Embed Size (px)

Citation preview

The Bonadio Group

Please see below for a brief summary of some of the significant changes enacted as

part of the Tax Cuts and Jobs Act (TCJA).

Individual Changes

Tax Rates

The new bill that was signed into law has seven income tax rates, but they are now

generally lower with the highest rate being reduced from 39.6% to 37%. The maximum

rate of 37% applies to single taxpayers with over $500,000 of taxable income and

married taxpayers with taxable income exceeding $600,000. The tax rates applicable

to net capital gains and qualified dividends did not change. These rates are effective

Jan. 1, 2018 through Dec. 31, 2025.

For the period starting Jan. 1, 2018 through Dec. 31, 2025, the AMT exemption amount

has been increased to $109,400 for married taxpayers who file jointly ($54,700 for

married taxpayer filing separately) and $70,300 for all other taxpayers. The exemption

phase out was increased significantly, with it not applying unless adjusted gross income

(AGI) exceeds $1 million for married taxpayers and surviving spouses or $500,000 for

all other taxpayers.

Elimination of Personal and Dependent Exemptions

In the past, taxpayers received an exemption for themselves, their spouse and each of

the eligible dependents that they claimed on their tax return. The TCJA eliminated these

exemptions through Dec. 31, 2025.

TAX CUTS AND JOBS ACT

Connect with us:

Lynn Mucenski-Keck, CPA

Manager

585.200.5144

Increased Standard Deduction

The new standard deductions are:

• Heads of household: $18,000

• Married filing jointly: $24,000

• All other taxpayers: $12,000

Although you may have historically had itemized deductions

exceeding these amounts, other changes to itemized

deductions may affect whether your itemized deduction

exceeds the standard deduction in a given year. The

increased standard deduction is effective through Dec. 31,

2025.

Changes to Itemized Deductions

• The overall phase out of itemized deductions has been

repealed.

• The itemized deduction for state and local taxes is

limited to a total of $10,000 ($5,000 for those using the

filing status of married filing separately). For example,

if you paid $15,000 in state income taxes and $6,000 in

real estate taxes on your home ($21,000 in total), you

would not be able to deduct the $11,000 that exceeds

the deduction threshold. In addition, taxes that were

prepaid in 2017 relating to the 2018 tax year must have

been assessed prior to December 31, 2017 in order to

be deductible on the 2017 tax return.

• Mortgage interest on loans used to acquire a principal

residence and a second home is only deductible on

debt up to $750,000 (down from $1 million). The new

law reduces the ceiling of acquisition indebtedness to

$750,000, unless the indebtedness was incurred before

Dec.15, 2017, where the limitation is still $1 million.

• The deduction for home equity indebtedness is

suspended. However, there is a possibility that home

equity indebtedness may be categorized as acquisition

indebtedness, loans used to acquire, construct, or

substantially improve a home. In addition, consideration

as to whether the indebtedness is used for business or

investment purposes should also be explored.

• Cash donations to public charities are now deductible

up to 60% of adjusted gross income.

• Donations to colleges and universities for ticket or seat

rights at sporting events are no longer deductible.

• Miscellaneous itemized deductions, such as investment

management fees, tax preparation fees, unreimbursed

employee business expenses and safe deposit box

rental fees are no longer deductible.

• Medical expenses are deductible by the amount the

expenses exceed 7.5% of adjusted gross income for

2018 (limit changes to 10% starting in 2019).

These changes (except as noted) to itemized deductions are

in effect from Jan. 1, 2018 through Dec. 31, 2025.

New Deduction for Qualified Business Income

A new deduction, often referred to as the pass-through

deduction, was introduced in the TCJA that allows

individuals a deduction of 20% of qualified business income

from a partnership, S corporation or sole proprietorship, as

well as 20% of qualified real estate investment trust (REIT)

dividends and qualified publicly traded partnership income.

The pass-through deduction is available for tax years after

December 31, 2017 through December 31, 2025.

The Bonadio GroupTAX CUTS AND JOBS ACT

This deduction will reduce taxable income, but not adjusted

gross income, and is available regardless of whether an

individual itemizes their deductions. There are many

limitations and restrictions to this provision, including the

following:

• The activity must give rise to a trade or business, which

is particularly important to rental real estate activities.

• If a married filing joint taxpayers’ taxable income

exceeds $315,000 (or $157,500 for all other taxpayers),

and the business is considered a specified service

trade or business the deduction will be reduced or

completely disallowed. A specified service trade or

business includes any trade or business involving

the performance of services in the fields of health,

law, accounting, actuarial science, performing arts,

consulting, athletics, financial services, brokerage

services, or any trade or business where the principal

asset of such trade or business is the reputation or

skill of one or more of its employees. In addition, the

performance of services that consist of investing

and investment management, trading, or dealing in

securities, partnership interests, or commodities.

• If a married filing joint taxpayers taxable income

exceeds $315,000 (or $157,500 for all other taxpayers)

and the business is not considered a specified service

trade or business, additional wage and property

limitations could apply that may lower or eliminate the

20% deduction.

• Temporary treasury regulations were recently released

regarding the 20% deduction, which provide further

guidance regarding the ability to aggregate businesses

in order to receive the most effective deduction. In

addition, guidance was provided regarding the

treatment of entities that have common ownership

and that provide service or property to related entities.

Due to the intricacies of the new law, we strongly

encourage our clients to reach out to their advisors

directly in order to review their current structure and

ensure appropriate planning takes place to receive the

maximum benefit of the 20% deduction.

Loss Limitation Rules

Effective for tax years beginning after Dec. 31, 2017, any

business loss over $500,000 for married taxpayers filing

jointly or $250,000 for all other taxpayers is disallowed. In

order to determine an individual’s business loss one must

combine all their deductions and gross income related to

their trades or businesses.

Any excess business loss is treated as part of the taxpayer’s

net operating loss carryover to the following year. The

limitation applies at the partner or S corporation shareholder

level. The limitation expires after Dec. 31, 2025.

Net Operating Loss Utilization Rules

The carryback of net operating losses is repealed effective

for tax years ending after Dec. 31, 2017. Net operating losses

generated for years beginning after 2017 cannot reduce

taxable income by more than 80%. Net operating losses

carryforward indefinitely under the new law.

Other Adjusted Gross Income Adjustments

• The tax law suspends the deductibility of moving

expenses and exclusion for reimbursement of qualified

moving expenses. The provisions related to members

of the Armed Forces remain. The suspension of the

moving deduction is applicable from Jan. 1, 2018 to

Dec. 31, 2025.

• The new law repeals the deduction for alimony paid

and the inclusion of alimony received for divorce

decrees executed after Dec. 31, 2018. Therefore,

clients considering modification of an earlier divorce

agreement should be aware that this may change the

tax consequences.

The Bonadio GroupTAX CUTS AND JOBS ACT

Sec. 529 Plans

Sec. 529 plans have been a widely used tool to help

taxpayers save money for college, presuming they distribute

that money for qualified higher-education costs. Depending

on your Sec. 529 plan, you may be eligible for a state tax

deduction for contributions to the plan. The TCJA expanded

the opportunities available for education tax planning by

permitting $10,000 per year to be distributed from Sec. 529

plans to pay for private elementary and secondary tuition.

Contact us to learn how these new rules may help you pay

for private school tuition for your family.

Child and Family Tax Credit

The updated child tax credit is designed to help reduce

the tax burden related to the disallowance of personal

and dependency exemptions, as well as changes made to

itemized deductions. The TCJA increased the child credit

for children under age 17 to $2,000 and also introduced a

new $500 credit for a taxpayer’s dependents who are not

their qualifying children. In addition, the phase-out limits

for these credits have increased to $400,000 for joint filers

($200,000 for others), so that more individuals will be able

to take advantage of this credit.

Utilization of Opportunity Zones

The new tax law also added the ability for certain

investments in Opportunity Zones to allow for potential

preferential tax treatment. Opportunity Zones are an

economic development tool, designed to spur economic

development and job creation in distressed communities.

The first set of Opportunity Zones, covering parts of 18

states, were designated on April 9, 2018. Individuals have the

ability to invest in Opportunity Zones, even if they do not

work, live, or have a business in a Opportunity Zone area.

In general, if an individual creates a gain with an unrelated

person they may defer the gain up to the amount invested

in a qualified opportunity fund if contributed within 180 days

beginning on the date of such sale or exchange. The gain

will be deferred until the date on which the investment in the

opportunity fund is sold or December 31, 2026. If applicable,

please contact us for further details.

Business Changes

Tax Rates: C Corporations

The new corporate tax rate is 21% effective for tax years

starting Jan. 1, 2018. The corporate AMT is repealed effective

for tax years beginning after Dec. 31, 2017. The law continues

to allow the prior year minimum tax credit to offset the

taxpayer’s regular tax liability for any tax year. However, for

tax years beginning after 2017 and before 2022, the prior

year minimum tax credit is refundable in an amount equal

to 50% (100% for tax years beginning 2021).

The significant reduction in the income tax rate for C

corporations has led many businesses to consider converting

to C corporation status. While changing one’s business

entity to a C corporation may be beneficial for some, it is

not the appropriate choice for all structures. If you have

been considering a change in entity structure, please reach

out to your advisor for further analysis and discussion.

Net Operating Loss Deduction

The new law limits the net operating loss (NOL) deduction

for NOLs arising in tax years beginning after Dec. 31, 2017,

to 80% of taxable income. Net operating losses generated

in taxable years beginning before January 1, 2018, will not

be limited. The new law also eliminates NOL carrybacks and

allows unused NOLs to be carried forward indefinitely.

Due to the limitation that exists for losses created in tax year

beginning after December 31, 2017, businesses that generate

a taxable loss should ensure that they are accelerating

deductions and deferring income to the greatest extent

possible for tax years beginning before January 1, 2018.

The Bonadio GroupTAX CUTS AND JOBS ACT

Repeal of Domestic Production Activity Deduction (DPAD)

The new tax act repeals the DPAD effective for tax years

beginning after Dec. 31, 2017.

Changes in Methods of Accounting

Taxpayers subject to Sec. 448 (other than tax shelters) with

three-year average annual gross receipts of $25 million or

less are eligible for the cash basis of accounting. The prior

year exception defining small businesses was removed.

Thus, if a business with gross receipts above the $25 million

threshold drops below this threshold, it may change to the

favored methods.

Taxpayers who meet the $25 million gross receipts test

are also not required to account for inventories and are

excluded from all parts of Sec. 263A. Lastly, the dollar

threshold for long-term contract income recognition for

certain construction contracts has been increased to $25

million.

Provided the income threshold has been met, the new law

could allow clients to change to more favorable accounting

methods and thereby allow income to be deferred until

actual receipt and expenses not recognized until paid.

The new provisions are effective for tax years beginning

after Dec. 31, 2017.

Taxable Year of Inclusion for Accrual Based Taxpayers

Under an accrual method of accounting, income is includible

in gross income when all the events have occurred which

fix the right to receive such income and the amount can be

determined with reasonable accuracy. The new tax law has

added that the “all events” test is treated as being met no

later than when the item is considered revenue for financial

statement purposes.

Depending on how an item is treated for financial statement

purposes, this could accelerate income recognition for some

accrual basis taxpayers.

Interest Expense Limitation Rules

Prior to the Tax Cuts and Jobs Act of 2017, the interest

expense limitation rule applied to a very narrow group

of businesses. However, under the new interest expense

limitation rule, the number of businesses affected is much

more expansive. The deduction for business interest is

limited to business interest income, 30% of the adjusted

taxable income (as defined in the new law), and the floor

plan financing interest.

The definition of adjusted taxable income for purposes of

the limitation is generally taxable income before income

tax, depreciation, and amortization for taxable years before

January 1, 2022. However, starting in the 2022 taxable year

the limitation becomes even more restrictive as adjusted

taxable income no longer allows a depreciation and

amortization addback, and is instead based on taxable

income before income tax.

The interest expense limitation rule occurs at the taxpayer

level. Therefore, the limitation is applied at the level of each

partnership or S Corporation. Currently, no aggregation

rules exist for partnerships or S Corporations. However, the

IRS has provided clarification that for a group of affiliated

C Corporations, the limitation will apply at the consolidated

tax return filing level.

There are two major exceptions in which the interest

expense limitation rule will not apply. The first exception is

provided for small businesses (IRC §163(j)(3)). The interest

expense limitation rule does not apply if a taxpayer has

average annual gross receipts for the 3-taxable-year period

ending with the prior taxable year that do not exceed

$25,000,000. However, for purposes of determining

whether the small business exception is met a taxpayer must

follow aggregation rules. The second exception to avoid the

interest expense limitation rule applies to business that can

qualify as a real property trade or business and choose to

make an irrevocable election.

The Bonadio GroupTAX CUTS AND JOBS ACT

The term real property trade or business means any real

property development, redevelopment, construction,

reconstruction, acquisition, conversion, rental, operation,

management, leasing, or brokerage trade or business.

Similar to the 20% pass-through deduction, the interest

expense limitation rule is very complex. If you suspect that

this limitation rule applies to your business, please reach out

to us for further review and planning.

Entertainment and Transportation Expenses

Generally, entertainment, leisure, amusement, or recreation

expenses incurred after December 31, 2017 are no longer

deductible, regardless if the ordinary and necessary trade

or business test is met. However, there are some exceptions,

including expenses for recreational, social, or similar

activities primarily for the benefit of employees may still

be 100% deductible.

Taxpayers may still deduct up to 50% of expenses for

meals (off the premises) provided they are considered

“directly related” or “associated with” the active conduct

of the trade or business. Taxpayers may continue to deduct

50% of the costs associated with meals provided for the

convenience of the employer through December 31, 2025.

However, expenses paid after December 31, 2025 in relation

to providing meals for the convenience of the employer will

no longer be deductible.

The act also repeals the deductibility of qualified

transportation fringe benefits, including commuting or

subsidized parking expenses (including pre-tax salary

reductions) of employees (except if necessary for employee

safety).

Now is a good time for taxpayers to review their current

accounting, reimbursement, and employee meal policies, as

well as their documentation procedures for meals. Taxpayers

should consider creating separate general ledger accounts

for entertainment, meals, and employee holiday parties in

order to have the expenses correctly categorized at year-

end for tax preparation. Taking the time to accurately record

expenses as meals or entertainment throughout the year

will help ensure that all eligible amounts are captured for

deduction.

Like Kind Exchanges

The new law restricts the non-recognition of gain in a Like

Kind Exchange to exchanges of real property effective for

exchanges completed by Dec. 31, 2017. Therefore, clients

who exchange personal property after December 31, 2017

will have to recognize a gain on the transaction. In addition,

for real property exchanges, consideration should be given

to any personal property in the building.

Changes to Cost Recovery

• Taxpayers are allowed to claim a 100% first-year

depreciation deduction on qualified property that is

acquired and placed in service after Sept. 27, 2017.

The use of the qualified property does not have to

originate with the taxpayer, which allows new and used

property to qualify for bonus depreciation. Starting in

2023, there will be a phase out of 20% each year until

2027 when the first year additional depreciation is 0%.

• The Section 179 deduction was also increased from

$500,000 in 2017 to $1,000,000 in 2018. In addition,

the deduction does not start to phase out until Sec.

179 acquired property exceeds $2.5 million. Lastly, the

definition of qualified real property that is eligible for

Sec. 179 expensing now includes improvements to

nonresidential real property such as roofs, heating,

ventilation, air conditioning, fire protection, and alarm

and security systems placed in service after Dec. 31,

2017.

The Bonadio GroupTAX CUTS AND JOBS ACT

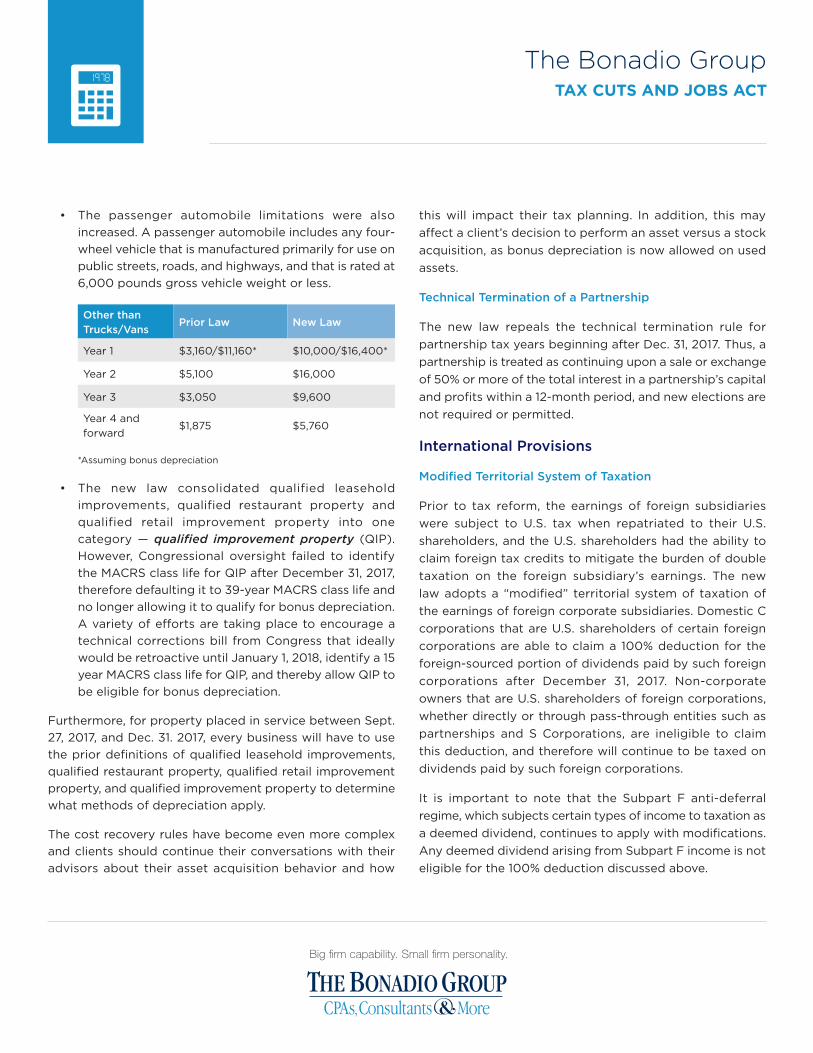

• The passenger automobile limitations were also

increased. A passenger automobile includes any four-

wheel vehicle that is manufactured primarily for use on

public streets, roads, and highways, and that is rated at

6,000 pounds gross vehicle weight or less.

Other than

Trucks/VansPrior Law New Law

Year 1 $3,160/$11,160* $10,000/$16,400*

Year 2 $5,100 $16,000

Year 3 $3,050 $9,600

Year 4 and

forward$1,875 $5,760

*Assuming bonus depreciation

• The new law consolidated qualified leasehold

improvements, qualified restaurant property and

qualified retail improvement property into one

category — qualified improvement property (QIP).

However, Congressional oversight failed to identify

the MACRS class life for QIP after December 31, 2017,

therefore defaulting it to 39-year MACRS class life and

no longer allowing it to qualify for bonus depreciation.

A variety of efforts are taking place to encourage a

technical corrections bill from Congress that ideally

would be retroactive until January 1, 2018, identify a 15

year MACRS class life for QIP, and thereby allow QIP to

be eligible for bonus depreciation.

Furthermore, for property placed in service between Sept.

27, 2017, and Dec. 31. 2017, every business will have to use

the prior definitions of qualified leasehold improvements,

qualified restaurant property, qualified retail improvement

property, and qualified improvement property to determine

what methods of depreciation apply.

The cost recovery rules have become even more complex

and clients should continue their conversations with their

advisors about their asset acquisition behavior and how

this will impact their tax planning. In addition, this may

affect a client’s decision to perform an asset versus a stock

acquisition, as bonus depreciation is now allowed on used

assets.

Technical Termination of a Partnership

The new law repeals the technical termination rule for

partnership tax years beginning after Dec. 31, 2017. Thus, a

partnership is treated as continuing upon a sale or exchange

of 50% or more of the total interest in a partnership’s capital

and profits within a 12-month period, and new elections are

not required or permitted.

International Provisions

Modified Territorial System of Taxation

Prior to tax reform, the earnings of foreign subsidiaries

were subject to U.S. tax when repatriated to their U.S.

shareholders, and the U.S. shareholders had the ability to

claim foreign tax credits to mitigate the burden of double

taxation on the foreign subsidiary’s earnings. The new

law adopts a “modified” territorial system of taxation of

the earnings of foreign corporate subsidiaries. Domestic C

corporations that are U.S. shareholders of certain foreign

corporations are able to claim a 100% deduction for the

foreign-sourced portion of dividends paid by such foreign

corporations after December 31, 2017. Non-corporate

owners that are U.S. shareholders of foreign corporations,

whether directly or through pass-through entities such as

partnerships and S Corporations, are ineligible to claim

this deduction, and therefore will continue to be taxed on

dividends paid by such foreign corporations.

It is important to note that the Subpart F anti-deferral

regime, which subjects certain types of income to taxation as

a deemed dividend, continues to apply with modifications.

Any deemed dividend arising from Subpart F income is not

eligible for the 100% deduction discussed above.

The Bonadio GroupTAX CUTS AND JOBS ACT

Sec. 902 of the code, which allowed U.S. corporate

shareholders to claim a deemed-paid foreign tax credit

on the earnings of foreign subsidiaries when distributed,

has been repealed, effective for tax years beginning after

December 31, 2017. Sec. 960, which allows domestic C

corporations (and individuals electing to be taxed under

Sec. 962) to claim a deemed-paid foreign tax credit for

Subpart F income when generated, has been retained with

modifications.

Transition Tax

To transition to the modified territorial system of taxation

discussed above, a mandatory one-time deemed repatriation

tax, or transition tax, applies to the previously untaxed

accumulated foreign earnings of certain foreign corporations

by treating the earnings as Subpart F income to their U.S.

shareholders in the foreign corporation’s last taxable year

which begins before January 1, 2018. The U.S. shareholders

are able to claim a participation exemption deduction

against these earnings, which result in and effective rate of

tax, before consideration of foreign tax credits, of between

8% and 15.5% of the previously untaxed accumulated foreign

earnings, depending upon the amount of such earnings that

are considered to be held in liquid assets. Foreign tax credits

may be claimed against this income at a reduced rate, based

on the participation exemption deduction claimed. Note

that the transition tax applies to all U.S. shareholders, even

those that are unable to take advantage of the dividend

received deduction discussed above. To ease the burden

on taxpayers, the law allows taxpayers to elect to pay their

net transition tax in eight installments, and it also allows

shareholders of S corporations that are U.S. shareholders

of foreign corporations to elect to defer payment of the net

transition tax indefinitely, until a triggering event (such as a

sale, liquidation, termination of S election) occurs.

GILTI

The new law creates a new category of income, Global

Intangible Low-Taxed Income (or GILTI). A U.S. shareholder

of a foreign corporation is required to include in income

its share of GILTI for taxable years of foreign corporations

beginning after December 31, 2017. GILTI is generally

treated as Subpart F income and is therefore treated as a

deemed dividend to the U.S. shareholder. GILTI is generally

defined as the earnings of a foreign corporation not already

subject to U.S. taxation, over the deemed intangible return

(defined as a 10% return on depreciable tangible assets

used in the foreign operations). A deemed-paid foreign

tax credit is available at a rate of 80%. Any unused foreign

tax credits attributable to GILTI expire unused and cannot

be carried forward. Additionally, C corporations that are

U.S. shareholders are able to claim a 50% deduction for

GILTI through 2025, after which the deduction is reduced

to 37.5%. Non-corporate owners that are U.S. shareholders

of foreign corporations, whether directly or through pass-

through entities such as partnerships and S Corporations,

are ineligible to claim this deduction, and therefore will be

taxed on 100% of GILTI.

State Impact

Federal tax reform does not just affect federal taxable

income, but also how taxes are calculated at the state level.

States largely use the federal Internal Revenue Code as

the basis of their states taxes, and then adjust accordingly.

The state implications of federal tax reform should also be

closely monitored. Please reach out to your advisor for

further discussions.

The Bonadio GroupTAX CUTS AND JOBS ACT

Albany | Batavia | Buffalo | East Aurora | Geneva | New York City | Rochester | Rutland | Syracuse | Utica

bonadio.com | facebook.com/TheBonadioGroup | twitter/bonadiogroup | linkedin.com/company/the-bonadio-group