Embed Size (px)

Citation preview

Tata Motors Ltd. 06th July 2011

1 | P a g e

CMP: Rs.1017 Recommendation: Buy Target Price: Rs.1453

Q4 FY11 Result Update

Key Highlights

Standalone Business

� Total income grew by 19.4% YoY (26.7% QoQ) to Rs.14,601 Cr.,

driven by volume growth of 12.5% YoY (26.5% QoQ). EBITDA margin

declined by 32 bps YoY (116 bps QoQ) to 9.0% due to 112 bps

increase in purchase of traded goods YoY, 31 bps increase in

employment cost on YoY, and higher marketing expenditure.

� Net realization per vehicle increased by 6.8% YoY (0.4% QoQ)

Rs.668,825 due to price hikes.

� Price hike in Tata Indica and Tata Indigo family is in the range

of Rs.3,000 – Rs.15,000,

� While in the Utility Segment it was around Rs.8,700 –

Rs.14,500,

� In Commercial vehicle is in the range of Rs.1,500 – Rs.30,000.

� Exports in Q4 FY11 were higher 45% YoY to 15,384 units. Exports to

Bangladesh, Sri Lanka & Bhutan showed continued growth while

certain Middle East and North African (MENA) countries showed

subdued sales in Q4 FY11 due to political crisis.

Jaguar Land Rover (JLR)

� Total income grew by 33.9% YoY (2.9% QoQ) to £2,736 mn, driven by

volume growth of 15.9% YoY (4.7% QoQ). EBITDA margin declined by

158 bps QoQ (higher by 636 bps YoY) due to higher marketing spend

(£15 mn of pre launch promotional expenses for Land Rover Evoque)

and 30-40 bps was related to one time write offs.

� Average realization per vehicle for JLR was higher by 15.5% YoY

(-1.8% QoQ) £ 41,388. The QoQ decline in average realization was

due to lower contribution from China; QoQ share of China in Q4

FY11 was 12.4% from 13% in Q3 FY11.

Valuation & Outlook

Tata Motor standalone business is facing strong headwinds due to macro

(India) headwinds such as inflation, rising interest rates and rising fuel

prices. We have factored in 11.5% CAGR growth for the CV segment in

FY11-13E and 10.3% CAGR growth for the PV segment in FY11-13E.

We expect macro concerns to ease out by Q3 and Q4 FY12, and expect

standalone business of PV & CV to show recovery. The Company has

witnessed slowdown in sales of Indigo and Indica family in Q1 FY12,

midsized sedan space, and faces competition from other players.

On Subsidiary front, JLR operating performance has improved and has

surpassed standalone profitability, driven by improving product mix, cost

cutting initiatives and favourable forex movement. We believe JLR has

potential to sustain higher profitability and volumes due to growth in

China, Russia and launch of Land Rover Evoque.

Key Data

Financial Year End March

Market Cap (Rs. Cr.) 54,740

Free Float Factor 0.65

52 Week H/L 1381.4/748.6

Avg. 12M volumes ('000) 3,568

Face Value 10

Bloomberg TTMT IN

Reuters TAMO.BO

NSE TATAMOTORS

BSE 500570

Source: BSE, SIHL Research

Shareholding Pattern

Q4 FY11 Q3 FY11

Promoters 34.8% 34.9%

FII's 23.6% 24.2%

DII's 12.9% 13.9%

Others 28.6% 26.9%

Source: BSE, SIHL Research

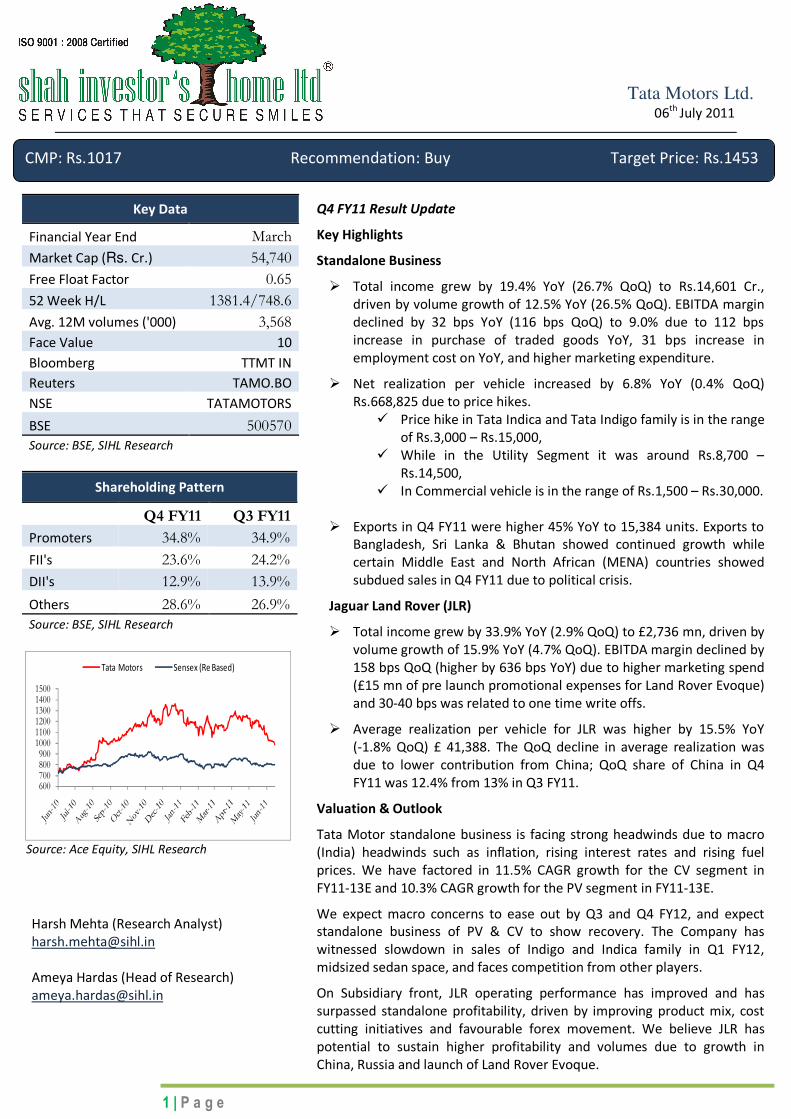

Source: Ace Equity, SIHL Research

600700800900100011001200130014001500

Tata Motors Sensex (Re Based)

Harsh Mehta (Research Analyst)

Ameya Hardas (Head of Research)

Tata Motors Ltd. 06th July 2011

2 | P a g e

Valuation & Outlook

We derive our SOTP (sum of the parts) valuation of Rs.1453/share by

valuing the standalone business at Rs.710/share, JLR business at

Rs.675/share and other subsidiary investments at Rs.67/share. We

recommend a BUY with a Target Price Rs.1453.

Exhibit 2: Volume Breakup (Quarterly)

Domestic Q4 FY11 Q4 FY10 YoY% Q3FY11 QoQ%

M&HCV 57,457 53,990 6.4% 45,771 25.5%

LCV 73,689 64,457 14.3% 65,563 12.4%

UTILITY 13,936 11,439 21.8% 9,260 50.5%

CARS 75,863 69,552 9.1% 50,264 50.9%

TOTAL 220,945 199,438 10.8% 170,858 29.3%

Exports Q4 FY11 Q4 FY10 YoY% Q3FY11 QoQ%

M&HCV 5,205 3,422 52.1% 5,112 1.8%

LCV 9,172 5,592 64.0% 9,054 1.3%

UTILITY 121 167 -27.5% 218 -44.5%

CARS 886 1,437 -38.3% 1,578 -43.9%

TOTAL 15,384 10,618 44.9% 15,962 -3.6%

TOTAL SALES 236,329 210,056 12.5% 186,820 26.5%

JLR Q4 FY11 Q4 FY10 YoY% Q3FY11 QoQ%

JAGUAR 10,041 10,908 -7.9% 13,172 -23.8%

LANDROVER 56,090 46,096 21.7% 49,983 12.2%

TOTAL 66,131 57,004 16.0% 63,155 4.7%

Source: Company Data, SIHL Research

Exhibit 1: Valuation Parameters

Valuation % of Holding either Directly

or through Subsidiaries Valuation Method

Value per

Share

Standalone Business - DCF Valuation 710

Jaguar Land Rover Plc 100 30% Discount to 3.5X EV/EBITDA ratio of FY13E EBITDA of £2,129 mn

675

Tata Motors Finance Ltd. 100 30% Discount to P/Bv ratio of FY13E BV of Rs.1,731 Cr. 23

Tata Daewoo Commercial Vehicle Co. Ltd 100 30% Discount to P/Bv ratio of FY13E BV of Rs.1,408 Cr.

18

Tata Technologies 81 30% Discount to P/Bv ratio of FY13E BV of Rs.904 Cr. 12

HV Axle Ltd. 85 30% Discount to P/Bv ratio of FY13E BV of Rs.623 Cr.

8

HV Transmissions Ltd. 85 30% Discount to P/Bv ratio of FY13E BV of Rs.517 Cr. 7

Target Price 1453

CMP 1017 Expected Return 42.9%

Tata Motors Ltd. 06th July 2011

3 | P a g e

Exhibit 3: Trend in Domestic Realization and EBITDA Margins

Source: Company Data, SIHL Research

Exhibit 4: Trend in JLR Realization and EBITDA Margins

Source: Company Data, SIHL Research

55

8,5

11

56

7,7

42

60

1,4

66

62

6,1

25

61

8,1

47

62

6,0

15

66

6,0

85

66

8,8

25

12.3%

13.2%

12.6%

9.3%10.5%

9.5%

10.1%

9.0%

0%

2%

4%

6%

8%

10%

12%

14%

500,000

520,000

540,000

560,000

580,000

600,000

620,000

640,000

660,000

680,000

Domestic Realization(in Rs.) (LHS) Domestic EBITDA Margins (RHS)

31

,33

7 32

,16

6

34

,58

6

35

,85

7

39

,57

9

40

,75

9

42

,11

9

41

,37

2

-3.0%

2.9%

9.8% 9.5%15.5% 16.6%

17.4% 15.8%

-5%

0%

5%

10%

15%

20%

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

JLR Realization(in £) (LHS) JLR EBITDA Margins (RHS)

Tata Motors Ltd. 06th July 2011

4 | P a g e

Exhibit 5: Market Share of CV

Source: Siam, SIHL Research

Exhibit 6: Market Share of Cars

Source: Siam, SIHL Research

Standalone Business

Passenger Vehicles

Tata Motors Ltd. ended FY11 on strong note with Passenger Vehicle segment

(domestic + exports) growing at 27% YoY. The market share for Passenger Car

segment is around 13.4% in Q4 FY11 which saw a shrinkage of 190 bps YoY. The

volumes of Nano improved from 509 units in November 2010 to around 10,000 units

in April 2011, and slowed down a bit to x in June 2011. Tata Motors is aggressively

looking at expansion of dealer networks in rural segment which is now the focus

market for Nano.

On Utility Vehicle front, the company registered volume of 43,063 units (domestic +

exports) which is up ~26% YoY. The launch of new Aria and Winger variants has not

provided much cheer in terms of volumes. Price hike in Tata Indica and Tata Indigo

family is in the range of Rs.3,000 – Rs.15,000, while in the Utility Segment it was

around Rs.8,700 – Rs.14,500.

74.4

%

72.5%

70.8

%

66.2

%

64.9

%

65.9% 69.4

%

64.9%

11

.7%

12

.3%

12

.9%

15

.3%

14

.5%

13

.8%

10

.2%

13

.4%

Tata Motors Ltd. 06th July 2011

5 | P a g e

Commercial Vehicles (CV)

On CV front (domestic + exports), Tata Motors registered a growth of 14% YoY in Q4

FY11. The growth in CV segment was led by both LCVs (18.3% YoY growth in Q4 FY11)

and M&HCV (9.1% YoY growth in Q4 FY11) even after competition rises in both

segment against the ACE and higher M&HCV segment. Tata Motors recently launched

the four-wheeler Magic Iris, which is also expected to provide end-to-end last mile

solutions for the fast growing rural customer. We estimate LCV volumes to remain

strong driven by strong demand for low tonnage goods. We forecast a 15% CAGR

growth in LCV volumes between FY11 and FY13E.

We expect standalone earnings to increase at 15% CAGR between FY11 and FY13E but

will face some challenges due to the following reasons:

� We estimate domestic Passenger Car volumes for Tata Motors to increase by 10%

in FY12 and FY13 (v/s 27.2% in FY11). We expect Tata Motors to face increasingly

tough competition from global auto giants of the likes of Hyundai, Volkswagen,

and GM which may result in Tata Motors losing market share to the extent of 60-

70 bps YoY.

� We believe Tata Motors Utility Vehicles to grow at a rate of 12% as against

Industry growth rate of 14% in FY12. Existing and new product launches by

market leader M&M, Toyota and Maruti’s launch of new utility vehicle R3 in Q4

FY12 (stretched version of SX4 platform) are expected to penetrate into market of

Tata Motors Utility Vehicles.

� We estimate 9.5% CAGR growth from FY11 to FY13 in M&HCV as Industrial

production is slowing down. Growth in the freight generating sectors like

steel, cement, coal and automobiles has slowed down over the last few months

and is expected to remain weak in FY12E. Tata Motors being the market leader in

M&HCVs (with X% market share), will be face the impact most.

Jaguar Land Rover (JLR) Business: A Saving Grace for Tata Motors

FY11 has been a turnaround year for JLR with volume growth of around 25% YoY to

243,621 units. The company has shown strong growth in the markets of China, Russia

and RoW which has improved volume share to 11.0%, 4.8% and 16.2% from 9.7%, 4.2%

and 15.3% YoY, respectively, for FY11. China continues to remain one of the most

profitable geographies and its increase along with richer Land Rover mix has helped

the average selling price (ASPs) for JLR to improve 15.5% YoY. However TATA MOTORS

witnessed a drop in QoQ share of China from ~13.0% in Q3 FY11 to 12.4% in Q4 FY11.

This contributed to the decline in average net realization QoQ by 1.8%.

Jaguar volumes were down 8% YoY and 24% QoQ in Q4 FY11. This was due to slowing

sales in the UK and European region. The decline in Jaguar overall volumes was partly

attributable to the termination of X-type series and supply constraints for the recently

launched XJ series, due to shortage of engine supplies from Ford.

Engines for Jaguar Land Rover are currently supplied by Ford from its UK plants. Ford is

already supplying more engines than the contracted number, but due to spurt in

demand of JLR vehicles Ford is falling short to matchup the pace of JLR growth

numbers.

Land Rover volumes have been growing strongly at 22% YoY and 12.2% QoQ in Q4

FY11. Demand remained strong even as Discover and Range Rover face similar engine

issues while Freelander and RR Sport continued to witness ~18% growth YoY.

Tata Motors Ltd. 06th July 2011

6 | P a g e

Jaguar Q4 FY11 Volume Share by Geography

Source: Company Data, SIHL Research

20%

33%22%

2%

4%

19%

North America UK

Europe (Exl. Russia) Russia

China Other

Land Rover Q4 FY11 Volume Share by Geography

Source: Company Data, SIHL Research

17%

26%

21%

5%

14%

17%

North America UKEurope (Exl. Russia) Russia

China Other

Management Guidance and Road map for JLR business

� JLR would be launching Land Rover Evoque in Sept 2011. It has received very

good response as it is priced in the lower end of the price band in terms of

other products of the portfolio (around £26,000).

� The capacity at Halewood plant has increased from 100,000 units to 150,000

units taking JLR’s overall capacity to 350,000 units per annum.

� Tata Motors has guided sales of 300,000 units for JLR in FY12, but we have

assumed a conservative growth rate of 17.7%, and that comes to around

286,764 units; we believe slowing growth rate in the Euro Zone may impact JLR’s

market to some extent and may result in a capacity utilization of 82%.

� Management expects to increase its China’s sales to 40,000 units (from 26,000

units) aided by strong demand from luxury vehicles in China and it is further

working on premium entry level segment for Jaguar, to compete with

BMW 3 Series and Mercedes C Class.

� JLR has recently completed a fund raising for £1 bn, of which £250 mn have

been used for repayment of preference capital to Tata Motors, redeemed at par

value and approximately £360m have been earmarked for refinancing existing

debt.

� JLR has carryover tax credits of £2–2.5 bn and hence tax rate is likely to continue

at lower levels going forward.

We believe weakness in the European market will be partially offset by reasonably

buoyant growth in China, Russia, US and other emerging markets. We estimate JLR

volumes to grow by 17.7% YoY in FY12E (Jaguar 15.1% and Land Rover 18.4%) and

12.7% YoY in FY13E (Jaguar 12.4% and Land Rover 12.7%).

We expect the UK market to show a declining growth rate (around 2%) for Luxury

cars in FY12 due to sluggish demands and a miniscule growth rate of 1% in FY13.

Growth in European market (excl. Russia) will remain flattish at around 7.1% and

3.6% in FY12 and FY13 respectively. We believe Russian market to grow at around

40% and 20% in FY12 and FY13 respectively.

Tata Motors Ltd. 06th July 2011

7 | P a g e

New plant in Pune (Chikli) to mark JLR’s India presence

JLR has officially opened its first assembly plant near Pune in Maharashtra. The facility

will assemble Land Rover Freelander 2 supplied in Complete Knock Down (CKD) form

JLR Halewood’s plant. The assembly plant at Pune is not a newly build one but was

earlier used by Mercedes.

JLR is also likely to set up a four – cylinder engine plant in India and will invest around

$700 mn. The cylinder engine plant is likely to have a capacity of 2,00,000 units and

will start by 2015. This will help JLR to reduce its reliance on Ford for supply of such

engines.

We believe EBITDA margins of JLR will decline by 40 bps in FY12E as,

� Incentives to US dealers have risen sharply for the Jaguar brand which in our view

is supporting growth for luxury car volumes in US.

� We believe Evoque EBITDA margins would be lower than existing margins

considering lower selling price (around £26,000), higher fixed costs initially on

lower volumes

� Sharp decline in UK volumes which is a second highest profitable market for JLR.

UK retail volumes of JLR declined by 38% YoY and 16% YoY in April and May 2011,

respectively which is a matter of concern and could weigh on JLR profitability. We

believe the outlook for the UK market remains weak.

Volume Breakup Standalone (Q1 FY12)

Domestic Q1 FY12 Q1 FY11 % YoY growth Q4 FY11 % QoQ growth

M&HCV 45,541 42,156 8.0% 57,456 -20.7%

LCV 67,829 55,073 23.2% 73,690 -8.0%

CARS 54,345 62,589 -13.2% 75,863 -28.4%

Tata Nano 21,978 14,779 48.7% 23,672 -7.2%

Indica Range 17,935 26,507 -32.3% 27,572 -35.0%

Indigo Range 14,432 21,303 -32.3% 24,619 -41.4%

UTILITY 10,436 9,650 8.1% 13,936 -25.1%

Total Domestic 178,151 169,468 5.1% 220,945 -19.4%

Exports Q1 FY12 Q1 FY11 % YoY growth Q4 FY11 % QoQ growth

Total Exports 14,886 12,243 21.6% 15,384 -3.2%

Total Sales 193,037 181,711 6.2% 236,329 -18.3%

Source: Company Data, SIHL Research

Volume for Q1 FY12 was 178,151 units saw a growth of 5.1% YoY (-19.4% QoQ). Our

estimate for FY12 volumes is 893,056 units. Q1 FY12 volumes comprises of 20% of

FY12E volumes. We believe our estimates are in line with company performance.

Tata Motors Ltd. 06th July 2011

8 | P a g e

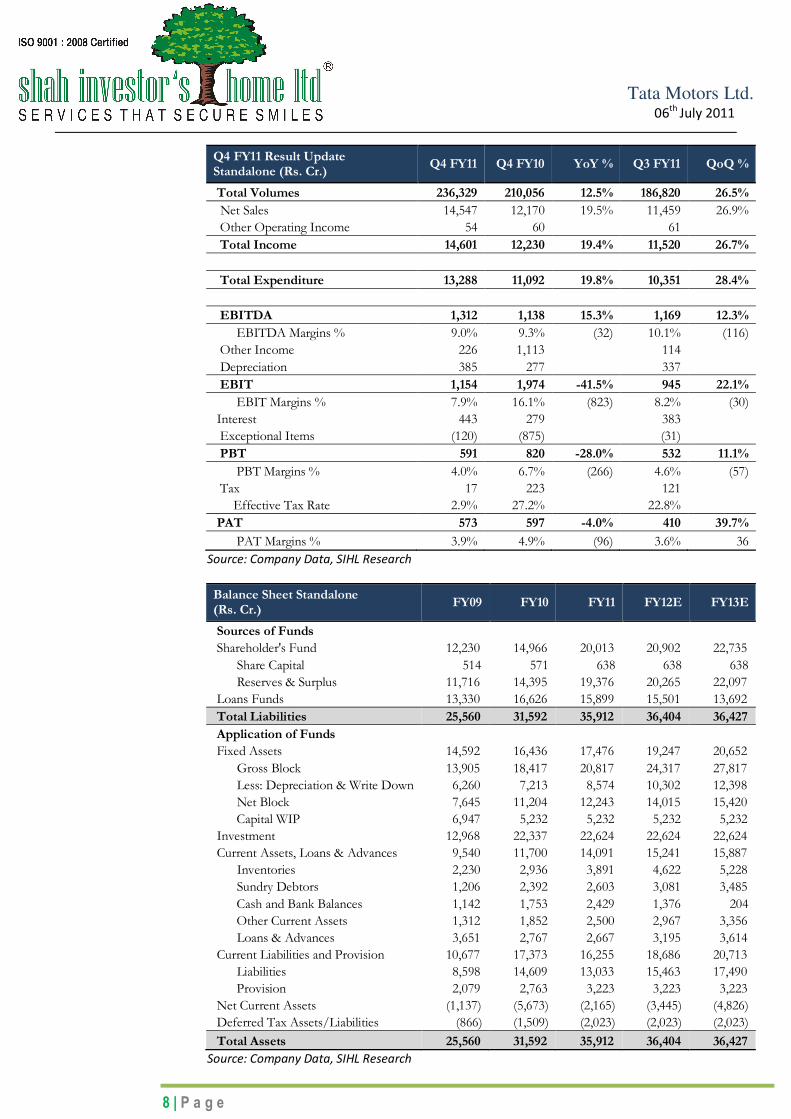

Q4 FY11 Result Update Standalone (Rs. Cr.)

Q4 FY11 Q4 FY10 YoY % Q3 FY11 QoQ %

Total Volumes 236,329 210,056 12.5% 186,820 26.5%

Net Sales 14,547 12,170 19.5% 11,459 26.9%

Other Operating Income 54 60 61

Total Income 14,601 12,230 19.4% 11,520 26.7%

Total Expenditure 13,288 11,092 19.8% 10,351 28.4%

EBITDA 1,312 1,138 15.3% 1,169 12.3%

EBITDA Margins % 9.0% 9.3% (32) 10.1% (116)

Other Income 226 1,113 114

Depreciation 385 277 337

EBIT 1,154 1,974 -41.5% 945 22.1%

EBIT Margins % 7.9% 16.1% (823) 8.2% (30)

Interest 443 279 383

Exceptional Items (120) (875) (31)

PBT 591 820 -28.0% 532 11.1%

PBT Margins % 4.0% 6.7% (266) 4.6% (57)

Tax 17 223 121

Effective Tax Rate 2.9% 27.2% 22.8%

PAT 573 597 -4.0% 410 39.7%

PAT Margins % 3.9% 4.9% (96) 3.6% 36

Source: Company Data, SIHL Research

Balance Sheet Standalone (Rs. Cr.)

FY09 FY10 FY11 FY12E FY13E

Sources of Funds

Shareholder's Fund 12,230 14,966 20,013 20,902 22,735

Share Capital 514 571 638 638 638

Reserves & Surplus 11,716 14,395 19,376 20,265 22,097

Loans Funds 13,330 16,626 15,899 15,501 13,692

Total Liabilities 25,560 31,592 35,912 36,404 36,427

Application of Funds

Fixed Assets 14,592 16,436 17,476 19,247 20,652

Gross Block 13,905 18,417 20,817 24,317 27,817

Less: Depreciation & Write Down 6,260 7,213 8,574 10,302 12,398

Net Block 7,645 11,204 12,243 14,015 15,420

Capital WIP 6,947 5,232 5,232 5,232 5,232

Investment 12,968 22,337 22,624 22,624 22,624

Current Assets, Loans & Advances 9,540 11,700 14,091 15,241 15,887

Inventories 2,230 2,936 3,891 4,622 5,228

Sundry Debtors 1,206 2,392 2,603 3,081 3,485

Cash and Bank Balances 1,142 1,753 2,429 1,376 204

Other Current Assets 1,312 1,852 2,500 2,967 3,356

Loans & Advances 3,651 2,767 2,667 3,195 3,614

Current Liabilities and Provision 10,677 17,373 16,255 18,686 20,713

Liabilities 8,598 14,609 13,033 15,463 17,490

Provision 2,079 2,763 3,223 3,223 3,223

Net Current Assets (1,137) (5,673) (2,165) (3,445) (4,826)

Deferred Tax Assets/Liabilities (866) (1,509) (2,023) (2,023) (2,023)

Total Assets 25,560 31,592 35,912 36,404 36,427

Source: Company Data, SIHL Research

Tata Motors Ltd. 06th July 2011

9 | P a g e

Income Statement Standalone (Rs Cr)

FY09 FY10 FY11 FY12E FY13E

Gross Sales 28,262 38,145 51,903 61,522 69,616

Less: Excise Duty 2,938 2,771 4,096 4,663 5,277

Net Sales 25,323 35,374 47,807 56,858 64,339

Other Operating Income 307 219 233 200 200

Total Income 25,630 35,593 48,040 57,058 64,539

Expenditure

(Inc)/Dec in Stock in Trade 177 (578) (354) (334) (363)

Consumption of Raw Material 16,188 20,393 27,058 32,283 35,259

Manufacturing Expenses 4,794 7,069 7,832 9,229 10,546

Employee Cost 1,539 1,823 2,294 2,601 3,030

Purchase of Traded Goods 2,180 4,513 7,363 8,759 10,203

Expense Capitalized 885 741 818 818 818

Total Expenditure 23,994 32,479 43,375 51,722 57,858

EBITDA (Ex OI) 1,636 3,114 4,666 5,337 6,681

EBITDA Margins % 6.4% 8.7% 9.7% 9.4% 10.4%

Other Income 1,063 1,996 571 500 500

Depreciation 875 1,034 1,361 1,728 2,096

EBIT 1,825 4,076 3,876 4,108 5,085

EBIT Margins % 7.1% 11.5% 8.1% 7.2% 7.9%

Interest 811 1,246 1,532 1,488 1,314

PBT 1,014 2,830 2,197 2,620 3,771

PBT Margins % 4.0% 7.9% 4.6% 4.6% 5.8%

Tax 13 589 385 472 679

Effective Tax Rate 1.2% 20.8% 17.5% 18.0% 18.0%

PAT 1,001 2,240 1,813 2,149 3,092

PAT Margins % 3.9% 6.3% 3.8% 3.8% 4.8%

EPS 22.26 44.24 33.67 39.92 57.45

Source: Company Data, SIHL Research

Cash Flow Standalone (Rs. Cr.)

FY09 FY10 FY11 FY12E FY13E

Cash Flow from Operations 1,295 6,586 (118) 4,104 5,397

PAT 1,001 2,240 1,813 2,149 3,092

Depreciation 875 1,034 1,361 1,728 2,096

Non Cash Adjustment (100) (1,151) - - -

Change in WC (481) 4,463 (3,292) 227 209

Cash Flow from Investing (10,585) (11,848) (2,400) (3,500) (3,500)

Capital Expenditure (4,029) (2,330) (2,400) (3,500) (3,500)

Other Investment Items (6,556) (9,518) - - -

Cash Flow from Financing 8,105 5,348 373 (1,657) (3,069)

Issue of Equity 4,110 - 2,359 - -

Issue/Repay of Debt 7,049 3,296 (727) (397) (1,809)

Dividend Paid (533) (286) (1,077) (1,077) (1,077)

Dividend Tax (109) (59) (183) (183) (183)

Other Financing Cash Flow (2,412) 2,397

Net Cash (1,185) 86 (2,146) (1,053) (1,172)

Opening Balance 1,865 669 716 2,429 1,376

Closing Balance 669 716 2,429 1,376 204

Source: Company Data, SIHL Research

Tata Motors Ltd. 06th July 2011

10 | P a g e

JLR Income Statement (in £ mn)

FY09 FY10 FY11 FY12E FY13E

Gross Income 4,974 6,555 9,905 12,224 14,186

Less: Excise Duty - - - - -

Dividend & Other Income - - 2 - -

Total Income 4,974 6,555 9,907 12,224 14,186

Expenditure

Manufacturing & Other Expenses 5,461 6,624 8,937 11,046 12,819

Expenses Capitalized (446) (462) (651) (773) (833)

Total Expenditure 5,015 6,162 8,287 10,273 11,985

EBITDA (41) 393 1,621 1,952 2,201

EBITDA Margins -0.8% 6.0% 16.4% 16.0% 15.5%

Product Development Expenditure 39 48 119 147 171

Depreciation 170 310 380 544 708

Interest & Discounting Charges 59 49 22 22 22

Amortization 3 11 - - -

Profit before Exceptional Items & Tax (312) (25) 1,099 1,239 1,301

Borrowings, Deposits & Loans Given - (39) (27) (27) (27)

PBT (312) 15 1,126 1,212 1,274

PBT Margins -6.3% 0.2% 11.4% 9.9% 9.0%

Tax Expenses 25 29 83 90 94

PAT (337) (14) 1,043 1,122 1,179

PAT Margins -6.8% -0.2% 10.5% 9.2% 8.3%

Source: Company Data, SIHL Research

JLR Balance Sheet (in £ mn)

FY09 FY10 FY11 FY12E FY13E

Shareholder's Fund (80) 1,379 1,680.3 2,802 3,982

Share Capital 924 2,320 1,658 1,658 1,658

Reserves & Surplus (1,004) (941) 23 1,145 2,324

Loans Funds 1,953 1,283 1,261 1,453 1,576

Secured Loans 416 1,270 824 950 1,031

Unsecured Loans 1,537 13 437 503 546

Total Liabilities 1,873 2,662 2,941 4,255 5,558

Fixed Assets 2,138 2,554 3,031 3,492 3,789

Gross Block 5,347 5,981 6,104 7,109 8,114

Less: Depreciation & Write Down 3,583 3,801 4,104 4,648 5,355

Net Block 1,764 2,180 2,000 2,461 2,759

Capital WIP 373 374 1,030 1,030 1,030

Investment 0 0 105 105 105

Goodwill (On Consolidation) 376 376 376 376 376

Current Assets, Loans & Advances 1,753 2,709 3,110 4,643 6,225

Inventories 917 995 1,152 1,418 1,646

Sundry Debtors 461 667 562 693 804

Cash and Bank Balances 128 680 923 1,948 3,098

Loans & Advances 247 367 473 583 677

Current Liabilities and Provision 2,453 2,988 3,735 4,416 4,992

Liabilities 1,690 2,349 2,910 3,591 4,167

Provision 763 639 825 825 825

Net Current Assets (700) (278) (625) 228 1,233

Deferred Tax Assets/Liabilities 16 27 55 55 55

Total Assets 1,873 2,662 2,941 4,255 5,558

Source: Company Data, SIHL Research

Tata Motors Ltd. 06th July 2011

11 | P a g e

TML Standalone Key Ratios

Particulars FY10 FY11 FY12E FY13E

BV 295.5 371.8 388.3 422.4

EPS 44.2 33.7 39.9 57.4 P/BV 3.4 2.7 2.6 2.4

P/E 22.6 29.6 25.0 17.4

ROE 15.0% 9.1% 10.3% 13.6% ROCE 12.9% 10.8% 11.3% 14.0%

EBITDA Margins 11.5% 8.1% 7.2% 7.9%

EV/EBITDA 17.1 17.3 12.7 10.1 Source: Company Data, SIHL Research

Peer Group Analysis (FY11)

Companies Financial Year End

Revenue (Rs. Cr.)

EBITDA Margin

PAT Margin

EV/ EBITDA

Debt/ Equity

ROE ROCE

Tata Motors Mar 123,133 13.7% 7.5% 5.3 1.7 48.1% 25.2% Mahindra & Mahindra Mar 36,842 16.5% 8.7% 9.5 1.2 22.4% 17.2% Maruti Suzuki Mar 37,578 9.9% 6.1% 9.3 0.0 16.1% 21.4%

Ashok Leyland Mar 11,118 11.0% 5.7% 8.2 0.6 15.9% 14.8% Source: Company Data, SIHL Research

Global Companies Peer Group Analysis (FY11)

Financial Year End

Current MCap

(USD mn)

Revenue (USD mn)

EBITDA (USD mn)

PAT (USD mn)

Products Debt/ Equity

ROE ROCE

BMW Dec 63,171 87,518 20,912 4,657 9 269.9 14.9 13.5

Toyota Mar 144,181 234,087 20,262 5,031 20 113.8 3.9 5.9

Ford# Dec 53,250 128,954 15,383 6,561 12 NA NA 222.3

Audi Dec 36,228 51,280 7,809 3,742 11 7.3 24.2 20.4

Volkswagen Dec 91,466 182,779 24,002 9,847 14 158.1 16.3 17.8

JLR* Dec - 15,958 2,611 1,680 9 0.75 62.0 42.2

Source: Bloomberg, SIHL Research

Notes:

� Global peer group analysis is made on US Dollar basis.

� *JLR is a not a listed company.

� #Equity of Ford has been in negative USD 15.7 bn since FY08, but it has been improving over the period of years. As of 31st

Dec 2010, total equity for Ford is negative USD 673 mn.

Tata Motors Ltd. 06th July 2011

12 | P a g e

Contact Details Shah Investor’s Home Ltd

164C, Mittal Tower,

C Wing, Nariman Point

Mumbai 400021

www.sihl.in

Contact: [email protected], +91-2204 0782/83

You can also access our reports on Bloomberg (ERH SIH<GO>)

Disclaimer:-

The Information provided by SMS or in newsletter or in any document has been prepared by Shah Investor’s Home Ltd

(SIHL). The Information provided by SMS or in newsletter does not constitute an offer or solicitation for the purchase or sale of any

financial instrument or as an official confirmation of any transaction. The information contained herein is from publicly available data

or other sources believed to be reliable, but we do not represent that it is accurate or complete and it should not be relied on as such.

SIHL or any of its affiliates/ group companies shall not be in any way responsible for any loss or damage that may arise to any person

from any inadvertent error in the information contained in this report or SMS. This Information provided by SMS, reports or in

newsletter is provided for assistance only and is not intended to be and must not alone be taken as the basis for an investment

decision. The user assumes the entire risk of any use made of this information. Each recipient of this Information provided by SMS,

report or in newsletter should make such investigation as it deems necessary to arrive at an independent evaluation of an investment

in the securities of companies referred to in this information provided by SMS, report or in newsletter (including the merits and risks

involved), and should consult his own advisors to determine the merits and risks of such investment. The investment discussed or

views expressed may not be suitable for all investors. This information is strictly confidential and is being furnished to you solely for

your information.

The information should not be reproduced or redistributed or passed on directly or indirectly in any form to any other

person or published, copied, in whole or in part, for any purpose. The information provided by report or SMS is not directed or

intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or

other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject

SIHL and affiliates/ group companies to any registration or licensing requirements within such jurisdiction. The distribution of this

Information provided by SMS or in newsletter in certain jurisdictions may be restricted by law, and persons in whose possession this

Information provided by SMS or in newsletter comes, should inform themselves about and observe, any such restrictions. The

information given or Information provided by SMS, report or in newsletter is as of the date of the issue date of report or the date on

which SMS provided and there can be no assurance that future results or events will be consistent with this information. This

information is subject to change without any prior notice. SIHL reserves the right to make modifications and alterations to this

statement as may be required from time to time. However, SIHL is under no obligation to update or keep the information current.

Nevertheless, SIHL is committed to providing independent and transparent recommendation to its client and would be

happy to provide any information in response to specific client queries. Neither SIHL nor any of its affiliates, group companies,

directors, employees, agents or representatives shall be liable for any damages whether direct, indirect, special or consequential

including lost revenue or lost profits that may arise from or in connection with the use of the information. Past performance is not

necessarily a guide to future performance. The disclosures of interest statements incorporated in the Information provided by SMS,

report or in newsletter are provided solely to enhance the transparency and should not be treated as endorsement of the views

expressed in the report. The analyst for this report certifies that all of the views expressed in this report accurately reflect his or her

personal views about the subject company or companies and its or their securities, and no part of his or her compensation was, is or

will be, directly or indirectly related to specific recommendations or views expressed in this report.