Embed Size (px)

Citation preview

1|GST – Reform or Challenge

GST

REFORM OR CHALLENGE Whitepaper – Q1/2017-18

A HISTORICAL CHANGE

This paper will focus on the earlier tax structure prevailing in India and

how the structure of Dual GST is implemented and has affected in India

along with IGST.

How many different taxes are there post-GST?

GST has a very complex yet simple structure. Every state and

government should benefit but burden does not go on consumers.

Central GST (CGST) - Levied by the Central Government on supply of goods & services within all the states. State GST (SGST) - Levied by the State Government on supply of goods and services within state. Integrated GST (IGST) - Levied by the Central Government on inter-state supply of goods and services but revenue is to be shared with relevant source and destination State Governments. Union Territory GST (UTGST) - Levied by the Central Government

on supply of goods & services within a union territory.

Q. Which taxes will be subsumed by GST?

A. Broadly, GST has replaced:

a. VAT (State as well as Central)

b. Excise Duty

c. Service Tax

d. Octroi / Entry Tax / LBT

e. CVD & SAD

Q. Which taxes will continue, in GST regime?

A. You will still be paying:

a. Custom’s Duty b. Professional Tax

c. Stamp Duty d. Motor Vehicle Tax

e. Electricity Duty f. VAT (for Petrolium products only)

“Technology is the key for GST – EBEX is making clients GST enabled

with effectively ZERO business downtime”

GST - INTRODUCTION

GST is destination based

taxation system and is widely

acknowledged worldwide.

The Goods and Service

Tax (largely known as GST) was

first introduced in France in the

year 1954. There are around

160 countries in the world that

have GST in place.

India has implemented Dual

GST which is CGST and SGST.

Inter State Transactions are to

be governed by IGST which

would be equal to CGST and

SGST. For understanding the

basic concept of GST, we need

to know basics about

destination and origin based

taxation and what they exactly

mean.

2|GST – Reform or Challenge

GST RATE FINALIZATION

Share of CGST & SGST is to be in equal parts that becomes 50% for each

body, of the rates stipulated for those specific Goods or specific Services. For

instance, if the goods under transaction attract 18% GST, then CGST share

remains 9% and SGST too is 9%.

REGISTRATION & GSTIN

GST registration is mandatory in many cases and is advisable in all cases,

except for very small scale daily earners. GST registartion must be done in

following cases:

i) if Annual Turnover is Rs. 20 Lacs or above. (Rs. 10 Lacs in case of north

eastern States).

ii) Every business registered under an earlier law will have to take

registration under GST.

iii) If an already registered business has been transferred to someone, the

transferee shall take registration with effect from the date of transfer.

iv) Anyone who makes inter-state supply of goods and/or services.

v) Casual taxable personal business

vi) Those already paying tax under Reverse Charge

vii) Input Service Distributor

viii)E-Commerce Operator

ix) Non Resident Taxable Person

“More awareness about GST is required to be created – EBEX welcomes

and supports the amendment in Taxation for brighter India”

GST will change the way India does business. India is moving forward, matching steps with international standards!

MAKE IN INDIA In order to make India a manufacturing

hub, it is imperative that the foreign

investors/companies find it conducive to do

business here. One of the major

impediments to a smooth business,

especially in the manufacturing sector, is

the uncertain and unpredictable indirect

tax regime.

Nand Kishore,

Partner Taxation, HSA Advocates

September 11, 2015

Ref : Business Standard

3|GST – Reform or Challenge

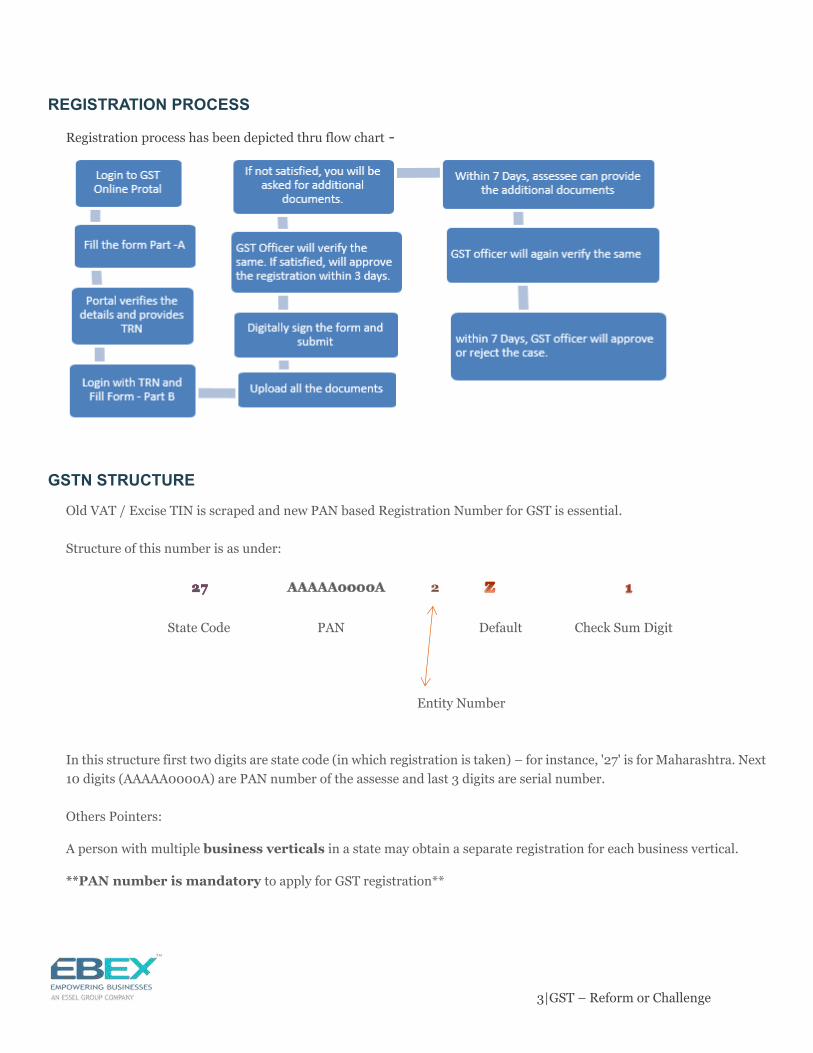

REGISTRATION PROCESS

Registration process has been depicted thru flow chart -

GSTN STRUCTURE

Old VAT / Excise TIN is scraped and new PAN based Registration Number for GST is essential.

Structure of this number is as under:

State Code PAN Default Check Sum Digit

Entity Number

In this structure first two digits are state code (in which registration is taken) – for instance, '27' is for Maharashtra. Next

10 digits (AAAAA0000A) are PAN number of the assesse and last 3 digits are serial number.

Others Pointers:

A person with multiple business verticals in a state may obtain a separate registration for each business vertical.

**PAN number is mandatory to apply for GST registration**

4|GST – Reform or Challenge

INCIDENCE OF GST

Incidence of GST is on following:

1. Supply of Goods / Services

2. Agreed to Supply Goods / Services for consideration (either in cash or kind)

3. 'Destination based' tax is to be charged

4. Branch Transfer / Stock Transfer from one state to another

In case of branch transfer/stock transfer, earlier, we were issuing the material under form F with Challan, in which no

tax is levied. But in GST regime, if the material is transferred from one branch to another in different states, Company

has to issue the invoice in its branch name applying IGST and paying tax to the Govt. However, another branch can take

the ITC (input tax credit) on that invoice. Hence, as such there is no revenue loss to the Company, till the ITC is available

for the material.

INTER & INTRA STATE SUPPLY

If source & destination are in same state, it is Intra-State Transaction, if Source & Destination are in different states, it is Interstate Transaction. In case of local invoice or within state invoice, CGST and SGST both need to be charged SEPARATELY and to be mentioned in the Return accordingly. In case of Inter State Supply, IGST will be applicable. Rate of IGST is equal to sum of rate under CGST and rate under SGST. Thus, rate under IGST is 18% (9 + 9). Tax Credit (or set-off, as was said in earlier days), shall be available for all these three taxes viz. CGST, SGST & IGST. Earlier, in spite of 'C' or 'H' or 'F' forms, CST @ 2% Tax was a cost to the assessee. Now, in GST Regime, IGST credit will be allowed, hence this 2% cost is avoided.

ANTI-PROFITING

Central Government may constitute an authority to examine if ITC availed under GST or reduction in price on account of any reduction in tax rate has actually resulted in a commensurate reduction in price of goods/ services supplied by a taxable person. In simple terms, Vendor has to pass on the benefit of ITC availed under GST regime to customer.

FREE ITEMS

There is a provision of charging GST on FREE Items, Buy 1 get 1 Free etc. Valuation of such free items will have to be made, at par with sale of these items. Thus if you are giving 1 item free for purchase of 10, you will have to invoice for 11 items, levy GST and then you may give credit for the basic value of 1 being free Item. Thus GST needs to be paid on all items, being delivered to the customer.

PROCUREMENT FROM UNREGISTERED VENDOR

If the Assessee has purchases from Unregistered Dealers, Assessee has to ACTUALLY pay GST on the same under Reverse Charges. Assessee can take set-off (credit) of the same in next month. Assessee has to issue a self-invoice which is to be signed by assessee only. To provide the benefit to small dealers, Govt. has come up with new relief, where if any registered dealer procures the material/services upto Rs. 5000/- per day from one or many unregistered vendors, NO RCM will be applicable.

5|GST – Reform or Challenge

COMPOSITE SCHEME

i. It is available for all assessee having Turnover <

Rs.75 lacs (Rs. 50 lacs for specified states).

ii. Under this scheme, 2.5% tax is applicable for

manufacturing companies and 1% tax is

applicable for all others.

iii. No Set-off or Tax Credit shall be available under

this scheme.

iv. This is optional.

v. Assessee has to apply for this and then GST

Official's permission is required to opt for this.

vi. If this scheme is availed, GST cannot be charged

in the invoices raised by the Assessee.

vii. If this is availed in one year and for next year

you intend to do away with this, you can apply

to GST officials and take permission for the

same i.e. either to Opt-in or Opt-out of the

scheme, you need permission from designated

authorities.

PRE-REQUISITE FOR CLAIMING ITC UNDER GST REGIME

Input Tax Credit (ITC) remains similar as in old regime, however compliance has increased: i) Assessee has to be in possession of Tax

Invoice, or Debit Note or Credit Note.

ii) Payment has to be made to the supplier

within 180 days. If the payment is not made

to the supplier within this period the ITC has

to be reversed by the Assessee. It can later

be availed, as and when actual payment is

made to the supplier.

iii) ITC for Reverse charges (GST paid on URD

purchase or other specific services), can be

availed in the month next to the month of

their actual payment.

Vendor has paid the tax and filed his return, as in GST regime, there is credit matching concept, in which credit is provided only after reconciling with vendor details uploaded in GSTN Server.

PLACE OF SUPPLY

Place of supply is very important to determine the tax applicable. The first point in the definition of GST requires determination of the place from where supply is made. Thus essentially the place which is most directly concerned with making supply needs to be identified for determining location of service provider. If such place is registered, then the same is the location of service provider. However, if such place is not registered but is a ‘Fixed establishment’, such fixed establishment would become the location of service provider. A fixed establishment is defined as a place which is characterized by a sufficient degree of permanence and suitable structure in terms of human and technical resources to supply services, or to receive and use services for its own needs. Thus the ambit of fixed establishment is sufficiently wide, subjective and open to interpretations. Any place with sufficient permanence from where the employees can make a taxable supply can become a location of service provider.

TIME OF SUPPLY FOR SERVICES

Time of Supply provisions- earliest of:

Date of invoice, if issued within 30 days from the date of supply of service

Date of provision of service, if invoice not issued within 30 days from date of supply of service

Date on which recipient shows the receipt of services in his books, in case above provisions do not apply

Receipt of payment (Bank account or books, whichever is earlier)

Time of supply for addition in value of supply by way of interest, late fee or penalty for delayed payment of consideration, shall be the date of receipt of such additional value by the supplier.

Under Reverse Charge Mechanism: -

Date of payment; or 60 days from date of invoice (whichever is earlier).

In case of associated enterprises (supplier of service located outside India) – date of entry in the books of accounts; or date of payment (whichever is earlier).

6|GST – Reform or Challenge

SET-OFF OF CREDIT

Under GST regime, credit of IGST, CGST, SGST & UTGST is available; however, credit utilization order is as under:

Credit against output tax

CGST SGST/UTGST IGST

CGST 1 Not Allowed 2 SGST/UTGST Not Allowed 1 2 IGST 2 3 1

1 – First 2- Second 3- Third

HSN CODING

HSN (Harmonized System of Nomenclature) is a standard coding used for identification of Goods or services and tax classification. HSN code number is widely used in many countries to classify goods for taxation purpose, claiming benefits etc. First 2 digit of HSN code is the Chapter ID for the goods & services. As per recent notification, requirement of HSN code in Invoice is as shown.

REVERSE CHARGE MECHANISM

There is a concept of reverse charge under following situations:

A. On import of goods/services ======================IGST is payable

B. GST payable on procurement through ============== Exemption upto 5000/- per day

Un-registered vendors

C. On some specified services ======================= List of services notified by

Government

7|GST – Reform or Challenge

RETURN FILING

RETURN filing due dates are as under:

A. (GSTN -1) - 10th of next month - Output GST (including Advance from Suppliers) i.e. Sale Return

B. (GSTN -2) - 15th of next month - Input GST i.e. Purchase Return. Reconciliation with vendor sales details have to

be done from 11th to 15th.

C. (GSTN -3) - 20th of next month –Final GST - Monthly return, along-with payment. Liability of payment shall be

calculated by the system itself, after filing of GSTR-1 & 2 as mentioned above.

D. (GSTN – 9) – 31st December of Next Financial Year - Annual Return, along-with Audit Report. Audit is compulsory

for Assessee having turnover of Rs.1 Crore and more.

Thus, during the year, total 37 Returns (12months X 3 each month = 36 plus 1 annual) are to be filed by Assessee,

for each of place of business. If the Assessee is carrying out business at more than one place, he has to obtain GST

registration at each of such place and has to file 37 returns for each of such place of business.

SOME KEY POINTS TO REMEMBER FOR THE COMPANY

a. In GST, Input Tax Credit (ITC) is available on almost all expenses incurred subject to

GST Law, accordingly, it is must to ensure that the invoice must contain all the details

which are necessary for claiming ITC.

b. Tax Invoice received from the vendor must be in the Name of Company with complete

address and not in the Name of Employee/ other person and further that the Tax

Invoice must mention Company GSTIN to enable the company to claim ITC.

c. Educate channel partners/vendors to ensure that they issue the Invoice in time and

deposit the requisite tax with the Government. They have to file the return in due course

so that company can claim the input tax credit. In this respect, it is advisable to review

the existing Contracts/POs with the vendors to include the indemnity clauses.

d. Educate employees for the changes and impact due to GST on business and accounting

system, so that there is no ambiguity at any level.

8|GST – Reform or Challenge

BENEFITS OF GST

a) Operations eased due to single Tax

In the earlier tax regime, retailors/consumers were

burdened with lots of taxes - Excise Duty, VAT, Service Tax,

Entertainment Tax, Customs Duty, Local Taxes etc. Many of

them did not understand these different types of taxes. In

GST regime, there is only one tax which they can easily

understand. So there is an operational ease to them.

Further, there will be less compliance as well.

b) Benefit due to anti-profiteering

In GST regime, the lowered tax rate from some sectors must

also benefit the respective consumers of sector. The GST

council has agreed on the fact that all benefits, either on

account of lower tax rate or credit eligibility should be

passed to customers.

c) Benefit to small vendors

In older regime, on imported goods, VAT liability was less as

compared to on domestic goods, due to which imported

goods were cheaper and gave more competition to local small

vendors. But in GST regime, IGST will be applicable on

imported goods which brings the imported goods in the same

level as domestic goods. Due to this, small vendors will be

benefited.

d) One Nation one tax

In older regime, value of one car was different in Delhi as

compared to Haryana due to difference in tax rate. But in

GST regime, this difference is removed. This will benefit to

the consumers as well as business entity. In entire nation

there is single tax and single price. Due to this, there will be

One Nation One Market. This will make the Indian

market more competitive than before and create a level

playing field between large & small enterprises

e) Improved Logistics

In GST regime, there will be one tax one nation and there is

no loss of credit of inter-state movement of goods. This will

result in consolidation of warehouses across the country.

Training Employees in GST

Regime

a) Explain the change

There are various changes in business models,

policies & accounting system due to GST impact.

We have to educate the people about the impact

and logic behind it so that they can understand the

same in better way.

b) Give Comparatives with old tax regime

We have to give comparative analysis with old tax

structure to make them understand the actual

impact on transaction level.

c) Practical Training

Practical training of employees with changes in

accounting software is necessary. They should be

educated about do’s & dont’s in case of P2P & O2C

processes. GST has impacted these processes

majorly.

d) Hand holding for first few cases

In initial stages, teething issues will come while

processing the cases. But, after some time, these

issues will be resolved. We have to handhold the

employees in few initial days.

e) Provide Study Material

In initial days, there will be various notifications,

and regular updates related to GST. The

employees should be kept well aware of it and

educated about the impact.

9|GST – Reform or Challenge

f) Benefit due to Non-Cascading effect

In earlier regime, due to non-creditable taxes i.e. CST there was cascading effect on value of goods & services. In GST,

this cascading effect has been removed.

In GST, to understand the impact we can take one example:

Say,

A consumer bought one pack of biscuit:

Earlier Regime GST

Cost Tax Cost Tax

Input Cost 100 100

Taxes Charged on Input (Creditable) 10 10

Taxes Charged on Input

(Non Creditable)

2 2 2

Processing Cost 50 50

Cost to Manufacturer 152 150

Margin 5 5

157 155

Output Tax to Retailor 15 15 15 15

Total Price Charged to Retailor 172 170

Tax Charged by Retailor 17 17 17 17

Tax Creditable (15) (15) (15) (15)

Net Price to Consumer 174 19 172 17

We can see, in GST regime the value of goods gets cheaper because the benefit of tax credit will be passed to

consumers.

10|GST – Reform or Challenge

g) Benefit to the E-commerce Operator

In earlier regime, different states under states VAT treated E-commerce operator separately. There was always

an ambiguity in it. But, GST clearly maps out the provisions applicable to the E-commerce sector since there is

one tax one nation, there should be no complication regarding inter-state movement of goods anymore.

h) Presence in Global Market

GST is applicable in most of the Countries. After implementation of GST in India, foreign investment will

increase as there will be less complexity of tax structure in India. Foreign companies were waiting for this move.

This will benefit to the economy as a whole.

i) Increase in Economic Growth

In GST, there will be boost in compliances which will increase the revenue of the government and reduce the

burden on fiscal deficit. These will benefit to the economic growth and GDP of the Country.

“After understanding the benefits of the GST, it seems that it is best

reform that came after 1991 reforms. However, whenever major

changes are implemented, always, there are some teething issues faced

in general”

11|GST – Reform or Challenge

CHALLENGES OF GST

a) Major changes in Business Model/Policy

In GST regime, the major challenge the industries are facing is to determine their place of supply according to GST

rules and make changes in their accounting system, business operation, policy decision etc. Example, companies are

thinking to go from centralized model system to de-centralized model. Existing accounting systems may be unable to

take this changes and additional IT professional or tax experts will be engaged to understand the impact on the

business and according to that changes will be made in systems, policies etc.

This will create the chaos in the industries. It will also increase operational cost of the company.

But these problems are short term in nature, once the systems are put in place, these will be resolved.

b) Increase in Compliance

All the small vendors are not very good in compliance work and record keeping. In GST, input credit can be availed

only if proper documentation has been kept and return has been filed through online system. There is always lack of

knowledge due to which they will face the losses.

However, they can be educated to understand the impact of GST on their business and these teething points can be

resolved.

c) Losses to Un-registered Vendors

In case of procurement from un-registered vendors, company has to pay the tax under reverse charge mechanism.

This will discourage the procurement from un-registered vendors and they will face the losses.

But, on the other hand, it will also encourage the small vendors to come-up in GST regime, which will in-turn help the

economy.

d) Online System - Lack of Knowledge & Training

In GST regime, all the process are online e.g. registration, return, input credit utilization etc. Due to lack of knowledge

and proper training, this will result in loss of credit to the businesses. However, government is trying to smoothen the

process, but it will take some time.

12|GST – Reform or Challenge

Conclusion

GST … Goods & Service Tax ... reality now… in India…

Some favor it … & some oppose it… all have their own perspective to see this big change

in the indirect taxation regime…

Industry has to decide whether GST will benefit or not... Whether, its

advantages will surpass the challenges…

EBEX Services

(Essel Business EXcellence Services Ltd)

Plot no 19 & 20, Film City

Sector 16A, NOIDA 201301

India; Ph:+91 120 499 6904