Embed Size (px)

Citation preview

Taxation of Investments - 2010

Anne Simpson, (Moderator) Allstate Insurance Company

Eric Bisighini, Hartford Life Insurance Co.

Jeff Callender, Deloitte Tax LLP

Biruta Kelly, Scribner, Hall & Thompson, LLP

2

1. Emerging IRS issues– Bad Debts

2. Gain Generation– Identified Mixed Straddles– Wash Sale Gains

3. Recent Developments – Section 1256 – Market-to-Market Rules– Hedging/Straddles– Anschutz

Overview

1. Emerging IRS Issues

Section 166 – Bad Debt Deduction

3

4

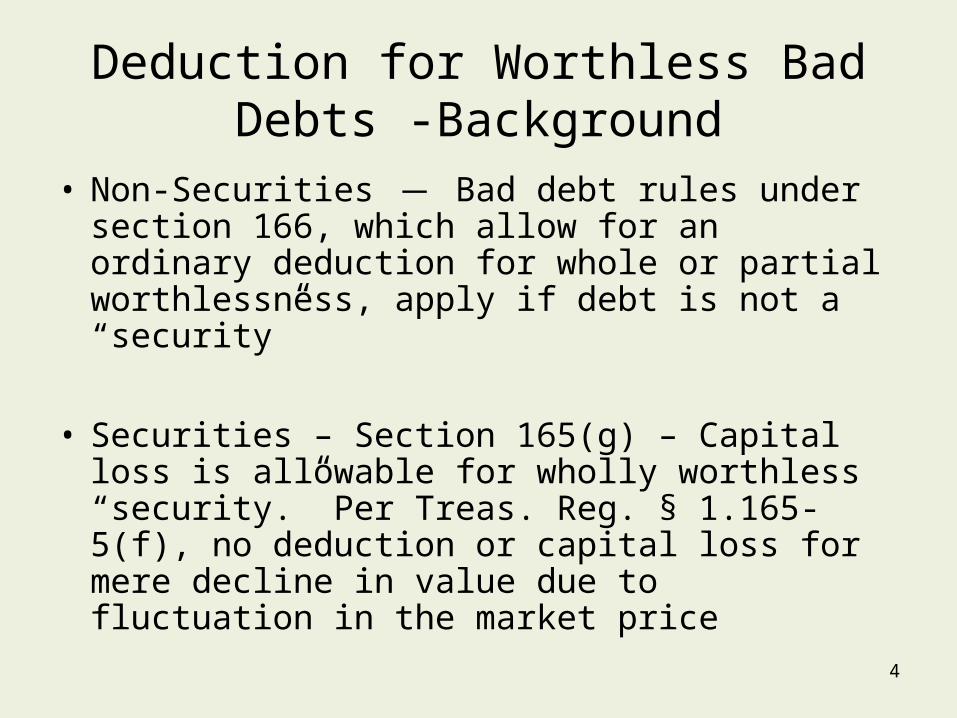

Deduction for Worthless Bad Debts -Background

• Non-Securities : Bad debt rules under section 166, which allow for an ordinary deduction for whole or partial worthlessness, apply if debt is not a “security”

• Securities – Section 165(g) – Capital loss is allowable for wholly worthless “security.” Per Treas. Reg. § 1.165-5(f), no deduction or capital loss for mere decline in value due to fluctuation in the market price

5

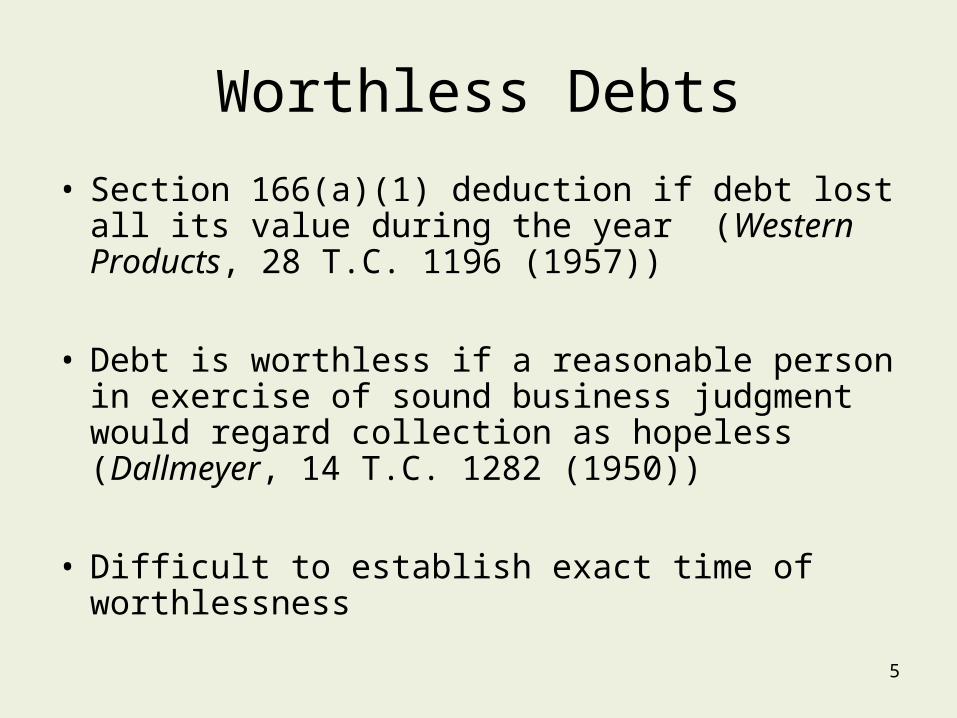

Worthless Debts

• Section 166(a)(1) deduction if debt lost all its value during the year (Western Products, 28 T.C. 1196 (1957))

• Debt is worthless if a reasonable person in exercise of sound business judgment would regard collection as hopeless (Dallmeyer, 14 T.C. 1282 (1950))

• Difficult to establish exact time of worthlessness

6

Partially Worthless Debts

• Sec. 166(a)(2) allows deduction for partially worthless debt

• Charge-off on books required for the taxable year of deduction

• IRS has broad discretion in allowing deduction for partial worthlessness Treas. Reg. §1.166-3(a)(2)(iii), (Stranahan, 42 F. 2d 729 (8th Cir. 1930), (plainly arbitrary or unreasonable), PepsiAmerica, 52 Fed. Cl. 41 (Ct. Fed. Cl. 2002) (rational basis)

Partially Worthless Debts (continued)

• In general, statutory guidelines require cost basis of assets to be charged off if the loss of principal is “other than temporary” – not same as tax standard, which is a worthlessness standard

7

8

SSAP 43R• Provides standards for write-downs of loan-

backed and structured securities (for additional guidelines, see SSAPs 26, 34, 36, 37)

• The unrealized loss that is interest-related is written down/off where there is an intent to sell or the holder does not have the intent and ability to hold for long enough to recover amortized cost basis

• The unrealized loss that is credit-related is written down/off if there is an other-than-temporary impairment (measured by discounted projected cash flows as compared to amortized cost basis).

9

Special Rule for Regulated Companies

• Treas. Reg. § 1.166-2(d) – conclusive presumption of worthlessness

• Applies to bank or “other corporation” which is subject to supervision by Federal authorities or by State authorities maintaining substantially equivalent standards

10

Special Rule for Regulated Companies (continued)

• Applies to insurance companies per Credit Life Insurance Co., (Claims Court oral bench opinion, rev’d on other grounds) 948 F. 2d 723 (Fed. Cir. 1991) (taxpayer did not claim bad debt deduction on its return).

• Conclusive presumption applies to accrued interest (Rev. Rul. 2007-32).

11

Special Rule for Regulated Companies (continued)

• The charge-off must be under (1) the “specific order” of regulators or (2) in accordance with established policies and upon regulatory audit with written confirmation that the charge-off would have been under specific orders if the audit had been made on the date of the charge-off (Treas. Reg. § 1.166-2(d)(1))

12

Special Rule for Regulated Companies (continued)

• The charge-off must be claimed as a deduction at the time of filing the return (Treas. Reg. § 1.166-2(d)).

• If not deducted in year of charge-off, may be claimed later with sufficient evidence of later worthlessness (see Treas. Reg. § 1.166-2(d)(2))

13

Check List ofIssues for Partial Bad Debt

Write Off• Is it a debt?

• Is it a non-security?

– “Security” defined as: stock or stock subscription in a corporation or bond, debenture, note or certificate or other evidence of indebtedness issued by a corporation or by a government with interest coupons or in registered form (REMIC regular interest treated as non-corporate debt for tax purposes (sections 860A and B))

14

Issues (continued)

• Is it worthless : Does conclusive presumption extend to insurance companies?– IRS National Office considering scope of

conclusive presumption

• Is insurance company an “other corporation” per Treas. Reg. §1.166-2(d)(1)?

• Is it subject to supervision by State authorities maintaining substantially equivalent standards?

Issues (continued)

– Was charge off ordered by regulators?

– Was charge off deducted on return?

15

• Are requirements of conclusive presumption met?

16

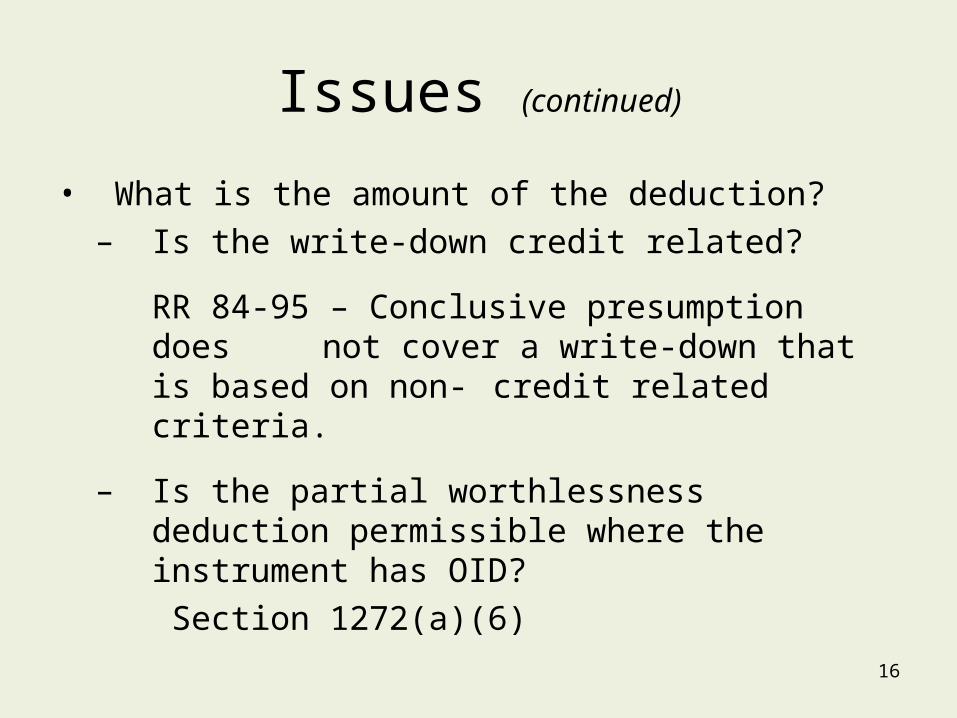

Issues (continued)

• What is the amount of the deduction?– Is the write-down credit related?

RR 84-95 – Conclusive presumption does not cover a write-down that is

based on non- credit related criteria.

– Is the partial worthlessness deduction permissible where the instrument has OID?

Section 1272(a)(6)

17

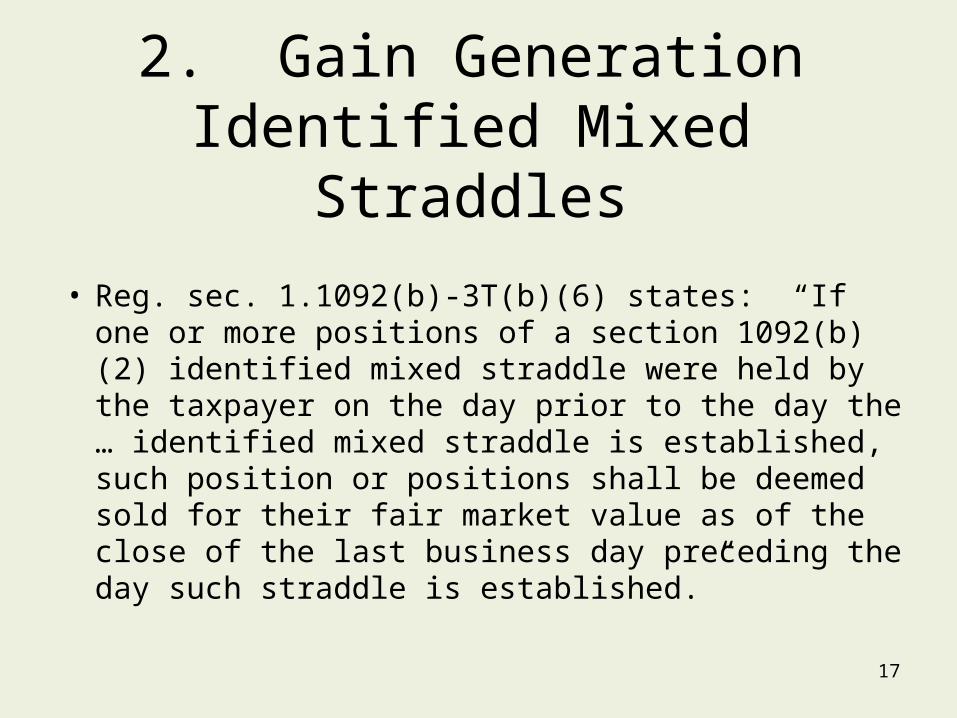

2. Gain GenerationIdentified Mixed Straddles

• Reg. sec. 1.1092(b)-3T(b)(6) states: “If one or more positions of a section 1092(b)(2) identified mixed straddle were held by the taxpayer on the day prior to the day the … identified mixed straddle is established, such position or positions shall be deemed sold for their fair market value as of the close of the last business day preceding the day such straddle is established.”

Identified Mixed Straddles

• Economic substance: How long should the mixed straddle be kept on?

• Caution: Reg. sec. 1.1092(b)-3T(d)(1):

“…Only the person or entity that directly holds all positions of a straddle may make the election under this section.”

18

Wash Sale Gains

Taxpayer has an unrealized gain position, and simply wants to sell the position and recognize the unrealized gain for US tax purposes.•Note that there is no similar rule applicable to realizing gains to the wash sale deferral rules (sec. 1091) for realized losses in certain fact patterns.•May it do so?•What about the economic substance rules?•How long must the taxpayer wait to buy the position back, if it so desires?

19

20

3. Recent DevelopmentsHedging and Straddles

• CCA 201034018 – Because Taxpayer did not satisfy same day identification requirements of Treas. Reg. §1.1221-2(f), section 1256 contracts that were used as hedges do not qualify for section 1256(e) exception and must be market-to-market. Inadvertent error exception of section 1221 regulations does not apply to section 1256(e) hedging exception

• CCA 201028039 – Loss on terminated NPC that hedged debt must be matched to debt had it hedged and spread over the life of the debt

21

Recent Developments (continued)

• CCA 201023055 – Similarly, loss on expired swaptions to be taken into account over the term to which the hedge relates

• CCA 201024049 – Taxpayer hedged pricing risk of inventory and claimed that puts were hedges but calls were not. Ruling states both subject to hedge timing rules of Treas. Reg. §1.446-4

• Variable contract hedging beginning to be examined by IRS

22

Recent Developments – Section 1256

• Dodd Frank Wall Street Reform and Consumer Protection Act, Pub. L. No.111-203

• Section 1256(b)(2)(B) provides exception to MTM for:

Interest rate swaps, currency swaps, basis swaps, interest rate caps, interest rate floors, commodity swaps, equity swaps, equity index swaps, credit default swaps, or similar agreements

23

Recent Developments – Section 1256 (continued)

• Applies to taxable years beginning after date of enactment

• Summitt, 134 T.C. No. 12 (2010) : Tax Court holds that a foreign currency call option is not a foreign currency contract subject to section 1256

– Section 1256(g)(2)(A) requires that, at the time the contract is entered into, there must be a physical or cash settlement upon expiration. Options are not required to be settled unless option is exercised

24

Recent Developments – Section 1256 (continued)

• In Rev. Rul. 2010-3, IRS rules that the London International Financial Futures and Options Exchange is a qualified board or exchange within the meaning of section 1256(g)(7)(c)

• Section 1256 contracts traded on the exchange must be market-to-market, automatic consent for change in method-of-accounting provided in Rev. Rul. 2010-3 for contracts entered into on or after January 1, 2010

• Also see PLR 200951031 and 201016002 (unnamed exchanges)

25

Recent Developments--Anschutz

• Anschutz Variable prepaid forward contracts plus securities lending agreements

• Taxpayer had entered into “master stock purchase agreements,” consisting of both VPFs and share lending agreements

• Holdings:– The combination of the VPFs and the share lending

agreements violated the requirements of sec. 1058 re no reduction in risk of loss, and thus was a taxable sale upon entering into them, with the amount of cash received on the VPFs as the proceeds.