Embed Size (px)

Citation preview

Taxes and Revenue in Texas

GOVT 2306

This section outlines the various sources of revenue in the state.

By running through this, you should get an idea of what types of taxes are imposed in the state, and what other way the state of Texas

obtains revenue.

The material here is drawn from various sources.

One is Chapter Two of the Fiscal Size Up: Revenue Sources and

Economic Outlook.

You can access the document by clicking here – it takes you to the Legislative Budget Board

– then hit “Budget” on the drop down menu, then “Fiscal Size Up.”

Another is this document created by the

House Research Organization: Sources of State Revenue in Texas.

This page from the Comptroller’s Office – Texas Taxes – should also

be helpful.

Among other things – the Comptroller is the

official tax collector for the state.

Still another is Article 8 of the Texas Constitution

It covers Taxation and Revenue

We will run through the subject of Article 8 and then the previous

documents.

Section One: EQUALITY AND UNIFORMITY; TAX IN PROPORTION

TO VALUE; INCOME TAX; EXEMPTION OF CERTAIN TANGIBLE

PERSONAL PROPERTY FROM AD VALOREM TAXATION.

This section allows for the collection of sales taxes – ad valorem taxation - by the state and

local governments.

Taxess have to be uniform throughout the state.

It details what entities are exempt from sales taxes – there’s lots of language concerning exemptions. This is a common subject of

amendments.

Section One contains over a dozen subsections detailing exemptions to sales

and property taxes that have been authorized by voters in past elections.

A handful of more exemptions are proposed in the

amendments offered in the election of November 2013

.

Of special note is the homestead exemption which is the

subject of Section 1-b.

The state is protective of primary residences.

Note also that Section 1-e prevents the state from levying property taxes – they are reserved

for local governments.

Sec. 1-e. ABOLITION OF AD VALOREM PROPERTY TAXES. No State ad valorem taxes shall be levied

upon any property within this State.

Section Two: OCCUPATION TAXES; EQUALITY AND UNIFORMITY;

EXEMPTIONS FROM TAXATION

Section Three: GENERAL LAWS; PUBLIC PURPOSES.

Taxes shall be levied and collected by general laws and for public

purposes only.

Section Four: SURRENDER OR SUSPENSION OF TAXING POWER.

The power to tax corporations and corporate property shall not be

surrendered or suspended by act of the Legislature, by any contract or grant to which the State shall be a

party.

Section Five was repealed in 1999

Section Six: WITHDRAWAL OF MONEY FROM TREASURY; DURATION OF

APPROPRIATION.

No money shall be drawn from the Treasury but in pursuance of specific

appropriations made by law; nor shall any appropriation of money be made

for a longer term than two years.

Section 7: BORROWING, WITHHOLDING, OR DIVERTING

SPECIAL FUNDS.

The Legislature shall not have power to borrow, or in any manner divert from its purpose, any special fund that may, or ought to, come into the Treasury; and shall make it penal for any

person or persons to borrow, withhold or in any manner to divert from its purpose any special

fund, or any part thereof.

Sec. 7-a. REVENUES FROM MOTOR VEHICLE REGISTRATION FEES AND

TAXES ON MOTOR FUELS AND LUBRICANTS; PURPOSES FOR

WHICH USED.

Sec. 7-b. REVENUES FROM FEDERAL REIMBURSEMENT;

PURPOSES FOR WHICH USED.

Section 8: RAILROAD COMPANIES; ASSESSMENT AND COLLECTION OF

TAXES.

All property of railroad companies shall be assessed, and the taxes collected in the several

counties in which said property is situated, including so much of the roadbed and fixtures as

shall be in each county.

Section 9: MAXIMUM STATE TAX; COUNTY, CITY, AND TOWN LEVIES;

COUNTY FUNDS; LOCAL ROAD LAWS.

(a) No county, city or town shall levy a tax rate in excess of Eighty Cents ($ .80) on the One

Hundred Dollars ($100) valuation in any one (1) year for general fund, permanent improvement

fund, road and bridge fund and jury fund purposes.

This section caps the tax rates local governments can charge.

Section 10: RELEASE FROM PAYMENT OF TAXES.

The Legislature shall have no power to release the inhabitants of, or property in, any county, city or town from the payment of taxes levied for State or county purposes, unless in case of

great public calamity in any such county, city or town, when such release may be made by a vote

of two-thirds of each House of the Legislature.

Section 11: PLACE OF ASSESSMENT; VALUE OF PROPERTY NOT RENDERED BY OWNER.

All property, whether owned by persons or corporations shall be assessed for taxation, and the

taxes paid in the county where situated, but the Legislature may, by a two-thirds vote, authorize the payment of taxes of non-residents of counties to be

made at the office of the Comptroller of Public Accounts. And all lands and other property not

rendered for taxation by the owner thereof shall be assessed at its fair value by the proper officer.

Sec. 12. (Repealed Aug. 5, 1969.)

Section 13: SALES OF LANDS AND OTHER PROPERTY FOR TAXES;

REDEMPTION.

(a) Provision shall be made by the Legislature for the sale of a

sufficient portion of all lands and other property for the taxes due thereon that have not been paid.

You can lose your land if you do not pay taxes on it.

Section 14: ASSESSOR AND COLLECTOR OF TAXES.

The qualified voters of each county shall elect an assessor-collector of

taxes for the county, except as otherwise provided by this section.

The tax assessor is a locally elected political office.

Section 15: LIEN OF ASSESSMENT; SEIZURE AND SALE OF PROPERTY.

The annual assessment made upon landed property shall be a special lien thereon; and all property, both

real and personal, belonging to any delinquent taxpayer shall be liable to seizure and sale for the

payment of all the taxes and penalties due by such delinquent; and such property may be sold for the

payment of the taxes and penalties due by such delinquent, under such regulations as the Legislature

may provide.

Sec. 16. (Repealed Nov. 6, 2001.)

Section 17: SPECIFICATION OF SUBJECTS NOT LIMITATION OF

LEGISLATURE'S POWER.

The specification of the objects and subjects of taxation shall not deprive the Legislature of the power to require other subjects or objects to be taxed in such manner as may be consistent with

the principles of taxation fixed in this Constitution.

Section 18: EQUALIZATION OF VALUATIONS; SINGLE APPRAISAL.

The Legislature shall provide for equalizing, as near as may be, the valuation of all

property subject to or rendered for taxation, and may also provide for the

classification of all lands with reference to their value in the several counties.

Section 19: FARM PRODUCTS, LIVESTOCK, POULTRY, AND FAMILY

SUPPLIES; EXEMPTION.

Farm products, livestock, and poultry in the hands of the producer, and family supplies for home and farm use, are

exempt from all taxation until otherwise directed by a two-thirds vote of all the members elect to both houses of the

Legislature.

Section 20: FAIR CASH MARKET VALUE NOT TO BE EXCEEDED;

DISCOUNTS FOR ADVANCE PAYMENT.

No property of any kind in this State shall ever be assessed for ad valorem taxes at a

greater value than its fair cash market value nor shall any Board of Equalization of any governmental or political subdivision or taxing district within this State fix the value of any property for tax purposes at more than its fair cash market value. . .

Section 21: INCREASE IN TOTAL PROPERTY TAXES; NOTICE AND

HEARING; CALCULATION.

Subject to any exceptions prescribed by general law, the total amount of property taxes imposed

by a political subdivision in any year may not exceed the total amount of property taxes

imposed by that subdivision in the preceding year unless the governing body of the

subdivision gives notice of its intent to consider an increase in taxes and holds a public hearing on the proposed increase before it increases

those total taxes.

Section 22: RESTRICTION ON APPROPRIATIONS.

In no biennium shall the rate of growth of appropriations from state tax revenues not dedicated by this constitution exceed the

estimated rate of growth of the state's economy. The legislature shall provide by general law procedures to implement this

subsection.

This places a cap on the rate of growth of state government.

Section 23: APPRAISAL OF PROPERTY; ENFORCEMENT OF

STANDARDS.

There shall be no statewide appraisal of real property for ad valorem tax purposes; however, this shall not preclude formula distribution of tax revenues to political

subdivisions of the state.

Section 24: PERSONAL INCOME TAX; DEDICATION OF PROCEEDS.

(a) A general law enacted by the legislature that imposes a tax on the net incomes of natural persons,

including a person's share of partnership and unincorporated association income, must provide that the portion of the law imposing the tax not take effect until approved by a majority of the registered voters

voting in a statewide referendum held on the question of imposing the tax. The referendum must specify the

rate of the tax that will apply to taxable income as defined by law.

This section states that an income tax cannot be imposed on the

state unless it is approved by the voters in a statewide referendum.

It does not prohibit a state income tax, but creates a high bar for it to

be imposed.

Texas is one of a small number of states that do not collect

state income taxes.

States with no state income tax.

That’s enough for the Article 8 of the Texas Constitution.

Now let’s run through detail from other sources for info on state

taxes.

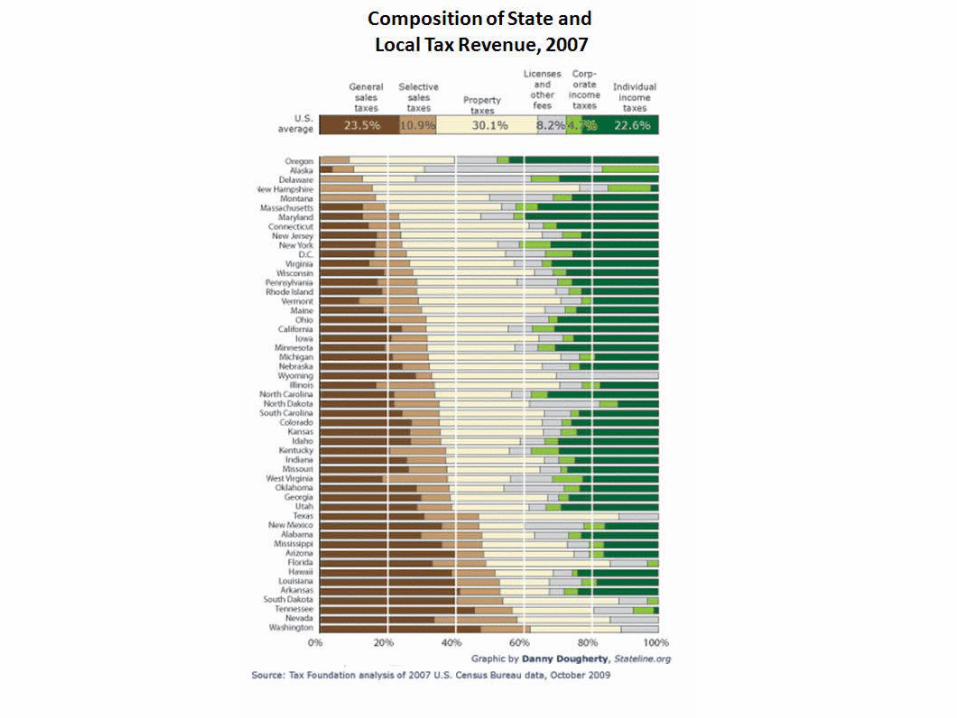

These two graphics should help get a preliminary idea of where funds

are collected in the state.

They are from the Fiscal Size Up 2012-13.

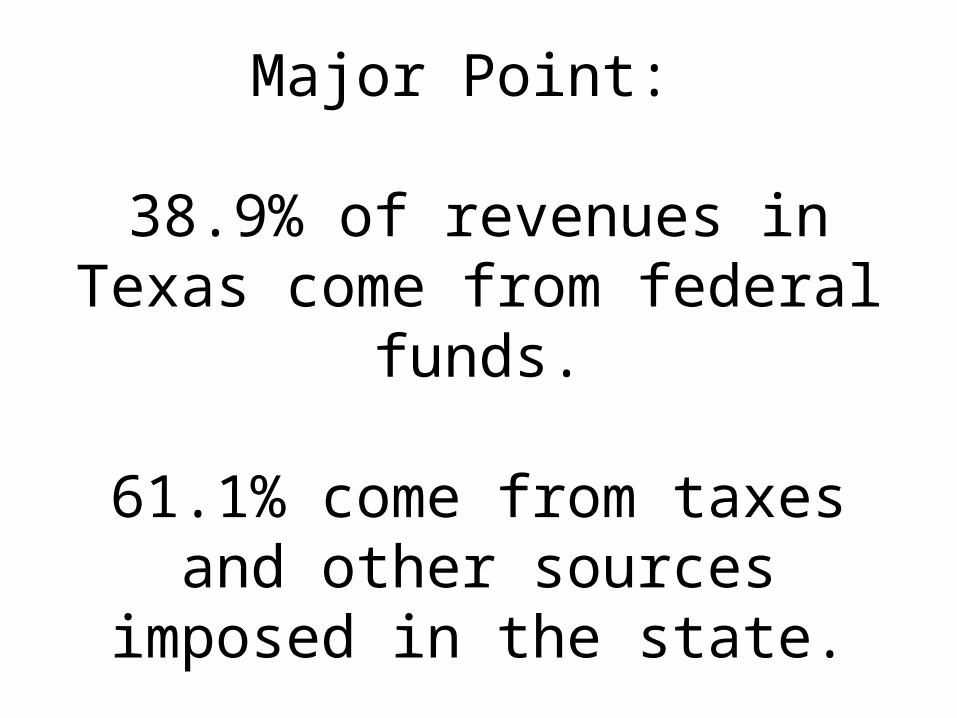

Major Point:

38.9% of revenues in Texas come from federal funds.

61.1% come from taxes and other sources imposed in the state.

Here’s a little background on Federal Funds.

Federal Funds are distributed to the state largely through grant in aid programs

unique to each spending item.

They are used to entice states – or compel them – to provide services they might not otherwise. Often these are programs that

provide benefits to the poor.

States might not otherwise provide those policies.

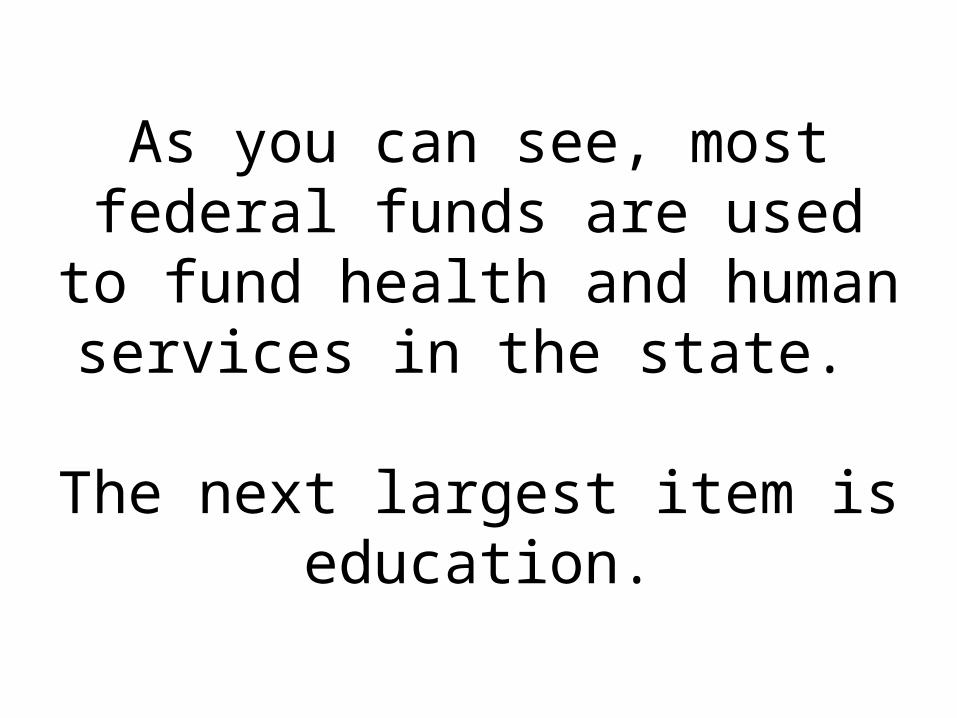

The next slide shows where federal funds are spent in the state.

As you can see, most federal funds are used to fund health and human

services in the state.

The next largest item is education.

The Supreme Court has ruled that control over these funds can be used by the

national government to influence state policy. Controversies exist depending on the degree of discretion given to states in how they can implement a given policy.

Are there conditions attached to these items?

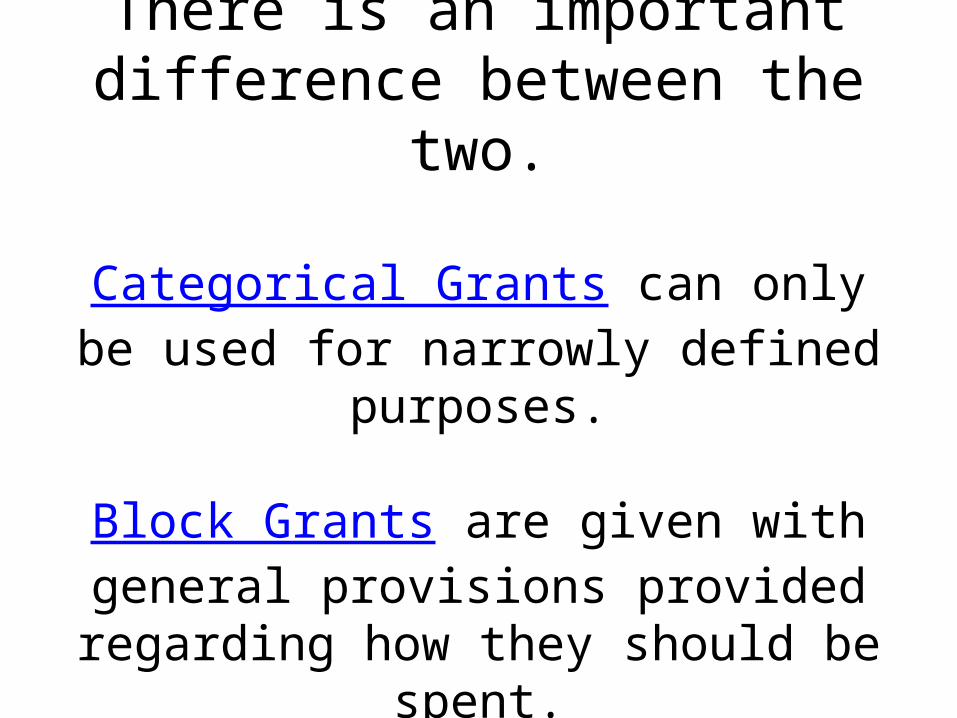

Here are two types of grants:

Categorical GrantsBlock Grants

There is an important difference between the two.

Categorical Grants can only be used for narrowly defined purposes.

Block Grants are given with general provisions provided regarding how they

should be spent.

Texas tends to prefer block grants to categorical grants.

It makes sense since it gives the states more control than they

would otherwise have.

Now for a closer look at the way revenue is collected in Texas.

Not all revenue is collected in taxes.

Some is collected in fees, fines, income and other sources.

Here’s a run through:

Taxes

Sales TaxOil and Gas Production Taxes

Motor Fuels TaxMotor Vehicle Sales and Rental Tax

Franchise TaxCigarette and Tobacco Taxes

Alcoholic Beverage TaxesInsurance Occupation Taxes

Utility TaxInheritance Tax

Hotel Occupancy Tax

Plus “other taxes”

“Other taxes” are levied on a variety of items such as cement, sulphur, attorney services, coin-operated

machines, and bingo rental receipts. CPA estimates these taxes will generate $375.1 million in the 2012–13

biennium, an increase of 9.0 percent from 2010–11 biennial collections of $344.2 million.

Here is a list of non-tax revenues

Federal ReceiptsFees, Fines, Licenses, and Penalties

Interest and Investment IncomeLottery Revenue

Land IncomeTobacco Settlement Revenue

Plus “other revenue”

The remaining $9.7 billion, or 5.3 percent, of state revenue comes from a variety of sources: sales of

goods and services, child support collections, revenue from unclaimed property, settlement of claims, and

various federal programs. CPA estimates that collections of other revenue in the 2012–13 biennium

will be 0.8 percent less than the 2010–11 biennial collections.

Here’s a quick run through the types of taxes that are collected in

the state.

The number in parenthesis is the percentage of state revenues

collected by that tax.

Sales Taxes (24.8%)

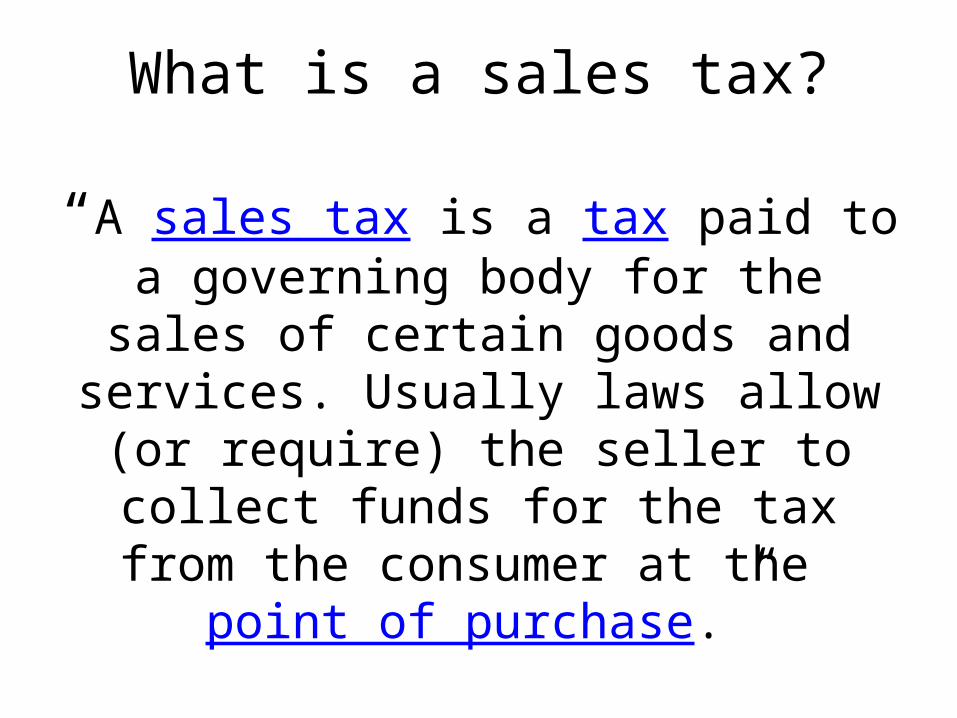

What is a sales tax?

“A sales tax is a tax paid to a governing body for the sales of certain goods and

services. Usually laws allow (or require) the seller to collect funds for the tax from the

consumer at the point of purchase.”

A sales tax is a type of excise tax, which collects revenue by adding a

cost to various items that are sold on the market. They are imposed by the

producer or retailer, and indirectly paid by the consumer.

Some items are exempt from taxes, notable items that are considered to

be essential, like non-processed food.

“The sales and use tax continues to comprise most of the state’s tax revenue.

The current state tax rate is 6.25 percent, the same rate in place since 1990. Subject to certain exemptions, the state sales and use tax is imposed on retail sales, leases, and rentals of goods purchased within or

brought into the state, as well as some taxable services.”

Click here for the page in the Comptroller’s website on

sales and use taxes.

Texas allows other – lower – levels of government to collect sales taxes as well,

but places a limit on how much can be collected in total:

Texas cities, counties, transit authorities and special purpose districts have the

option of imposing an additional local sales tax for a combined total of state and local

taxes of 8 1/4% (.0825)

Sales taxes are controversial because they are argued to be regressive. The poor pay

a higher percentage of their income in sales taxes than the wealthy.

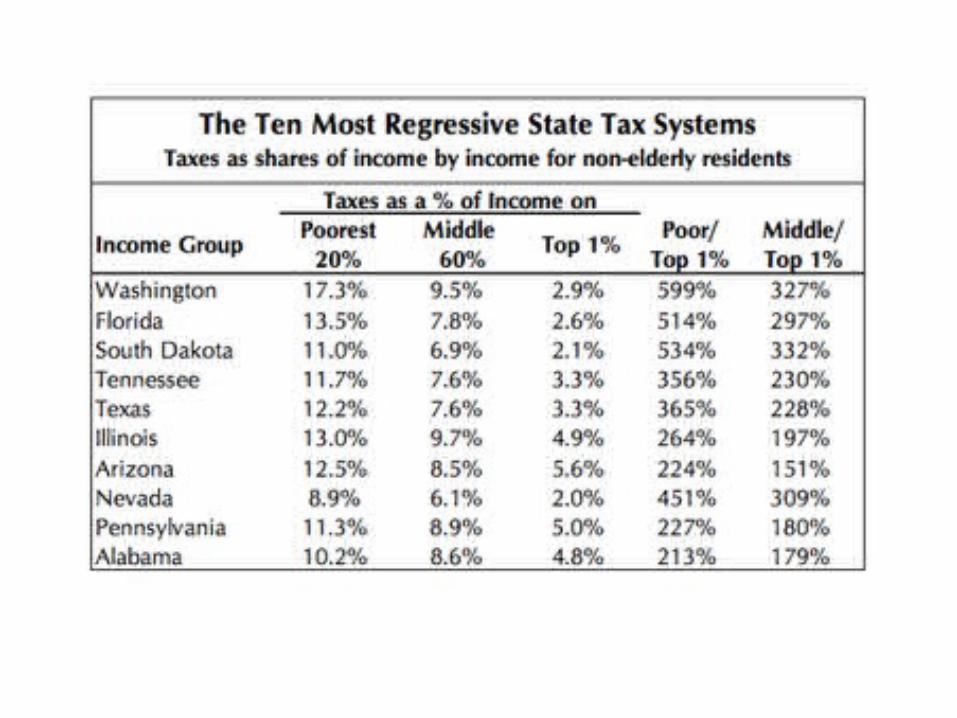

I can’t really vouch for the numbers on the following chart, but it shows the

percentage of income paid in sales taxes by different income categories.

From The Hill: “Practically every state charges a higher share of taxes from lower- and middle-class families than the highest earners, a new

study from a liberal-leaning group found.

The Institute on Taxation and Economic Policy found that the bottom 20 percent of earners paid an effective tax rate of 11.1 percent to state and local governments, while the top-earning quintile paid about half as much, 5.6 percent. The middle 20 percent pays a rate of

9.4 percent.”

Since many states use sales taxes, state tax systems are commonly argued to be more regressive than those on the national level.

The national government uses the income tax, which tends to be progressive. The

higher the income, the higher the tax. We cover this in GOVT 2305, but

click here for a reminder of how the national income tax is collected.

Franchise Tax (4.5%)

What is a franchise tax?

A tax levied at the state level against businesses and partnerships chartered within that state. In some states, companies with operations in that state may also be liable for the tax even if they

are chartered in another state. This is a privilege tax that gives the business the right to be

chartered and/or operate within that state.

The Comptroller’s Office defines the Franchise Tax this way: “The Texas franchise tax is a privilege tax

imposed on corporations, including banking corporations and limited liability companies, that are chartered in Texas.

The tax is also imposed on non-Texas corporations that do business in Texas.”

The current franchise tax was established in 2006 in a special session of the 79th Legislature. The value of businesses

subject to taxation was changed. This has been controversial every since because the

revenue collected from the revision was lower than what was collected before.

Click here for background on the controversy associated with the franchise tax

.

The margins tax replaced the franchise tax in 2006, when the 79th Legislature, in its third called session, enacted HB 3 by J. Keffer. The margins tax was designed to generate more

revenue by applying to a broader base of businesses. According to the comptroller, the

new tax applied to 180,000 more business entities and lowered the tax rate that taxable businesses would pay. It was created to help generate revenue for the Property Tax Relief

Fund, which helps the state pay for reductions in local school district property taxes.

In fiscal 2008-09, the margins tax generated $8.7 billion. In fiscal 2010-11, it is expected to generate $5.8 billion, and in fiscal 2012-13, $5.3 billion. According to

studies by the comptroller’s business tax advisory commission, the tax is bringing in less revenue because

more businesses than anticipated are calculating it using total revenue minus cost of goods sold.

Proposals to change the margins tax include clarifying what can and cannot be claimed under the various

exemptions, increasing the rates on which the margin is taxed, and expanding the types of business entities

required to pay the tax.

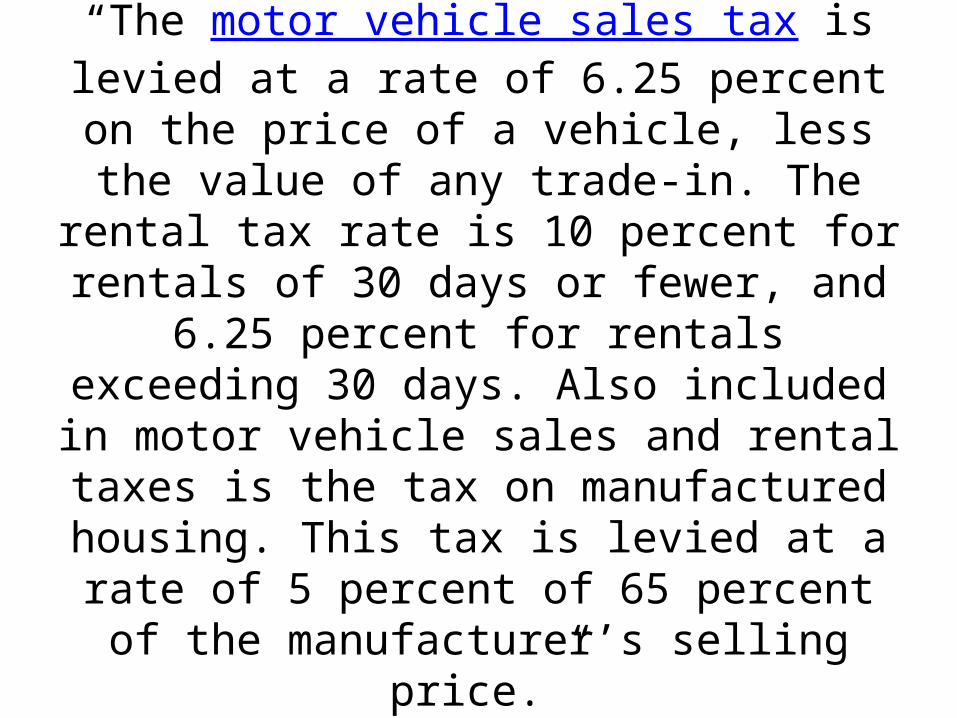

Motor Vehicle Sales and Rental Taxes (3.5%)

“The motor vehicle sales tax is levied at a rate of 6.25 percent on the price of a vehicle, less the value of any trade-in. The rental tax rate is 10

percent for rentals of 30 days or fewer, and 6.25 percent for rentals exceeding 30 days. Also

included in motor vehicle sales and rental taxes is the tax on manufactured housing. This tax is

levied at a rate of 5 percent of 65 percent of the manufacturer’s selling price.”

Motor Fuel Taxes (3.4%)

“Texas taxes three major types of motor fuel: gasoline, diesel fuel, and liquefied petroleum gas (LPG—propane, butane, or

compressed natural gas). Currently, gasoline and diesel fuel are taxed $0.20 per gallon; LPG is taxed at a rate of $0.15 per gallon.

In the 2010–11 biennium, motor fuels tax collections totaled $6.1 billion. CPA estimates that fuel tax collections will grow 2.6

percent, forecasting $6.3 billion in revenue for the 2012–13 biennium. Historically, motor fuel taxes have accounted for about 10 percent to 12 percent of total state tax collections;

however, in the 2010–11 biennium the motor fuel taxes accounted for only 8.3 percent of total tax collections. Motor fuel taxes are expected to comprise 7.8 percent of total tax

collections for the 2012–13.”

Severance Taxes (2.6%)

What is a Severance Tax?

Severance taxes are incurred when non-renewable natural resources are extracted (or severed) within a taxing jurisdiction. Resources that typically

incur severance taxes when extracted are oil, natural gas, coal, uranium, and

timber. Some jurisdictions use other terms like gross production tax.

In Texas, this applies mostly to:

Oil and Gas Production Taxes

The state levies an oil production tax at 4.6 percent of value, a natural gas production tax at 7.5 percent of

value, and an oil regulation tax of three-sixteenths of one cent per barrel of oil produced. During the 2010–11 biennium, annual oil production was approximately

324.8 million barrels in fiscal year 2010 and 377.7 million barrels in fiscal year 2011. Oil was taxed at a

price of approximately $72.75 per barrel in fiscal year 2010 and $87.85 per barrel in fiscal year 2011. Annual

natural gas production was 7.1 trillion cubic feet in fiscal year 2010 and 7.3 trillion cubic feet in fiscal year 2011, while taxable natural gas prices were $3.96 per

thousand cubic feet (mcf) in fiscal year 2010, and approximately $4.13 per mcf in fiscal year 2011.

This is the source of funds that are deposited into the rainy day fund.

Otherwise known as the Economic Stabilization Fund.

Cigarette and Tobacco Taxes (1.6%)

From the Comptroller’s office: A tax is imposed on cigars and

tobacco products when a permit holder receives them for the

purpose of making a first sale in this state

Excise taxes on tobacco products and alcoholic beverages are among the oldest and most common taxes in the world. Texas has taxed liquor since the days of the republic and cigarettes

since the Great Depression. All 50 states and the federal government impose these so-called “sin” taxes.

Tobacco and alcohol taxes. Texas levies two separate tobacco taxes — one on cigarettes and another on cigars and other

tobacco products, including chewing tobacco, smoking tobacco, and snuff. Taxes on cigarettes are levied per package.Taxes on cigars and other tobacco products are set by weight. The state

levies separate taxes on package sales of liquor (distilled spirits), beer, malt liquor, and wine and on by-the-drink sales of mixed

drinks.

Most tobacco and alcohol tax revenue goes into the General Revenue Fund. Some tobacco tax revenues are dedicated to special purposes,

such as to property tax relief or to the Physician Education Loan Repayment Program. The

program provides loan repayment funds to physicians who agree to practice in a Health

Professional Shortage Area, usually an underserved rural area, for at least four years.

Cigarette and alcohol – along with others like the pole tax – are focused on

behaviors considered by some to be undesirable.

The revenue is sometimes earmarked for projects associated with the consequences of the activity – like lung cancer research

or funding for victims of domestic violence.

Some argue that Texas could increase revenue by legalizing and

taxing casino gambling and marijuana.

While this may be true, there are political forces opposed to both

moves.

Insurance Occupation Taxes (1.6%)

Alcoholic Beverage Taxes (1.0%)

From the Comptroller: A gross receipts tax is imposed on the amount received from the sale, preparation or service of mixed beverages and from the sale, preparation or service of ice or

nonalcoholic beverages that are sold, prepared or served for the purpose of being mixed with an alcoholic beverage and consumed on the premises of the mixed beverage permittee.

This is also considered a sin tax.

Utility Tax (0.5%)

Hotel Occupancy Tax (0.4%)

From the Comptroller: A tax is imposed on a person who pays for a room or space in a hotel costing $15 or more each day. Local hotel taxes

apply to sleeping rooms costing $2 or more each day. The tax covers hotels, motels and bed and

breakfasts, as well as condominiums, apartments and houses rented for less than 30 consecutive days. Persons leasing their houses

or rooms in their house must collect hotel occupancy tax from their customers, in the

same way a hotel or motel collects the tax from its patrons.

These are popular taxes – especially in municipalities –

because they impose taxes on visitors, not residents.

Inheritance Tax (0.0%)

Texas once had an estate tax, but it is being phased out.

No Texas inheritance tax is due on estates with date of death on or

after January 1, 2005.

Two links from the Comptrollers office explain the shift here and

here.

Other Taxes

“Other taxes” are levied on a variety of items such as cement, sulphur, attorney services, coin-

operated machines, and bingo rental receipts. CPA estimates these taxes will generate $375.1 million in the 2012–13 biennium, an increase of 9.0 percent from 2010–11 biennial collections of

$344.2 million.

Non Tax Revenues

As you probably guessed, these are revenues received by the state

through sources other than taxes

Fees, Fines, Licenses, and Penalties

These accounted for 8.2% of total revenue in 2012-2013.

Interest and Investment Income

This accounted for 1% of total 2012-2013 revenue

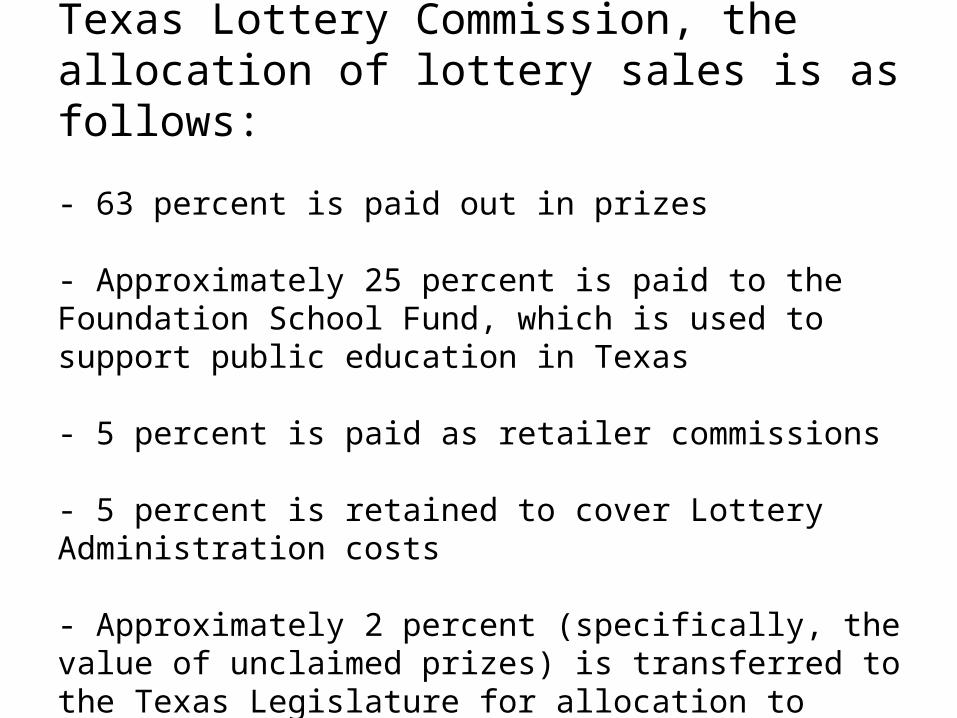

Lottery Revenue

1.9% of state revenue came from the sale of lottery tickets.

Click here for the Wikipedia on Texas Lottery.

The voters approved an amendment to the Texas

Constitution in November 1991 authorizing lottery sales in Texas.

It is overseen by the Texas Lottery Commission, which was

established in 1993.

From Wikipedia: According to the Texas Lottery Commission, the allocation of lottery sales is as follows:

- 63 percent is paid out in prizes

- Approximately 25 percent is paid to the Foundation School Fund, which is used to support public education in Texas

- 5 percent is paid as retailer commissions

- 5 percent is retained to cover Lottery Administration costs

- Approximately 2 percent (specifically, the value of unclaimed prizes) is transferred to the Texas Legislature for allocation to other programs in Texas

Controversy: The lottery was sold as benefiting public education, but

is it really?

- Lottery a tiny share of school funding.- Is the Texas Lottery really funding education?

- Texas School Funding at a Glance.- Transfers top $15 billion.

Land Income

This accounted for 0.8% of state 2012-2013 revenue

Tobacco Settlement Revenue

From the TDSHS: In 1996, Texas filed a federal lawsuit accusing the tobacco industry of

violating conspiracy, racketeering, consumer protection, and other provisions of state and

federal law. The state sought to recover billions of tax dollars it had spent to treat tobacco-related illnesses. In settling the lawsuit, the

industry agreed to pay the state $15 billion over 25 years and to pay about $2.3 billion through 2003 to Texas counties and hospital districts

based on their provision of indigent health care.

Other Revenue

The remaining $9.7 billion, or 5.3 percent, of state revenue comes from a variety of sources:

sales of goods and services, child support collections, revenue from unclaimed property,

settlement of claims, and various federal programs. CPA estimates that collections of

other revenue in the 2012–13 biennium will be 0.8 percent less than the 2010–11 biennial

collections.

This is plenty.

Hopefully this section gives you an idea of the nature of taxation in

the state.