Embed Size (px)

Citation preview

axncrement

inancingin New Orleans

April 2003

TIF

BGR Board of DirectorsLouis M. Freeman, ChairmanDavid Guidry,Vice ChairmanDionne M. Rousseau, SecretaryLynes R. Sloss, TreasurerLauren AndersonKim M. BoyleTerrel J. BroussardRobert W. BrownBertel DejoiePatricia C. DenechaudJean C. FeltsRussell S. HoadleyGeorge D. Hopkins, Jr.Jan S. JobeHans B. JonassenYvette JonesMaurice L. Lagarde IIIBetty V. LauricellaCarolyn W. McLellanRobert W. MerrickWilliam A. OliverRoger W. PeckR. Hunter Pierson, Jr.Robert D. ReilyGregory St. EtienneRoderick K. WestSterling Scott WillisAnn S. WinkLeonard Vance WormserMary K. Zervigon

Honorary BoardWilliam A. Baker, Jr.Bryan BellHarry J. Blumenthal, Jr.Edgar L. Chase IIIRichard W. Freeman, Jr.Ronald J. French, M.D.Paul M. HaygoodDiana M. LewisM. Hepburn ManyAnne M. MillingR. King MillingGeorge H. Porter III, M.D.Edward F. Stauss, Jr.

BGR EconomicDevelopment CommitteeTerrel J. BroussardJean C. FeltsLouis M. FreemanDavid GuidryMaurice L. Lagarde IIIRoderick K. WestSterling Scott WillisAnn S. Wink

BGR Project StaffJanet R. Howard, President & CEOPatricia E. Morris, Director of ResearchStephen Stuart, Research AnalystPeter Reichard, Research AnalystAmy T. Pease, PublicationsHelen L. Williams, Executive Assistant

AcknowledgmentThis report is the first of BGR’s studies onthe use of economic development incentivesin the City of New Orleans. BGR greatlyappreciates the financial support of the individuals, companies and foundations thatmade this study possible. The findings, conclusions and recommendations in thisreport are those of BGR and do not neces-sarily reflect the views of its financial supporters.

BGRThe Bureau of Governmental Research is a private, nonprofit, independent researchorganization dedicated to informed publicpolicy making and the effective use of public resources for the improvement of government in the Greater New Orleansmetropolitan area.

This report is available on BGR’s websitewww.bgr.org.

Bureau of Governmental Research225 Baronne Street, Suite 610New Orleans, Louisiana 70112Phone (504) 525-4152Fax (504) [email protected]

Tax Increment Financing in New Orleans

Table of Contents

Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . .1

I. Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .7

II. What is TIF? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .7

III. TIF in the United States . . . . . . . . . . . . . . . . . . . . . . . .8

IV. Why Do Local Governments Use TIF? . . . . . . . . . . . . .11

V. Criticisms of TIF . . . . . . . . . . . . . . . . . . . . . . . . . . . .12

VI. Special Issues with Sales TIF . . . . . . . . . . . . . . . . . . .14

VII. Louisiana TIF Statutes Relating to New Orleans . . . . .15

VIII. TIF Use in Louisiana . . . . . . . . . . . . . . . . . . . . . . . . .20

IX. Future TIF Use in New Orleans . . . . . . . . . . . . . . . . .24

X. Recommendations . . . . . . . . . . . . . . . . . . . . . . . . . . .27

Appendix A - St. Thomas TIF

Appendix B - World Trade Center TIF

Tax Increment Financing in New Orleans 1

EXECUTIVE SUMMARYRecently, the City of New Orleans hasturned its attention to a widely usedlocal economic development tool: taxincrement financing (TIF). Last fall theCity Council approved the City’s firstsales TIF district in connection with theredevelopment of the former St. Thomashousing project. Another financing planwith TIF-like characteristics utilizing thehotel occupancy tax is under considera-tion in connection with the proposedconversion of a portion of the WorldTrade Center into a hotel. A bill to cre-ate a TIF district for the Lake ForestPlaza Shopping Center site was recentlyintroduced into the State Legislature.Another to create a TIF district for alarge portion of eastern New Orleanshas been filed. In May, City Council willconsider a TIF-like arrangement for aLowe’s Home Improvement Warehouse.Recognizing the importance of the issue,City Council has begun to develop policies and procedures to govern theuse of TIF.

What is TIF?TIF is a financing mechanism thatenables a local government to capturenew tax revenues generated in a desig-nated area and reinvest them in thatarea to fund improvements. The localgovernment freezes the tax base in theTIF district at the pre-development levelfor a period of years.1 Taxing bodiescontinue to receive the taxes on the pre-development base, but the incrementaltaxes are applied to infrastructure andother improvements designed to spurprivate sector development. In theory,the TIF district finances its own revital-ization and eventually generates largertax revenue for the community as a whole.

A Brief CritiqueTIF provides cash-strapped municipali-ties – of which New Orleans surely isone – with a means of making invest-ment in infrastructure and economicdevelopment projects under severefinancial and political constraints. TIFhas tremendous political appeal in thatit can be implemented without raisingtaxes and, in many cases, withoutobtaining voter approval. It has a cer-tain conceptual beauty in that theinvestment is, in theory, self-financingand the development supporting itwould not have occurred otherwise.

Under closer scrutiny, the underlyingpremise that a TIF is self-financing isopen to question. Because of the diffi-culty of making long-range projections,it is difficult to assess whether develop-ment in an area would have occurredwithout TIF. It is even more difficult todetermine whether, and to what extent,gains in a TIF district are offset by stag-nation, decline, or reduced growth inother areas and businesses. To theextent that other areas and businessesare negatively impacted, the existingrevenue base of the local government is reduced. In addition, successful TIFdistricts can increase a local govern-ment’s operating costs without providingadditional operating funds to the localgovernment. The end result in that caseis a transfer of the additional operatingcosts to residents outside the TIF district.

Given the many unknowns surroundingthe performance of TIF districts, and thetypes of dislocations that can occur, it isexceedingly dangerous to view TIF asfree money. Rather, TIF should be con-sidered an allocation of future resourcesand assessed with a stringency befitting

2 Bureau of Governmental Research

other long-term investments of futurerevenue. The investment should bemade only if it is effective, efficient,equitable, and in furtherance of adefined public policy.

For reasons discussed below, propertyTIF, the most widely used form of TIF, ispreferable to sales TIF. Unfortunately,because of the nature of the local taxstructure, property TIF is less practicalin New Orleans than in other jurisdic-tions. In Louisiana, property TIF canonly capture taxing bodies’ ad valoremmillage that is not dedicated to a specialpurpose. In 2001, undedicated millagefor the City of New Orleans was 14.91mills out of 169.29 total mills collectedin New Orleans. Thus, for every $1 mil-lion of incremental assessed value (or$6.6 million of fair market value), only$14,910 out of $169,290 in total proper-ty taxes paid would be available for aTIF district. If the general millages of theOrleans Parish School Board andOrleans Levee Board are subject to cap-ture (a matter which is unclear), anadditional $15,500 would be availablefor TIF. The homestead exemption andthe exemptions enjoyed by nonprofits,government, and some industries fur-ther diminish the potential of propertyTIF use by reducing the tax base.

The tax structure, combined withrequirements for voter approval of bondsbacked by property tax increments (butnot for bonds backed by sales tax incre-ments), skews the use of TIF towardsales TIF. This is unfortunate, becausesales TIF suffers from more seriousproblems than does property TIF:

t Sales tax revenues are more volatilethan property tax revenues, a factthat makes sales TIF debt financ-ing riskier and more expensive.

t Sales TIF districts are more likelythan property TIF districts to cap-ture revenues unrelated to TIFinvestment, thus reducing currenttax revenues available to the juris-diction.

t Because sales TIF districts needlarge, creditworthy retailers orshopping centers to generate sig-nificant tax increments, the questfor a TIF source can lead to landuse distortions, unnecessary subsi-dies for big retailers, and a distor-tion of a local government’s invest-ment priorities.

t Subsidizing a retail operation withTIF revenues gives it an unfairadvantage over its competitors.

t Unless contractually constrained,the retailer can enjoy the TIF sub-sidy and deprive the local govern-ment of projected benefits bydeparting when the TIF periodends.

There are other factors that suggest thatTIF might not provide the most effectivesolution to blight or economic develop-ment issues. Regardless of the type ofTIF, because the repayment obligation islimited to a specific funding source, TIFdebt is more expensive than generalobligation debt. Whether the premiumpaid to limit the obligation is worthwhilewill depend on the particular circum-stances. In some cases, such as the St.Thomas TIF, it is clear that the Citycould save millions of dollars in tax revenue by issuing lower-interest gener-al obligation bonds. The capacity toissue such debt exists under the City’sdebt limit, which is 35% of grossassessed value, or $816.8 million as

Tax Increment Financing in New Orleans 3

of Dec. 31, 2002. Debt outstanding as of late February was $473.4 million, or58% of capacity.

As in the use of other economic develop-ment incentives, the effective, efficient,and equitable use of TIF depends on thewisdom, financial sophistication, andintegrity of those involved in the pro-cess. To the extent that decisions arebased on sophisticated analysis, madewith an unwavering focus on the publicgood, and implemented through skillfulnegotiation, the chances of successfullyusing TIF increase. To the extent thatdecisions are driven by relationships,political deals, and other agendas, orthat the government lacks the high level of expertise needed to analyze andimplement complicated transactions,TIF is likely to be an expensive mistakethat results in an unnecessary transferof wealth to private entities.

The potential problems associated withTIF are more than theoretical. NewOrleans’ two TIF districts – oneapproved for the St. Thomas redevelop-ment and another under considerationfor the proposed World Trade Centerhotel – provide case studies of the prob-lems. A summary of the problems asso-ciated with these TIF districts can befound on pages 21 to 23 of this report.More detailed information is available in the appendices.

The trend with respect to TIF is disturb-ing. In just the past month, CityCouncil has received a proposal for aTIF-like arrangement for a Lowe’s, a bill has been introduced to create a TIFdistrict for Lake Forest Plaza shoppingmall, and another bill has been filed tocreate one for eastern New Orleans.Collectively and individually, they raiseserious concerns, including the specter

of businesses routinely turning to theCity for subsidies and the prospect offreezing the tax base for a huge swath of the City.

As noted above, the effective use ofproperty TIF in New Orleans is severelylimited by the prior dedication of mostof the tax revenues. Ironically, thewidespread use of sales TIF would cre-ate a similar limitation on government’sfuture flexibility by converting unre-stricted tax revenues into dedicatedtaxes. In addition, the proliferation oflong-term dedications will contribute tothe balkanization of government withinthe City, even as the community focusesincreasingly on regionalism.

Given the potential expenses, risks, and abuses associated with TIF, theCity should use TIF cautiously and onlyin tightly circumscribed conditions.BGR believes that the City should aban-don completely the use of TIF and TIF-like arrangements based on sales andhotel occupancy taxes and restrict theuse of TIF based on property taxes topublic infrastructure and pre-develop-ment improvements in blighted areas.

Strict parameters for the use of TIFshould be established at the state levelthrough revision of TIF statutes and atthe local level through the adoption ofstringent policies and procedures.Specific recommendations for changesin legislation and the establishment ofCity policies and procedures for the useof TIF are set forth below.

4 Bureau of Governmental Research

RECOMMENDATIONS

State Legislationt State law should impose severe

limitations on TIF based on salesand hotel occupancy taxes, limitingtheir use to “main street” programsdesigned to revitalize commercialcenters of smaller municipalities.The use of sales TIF for large-vol-ume, major retail stores and shop-ping malls should be prohibited.

t The state should eliminate TIF leg-islation designed to accommodatespecific projects. It should estab-lish a cohesive set of general lawsto replace the multitude of statuteson the books.

t State law should limit the use ofTIF to blighted areas and requirelocal governments to make a find -ing that an area is blighted. Thestatutes should define the specificcharacteristics of blighted propertyand define a blighted area in quan-titative terms.

t State law should include a mean-ingful “but for” test conditioningthe use of TIF on a finding that TIFis necessary for appropriate, futureredevelopment (as opposed to aspecific project) to occur in a desig-nated area.

t State law should limit TIF expendi-tures to prep work needed to makethe urban landscape more attrac-tive for investment. Eligible costsshould include expenditures forpublic improvements, such asstreets and sewer and water sys-tems, demolition, site preparation,property assembly, and

environmental clean-up. TIFshould not be used to providefunding for privately owned pro-jects and assets.

t State law should limit the durationof TIF districts.

City Policies andProceduresBGR recommends that the City imple-ment the following recommendationsregardless of whether state law ischanged.

Master Planning

t Before allowing additional TIF dis-tricts, the City should develop andadopt a city-wide economic devel-opment plan. Any TIF districtshould conform with, and promotethe objectives of, the economicdevelopment plan.

t As part of the economic develop-ment plan, the City should developa city-wide master plan for TIF. Itshould designate areas of the Citythat are eligible for TIF and estab-lish detailed criteria and prioritiesfor authorizing TIF districts withinthem. The plan should be based onan in-depth expert analysis of theCity and should be prepared andadopted after city-wide public hearings.

t The TIF master plan and all TIFdevelopments should conform withthe master plan for the City.

t To encourage prioritization andcareful targeting of projects, theCity should establish a cap, basedon a dollar amount or a percentageof the City’s General Fund, on the

Tax Increment Financing in New Orleans 5

amount of taxes that can be divert-ed from the General Fund to TIFdistricts.

Criteria for TIF

t In view of the problems associatedwith their use, the City shouldabandon the use of TIF based onsales taxes or hotel occupancytaxes.

t The City should identify, and desig-nate as eligible for TIF, blighted orbrownfield areas that offer thegreatest potential for development,assuming an appropriate amountof public funding. Blight should bedefined in meaningful, quantitativeterms to reduce the risk of theunnecessary use of TIF.

t To limit the use of TIF to areas inwhich development would not oth-erwise occur, the City should con-dition the use of TIF on a findingthat TIF is necessary for appropri-ate, future redevelopment (asopposed to a specific project) tooccur in the designated area.

t The City should establish stringent,minimum standards for consider-ing TIF districts. These shouldinclude, among other things,requirements for significant equityinvestment by the developer/owner, high ratios of private topublic investment, and a findingthat projected net benefits to theCity exceed projected costs by asignificant margin (e.g., 200 to300%). The criteria should beviewed as minimum eligibilityrequirements, rather than asauthorization for any transactionthat satisfies them.

Review Process

t The City should require detailedsupporting documentation that willenable it to determine whether aproposed TIF district is necessary,viable, and rewarding. Basic docu-mentation would include cost-ben-efit analyses and financial feasibili-ty studies prepared for the City byindependent consultants. In thecase of public-private partnerships,the City should gather additionaldetail through the developer’s/owner’s financial statements,detailed projections (including cashflow and revenues and expenses),rate of return and profitabilityanalyses, and, where appropriate,independent market studies.

t The analysis of a proposed TIF dis-trict should include a comparisonof the cost of tax increment financing against alternativefinancing methods, including theissuance of general obligationbonds.

t The City should establish a uni-form system for evaluating andapproving TIF districts.

t The evaluation should include care-ful scrutiny and evaluation of cost-benefit and other analyses. Factorssuch as the duration of the TIFand the percentage of incrementaltaxes subject to reinvestment inthe district should be pegged to theprojected costs and benefits, inaccordance with predeterminedstandards.

t To protect the interest of the City’sresidents and taxpayers, the Cityshould obtain advisors or staff withthe sophisticated financial, legal,

and managerial expertise needed toevaluate, implement, and monitorsuch districts effectively.

Requirements to EnsureObjectivity and Accountability

t Developers and owners of TIF pro-jects should be required to providethe City with the information nec-essary to compare projected bene-fits with actual benefits on anongoing basis.

t The City’s TIF policy should includeprovisions to reduce the life of theTIF if the developer fails to meetprojections, provided that obliga-tions under TIF bonds are notimpaired.

t TIFs for projects should includearrangements that allow the publicto recoup, to the extent possible,its investment from the develop-er/owner if the projected publicbenefits do not materialize.

Minimizing Investment andMaximizing Return

t The City’s TIF policy should requirea significant equity investment bythe developer/owner comparable tothe investment that would berequired by a private lender.

t TIF investments should be struc-tured to allow the City to recaptureall or a portion of the public sub-sidy to the extent practicable,through mechanisms such as long-term ground leases, subordinatedloans, and revenue participations.

t The life span of a TIF districtshould be restricted to a reason-able period. In no case should the

duration of a TIF district and itsbonds exceed the shorter of 20years or the expected life of theproject supporting the TIF.

t TIF funds should be redirected tothe City’s General Fund after theTIF period expires or when they areotherwise not required for the TIFdistrict generating them. Cross-subsidization of other TIF districtsshould not be permitted.

Transparencyt All meetings relating to TIFs should

be conducted in accordance withboth the letter and the spirit of theopen meetings law. Practices thatundermine transparency, such asone-on-one briefings and behind-closed-door negotiations betweencouncilmembers and potentialdevelopers/owners, should beavoided.

t All documentation relating to TIFsshould be available to the public.

t City Council should provide thepublic on an annual basis with areport on TIF districts, includingthe amount of public funds dedi-cated to TIF and the performanceof the various districts.

6 Bureau of Governmental Research

Tax Increment Financing in New Orleans 7

I. INTRODUCTIONRecently, the City of New Orleans hasturned its attention to a widely usedlocal economic development tool: taxincrement financing (TIF). Last fall theCity Council approved the City’s firstTIF district in connection with the rede-velopment of the former St. Thomashousing project. Another district withTIF-like characteristics has been pro-posed in connection with the conversionof a portion of the World Trade Centerinto a hotel. A bill to create a TIF dis-trict for the Lake Forest Plaza ShoppingCenter site was recently introduced intothe State Legislature. Another to createa TIF district for a large portion of east-ern New Orleans has been filed. In May,City Council will consider a TIF-likearrangement for a Lowe’s HomeImprovement Warehouse. Anticipatingadditional TIF proposals, the CityCouncil has begun to develop policiesand procedures to govern the use of TIF in the future.

As local governments have struggled todeal with increased blight and dimin-ished resources, TIF has increased inpopularity. However, whether it is effec-tive and efficient has been the subject of growing debate. Proponents of themechanism maintain that TIF createsmore jobs, greater property values, moretax revenues, and revitalized blightedareas. Critics dispute the effectivenessof TIF as an economic development tooland raise questions about the cost andequity of the financing mechanism.

In this report, BGR:

t provides an overview of the use ofTIF around the United States,

t reviews the perceived benefits ofTIF, as well as the pitfalls andpotential abuses associated withthe mechanism,

t describes Louisiana law,

t reviews the TIF approved for theformer St. Thomas site and the TIFproposed for the World TradeCenter, and

t makes recommendations concern-ing state law and the future use ofTIF in New Orleans.

II. WHAT IS TIF?TIF is a financing mechanism thatenables a local government to capturefuture incremental tax revenues in adesignated area and reinvest them inthat area to fund public improvements.Basically, the local government freezesthe tax base in the TIF district at thepre-development level for a period ofyears.2 Taxing bodies continue to receivethe taxes on the pre-development base,but the incremental taxes are applied toinfrastructure and other improvementsdesigned to spur private sector develop-ment. In theory, the TIF district financesits own renewal and eventually gener-ates greater tax revenue for the commu-nity as a whole.

The establishment of a TIF involves anumber of decisions, including:

t the designation of the geographicarea for the TIF district,

t the development of a plan forimprovements in the district,

t the designation of the tax incre-ment to finance the improvements,

8 Bureau of Governmental Research

t in some cases, the establishment ofa TIF authority, and

t the designation of the financingmechanism.

These are discussed more fully below.

III. TIF IN THE UNITED

STATES

A. OverviewIn 1952, California became the firststate to authorize TIF, allowing redevel-opment agencies to use TIF to provide alocal match for federal funding of urbanrenewal projects.3 The mechanismenabled cities to force other tax recipi-ent bodies in the improved area to con-tribute to the cost of urban renewal.Prior to that time, the cities alone borethe cost of the local match, while all taxrecipient bodies benefited from theincreased tax base.

Nationwide, TIF did not gain widespreadpopularity until the 1970s. In thatdecade, the federal government beganreducing the amount of funds availablefor urban renewal. States and cities,seeking to fill the gap with tax increas-es, met with opposition.4 In addition,the imposition of tax and expenditurelimits on local governments, such asCalifornia’s Proposition 13, severelyrestricted the ability of local govern-ments to raise property taxes and issuedebt. The trends of federal spendingcuts and voter opposition to new taxescontinued in the 1980s and 1990s,leading many states to adopt TIF legislation to facilitate infrastructureand economic development.5

Today, 47 states and the District ofColumbia authorize the creation of newTIF districts. The most active users ofthe financing mechanism includeCalifornia and several Midwesternstates. About three-fourths of Californiacities have now established redevelop-ment agencies, the authorities that canuse TIF.6 As of the late 1990s,Minnesota had established more than1,700 TIF districts; Wisconsin, morethan 800; Illinois, more than 400.7 Theuse varies widely among cities. Chicagohas more than 120 TIF districts; NewYork City has none.

B. Variations on a ThemeTIF statutes vary widely as to the crite-ria for designating a TIF district, permis-sible uses, the types of taxes used, themaximum term for a district, and therequired procedures.

1. Designating a TIF District

Use of TIF begins with the establish-ment of a TIF district, the geographicarea in which incremental taxes will becaptured and applied to improvements.TIF districts can be drawn tightlyaround one development project orbroadly around an entire neighborhood.Two of the more common requirements– a finding of blight and satisfaction ofthe “but for” test – are discussed below.

Blight. Reflecting the genesis of TIF as a tool for urban revitalization, 18 statescondition the use of TIF on a finding ofblight. In 15 of the 18 states, blight isdefined in qualitative terms by referenceto characteristics such as the presenceof abandoned buildings and excessivevacancies. The other three states quantify blight. For example, Alabamarequires at least 50% of the buildings

Tax Increment Financing in New Orleans 9

in a redevelopment district to fit thestatutory criteria for blight.8 Louisianadoes not require a finding of blight.

Over the years, the blight requirementhas often been loosely interpreted, lead-ing to the use of TIF in suburbs andother areas that are not blighted.Several states that require a blight finding, including California and Illinois,have sought to strengthen the connec-tion between TIF investment and urbanredevelopment by enacting stricter standards.

“But For” Test. Seventeen states andthe District of Columbia require localgovernments to determine that develop-ment would not occur “but for” the TIF.The test is formulated differently in thevarious statutes.

Twelve of the 17 states require a findingthat TIF is necessary for any redevelop-ment to occur. Illinois, for example, pro-hibits approval of a TIF redevelopmentplan unless the “municipality finds thatthe redevelopment project area on thewhole has not been subject to growthand development through investment by private enterprise and would not rea-sonably be anticipated to be developedwithout the adoption of the redevelop-ment plan.”9

The other five states and the District ofColumbia focus on whether the specificdevelopment would occur. Nebraska, forexample, requires the local governmentto find that “the redevelopment projectin the plan would not be economicallyfeasible without the use of tax incre-ment financing.”10

Louisiana does not impose a “but for”test.

2. Permitted Uses

The purposes for which TIF revenuescan be expended vary from state tostate. All 47 TIF states authorize the useof TIF funds for public works andinfrastructure and a variety of sitepreparation and pre-development activi-ties. Some of the more common activi-ties include property assembly, demoli-tion, clearing and grading of land, andadministrative expenses.

Only five states restrict the use of TIFfunds to infrastructure, site preparation,and pre-development activities. Theother 42 states have added building renovations as eligible uses.

Of the 42 states, 33 also allow newbuilding construction for a variety ofpurposes. These include 15 states inwhich private use or ownership isexplicitly allowed by the statutes.

Many states allow a wide range of devel-opments in a TIF district. These mayinclude affordable housing, manufactur-ing plants, hotels, sports stadiums,downtown improvement, and historicrenovations. Some states imposerequirements to address particularissues of concern. California and Texas,for example, set aside portions of TIFrevenue for the construction or rehabilitation of affordable housing inthe TIF district.

Louisiana allows a broad array of devel-opment projects in a TIF district.

3. The Designated Tax Increment

Property tax is the dominant source ofrevenue for TIF. Forty-seven states andthe District of Columbia authorize TIFbased on property taxes.

10 Bureau of Governmental Research

BGR found that 13 states and theDistrict of Columbia currently authorizethe creation of new TIF districts basedon sales taxes. Some of these states per-mit the use of sales TIF for broad pur-poses similar to those for which proper-ty TIF can be used. Others restrict salesTIF to a more limited universe of pro-jects. For example, Wyoming and theDistrict of Columbia limit the use ofsales TIF to downtown districts; Kansasallows sales TIF only for historic the-aters, auto racetracks, and multi-sportathletic complexes.

California withdrew the authority to create sales TIF districts in 1993 out of concern that automobile dealerships,large-volume retailers, and other salestax generators were receiving unneces-sary subsidies, and that the sales taxpotential of projects was driving landuse and TIF decisions.11 Illinois is phasing out the use of sales TIF, whichwas based in that state on state salestaxes.12

A few states allow TIF for employment,hotel occupancy, and various entertain-ment taxes. Maine, for example, allowsthe reimbursement of a certain percent-age of state employment withholdingtaxes to be captured by a TIF district.

Louisiana allows TIF for property, sales,and, in certain cases, hotel occupancytaxes.

4. Limits on the Duration of TIFDistricts

At least 25 states with TIF statutesimpose limits on the duration of the TIF. With few exceptions, the time limitsrange from 20 to 30 years. Louisianastatutes do not limit the term to a specific number of years.

5. Required Documentation

State statutes vary as to the type of doc-umentation required for TIF. Althoughmost require formal redevelopmentplans, the contents of the plan varyfrom state to state. Plans may includethe following:

t Purpose and objectives of the TIF

t Official finding of blight in the proposed area

t The TIF district’s boundaries

t Proposed land use

t Proposed development activitiesand project timetables

t Sources and uses of public and private financing for these costs

t Terms of TIF bonds

t Economic impact or cost-benefitanalysis

t Estimate of tax impacts on localgovernments

t Other public costs

t Timeframe for paying off the TIF

In conjunction with the redevelopmentplan, some states require local govern-ments to prepare special studies.Examples include economic and finan-cial feasibility studies and neighborhoodand environmental impact analyses.While such studies can provide usefulinformation, they are also imprecise andsubject to manipulation. Accordingly,they must be used cautiously.

Some of Louisiana’s TIF statutes indi-rectly incorporate a requirement for aneconomic development plan. Others,such as the sales TIF statute for NewOrleans, do not. The state does notrequire any studies.

Tax Increment Financing in New Orleans 11

6. Financing Options

TIF improvements can be made andfinanced through a number of options.One option is for the local governmentto issue debt to finance an up-frontinvestment. A second option is for thelocal government to make and pay forimprovements on a cash basis as incre-mental tax revenue is collected. This iscommonly referred to as “pay-as-you-go”financing. The third is for a developer tofund projects up-front and receive reim-bursements as TIF proceeds arereceived.

Louisiana’s property and sales TIFstatutes applicable to New Orleans atlarge allow the local government to issuerevenue bonds. They are silent as topay-as-you-go financing and reimburse-ment of the developer.

IV. WHY DO LOCAL

GOVERNMENTS USE

TIF?Proponents of TIF cite the following benefits, some of which apply to othereconomic development tools.

Expected Benefits. As the above history indicates, TIF provides cash-strapped local governments with ameans of making infrastructure andother capital improvements. It enableslocal governments to undertake revital-ization and economic development projects that, given political realities,would not be feasible otherwise. If theprojects are carefully conceived and executed, the community enjoys multi-ple benefits: increased employment,improved environment, additional pri-vate investment, increased tax revenues,and civic pride.

TIF is perceived as a good mechanismfor encouraging and leveraging public-private partnerships to address issues of unemployment, poverty, and blight.By funding public infrastructureimprovements and demolition, sitepreparation, property assembly, andenvironmental clean-up costs, local gov-ernments make the urban landscapemore attractive for private investment.In a successful TIF district, the initialpublic-private investment attracts addi-tional private investment, multiplyingthe benefits of the initial investment.

Self-Financing Investment. Much ofthe popularity of TIF stems from theself-financing nature of the mechanism.In a pure TIF, the local government’srepayment obligation is limited to theincremental taxes generated in the TIFdistrict. In theory, these incrementalrevenues have been generated by theTIF investment. Thus, the public suffersno loss of revenues; it pays for thedevelopment out of funds that it wouldnot have otherwise received.

Limited Obligation. The limited natureof the obligation also contributes toTIF’s appeal. Because TIF indebtednessdoes not constitute a general obligation,the local government is not liable if theanticipated revenue stream does notmaterialize. In addition, TIF bonds gen-erally do not count against the munici-pality’s debt limit.13

Political Appeal. TIF has tremendouspolitical appeal for a variety of reasons.Most importantly, it allows local govern-ments to make the desired investmentwithout raising tax rates or cutting cur-rent expenditures. In most states, theinvestment can be made and supportingdebt issued without voter approval.14

12 Bureau of Governmental Research

Flexibility. TIF also provides local governments with significant flexibilityand control over the investment offuture tax revenue. In addition, TIFavoids the bureaucracy associated withintergovernmental revenue transfers.15

TIF’s local focus can lead to swifter government action to assist privatedevelopment than would otherwise bepossible. 16

Equitable Sharing of DevelopmentCosts. Prior to the development of TIF,the municipality or county was the onlylocal tax recipient body to bear the costof redevelopment. Other taxing bodiesthat would ultimately benefit from theincreased tax base made no contribu-tion. TIF legislation in many states distributes costs more fairly by forcingoverlapping tax recipient bodies to sharein the TIF investment.

V. CRITICISMS OF TIFAs the use of TIF has proliferated, themechanism has come under attack forbeing ineffective, inefficient, andinequitable. Critics claim that TIF has harmful side effects that negate orreduce benefits. These include the following:

Increased Costs Transferred toOthers. TIF can impose significantfinancial burdens on local governmentby increasing operating costs (such asfire and police protection) without pro-viding offsetting resources. The problemis particularly acute in states that provide for the capture of the tax incre-ment that would otherwise have gone tooverlapping tax bodies, such as schoolsystems.

In addition to increasing the costs ofgovernment, TIF can transfer financialburdens from certain groups of resi-dents to others. When taxes generatedwithin a TIF district are retained forphysical improvements, taxpayers out-side the district pick up the tab for anyincreased government services in theredevelopment area. Those outside thedistrict also cover the TIF district’s prorata share of the local government’soverhead and other general operatingcosts.

Negative Impact on Other Businesses.TIF can also confer benefits on certainbusinesses at the expense of others. For example, a successful TIF-supportedretail development will draw businessaway from retail businesses located outside the TIF district. A TIF for a hotel can provide the owner with a competitive pricing edge and drawguests away from non-subsidized hotels.The advantages provided by the publicsubsidy raise serious equity issues thatmust be carefully evaluated.

Reduced Operating Revenues. In addi-tion, to the extent that a business in aTIF district attracts sales from business-es outside the district but inside thelocal jurisdiction, the existing revenuebase of the local government is reduced.The general fund is deprived not only ofthe incremental revenues in the TIF dis-trict, but also of the tax revenues that itwould have received from adverselyaffected businesses.

Negative Impact on Other Areas. Asan unintended consequence, TIF dis-tricts can have a negative impact onunsubsidized areas by drawing invest-ment and revenues away from them.This is particularly true where there islimited demand for a good or service.

Tax Increment Financing in New Orleans 13

To the extent that development in theTIF district is offset by stagnation ordecline elsewhere in the taxing jurisdic-tion, the local government is engaged in a zero-sum game.

Intra-Regional Competition. On theregional level, TIF is sometimes used asa weapon in bidding wars for businessdevelopment. The use of TIF by localgovernments to lure businesses from aneighbor leads to a zero-sum game forthe region and state: one communitywins, one loses, but there is no netgain.17

Some states have enacted laws toaddress the piracy issue, particularlywith respect to retail stores:

t California prohibits any form offinancial assistance to an automo-bile dealership or large volumeretailer relocating from one com-munity to another in the samemarket area, unless the two com-munities enter into a sales tax-sharing arrangement.18

t Illinois prohibits the use of TIF tosubsidize a retailer relocating with-in a 10-mile radius, unless theclosed store is inadequate, obso-lete, or no longer in a viable retaillocation.19

t Maine’s employment TIF programrequires a finding that the TIFdevelopment will cause no sub-stantial harm to existing Mainebusinesses.20 In addition, a partici-pating retail business must demon-strate that it receives 50% or moreof its revenue from out-of-statesales or that increases in its saleswill not include sales shifted fromother Maine businesses.21

Expensive Funding. TIF bonds can bean expensive funding source. Becausethey are project-based or otherwisepayable from restricted sources, suchbonds can command a far higher inter-est rate than general obligation bonds.This is the downside of limiting the obli-gation to repayment from a specifiedsource, rather than pledging the fullfaith and credit of the government.

Unwarranted Private Subsidy. WhenTIF is used to fund public infrastructureimprovements, such as streets andsewer and water systems, and to pay for demolition, site preparation, propertyassembly, and environmental clean-upcosts, it represents a public investmentin the prep work needed to make theurban landscape more attractive forinvestment. TIF becomes more problem-atic when it is used to provide capitalfor privately owned projects and assets.In that case it acts as a circuitous taxabatement, redirecting public money toa developer/owner.

TIF is supposed to create conditionsthat encourage economically viabledevelopment. It is not intended to com-pensate for financial weaknesses in adeveloper/owner or inadequacies in thefinancial structure of a transaction (e.g.,inadequate equity investment). Nor is itintended to offset the lack of demand fora service or a product.

Loss of Benefits. The benefits of TIFcan be lost if the project is improperlystructured. For example, as a spin-offeffect, TIF is supposed to create othersources of revenue for a city. When TIFis used in tandem with other incentivesthat abate or divert other types of taxes,the community loses the additional ben-efit of revenue streams that the TIF

14 Bureau of Governmental Research

development would otherwise generate(e.g., when incremental property andsales tax revenues are both diverted).

Fragmentation of the Tax Base.Allowing too many TIF districts can leadto a fragmented tax base in which thedistricts and neighborhoods experienc-ing growth lock up the incremental taxrevenue they create.22

Complex Analysis and Oversight. TIFis a complicated financing mechanism.To work effectively and efficiently, itrequires a significant, long-term com-mitment of municipal resources and ahigh level of professional expertise forevaluation, implementation, and admin-istration.23 Such expertise runs thegamut from finance and accounting toreal estate development. In addition,successful evaluation depends on theaccuracy and rigor of the underlyingmarkets, cost-benefit, and other impactstudies.

Some of the criticisms leveled at TIF can be mitigated or avoided throughcautious, appropriate use of the TIFmechanism.

VI. SPECIAL ISSUES

WITH SALES TIFSales TIF districts can under some cir-cumstances provide far larger tax rev-enue streams than property TIF districtswould. This is true in areas with lowassessments, large amounts of exemptproperty, or limitations on the types ofproperty taxes that can be accessed forTIF. In those circumstances, sales TIFmay be more feasible than property TIF.

There are, however, concerns with salesTIF that are not present (or are less pro-nounced) in the case of property TIF.These concerns include the following:

Land Use Distortions. Because theamount of revenue generated by a salesTIF district depends on sales volume,the mechanism favors the inclusion ofhigh-volume retailer establishments,such as malls, big box stores and cardealerships, in the TIF district. The needfor large retailers to support the TIF canlead to distorted land use decisions,with the decision being driven more by aperceived need for a subsidy of a givensize than by sensible planning. Concernover distorted land use was one of thefactors that led California to repealauthorization for sales TIF.24

Subsidies for Big Retailers. The questfor large revenue sources can result inunnecessary subsidies for big retailers.This is both ineffective and inequitable,since it results in both a waste of publicdollars and provides businesses with asubsidized competitive advantage. Thiswas another factor that led California toterminate sales TIF authorization.25

Capturing Non-incremental andUnrelated Revenues. Instead of creat-ing new revenues, sales TIF districtsmerely shift business from other entitiesin the region, or even worse for the localjurisdiction, from other businesses with-in its boundaries. Losses suffered bythose businesses actually result in aloss of current tax revenues available tothe local jurisdiction.

Factors other than the TIF districtimprovements (e.g., an upturn in gener-al economic conditions or changes inpersonal spending habits) may be fueling the increase in taxes. In that

Tax Increment Financing in New Orleans 15

case, the local jurisdiction is divertingfrom the general fund revenues that arenot attributable to the TIF investment.

Less than Optimal Value. Becausesales TIF districts require a significantgenerator of sales taxes, they are morelikely to be used for retail developmentthan for other uses, such as manufac-turing and high-tech exports, that gen-erally have a greater economic impact.26

This can result in a commitment ofcommunity resources to an economicdevelopment strategy that is less thanoptimal. The risk is particularly pro-nounced in the case of local govern-ments that turn to sales TIF because ofstructural weaknesses in their propertytax base.

Unstable Revenues. A sales tax base isinherently less stable than a propertytax base. 27 Sales TIFs are more suscep-tible to revenue fluctuations caused bylocal economic declines, competitionfrom stores outside the district, andgeneral changes in shopping patterns.This makes it riskier and more expen-sive to finance debt issues based on TIF.

Loss of Benefits. Unless contractuallyconstrained, the retailer can enjoy theTIF benefits and deprive the local gov-ernment of projected benefits by depart-ing when the TIF period ends.

VII. LOUISIANA TIFSTATUTES RELATING

TO NEW ORLEANSLouisiana statutes contain a confusingarray of provisions on the use of taxincrement financing. The statutes con-sist of provisions that apply generally tolocal governments and provisions on thesame subject that apply only to certain

size local governments. The result is acrazy patchwork of provisions that canbe understood and reconciled only if oneperforms a demographic analysis of themunicipalities and parishes inLouisiana.

The TIF statutes applicable to NewOrleans are set forth in the state’sCooperative Economic DevelopmentLaw. That law addresses the use of TIFby both economic development corpora-tions and by local governmental subdivi-sions.

Under the general statutes applicable toNew Orleans, the City can establish TIFdistricts and issue revenue bondspayable from or secured by property orsales tax increments. TIF bonds basedon property taxes must be approved bythe voters; voter approval is not requiredfor bonds based on sales taxes. The dif-ferent voting requirements, along withlegal constraints on the capture of prop-erty tax revenue, skew the use of TIFtoward sales taxes.

There are also two special interest TIFstatutes directed at special areas in theCity: Algiers, through a special provisionin a TIF law that applies to local govern-ments with less than 200,000 people;and the World Trade Center property, asa special taxing district. Two other spe-cial interest TIF statutes have been pro-posed for the Lake Forest Plaza shop-ping mall in eastern New Orleans andfor the large area of New Orleans east ofthe Industrial Canal.

A. Property TIFLa. R.S. 33:9032 authorizes local gov-ernmental subdivisions to issue revenuebonds payable solely from incrementalproperty taxes collected in an economic

16 Bureau of Governmental Research

development area. The tax incrementscan be used to finance or refinance aneconomic development project or to payfor the costs of an economic develop-ment project. The costs of an economicdevelopment project are broadly definedin La. R.S. 33:9035 to embrace “all rea-sonable or necessary costs incurredincidental to or in furtherance of an eco-nomic development project …, providingthat any such costs are reasonablyrelated or attributable to an approvedeconomic development plan.”

The tax increment consists of the incremental ad valorem tax revenuescollected for any or all taxing authoritiesfrom property in an economic develop-ment area; however, it does not includetax revenues previously dedicated for aspecial purpose.

The bonds require voter approval. Thelimitation of tax revenues to undedicat-ed ones and the requirement for voterapproval are significant differences fromthe TIF statutes of most states. As isdiscussed more fully below, theserestrictions seriously restrict the useful-ness of property TIF in New Orleans.

La. R.S. 33:9032, which is only half apage long, lacks the type of detail that isnormally found in statutes authorizingbond issues. The statute does not con-tain any direction concerning the desig-nation of an economic development areaor the process for dedicating of taxincrements. The establishment of aneconomic development area is cir-cuitously addressed through other provisions in the state’s CooperativeEconomic Development Law.Specifically, La. R.S. 33:9034 gives localgovernments the powers, rights, duties,and obligations of an economic develop-ment corporation. The powers include

the power to establish an economicdevelopment area, subject to approval ofthe chief executive officer or governingauthority of a local government. La. R.S.33:9034 contains no provision specify-ing the process for dedicating incremen-tal tax revenues to a TIF district.

B. Sales TIFThe use of sales TIF by New Orleans isgoverned by La. R.S. 33:9033.3. Thestatute is much more detailed than thecorresponding property TIF statute.

La. R.S. 33:9033.3 applies to municipal-ities with a population between 190,000and 215,000 or with a population inexcess of 400,000, and to parishes witha population between 400,000 and475,000 as of the latest decennial cen-sus (the “Designated Municipalities”).Currently, the populations ofShreveport, New Orleans, JeffersonParish, and East Baton Rouge Parishfall within those ranges.

The statute authorizes the DesignatedMunicipalities to issue revenue bondsthat are either payable from revenuesgenerated by economic developmentprojects with a pledge of sales tax increments for any shortfall, or payablesolely from incremental sales tax rev-enues generated in an economic devel-opment area. The municipality is alsoauthorized to pledge the revenues fromany millage levied for economic develop-ment or any other funds available foreconomic development. Incrementalsales tax revenues are restricted tothose of the local government and donot include tax revenues dedicated for a special purpose.

Tax Increment Financing in New Orleans 17

Sales TIF bonds can be used to financeor refinance all or any part of an eco-nomic development project. “Economicdevelopment project” is broadly definedto embrace “any and all projects suit-able to any industry determined by themunicipality or, as appropriate, theissuers of revenue bonds, to create economic development.”

The total amount of principal and inter-est falling due in any calendar year can-not exceed 75% of the amount of thepledged sales tax increment that themunicipality estimates will be receivedin the first full calendar year after theeconomic development project has beencompleted. The statute does not specifyhow the remaining increment can beused.

The sales TIF statute requires a munici-pality that proposes to issue sales TIFbonds to designate the boundaries ofthe TIF district and the portion of localsales taxes to be used for the tax incre-ments. No voter approval is required forthe issuance of the bonds.

Neither property nor sales TIF bonds aresubject to any statutory debt limitationsor restrictions. There is no statutorylimit on the duration of a TIF district.

C. Issuance of TIF Bondsby Economic DevelopmentCorporationsAs noted above, bonds secured by taxincrements can be issued by economicdevelopment corporations with the consent of the affected governmentalentities. Interestingly, the law does notstate whether the consent of voters isrequired for economic development cor-porations to issue revenue bondssecured by property TIF.

D. Special Provision forAlgiersLegislation passed in 2002 provides spe-cial property and sales TIF authority forall municipalities and parishes with200,000 people or less. The new law, La.R.S. 33:9038.1-9038.9 (the “SmallJurisdiction Statute”), also applies toAlgiers. It is unclear exactly how thestatute relates to the property and salesTIF statutes that apply to New Orleansat large.

The Small Jurisdiction Statute allowsthe City, or with the City’s consent, anindustrial development board or publictrust with jurisdiction in Algiers to issuerevenue bonds payable from or securedby incremental property, sales, or hoteloccupancy tax revenues. The City estab-lishes the district from which the incre-ments are to be pledged and deducted.

Property TIF may capture all incremen-tal property taxes, if this does not resultin a violation of dedications or otherlimitations and if all affected tax recipi-ent bodies consent to the capture of the incremental property taxes. Revenuebonds secured by property taxes mustalso be approved in a special election forqualified electors within the proposedboundaries of the TIF district. If thereare no electors, as in the case of vacantor purely commercial land, no electionis required.

In contrast to TIF districts establishedin larger jurisdictions, the small govern-ment TIF districts may capture all incremental state and local sales andhotel occupancy taxes in the district, if the appropriate tax recipient bodiesconsent. State sales tax increments

18 Bureau of Governmental Research

cannot exceed the pledged local increment. No voter approval is requiredfor the issuance of the bonds.

The annual debt service for both proper-ty and sales TIF bonds is limited to apercentage of tax increments. At the endof the life of a TIF, any unspent incre-ments set aside for debt service reservesmust be deposited in a trust fund to“promote other economic developmentopportunities.” In addition, incrementalrevenues can be deposited in a specialtrust fund to loan, grant, donate, orpledge for other economic developmentprojects.

The districts can levy up to five mills ofproperty tax, up to 2% of sales taxes,and up to 2% of hotel occupancy taxes,or any combination, on property withinthe district. The statute does not man-date specific uses for these taxes. As isthe case of property taxes, a specialelection for qualified electors is required.

The Small Jurisdiction Statute is moredisturbing than the statutes generallyapplicable to New Orleans in severalrespects. First, it eliminates the require-ment for city-wide voter approval ofproperty TIF bonds: the only voterequired is for voters in the district whowould benefit from the redirection of taxincreases. Second, it allows the captureof state sales taxes. Third, it gives localgovernments the option of placing taxincrements in a trust fund for other economic development projects.

E. World Trade CenterTaxing DistrictLa. R.S. 33:9038.21, enacted in 2002,created a special taxing district for theWorld Trade Center at the foot of Canal

Street. The taxing district includes the33-story World Trade Center building, aparking garage, and adjacent land.

The legislation’s stated purpose is tofacilitate cooperative economic develop-ment among the City, the World TradeCenter of New Orleans Inc. (WTCNO),and a developer, WTC Development Ltd.,to renovate, restore, and develop theWorld Trade Center property and toimplement a lease between WTCNO and WTC Development Ltd.

The World Trade Center taxing districtis authorized to levy and collect its ownhotel occupancy tax in lieu of the hoteloccupancy tax in Orleans Parish at arate that is at least equivalent (currently13%). The taxes can be used to pay revenue bonds issued by the district orany other financing of the property,including loans or mortgages, bonds, or certificates of indebtedness.

The tax can be levied through an ordi-nance adopted by the district’s three-member board of commissioners, com-posed of the City Council president, thepresident of New Orleans BuildingCorp., and the managing director ofadministration of WTCNO. Approval bythe affected hotel tax recipients is notrequired for the capture.

The district will dissolve one year afterthe earlier of the repayment of revenuebonds issued by the district or the ter-mination of a lease between WTCNOand WTC Development Ltd.

The statute prohibits the hotel fromadvertising below-market room rates; itdoes not specify how the market rate isto be determined.

Tax Increment Financing in New Orleans 19

F. Lake Forest Plaza TIFProposalDuring the spring session, the StateLegislature will consider a bill (S.B. 808)to create a TIF district for the LakeForest Plaza Shopping Center in easternNew Orleans. The purpose of the districtis broadly stated as “renovation, restora-tion, and development within the dis-trict.” The purpose would be accom-plished through cooperative economicdevelopment among the district, theCity, and the owners of businesses andproperty within the district. The dis-trict’s governing board would consist ofthe president of City Council, and thestate senator and state representativewhose legislative districts include theproposed TIF district.

The bill would authorize the district tolevy and collect its own hotel occupancytax at a rate at least equal to the hoteloccupancy tax rate in Orleans Parish. Itis in lieu of any hotel tax other than atax on a per-head or per-person basis.The tax may be levied without theapproval of the hotel tax recipient bod-ies. The district may pledge the tax col-lections to pay revenue bonds that itissues. It may also pledge the collectionsto “any purpose” set forth in the legisla-tion. Such financing may include loans,mortgages, bonds, or certificates ofindebtedness. The bill includes a prohi-bition on advertising below-market roomrates.

The bill also grants the Lake ForestPlaza district the TIF powers grantedsmall municipalities and parishes underthe Small Jurisdiction Statute. As notedpreviously, that statute allows captureof any incremental property or sales

taxes generated by development in thedistrict, as long as the capture is legaland the tax recipient bodies consent.

The Small Jurisdiction Statute wouldalso allow the district to levy and collectup to five mills of property tax, 2% ofsales tax, and 2% of hotel occupancytax. TIF bonds backed by property taxincrements and additional tax leviesrequire approval of qualified electors inthe TIF district, if any live there.

S.B. 808 also contains a cryptic provi-sion defining a “general sales tax incre-ment” as a portion of the general salestax increment determined and collectedby the Lake Forest Plaza District in lieuof other such taxes levied by other tax-ing authorities. The import of the provi-sion is unclear, since neither the term“general sales tax increment” nor theterm “general sales tax” is used else-where in the bill. However, the provisionopens the door to a possible capture ofnon-incremental sales taxes.

G. New Orleans East TIFProposalA bill to create a special taxing districtfor all of eastern New Orleans (H.B.1737) has been pre-filed, but not for-mally introduced, for this spring’s legislative session. The bill would createthe New Orleans East Tax IncrementFinancing District, bounded by theIndustrial Canal, Lake Pontchartrain,and the Orleans Parish line.

The purpose of the district is “to providefor the orderly planning, development,acquisition, construction, and effectua-tion of the services, improvements, andfacilities to be furnished by the district.”

20 Bureau of Governmental Research

The district would be governed by aboard of commissioners consisting ofmembers appointed by state legislatorsfor eastern New Orleans, CityCouncilmembers from districts D and E,and the Mayor, and five membersappointed by the other members from alist provided by the appointing parties.

The bill authorizes the district to createeconomic development areas and toissue revenue bonds for economic devel-opment projects. The bonds would beguaranteed by or payable from sales taxincrements collected in an economicdevelopment area designated by the dis-trict. It is unclear which tax incrementsare covered, since the bill excludes dedi-cated revenues and sales taxes collectedby the state or any political subdivisionother than the district. The bill does notgive the district authority to levy anytaxes.

The sales TIF provisions appear to bebased on the language of the TIF statutefor New Orleans, R.S. 33:9033.3. Themajor difference is that the district, andnot the City, has the power to designatethe sales tax increment and issuebonds.

The bill would authorized the district touse property tax increment financing asprovided elsewhere in CooperativeEconomic Development Law. This couldsubstantially impact future city propertytax revenue, because eastern NewOrleans encompasses 65% of the city’sland.28

Eligible projects that may be undertakenin the district are the same as thoseallowed in R.S. 33:9033.3.

VIII. TIF USE IN

LOUISIANA

A. Sales TIF in OtherCitiesThe use of TIF outside New Orleans hasbeen limited to a handful of sales TIFdistricts established to subsidize con-struction of retail development or buildinfrastructure for retail. Two cities,Ruston and Monroe, established salesTIF districts capturing both state andlocal sales tax increments.

Monroe has issued several series ofbonds for roads and infrastructure fortwo retail areas, with large, nationalretailers, such as Wal-Mart, HomeDepot, Lowe’s, and Target. Most recently, it issued $9.25 million ofbonds with a maturity of 19 years andan interest rate of 5.49%.

In 2001, Ruston issued $2 million ofbonds to fund engineering studies forroad construction to service a retail areawith a Wal-Mart, auto dealerships, andother stores. Ruston expects to repaythe bonds out of incremental state salestaxes, without using local sales taxes,an option no longer available. It plans toissue additional bonds to design andbuild the roads.

Lake Charles created a TIF district in1996 for Prien Lake Mall. The city,school board, and law enforcement dis-trict agreed to reimburse the mall devel-oper for expansion costs in an amountnot to exceed $8,000,000.

Shreveport created a 92.4-acre down-town entertainment TIF district in 1999and spent $1 million of general funds onstreetscape improvements. The first $1million collected by the TIF district,

Tax Increment Financing in New Orleans 21

which captures incremental revenuesfrom the city’s 2.5% sales tax, will reim-burse the city for those improvements.

B. TIF in New OrleansOnly two TIFs in New Orleans have sig-nificant history and information avail-able for analysis: a TIF for the St.Thomas redevelopment, which wasapproved by City Council last fall, andthe proposed TIF for a hotel in theWorld Trade Center, which continues tobe negotiated by the City. BGR takes noposition with respect to the merits ofeither development.

1. St. Thomas

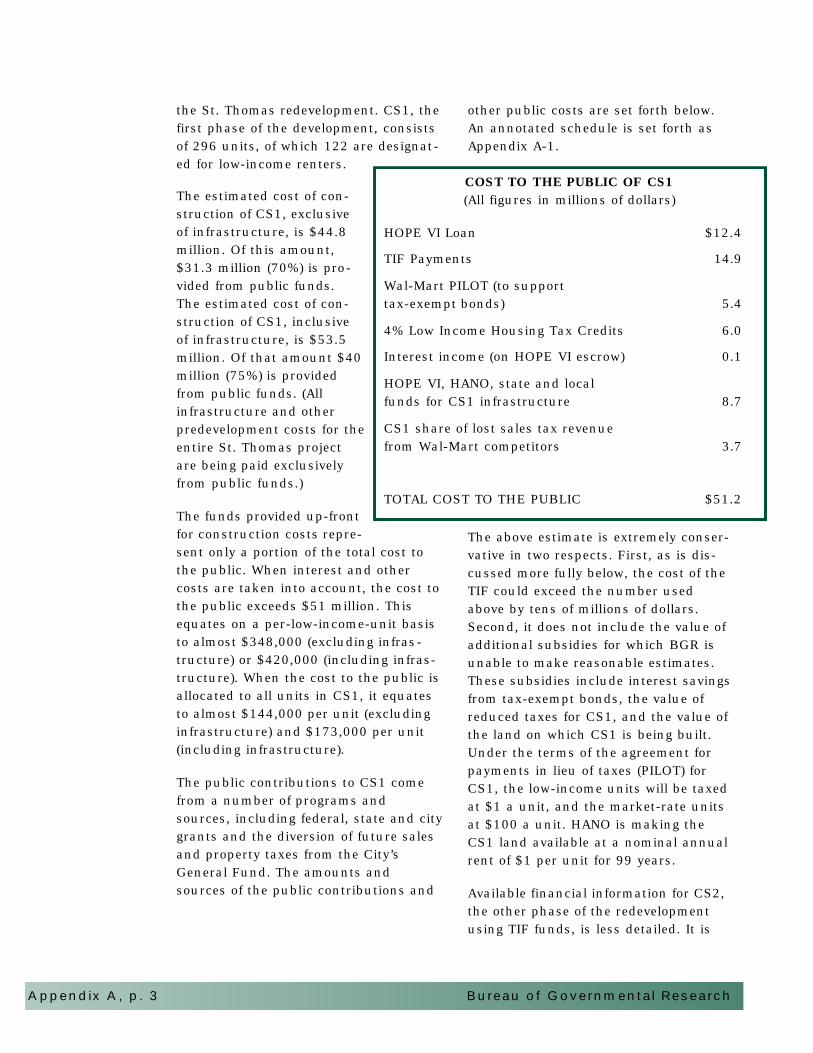

The St. Thomas TIF district includes theformer St. Thomas public housing siteand an adjacent parcel of land on whicha Wal-Mart Super Center will be con-structed. The district was formed toassist with the financing of a HOPE VIredevelopment project for St. Thomas.The district will capture future Citysales tax revenues (2.5%) from the Wal-Mart Super Center. The incrementaltaxes from Wal-Mart will not be divertedto Wal-Mart, but will be used instead torepay $20 million of debt incurred tofinance the construction of two mixed-income rental portions of the former St.Thomas site, known as CS1 and CS2.Further discussion of the St. ThomasTIF is presented in Appendix A to thisreport.

The St. Thomas TIF raises the followingconcerns:

Private Subsidy. The St. Thomas TIF ispart of a package of substantial subsi-dies to a private developer. For the con-struction of CS1, one of the mixed-income rental portions of the project,

the cost to the public (including interestand other costs) will equate on a per-low-income-unit basis to almost$348,000 (excluding infrastructure) and$420,000 (including infrastructure).

Low-Priority Use of Funds. The revenues from the TIF district are beingused to finance market-rate housing – atroubling application of public funds ina city that suffers from a lack of decentlow-income housing.

Expensive Financing. The cost of theTIF bonds is extraordinarily high. TheCity has authorized the issuance ofbonds with an anticipated interest rateof 8 to 8.5%. Although for technical rea-sons the stated maturity is 45 years, theCity anticipates retiring the bonds in amaximum 13.5 years. The interest rateexceeds the rate for bonds issued bylocal governments with ratings compa-rable to New Orleans (currently around4.5%) by a significant margin. The inter-est differential between $20 million inbonds, payable over 13.5 years andbearing interest at 8.5% and bondsbearing interest at 4.5% would be $7.1million (or $5.8 million discounted at3% for inflation).

If the bonds remain outstanding for thestated maturity, which the City does notanticipate, the interest payments alonecould total $67 million. Under thatworst-case scenario, the citizens of NewOrleans would divert $87 million fromthe general fund to pay for $20 millionin debt.

Reduced Sales Tax Revenue. The St.Thomas TIF district will result in a lossof sales tax revenues currently flowingto the City’s General Fund. As a resultof the loss of tax revenues from otherbusinesses, the City estimates a sales

22 Bureau of Governmental Research

tax loss in the range of $402,000 to$554,000 a year for the life of thebonds. This loss in sales tax revenue isin addition to the total annual debt ser-vice paid by the TIF district over 13.5years, which could average approxi-mately $2.5 million per year. The addi-tion of $2.5 million to the City’s GeneralFund could translate into hiring 75 newpolice officers.

Multiple Subsidies. In addition to thesales TIF, the City is foregoing most ofthe future property taxes from themixed-income rental housing, and isredirecting to CS1 the property taxesfrom Wal-Mart for 20 years. In general,jurisdictions using TIF anticipateincreases in other tax streams to help justify a TIF district.

Historic Restoration Incorporated (HRI),the developer of the project, claims thatthe TIF is justified by significant netbenefits, which according to a cost-ben-efit analysis prepared by MetroSourceLLC for the Industrial DevelopmentBoard of New Orleans, would equalapproximately $110 million for the Cityover a period of 50 years. HRI projectsincreased sales tax revenues of $125million (on a net present value basis,using a 2% inflation factor) for the City,Orleans Parish School Board, and theRegional Transit Authority over 25years.

2. World Trade Center

In 2002, the State Legislature created aspecial taxing district for a proposedhotel development in the first 18 floorsof the World Trade Center building atthe foot of Canal Street. The taxing dis-trict differs from a traditional TIF dis-trict in that it will levy and collect a site-specific hotel occupancy tax in lieu of

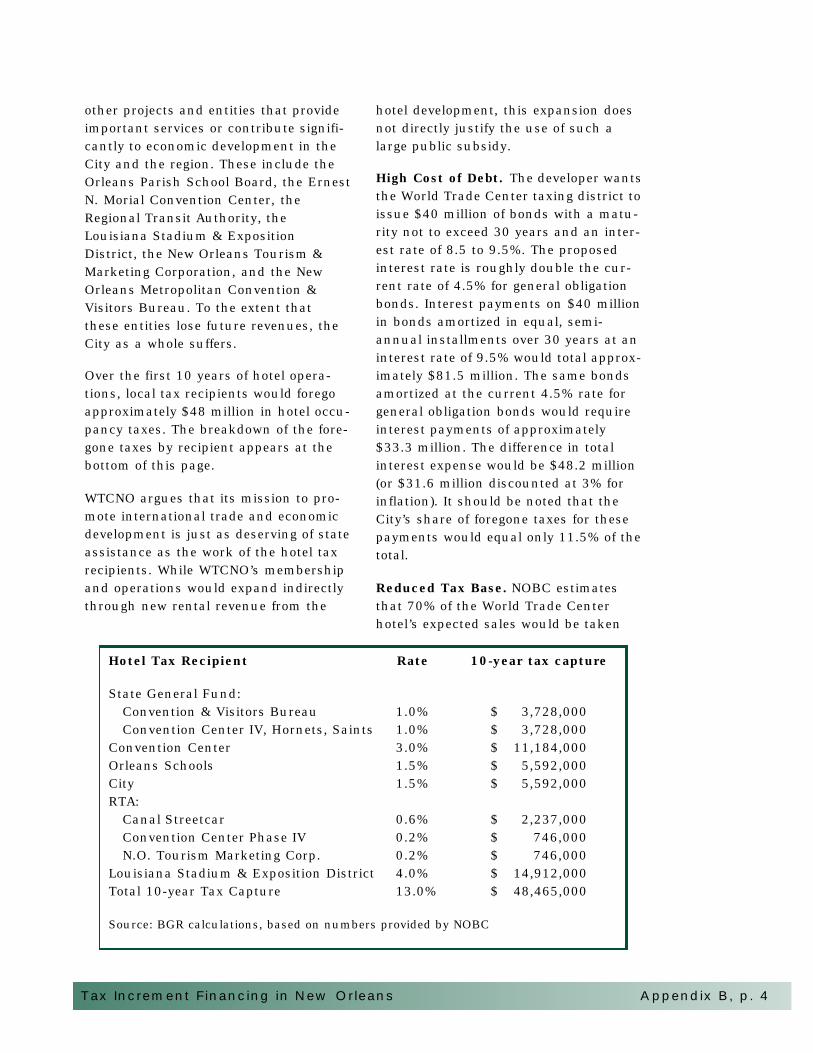

the hotel occupancy tax levied inOrleans Parish. The rate will be equal tothat of the replaced tax, currently 13%.Based on the hotel developer’s revenueprojections, the district has the potentialto capture approximately $48 million oftaxes in the first decade of the hotel’soperation.

The tax can be used to pay revenuebonds issued by the district or anyother financing of the property.According to current reports, the districtplans to issue $40 million in revenuebonds, with a maturity not to exceed 30years and an expected interest rate of8.5 to 9.5%. In addition, TIF bondhold-ers would receive an additional distribu-tion equal to 50% of net income fromthe hotel. Further discussion of theWorld Trade Center hotel project andTIF is presented in Appendix B of thisreport.

The World Trade Center TIF suffers fromthe following problems:

Inadequate Private Equity. The publicis being asked to compensate for inade-quate equity investment in a project.The City claims the developer’s equitycontribution is $1.5 million; the devel-oper claims $5.2 million. Neitheramount is adequate for a $140 millionhotel project. Currently, lenders are will-ing to loan 50% to 60% of a hotel pro-ject’s cost, expecting developers to piecetogether the remainder in equity andsubordinated debt. There is a fundinggap for which the developers are seekingpublic funding. In essence, the City andother tax recipient bodies are putting upthe equity, while the return on theirinvestment is going to the TIF bondhold-ers and the developer.

Tax Increment Financing in New Orleans 23

Inadequate Return on Investment.Under the lease executed before the TIFwas introduced, the City would receive50% of net revenues from the WorldTrade Center property. The World TradeCenter of New Orleans Inc. (WTCNO),the nonprofit organization that leasesthe property from the City and will sub-lease a portion to the developer to buildthe hotel, currently expects the City’s50% share to equal $861,000 to $1.9million per year for the first decade ofhotel operation.

The addition of the TIF dramaticallyreduces the value of the World TradeCenter lease to the City and the commu-nity. The hotel tax capture is projectedto cost the City between $462,000 and$635,000 per year for the first decade ofhotel operation, leaving the City with anet amount of $399,000 to $1.3 millionper year. Collectively, the City and otherhotel tax recipients would forego an esti-mated average of $4.8 million per yearin hotel occupancy taxes.

Negative Impact on Critical Servicesand Economic Engines. The districtwould divert revenues from other pro-jects and entities that provide importantservices or contribute significantly toeconomic development in the City andthe region. These include the OrleansParish School Board, the Ernest N.Morial Convention Center, the RegionalTransit Authority, the LouisianaStadium & Exposition District, the NewOrleans Tourism Marketing Corp., andthe New Orleans MetropolitanConvention & Visitors Bureau. To theextent that these entities lose futurerevenues, the City as a whole suffers.

High Cost of Debt. The cost of the TIFbonds is extraordinarily high. The antic-ipated rate of 8.5 to 9.5% exceeds the

rate that the City could expect to pay forgeneral obligation bonds (currentlyaround 4.5%) by a significant margin.The difference in total interest expense,based on similar amortizations over thestated maturity of the bonds, could be$48.2 million (or $31.6 million discount-ed at 3% for inflation). It should benoted that the City’s share of foregonetaxes for these payments would equalonly 11.5% of the total.

Reduced Tax Base. As a result of theloss of hotel-motel taxes from otherhotels, the City and other hotel taxrecipients would lose revenues that cur-rently flow to them. The City has esti-mated the tax loss at $2.8 million in thefirst year, but the developer disputesthis amount, arguing that other marketfactors will reduce lost tax revenues to anegligible amount.

Unfair Competitive Advantage.Opponents maintain that the districtwould provide the hotel developer withan unfair competitive advantage, allow-ing it to reduce room rates by transfer-ring a significant cost to the public.Proponents respond that their roomrates will track those of other large,competing hotels downtown and thatthe TIF investment is necessary to makethe city-owned World Trade Centerusable in any form of commerce.Although the TIF legislation prohibitsthe hotel from advertising below market-rate rooms, preventing the hotel fromoffering reduced room rates would bedifficult, if not impossible.

24 Bureau of Governmental Research

IX. FUTURE TIF USE

IN NEW ORLEANSAs noted at the outset of the report, TIF is one of a number of economicdevelopment tools available to local governments. It provides cash-strappedmunicipalities – of which New Orleanssurely is one – with a means of makinginvestment in infrastructure and eco-nomic development projects undersevere financial and political con-straints. TIF has tremendous politicalappeal in that it can be implementedwithout raising taxes and, in manycases, without obtaining voter approval.It has a certain conceptual beauty inthat the investment is, in theory, self-financing and the development support-ing it would not have occurred other-wise.

Under closer scrutiny, the underlyingpremise that a TIF is self-financing isopen to question. Because of the diffi-culty of making long-range projections,it is difficult to assess whether develop-ment in an area would have occurredwithout TIF. It is even more difficult todetermine whether, and to what extent,gains in a TIF district are offset by stag-nation, decline, or reduced growth inother areas and businesses. To theextent that other areas and businessesare negatively impacted, the existingrevenue base of the local government is reduced. In addition, successful TIFdistricts can increase a local govern-ment’s operating costs without providingadditional operating funds to the localgovernment. The end result in that caseis a transfer of the additional operatingcosts to residents outside the TIF district.

Given the many unknowns surroundingthe performance of TIF districts, and theidentifiable types of dislocations thatcan occur, it is exceedingly dangerous toview TIF as free money. Rather, TIFshould be considered an allocation offuture resources and assessed with astringency befitting other long-terminvestments of future revenue. Theinvestment should be made only if it iseffective, efficient, equitable, and in fur-therance of a defined public policy.

For reasons discussed in Section VI,property TIF, the most widely used formof TIF, is preferable to sales TIF.Unfortunately, because of the nature ofthe local tax structure, property TIF isless practical in New Orleans than inother jurisdictions. In Louisiana, proper-ty TIF can only capture taxing bodies’ad valorem millage that is not previouslydedicated to a special purpose. In 2001,this millage for the City of New Orleanswas 14.91 mills out of 169.29 total millscollected in New Orleans. Thus, forevery $1 million of incremental assessedvalue (or $6.6 million of fair marketvalue), only $14,910 out of $169,290 in total property taxes paid would beavailable for a TIF district. It is unclearwhether the general millage of theOrleans Parish School Board andOrleans Levee Board would be col-lectible for the TIF. If they were, it wouldincrease the capture by $15,500 per $1million of incremental assessed value.The homestead exemption and theexemptions enjoyed by nonprofits, gov-ernment, and industry further diminishthe potential of property TIF use byreducing the tax base.

The tax structure, combined withrequirements for voter approval of bondsbacked by property tax increments (butnot for bonds backed by sales tax incre-

Tax Increment Financing in New Orleans 25

ments), skews the use of TIF towardsales TIF. The latter suffers from moreserious problems than does the propertyTIF:

t Sales tax revenues are more volatilethan property tax revenues, a factthat makes sales TIF debt financ-ing riskier and more expensive.

t Sales TIF districts are more likelythan property TIF districts to cap-ture revenues unrelated to the TIFinvestment, thus reducing currenttax revenues available to the juris-diction.

t Because sales TIF districts needlarge, creditworthy retailers orshopping centers to generate significant tax increments, thequest for a TIF source can lead toland use distortions and unneces-sary subsidies for big retailers.

t Subsidizing a retail operation withTIF revenues gives it an unfairadvantage over its competitors.

t Unless contractually constrained,the retailer can enjoy the TIF sub-sidy and deprive the local govern-ment of projected benefits bydeparting when the TIF periodends.

Furthermore, a reliance on sales TIFmay distort the City’s investment priori-ties by directing public dollars intoinvestments that do not offer the great-est return. Retail development mayreceive tax dollars that could have beendirected to alternative developmentswith a greater potential for impact onthe economy, such as businesses thatexport goods to out-of-town customers.It would be unfortunate if funds were

directed to less promising developmentsbecause they produce large streams ofsales taxes and do not require voterapproval.

There are other factors that suggest thata TIF might not provide the most effec-tive solution to blight or economic devel-opment issues. Regardless of the type ofTIF, because of the limited nature of theobligation, TIF debt is more expensivethan general obligation bonds. Whetherthe premium paid to limit the obligationis worthwhile will depend on the partic-ular circumstances. In some cases, suchas the St. Thomas redevelopment, it isclear that the City could save millions ofdollars in tax revenue by issuing lower-interest general obligation bondsand targeting key areas for infrastruc-ture investment. The capacity to issuesuch debt exists under the City’s debtlimit, which is 35% of gross assessedvalue, or $816.8 million as of Dec. 31,2002. Debt outstanding as of lateFebruary was $473.4 million, or 58% ofcapacity.

As in the use of other economic develop-ment incentives, the effective, efficient,and equitable use of TIF depends on thewisdom, sophistication, and integrity ofthose involved in the process. To theextent that decisions are based onsophisticated analysis, made with anunwavering focus on the public good,and implemented through skillful nego-tiation, the chances of successfullyusing TIF increase. To the extent thatdecisions are driven by relationships,political deals, and other agendas, orthat the government lacks the high levelof expertise needed to analyze andimplement complicated transactions,TIF is likely to be an expensive mistakethat results in an unnecessary transferof wealth to private entities.

26 Bureau of Governmental Research

The potential problems associated withTIF are more than theoretical. The St.Thomas TIF and the TIF under consider-ation for the World Trade Center providecase studies of the problems associatedwith TIF.

The trend with respect to TIF is disturb-ing. In just the past month, City Councilhas received a proposal for a TIF-likefinancing for a Lowe’s, a bill has beenintroduced to create a TIF district forLake Forest Plaza shopping mall, andanother bill has been filed to create onefor eastern New Orleans. Collectivelyand individually, they raise serious concerns, including the specter of businesses routinely turning to the Cityfor subsidies and the prospect of freez-ing the tax base for a huge swath of theCity.

As noted above, the effective use ofproperty TIF in New Orleans is preclud-ed as a practical matter by the priordedication of most of the tax revenues.Ironically, the widespread use of salesTIF would create a similar limitation ongovernment’s future flexibility by con-verting unrestricted tax revenues intodedicated taxes. In addition, the prolif-eration of long-term dedications willcontribute to the balkanization of gov-ernment within the City, even as thecommunity focuses increasingly onregionalism.

Given the potential expenses, risks, andabuses associated with TIF, the Cityshould use TIF cautiously and only intightly circumscribed conditions. BGRbelieves that the City should abandoncompletely the use of TIF and TIF-likearrangements based on sales and hoteloccupancy taxes and restrict the use of

TIF based on property taxes to publicinfrastructure and pre-developmentimprovements in blighted areas.