Embed Size (px)

Citation preview

TAX UPDATES:WITHHOLDING TAX ONCOMPENSATION(REVENUE REGULATION 3-2015)

Department of Health

May 7, 2015

By: Andy B. Bisares

Revenue Officer III - Assessment

RDO 31, Sta. Cruz, Manila

TOPIC OUTLINE

I. Introduction

II.Overview on Withholding Tax on Compensation

III. Latest Amendments

PART IINTRODUCTION

INTRODUCTION

“In this world, nothing is certain but

DEATH and TAXES.Benjamin Franklin

INTRODUCTION

“TAXES are the single largest expense in a person’s lifetime.”

Robert Kiyosaki

INTRODUCTION

EmployeeYou have a J.O.B.

5% - 32%Time = Money

Business Owner You own a

SYSTEM 0% - 30%

People works with you = Money

Self-employed

You own a J.O.B.5% - 32%

Time = Money

InvestorYou own INVESTMENTS

5% – 20%Your money works for you =

Money

CashflowQuadrant

ACTIVE INCOME PASSIVE INCOME

PART IIOVERVIEW ON WITHHOLDING TAX

OVERVIEW ON WITHHOLDING TAX

A system designed to effectively collect taxes.It encourages voluntary complianceIt reduces cost of collection effortIt prevents delinquencies and revenue lossIt prevents dry spell in the fiscal condition of the

government by providing revenues throughout the taxable year

OVERVIEW ON WITHHOLDING TAX

Types of Withholding Taxes:1) Withholding Tax on Compensation

2) Expanded Withholding Tax

3) Final Withholding Tax

4) Withholding Tax on Government Money Payments

OVERVIEW ON WITHHOLDING TAX

Withholding Tax on CompensationCompensation or Wages – means all remuneration

for services performed by an employee for his employer under an employer-employee relationship unless exempted by the Code

OVERVIEW ON WITHHOLDING TAX

Compensation includes:1) Salaries and wages

2) Emoluments

3) Honoraria

4) Allowances

5) Commissions

6) Director’s fees if at the same time an employee

6) Taxable bonuses and fringe benefits unless subject to Fringe Benefit Tax

7) Taxable pensions and retirement pay

8) Other income of similar nature

OVERVIEW ON WITHHOLDING TAX

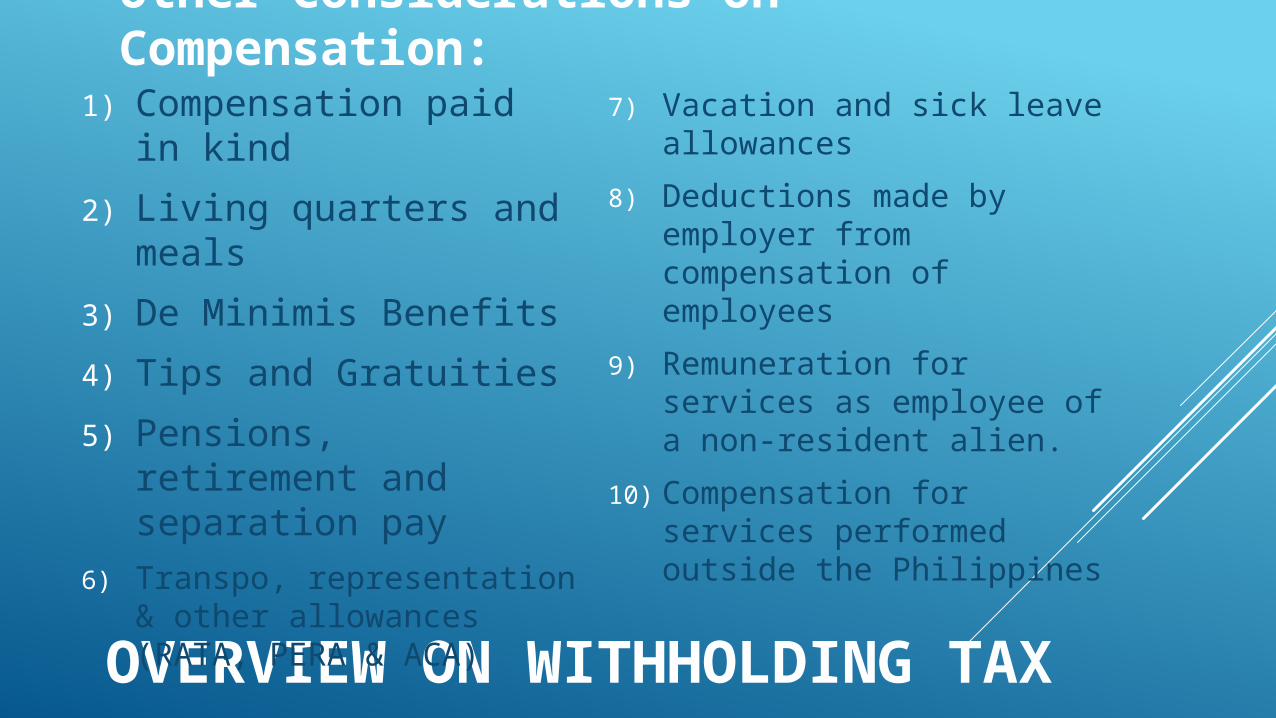

Other Considerations on Compensation:

1) Compensation paid in kind

2) Living quarters and meals

3) De Minimis Benefits

4) Tips and Gratuities

5) Pensions, retirement and separation pay

6) Transpo, representation & other allowances (RATA, PERA & ACA)

7) Vacation and sick leave allowances

8) Deductions made by employer from compensation of employees

9) Remuneration for services as employee of a non-resident alien.

10) Compensation for services performed outside the Philippines

OVERVIEW ON WITHHOLDING TAX

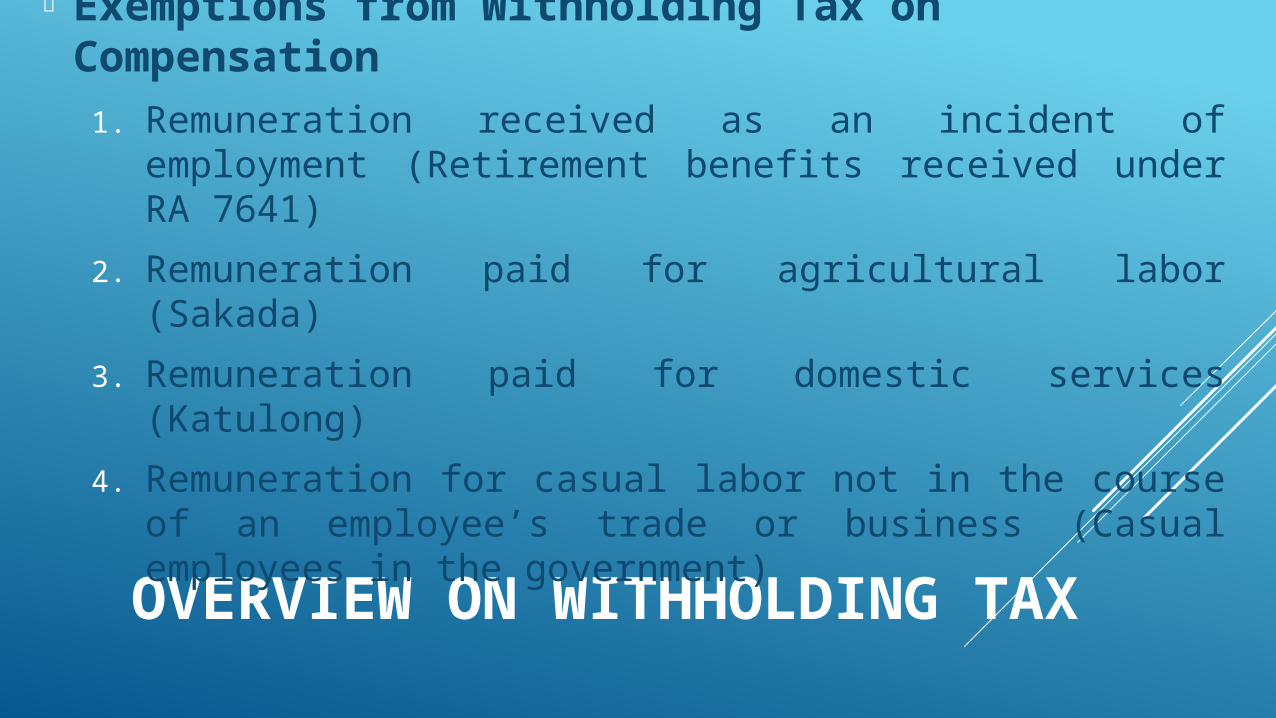

Exemptions from Withholding Tax on Compensation1. Remuneration received as an incident of employment

(Retirement benefits received under RA 7641)

2. Remuneration paid for agricultural labor (Sakada)

3. Remuneration paid for domestic services (Katulong)

4. Remuneration for casual labor not in the course of an employee’s trade or business (Casual employees in the government)

OVERVIEW ON WITHHOLDING TAX

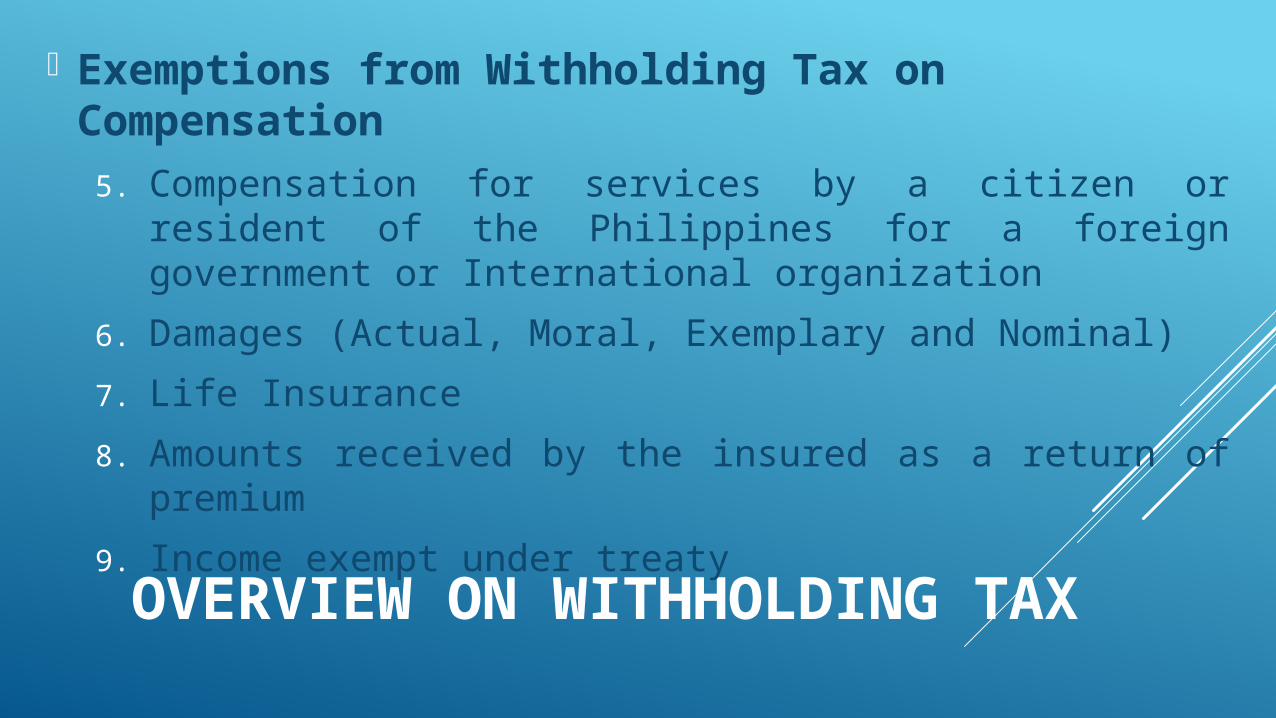

Exemptions from Withholding Tax on Compensation5. Compensation for services by a citizen or resident of the

Philippines for a foreign government or International organization

6. Damages (Actual, Moral, Exemplary and Nominal)

7. Life Insurance

8. Amounts received by the insured as a return of premium

9. Income exempt under treaty

OVERVIEW ON WITHHOLDING TAX

Exemptions from Withholding Tax on Compensation

10. GSIS, SSS, Medicare and other contributions

11. Minimum wage earners or annual income of P60,000 whichever is higher

12. Government employees with salary grades 1-3

13. De Minimis Benefits

14. Thirteenth (13th) month pay and other benefits

OVERVIEW ON WITHHOLDING TAX

DE MINIMIS BENEFITS1) Monetized unused vacation leave of private employees

credits not exceeding 10 days (RR 8-00) and monetized value of leave credits of gov’t. employees (RR10-00)

2) Medical cash allowance - P750 per semester/employee

3) Rice subsidy –P1,000 or 1 sack of rice (not more than P1,000)

4) Clothing allowance – P3,000 per annum

5) Medical Benefits – P10,000 per annum

6) Laundry allowance – P300 per month

OVERVIEW ON WITHHOLDING TAX

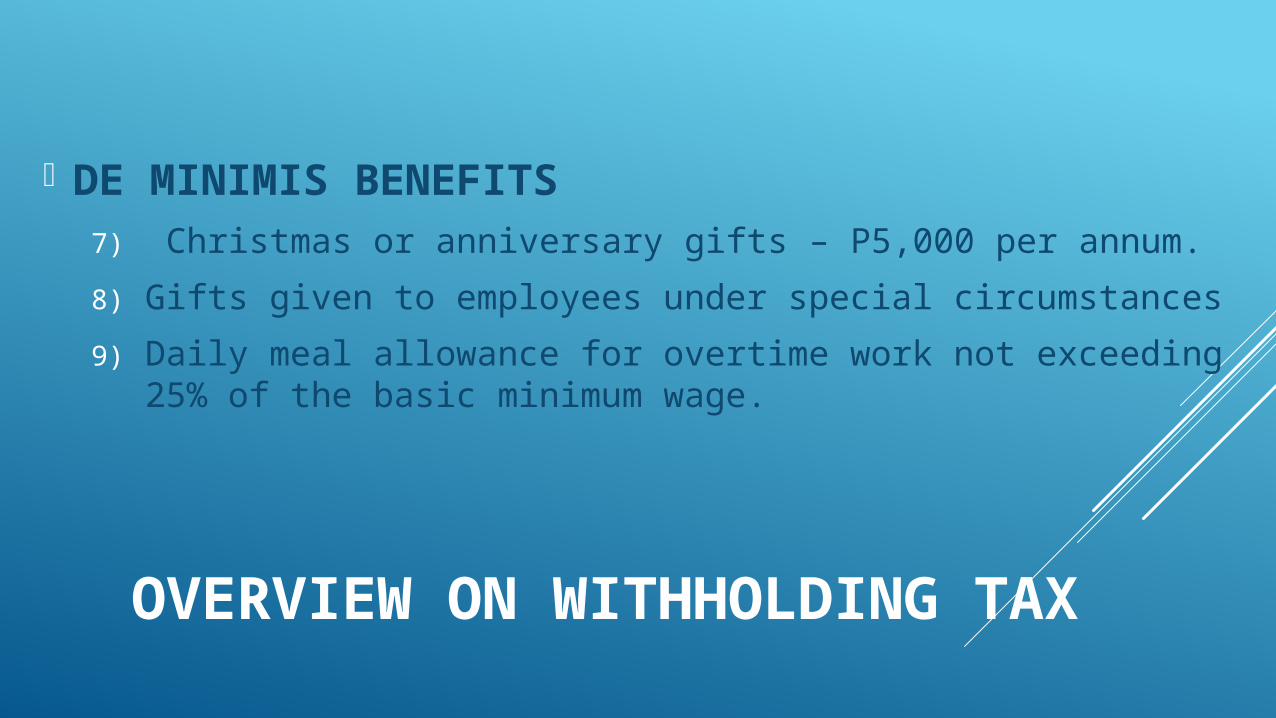

DE MINIMIS BENEFITS7) Christmas or anniversary gifts – P5,000 per annum.

8) Gifts given to employees under special circumstances

9) Daily meal allowance for overtime work not exceeding 25% of the basic minimum wage.

OVERVIEW ON WITHHOLDING TAX

DE DUCTIONS FROM GROSS COMPENSATION INCOME:

1) Basic Personal Exemptions – P50,000 per taxpayer

2) Additional Exemptions for qualified dependent children – P25,000 per child, maximum of 4

3) Health or Medical Insurance – 2,400 per year

PART IILATEST AMENDMENTS ON WITHHOLDING TAX ONCOMPENSATION

REVENUE REGULATION 3-2015

Implementing the provisions of Republic Act 10653

Subject: An Act Adjusting the 13th Month Pay and Other Benefits Ceiling Excluded from the Computation of Gross Income

Latest amendment to the Withholding Tax Law: Republic Act 8424 as implemented by RR 2-98

REVENUE REGULATION 3-2015

13th Month Pay & Other Benefits:1) 13th Month Pay – 1 month basic salary

2) Other benefits include the following: Christmas bonus

Productivity incentive bonus

Loyalty awards

Gifts in cash or in kind

Other benefits if similar in nature including Additional Compensation Allowance (ACA)

REVENUE REGULATION 3-2015

NEW LAW 13TH Month Pay & Other Benefits:

P82,000.00Note:

1) It does not apply to self-employed individuals and income generated from business

2) It applies to 13th Month pay and Other benefits paid or accrued beginning January 1, 2015.

OLD LAW 13th Month Pay & Other

Benefits:

P30,000.00

“TAXES are part of our world and will always be

part of our lives. So instead of complaining, lets simply understand them and put them to good use in our

lives”Tom Wheelright

THANK YOU.RDO 31, Sta. Cruz, ManilaSpeaker: Andy Bisares

Revenue Officer III - AssessmentOIC RDO: Max T. Cebrecus Jr.Asst. Chief, Assessment Section: Ronan Martirez

Hotline Number: 567-42-79