Embed Size (px)

Citation preview

TAX FOUNDATION, INC .50 RodceM*r Mama, Now York 20, Now York

TAX FOUNDATION, INC .

BOARD OF TRUSTEESORVAL W. ADAMS *ROSWELL MAGM LChow—1ZiaesRwNat o*dBank Crwwk SwineB MooreEll woRTH C ALVORD WALTER T. MARGETTS, JR.Ahm do Ahord D wwr, Kayser-Rath Corporation

GEowE D. BAILEY •HERBERT J. MILLER

-Towcke, Rasa, Ba7ey B Smut Federal A#"s Cowgrelor, Tar Fow datw two. IAC.

CARLA. Brnsm RAYMObD MOLEY

Chasrm

Extra &e Comitue;YalleyNation al Bank New"reek

ALFRED G. BUEHLElt ALFRED PARKrAtProfessor ofP"lkFiance. Eucndre$&Tetary, TicForAdatiorr. IAG

Unirasiay of pouwybwja WI.LARD F. ROCKWELL, JR.

HARRYR BYRD, TR . Preddent.RockwellMmutfactkift Compares

E~torandPr eaidoet. WinchesterEreaasSar

_ DR. WALTER E. SPAHR

NoRTOx CLArrNoRToN

Fzer. Vice President.Swel onswNationalCommittee on Monetary Polic_r -

PreaCE& 1Yeyahaeaaer Coaspny N[AujacEPE.CRAxE President. ~pBancorporation

Sandord 09 Company (Ne- lax))

- JAMES M. SYMESJUSTM W. DART Char mr. PennsyhawisRailroadCompanyPresidea . R=6Dray&Chemical Company GARDINER SYMO?~-DsJOHN DEL AITTRE Chairmen, Tennessee catTrassmsitsion Co-Presdenr. Farman do Mechanic REESE H. TAYLORSayings Bank ofMh waspodt CA"Man. Union Oil Company of CaliforniaRoBERT Dt GKwm DONALDF. VALLEYVim Preaident. DiGiorgaFndt Carpora(ioa: Chairman, National Bank of Detroit

*WALLISE.DUNCKEL W. ALLEN WALLIS

_r= President, aankrn Trust Campany Domr. Grodr ate School of Business,

LamFLEmm, JR . Uwrersity of ChicagoAndason.ChWmB Company CLOUD WAMFLSR

*ROBERTW. FRENCH Chairman, Carrier Corporation

President, Tax Foaalarioa, lAc. BEN H. WOOTEN

*RICHARD C. GERSTFNBERG _ Chairman.First National Bank inDaunt

VittPre"" (Flame).

- THEODORE O. YNTEMAGeneral Motors Corporation

- ChairmanofFinance Comm. do V- P

*GORDON GRANDFord Motor Company

Vice President. Law ad Administration, TRUSTEES ADVISORY COUNCI LOlin Mathieson Chemical Corporation, S. SLOANCOLT

- EDMUND L. GRIMES Di: error, Bankers Trust Company—

Chairnwn, Commercial Credit Company FREDERIC G. DaNNE RPRENTIS C. HALE Chairman, General Motors CorporationChairman. Broadway Hale Stores, I z F. PEAVEY HEFFELFINGE R

;JoHw W. HANES Chairman, F. K. Peavey R CompanyDirector. Olin Mathiesoa Chemical Corporation H. J . HEINZ I IGILBERT W. HUMPHREY Chairman. H. J. Heinz CompanyChairman, The M. A . Hanna Company CHARLES R. HOOKROY C. INGERSOLL Honorary Chairman, Armco Steel CorporationHonorary Chairman. Borg-Warner Corporation T. S . PETERSENFREDERICK R. KAPPEL Standard Oil Company of California

_Chairman, American Telephone and Tekgraph Co. A. W. ROBERTSONDONALD P . KIRCHER Westinghouse Electric Corporation

President, Singer Manufacturing Company

- DR. GUY I- SNAVELY

•Executive Committee

OFFICER S_

ROSWELL MAGILL

GORDON GRANDChairman

Vice Chairman

ROBERT fir'.FRENCH

JOHN W. HANESPresidw

Chairman, Executive Committee

WALLIS B . DUNCKELTreasurer

ALFRED PARKE RExecutive Secretary

~, y~ i~~

_,

-

~ ,

~; I ~ ~.

•

, .

,',

',

_

,~,

'`

r'Yi

,~

•,,,

I

_

1-, i

~

~.,

15 i:i

1...

..

~~

~

1.1

i I~ l

I I I

i

i l

-1 .

I~i~

. . I

_I

. . ~' .

~ ~ ' ~ ~

..

".

'

li

~) f

~` ./

i.

,l i I

~ ~ i. ~ ',

~

~ I

~~ y

L' ~

,', ~

1 l

f

,_

_ .

.,~

11

~ .~ .

i~i . JI'

'

FOREWOR D

The startling growth of state government expenditures from S7 .1 billion in 1946to $31 .6 billion in 1960 indicates the heavy pressures to which state tax structure shave been subject in the post-World War II years . It may be that the d:gree of pres-sure will be somewhat less in the future. Nevertheless, most states still face Iarge. needs and demands for increased expenditures . They must decide to what extent

increased state government seniors can be provided, and if so how these increases

-are to be financed . Among the alternatives acre greater utilization of existing taxesor adoption of new taxes.

_

The purpose of this study is :0 examine the present and prospective role of the

=retail sales tax and Ike individual income tax in state tax structures . The study

anal,-m the characteristics of these taxes, the extent of their utilization, factors affect-

_-

ittg their further utilizat o a, and thek advantages and disadvantages as compared witheach otiier and with other forms of taxation. The study does not examine in detailthe question of the Icvel and extent of services provided by state governments, bu tdecisions on the expansion of existing programs and adoption of new programs wil lobviously affect the seriousness of the tax problem.

This study was carried out under the direction of Professor C. Lowell Harriss of

_Columbia University with the participation of the Research Staff of the Tax Founda-tion under the supervision of George A. Bishop and Phoebe C. Main .

The study was made possible by a grant from Johnson & Johnson, New Bruns-

-wick, N. J . However, Johanson & Johnson had no part in the analysis or the formula-tion of conclusions presented in this report, and is not to be understood, by virtu eof its grant, as approving any statement or view expressed or implied herein .

An earlier version of this study was reviewed by a number of experienced ta xadministrators, professors of public finance, and corporate tax executives . Thei rsuggestions have Imen of great value even when, for one reason or another, theyhave not been incorporated in the present version .

Tax Foundation, Inc., a non-profit organization, is engaged in research and citi-zen education on government spending and taxation . Its purpose is to aid in the de-velopment of more efficient government at least cost to the taxpayer . It also serves as anational information agency for organized taxpayer research groups throughout th ecountry.

TAX FOUNDATION, INC .

January, 1962

TABLE OF 'CONTENTS

PAGE :

r

-

FOREWORD 5-

L .

INTRODUCTION -. '

U .

LONG-TERM CHANGES IN STATE TAX STRUCTURES 10

-

IIL

CRITERIA FOR JUDGING A REVENUE SYSTEM 18

A. Revenue .9

-

-

B. Distribution of Tax Burdens 18

_

G Economic Efficiency 20

=D. , Administration and Ce M_ ga = 21

IV. -, THE RETAIL SALES TAX 22

A. Nature of the Tax 22

B. What is Subject to Tai 24

=

C. Distribution of Saks Tax Burden 26

-

== D. Extent of Increased Reliance on Retail Saks Taxes 31

E. "Fairness" of the Tax -3

F. Effects on Business and Economic Growth 35

=

G. Administration and Compliance — 37

V.

THE INDIVIDUAL INCOME TAX 40

_

A. Nature of the Tax 40

B. Extent of Increased Reliance on Individual Income Taxes 48

-

C. "Fairness" of theTax 49

D. Effect on Business and Economic Growth -

5 1

E. Administration and Compliance _ 5 1

VI.

CHOICE AMONG ALTERNATIVES IN THE REVISION OF STAT ETAX STRUCTURES - 54

_

A. Factots Influencing State 'faz Structures 54

B. ._uprnditure Cuatrul

Y

S5, C, . Possibi'lit as of Gfeate: Reliance on RPwcnne' Sources 4)1her -l-han

.--

'Individual Income or Retail Sales Taxes SG

D. Retail Sales TaAcAoa .w... .w_ 58

Individual Income Tmtion 59

-J

F. B:1aaein the Auments,

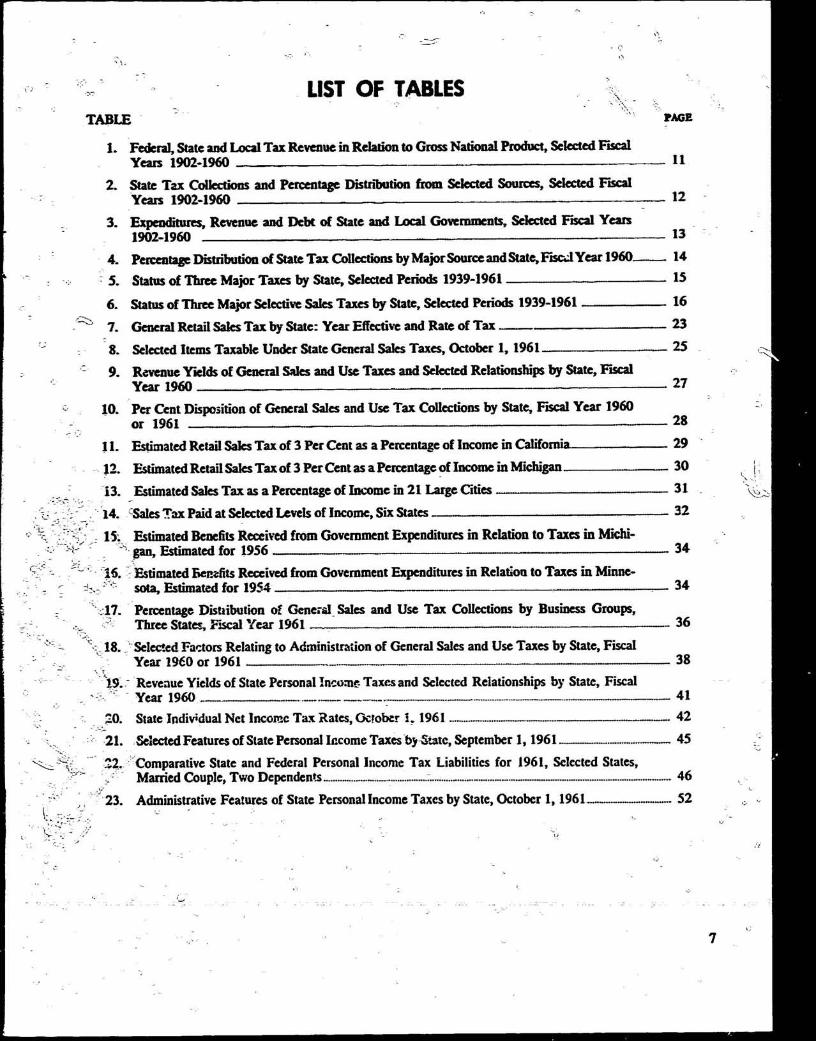

LIST OF TABLESTABLE PAGE

1 . Federal, State and Local Tax Revenue in Relation to Gross National Product, Selected FiscalYears 1902-1960 11

2. State Tax Collections and Percentage Distribution from Selected Sources, Selected Fiscal= Years 1902-1960 12

3. Expenditures, Revenue and Debt of State and Local Governments, Selected Fiscal Years1902-1960 13

"

4. Percentage Distribution of State Tax Collections by Major Source and State, FncJ Year 1960 14

-

- 5 . Status of Three Major Taxes by State, Selected Periods 1939-1961 15

6 . Status of Three Major Selective Saks Taxes by State, Selected Periods 1939-1961 16

7. General Retail Saks Tax by State : Year Effective and Rate of Tax 23

8 . Selected Items Taxable Under State General Saks Taxes, October 1, 1961 25

=

9. Revenue Yields of General Sales and Use Taxes and Selected Relationships by State, FiscalYear 1960 27

10. Per Cent Disposition of General Sales and Use Tax Collections by State, Fiscal Year 1960 =- or 1961 28

11. Estimated Retail Saks Tax of 3 Per Cent as a Percentage of Income in California 29

12 . Estimated Retail Saks Tax of 3 Per Cent as a Percentage of Income in Michigan 30

_

43 . Estimated Sales Tax as a Percentage of Income in 21 Large Cities 3 1

-

14. 'Sales Tax Paid at Selected Levels of Income, Six States 32

15 Estimated Benefits Received from Government Expenditures in Relation to Taxes in Michi -gan, Estimated for 1956 34

15. Estimated Renzfits Received from Government Expenditures in Relation to Taxes in Mine -- sota, Estimated for 196.4 34

._ 17. Percentage Distribution of Gene . al - Sales and Use Tax Collections by Business Groups ,-

-

- Three States, Fiscal Year 1961 36

-

= : 18. Selected Factors Relating to Administration of General Sales and Use Taxes by State, Fisca lYear 1960 or 1961 38

=13 . Revenue Yields of State Personal Income- Taxes and Selected Relationships by State, FiscalYear 1960 41

=

20. State Individual Net Income Tax Rates, October

1961 -42

=

-21 . . Selected Features of State Personal Income Taxes -by State, September 1, 1961 45

2. .~ Comparative State and Federal Personal Income Tax Liabilities for 1961, Selected States ,Married Couple, Two Dependents

23 . Administrative Features of State Personal Income Taxes by State, October 1,1961 52

7

R,

f Retail sales and individual InC0me 4-XXesIn -State Tax Struchrres

-1

7

C;

I. INTRODUCTION

Rising expenditures have put increasingly heavy pres-

New revenue sources, big ones, Have<been required— ' . "

surer on state treasuries. American taxpayers have ob-

and found.viously responded. Per capita state taxes, after allowin gfor

What criteria or principles ought to guide the develop-

changes in the purchasing power of the dollar, are

ment of a state revenue structure? Chu ter III examines

=now about one and two-thirds those at the end of WorldWar II

four groups of considerations—revenue; fairness and :- :. Yet no end of strain on state finances is in sight .

other factors bearing upon the distribution of tax bur-

Some states may find that existing revenue systems can

dens ; the effects of the state's tax system on the efficiency =u'

meet their "needs' as economic growth expands tax

with which the economy operates ; and the problemra* ,of

_bases. In other states, however, citizens must match the

administration and taxpayer compliance .

-

benefits of greater spending against the disadvantages of

The discussion of the two taxes—the sales tax and the

adding new revenue sources, of increasing the weight of

tax on individual income—describe the general structure

existing taxes, or of both. Every state also has the oppor-

of each, and the major features and problems, including

tunity of improving its established revenue system . The

those of administration and compliance. Because of the

higher the total tax bill, the greater the reason for re-

importance attached to questions of "fairness," and als o

examining both the broad outlines of the existing struc-

to the effects of the tax on economic growth, each topi cture and the details of particular taxes .

receives explicit attention .

The choice; are difficult . Nothing will make them

In making choices about expenditures and taxes, the

easy . Facts and analysis, however, will help in making

public must do so within limits set by existing realities.

them wise . This study provides facts and analysis about

Each state's position is somewhat unique, but importan t

two of the most important existing or potential sources

considerations which have general applicability are dis -

of state revenue—the tax on retail sales and the tax on

cussed in Chapter VI .individual income .

The concluding chapter summarizes the main con -A summary of trends in state finances since 1902 siderations affecting choice between a tax on retail sale s

(Chapter II) shows how state governments have ex- '--and one on individual income . The section balancing thepanded their own spending activities and have under- Y arguments attempts to help the reader make an informe d

taken heavy responsibilities for financmg local services.

judgment.

9

Il. IONG-TERM GRANGES IN TAX;-:STATE STRUCTURES

states adopted the tax in 1933 and ten did so in 1935.

-Many were "temporary," but during the decade only tenstates repealed the sales tax or let it expire.

Twenty states adopted taxes on personal income i nthe period from 1929 to 1937 . The crest was reached in1933, with six enactments. Only two states allowed their 'personal income taxes to lapse .

_

Levies measured by corporation income were newlyimposed by 20 states between 1929 and 1937, with thepeak of adoptions also occurring in 1933 . `

_- = From IM to 1930

State noes grew more than ninefold in dollars, and by-almost two and a half times as much as gross national

Prod criGNP ), in the fast three decades of this century.r;State ttates were only one-seventh of the total of Fc&-ral-

state-local taxes in 1902; by 1932 they vmw almost one--- fourth . The expansion in the absolute and the relativ e`4

. importance of state taxes was tl lutilt of- expansion in`-'state spending, which grew even afore than state taxa-tion . Two types of spending accounted for most of th eincrease--highways and aucatioa. States themse1w`undertook more and more responsibility for building andmaintaining major highways . Far education, however,

": , . . -states, though increasing-their outlays for state-operate dcolleges and universities, made most of their effortsin theform of grants to localities .

Tax changes in this period fall into three broad groups .(1) The relative importance of the property tax as asource of state 'tcvenue declined. (2) Motor vehiclelicense and motor fuel revenues grew tremend9usly, es -

;_:,pecially after World War I. However, spending on facili-ties for motorists increased more rapidly. (3) Taxes oncorporation and personal income were adopted by abou tone out of four states after Wisconsin's successful entryinto the field of income taxation, beginning in 1911 .Income tax revenue, however, was only a small fractionof that from the taxes on motor fuel and licenses .

-

Among the many less important changes in revenuesystems was the general adoption of state inheritance orestate taxes . A Federal credit in effect put compellin gpressure on states to Bract such levies.

The 1930's

The depression of the 1930's was unusually deep andexceptionally long. Its effects on state (and local) fi-nances were profound . Revenues dropped sharply. Theability to borrow also fell markedly and in some rase sdisappeared. States and localities ieduced not only capi-tal outla but al re lar serv's the cut ~rsonnelys

so gu

;,e

`

At the end of the decade, then, the states, with just aand pay rates . Yet, especially in view of rising demands

few exceptions had given up significant use of one broad-for welfare assistance, expenditures could =not be cut_ asmuch as revenues fell.

base tax, that on property . All but six were placing heavyreliance upon other br?ad-bast, taxes—levies on retail

Receipts from taxes on individual and business income

sales and the income of indivic aals=oF on corporatio nand from inheritance taxes fell sharply. By contnist,

inceme taxes .yields from motor fuel and vehicle taxes and the few

"taxes on business gross receipts held up fairly well . Col-

Expenditure pressures vtere by no means satisfied by

lecdons from the property tax dropped, adding some

"these revenues changes . , Stater took advantage of th erepeal of prohibition -and began to tax rlcoholic bever-

what to the financial difficulties of the states but creating

awes or to engage in liquor retailing at substantial_profit,truly serious trouble for cities, towns, counties ; and

Taxes on tobacco p*od~y;~ also a~speared.school districts, all of which were almost entirely depend-

,

ent upon this revenue source . Property tax delinquency

In 1940, none of tie tuxes yet menroned %as th erose to an average of 20 percent in 1933 ; it ranged from 0 largest source of stoic tax. revenue . That place was oc-

:

10:,

6 per cent in Massachusetts to 40 per cent in Michigan .Localities turned to states for financial help. Owners ofproperty Uso sought relief from state legislatures . _

Although state responses varied widely in detail, threegeneral changes appeared, and appeared very quickly ,throughout most of the country . (1) States undertook topay for a bigger portion cl the total of state-local spend-ing. (2) They reduced their own use of the property tax .(3) They used other taxes more heavily, and, mos tstrikingly, added new ones.

By 1937 all but 13 states had adopted (a) one or bothof two taxes with broad bases and good revenue poten-Val, or (b) a tax on corporation income. The exceptionsincluded states which had not drasticaLy limited th emaximum rates to be imposed on property and states inwhich the. use of gasoline tax. revenues for general putposes was not prevented by earmarking-

The most striking change was the introouction ofretail sales taxes. Powerful pressure to maintain spend-ing, especially on schools, overcame opposition to t,&unfamiliar and widely criticized type of taxation .

Although West Virginia had lea the way in 1921 an dGeorgia had followed in 1929, it was the depressio nwhich inspired the first widespread use of retail salestaxes. By the close of the 1937 legislative sessions, atotal of 31 states enacted sales taxes (Table D. A dozen

,

777-

copied by the payroll tax adopted under Federal pressure The reenactment of the Louisiana retail sales and us efor financing unemp1oymer4 :ivcur1nce bette6ts.

" -i , , '̀tax in 1942 (after a two year lapse), was the only broad -'

l

r tax adopted by the state-s in the decade from 1937_basedGrants from the Feder-.d govctnntenivaried from year through 1946. State revenues rose more than expendi -

to year, but by 1940 were at itkv~!

rep times u; igh lures during the period, and most states accumulatedin 1932.

- surpluses. Rates of eleven broad-base taxes were re-

Meanwhile, in a number of Mates.thc-s6eral property duped by the states during the period (Table 5) .

tax was reorganized. Some -stain _-prd+r..1k,'. f0 the ex-Frain 1946 to 1961

-emption of all intangible, -And in 2 ' W"cascs tangible,personal property- Other slates_M. iW coward the classi- When the war ended, pent-up demands for spendin gfied property tax by assesoW-a: -coring tangible- were released. Needs for capital outlays had accumu-

=

property at lower rat.: thin seal property. To `com- lated. Inflation had raised costs. Population had grown.pensate the localisms -io the rawang loss of revenue, Reserves had accumulated. The country was more thanthe states offered 'A .,i)'0M shw--i of the proceeds ,of ever urban--4nd suburban-and such areas demand

_certain of the newLlr :mpocd t•~res. more governmental services than rural areas . Auto usage

began a rise which was to lead to vast increases in stree tMlorld Mlsr 11 and highway spending- Conditions in the capital market

r .

Dorian the period frr►ai 1940 to 1946, state expondi-were favorable to borrowing. The tremendous growth in

` .

s-' tures incte sed slowly- 'CapivA outlays actually dropped,school-age population forced large expansion in spent! -

edunn on education.

ing

in part because a `'stAnfages of labor and materials . >Spend-mg on otbt stets functions increased as the price Total state expenditures doubled between 1946 att dlevel rose, but-army a 7,itile. 1950 and doubled again in the 1950's (Table 3) . setae

_c~

,

Table 1

~.

G

FEDERAL, STATE AND LOCAL TAX REVENUE IN RELATIONTO GROSS NATIONAL PRODUCT

Selected Fiscal Yours 1902 - 1960

-

-

-

- Toz Revenue

-

Gross _ Aso Pcsntayeo fNational

-

Amountb (Billions) Gross Notional F-so_duct

--

Fiscal

Producto_

or

(Billions)

- -Total

Federal

state Local

Total

Federal

State

loco!

-

1902

(e)

$

1 .4

$0.5

$0.2 $ 0. T11922

$ 70 .3

7.4

3.4

_

0.9 3.1

10.5

4 .8

==- 1 .3

4.1932

_

76 .3

8 .0

1 .8

1 .9 10.5

2.4

2•5

5 .6

-1940

91 .1

14 .2

5.6

4 .2 4 .5

15.6

6 .1

4.6

`4.91946

213 .6

49 .0

37.9

6.0 5 .2

23.0

17.7

-2.8

2.41950

258.1

54.8

37.9

-9 .0 8 .0

-21.2

14.7

3 .5

3. 11955

363.1

87.9

63.3

=

12.7 ' 11 .9

74.2

17.4

,3 .5

' 3 . 31960

482.8

127.0

88 .4

20.2 18.4

26 .3

18 .3

4 .2

3 .8

"

a . For calendar year ending six months before, eu&of fiscal year, i.e.,,fisc l year j"O collectioasopplicd :o ca endwryear 1959 gross national prodaet. =

b . Includes social insurance taxes ._

c. Not available.

Source:

V. S. Department of Commerce.

,

i

, ,

IC .

-

Table 2 -

STATE TAX COLLECTIONS FROM SELECTED SOURCE S

Selected Fiscal Y*ws 1902 — 1%0

_

c

General sales tJee~leT-Fiseal

Taal

at Gross

Inaviiwl

Corporation

flish . t

erect Com -Yew

Tears

Receipts

Mew

Inewe users

P-p-y

pe-series

06.4

A. Aureart (MIli.ns)

;%

i90Q

i ; 156

-

-

- -

S82

(c)

S

741922

947

-

S

43

- - S S8 $ 165

348

(c)

3331932

1,810

S

7

74 1162

328

(c)

3401410

4,157

_

499

2%

155 1.226

260

S 144

967`

1946

5.971

899

389

442 1.325

249

LOU

1.6331950

8, ."ll

1,670

r 724

S86 2.299

30

LOU

2.3411955

12.735

2.637

- 1.091

737 3.114

412

1.138

- 3,2731960

20,352

4.302

2.209

1.180 6803

607

2.316

46935

1!. Pdreente:e Distribetion

1902

100

-

-

- -

52.6 - --

(e)

=47d1922

100

-

4.5 __17.4

36.7

(c)

35-21932

100

0-4

3-9

4 .2 45.6

17-4

(1)

21-61940

100

12.0

S-0

3 .7 29-5

6-3

203

_

2331946

100

1S-I

6-5

7-4 22.2

4-2

17-3

27-3i9s0

.00

18-6

8-1

=

6-5 25-7

3-4

11 .5

26.2_

19Mc

100

20.7

8.6

S-8 27-0

3-2

8.9

25.71960

100

21-1

10.9

5.8 23.6

3 .0

114

24.2

ja. taelades rotor fuel tai asa scoter vehicle end operators licences . 1

=

b. Includes death gad gift, tobacco. alcoholic beverages, severance, life issaraee premiss, pablie atiliti . security traasfer,pari-mutuel g ad other.

e. Not available .Source :

t . S Depertnew o; Coaraseice.

of this increase was for traditional state functions . But on retail sales in others, and here and there on miscel-other focal were at work. Growth of highway spending laneous items.was tied closely to the Federal highway program. Evenmore powerful was the increasing pressure from local The increase in state grants contributed to a change in

governments for financial aid. Although property tax the relativY size of state and local spending. Whereas i n

revenues rose rapidly, they failed to satisfy demands, and 1902 the states were spending only 17 per cent of the

localities turned to states with success . State payments to

5total, their share was 53 per cent in 1959 . 1

local governments doubled between 1946 and 1950 and Where did the states get the money? The growth of th edoubled again between 1950 and 1960 (Table 3) . A few economy automatically increased yields of many existingstates also acted (eight in 1947) to permit local govern- taxes. Deliberate action has also been required, and therements to impose new taxes. New York authorized locali- has =n much . Each set of kgislati%v sessions bringsties to impose certain specified levies ; Pennsylvania, on dozens of major changes and hundreds or thousands o fthe other hand, granted local governments permission toenact any tax not being imposed by the state. The resultsincluded local -taxes on wages and salaries, in some cases,

, State grams to localises are counted as state expenditures inthese figures.

12

i i n amendments to state tax systems. Although aver

The major emphaSK, without question, has been an

the rats there have been broad studies of state systems

wounawmQtion taxes. Tobacco and motor fud taxes among

as a wbok, the changes actually made have for the most

the selective erases have been made to product ever-

part been piecemeal- The results include considerable

increasing reaeaures_ Alcoholic beverage tax rates hav evariation (Table 4).

also ban used. More important, however, has been the

EXPENDITURES, -REVENUE AND DEBT OF STATE AND LOCAL GOVERNMENTS

Selected Fiscal Years 1902 -1%0a(Wiliens)

Etr~ettditures

Revenue

Inver-

Froea

later-Fiscal

govern-

- Own

govern-

Gros sYear

Total

Direct"

watttold

Total

Sources

taentole

Debtb

A. ' State Go"n mmds

1902 ;

188 S

136 S

52 S

192 S

183 ;

,-

9 ;

2301922 1 1 397 : 1085 _ 312 1,360 11234 126 1,1311932 2,829 2,028 801 2,541 2,274 267 2,8321940 -

5,209 3,555 1,654 5,737 5,012 725 3,5901946 7,066 4,974 2,092 8,576 7,712 865 2,3531950 15,082 10,861 4,217 13,903 11,480 U23 5,2851955 20,357 14,371 5,987 19,667 16,678 2,988 11,1981960 31,596 22,309 9,283 32,838 26,093 6,745 18,543

B. Local Government s

1902

; 965

; 959

; 6

$ 914

; 858

; 56

; 1,8771922

4,594

4,567

27

4,148

3.827

321

8,9781932

6,420

6,375

4S

6,192

5,381

811

16,3731940

7,743

7,685

58

7,724

5,792

1,932

16,6931946

9,156

9,093

63

- 9,561

7,416

2,145

13,5641950

17,189

17,041

- 148

16,101

11,673

4,428

18,8301955

A6,230

26,004

226

24,166

17,811

6,355

33,0691960

39,280

39,071

209

37,527

27,576

9,951

51,21 3

a. I960 data include Alaska and Haxaii.b. Short- and long-term debt outstanding at end of fiscal year .c. Direct expenditures are amounts as finally disbursed by units of government for their own fane :ioas regard-

less of source of receipts . Include expenditures for utility, liquor stores, and iasurance trust; exclud epayments for debt retirement .

d. Intergovernment%I expenditures : state, principally fiscal aids and shared taxes to local government ; local ,principally payments to state government for shares of p- -:-grams administered by the state, services per -formed by the state and repayment of advances .

e. Intergovernmental revenue : state, principally Federal aid ; local, principally fiscal aids and shared taxe sfrom the state.

Source : U. S. Department of Commerce .

13

"• tee 1"! rr !' p

~• ~~R rir

ifWE~at

R

ri Z ~ • ~

d

•x w

r ~r

s

f.f

N b. iw f . : .N S .Mi►inM~~~b1~ N .~.M Ni~~.lbh V ~M~AMN41M~+ FIMi~~MIJ fJM~~i(Ar~i1~r ~

1i

F

I w w M N M I N N r I r IN at w X M ~• ~+ 1 '" 1 N N 1 1 M 1 1 N 1 M M M N 1— r M N N Zi

( M N N N w I N X 1 1 ++ « +!• N 1 N X N I K 1 r M 1 1 X I I M I II K K N I ~A - X K «+ I N I I w r 1

1 M M r M X I X I I I M r N N I + f X I N I N K I I I I I K I N N N M I I Z 1 ••• Z I N I I N N I

I N N 01 N I l f l l l W O( N N I K I I I M I N N I I I I I M I K K II N 1 0 1 1 (M I I N I I -- Of

M K r N +'+ X I M X w I I N w r N I w ..• I ~• fK M r I I I X r N K K 1 N w w— N K K 1 N M N 1 1 N

I N N N M w I I O( I w l 1 +++ N K N I +~'+ N 1 ~+ +~ N M I I I f N N K N I M K r+ +~ w N N ( ~• r m l 1 Of

I N N r r r I I w ( N I I N N ++ N I w ~* I r N N N I I I I N r N N 1 OC N N i N M N 1 K r r I I N

I N *~ Of N N I I N I N I I K N M K I K K I N Of N N I I I I M OC N K I N N Of I N Of N I N N K I I K

• M N w r I w I M M w I I (K ~' N M 1, r N I- N N — I I N X w w N N 1 M r f 1 — I K I K N N 1 Z M

I w N N N I Oi 1 O( 1 +++ 1 1 A< N N K I K w 1 ++ «• N N I I N I M +•+ N pf _ I N •- I I N I K I N w -- 1 1 ~-

M IK w ~+ I X I N I N 1 1 O( N w M 1 w w I w M M N 1 1 M 1 M w It M 1 Of `+ I I M I N I N ++ •+ I I w

M N 09 M 1 M 1 N I N I I N N M N I Of 11 1 N Of K N I I N I N pf K N I N N I 11 N 0 K I N N N I I N

~

J

~

>

~

~0

I

j

, I

r Nrrwrr N Nrww N Nr Nr i Nrrw Nrr Nr N Mr Mr N N Z K K .- iJ, N Nr xrr N K r N

J

I Nrr N N r N r I K N N N N w N r 0i K OG N N N r N N N w X r OC K r K N w IIC r K w K N N X r x x

1 Nr N N M Nrr I r N NrX rr N Nr Mww N Nrr Nr K Nr r K N N .,

rrr K xrV' r r x

I N r N K r r r r I Nrr N x w r N r K N N M M K,_ .N. r N K M N r x x r K N K r r r r r r x N w N N

i

r K N Z I r r N Nrrr M r r 116 N r Z r r r r r r r r 'I r r r 1 K r 1 r r .. K ,r K r Z w r rw

I Nr I I Nr Nr Ir N N r Nr Nr I

N NrXr N N K N . r N lrr N 1 .+. NQ'wrrr K Irrr Z

1 MOC I I NXI r NZ Nr Nwr I wXZ N I X X X NZwr ( r M N I rw~.w Nr xr I rZ r f

I N N l l r I X N I X X I N N N r Z I r I I N I I I I N I X N I N x w I x x OC K n M x K 1 x 1 Z 1

ZI

r

=

ti

r M N N M N r N N N N N r M N N N N N r N N N~ 0 : r., N r r N r N K r K N .+ r K r N N .. w ~. r r N N 4

I N Nr Nr N NOI I N r N r N NIY.rY..rr M N rrrrrwl>< N Krr N N r N xr Krrr N Nrr r

I M N r w r w N w ( N M N Nrw Nrrw Nrr N r N r M N r N r N r r r r r r K N N K r N w K M K

I N N N M N K M N I r N Nrr N N x M N x M N K N N N N M N M N N IK r K x x N N K N K N r x x x x

F'+i

YYY~~q~r

~

tl"e

V

Ill. CRITERIA FOR JUDGING A REVENUE SYSTE MWhat features make one revenue system better tha n

another? What are the criteria to be used in judging atax system?

Evaluation of criteria can benefit from a far more ex-tensive summary of economic elements than is possc'bde

_

hen. Five points, however, are too important to over-look in even a highly condensed discussion of criteria .

1. Taxes are paid by propk—not by "reall estate, ""gasoline," "business,° or any inanimate thing. A taxcollected from a corporation is, in any significant sense,paid by customers, employees or other suppliers, o rstockholders (in the form of a reduction in either divi-dends or net worth) .

2. _Although there is truth in the assertion IthAt everyone's taxes must really be paid out of his income, thisfact does not mean that income is necessarily the bes tbasis for all taxation. The income a person receives is th emarket's measure of the worth of what he and his prop-erty have produced, i .e. put into the economy. His spend-ing for consumption is the measure of what he takes fromthe production of the rest of the economy. Taxes basedon income are taxes governed largely by the value ofcontributions to society. Taxes based on expenditure arelevies governed by what a person uses up of withdrawsfrom the economy.

3. Present costs of government are so high that m.Sinevitably have an important impact upon everyone . Theaverage—about $780 per capita—is higher than some _

A. REVENU E

people can pay; it is above what others can reasonably_ be expected to bear. Consequently, some people mus t

pay more than others . In deciding how the heavy costsare to be shared, the public faces difficult problems ofachieving "justice."

4. High tax rates in themselves--disregarding the -amounts they take from the people—produce bad effects .When the rate is ' high, efforts to escape tax becomeworthwhile. Individuals and businesses will take whatwould otherwise be a second. third, or fourth choice intheir investment, consumption, or business decisions i fby doing so they can save a heavy tax. High rates appliedto a small base invitz the manipulation of the base.Economic distortions result. What determines the heightof tax rates? The level of spending is obviously of prim eimportance, but the sine of the tax base is acso crucial .The broader the base, the lower the tax rate needed t oproduce any given volume of revenue. The broader thebase, the greater the difficulty of manipulating it to saveany substantial portion of the tax.

5. The size of the taxing jurisdiction profoundly influ-ences the choices it can make among revenue sources.Therefore, the criteria properly used in evacuating a stat erevenue system differ from those appropriate wher eithe rnational or local systems are considered . Yet each tax ateach level of government must be judged as part of thewhole system of public finance_ This system include sgovernment spending, an element which the public mustalways keep in view when examining the tax cystem .

The chief job of a tax system is to bring adequaterevenues. Each particular tax must be judged first on thebasis of its revenue potential, and this involves chiefl ythe breadth of its base . Large expenditures call for taxeswith broad bases_

Revenue srahilin is important for states and'.ocalities .Most state-local expenditures (except capital outlays )fluctuate little from year to year. Paying for them re-quires revenues which arc also highly stable during busi-

ness fluctuations. A situp in revenues during recessionsmay not only force curtailment of normal operations bu talso prevent states and localities from providing ade-quately for the increase in relief loads. Exceptionally hig hrevenues during boom times invite wasteful spending . Ofcourse, reduction in tax rates or in debt is always pos-sible . So is the accumulation of surplus. However, themoney on hand is likely to become, soon, money spent —perhaps even the start of a new program or a permanen texpansion of one already established.

B. DISTRIBUTION OF TAX BURDEN S

Fairness, Justice, Equity

All of us agree that where taxes arc involved, fairnes sis of paramount importance . However, we run into dif-ficulty in trying to dcfine what we mean by such esscn-

18

tially interchangeable terms as "fairness," "justice,"- and"equity."

" -

1 . On one aspect of equity there will be a consensus ."Every taxpayer shall be treated according to legal rules

which apply equally to all taxpayers in the same class ."

more than ottxrr . On occasion. these benefits can serieFairness requires that there be no prejudice, whether by as an equit2ale basis for imposing a tax .

= -- -_

:" .-

accident or design, in the application or administrationof the law. Nor fuel and licensc taxes and the part of the socia l

: '~s".uity payroll taxes on the employee axe commonly -2 . Widespread agreement can be expected on another

-- justified on the benefit basis. Perluts more significant is

- -_. "concept—horizontal equity. -Equals shall be treated-' another aspet t of benefit. Reti&ms of some communities - =equally:' Everyone on the same income love ll o- con- pay higher taxes than residents of whers be- ::se of dif-suming about the same things, and otherwise in essentially ferences in the goveannser t service ; received. The same

"similar circumstances, shall bear the same portion of the applies at the state'!e%mee_ One merit of deoentraliution in

- -expenss: of government . When their circumstances differ _ government 1!- L;.at it offers more opportunity than doesin ways that are significant for the sharing of the costs of a centralized system for people to decide fieeiy whether

=government--size of family or total of medical expen& the benefit of certa_ is put licy. _exPendirues 'are x"orth

-rfaces, for examp~ requires that tax loads their cos

-L

-

-differ- _

-

--

-' Shifting Trieste retpk Otdside the State _ -

-3. The difficult problems that then arise are those - . = -- States eve- tried to take advantage of the possibilitie s

'_

which involve sertical equity. Now much of that differ- fof passing some c2' their tax burden to outsiders . One

=

-ehew will warrant flow much difference in tax? Them is k;a i of opportunity arises from the deductihiiity pro -little consensus in answering this question, but the_un- . vlded in Federal tax, lases. Rational seli:-interest requires_equal treatment of taxpayers must rest on reasonable,-not

-_-suety state to camider carefully ; all the opportunitiescapricious, bases.

- _ _Congr -ss albws. A second type of opportunity to shift

=Throughout much of the Western world there has -=-' burdens to pasons outside the state appears chiefly i n

grown up a general notion that tax burdens should re- taxes wf5ch fall initial:y-on bttsinesses . Property taxes

_floc[ "ability to pay" This concept, however, is about as on_ mi_-oad terminal property may bring far more rev-

unclear as "fairness:' There is also wide acceptance of ,=ax than local 'z~idents can ptr~il+ly be said to bear. Atthe idea that the tax system should be progressive. What fast a portion of state ewx wit:r, pr+ .pe :ty, excise and pay-basis is there for deciding how much more in taxes it is = = roll taxes on business fems, especially levies on the big-

= -fair to demand from the family with as income of S10, gat companies,-Arc widely diffused among consumers

,000 than from the almost similarly situated family with and stoekWdcrs over much or all of the country. Non-S9,800 or the very differently situated family with S8,000 -- residents aiso pay part of the individual income and in-or S 12,000? Ardent supporters of progression as a device `-' lteritance and estate ':axes colkcted by many states.for discriminating fairly may disagree strongly on the Tourists payS*..s and excise taxes. In general, however,fairness of a given set of rates. When does increasingly the sl-iUty to shift tax': to residents of other states i ssteep rate progression become unfair? Ur%hed_-Caution should take precedence over greed .

Some advocates of progression make much of the '--Other Considerstionf Affecting the Distribution of Tax Br"rdenspoint that reducing economic inequality is socialy desir-able . Whatever reasons can be cited for this argument i njudging Federal taxes, it cannot have appreciable weightat the state level . Imagine, for example, a state trying t odiscriminate against upper income and wealth groupsheavily enough to reduce inequality significantly . Anexodus, more gradual than sudden, of people of wealthand talent would largely defeat the attempts.*

Benefits from Government Spending as a Basis for Taxatio n

Another basis for differentiating tax burdens may b ethe government services received—the benefit principle .Although governmental spending is presumably done t ofurther the general public interest, individuals as such dobenefit from some expenditures, and some individuals

• The apparent exception in state death taxes rests largely on th eFederal credit .

Four more points deserve mention . (1) Differences i ntaxes arc :ustificd in some cases by the desire to influenceproduction and consumption in the interest of the gen .:raiwelfare—philanthropic exemptions offer ore example,high rates or. whisky another. (2) Unfortunately, con-clusions about how taxes are in fact shared among mem-bers of the community are always tentative . Our knowl-edge of shifting--espec ially of taxes on bush.ess—is farfrom satisfactory. (3) One explanation of differences i nthe sharing of taxes is that political power is unequal .The sralc of progression of an income tax, for example .may rest in part upon the fact that the highs* the positro nin the income scale, the fewer the voters . (4) An idea,tae would create ne serious hardship. In the real world .unfortunately, hard cases are to be expected . Y hay de-serve attention . But they must not dominate . A tax. law

,̀'designed specifically to meet the unu,-ual situation willhave unwelcome results as it applies more broadly.

(

i

C, fr~f,Y!t,QH1C -_RFFICIENC ~ _

1- l~AWngAtiocatien Distwtionsata Minirom

eratiotu.3 Exceptions may appear if business as such put sEfficiency in the alloca on d productive resources ~ government 1i- special cosh---m receives special benefits

(h~:mait and material) is important in .. adfvzncing the

'from expenditures- Except for highways, examples at the_ general welfare. Taxes affect rewarce aflo~atiou. -ihc - _stP.te level are rarely important.

-' general objective shoutl be taxes which hinder as little - ~ In esterase with the days when our economy was pre -=°

as possible the etiiciew. operation of face markets. As ageneral principle, taxes should be neuttal or impartial-in -

: _ dominantly agricultural, those persons who today mak e

-=

their effects on resauroe 211mation—among Fivate in=—ions about where to produce have some choice

about where to locate. Taxes and governmental servicese'ustries, regions, acxttpations, ms'ilxtds : of operation, ' AM amot$ the factors which influence decisions on busi-forms of organization, and so on.

tress location. High taxes- are certainly not a favorabl eThe inevitable repressive effects o a tax should inter-

fere as little as possible with tirs accomplishment- ofgovernmental objectives of the public . For example, i fthe improvemeat of transportation is a =cal of publicpolicy, as evidenced by highway spend rg,- taxes whic hburden railroads may quite probably aggravate the dif-ficulty the expo_ ndhure seeks to alleviate.f '

-

-tunues to use what u essentially pncutg or the dualobjective of getting revenue and reducing expen&-ture .Nevertheless, occasional reexamination of the entir erange of possibilities is in order.

Taxes also have a job to do in alerting citizens to th ecosts of government. Taxes which make the public awareof what it is paying for governmental services can help

c , in comparing the worth of the services received with themoney sacrificed to pay for them. Every citizen should b emade to recognize the fact that he pays taxes . Otherwisethe sense of political responsibility will not develo padequately.

Certainty

Tax statutes, regulations, and administration shouldbe reason?hly stable in their basic elements . Otherwise,

However, taxes on business do not improve the proc-

uncertainty about tax laws adds to the difficulties of busi -

ess by which consumers indicate their desires . Further-

ness and personal planning for the future . Although it is

more, business taxes do not help-indicate to managers

not necessarily true that "an old tax is a good tax," th e

*Teich inputs most need economizing . A business has an

economy will have adjusted to it . A considerable degre e

incentive to sacs on taxes. Unfortunately, in adopting

of certainty in the tax system is desirable, especially when

methods which cut the tax bill, it may not operate more

taxes are as heavy as they arc today ; otherwise, decision

r'"efficiently in the sense of less labor or fewer materials

making becomes needlessly complicated, and efficienc y

--Ter emit of output . A business, in fact, may wisely adopt

suffers .methods which are inherently second choice because th e

artificial factor of taxes makes such methods best under

y ne reduction in business taxes would presumably lead to antire-ciresumstattces .

- —

increase in taxes on individuals and thereby enlarge the influenceof taxes on personal decisions. To some extent production as well

-

The broad public interest would be advanced by gen-

as consumption would be involved . On the whole, however, the

erall3 • freeinbusiness decisions from most tax consid-

total effect on the creation of income would doubtless be lessg

than _when "business" pays, Me same total . . ._

.2~

element unless they finance governmental services which'eitber facilitate economic activity or appeal to the peoplewhomust foot the bill. -

;Inl(eeisee oa the Oonntrt : tar 6ourarameM Sarin

In free markets it is prices which make buyers awar e~. of cost and which induce economizing. Revenue sources

' Where for some persuasive reww. interfereace with - 6 have a comparable job as regards government spending .ft market economy seems likely to =e-. a the public - -

_ interest, tax discrirn.~nations may be-`dev=_cd to alter

Sometimes a government may charge for a service i n

resource allocation . Taxes may, on occasion . serve a

a way that influences the quantity demanded, for ex-

useful regulatory

-ample, tuition in universities. i'tt.. charge not only col-purpose—thcwgh, of ceur~e, : ihty m1y:kL revenue; it can also reduce the need for governmen taiso regulate hanm.ully.

_

to spend to provide the function. States have few oppor-

: "Businoes" as an Object of Taxation

AlthoLe, "business" is a favorite oojec: of ("r-dun,= one can well ask, "Why"? Business is our major agenc y

' for organizing to produce—for allocating productivecapacity and its use today and for undertaking economicgrowth. Businesses are groups of people seeking to t; nc-fit themselves by serving otners. Taw are riot likely tohelp business serve efficiently in produdng. = -,- -

Broadly, the public interest calls iri each business (1 )-to tern out products or services which are wanted morethat. somahing else, as re3scted in freely mzde con-sumer decisions expressed is the market or through gov -ernmental age pcics and (2) to use methods which econ-omize on labor, materials, capital, and other "inputs"according to their relative scarcity and productivity.