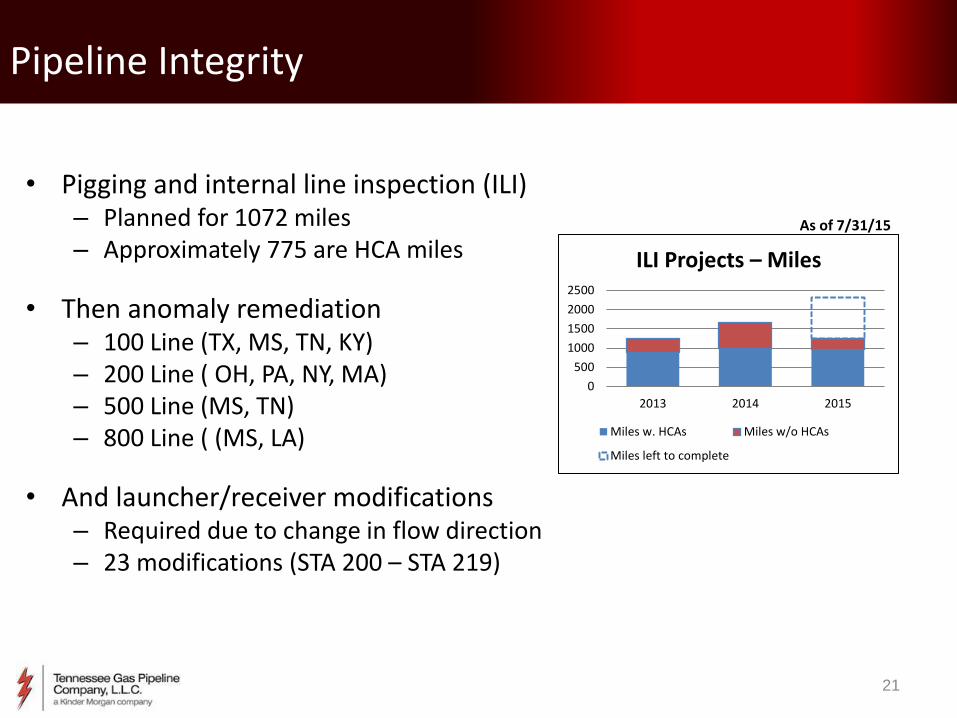

Pipeline Integrity

• Pigging and internal line inspection (ILI) – Planned for 1072 miles – Approximately 775 are HCA miles

• Then anomaly remediation – 100 Line (TX, MS, TN, KY) – 200 Line ( OH, PA, NY, MA) – 500 Line (MS, TN) – 800 Line ( (MS, LA)

• And launcher/receiver modifications – Required due to change in flow direction – 23 modifications (STA 200 – STA 219)

0

500

1000

1500

2000

2500

2013 2014 2015

ILI Projects – Miles

Miles w. HCAs Miles w/o HCAs

Miles left to complete

As of 7/31/15

22

Pipeline Integrity - Continued

• Hydrotest and Stress Corrosion Cracking (SCC) – 7 projects remaining 121 miles – 10 HCA miles – 200 Line- valve sections 261 and 262 – 100 Line, June - Nov – 800 Line valve section 843, Sept – Oct

• Class Changes – 100 & 500 Line – 17 miles of pipe to be replaced – 50% complete

• Other Integrity Work – 200 Line in Ohio – Pipe Inspections – Locational (IMU) Pig runs

0

50

100

150

2013 2014 2015

Pressure Test Projects - Miles

Miles w. HCAs Miles w/o HCAs

Miles left to complete

As of 7/31/15

23

Question

• It seems like we are seeing more events and postings that are causing interruptible service to be interrupted, including a few with warnings about firm service being interrupted, why?

24

Answer

• TGP utilization is at historical highs

• Good news: TGP is serving more customer needs than ever before

• Bad news: Limited flexibility to perform maintenance or repairs without an interruption.

25

Answer continued

Recent causes for limiting interruptible service – Planned maintenance – Unplanned maintenance – Required class location upgrades – Integrity work

• Installing/modifying pig launchers and receivers • Managing speed of internal tools during pig runs • Anomaly remediation (if required)

– Soil movement remediation program – Expansion Project work

• Tie-ins for new construction • Rebuilding of compressor stations • New interconnections

26

Top Ten List – Compressor Station Maintenance

• Top ten compressor station maintenance items – Reciprocating power piston damaged

– Reciprocating power head cracked

– Metal detection in lubricating oil

– Turbocharger overhaul or replacement

– Centrifugal power turbine replacement

– Hardware or software automation issue

– Environmental compliance

– Valve not operating properly during start/stop

– Component vibration exceeding limit

– Complete rebuild of compressor station

– Emergency shut down (ESD)

27

Top Ten List – Pipeline maintenance

• Top ten pipeline maintenance items – ID/OD metal loss (magflux internal inspection tool)

– Diameter (dent) analysis (Caliper tool)

– Seam corrosion (AFD tool)

– Stress corrosion cracking (hydrotest or emat tool)

– Non piggable inspections (hydrotest or direct inspection)

– Construction records program (hydrotest)

– Wrinkle bend inspections

– Pressure weld inspections

– Soil movement monitoring program

– Third party damage to the pipe

28

Operational Expectations

• Continued high utilization driven by Marcellus and Utica supplies

– Both East and West from on TGP 300 Line

– South on TGP 200 Line

– South on TGP 500 Line

– South on TGP 100 Line

• Exports to Mexico & Canada increase

• Maintenance activities continue

– Scheduling of work on 100, 200, 300, 400, 500, 800 lines

• SOP, SIP, (maybe PIP) may be at risk depending on many factors including amount of integrity remediation, weather, permitting, etc.

• Available capacity is and will continue to be tight

29

FERC Ruling on Scheduling NOPR

• FERC – Rule to modify regulations for the scheduling of transportation services on interstate natural gas pipelines to:

(1) improve coordination of the gas and electric industries, and (2) provide additional liquidity and scheduling flexibility to all shippers

• INGAA collectively and KM individually participated during process • Order 809 - effective April 1, 2016 for the entire gas industry

– No change to start of Gas Day – remains 9 am CCT – Timely Cycle nomination deadline; changed from 11:30am to 1pm CCT – Additional intraday nomination cycle at 7 pm CCT

• Reduced cycle processing times by 1 hour, and • Adjusted cycle timelines to minimize overlaps

• In addition NAESB 2.1 (now 3.0) modifications ordered

DART and KM processes will be upgraded to be compliant by deadline date

30

Station 245 HP Replacement

Main Line #1 Tie-in

with coating removed for

cut

Compressor Building construction

31

Station 114 Rebuild

View of Yard Piping New Header

New Scrubber

32

At Compressor Building

In the Yard

Use of Hydrovac

33

Hydrotest Work

Clearing and Grubbing

Pipe Replacement Test Heads

34

Pigging

Pig Launcher

35

Loading magflux tool into launcher

Removing tool from receiver

Pigging

36

Caliper Pig Received

Caliper Pig Pre-Launch

Difficult Operations at Times

37

Tennessee Gas Pipeline 24 Hour Contact List

Gas Control

24 hour and emergency

800-231-2800

Ganesh Venkateshan –

Mgr.

713-420-2099

Cell –205-746-5752

Layne Sanders –

Director

713-420-5024

Cell – 832-563-5024

Danny Ivy - VP

713-369-9311

Cell – 713-829-2761

Ray Miller – VP

713-369-9330

Cell – 713-206-8338

Transport and Storage

Services

24 hour Scheduling Hotline

713-369-9683

Cathy Soape – Manager

713-420-3814

Cell – 713-922-5083

Debbie Vasquez – Manager

713-420-3864

Cell – 713-806-7723

Sherri Glazebrook – Director

713-420-3677

Cell – 281-678-1183

Gene Nowak – VP

713-369-9329

Cell – 713-252-9759

Commercial/Marketing

Ernesto Ochoa – Director

713-420-1734

Cell – 281-414-3823

Sital Mody – VP

713-420-7336

Cell – 832-643-0042

Norman Holmes - VP

713-420-4442

Cell – 205-901-0456

Kim Watson – President

713-369-3229

Cell – 713-204-5423

Field Operations

Ron Bessette– Director

(Northeast)

860-763-6027

Cell – 985-209-4478

John Pannel – Director (Central)

615-221-1511

Cell – 615-714-1930

Cy Harper – Director (South)

281-689-4534

Cell – 205-613-6701

Tom Dender – VP

205-325-3883

Cell – 7205-572-1549

Gary Buchler – COO GAS

Pipelines

713-369-8463

Cell – 713-824-3904

Colorado Springs, CO Office

713-420-2600

Two North Nevada Ave

Colorado Springs, Co 80903

Birmingham, AL Office

713-420-2600

569 Brookwood Village St

Birmingham, AL 35209

Downers Grove, IL Office

630-725-3000

3250 Lacey Rd

Suite 700

Downers Grove, IL 60515

Houston, TX Office

713-369-9000

1001 Louisiana St

Houston TX 77002

August 2015

39

The Macro View

Trends continue

Dramatic supply growth

Growing long-term demand Changing trade balance New Infrastructure

40

Key Assumptions

+2.7

+6.9 +0.9 Bcfd

+18.6 Bcfd +4.7 Bcfd

-3.4 Bcfd

+5.7 Bcfd

41

Supply

42

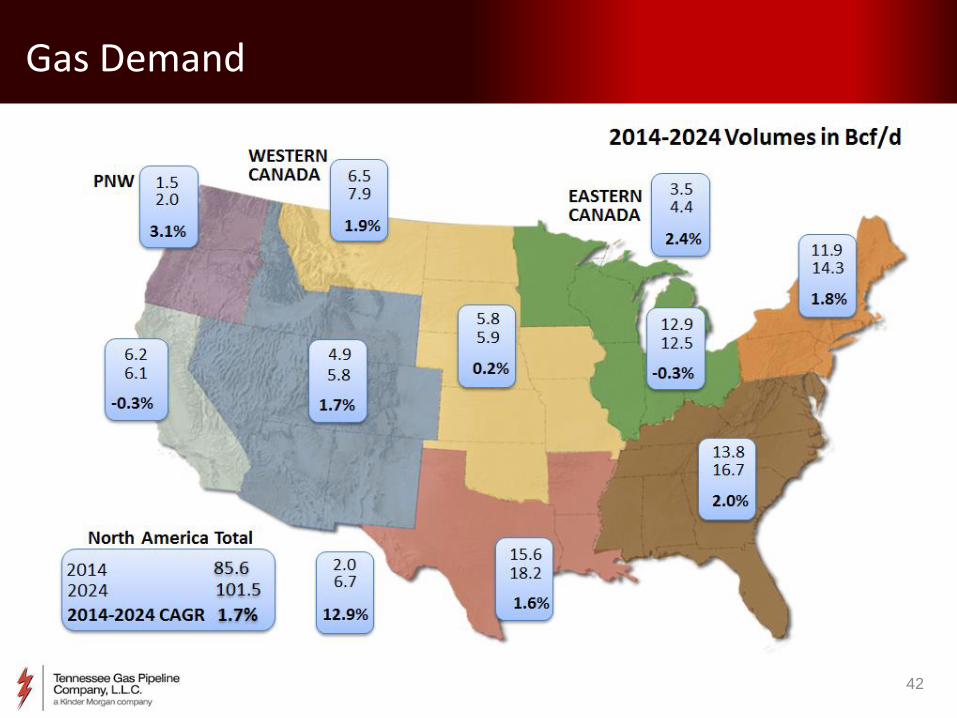

Gas Demand

43

Flows Change

Marcellus Shale

Utica Shale

Southeast

Northeast

EagleFord Shale

Haynesville Shale

44

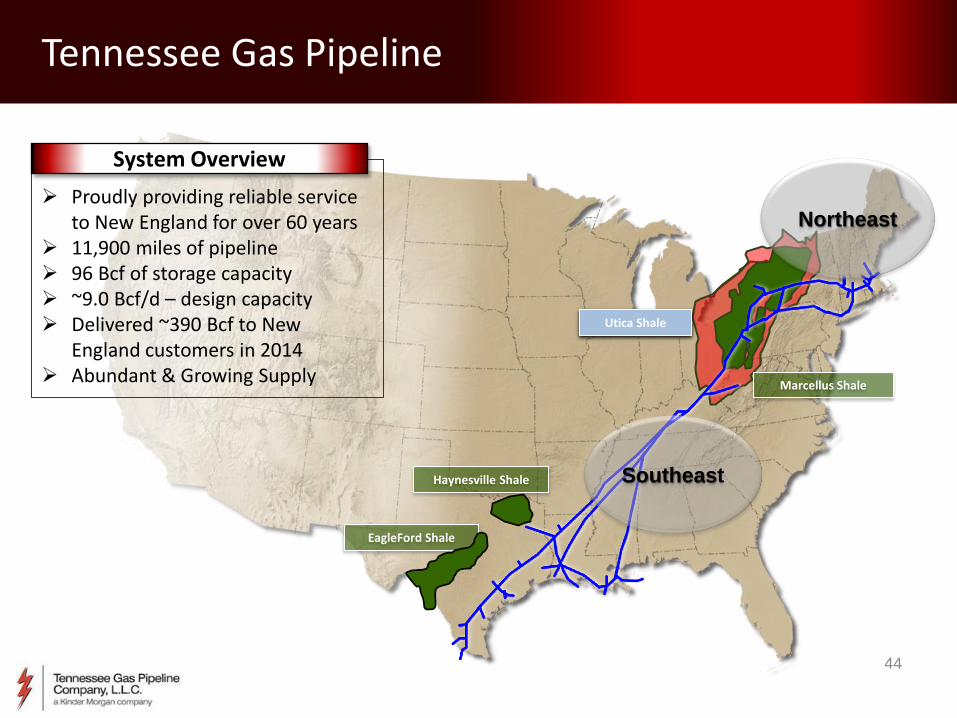

Tennessee Gas Pipeline

Proudly providing reliable service to New England for over 60 years

11,900 miles of pipeline 96 Bcf of storage capacity ~9.0 Bcf/d – design capacity Delivered ~390 Bcf to New

England customers in 2014 Abundant & Growing Supply

System Overview

45

0

5

10

15

20

25

30

35

40

45

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9

202

0

202

1

202

2

202

3

202

4

202

5

202

6

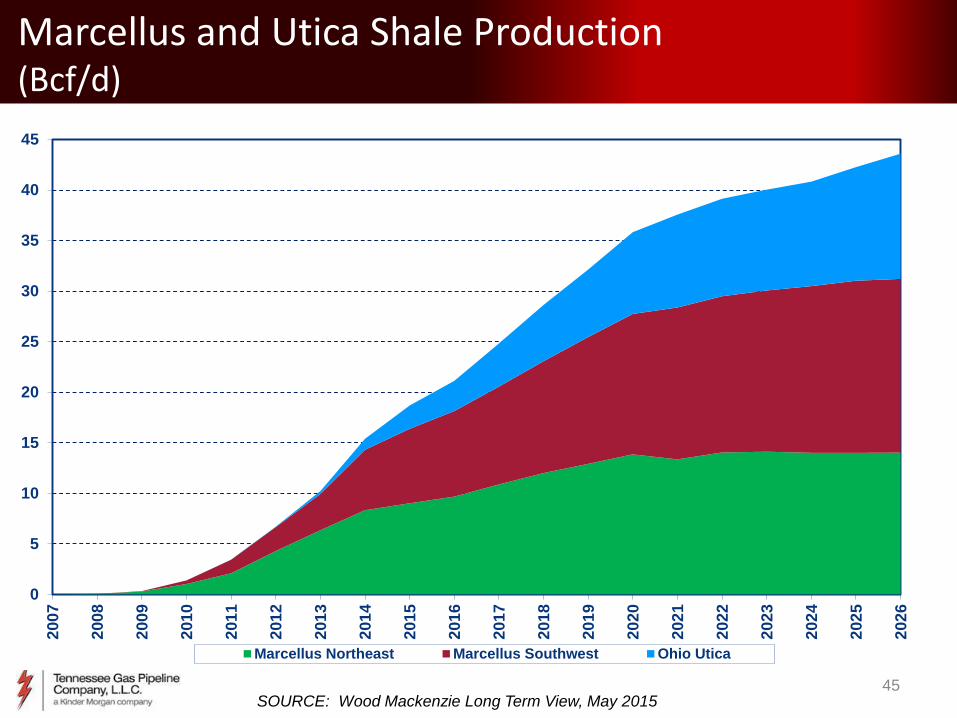

Marcellus Northeast Marcellus Southwest Ohio Utica

SOURCE: Wood Mackenzie Long Term View, May 2015

Marcellus and Utica Shale Production (Bcf/d)

46

Winter Period (Nov – Mar) Average Dth/d

Market Area Supply

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

09-10 10-11 11-12 12-13 13-14 14-15

Utica

Marcellus

Rex

Dracut

Distrigas

Wright

Shelton

Niagara

47

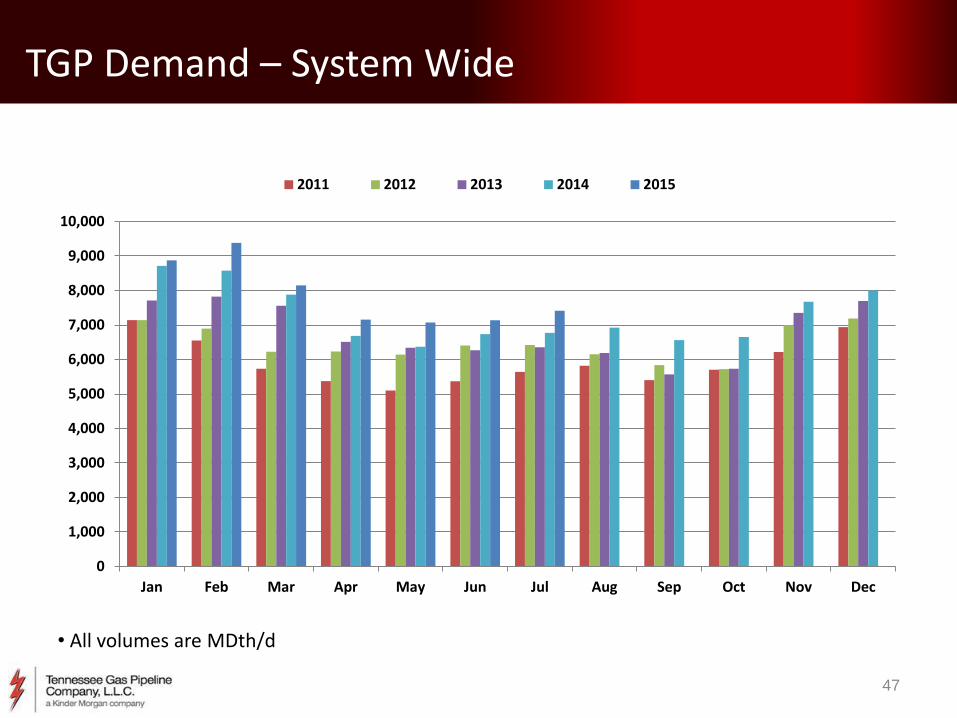

TGP Demand – System Wide

• All volumes are MDth/d

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2011 2012 2013 2014 2015

48

TGP Increasing Annual Throughput

*2015 through July

MD

th/d

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2010 2011 2012 2013 2014 2015 YTD

Z6

Z5

Z4

Z3

Z2

Z1

ZL

Z0

49

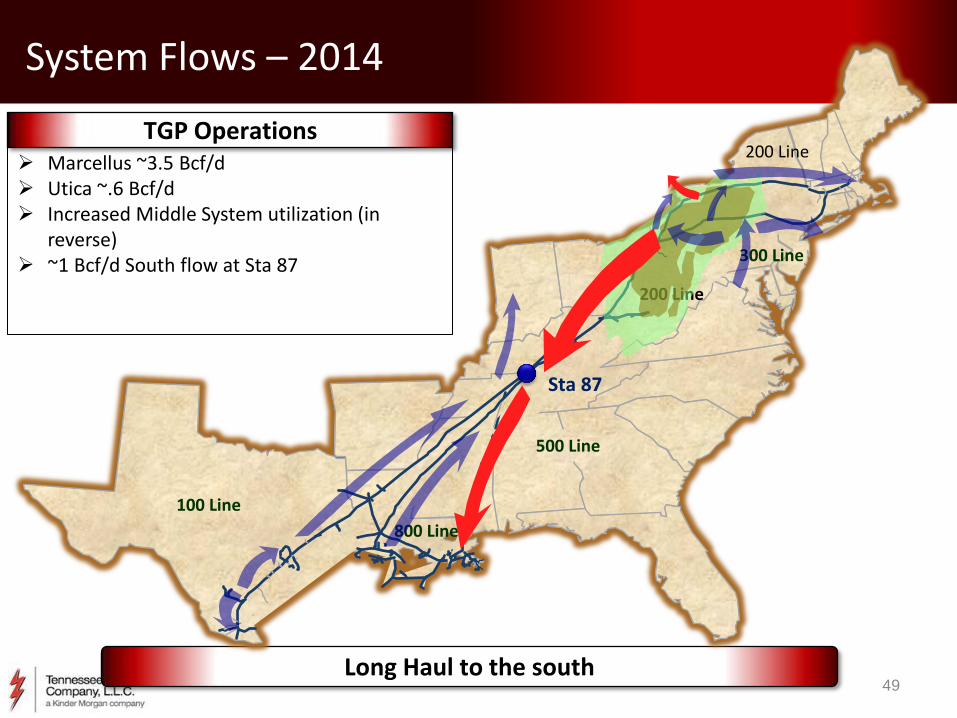

System Flows – 2014

Long Haul to the south

Marcellus ~3.5 Bcf/d Utica ~.6 Bcf/d Increased Middle System utilization (in

reverse) ~1 Bcf/d South flow at Sta 87

TGP Operations

800 Line

500 Line

200 Line

300 Line

100 Line

200 Line

Sta 87

50

System Flows – 2015

800 Line

500 Line

200 Line

300 Line

100 Line

200 Line

Long Haul to the south

Sta 87

Marcellus ~3.5 Bcf/d Bifurcated flows with long haul to the south Utica ~1 Bcf/d ~1.6 Bcf/d South flow at Sta 200 and ~1.5

Bcf/d at 87 Consistent exports to Mexico and Canada High system utilization- Maintenance

performed at mutually agreeable times

TGP Operations

51

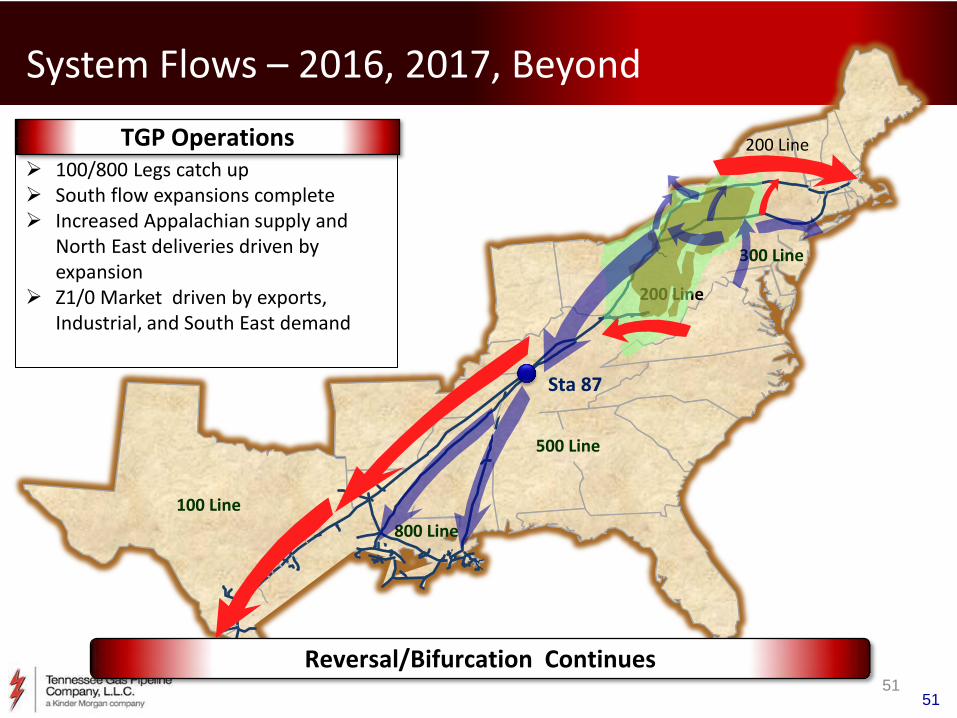

System Flows – 2016, 2017, Beyond

51

800 Line

500 Line

200 Line

300 Line

100 Line

200 Line

Reversal/Bifurcation Continues

Sta 87

100/800 Legs catch up South flow expansions complete Increased Appalachian supply and

North East deliveries driven by expansion

Z1/0 Market driven by exports, Industrial, and South East demand

TGP Operations

53

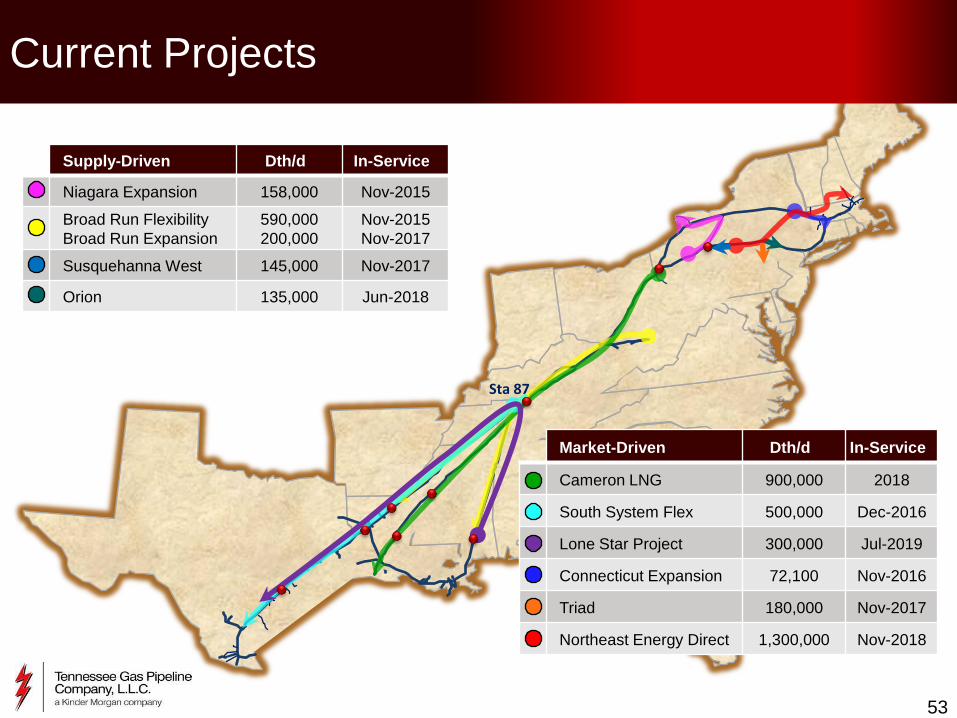

Sta 87

Supply-Driven Dth/d In-Service

Niagara Expansion 158,000 Nov-2015

Broad Run Flexibility

Broad Run Expansion

590,000

200,000

Nov-2015

Nov-2017

Susquehanna West 145,000 Nov-2017

Orion 135,000 Jun-2018

Market-Driven Dth/d In-Service

Cameron LNG 900,000 2018

South System Flex 500,000 Dec-2016

Lone Star Project 300,000 Jul-2019

Connecticut Expansion 72,100 Nov-2016

Triad 180,000 Nov-2017

Northeast Energy Direct 1,300,000 Nov-2018

Current Projects

54

Increase in new and redundant taps to minimize the impact of outages on customers without FT

Increased number of inquiries from power plants, LDCs, and related to pipeline expansions

Fewer producer inquiries for new facilities; increased number for upgrades to existing facilities

Projects in development — Marcellus Production: 6 Projects, 2.2 Bcf

• Top Receipts: Access Midstream (1,000 MMscf/d); Columbia Gas “Cobb” upgrade

(790 MMscf/d)

— Utica Production: 5 Projects, 658 MMscfd

• Top Receipts: M3 (290 MMscf/d)

— Deliveries: 10 Projects, 4.4 Bcf/d

• Top Deliveries: Columbia Gas “Milford” upgrade (349 MMcf/d), Iroquois Wright (950

MMcf/d), NET Mexico (500 MMcf/d), Cheniere Sinton (1,000 MMcf/d), Sempra (1,200

MMcf/d)

Interconnect Trends

55

Development Trends

Marcellus

Utica

LNG

Export

Canada

Southeast

New

England

Eagle Ford

Haynesville

Mexico

Supply-Push — Resolve remaining capacity

constraints

— Address new supply growth

— Connect supply to liquid trading points

Market-Pull — LNG export

— Pipeline export (Mexico, Canada)

— Power generation

— Shifting receipt points to match with supply

— Supply diversification

Reviewing “out of corridor” expansions

56

Connecting New Supply

LNG

Export

Southeast

NE-PA Marcellus — Relief coming from Atlantic

Sunrise, Constitution and NED

SW-PA, OH, WV Marcellus/Utica — Significant volumes committed to

Midwest markets

— Traditional long-haul pipes out of the region nearing completion of becoming bi-directional

Northeast supply still looking to connect with Gulf and Southeast markets

— 8+ Bcf/d of physical flow expected to reverse direction by 2024

— Combination of filling existing projects and new development

+18.6 Bcf/d

New

England Canada

Mexico

57

New England LDC & Power-Gen

Power Generation

— PJM

— NYISO

— Southeast

— ERCOT

LNG Export

— Gulf – MS

— Cameron – LA

— Golden Pass – TX

— Freeport – TX

— Brownsville – TX

Pipeline Export

— Mexico

— Canada

Connecting New Markets

Marcellus

Utica

Haynesville

Eagle Ford

+2.7

+6.9

+5.7 Bcf/d

+4.7 Bcf/d

Active Pursuits

58

BD Summary

Thank you for keeping us busy

New faces on the team

Focus on execution for our current project backlog — Ten major projects in development – 4.5 Bcf/d of new capacity

New project development transitioning from “producer-push” to “market-pull”

— Driven by lower commodity prices, LNG and Mexico export, and power generation growth

Northeast supply keeps coming (with no end in sight)

Significant projects carrying much of this supply out of the region – to Gulf/Export, Southeast, Midwest

— NED targets the New England market directly

59

59

Northeast Energy Direct

And Connecticut Expansion Update

Curtis Cole

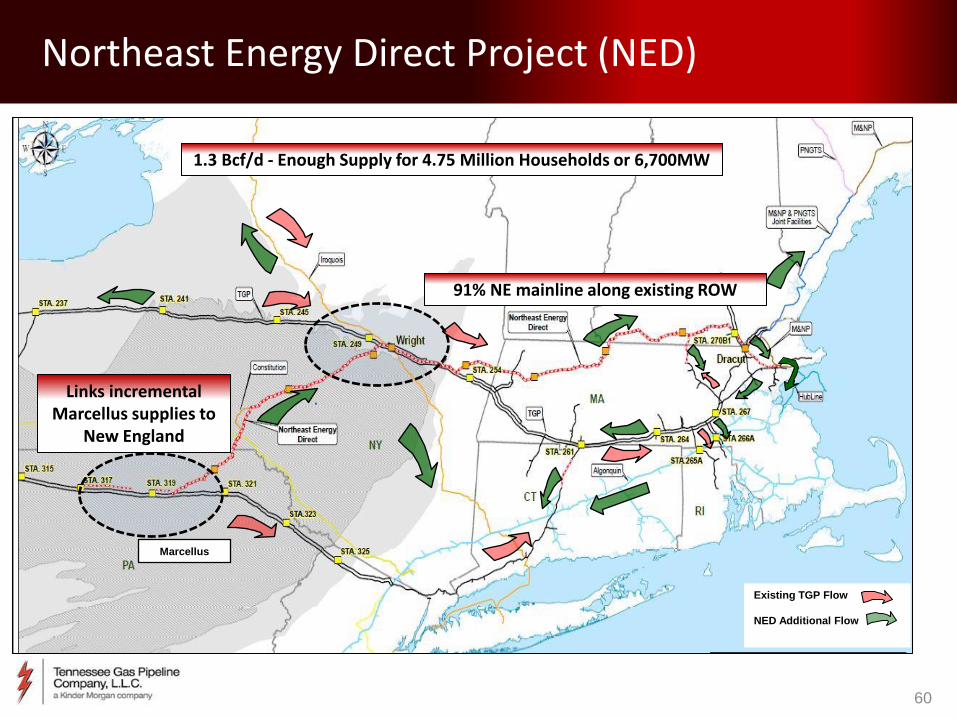

Northeast Energy Direct Project (NED)

60

Marcellus

Existing TGP Flow

NED Additional Flow

1.3 Bcf/d - Enough Supply for 4.75 Million Households or 6,700MW

91% NE mainline along existing ROW

Links incremental Marcellus supplies to

New England

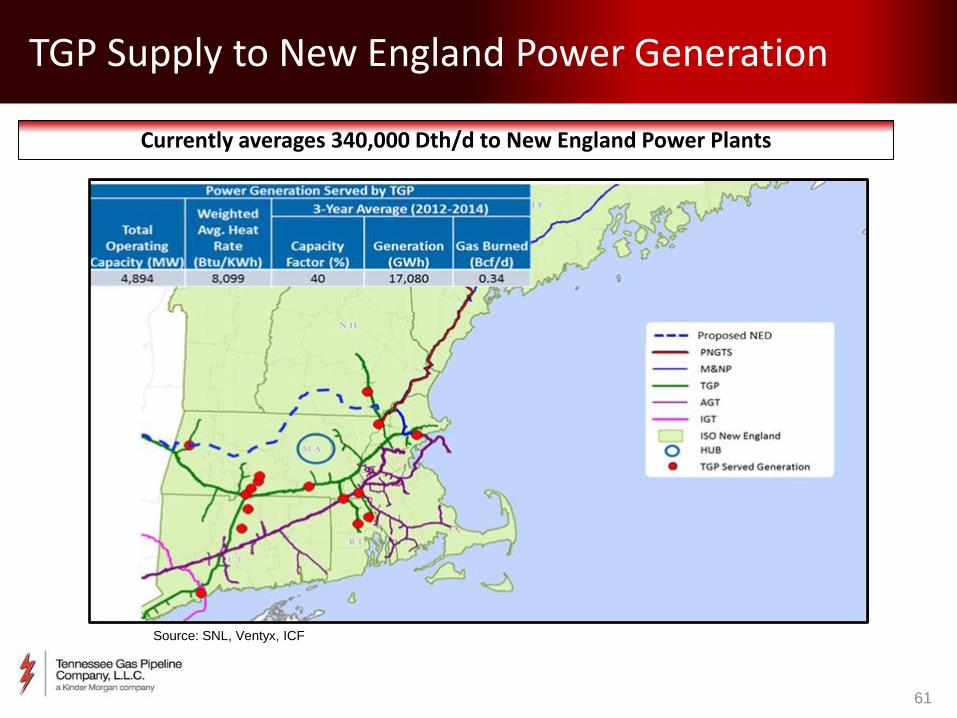

TGP Supply to New England Power Generation

61

Currently averages 340,000 Dth/d to New England Power Plants

Source: SNL, Ventyx, ICF

Northeast Energy Direct – The Right Solution for EDCs

62

TGP is an active participant in each of the New England State proceedings regarding the EDC solution for pipeline infrastructure

Provides EDC or generators with rate certainty and benefits

of scale

Services designed for power generation No-Notice Hourly flexibility Park & Loan options

NED Bridges Critical Gaps

63

Balanced approach to solving long-term energy needs includes: Large-scale renewables Enhanced Demand Reduction programs Expanding natural gas pipeline capacity to the region

Opportunity for EDC to lower energy costs and increase reliability to

gas and power grids Natural Gas-Fired Generation Supports Renewables

Integrated response: Not “either-or” Environmentally cleanest fossil fuel allows conversion Provides necessary and flexible backup source of generation to support

growth in wind and solar

Thanks to our committed project shippers

64

National Grid (MA) & (RI)

Liberty Utilities (Energy North Natural Gas) Corp. (NH)

Columbia Gas of Massachusetts (MA)

The Berkshire Gas Company (MA)

Connecticut Natural Gas Corporation (CT)

Southern Connecticut Gas Corporation (CT)

Westfield Gas & Electric (MA)

…and others

Executed over 550,000 Dth/d

of Anchor Shipper

Precedent Agreements

with key New England LDCs

NED Timeline

65

Milestone Date

Conduct open houses (complete) January - April 2015

FERC holds scoping meetings July- August 2015

File ER Draft #1 (Resource Reports 1 through 12) (complete) March 13, 2015

File ER Draft #2 (Resource Reports 1 through 12) July 2015

File certificate application with FERC (includes final ER) October 2015

FERC reviews application, conducts public comment meetings, addresses comments, prepares and issues draft and final EIS

October 2015- October 2016

Requested date for FERC certificate order October 2016

Accept certificate order November 2016

Commission issues permission to fell trees and start HDD’s January 2017

Start remaining construction April 2017

Anticipated in-service date for NED project (mainline and certain laterals) November 1, 2018

Milestone Date

NED Benefits

66

Critical component to any regional solution to address gas & electric reliability

Transformative solution that will lower gas and electricity prices for all New England consumers

Direct access to incremental supply from the most prolific shale play in the US

Vital enabler of renewables growth efforts

Provides incremental supply to all New England pipelines

Directly replaces declining Canadian imports

6

7

Capital: $85.7MM

Commercial Benefit: Additional capacity to serve New England market

Capacity: 72,100 Dth/d

Customers: Yankee, Southern Connecticut, Connecticut Natural

Estimated In-service: November 2016

Project Scope: 13.46 miles of pipeline loop Acquisition of Thompsonville

Lateral

Project Status: Contracts executed Lateral acquired FERC certificate filed July 2014

Docket CP14-529-000 MEPA certificate received

Connecticut Expansion Project