Embed Size (px)

Citation preview

Tax Management

Estates, Gifts and Trusts Journal™

Reproduced with permission from Tax Management Es-tates, Gifts, and Trusts Journal, Vol. 41, No. 6, p. 219,11/10/2016. Copyright � 2016 by The Bureau of NationalAffairs, Inc. (800-372-1033) http://www.bna.com

An Oxymoron? The DeathbedLifetime QTIP for BasisAdjustment and AssetProtectionBy Richard S. FranklinMcArthur Franklin PLLCWashington, D.C.andGeorge D. KaribjanianProskauer Rose LLPBoca Raton, Florida*

‘‘Deathbed’’ estate planning is one concept that hasalways piqued the interest of estate planners. For themost part, death is one of the few great unknowns ofthe human existence — no one truly knows when onewill die. When the probability of death is heightened,estate planners have long sought to utilize this insightto maximize the wealth transfer potential for the soon-to-be-deceased client and the client’s family. Based onthe premise that a client’s death is imminent, this ar-ticle will combine two distinct concepts — deathbedtransfers and self-settled spendthrift trusts — to pres-ent a technique that, while only applicable under lim-ited circumstances, could reap big rewards.

INTRODUCTION TO INCOMETAXATION OF DEATHBEDTRANSFERS

Prior to 1982, deathbed planning had significant in-come tax advantages. Pursuant to the general rule un-der §1014,1 regardless of (a) the decedent’s cost basisin a particular appreciated asset that he or she mayown, and (b) the timing of the decedent’s acquisitionof such asset in proximity to his or her death, the costbasis of the appreciated asset upon the decedent’sdeath was automatically adjusted to the asset’s thenfair market value (referred to as the ‘‘General BasisAdjustment Rule’’). Because there were no timing re-strictions on the General Basis Adjustment Rule, itwas possible to transfer low basis assets to a dyingperson, have such assets become subject to the Gen-eral Basis Adjustment Rule upon the decedent’s death,and have the dying person bequeath those assets im-mediately back to the donor. As a result of acquiringthe assets from a decedent, the donor’s basis was in-creased to the assets’ fair market value as of the dece-dent’s date of death.

This loophole, however, was closed in 1982 withthe enactment of §1014(e), which imposes a one year‘‘re-transfer threshold’’ in order to qualify for theGeneral Basis Adjustment Rule. Under §1014(e), as-sets no longer qualify for the General Basis Adjust-ment Rule if they are gratuitously transferred to a do-nee and then, within one year thereafter, retransferredback to the donor as a result of the donee’s death (re-

* � 2016 Richard S. Franklin & George D. Karibjanian. AllRights Reserved.

1 See generally §1014(a)(1). Unless otherwise specified, all sec-tion references are to the Internal Revenue Code of 1986, asamended (IRC), and the regulations thereunder.

Tax Management Estates, Gifts and Trusts Journal

� 2016 Tax Management Inc., a subsidiary of The Bureau of National Affairs, Inc. 1ISSN 0886-3547

ferred to as the ‘‘One Year Rule’’).2 Beyond this sim-plistic example, however, the language of §1014(e) issomewhat nebulous and, since its enactment, the In-ternal Revenue Service (Service) has provided littledetailed information as to its application.3

INTRODUCTION TO SELF-SETTLEDSPENDTHRIFT TRUSTS

In present-day estate planning, asset protection hasgrown to become one of the primary elements incrafting a sound estate plan. While most testamentarytrusts have historically contained a spendthrift feature(described in more detail below), in recent years theobjective has been to minimize the creditor exposureof the client during his or her lifetime. Until 1997, nodomestic jurisdiction allowed a settlor to create a‘‘self-settled spendthrift trust’’ (SST), which is an ir-revocable trust for his or her own benefit, and have hisor her retained interest feature spendthrift protection.4

In 1997, Alaska became the first state to enact legis-lation approving the use of SSTs. As of August 1,2016, 16 states have adopted legislation allowingSSTs.5

With a standard SST, during the settlor’s lifetime,the trustee has the discretion to pay to the settlor (and,in some instances, the settlor’s descendants) any por-tion or all of the trust’s income and principal. Assum-ing that the other formation requirements are met(which customarily include a specific designation ofgoverning law and a local resident or institution act-ing as a trustee), the applicable state law recognizesspendthrift protection as to the settlor.6

SSTs are not limited to the settlor’s initial retentionof a current beneficial interest. The SST can also take

the form of a transfer in trust for the benefit of a thirdparty which, upon the termination of the third party’sinterest, continues in further trust for settlor’s benefit.For example, the settlor can create a trust for his orher spouse, qualify that trust for the federal estate taxmarital deduction as ‘‘qualified terminable interestproperty’’ (QTIP) (such a trust is referred to as a‘‘Lifetime QTIP Trust’’),7 and provide in the trust in-strument that if the spouse predeceases the settlor, theremainder of the trust is to be held in further trust forthe settlor’s benefit (the ‘‘Resulting Trust’’). Becausethe settlor created the Lifetime QTIP Trust, which has,as one of its provisions, the Resulting Trust for thesettlor’s benefit, the Resulting Trust is technically anSST.

In states that authorize SSTs (SST States), the factthat the Resulting Trust is an SST is of zero conse-quence — the laws of the state already allow for self-settled spendthrift trust protection. Other states,though, have adopted statutes allowing for some self-settled spendthrift trust protection without adoptingfull SST legislation. As of August 1, 2016, 11 addi-tional non-SST States, along with 6 SST States(Quasi-SST States), have enacted statutes (Quasi-SSTStatutes) to specifically abrogate the rule against SSTsfor Resulting Trusts benefiting the settlor that are cre-ated upon the termination of a Lifetime QTIP Trust.8

For example, under the Arizona Quasi-SST Statute,

2 See Economic Recovery Tax Act of 1981, Pub. L. No. 97-34.3 Jeff Scroggin, Understanding Section 1014(e) & Tax Basis

Planning, LISI Estate Planning Newsletter #2192 (Feb. 6, 2014)available at http://www.leimbergservices.com (hereafter ‘‘Scrog-gin Article’’).

4 See Restatement (Second) of Trusts (1959), §156; Restate-ment (Third) of Trusts (2003), §58(2); N.Y. Est. Powers & TrustsLaw §7-3.1.

5 See Alaska Stat. §34.40.110(a) (Alaska); Del. Code Ann. tit.12, §3570–§3576 (Delaware); Haw. Rev. Stat. §554G (Hawaii);Miss. Code Ann. §91-9-701–§91-9-723 (Mississippi); Mo. Rev.Stat. §456.5-505 (Missouri); Nev. Rev. Stat. §166.010–§166.170(Nevada); N.H. Rev. Stat. Ann. §564-D:1-18 (New Hampshire);Ohio Rev. Code §5816.01–§5816.14 (Ohio); Okla. Stat. Ann. tit.31, §10–§18 (Oklahoma); 18 R.I. Gen. Laws §18-9.2 (Rhode Is-land); S.D. Codified Laws §55-16-1–§55-16-16 (South Dakota);Tenn. Code Ann. §35-16-101–§35-16-112 (Tennessee); Utah Code§25-6-13 (Utah); Va. Code Ann. §64.2-745.1, §64.2-745.2 (Vir-ginia); W. Va. Code §44D-5-503a–§44D-5-503c (West Virginia);Wyo. Stat. Ann. §4-10-502, §4-10-504, §4-10-506(c), §4-10-510–§4-10-523 (Wyoming).

6 For example, under Del. Code Ann. tit. 12, §3570(11), in or-der to qualify as an SST in Delaware, the trust instrument must(a) expressly provide that Delaware law govern the validity, con-

struction and administration of the trust, (b) be irrevocable, and(c) contain a spendthrift clause.

7 Establishing a Lifetime QTIP Trust is complicated and it in-volves more considerations than are applicable in the context ofcreating a testamentary QTIP. For background on Lifetime QTIPTrusts, ideas for specific uses of Lifetime QTIP Trusts, and prac-tical implementation information, see Richard S. Franklin, Life-time QTIPs — Why They Should be Ubiquitous in Estate Plan-ning, 50 U. Miami Heckerling Inst. on Est. Plan., ¶16 (Jan. 14,2016) (hereinafter ‘‘Ubiquitous’’).

8 This article uses the term ‘‘Quasi-SST Jurisdiction’’ which isderived from the term ‘‘Inter-Vivos QTIP Trust Jurisdiction’’ ascoined by Barry Nelson of North Miami Beach, Florida. The 11Quasi-SST Jurisdictions that do not authorize SSTs are: Arizona(Ariz. Rev. Stat. §14-10505(E)), Arkansas (Ark. Rev. Stat. §28-73-505(c)), Florida (Fla. Stat. §736.0505(3)), Kentucky (Ky. Rev.Stat. Ann. §386B.5-020(8)(a)), Maryland (Md. Code, Est. &Trusts §14.5-1003), Michigan (Mich. Comp. Laws §700.7506(4)),North Carolina (N.C. Gen. Stat. §36C-5-505(c)), Oregon (Or. RevStat. §130.315(4)), South Carolina (S.C. Code Ann. §62-7-505(b)(2)), Texas (Tex. Prop. Code §112.035(g)), and Wisconsin(Wisc. Stat. Ann. §701.0505(2)(e)). The 6 SST States that haveenacted Quasi-SST Statutes are: Delaware (Del. Code Ann. tit. 12,§3536(c)), New Hampshire (N.H. Rev. Stat. Ann. §564-B:5-505),Ohio (Ohio Rev. Code §5805.06(B)(3)), Tennessee (Tenn. CodeAnn. §35-15-505(d)), Virginia (Va. Code Ann. §64.2-747.B.3.),and Wyoming (Wyo. Stat. Ann. §4-10-506(f)). Within an SSTState that also has enacted a Quasi-SST Statute, a lifetime QTIPcould be created to qualify under one statutory scheme or theother or perhaps both. Typically, the requirements to establish aSST Trust are more involved than to qualify a Lifetime QTIP

Tax Management Estates, Gifts and Trusts Journal2 � 2016 Tax Management Inc., a subsidiary of The Bureau of National Affairs, Inc.

ISSN 0886-3547

the settlor of a Lifetime QTIP Trust is not considered,for creditor purposes, to be the settlor of any Result-ing Trust if (a) the QTIP election is made as to theLifetime QTIP Trust pursuant to §2523(f), and (b) thesettlor is the beneficiary of the Resulting Trust afterthe donee spouse’s death. Hence, if the settlor is notconsidered to be the settlor for purposes of this rule,Arizona’s other rules governing creditor’s rights innon-SSTs would apply, which generally permit spend-thrift trust protection of a trust beneficiary’s interests.These statutes create opportunities that should not beoverlooked.

With this background, the challenge is now to de-termine analytically whether, under certain circum-stances, when a spouse’s death is imminent, it is pos-sible to meld the income tax advantages associatedwith an automatic basis adjustment upon death andself-settled spendthrift trust protection to achieve in-come tax and asset protection benefits for the donor/surviving spouse.

THE DEATHBED STRATEGY —DEATHBED LIFETIME QTIP TRUST

Combining the basics of deathbed planning with aninter-vivos SST, consider the following scenario:

ExampleAs of August 1, 2016, W and H, Floridaresidents, are in their first marriage and areages 75 and 80, respectively. They each havea revocable trust funded (for over one year)with $10 million of assets, all of which havea zero basis for income tax purposes and noportion of the potential gain is income inrespect of a decedent.Each revocable trust provides that, upon thesettlor’s death, two trusts are to be created –first, a pre-residuary pecuniary QTIP trust, tobe funded with the minimum amount neces-sary to reduce federal estate taxes to thelowest possible amount, and second, a re-siduary ‘‘bypass’’ (i.e., credit shelter) trust tobe funded with the balance of the assets. Theformula adjusts for assets passing outside ofthe revocable trust that do not qualify for themarital deduction.

Upon the surviving spouse’s death, all re-maining assets pass to long-term generation-skipping transfer (GST) tax-exempt and non-exempt trusts for the couple’s descendants.H becomes ill and, with his health in rapiddecline, enters hospice care and is expectedto die within a few days. W and H havemade no prior taxable gifts.

W is aware that upon H’s death, the entire $10 mil-lion of assets in H’s revocable trust will be subject tothe General Basis Adjustment Rule and that testamen-tary trusts will be created for her that will providecreditor protection features with a standard spendthriftclause.

Query whether this plan can be enhanced to pro-vide even greater tax and creditor protection benefits.One approach is the adoption of the ‘‘Deathbed QTIPTrust Strategy’’ (Deathbed Strategy) which is imple-mented as follows:

Implementation of Deathbed Strategy in Ex-ampleUpon the diagnosis of H’s terminal condi-tion, W quickly establishes a Lifetime QTIPTrust for H’s benefit and funds it with $5.45million of assets from her revocable trust (allof which, as stated above, have a zero costbasis). W timely files a Form 709, U.S. Gift(and Generation-Skipping Transfer) Tax Re-turn (709), and elects, pursuant to §2523(f),to qualify the entire Lifetime QTIP Trust forthe federal gift tax marital deduction.9 Wnames a non-trust beneficiary to be thetrustee of the Lifetime QTIP Trust (if she sodesires, W, however, can be an administra-tive trustee).The Lifetime QTIP Trust provides that, uponH’s death, the balance of the trust assets areto be held in a discretionary Resulting Trustfor W and W’s descendants. With H’s avail-able applicable exclusion amount under§2010 (AEA) having been allocated againstthe Resulting Trust, the self-adjusting for-mula provision in H’s revocable trust passesthe balance of H’s assets to a standard testa-mentary QTIP trust for W’s benefit.Alternatively, W could fund the LifetimeQTIP Trust with her entire $10 million ofTrust under a Quasi-SST Statute.

Most of the Quasi-SST Statutes provide that after the doneespouse’s death, if the donor spouse has an interest in the Result-ing Trust, the donor spouse is not deemed to be the settlor of thetrust that created the Resulting Trust (i.e., the Lifetime QTIPTrust). Tennessee’s statute, however, takes a slightly different ap-proach. Rather than deeming the donor spouse to not be the set-tlor, Tennessee’s statute deems the settlor’s interest in the Result-ing Trust to not be property that may be distributed to the donorspouse. Ohio’s statute takes a similar approach.

9 If W dies during the calendar year in which she transferred theassets to the Lifetime QTIP Trust, then, under §6075(b)(3), thedeadline for W’s executor to file the resulting 709 is not April 15in the calendar year after the year in which the gift occurred, butrather is the deadline, including extensions, for filing W’s Form706, U.S. Estate (and Generation-Skipping Transfer) Tax Return(706).

Tax Management Estates, Gifts and Trusts Journal

� 2016 Tax Management Inc., a subsidiary of The Bureau of National Affairs, Inc. 3ISSN 0886-3547

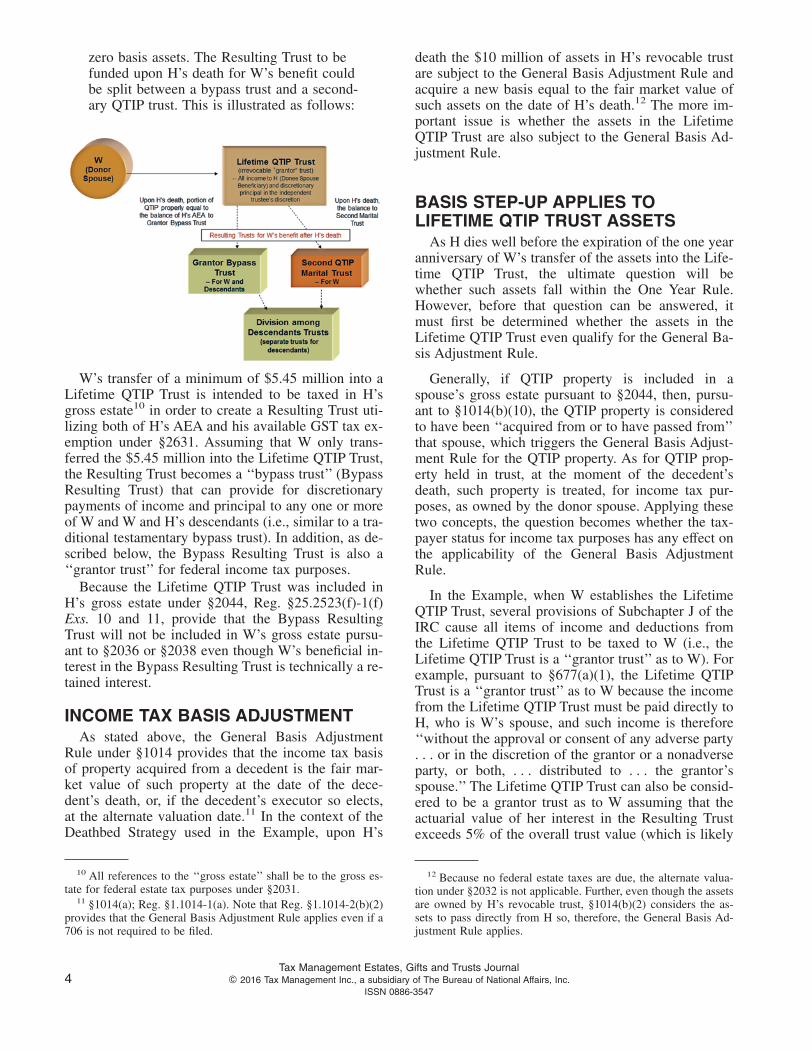

zero basis assets. The Resulting Trust to befunded upon H’s death for W’s benefit couldbe split between a bypass trust and a second-ary QTIP trust. This is illustrated as follows:

W’s transfer of a minimum of $5.45 million into aLifetime QTIP Trust is intended to be taxed in H’sgross estate10 in order to create a Resulting Trust uti-lizing both of H’s AEA and his available GST tax ex-emption under §2631. Assuming that W only trans-ferred the $5.45 million into the Lifetime QTIP Trust,the Resulting Trust becomes a ‘‘bypass trust’’ (BypassResulting Trust) that can provide for discretionarypayments of income and principal to any one or moreof W and W and H’s descendants (i.e., similar to a tra-ditional testamentary bypass trust). In addition, as de-scribed below, the Bypass Resulting Trust is also a‘‘grantor trust’’ for federal income tax purposes.

Because the Lifetime QTIP Trust was included inH’s gross estate under §2044, Reg. §25.2523(f)-1(f)Exs. 10 and 11, provide that the Bypass ResultingTrust will not be included in W’s gross estate pursu-ant to §2036 or §2038 even though W’s beneficial in-terest in the Bypass Resulting Trust is technically a re-tained interest.

INCOME TAX BASIS ADJUSTMENTAs stated above, the General Basis Adjustment

Rule under §1014 provides that the income tax basisof property acquired from a decedent is the fair mar-ket value of such property at the date of the dece-dent’s death, or, if the decedent’s executor so elects,at the alternate valuation date.11 In the context of theDeathbed Strategy used in the Example, upon H’s

death the $10 million of assets in H’s revocable trustare subject to the General Basis Adjustment Rule andacquire a new basis equal to the fair market value ofsuch assets on the date of H’s death.12 The more im-portant issue is whether the assets in the LifetimeQTIP Trust are also subject to the General Basis Ad-justment Rule.

BASIS STEP-UP APPLIES TOLIFETIME QTIP TRUST ASSETS

As H dies well before the expiration of the one yearanniversary of W’s transfer of the assets into the Life-time QTIP Trust, the ultimate question will bewhether such assets fall within the One Year Rule.However, before that question can be answered, itmust first be determined whether the assets in theLifetime QTIP Trust even qualify for the General Ba-sis Adjustment Rule.

Generally, if QTIP property is included in aspouse’s gross estate pursuant to §2044, then, pursu-ant to §1014(b)(10), the QTIP property is consideredto have been ‘‘acquired from or to have passed from’’that spouse, which triggers the General Basis Adjust-ment Rule for the QTIP property. As for QTIP prop-erty held in trust, at the moment of the decedent’sdeath, such property is treated, for income tax pur-poses, as owned by the donor spouse. Applying thesetwo concepts, the question becomes whether the tax-payer status for income tax purposes has any effect onthe applicability of the General Basis AdjustmentRule.

In the Example, when W establishes the LifetimeQTIP Trust, several provisions of Subchapter J of theIRC cause all items of income and deductions fromthe Lifetime QTIP Trust to be taxed to W (i.e., theLifetime QTIP Trust is a ‘‘grantor trust’’ as to W). Forexample, pursuant to §677(a)(1), the Lifetime QTIPTrust is a ‘‘grantor trust’’ as to W because the incomefrom the Lifetime QTIP Trust must be paid directly toH, who is W’s spouse, and such income is therefore‘‘without the approval or consent of any adverse party. . . or in the discretion of the grantor or a nonadverseparty, or both, . . . distributed to . . . the grantor’sspouse.’’ The Lifetime QTIP Trust can also be consid-ered to be a grantor trust as to W assuming that theactuarial value of her interest in the Resulting Trustexceeds 5% of the overall trust value (which is likely

10 All references to the ‘‘gross estate’’ shall be to the gross es-tate for federal estate tax purposes under §2031.

11 §1014(a); Reg. §1.1014-1(a). Note that Reg. §1.1014-2(b)(2)provides that the General Basis Adjustment Rule applies even if a706 is not required to be filed.

12 Because no federal estate taxes are due, the alternate valua-tion under §2032 is not applicable. Further, even though the assetsare owned by H’s revocable trust, §1014(b)(2) considers the as-sets to pass directly from H so, therefore, the General Basis Ad-justment Rule applies.

Tax Management Estates, Gifts and Trusts Journal4 � 2016 Tax Management Inc., a subsidiary of The Bureau of National Affairs, Inc.

ISSN 0886-3547

if the Resulting Trust provides her with mandatory in-come).13

As the Lifetime QTIP Trust is a ‘‘grantor trust,’’Rev. Rul. 85-13,14 in effect, concludes that during H’slife, W owns the assets of the trust for income tax pur-poses. Contrast this with the purpose of §1014 (alsoan income tax provision), which is to grant a benefitfor assets ‘‘acquired from a decedent.’’ If Rev. Rul.85-13 stands for the premise that, for ‘‘grantor trust’’purposes, the grantor (i.e., W) ‘‘owns’’ the property,then, under §1014, does ‘‘grantor trust’’ property ac-tually ‘‘pass’’ from a decedent (i.e., H) since the dece-dent is not treated as ‘‘owning’’ the property for in-come tax purposes? Stated differently, does Rev. Rul.85-13 indirectly create an exception to the GeneralBasis Adjustment Rule under §1014(a) for LifetimeQTIP Trusts that are taxed for income tax purposes tothe grantor?

The short answer is that there does not appear to besuch an exception. The phrase ‘‘acquiring the propertyfrom a decedent’’ in §1014(a) is explained in§1014(b), which appears to refer to the actual transferof property as a result of a decedent’s death and not tothe ‘‘income tax’’ transfer of such property. This con-clusion is reinforced by the reference in Reg.§1.1014-2(b)(2) to the decedent’s 706 (or lackthereof): ‘‘It is not necessary for the application ofthis paragraph that an estate tax return be required tobe filed for the estate of the decedent or that an estatetax be payable.’’ If §1014(a) were only to apply toproperty owned by another for income tax purposes,the issue of the decedent’s 706 would be irrelevant —the true test would be whether such assets were taxedto the decedent for income tax purposes, which is nota test under any of the Treasury Regulations under§1014.

Effects of the One-Year RuleAlthough there are three exceptions within §1014

to the General Basis Adjustment Rule, for purposes ofthe Deathbed Strategy, only one exception is pertinent— the §1014(e) One Year Rule.15

Specifically, §1014(e)(1) provides as follows:

(e) Appreciated property acquired by dece-dent by gift within 1 year of death.

(1) In general. In the case of a decedent dy-ing after December 31, 1981, if —

(A) appreciated property was acquiredby the decedent by gift during the1-year period ending on the date of thedecedent’s death, and(B) such property is acquired from thedecedent by (or passes from the dece-dent to) the donor of such property (orthe spouse of such donor),

the basis of such property in the hands ofsuch donor (or spouse) shall be the adjustedbasis of such property in the hands of thedecedent immediately before the death of thedecedent.

As stated above, the general rule is fairly straight-forward — if gifted property passes back to the donoras a result of the death of the recipient within one yearof the gift, the General Basis Adjustment Rule doesnot apply. However, a more careful reading of thestatute may present an ‘‘exception-to-the-exception.’’The statute refers to property re-acquired by the ‘‘do-nor’’ of the property. Who exactly is the ‘‘donor’’ inthis instance — is this to be interpreted literally, i.e.,directly to the donor, or is this to be interpreted gen-erally, i.e., directly to the donor or indirectly to the do-nor through a trust in which the donor is a benefi-ciary?

Under the facts in the Example, H is in hospice careand expected to die within a few days. The LifetimeQTIP Trust assets will be included in H’s gross estatepursuant to §2044. The remainder, however, is not re-turning directly to W, but, rather, is returning indi-rectly to W in the form of a current interest in a Re-sulting Trust (or Trusts). Therefore, it would appear asif the premise of the Deathbed Strategy falls outsidethe literal wording of §1014(e)(1).16

However, a more in-depth analysis may lead to adifferent conclusion. The legislative history to§1014(e) appears to provide for a far more expansivereach than the statutory language. Specifically, thelegislative history states:17

For decedents dying after December 31,1981, the bill provides that the stepped-up

13 See §673(a).14 1985-1 C.B. 184.15 Reg. §1.1014-1(c)(1). Also excepted from the General Basis

Adjustment Rule are unexercised incentive stock options and op-tions to purchase pursuant to an employee stock purchase plan.Reg. §1.1014-1(c)(2).

16 See Mark R. Siegel, I.R.C. Section 1014(e) and Gifted Prop-erty Reconveyed in Trust, 27 Akron Tax J. 33 (2011–2012) at 45:

Consistent with the statutory language contained in§1014(e)(1), the legislative history to §1014(e) clearlyindicates congressional concern about the situationwhere the donee-spouse dies within a year of the trans-fer and leaves the donor-spouse the property outright.The statutory language found in §1014(e)(1) lends sup-port to the argument that the step up in basis is notbarred where, rather than returning the property di-rectly to the donor, the donee-spouse instead providesthat the property passes in trust for the survivingdonor-spouse.

17 H.R. Rep. No. 97-201, at 188 (1981).

Tax Management Estates, Gifts and Trusts Journal

� 2016 Tax Management Inc., a subsidiary of The Bureau of National Affairs, Inc. 5ISSN 0886-3547

basis rules contained in section 1014 will notapply with respect to appreciated propertyacquired by the decedent through gift within[one-year] of death (including the gift ele-ment of a bargain sale), if such propertypasses, directly or indirectly, from the donee-decedent to the original donor or the donor’sspouse. (Emphasis added.)

It is unclear how the phrase ‘‘directly or indirectly’’is to be interpreted, especially since such languagewas not adopted in the final statute. If the legislativehistory is applied to interpret the statute, the statutoryphrase ‘‘acquired from the decedent by (or passesfrom the decedent to) the donor’’ would be interpretedto include indirect interests for the donor’s benefit. Anarrow interpretation is that ‘‘indirectly’’ refers totransfers in trust where the funds will ultimately bedistributed outright to the donor, such as if the trustagreement provides that if a particular asset is sold,the sales proceeds are to be distributed outright to thesurviving spouse.18 A broader application is that ‘‘in-directly’’ could include a mandatory or discretionaryincome interest in a trust. If the broader interpretationis applied, then under facts similar to the DeathbedStrategy, the General Basis Adjustment Rule wouldnot apply to the entire Resulting Trust for W.

Since §1014(e) was enacted, the Service has pro-vided little detailed information on how to apply§1014(e).19 A search for guidance located only fivepublished Private Letter Rulings in which §1014(e)was a primary focus (1014(e) PLRs), and, in eachsuch ruling, the Service relied on the ‘‘direct or indi-rect’’ language from the legislative history in inter-preting the scope of §1014(e).20

How best to plan to avoid the 1014(e) PLRs de-pends on the standard of living of the donor spouse.

If the donor spouse does not necessarily need fullaccess to the funds, the Resulting Trust for the donorspouse should be prepared as a discretionary trust un-der which the distribution of income and principal

among the donor spouse and the donor spouse’s de-scendants is at the complete discretion of independenttrustees. Drawn in this manner, it would appear im-possible to actuarially determine the ‘‘definite’’ inter-est in the donor spouse. After all, if the portion sub-ject to §1014(e) cannot be actuarially determined, itcan be concluded that the §1014(e) portion has novalue. The end result is that the default rule of§1014(a) would apply and the §1014(e) excepted por-tion would have no value; therefore, the entire Result-ing Trust is subject to the General Basis AdjustmentRule.21

What if, however, the donor spouse must have ac-cess to some of the funds — not enough access to re-quire an outright payment of all assets back to the do-nor spouse, but partial access by means of a manda-tory income interest? Under the 1014(e) PLRs, thesuggestion is made that §1014(e) would apply to anyportion of assets in trust where the donor spouse hasa definite interest, such as a mandatory income inter-est. Under that scenario, the 1014(e) PLRs infer that§1014(a) and §1014(e) would apply proportionatelybetween the determinable interest for the spouse (i.e.,the mandatory income interest) and the other interestsin the trust, with the default rule of §1014(a) applyingand then excepted by any portions deemed to be sub-ject to §1014(e) (Bifurcation Rule).

For example, at 65 years of age, by applying a2.2% interest rate as determined under §7520 (7520Rate), the life estate factor for valuing a trust interestis 31% (with a remainder factor of 69%). At age 75,applying the same 2.2% 7520 Rate, the life estate fac-tor is decreased to 21% (and the remainder factor isincreased to 79%). Under the Bifurcation Rule, if W,a 75-year-old Florida resident, creates a LifetimeQTIP Trust on H’s deathbed and, upon H’s death, theResulting Trust is a mandatory income trust for W’slifetime, the entire Resulting Trust would be subjectto the General Basis Adjustment Rule under §1014(a),but a portion of the Resulting Trust equal to the 21%actuarial value of W’s income interest is subject to theOne Year Rule under §1014(e).22

Complexities are added to the Bifurcation Rule ifthe donor spouse requires more than just the income

18 See Siegel, above n. 16, at 46: ‘‘The language may be lim-ited only to situations where the appreciated property is sold andthe fiduciary is directed to distribute the proceeds to the donor. Forexample, in the context of the sale of appreciated property by atrust, the language may be intended to cover the limited situationwhere the donee created a trust and the trustee of that trust sellsthe appreciated property and distributes the proceeds to the donoraccording to the trust agreement. In contrast, the statute may notexpressly cover the donee-decedent’s testamentary trust fundedwith the appreciated property with the donor as beneficiary of alife interest or term certain interest.’’

19 Scroggin Article, above n. 3, at 4.20 Id., citing PLR 9026036, rev’d in part on different issue by

PLR 9321050, PLR 9308002, PLR 200101021, PLR 200210051.Although Private Letter Rulings are binding only on the request-ing party, they do provide insight on the Service’s position as to aparticular issue.

21 See Howard M. Zaritsky, Tax Planning for Family WealthTransfers During Life: Analysis With Forms, ¶8.07[5][c] (Thom-son Reuters, 5th ed. 2013, with updates through May 2016). Seealso Lester B. Law & Howard M. Zaritsky, Basis, Banal? Basic?Benign? Bewildering?, 49 U. Miami Heckerling Institute on Es-tate Planning, IV.E.3(d) (unpublished) (2015); Steve Akers, Cur-rent Developments and Hot Topics 47–48 (June 2014) availableat http://www.bessemer.com/advisor.

22 Although the Bifurcation Rule is inferred within the 1014(e)PLRs, no mention is made as to how to implement the Bifurca-tion Rule within the trust, that is, do all appreciated assets receivea pro-rata basis increase totaling 79% of all trust appreciation, arecertain assets allocated to the ‘‘remainder’’ so that such assets are

Tax Management Estates, Gifts and Trusts Journal6 � 2016 Tax Management Inc., a subsidiary of The Bureau of National Affairs, Inc.

ISSN 0886-3547

from the Resulting Trust. The actuarial calculationwhen the donor spouse retains the income interest inthe Resulting Trust is a simple calculation; complica-tions arise, and an increase in the portion subject to§1014(e) is likely, if the Resulting Trust also providesthat the donor spouse is granted a discretionary prin-cipal right subject to an ascertainable standard or a ‘‘5and 5’’ annual withdrawal right (5&5 Right). The rea-son for the increase in the value of the §1014(e) por-tion is that both principal rights can be ascertained forvaluation purposes (although the valuation process forthe discretionary principal interest can be extremelycomplex). For this purpose, the better plan is to notinclude a 5&5 Right and provide that the income andprincipal distributions be wholly discretionary and notsubject to an ascertainable standard.23 This should al-low the trustees to assert the argument that all discre-tion in favor of W is ‘‘unascertainable’’ for valuationpurposes, which would effectively negate the imposi-tion of §1014(e).24

Is it a certainty that the Bifurcation Rule will be ap-plied? Not according to a recent Tax Court opinion. InEstate of Kite v. Commissioner,25 Mrs. Kite trans-ferred certain stock into a Lifetime QTIP Trust for Mr.Kite seven days before his death on February 23,1995. The Lifetime QTIP Trust provided that, uponMr. Kite’s death, the balance of the trust would beheld in an income trust for Mrs. Kite’s lifetime (i.e., atrust that would qualify for the QTIP election in Mr.Kite’s gross estate). Upon Mr. Kite’s death, the Life-

time QTIP Trust was included in his gross estate un-der §2044. From a reading of the opinion, the issuesbefore the Tax Court did not include the applicabilityof §1014(e). However, footnote 9 of the opinionstated, ‘‘All of the underlying trust assets, includingthe OG&E stock transferred to Mr. Kite in 1995 [theLifetime QTIP Trust],[26] received a step-up in basisunder sec. 1014.’’27 It was very apparent that Mr. Kitedied very soon after the creation of the Lifetime QTIPTrust, yet the Tax Court stated that the assets in theLifetime QTIP Trust were all subject to the GeneralBasis Adjustment Rule. Query whether the Tax Court(a) neglected to consider §1014(e) in its opinion, (b)the Service neglected to consider the applicability of§1014(e) in its audit of the matter and arguments be-fore the Tax Court, and/or (c) the Tax Court ignoredthe 1014(e) PLRs and focused on the literal languageof §1014(e) and concluded that, since Mrs. Kite, thedonor, did not receive outright ownership of the assetspassing from the Lifetime QTIP Trust, the statutoryprovisions of §1014(e) did not apply.28

CONTINUING GRANTOR TRUSTSTATUS FOR RESULTING TRUSTS

If, upon a spouse’s death, the testamentary docu-ments provide for a bypass trust, the bypass trust is itsown taxpayer for income tax purposes. Under a mod-ern drafting approach, the bypass trust would be a to-tal discretionary trust for the benefit of either the sur-viving spouse or the surviving spouse and the descen-dants of the deceased spouse. If, in a particulartaxable year, such discretion is not exercised so thatthere are no distributions carrying out distributable netincome, the bypass trust pays all income taxes on itstaxable income. Although this would result in taxableincome being taxed at a potential top federal incometax rate of 43.4% (with additional state income taxesif the trust is subject to state income taxation), thiswould also mean that 56.6% of all such taxable in-come (or less, if state income taxes are applicable)would be reinvested into principal. In an ideal world,it would be extremely income tax advantageous forthe bypass trust to be a grantor trust as to the surviv-ing spouse so that all federal (and potential state) in-come tax dollars could remain in the bypass trust.

the only assets that receive the basis increase, or is there someother mechanism to implement the General Basis AdjustmentRule?

23 Emphasis is made to ‘‘for this purpose’’ as there may beother reasons why a 5&5 Right may be advantageous; see, for ex-ample, the applicability of the estate tax credit for the tax on priortransfers under §2013.

24 In any event, the addition of a principal distribution powercould cause the valuation methodology to fall outside of a stan-dard actuarial calculation involving the 7520 Rate. See John A.Bogdanski, Federal Tax Valuation ¶5.07[4][b][ii] (Thomson Reu-ters 1996, with updates through April 2016), citing PLR 9811044,which involved the partition of a trust in which the income ben-eficiary possessed a discretionary right to receive income andprincipal for her lifetime, and the Service declined to issue an ad-vance ruling as to the amount of the gift from the income benefi-ciary to the remainder beneficiaries on account of the severance,stating that ‘‘[S]ince the gift is not an absolute right to distribu-tions of income or principal, it cannot be valued by use of thetables contained in Section 2512. Rather, the value of the giftshould be determined in accordance with the general valuationprinciples contained in [Reg. §] 25.2512-1.’’ While it may be thatsuch a valuation is not definable, nevertheless, it involves a muchmore complex approach to valuing the trust interests. See alsoSiegel, above n. 16, at 50.

25 T.C. Memo 2013-43. For an analysis of the court’s order andRule 155 computations issued in an unpublished opinion on Oc-tober 25, 2013, see Steve R. Akers, Estate of Kite v. Commis-sioner, LISI Estate Planning Newsletter #2185 (Jan. 21, 2014).

26 The court loosely refers to ‘‘the stock transferred to Mr.Kite’’ in the quoted sentence from footnote 9. However, whenread together with footnote 5 and the accompanying text in thebody of the opinion, it is clear that the court is referring to thestock transferred to the Lifetime QTIP Trust.

27 See Kerry A. Ryan, Kite: IRS Wins QTIP Battle but LosesAnnuity War, Tax Notes, 2013 TNT 239-9 (Dec. 12, 2013).

28 Note, however, that there are further potential issues with theapplicability of §1014(e), and, in particular, the disposition of as-sets that could potentially be subject to the provisions of§1014(e)(2). See Scroggin Article, above n. 3, at 8–10.

Tax Management Estates, Gifts and Trusts Journal

� 2016 Tax Management Inc., a subsidiary of The Bureau of National Affairs, Inc. 7ISSN 0886-3547

As stated above, once the Lifetime QTIP Trust iscreated, the trust is a grantor trust as to the donorspouse. Unlike traditional bypass trusts, upon the do-nee spouse’s death, regardless of whether the Result-ing Trust is a bypass trust or QTIP trust, or both, it ispossible to structure the Resulting Trust (or Trusts) tobe grantor trusts as to the donor spouse. This can oc-cur even though the Lifetime QTIP Trust assets havebeen included in the donee spouse’s gross estate un-der §2044. This result is achieved by applying the lan-guage of Reg. §1.671-2(e)(5), which provides, in per-tinent part:

If a trust makes a gratuitous transfer of prop-erty to another trust, the grantor of the trans-feror trust generally will be treated as thegrantor of the transferee trust. However, if aperson with a general power of appointmentover the transferor trust exercises that powerin favor of another trust, then such personwill be treated as the grantor of the trans-feree trust, even if the grantor of the transf-eror trust is treated as the owner of the trans-feror trust under subpart E of the InternalRevenue Code. (Emphasis added.)

Pursuant to this regulation, absent the donorspouse’s death, a change in the taxpayer for incometax purposes occurs only if someone other than thegrantor spouse possesses a general power of appoint-ment over the particular trust and actually exercises itin favor of another trust. Recall that prior to the intro-duction of §2056(b)(7) under the Economic RecoveryTax Act of 1981, the primary manner in which a sur-viving spouse’s terminable interest could qualify forthe marital deduction was if the surviving spousewere granted a general power of appointment over thetrust principal. The theory for this was that the gen-eral power of appointment granted the spouse virtualownership of the property.29 Reg. §1.671-2(e)(5) fol-lows the same logic. If the donee spouse were granteda general power of appointment and exercised it, thedonee spouse would have actual ownership and wouldhave appointed the property however he or shepleased; for this reason, he or she should become the‘‘grantor’’ of the property. However, with a QTIPelection, the effect is a ‘‘fiction’’ in terms of actualcontrol. It is possible to qualify a trust for the QTIPelection even if the donee/deceased spouse were onlygiven the income from the trust with no discretionaryprincipal or the granting of a testamentary limitedpower of appointment. For this reason, since the

donee/deceased spouse lacks actual control over theLifetime QTIP Trust property, there should be no shiftin grantor status.30 Therefore, as a result of inter-vivosplanning, the scenario is created under which a By-pass Resulting Trust can be exponentially enhancedby the ability to retain the income tax dollars withinthe trust.31

One final benefit to this analysis — there is nocomparable rule to the One Year Rule of §1014(e)with respect to Reg. §1.671-2(e)(5) and ‘‘grantortrust’’ status. Therefore, even if the donee spouse dieswithin one day after the Lifetime QTIP Trust has beencreated, the provisions of Reg. §1.671-2(e)(5) shouldapply as to the Resulting Trust.

CREDITOR PROTECTIONIn addition to tax planning, an additional key to the

Deathbed Strategy is grounded in state law. Certainasset protection features are available if all trusts cre-ated under the Lifetime QTIP Trust are governed un-der the laws of either an SST State or a Quasi-SSTState.

Creditor Protection During H’sLifetime

As described above, the Lifetime QTIP Trust is anirrevocable trust under which W, as the settlor, has notretained any current interests. For the duration of H’slifetime, H is the sole current recipient of trust incomeand, depending on the trust provisions, will be thesole recipient of discretionary principal distributions.

29 Richard B. Stephens, Guy B. Maxfield, Stephen A. Lind &Dennis A. Calfee, Federal Estate and Gift Taxation, ¶5.06(WG&L, 9th ed. 2013, with updates through June 2016), citing S.Rep. No. 80-1013, at 1238 (1948), reprinted in 1948-1 C.B. 285,342.

30 See Jeffrey N. Pennell, Myths, Mysteries, & Mistakes, §3.Note that Reg. §1.671-2(e)(5) was released in T.D. 8831 on Au-gust 23, 1999, or 17 years after Congress passed the QTIP legis-lation, so if Treasury intended to include QTIP trusts as part ofthis regulation, it would have done so. Since Treasury did not in-clude references to QTIP trusts within Reg. §1.671-2(e)(5), elect-ing QTIP treatment does not convert ‘‘grantor trust’’ status.

31 As to the bypass trust, the benefits include having the donorspouse pay the income tax on the income earned by the bypasstrust, which enhances the bypass trust by preserving the assets thatwould otherwise have been used to pay such income taxes, that is,‘‘supercharging’’ the bypass trust. See Mitchell M. Gans, JonathanG. Blattmachr & Diana S. C. Zeydel, Supercharged Credit Shel-ter Trust,SM 21 Prob. & Prop. 52 (July/Aug. 2007); and JonathanG. Blattmachr, Mitchell M. Gans & Diana S. C. Zeydel, Super-charged Credit Shelter TrustSM versus Portability, 28 Prob. &Prop. 10 (Mar./Apr. 2014). See also American Bar AssociationSection on Real Property Trust and Estate Law, Estate Tax Com-mittee of the Income and Transfer Tax Group, Portability — TheGame Changer, 47 U. Miami Heckerling Inst. on Est. Plan. (Jan.2013) available at http://apps.americanbar.org/dch/committee.cfm?com=RP512500); Richard S. Franklin & Lester B.Law, Portability’s Role in the Evolution Away from TraditionalBypass Trusts to Grantor Trusts, 37 Tax Mgmt. Est., Gifts & Tr.J. 135 (Mar./Apr. 2012).

Tax Management Estates, Gifts and Trusts Journal8 � 2016 Tax Management Inc., a subsidiary of The Bureau of National Affairs, Inc.

ISSN 0886-3547

As is the case with most irrevocable trusts, the Life-time QTIP Trust will likely include a ‘‘spendthriftclause,’’ which provides, in general, that the holder ofa beneficial interest in the trust may not transfer or as-sign such interest and that such interest may not beused to satisfy the obligations of any creditors of theinterest holder. It is important to include a spendthriftprovision because some states mandate spendthriftprotection while other states require it to be part of thetrust agreement.32

In the Example, because H did not create the trust,H’s interest in the Lifetime QTIP Trust should be pro-tected from H’s creditors (but this protection endsonce income is actually distributed to H because H’sincome right is mandatory and, once distributed to H,the income then becomes H’s property).33 The use ofthe spendthrift provision for H’s income interest is a

standard feature that would be found in almost everyirrevocable trust. Where the Deathbed Strategy devi-ates from the norm is upon H’s death.

H’s Death — Protection for WUpon H’s death, as set forth above, the Lifetime

QTIP Trust provides for an interest in W in the Re-sulting Trust, which is a discretionary trust interest forW (in the form of a bypass trust), a mandatory incometrust interest for W (in the form of a QTIP trust), orboth.

At first glance, once the Resulting Trust is created,W, who created the Lifetime QTIP Trust, now has abeneficial interest in a trust created under the LifetimeQTIP Trust. In other words, the Resulting Trust istechnically an SST for W’s benefit and, as previouslystated, most states do not provide creditor protectionfor such self-settled interests. As the objective is toprovide creditor protection for W, the Lifetime QTIPTrust must be established in either an SST State or aQuasi-SST State. In the Example, because W estab-lished the Lifetime QTIP Trust under Florida law, andsince Florida is a Quasi-SST State, W’s interest in theResulting Trust will be protected from the claims ofher creditors after H’s death.34

Most importantly, unlike §1014(e), state law doesnot impose a One Year Rule. As the One Year Rule ispurely a tax concept, none of the SST States nor the

32 Under the Uniform Trust Code (UTC), spendthrift protectionmust be specifically elected. The approach under the UTC is oneof negative inference, as UTC §501 provides that, to the extent abeneficiary’s interest is not subject to a spendthrift provision, thecourt may authorize a creditor or assignee of the beneficiary toreach the beneficiary’s interest by attachment of present or futuredistributions to or for the benefit of the beneficiary or other means.The UTC then explains the nature of a ‘‘spendthrift provision’’ inUTC §502, which provides that (a) a spendthrift provision is validonly if it restrains both voluntary and involuntary transfer of abeneficiary’s interest; (b) a term of a trust providing that the inter-est of a beneficiary is held subject to a ‘‘spendthrift trust,’’ orwords of similar import, is sufficient to restrain both voluntary andinvoluntary transfer of the beneficiary’s interest; and (c) a benefi-ciary may not transfer an interest in a trust in violation of a validspendthrift provision and, except as otherwise provided in this[article], a creditor or assignee of the beneficiary may not reachthe interest or a distribution by the trustee before its receipt by thebeneficiary. This trend is carried forward by states that adopt theUTC, for example, Fla. Stat. §736.0501 and §736.0502. In otherstates, spendthrift protection is the default, for example, N.Y. Est.Powers & Trusts Law §7-3.1(b)(2), which provides:

All trusts, custodial accounts, annuities, insurance con-tracts, monies, assets, or interests described in subpara-graph one of this paragraph shall be conclusively pre-sumed to be spendthrift trusts under this section andthe common law of the state of New York for all pur-poses, including, but not limited to, all cases arisingunder or related to a case arising under sections onehundred one to thirteen hundred thirty of title elevenof the United States Bankruptcy Code, as amended.

33 Although beyond the scope of this article, questions aboundas to certain protection afforded to discretionary distributions asto exception creditors. For example, pursuant to Nev. Rev. Stat.§163.419(4), unless otherwise provided in the trust instrument, re-gardless of whether a beneficiary has an outstanding creditor, atrustee of a discretionary interest may directly pay any expense onthe beneficiary’s behalf and may exhaust the income and principalof the trust for the benefit of such beneficiary. The protection af-forded by this provision is all-encompassing and is not subject tothe rights of any exception creditor, such as a spousal paymentsor child support. See Steven J. Oshins, 4th Annual Dynasty TrustState Rankings Chart (http://www.oshins.com/images/Dynasty_Trust_Rankings.pdf) and 7th Annual Domestic Asset

Protection Trust State Rankings Chart (http://www.oshins.com/images/DAPT_ Rankings.pdf). Contrast this view with Fla. Stat.§736.0504(2), which provides that if a trustee may make discre-tionary distributions to or for the benefit of a beneficiary, a credi-tor of the beneficiary may not compel a distribution that is subjectto the trustee’s discretion, or attach or otherwise reach the inter-est, if any, which the beneficiary might have as a result of thetrustee’s authority to make discretionary distributions to or for thebenefit of the beneficiary. The Florida Second District Court ofAppeal, in Berlinger v. Casselberry, 133 So.3d 961 (Fla. Dist. Ct.App. 2013), distinguished between attaching the interest and at-taching distributions from the interest when it upheld an ex-spouse’s right as an exception creditor to attach discretionary dis-tributions from the interest. See also Barry A. Nelson, Bacardi onthe Rocks, 86 Fla. Bar J. 21 (Mar. 2012); Barry A. Nelson, Bac-ardi: The Hangover, 88 Fla. Bar J. 40 (Mar. 2014).

34 Fla. Stat. §736.0505(3) provides:

(3) Subject to the provisions of s. 726.105, for pur-poses of this section, the assets in:

(a) A trust described in s. 2523(e) of the InternalRevenue Code of 1986, as amended, or a trust forwhich the election described in s. 2523(f) of theInternal Revenue Code of 1986, as amended, hasbeen made; and

(b) Another trust, to the extent that the assets inthe other trust are attributable to a trust describedin paragraph (a), shall, after the death of the set-tlor’s spouse, be deemed to have been contributedby the settlor’s spouse and not by the settlor.

Tax Management Estates, Gifts and Trusts Journal

� 2016 Tax Management Inc., a subsidiary of The Bureau of National Affairs, Inc. 9ISSN 0886-3547

Quasi-SST States establishes a mandatory minimumperiod of duration for the donee spouse’s interest tomerit the creditor protection feature relating to the do-nor spouse’s interest in the Resulting Trust. Hence,W’s creation of the Lifetime QTIP Trust on H’s death-bed does not exclude the protection of W’s interest inthe Resulting Trust from the claims of her creditors.35

The asset protection feature of the Quasi-SST Stat-utes is applicable so long as the donor spouse makesa timely and proper gift tax QTIP election.36 If the do-nee spouse dies before the QTIP election is due to betimely made, a timely election can nevertheless bemade by his or her executor and such election is ret-roactive for federal transfer tax purposes.37 Becausethe Quasi-SST Statute is linked directly to the QTIPelection, presumably the protection provided by theQuasi-SST Statute should likewise be retroactive.

It is important to acknowledge that, while a Quasi-SST Statute ‘‘switches’’ the settlor for state law pur-poses only, such statutes have no effect on ‘‘grantortrust’’ status for federal income tax purposes. For ex-ample, the Florida Quasi-SST Statute (Fla. Stat.§736.0505(3)) provides that the donee spouse isdeemed to be the settlor but only after the doneespouse’s death.38 As described above, Reg. §1.671-2(e)(1) and §1.671-2(e)(2) provide that the donorspouse is the ‘‘grantor’’ for income tax purposes whenthe trust is created and continues as the ‘‘grantor’’even after the death of the donee spouse, unless, as setforth in Reg. §1.671-2(e)(5), the donee spouse isgiven, and exercises, a general power of appoint-ment.39 No reference is made within Reg. §1.671-2(e)to the effect of state law on ‘‘grantor’’ status, so it can

be concluded that state law has no effect on such sta-tus.

Negating a §2041 ArgumentLifetime QTIP Trust planning is not new — it has

been in existence for as long as the QTIP election hasbeen the law. However, due to enhanced awareness ofcreditor issues, practitioners began to focus on a newpotential wrinkle to the transfer tax consequences ofLifetime QTIP Trust planning.

Suppose in the Example that W is a resident ofNew York and not Florida. As stated above, Reg.§25.2523(f)-1(f) Exs. 10 and 11 provide clear guid-ance that the Bypass Resulting Trust for W’s lifetimeis not included in W’s gross estate upon her death.However, as described above, because the Bypass Re-sulting Trust is created under a trust document createdby W, and because the Bypass Resulting Trust benefitsW, the Bypass Resulting Trust is technically an SSTas to W, which means that W’s creditors can poten-tially reach a portion (or all) of the Bypass ResultingTrust. Recall that under §2041(b)(1), the basic defini-tion of a ‘‘general power of appointment’’ is a powerwhich is exercisable in favor of the decedent, his orher estate, his or her creditors, or the creditors of hisor her estate. If W’s creditors can reach a portion of aBypass Resulting Trust, would that portion then be in-cludible in W’s gross estate under §2041? Support forexcluding such property from W’s gross estate cannotbe found in Reg. §25.2523(f)-1(f) Exs. 10 and 11 be-cause those examples only refer to §2036 and §2038and do not contemplate gross estate inclusion under§2041. One alternative for avoiding this concern is toestablish the Bypass Resulting Trust in either an SSTState or a Quasi-SST State. If creditors cannot reachthe Bypass Resulting Trust, there should be no poten-tial §2041 gross estate inclusion of the Bypass Result-ing Trust. In the actual facts of the Example, the§2041 concern is avoided because the Lifetime QTIPTrust is established under Florida’s Quasi-SST Stat-ute.40

Interaction with ApplicableFraudulent/Voidable Statutes

The creditor protection feature of the Quasi-SSTStatutes is not elective or discretionary (i.e., it appliesif a Lifetime QTIP Trust is established, a timely gifttax QTIP election is made and the donor spouse re-

35 Also consider that the asset protection afforded by the Quasi-SST Statutes is seemingly not limited to residents of the particu-lar state having such a statute. For example, a resident of Georgia,which is neither an SST State nor a Quasi-SST State, could takesteps to properly establish a nexus to Florida when creating aLifetime QTIP Trust, such as using a Florida trustee and usingFlorida for the trust’s situs. This nexus would provide a basis forusing Florida law, thereby allowing the Georgia resident to takeadvantage of the creditor protection benefits of Florida’s Quasi-SST Statute.

36 Likewise, the QTIP election for transfer tax purposes causesthe donee spouse to be the deemed transferor for gift, estate andGST tax purposes. See Ubiquitous, above n. 7, at ¶1600.6[B].

37 See above n. 9.38 Most of the Quasi-SST Statutes invoke the protection only

after the donee spouse’s death and ignore any termination of thedonee spouse’s interest during his or her lifetime. Exceptions tothis general rule include Maryland (Md. Code, Est. & Trusts§14.5-1003(a)(2)(iii) (‘‘The individual’s interest in the trust in-come, trust principal, or both follows the termination of thespouse’s prior interest in the trust.’’)) and Michigan (Mich. Comp.Laws §700.7506(4) (preamble) (‘‘. . .that follows the terminationof the individual’s spouse’s prior beneficial interest. . .’’).

39 Moreover, most of the Quasi-SST Statutes specifically limitthe statute’s applicability to the particular state statute with a

clause such as ‘‘for purposes of this section.’’ That being said, theMaryland, Michigan and Oregon statutes are not so specificallynarrow, but it is unlikely that such a statute would be deemed bythe Service to have an effect on grantor trust status.

40 See Ubiquitous, above n. 7 at ¶1602.1[B].

Tax Management Estates, Gifts and Trusts Journal10 � 2016 Tax Management Inc., a subsidiary of The Bureau of National Affairs, Inc.

ISSN 0886-3547

tains a current beneficial interest in any ResultingTrust). However, there is one additional requirementin order to invoke this protection — the transfer maynot be in violation of the particular state’s fraudulenttransfer laws.

Under the law of most states, a transfer made or anobligation incurred by a debtor is voidable as to acreditor if the debtor made the transfer or incurred theobligation with actual intent to hinder, delay, or de-fraud any creditor of the debtor. Such voidability ispresent regardless of whether the creditor’s claimarose before or after the transfer was made or the ob-ligation was incurred.41 In terms of what is ‘‘actual in-tent,’’ such laws provide a non-exclusive list of ex-amples often referred to as the ‘‘badges of fraud.’’Some of the ‘‘badges of fraud’’ include the following:(a) the debtor retained possession or control of theproperty transferred after the transfer; (b) the transferor obligation was disclosed or concealed; (c) beforethe transfer was made or obligation was incurred, thedebtor had been sued or threatened with suit; (d) thetransfer was of substantially all the debtor’s assets;and (e) the debtor removed or concealed assets.42

As a result of such fraudulent transfer statutes, if Wis determined to have had the intent to avoid a spe-cific creditor, the transfer of property to the LifetimeQTIP Trust could be reversed. Not only would thetransferred assets be available for W’s creditors, butany tax advantages achieved by the transfer would benegated. This is not to say that every transfer involv-ing an asset protection technique is done with an in-tent to hinder, delay or defraud; on the contrary, if thedonor spouse had no pending creditor issues, fraudu-lent transfer statutes should not be a concern.

What if, however, after engaging in the DeathbedStrategy, W is involved in a transaction from whichlegal action is commenced, the result of which is ajudgment against W. Assume that W has no assetsavailable to satisfy the judgment. To what degree doesthe Deathbed Strategy intersect with the fraudulenttransfer law as to future creditors? In some Quasi-SSTStatutes, the intersection is direct — consider theopening language of the North Carolina Quasi-SSTStatute: ‘‘Subject to the Uniform Voidable Transac-tions Act, Article 3A of Chapter 39 of the GeneralStatutes. . . .’’43

As stated above, fraudulent transfer law applieswhether the creditor’s claim arose before or after thetransfer. The Deathbed Strategy involves taking ad-vantage of the creditor protection laws of either an

SST State or a Quasi-SST State, thereby presenting adefinite and acknowledged asset protection element tothe transaction. Is this ‘‘asset protection’’ intentenough to signify the ‘‘actual’’ intent needed to in-voke fraudulent transfer law? For example, under theExample, W transfers all of her $10 million of assetsinto the Lifetime QTIP Trust, and soon thereafter Hdies, with the Lifetime QTIP Trust providing for thebalance to pass into a discretionary Bypass ResultingTrust and a QTIP Resulting Trust. W has an interestin both Resulting Trusts. In effect, W will have trans-ferred all of her assets into the Lifetime QTIP Trust,which appears to satisfy one of the ‘‘badges of fraud.’’Even though she had no creditor issues at the timethat she created the Lifetime QTIP Trust, has W nowrun afoul as to a future creditor because she violatedone of the ‘‘badges of fraud’’? This is unclear and thisrisk should not be understated.

Potential Effect of the UVTA’s New §10and the UVTA Official Comments

The creditor issue is further enhanced if a stateadopts the UVTA and its courts apply the new Com-ments issued as part of the UVTA to the applicationof its UVTA law. If H and W are not residents of ei-ther an SST State or a Quasi-SST State, the ability toimplement the Deathbed Strategy may be hampered.

Section 10(b) of the UVTA (which is not present inthe UFTA) provides as follows:

(b) A claim for relief in the nature of a claimfor relief under this [Act] is governed by thelocal law of the jurisdiction in which thedebtor is located when the transfer is madeor the obligation is incurred.

Under pre-UVTA law, many individuals sought toachieve greater asset protection by creating SSTs, and,if the individual’s state of residence (Resident State)had not enacted SST legislation, the individual wouldcreate the SST in an SST State. If a judgment wererendered against the individual in the Resident State,and if the creditor sought to enforce the judgment inthe SST State, often a conflict of laws issue wouldarise, with the SST State denying the enforcement ofthe judgment due to the fact that the SST State allowsthe creation and protections afforded to SSTs.44

In adopting the UVTA, the Uniform Law Commis-sion was not shy about its purpose with respect to

41 See generally §4(a)(1) of the Uniform Fraudulent TransferAct (the ‘‘UFTA’’), which was revised in 2014 and renamed the‘‘Uniform Voidable Transactions Act’’ (‘‘UVTA’’).

42 See generally UFTA/UVTA §4(b).43 N.C. Gen. Stat. §36C-5-505(c).

44 Many articles have been written on this topic; for this par-ticular purpose, the authors cite George D. Karibjanian, Gerard‘‘J.J.’’ Wehle, Robert L. Lancaster & Michael A. Snerringer, TheNew Uniform Voidable Transactions Act: Good for the Creditors’Bar, But Bad for the Estate Planning Bar? — Part Two, LISI As-set Protection Planning Newsletter #317 (Mar. 15, 2016) (hereaf-ter ‘‘UVTA I’’) and George D. Karibjanian, Gerard ‘‘J.J.’’ Wehle& Robert L. Lancaster, History Has Its Eyes on UVTA — A Re-

Tax Management Estates, Gifts and Trusts Journal

� 2016 Tax Management Inc., a subsidiary of The Bureau of National Affairs, Inc. 11ISSN 0886-3547

SSTs — it wished to eliminate them. For example, inhis ‘‘White Paper’’ on the UVTA, Uniform Law Com-mission Reporter Kenneth C. Kettering stated:45

The avoidance laws of some jurisdictions aresubstantially debased by comparison with theUVTA. That is notably so in ‘‘asset havens’’that have eviscerated, or completely ex-punged, their avoidance laws, commonly aspart of a package of local laws that facilitatethe local formation of so-called ‘‘asset-protection trusts’’ by persons seeking toshield their assets from their creditors. . .Sec-tion 10 reflects the committee’s conclusion,which was to include no escape hatch in thestatutory text. It addresses asset tourismthrough a comment stating that a debtor’s‘‘principal residence,’’ ‘‘place of business,’’or ‘‘chief executive office’’ should be deter-mined on the basis of genuine and sustainedactivity, not on the basis of artificial manipu-lations.

In the seventh paragraph to new Comment 8 toUVTA §4 (Paragraph 7), the Uniform Law Commis-sion set forth its intentions regarding traveling to aparticular SST State to create an SST:46

By contrast, if Debtor’s principal residenceis in jurisdiction Y, which also has enactedthis Act but has no legislation validatingsuch trusts, and if Debtor establishes such atrust under the law of X and transfers assetsto it, then the result would be different. Un-der §10 of this Act, the voidable transfer lawof Y would apply to the transfer. If Y fol-lows the historical interpretation referred toin Comment 2, the transfer would be void-able under §4(a)(1) as in force in Y.

The effect of this particular provision and others47

is clear-cut — if the donor spouse’s Residence Statehas adopted the UVTA and is not either an SST Stateor a Quasi-SST State, and if the Lifetime QTIP Trustis established in either an SST State or a Quasi-SSTState, then, because the Resulting Trust is an SST, thetransfers to the Lifetime QTIP Trust are voidable perse. Thus, the assets are not free from the claims of thedonor spouse’s creditors, which can include future,presently unknown creditors. The interpretation of this

Comment cannot be clearer — the effect of this inter-pretation increases the risk of gross estate inclusion ofthe Bypass Resulting Trust in the donor spouse’s es-tate. Such a result clearly imperils the effectiveness ofthe Deathbed Strategy for this particular donorspouse.48

The concerns under Paragraph 7 as to future credi-tors are not, however, present if the Lifetime QTIPTrust is established by a resident of one of the Quasi-SST Jurisdictions under the law of his or her homestate. Consider this passage from Paragraph 7 that im-mediately precedes the above-quoted provision:49

If an individual Debtor whose principal resi-dence is in X establishes such a trust andtransfers assets thereto, then under §10 ofthis Act the voidable transfer law of X ap-plies to that transfer. That transfer cannot beconsidered voidable in itself under §4(a)(1)as in force in X, for the legislature of X,having authorized the establishment of suchtrusts, must have expected them to be used.(Other facts might still render the transfervoidable under §4(a)(1).)

Therefore, so long as the debtor did not violateother provisions of the UVTA in creating the LifetimeQTIP Trust, the transfer is not voidable per se.

Application of §1014(a) and CreditorProtection to Example

To summarize the effect of §1014(a) and applyingthe particular creditor protection statutes, supposethat, in the Example, W does not create the LifetimeQTIP Trust. Upon H’s death, W will have a beneficialinterest in a testamentary QTIP trust and a traditionalbypass trust created by H’s revocable trust, and shewill continue to own her $10 million of assets in herrevocable trust. H’s entire gross estate will be subjectto the General Basis Adjustment Rule of §1014(a).W’s beneficial interests created in the testamentarytrusts under H’s revocable trust would be protectedfrom W’s creditors by a standard spendthrift provi-sion.50 However, W’s revocable trust with her $10million of assets remains with a zero basis for incometax purposes and subject to the claims of her creditors.

If, however, W creates and funds the proposed Life-time QTIP Trust with $5.45 million (and makes a

sponse to Asset Protection Newsletter #319, LISI Asset ProtectionNewsletter #320 (Apr. 18, 2016) (hereafter ‘‘UVTA II’’).

45 UVTA I, above n. 44, at 3 (citing Kenneth C. Kettering, TheUniform Voidable Transactions Act; or, the 2014 Amendments tothe Uniform Fraudulent Transfer Act, 70 The Business Lawyer778 (Summer 2015), at 800-1).

46 UVTA I, above n. 44, at p. 4.47 Other Comments have an effect on the ability of creditors to

reach an SST. See, for example, Comment 2 to UVTA §4.

48 As set forth in both UVTA I and UVTA II, above n. 44, Com-ments are not adopted by states as part of their respective laws andare only intended to provide the Uniform Law Commission’s in-terpretation of a particular provision; however, many states willrely on the Comments, and it is with that background that greatattention must be paid to the Comments.

49 Comment 8 to UVTA §4.50 Creditors are, however, likely able to reach the income of the

QTIP once distributed to W.

Tax Management Estates, Gifts and Trusts Journal12 � 2016 Tax Management Inc., a subsidiary of The Bureau of National Affairs, Inc.

ISSN 0886-3547

timely gift tax QTIP election), upon H’s death, assum-ing that the value has not increased above $5.45 mil-lion, this amount passes to the grantor Bypass Result-ing Trust under the Lifetime QTIP Trust. Assumingthat W’s beneficial interests in the grantor Bypass Re-sulting Trust are limited to discretionary distributionsby an independent trustee, the authority for which isnot subject to an ascertainable standard, the GeneralBasis Adjustment Rule should also apply to adjust thebasis of this $5.45 million of assets to the fair marketvalue of such assets on H’s death. Additionally, thegrantor Bypass Resulting Trust is protected from W’screditors as a spendthrift trust created by H (i.e., as aresult of Florida’s Quasi-SST Statute). The formula inH’s revocable trust adjusts automatically to fund thetestamentary QTIP trust under his revocable trust withH’s $10 million of assets (i.e., because H’s AEA wasapplied to the Lifetime QTIP Trust). A standardspendthrift provision protects the testamentary QTIPtrust from W’s creditors.51 Therefore, in this permuta-tion, $15.45 million of the entire $20 million estate re-ceives an automatic basis adjustment to fair marketvalue on H’s death and is protected from W’s credi-tors.

Alternatively, if W funds the Lifetime QTIP Trustwith her entire $10 million of zero basis assets andshe makes a timely gift tax QTIP election, upon H’sdeath the $10 million is split between a grantor By-pass Resulting Trust and the secondary QTIP Result-ing Trust. As indicated above, the basis of the $5.45million of assets transferred to the grantor Bypass Re-sulting Trust will be adjusted to fair market value onH’s death. The $4.55 million of assets transferred tothe secondary QTIP Resulting Trust will likewise re-ceive a basis adjustment (which is potentially subjectto the Bifurcation Rule eliminating a basis adjustmentfor the portion representing W’s mandatory incomeinterest). Both Resulting Trusts will be protected fromW’s creditors pursuant to the Florida Quasi-SST Stat-ute as spendthrift trusts deemed to have been createdby H. The formula in H’s revocable trust will adjustautomatically to fund the testamentary QTIP trust un-der his revocable trust with H’s $10 million of assets.Therefore, in this permutation, at least $19 million52

of the entire $20 million estate (and possibly the en-

tire estate if the Bifurcation Rule does not apply) re-ceives an automatic basis adjustment to fair marketvalue on H’s death. In addition, regardless of the po-tential application of the Bifurcation Rule, the entire$20 million estate is protected from W’s creditors.53

PLAN IN ADVANCE FOR DEATHBEDLIFETIME QTIP TRUST

If the discovery of a spouse’s terminal illness issudden and death is truly imminent, there may not besufficient time prior to such spouse’s death to draft thenecessary paperwork and complete the asset transfersinto the Lifetime QTIP Trust. For this reason, considerplanning in advance and creating the Deathbed Strat-egy from within the couple’s current estate planningdocuments.

In the context of the Example, each of W’s and H’srevocable trusts could have provisions that trigger theestablishment of the Lifetime QTIP Trust upon a re-lease of the right to revoke all or a portion of the par-ticular revocable trust (the ‘‘Release’’). Suppose thatW’s revocable trust contains an article that providesthat if W executes a Release, the revocable trust be-comes irrevocable as to the assets subject to the Re-lease and such assets are immediately thereafter trans-ferred to a Lifetime QTIP Trust for H. The LifetimeQTIP Trust can be created either under a different pro-vision of the revocable trust, or under an inter-vivosdocument that is created at the time that the revocabletrust was modified to provide for the Release. Whensuch a deathbed situation arises, a one page Releasecould be quickly signed by the donor spouse, therebyimplementing the Lifetime QTIP Trust arrangement.

The ‘‘triggering’’ mechanism for the Release can bedescribed in the revocable trust as follows:

51 As previously stated, although the entire testamentary QTIPtrust would be protected, once the income is distributed to W, theincome in W’s hands is now available for W’s creditors.

52 If the $4,550,000 million passing to the secondary QTIP Re-sulting Trust is subject to the Bifurcation Rule, then, assumingthat W is 75 years of age and a 2.2% 7520 Rate, 21% of this trust,or $995,500, is subject to §1014(e) and receives no basis adjust-ment. The remaining portion of the secondary QTIP ResultingTrust, or $3,594,500, plus the $4,450,000 million grantor bypassResulting Trust and H’s $10,000,000 estate all receive an auto-matic basis adjustment.

53 A couple of planning ideas to consider: (i) the secondaryQTIP Resulting Trust could allow the independent trustee to havebroad authority to distribute assets back outright to W without cre-ating any adverse transfer tax consequences. See generally How-ard M. Zaritsky, Tax Planning for Family Wealth Transfers Dur-ing Life: Analysis With Forms, ¶3.07 (Thomson Reuters, 5th ed.2013, with updates through May 2016). Therefore, if the §1014(e)analysis as outlined herein is incorrect, or if the asset protectionadvantages of the Resulting Trust are not of a high concern to W,the independent trustee could distribute these assets back to W ifthe independent trustee determined that to be appropriate; and (ii)the testamentary QTIP under H’s revocable trust could also havea clause granting an independent trustee broad authority to distrib-ute assets to W. In the context of the Example, the testamentaryQTIP trust is neither exempt from estate taxes at W’s death or ex-empt from GST taxes, but it is protected from the claims of W’screditors with a spendthrift clause. If the independent trusteethought it was appropriate, assets of the testamentary QTIP couldbe distributed out to W so that she has some assets in her indi-vidual name and control without jeopardizing the automatic basisadjustment that would be available for $19 million of the aggre-gate estate. This possibility may give W more comfort in imple-menting the Deathbed Strategy.

Tax Management Estates, Gifts and Trusts Journal

� 2016 Tax Management Inc., a subsidiary of The Bureau of National Affairs, Inc. 13ISSN 0886-3547

If, at any time, the Settlor releases the rightunder Paragraph __ to amend or revoke thisDeclaration (the ‘‘Exercise’’), the propertyheld under this Declaration subject to suchExercise shall, as of the date of the Exercise,be disposed of as provided in Article __ ofthis Declaration. The Exercise may encom-pass all or a portion of this Declaration andthe assets herein contained. The Exerciseshall be effected by a written instrument ex-ecuted with the same formalities as requiredfor the execution of any amendment to thisDeclaration and shall be delivered to thethen-acting Trustee of this Declaration.

In effect, the exercise provisions would be analo-gous to disclaimer provisions — i.e., they remain dor-mant unless the spouse who would be the survivingspouse decides to execute the plan. In addition, de-pending on the applicable state law, the revocabletrust should allow an agent under a durable power ofattorney to implement the Release and the settlor’sdurable power of attorney should authorize the agentto implement such Releases.54 Notwithstanding theprovisions under applicable state law regarding the

formalities of executing documents relating to testa-mentary dispositions, it is highly recommended that,at a minimum, the Release be notarized. Since notari-zations require the insertion of the date of notariza-tion, the notarial clause can act as a validation that theRelease was executed prior to the death of the doneespouse.

CONCLUSIONThe Deathbed Strategy offers significant rewards,

particularly for individuals residing in one of the 17states with Quasi-SST Statutes (11 Quasi-SST Statesand six SST States with Quasi-SST Statutes),55 butthe strategy also carries risks. Implementation of thestrategy should be carefully considered and discussedwith the clients, as the strategy involves the relin-quishment of full fee ownership of assets by the do-nor spouse. The strategy is potentially subject to re-duced income tax benefits and, depending on the do-micile of the donor spouse, could be severelyhampered if the donor spouse’s Residence Stateadopts the UVTA and the donor spouse crosses statelines to form the lifetime QTIP in an SST State orQuasi-SST State. However, for those clients who fitwithin the parameters and who are not risk adverse,the strategy can provide significant income tax andcreditor protection advantages.

54 For example, while under Florida law, an attorney-in-factmay not create, amend or revoke a Will, Fla. Stat.§709.2202(1)(b) provides that the attorney-in-fact can, with re-spect to a trust created by or on behalf of the principal, amend,modify, revoke, or terminate the trust, but only if the trust instru-ment explicitly provides for amendment, modification, revocation,or termination by the settlor’s agent.

55 These are in addition to the 10 other SST States where self-settled trust protection is presumed even without a Quasi-SSTStatute.

Tax Management Estates, Gifts and Trusts Journal14 � 2016 Tax Management Inc., a subsidiary of The Bureau of National Affairs, Inc.

ISSN 0886-3547